Composite Material Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 70.94 Billion |

| Market Size (2031) | USD 89.93 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

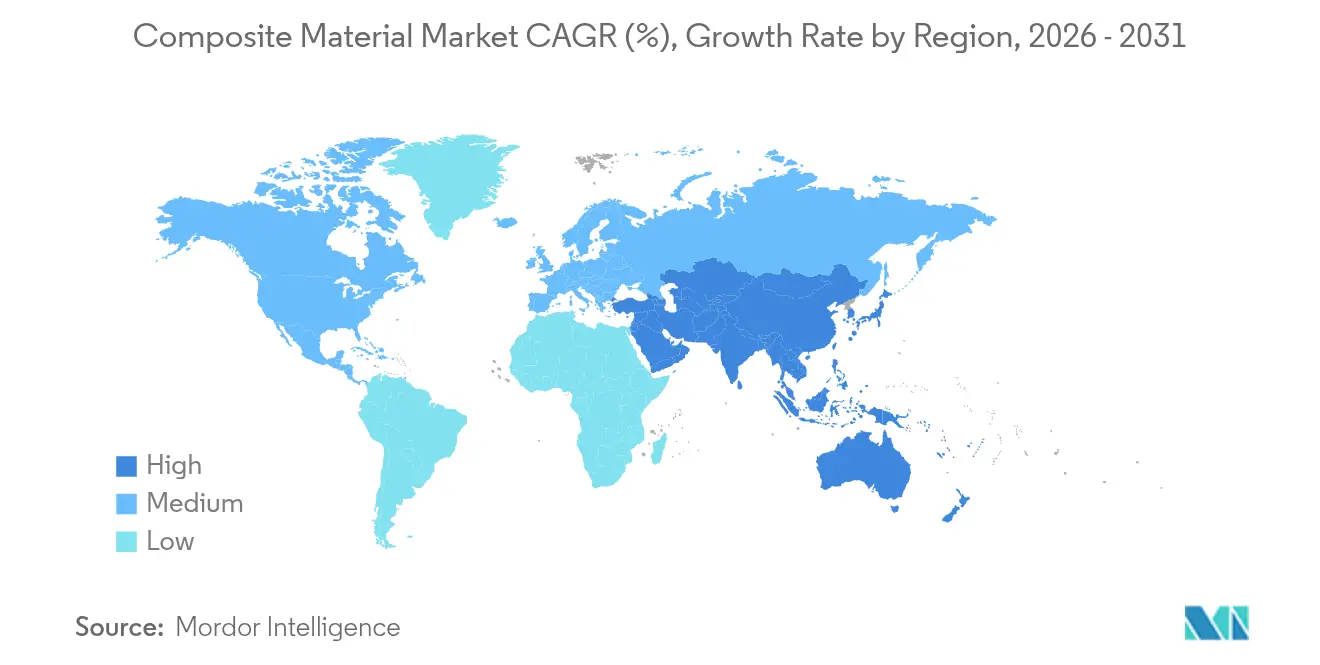

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

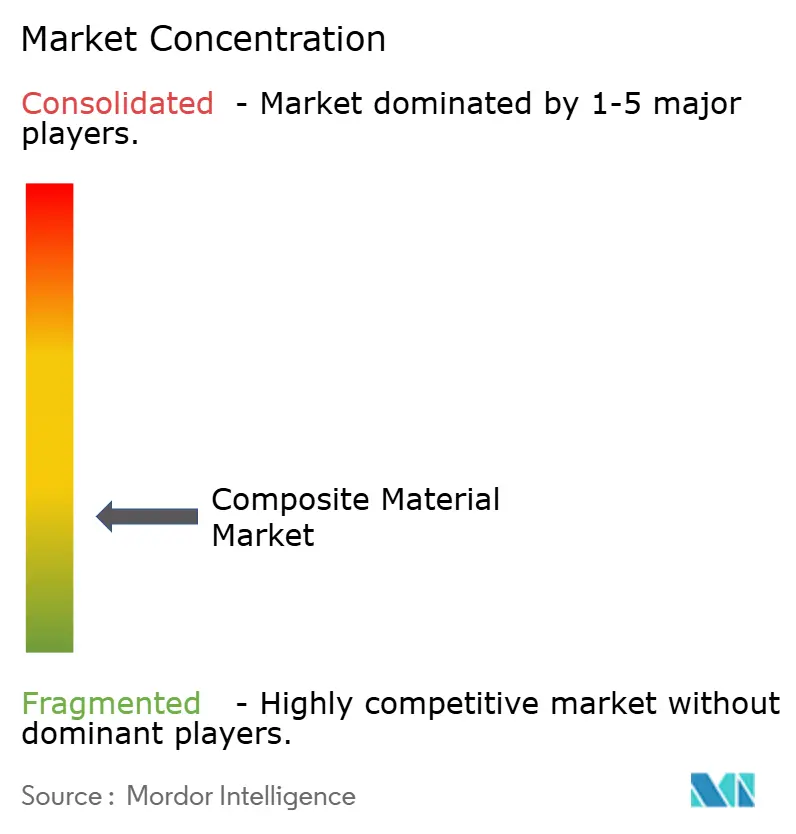

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composite Material Market Analysis by Mordor Intelligence

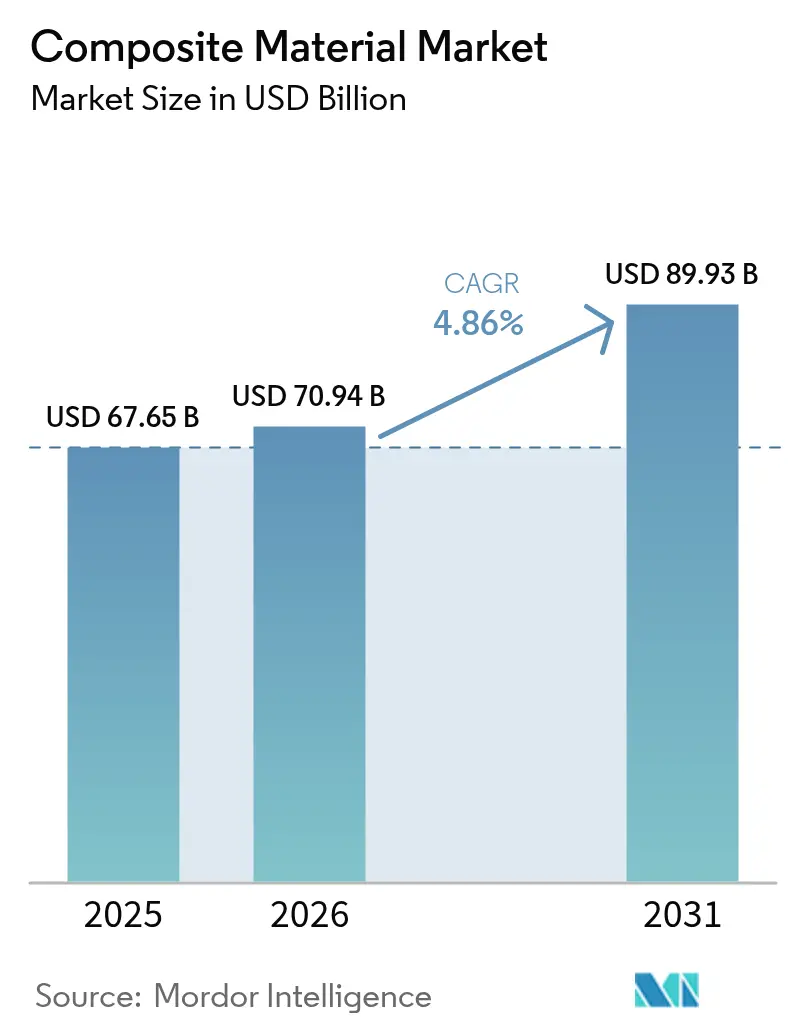

The Composite Material market size is expected to grow from USD 67.65 billion in 2025 to USD 70.94 billion in 2026 and is forecast to reach USD 89.93 billion by 2031 at 4.86% CAGR over 2026-2031. Robust demand for lightweight, high-performance materials in transportation, energy, infrastructure and electronics is widening the application portfolio, while continuous process automation is lowering cycle times and defects. Asia-Pacific, holding 45.12% of global revenue in 2024, remains the epicenter of volume growth as wind-turbine expansion, electrification programs and large-scale infrastructure projects accelerate regional consumption. Rapid progress in ceramic matrix technologies, steady substitution of metals by polymer matrix grades and an improving supply base for specialty reinforcements are strengthening competitive barriers for late entrants. Recycling limitations, however, continue to cloud long-term circularity targets and could restrain adoption if end-of-life solutions do not keep pace with installation rates.

Key Report Takeaways

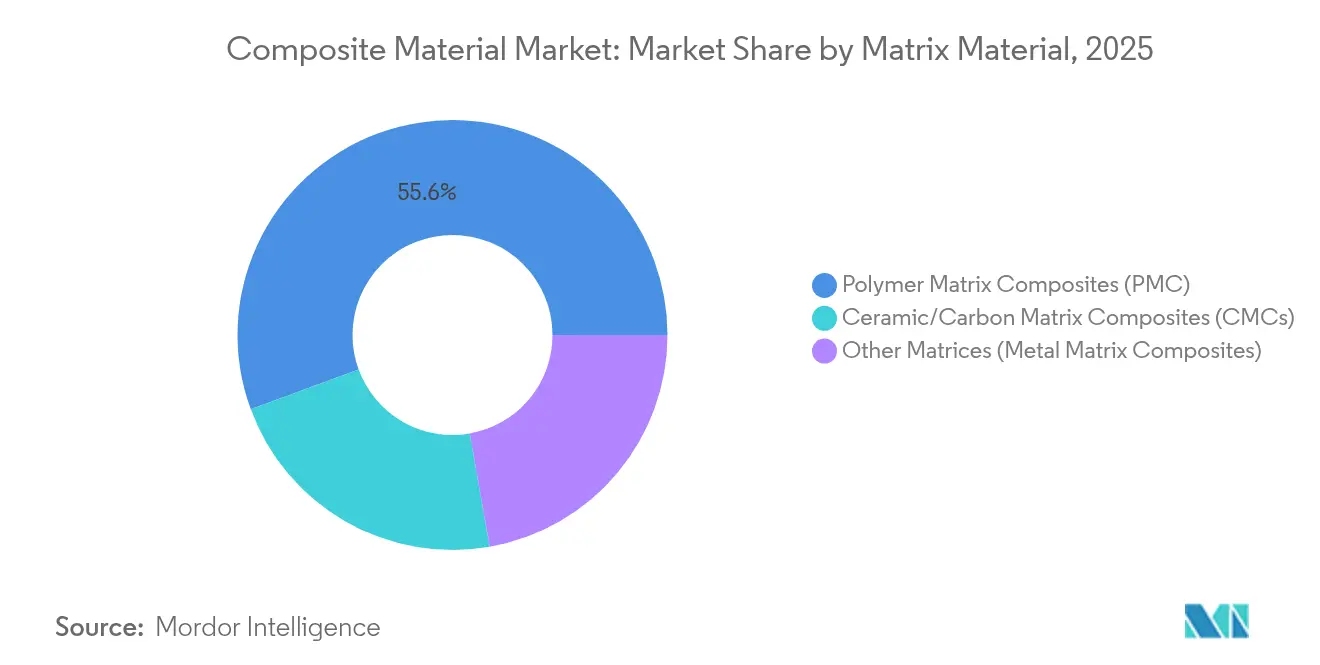

- By matrix material, polymer matrix composites commanded 55.62% of the composites market share in 2025, while ceramic matrix composites are poised to climb at an 8.12% CAGR through 2031.

- By reinforcement fiber, glass fiber held 54.63% revenue share in 2025; alternative fibers are forecast to expand at a 6.83% CAGR to 2031.

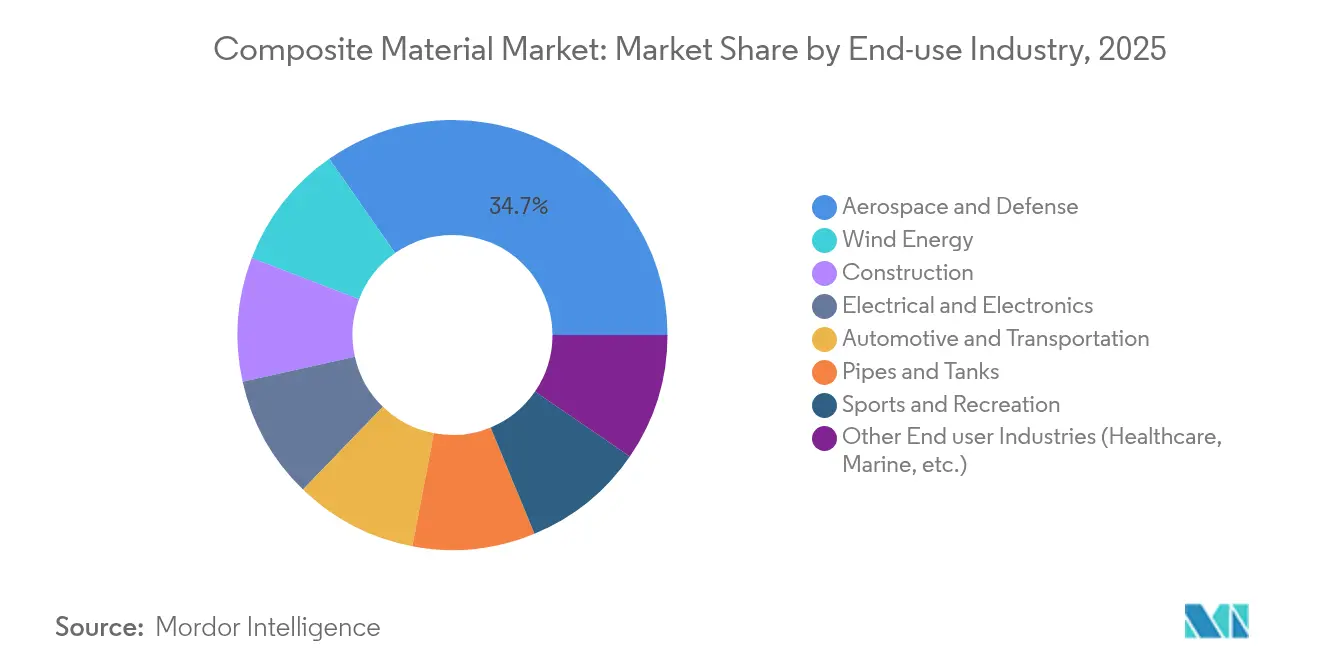

- By end-use industry, aerospace and defense accounted for 34.72% of the composites market size in 2025, whereas wind energy is surging at a 8.6% CAGR over the same horizon.

- By geography, Asia-Pacific led with 44.85% of global sales in 2025 and is tracking a 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Composite Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-driven carbon-fiber demand in e-mobility | +1.5% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Increasing usage in the manufacturing of wind turbine blades | +1.8% | Europe, Asia-Pacific, North America | Long term (≥ 4 years) |

| Growing adoption of thermoplastic composites in mass-production automotive | +1.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing use of composites in the aerospace and defense industry | +1.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancement in the Field of Material Science | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven Carbon-Fiber Demand in E-Mobility

Electric vehicles integrate roughly 450 lb of plastics and polymer composites—an 18% rise compared with internal-combustion platforms—because every 10% curb in curb weight typically stretches driving range by 6-8%[1]American Chemistry Council, “Chemistry and Automobiles 2024,” americanchemistry.com. Battery enclosures have become a flagship application, where carbon-fiber reinforced polymers deliver a 30% mass cut versus aluminum without sacrificing thermal stability. Body panels molded from glass-fiber reinforced thermoplastics enable cost-competitive lightweighting, while natural-fiber laminates in interior trim broaden sustainability credentials. Automakers are converging on multi-material architectures that blend carbon, glass and bio reinforcements to optimise stiffness, crashworthiness and lifecycle emissions. Supply chains are responding by expanding tow capacity and qualified prepreg lines across North America, Europe and East Asia to avert bottlenecks during the 2026-2028 model-launch window.

Increasing Usage in the Manufacturing of Wind Turbine Blades

Global wind installations climbed 17% in 2024 and 35% in 2025, pushing cumulative capacity toward the 450 GW mark envisaged for 2035. Next-generation offshore machines now exceed 15 MW, requiring blades longer than 110 m that can only be realised with tailored composite lay-ups. More than 1 million t of glass and carbon reinforcements will be consumed annually for blade manufacture by the end of the decade, intensifying pressure on glass-fiber melt capacity and high-modulus carbon supply. While glass-fiber reinforced plastics continue to dominate on a cost-per-meter basis, selective carbon spar caps are proliferating to curb tip deflection and blade-root mass. Europe is piloting thermoplastic blades for weldable root joints, potentially enabling recycling routes that avoid co-processing in cement kilns. The sector’s emerging blade-circularity regulations make material traceability and resin reformulation urgent priorities for OEMs and fabricators.

Growing Adoption of Thermoplastic Composites in Mass-Production Automotive

Thermoplastic composites slice processing time by up to 60% compared with legacy thermoset systems, a prerequisite for 100 000-unit vehicle programs. Automated tape-laying now yields structural panels in minutes rather than hours, while injection over-molding unites metal inserts and ribbed thermoplastic skins in a single press cycle. Pultruded crash rails and roof bows bring continuous production economies to energy-absorbing sub-frames, broadening design freedom for battery-electric platforms. OEMs also value the intrinsic recyclability of fully thermoplastic architectures, which supports closed-loop scrap reuse goals and regulatory end-of-life directives. Technology suppliers such as Syensqo have validated composite formulations that tolerate quick-step consolidation without blistering, enabling press-shop takt times aligned with conventional steel stampings. As a result, the composites market is seeing heightened interest from volume manufacturers rather than niche supercar builders alone.

Increasing Use of Composites in the Aerospace and Defense Industry

Carbon-fiber laminates now comprise up to 50% of the empty weight of wide-body airliners, underpinning fuel-burn reductions of 15-20% on long-haul routes. Ceramic matrix composites are redefining propulsion envelopes by tolerating 1 600 °C turbine-inlet temperatures, boosting thermal efficiency and cutting cooling-air penalties. GE Aerospace’s LEAP program has already logged 25 million flight hours with CMC shrouds, validating durability for civil fleets. Defense agencies leverage carbon-based structures for hypersonic vehicles where thermal stability and radar transparency coincide. Concurrently, space-launch providers specify ultra-high temperature CMCs capable of surviving re-entry spikes beyond 1 700 °C, unlocking reusable architectures for small-lift boosters. These breakthroughs ripple downstream into commercial drone fuselages and satellite antenna reflectors, reinforcing the sector’s role as a crucible for next-generation composite systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of composite materials | -0.8% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Challenges in recycling composite materials | -0.6% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Skilled-Labour Gap in Automated Lay-up Processes | -0.4% | Global, with concentration in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Composite Materials

Carbon-fiber composites typically price at five-to-ten times steel on a delivered-part basis, deterring penetration into cost-sensitive segments. Aerospace-grade prepregs entail autoclave curing, tight environmental controls and extensive non-destructive testing, each inflating unit expense. Automotive programs confront similar hurdles, confining carbon-fiber usage largely to premium marques despite favorable weight-benefit ratios. Production scale remains a pivotal barrier, since fiber-spinning lines and precursor plants run capital-intensive. Breakthroughs such as National Renewable Energy Laboratory’s thermoforming route promise 90-95% cost savings for recyclable carbon sheets, yet commercial deployment will require multi-year qualification campaigns[2]National Renewable Energy Laboratory, “Recyclable Carbon Fiber Composites Made Greener With Thermoforming,” nrel.gov. Until raw-material prices drop or design engineers capture superior system-level savings, many potential adopters may defer high-volume substitution.

Challenges in Recycling Composite Materials

Roughly 12 000 t of recyclable carbon fiber will flow out of retired aircraft in 2025, swelling an already complex waste stream. Thermoset matrices resist remelting because of cross-linked chemistries, forcing recyclers to rely on pyrolysis, solvolysis or grinding, each degrading mechanical properties. Wind-energy stakeholders anticipate parallel issues as first-generation turbine blades reach end of life; Europe alone is forecast to accumulate thousands of composite blades annually by 2030. Regulatory frameworks are tightening landfill bans, accelerating the hunt for circular routes such as cement-kiln co-processing, resin re-polymerisation and thermoplastic blade redesigns. Technological scale-up remains nascent, making recycling an enduring drag on the composites market growth trajectory until cost-competitive, high-quality secondary fiber streams emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Matrix Material: Polymer Grades Dominate While Ceramics Gain Altitude

Polymer matrix composites (PMCs) delivered 55.62% of 2025 revenue, reinforcing the composites market as the preferred option for balanced performance and manufacturability. Thermoset epoxies remain mainstream in aerospace, marine and wind blades, yet recyclable thermoplastics are steadily eroding share in automotive and consumer goods. Commercial thermoplastic UD-tape lines now exceed 1 m wide, favouring high-throughput press forming for battery trays and seat structures. In parallel, the composites market size attributable to ceramic matrix composites is projected to post an 8.12% CAGR between 2026 and 2031, propelled by aerospace propulsion and concentrated solar-power receivers.

CMCs withstand more than 1 600 °C, replacing nickel super-alloys and slashing cooling demands, thereby unlocking unrivalled thermal efficiencies. Investment outlays are significant, but once quiver production stabilises, their life-cycle value proposition offsets initial premiums through weight savings, fuel burn reductions and lower maintenance. Metal matrix composites occupy a smaller niche that thrives on extraordinary thermal conductivity and wear resistance for electronic substrate carriers and brake rotors. Additive-manufacturing pathways and five-axis CNC finishing are broadening design envelopes, hinting at incremental penetration in the latter half of the decade.

By Reinforcement Fiber: Glass Rules, Carbon Climbs and Bio Fibers Emerge

Glass fiber retained a 54.63% share of 2025 volume across the composites market, thanks to its favorable cost-to-strength ratio, corrosion immunity and electrical insulation. Innovations in low-alkali E-glass formulations have delivered modulus enhancements without meaningful price inflation, solidifying its foothold in construction rebars, boat hulls and electrical enclosures. Carbon fiber continues to scale, capturing premium demand in aerospace skins, wind-turbine spars and performance sport goods where 60% weight reductions reward end-users with tangible efficiency gains. The composites market size for higher-tensile 24k and 60k carbon tows is expanding quickly as automotive and energy customers validate mid-modulus grades.

Natural and bio-based fibers—hemp, kenaf, flax and bamboo—register the fastest growth at a 6.83% CAGR, stimulated by OEM sustainability pledges and regulatory mandates for renewable content. Hybrid fabrics interlacing natural yarns with glass rovings are mitigating historical deficits in moisture uptake and dimensional stability, extending bio fiber reach into door panels, rear shelves and acoustic headliners. Research on silane coupling agents and nano-cellulose coatings promises further property convergence between bio and engineered fibers.

By End-Use Industry: Aerospace Dominance and Wind-Energy Momentum

Aerospace and defense consumed 34.72% of composites market volume in 2025, cementing its status as the value driver for high-modulus carbon grades. Wide-body programs exploit composite fuselage barrels that cut fastener counts and deliver better fatigue performance than aluminum-lithium rivals. Regional jet and eVTOL developers replicate this design philosophy to reconcile payload limits with battery mass. Wind energy, conversely, is the fastest-growing end-use, as governments target net-zero grids by mid-century.

Blades represent up to 70% of a turbine’s composite weight, with each 15 MW offshore unit requiring more than 100 t of laminates. Automotive and transportation sectors leverage composites to offset battery weight, enhance crash energy absorption and dampen vibration; applications range from structural flooring to side-impact beams. Pressure-resistant thermoplastic composite pipes attract oil-and-gas operators seeking corrosion immunity and reduced installation costs in sour environments. Civil engineers adopt FRP bars, stay cables and bridge panels to address chronic reinforcement corrosion in coastal regions, anchoring long-term durability advantages.

Geography Analysis

Asia-Pacific anchors the composites market with 44.85% revenue in 2025 and is projected to grow at 7.45% through 2031 as China escalates offshore wind installations, India expands metro rail networks and Southeast Asia upgrades grid infrastructure. The regional composites market size also benefits from escalating carbon-fiber capacity; South Korea’s Hyosung is lifting annual output to 9 000 t to meet aerospace and hydrogen-tank demand. Japan’s value chain focuses on high-precision tow spreading and prepreg technologies, serving both domestic air-frame programs and export customers.

North America trails closely, propelled by sustained aerospace deliveries, federal investments in renewable energy and a resurgent recreational-marine segment. The United States Department of Energy earmarked USD 20 million to advance wind-turbine composite recycling, signalling policy momentum toward circularity. Canadian provinces sponsor advanced-materials clusters that couple academic R&D with injection over-molding pilot lines, aiming to retain domestic IP around bio-based thermoplastics.

Europe commands sophisticated design capabilities and stringent environmental regulations that foster rapid adoption of bio-resins and closed-loop processes. Although supply-chain disruptions and energy-cost spikes trimmed production in late-2024, the bloc maintains a 21.74% share of global volumes. Initiatives such as Vestas’s circular blades and low-emission towers illustrate how EU climate policy is steering OEM priorities toward holistic sustainability. Eastern European nations, leveraging skilled labor and proximity to Western markets, are courting investment in pultrusion and filament-winding plants.

South America and the Middle East & Africa, while collectively smaller, are registering outsized percentage gains as infrastructure modernization and desalination projects specify composite solutions. Brazilian wind corridors, Saudi desalination brine lines and South African electric-bus bodies are notable demand pockets. Technology transfer from multinational players, combined with local reinforcement supply (sisal, jute), is catalysing indigenous innovation and gradually narrowing cost gaps with imported parts.

Value Chain Analysis

The composite materials value chain starts with upstream feedstocks and intermediates (acrylonitrile and other precursors, glass and carbon fibers, and resin systems such as epoxies and high-performance thermoplastics). It then moves into intermediate forms such as fabrics, UD tapes, and prepregs, followed by converters and fabricators using processes including AFP/ATL, RTM/infusion, compression molding, pultrusion, and filament winding. In aerospace-grade applications, qualification and traceability requirements extend the chain through testing, certification, and NDT, while end-use OEMs and Tier suppliers in aerospace and defense, wind energy, automotive and transportation, construction, and pipes and tanks drive specifications and volume pull. For example, Syensqo and Toray entered a five-year strategic supply agreement effective January 2026 to support aerospace programs and reinforce supply security for qualified carbon fiber inputs.

Key constraints cluster around reinforcement and resin availability and the time required to qualify alternates. Lead times for carbon fiber tow can stretch to roughly 16 to 20 weeks during aerospace rate increases. On the supply side, capacity additions and regionalization are reshaping sourcing options, highlighted by Sinopec Shanghai Petrochemical commencing Phase I commercial operation of a 30,000 t/y large-tow carbon fiber production line in May 2026. Downstream, yield loss and scrap management are becoming more operationally important as automation scales, with greater attention on closed-loop recycling of manufacturing scrap and circular-material programs to reduce landfill exposure and strengthen lifecycle performance claims.

Competitive Landscape

The composites market is fragmented, with global leaders integrating fiber production, fabric manufacturing, and part fabrication to streamline raw material access and certification timelines. Mergers and acquisitions, such as Owens Corning’s USD 755 million divestiture of its glass-reinforcements business to Praana Group, drive scale and portfolio realignment. SGL Carbon’s 2025 restructuring of its Carbon Fibers unit highlights wind sector demand volatility and high capital requirements. Technology investments in automation, resin infusion, and rapid-cycle materials, like Toray’s acquisition of Gordon Plastics’ assets, enhance competitiveness. Companies like Syensqo focus on thermoplastic innovations to capture OEM value. Sustainability is a key growth area, with start-ups like Pond Biomaterials and Composite Recycling advancing bio-based resins and fiber recovery. Collaborations on self-healing and multifunctional laminates, alongside intellectual property in nano-fillers and graphene coatings, are expected to strengthen pricing power and raise entry barriers despite rising demand.

Composite Material Industry Leaders

Owens Corning

Hexcel Corporation

Mitsubishi Chemical Group Corporation.

Syensqo

Toray Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace sits at the intersection of high-rate manufacturing and qualification-ready material systems, where aerospace and adjacent mobility programs seek faster certification and more repeatable production. Evidence of this shift includes Toray Advanced Composites expanding NCAMP qualifications in May 2026 for its Cetex TC1225 LMPAEK thermoplastic composite system (including T700 UD tape), which supports automation-centric AFP/ATL workflows and helps shorten the pathway from material selection to qualified production. Parallel capability build-outs, such as Hexcel breaking ground in May 2026 on the Hexcel Applications Center at Wichita State University NIAR, also point to demand for industrialized automation, process development, and workforce enablement across composite part manufacturing.

Circularity and lower-carbon manufacturing also offer actionable opportunity areas as end users face tighter sustainability requirements and end-of-life challenges for composite structures. Owens Corning commissioning a circular glass fiber production line in L’Ardoise, France (December 2025) and then beginning operations using 75% green hydrogen for melting (January 2026) shows reinforcement producers moving from pilots to industrial practice on both recycled content and process emissions. On the supply side, new high-performance carbon fiber lines, including China National Building Material Group Zhongfu Shenying placing additional lines into operation in Lianyungang in June 2026, expand the capacity base. This creates room for broader adoption in wind blades, aerospace structures, pressure vessels (including hydrogen storage), and lightweight transportation platforms, provided qualified prepreg and tape capacity and localized converting can keep pace.

Recent Industry Developments

- June 2026: Hexcel Corporation announced a long-term industrial partnership with Deutsche Aircraft to supply advanced composite solutions for the D328eco regional aircraft program. The agreement reinforces multi-year demand visibility for qualified aerospace composite materials and supports platform-level design-in of composites across aerostructures.

- May 2026: Hexcel Corporation broke ground on the Hexcel Applications Center at Wichita State University’s National Institute for Aviation Research (NIAR). The facility expands capabilities in automated composite manufacturing and process development, supporting the workforce and process development needed for higher-rate composite part production.

- November 2024: Toray Industries Inc. expanded its thermoplastic composite materials portfolio by acquiring Gordon Plastics’ assets in Colorado, including a 47,000 sq. ft. facility. The acquisition added polymer processing know-how and capacity to support thermoplastic composite adoption across transportation and industrial applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from composite materials that combine a matrix (polymer, metal, or ceramic) with a reinforcement (such as fibers), supplied into major industrial uses worldwide and measured in value terms.

Scope exclusions: We exclude metal alloys and monolithic plastics that do not use a composite structure, along with lab-scale materials that are not yet commercialized.

Segmentation Overview

- By Matrix Material

- Polymer Matrix Composites (PMC)

- Thermoset Resins

- Thermoplastic Resins

- Ceramic/Carbon Matrix Composites (CMCs)

- Other Matrices (Metal Matrix Composites)

- Polymer Matrix Composites (PMC)

- By Reinforcement Fiber

- Glass Fiber

- Carbon Fiber

- Aramid Fiber

- Other Fibers (Natural/Bio Fiber)

- By End-use Industry

- Automotive and Transportation

- Wind Energy

- Aerospace and Defense

- Pipes and Tanks

- Construction

- Electrical and Electronics

- Sports and Recreation

- Other End user Industries (Healthcare, Marine, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Malaysia

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Turkey

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Nigeria

- Qatar

- Egypt

- United Arab Emirates

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on demand and supply signals that are publicly verifiable. We mainly use sources such as USGS materials statistics, UN Comtrade trade data, World Bank and IMF macro indicators, OECD industry output series, and IEA energy and industrial activity datasets, depending on relevance by end use.

After that, we cross-check industry direction using company annual reports, investor presentations, technical journals on composites processing and performance, association publications (for example, aerospace, wind, and automotive bodies), and reputable press coverage. Where needed, our analysts also use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to sanity-check capacity moves and pricing commentary. The sources listed here are illustrative and many additional public references are consulted for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work is used to convert general signals into usable inputs, especially where public data is not reported in a consistent way for composites. We speak with raw material suppliers, processors, distributors, and end users across APAC, EMEA, and the Americas, and then confirm assumptions like typical pricing ranges, substitution triggers, and utilization trends through follow-up checks so we can align the model to what is actually being bought and sold.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 47% |

| Mid tier: 61% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 14% | Managers: 56% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where production and trade data help reconstruct the demand pool by major end uses, and then the totals are translated into value using realistic pricing assumptions. To keep the model grounded, we corroborate the outcome with selective bottom-up approximations like sampled supplier roll-ups, channel checks, and volume-by-application estimates multiplied by typical average selling prices, and then adjust for overlaps.

Inputs are chosen to match how composites are purchased and processed. Common examples include reinforcement fiber consumption trends, resin and precursor price movements, composite part shipment indicators in aerospace and automotive, wind blade build rates, and construction activity proxies that influence pultruded profiles and panels. Forecasts are mainly built using scenario analysis, where growth rates for these drivers are mapped to end-use adoption, and then reviewed with interview feedback so the assumptions stay practical. When the bottom-up side has gaps (for smaller countries or fragmented processors), we use proxy ratios from comparable markets and test them against trade flows and announced capacity changes before finalizing.

Data Validation & Update Cycle

Model outputs are checked against independent signals like trade balances, capacity utilization direction, and raw material pricing trends, and then variances are investigated rather than averaged away. Outliers are re-worked through assumption reviews, and if a number still looks unusual, we re-contact sources to confirm what changed in the market.

Before sign-off, the work goes through multi-step analyst reviews that focus on year-over-year logic, unit consistency, and currency conversion timing. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major plant additions, sharp feedstock price moves, or demand shocks in aerospace, wind, or automotive. Right before delivery, an analyst performs a fresh pass so the latest public and interview-led signals are reflected.

Mordor Intelligence's Composite Material Market Size Versus Other Published Estimates

Published market sizes for composite materials often do not match because each publisher draws the line differently on what counts as a composite, which end uses are included, and how prices are converted into annual revenues. Differences in base year selection and the speed of refresh also matter, since composites pricing can move with resin and fiber inputs.

The main gap comes from scope expansion into adjacent categories like filler-heavy plastics, coatings, and nano-composites, where Mordor Intelligence counts revenues only when a reinforced composite material is sold as a composite input (rather than broader chemicals or additives that sit around the value chain). Other spreads usually come from how average selling prices are built, since some approaches lean on list prices or long-run averages, and from how regional volumes are inferred when trade codes do not perfectly isolate composite forms.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 70.94 B (2026) | |

| Industry Publisher A | USD 89.81 B (2024) | Uses a broader market framing that can blend finished composite components and adjacent material categories into the total, and the base year is earlier, which shifts the value when prices and demand cycles change. |

| Global Research Group B | USD 112.42 B (2025) | Often aggregates a wider composites umbrella with multiple process and application buckets, which can lift totals when non-material revenues or loosely defined composite formats are counted, and it relies on a different price progression over the forecast window. |

Overall, the spread is mainly explained by how wide the composite definition is drawn and how pricing is converted into revenue by year. By keeping the scope tied to clearly identifiable composite material sales and then cross-checking it with trade, capacity, and interview inputs, we end up with a number that is easier to trace and repeat when the market is updated.

Key Questions Answered in the Report

What is the current size of the composites market?

The composites market is valued at USD 70.94 billion in 2026 and is projected to reach USD 89.93 billion by 2031.

Which region holds the largest share of composites consumption?

Asia-Pacific leads with 44.85% of global revenue and is also the fastest-growing region at a 7.45% CAGR through 2031.

Why are ceramic matrix composites (CMCs) attracting attention?

CMCs can operate above 1 600 °C, enabling lighter, more efficient jet-engine and energy-system components and are forecast to expand at an 8.12% CAGR.

What is the main obstacle to broader composites adoption?

High material cost and limited large-scale recycling options remain the primary challenges constraining wider penetration into cost-sensitive sectors.

Which manufacturing processes are becoming mainstream in automotive composites?

Rapid-cycle thermoplastic techniques such as automated tape laying, compression molding and injection over-molding are now aligning with mass-production takt times.

Page last updated on: