Fiberglass Fabric Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

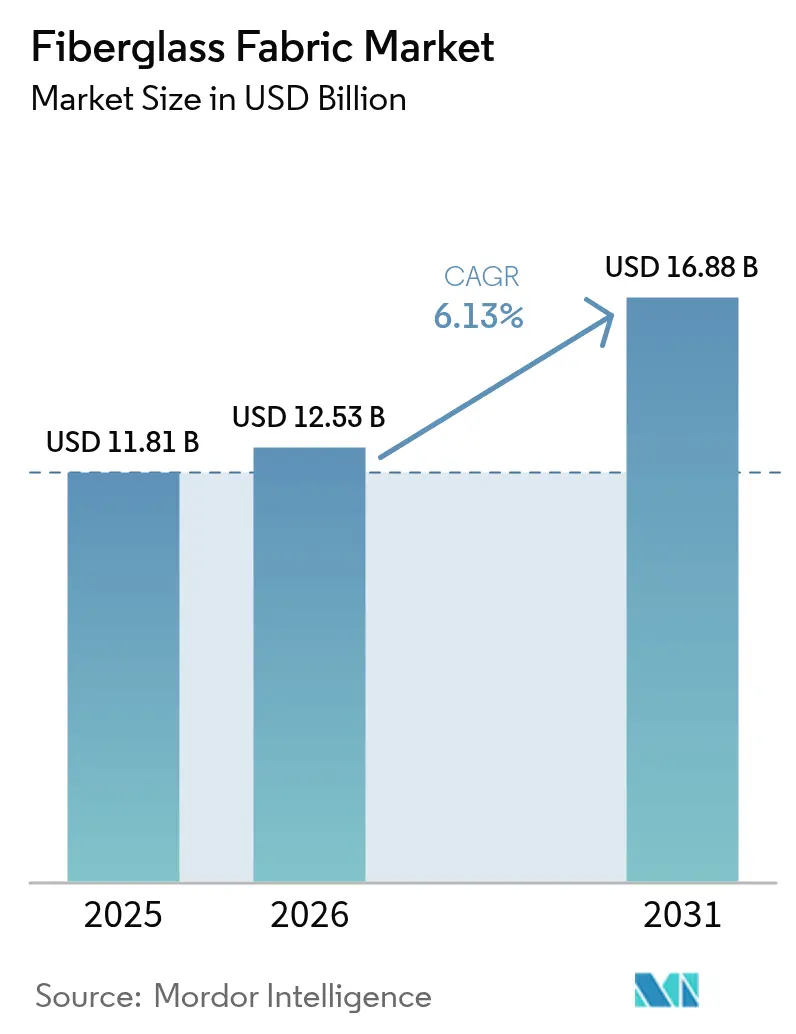

| Market Size (2026) | USD 12.53 Billion |

| Market Size (2031) | USD 16.88 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiberglass Fabric Market Analysis by Mordor Intelligence

The fiberglass fabric market size is expected to grow from USD 11.81 billion in 2025 to USD 12.53 billion in 2026 and is forecast to reach USD 16.88 billion by 2031 at 6.13% CAGR over 2026-2031. Broadly adopting lightweight composites in wind-turbine blades, automotive structures, and aerospace interiors underpins steady volume gains as end users pursue fuel efficiency and lower life-cycle costs. Cost-effectiveness and ample raw-material availability give fiberglass fabrics a competitive edge over carbon-fiber and aramid reinforcements, while progress in zero-carbon melting furnaces reduces manufacturing emissions and strengthens the material’s sustainability profile. OEMs in construction, electronics, and marine sectors also leverage woven and non-woven fiberglass to meet tightening energy-efficiency and durability codes, expanding overall addressable demand. Meanwhile, regulatory scrutiny—such as California’s 2027 ban on fiberglass in mattresses—prompts producers to accelerate recycling programs and bio-based product lines, keeping the fiberglass fabric market resilient and adaptable.

Key Report Takeaways

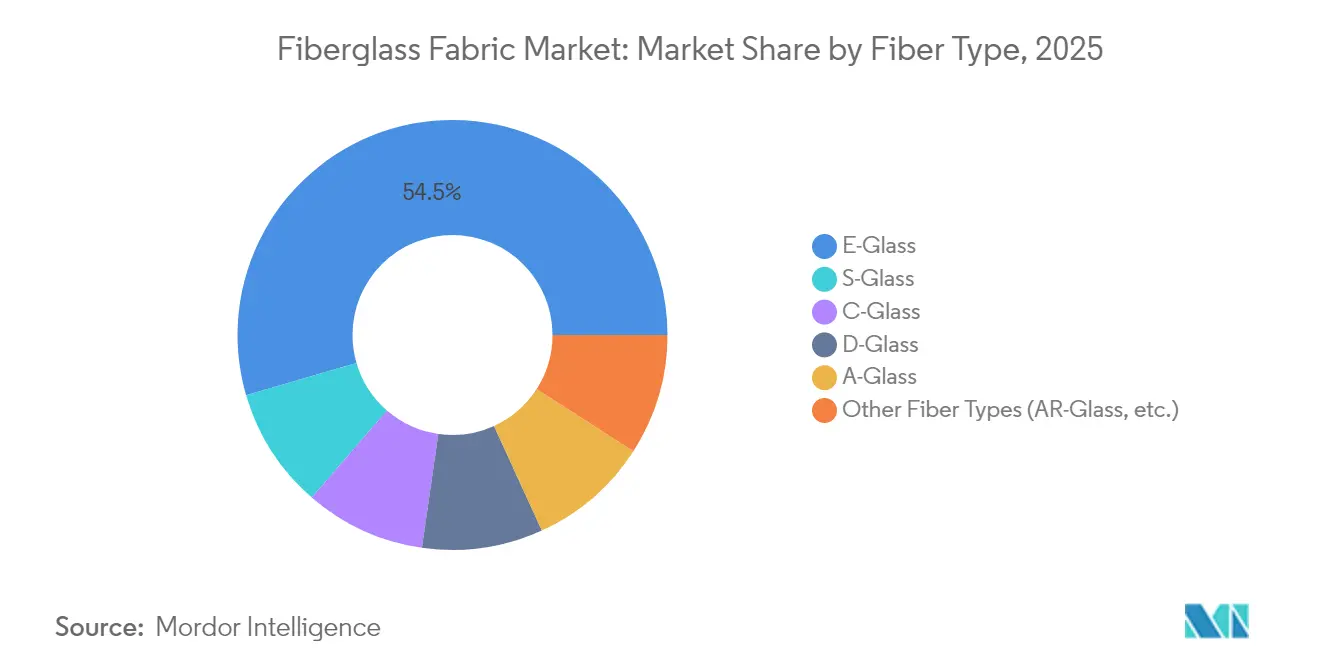

- By fiber type, E-Glass held 54.52% of the fiberglass fabric market share in 2025, while S-Glass is advancing at a 6.69% CAGR through 2031.

- By fabric type, woven structures accounted for 48.62% of the fiberglass fabric market size in 2025; non-woven fabrics exhibit the fastest CAGR at 6.39% through 2031.

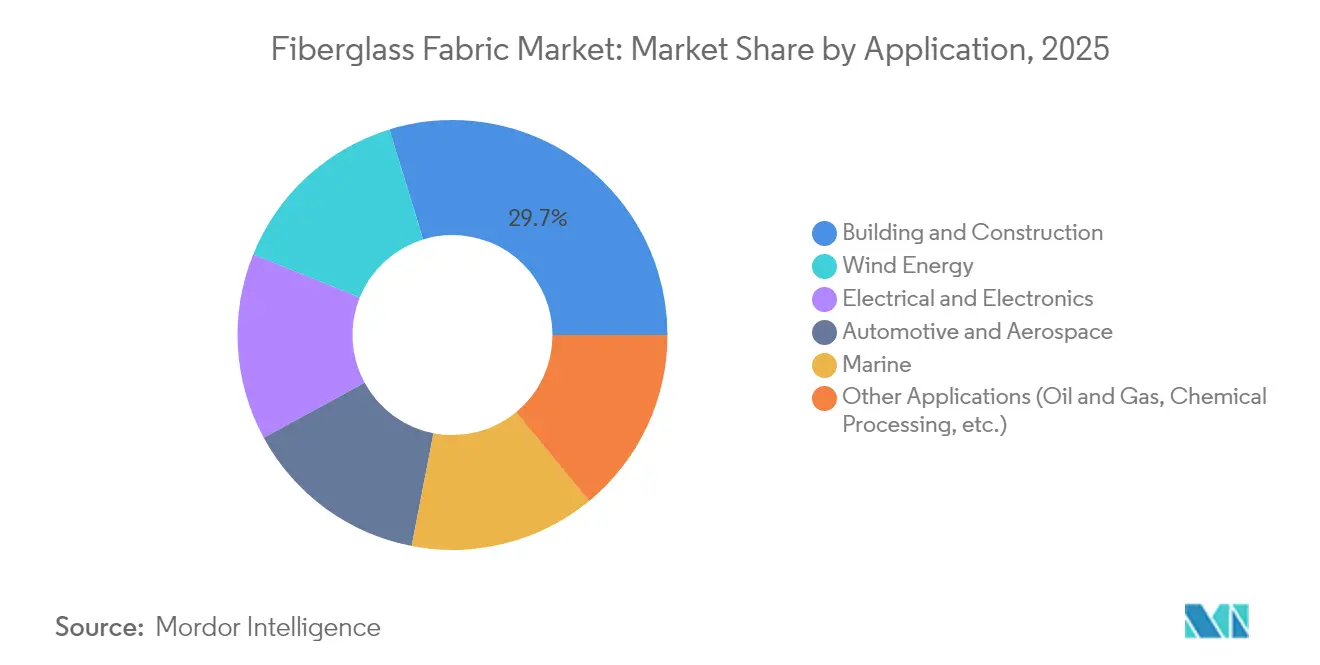

- By application, building and construction led with 29.74% revenue share in 2025, whereas wind energy is projected to grow at a 7.02% CAGR to 2031.

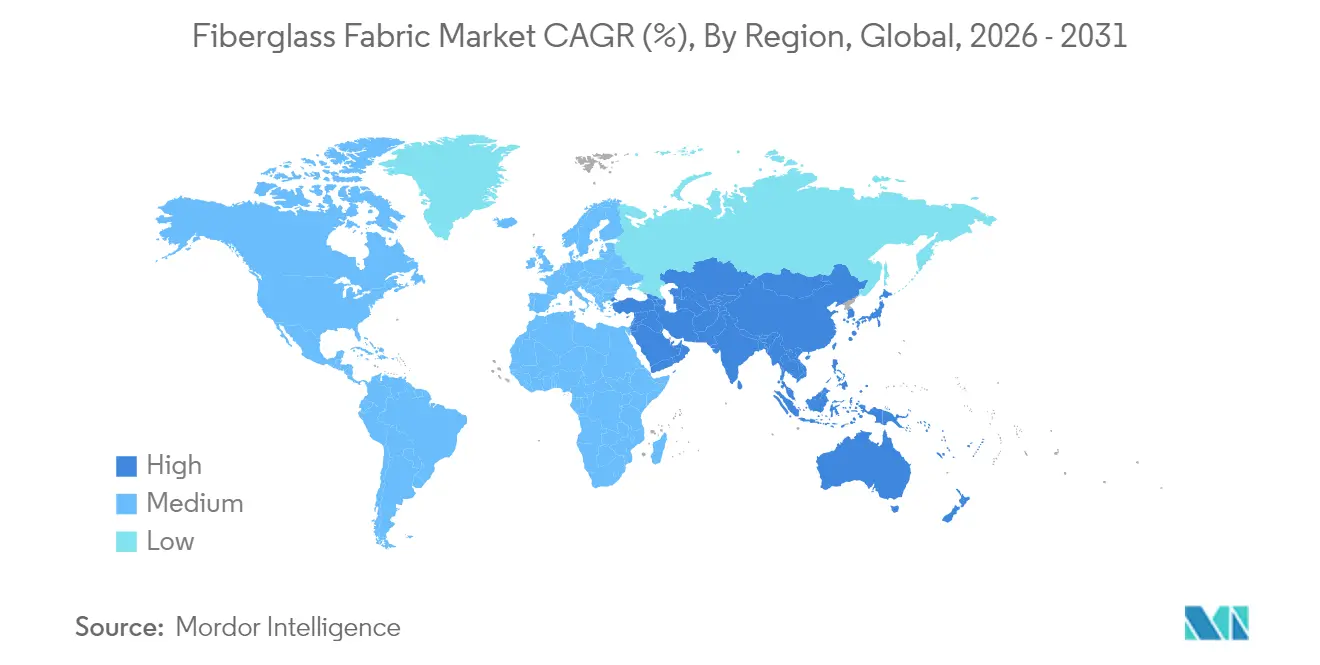

- By geography, Asia-Pacific commanded 41.47% share of the fiberglass fabric market in 2025 and is expanding at a 6.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Fiberglass Fabric Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for lightweight, high-strength materials in automotive & aerospace | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of wind-energy installations | +2.1% | Global, led by Asia-Pacific and Europe offshore markets | Long term (≥ 4 years) |

| Energy-efficient buildings boost insulation textiles demand | +1.2% | North America & Europe, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Electronics miniaturization driving EMI-shielding fabrics | +0.9% | Asia-Pacific core, spill-over to North America tech hubs | Short term (≤ 2 years) |

| Retrofitting of industrial chimneys | +0.6% | Europe and North America industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for lightweight materials in automotive & aerospace

Automakers and aerospace firms increasingly use lightweight materials to meet stringent regulations and enhance performance. In the United States, new fuel-economy and emissions rules for 2027-2032 are driving global supply chains to prioritize weight reduction. Ford exemplifies this trend with its composite C-brace in the Bronco Raptor, incorporating fiberglass-reinforced brackets and under-body panels that reduce mass without compromising safety. In civil aviation, a Dutch consortium is progressing toward validating fully composite liquid-hydrogen tanks by 2025, emphasizing the industry's reliance on high-strength glass fabrics for cryogenic containment. The strategic importance of these materials is further highlighted by private-equity investments, such as AURELIUS acquiring Teijin Automotive Technologies North America in 2024 for over USD 1 billion to leverage their lightweighting expertise. While natural-fiber composites offer up to 60% lower greenhouse gas emissions, they currently lack the mechanical consistency of fiberglass, reinforcing fiberglass's position in safety-critical applications.

Expansion of wind-energy installations

The Global Wind Energy Council recorded 117 GW of new capacity in 2024, with 8.8% annual growth expected through 2030. Blade lengths surpassing 115 m, such as Vestas’ V236 design, elevate material-volume requirements per turbine and favor hybrid E-Glass and S-Glass lay-ups that manage cost and stiffness targets. Local content policies accelerate manufacturing shifts; Kineco Exel Composites began supplying pultruded glass–carbon planks from Goa in late 2025 for Asian offshore projects. Polyurethane-carbon spar-cap technology, qualified by Dow and Vestas, achieves cure rates above 90%, yet most shear webs retain glass-fiber cores for robustness. Although SGL Carbon noted a 35.2% sales decline to wind customers due to raw-material inflation, glass-fiber suppliers benefit from substitution to lower-price reinforcements, bolstering the fiberglass fabric market.

Energy-efficient buildings boost insulation textiles demand

Fiberglass insulation captures 71% of U.S. residential installations because it meets ENERGY STAR targets at a competitive cost[1]A.M. Schletz, “High-Performance Glass-Fiber Insulation Trends,” International Journal of Applied Glass Science, ceramics.onlinelibrary.wiley.com. Retrofit activity in commercial metal buildings broadens sales, especially for laminated glass-fiber rolls specified under ASHRAE 90.1 standards. California’s Assembly Bill 1059 bans textile fiberglass in mattresses and upholstered furniture from 2027, influencing manufacturers to develop encapsulated or surface-treated formats that mitigate fiber-emission concerns[2]Stephanie Potts, “California Bans Fiberglass in Mattresses and Other Furniture,” TÜV SÜD, tuvsud.com. New polyurea resins also reduce labor and mold costs by replacing certain fiberglass lay-ups in architectural elements, yet glass fabrics remain preferred for fire-resistant insulation jackets in high-rise façades. Improving furnace efficiency and higher recycled cullet ratios further lower embodied energy, aligning the material with green-building schemes.

Electronics miniaturization driving EMI-shielding fabrics

Next-generation 5G and IoT devices raise electromagnetic-compatibility thresholds, stimulating demand for glass cloths coated with nanocarbon or metal oxides that provide >20 dB shielding effectiveness at gigahertz frequencies. Asian contract manufacturers integrate these fabrics into flexible printed-circuit laminates for smartphones and vehicle control units. Research into non-circular glass-fiber cross-sections shows 15-20% higher transverse stiffness, enabling thinner laminates without sacrificing rigidity. Commercial viability depends on scaling modified bushing plates; producers that master such technologies can access premium niches while defending share against conductive polymer films.

Restraints Impact Analysis of Fiberglass Fabric Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material & energy cost volatility | -1.4% | Global, with acute impact in energy-intensive regions | Short term (≤ 2 years) |

| Rising competition from carbon & basalt fiber fabrics | -0.8% | High-performance applications globally, concentrated in aerospace and automotive | Medium term (2-4 years) |

| Costly end-of-life fiberglass disposal regulations | -0.6% | Europe and North America, expanding to Asia-Pacific developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material & energy cost volatility

Glass melting consumes significant natural-gas and electricity inputs; spikes in European energy prices during 2023-2024 squeezed margins despite Sibelco’s 22% EBITDA rise from portfolio mix improvements. Silica-sand prices trend upward as 380 million t global output faces higher logistics and permitting costs[3]Shujie Wang, “Silica Sand Focus: Abundant Yet Critical,” Geoscience Queensland, geoscience.data.qld.gov.au. U.S. EPA rules for wool-fiberglass furnaces require continuous chromium-emission monitoring, adding compliance capital to North American plants[4]U.S. Environmental Protection Agency, “Emissions Standards for Wool Fiberglass Manufacturing,” epa.gov. Producers hedge volatility through captive renewable-energy assets; China Jushi’s zero-carbon plant integrates a 200 MW wind farm to stabilize power supply. Process scrap recycling, such as Johns Manville’s 10,000 t program in Slovakia, offsets virgin-glass demand and buffers cost swings.

Rising competition from carbon & basalt fiber fabrics

Automotive demand for carbon fiber may triple to 32,000 t by 2025, enticing large investments like Zhongfu Shenying’s USD 866 million expansion that adds 30,000 t annual capacity. Basalt fiber offers roughly 15% greater tensile strength than E-Glass at room temperature, although it loses more stability above 300 °C, limiting turbine-exhaust applications. Wind-blade OEMs increasingly specify carbon-fiber spar caps; Nordex awarded Fiberline its biggest contract yet for Delta4000 blades, eroding some glass demand. Nevertheless, recycled carbon fiber still struggles with length-consistency and cost, and many mass-market products stay anchored to glass reinforcement, sustaining the fiberglass fabric market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fiberglass Fabric Market Segment Analysis

By Fiber Type:

E-Glass dominance faces S-Glass innovationE-Glass maintained 54.52% market share in 2025 due to mature global supply networks and unit costs below USD 5/lb that meet mainstream engineering targets. S-Glass, advancing at the fastest CAGR of 6.69%, captures aerospace, defense, and rotorcraft parts where 30-35% higher tensile strength justifies its premium pricing. Specialty grades such as E6 enhanced glass bridge some performance gaps, while bioabsorbable glass fibers add opportunities in medical textiles. Suppliers balancing E- and S-Glass capacity can flex volume toward the most profitable mixes through 2031.

Adoption of AR-Glass for cement reinforcement and C-Glass for chemical containment remains steady, whereas D-Glass continues niche growth in high-dielectric radar radomes. Developers of non-circular cross-sections seek to commercialize kidney-shaped and trilobal filaments that exhibit 12-18% higher flexural stiffness at similar weight, yet require new weaving parameters. E-Glass remains the anchor product, and the fiberglass fabric market preserves supply security via multi-continent melter networks.

By Fabric Type:

Woven structures lead despite non-woven growthWoven fabrics captured 48.62% of revenue in 2025, underscoring their versatility for uni- and biaxial laminates in hulls, automotive hood liners, and aircraft flooring panels. Plain-weave and twill styles offer predictable drape and dimensional accuracy, and recent multi-end rovings enhance surface aesthetics for Class-A exterior panels.

Non-woven fabrics expand at the fastest CAGR of 6.39% as battery separators, filtration elements, and spray-up boat decks scale. Continuous-filament mats achieve isotropic strength, favoring large-surface insulation jackets, whereas chopped-strand mats support closed-mold pool production. Additive manufacturing opens a frontier: 3D-printed glass-fiber preforms reduce waste by matching load paths directly, and prototype boats built via Continuous Fiber Manufacturing validate marine potential. Woven and non-woven innovations widen fabric-type choices and strengthen the fiberglass fabric market against competitive substitutes.

By Application:

Construction Dominance Challenged by Wind Energy SurgeBuilding and construction applications command 29.74% market share in 2025, driven by fiberglass's dominance in residential insulation, accounting for 71% of US home installations due to superior thermal conductivity properties and regulatory compliance with ENERGY STAR standards. The segment's strength extends to commercial applications, including metal building insulation systems that enhance energy efficiency in industrial structures. However, regulatory headwinds from California's 2027 ban on textile fiberglass in mattresses and furniture are prompting innovation in alternative materials and safer production processes.

Wind energy emerges as the fastest-growing application at 7.02% CAGR through 2031, propelled by the Global Wind Energy Council's reported 117 GW of new installations in 2024 and projected 8.8% industry growth through 2030. Automotive and aerospace applications benefit from lightweighting mandates, with EPA emissions standards and CAFE requirements driving composite adoption in chassis components and structural elements. Electrical and electronics applications are expanding due to miniaturization trends requiring EMI shielding capabilities, while marine applications are experiencing innovation through 3D printing technologies and sustainable material development. Oil and gas, chemical processing, and other industrial applications continue to rely on fiberglass for corrosion resistance and structural integrity in harsh operating environments.

Geography Analysis

APAC Fiberglass Fabric Market

Asia-Pacific generated 41.47% of 2025 global revenue and leads future growth with a 6.93% CAGR, propelled by China’s scale and India’s infrastructure stimulus. China Jushi’s USD 812 million zero-carbon furnace complex elevates regional capacity to 400,000 t and provides local customers faster delivery cycles. Southeast Asian economies attract foreign OEMs seeking tariff advantages, and Vietnam’s coastal industrial parks host new woven-fabric looms that shorten European wind-blade lead times. India’s “Make in India” push encourages glass-fiber producers to partner with state governments on greenfield melts, ensuring raw-material availability for domestic rotor factories.

North America Fiberglass Fabric Market

North America benefits from federal tax credits that extend wind-farm deployments and building-insulation retrofits. U.S. composite shipbuilders also stimulate demand for stitched multiaxial glass fabrics that lower weight while improving impact tolerance in workboats. Meanwhile, the fiberglass fabric market size for the region remains under expansion as automotive OEMs prototype glass-thermoplastic door modules to comply with updated CAFE standards.

Europe Fiberglass Fabric Market

Europe experiences mixed signals: a softer residential-construction cycle restrains short-term insulation textiles, yet offshore-wind targets and aerospace ramp-ups sustain baseline volume. The U.K. enforces anti-dumping duties up to 99.7% on Chinese and Egyptian fabrics, prompting EU buyers to diversify toward Turkish and local producers, thereby adjusting supply chains. Regulatory focus on circularity spurs investments in glass recycling, with German plants piloting high-purity cullet streams that feed new E-Glass pulls.

South America and MEA Fiberglass Fabric Market

South America’s composite pipe and tank markets grow gradually as oil majors modernize corrosion-resistant infrastructure in Brazil. Regional wind-farm auctions in Chile and Colombia call for 100-m onshore blades, opening opportunities for local fabric conversion. The Middle East & Africa region remains a smaller slice, yet United Arab Emirates desalination projects specify glass-fiber composite gratings for corrosion resistance, anchoring a steady, if niche, demand profile across arid climates.

Competitive Landscape

The global supply chain is highly consolidated and dominated by a few vertically integrated players managing melting, yarn production, and fabric weaving, ensuring cost efficiency and quality control. Owens Corning’s USD 755 million divestiture of its glass-reinforcements division to Praana Group in 2024 reshaped North American leadership and emphasized building-material synergies. China Jushi maintains cost leadership through scale, backward integration, and renewable energy use. Competitive differentiation focuses on low-carbon production, closed-loop recycling, and advanced fabric architectures like ±45° triaxials. Technological advancements, including AI-driven batching and digital twin modeling, enhance operational efficiency, while EMI shielding and compostable glass opportunities attract agile innovators.

Fiberglass Fabric Industry Leaders

Owens Corning

Hexcel Corporation

China Jushi Co., Ltd.

Saint-Gobain

Chongqing Polycomp International (CPIC)

- *Disclaimer: Major Players sorted in no particular order

Fiberglass Fabric Market Companies Covered in this Report

- Ahlstrom

- BGF Industries Inc.

- Central Glass Co. Ltd

- China Jushi Co., Ltd.

- Chongqing Polycomp International (CPIC)

- CTG Group

- Fulltech Industries Corp.

- Hexcel Corporation

- Johns Manville

- Mid-Mountain Materials Inc.

- Owens Corning

- Saertex GmbH & Co. KG

- Saint-Gobain

- Taiwan Electric Insulator Co. Ltd

Recent Industry Developments in Fiberglass Fabric Market

- May 2025: Tech-Fab Europe, headquartered in Frankfurt, Germany, and a member of EuCIA in Brussels, Belgium, published a life cycle assessment (LCA) study on glass fiber fabrics. The study highlights the environmental benefits of developing a robust European supply chain for glass fiber products. It further emphasizes the importance of such a supply chain in enabling European manufacturers to produce sustainable composite solutions across various markets.

- October 2023: California enacted AB 1059, a legislation that restricts using textile fiberglass in mattresses, juvenile products, and upholstered furniture. Effective January 1, 2027, this law expands upon Article 5.5 of Chapter 3, Division 8 of the Business and Professions Code, which already limits the use of flame retardants in these product categories.

Fiberglass Fabric Market Report Scope and Research Methodology

Market Definition and Coverage

Our study treats the fiberglass fabric market as the value generated from freshly manufactured woven and non-woven fabrics made with glass filaments, predominantly E-glass and S-glass, supplied to end uses such as construction reinforcements, wind-turbine blades, printed-circuit boards, marine laminates, and automotive or aerospace composites. According to Mordor Intelligence, this universe was worth USD 11.81 billion in 2025 and is forecast through 2030 under constant-currency terms.

Scope exclusion: recycled chopped strands and glass-fiber mats sold as insulation materials lie outside this definition.

Segments Covered in This Report

- By Fiber Type

- S-Glass

- C-Glass

- D-Glass

- A-Glass

- E-Glass

- Other Fiber Types (AR-Glass, etc.)

- By Fabric Type

- Woven Fiberglass Fabrics

- Non-Woven Fiberglass Fabrics

- By Application

- Automotive and Aerospace

- Building and Construction

- Wind Energy

- Electrical and Electronics

- Marine

- Other Applications (Oil and Gas, Chemical Processing, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed fabric converters in China, OEM composite buyers across Europe and North America, and engineering consultants active in offshore wind. Discussions clarified average selling prices, scrap rates, and specification switches (for instance, heavier GSM cloths in 100-meter blades) that are seldom published, allowing us to fine-tune utilization factors and five-year price curves.

Desk Research

We began by mapping demand pools with public trade data from UN Comtrade, USITC, and Eurostat that specify HS codes for glass fabrics, and we layered that with production disclosures from listed fiberglass makers aggregated in D&B Hoovers and Factiva. Construction outlooks from FIB, turbine installation datasets from GWEC, and vehicle build statistics from OICA supplied the activity indicators that anchor consumption ratios. Standards and patent trends captured through Questel helped our team spot technology shifts toward multi-axial non-crimp fabrics. These references illustrate but do not exhaust the secondary corpus consulted.

Market-Sizing & Forecasting

A top-down construct converts gross production and trade flows into apparent domestic supply, which is then reconciled with a bottom-up check that multiplies sampled ASPs by indicative volumes reported by leading suppliers and channel partners. Key variables include residential floor-space completions, nacelle additions, PCB square-meter output, average layer ply counts, resin-to-fabric ratios, and exchange-rate adjusted ASP trajectories. Multivariate regression is run on these drivers to project demand, while scenario analysis captures upside from faster wind build-outs or downside from carbon-fiber substitution. Gaps in bottom-up estimates, common in fragmented marine segments, are bridged by interpolating fiber-through-resin conversion factors validated in interviews.

Data Validation & Update Cycle

Intermediate outputs pass a variance scan against historic import parity values and independent shipment tallies. Senior reviewers challenge anomalies, and adjustments loop back to contacts where divergence exceeds threshold flags. Models refresh annually, with rapid updates triggered by events such as anti-dumping duties or major capacity additions, so clients receive our most current baseline.

How Mordor Intelligence's Fiberglass Fabric Market Size Compares to Other Published Estimates

Published figures often differ because studies mix insulation mats with fabrics, assume one price fits all across grades, or freeze input series for years. We acknowledge these realities up front and show how disciplined scope setting and rolling price audits keep our totals balanced.

Key Gap Drivers: competitor numbers diverge when industrial yarn or glass wool inflates the pot, when aggressive turbine scenarios stretch volumes, or when static ASP mark-ups skip freight and energy surcharges that our quarterly checks capture.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.81 B (2025) | Mordor Intelligence | - |

| USD 14.01 B (2024) | Global Consultancy A | Includes insulation mats and specialty glass fabric coatings |

| USD 9.39 B (2024) | Trade Journal B | Uses single global ASP and omits freight-adjusted regional splits |

Taken together, the comparison shows that our measured scope, dual-path modeling, and annual refresh cycle provide a midpoint that decision-makers can trace back to concrete variables and reproducible steps, lending superior dependability to Mordor Intelligence estimates.

Key Questions Answered in the Report

What is the current Fiberglass Fabric Market size?

The fiberglass fabric market is valued at USD 12.53 billion in 2026 and is projected to reach USD 16.88 billion by 2031 on a 6.13% CAGR trajectory.

Which region leads the fiberglass fabric market?

Asia-Pacific holds the largest regional share at 41.47% in 2025 and is also expanding fastest at a 6.93% CAGR through 2031.

Which application segment is growing the fastest?

Wind energy is the fastest-growing application segment, projected at a 7.02% CAGR because of rising offshore-turbine deployments.

How are environmental regulations affecting the market?

Regulations such as California’s AB 1059 and stricter EPA standards are incentivizing producers to invest in recycling, zero-carbon furnaces and safer fiber treatments, reshaping competitive strategies.

Page last updated on: