Stretch And Shrink Film Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

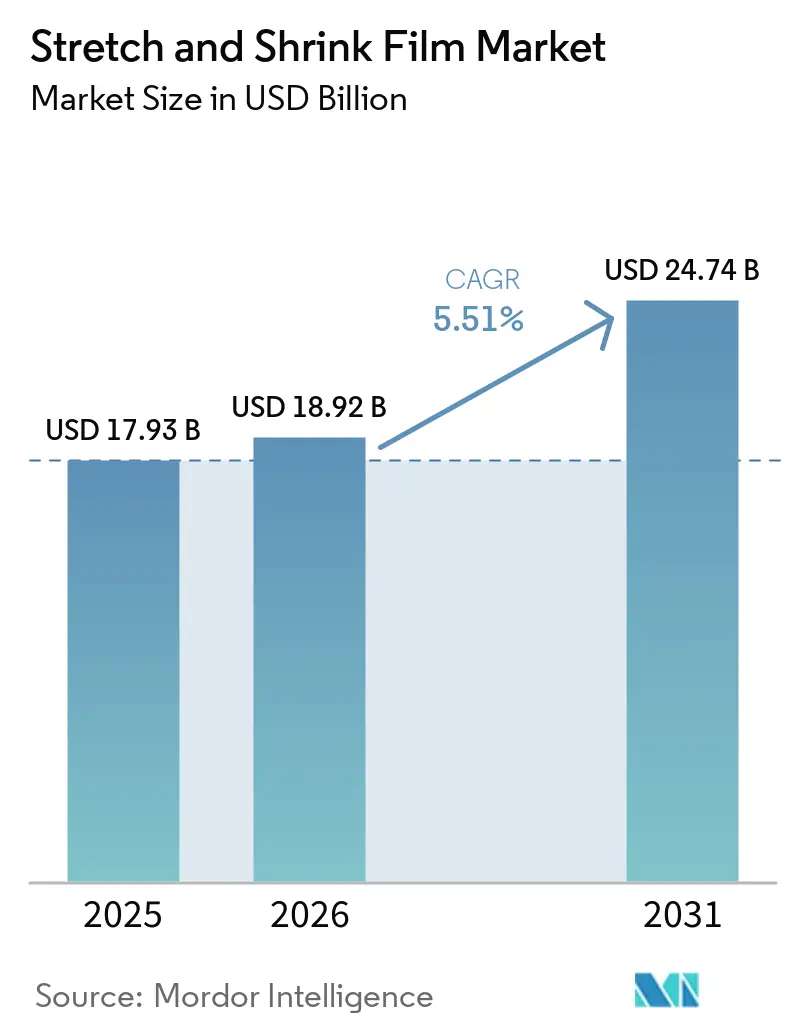

| Market Size (2026) | USD 18.92 Billion |

| Market Size (2031) | USD 24.74 Billion |

| Growth Rate (2025 - 2030) | 5.51% CAGR |

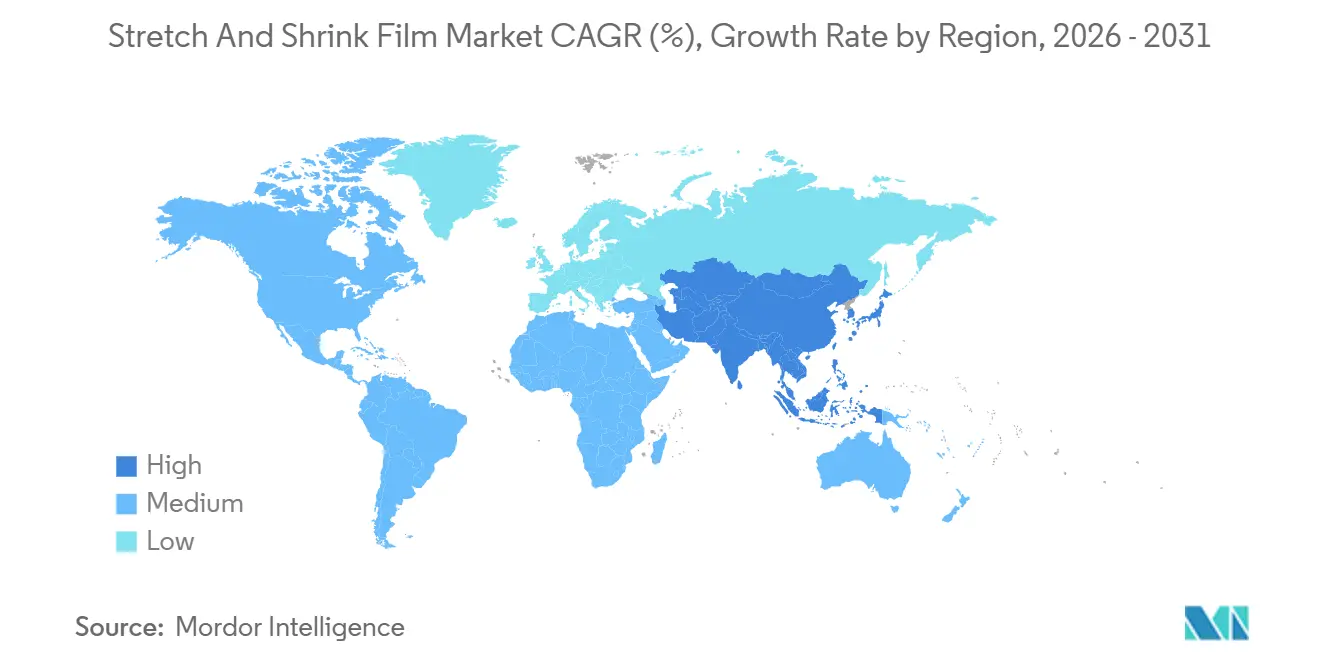

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

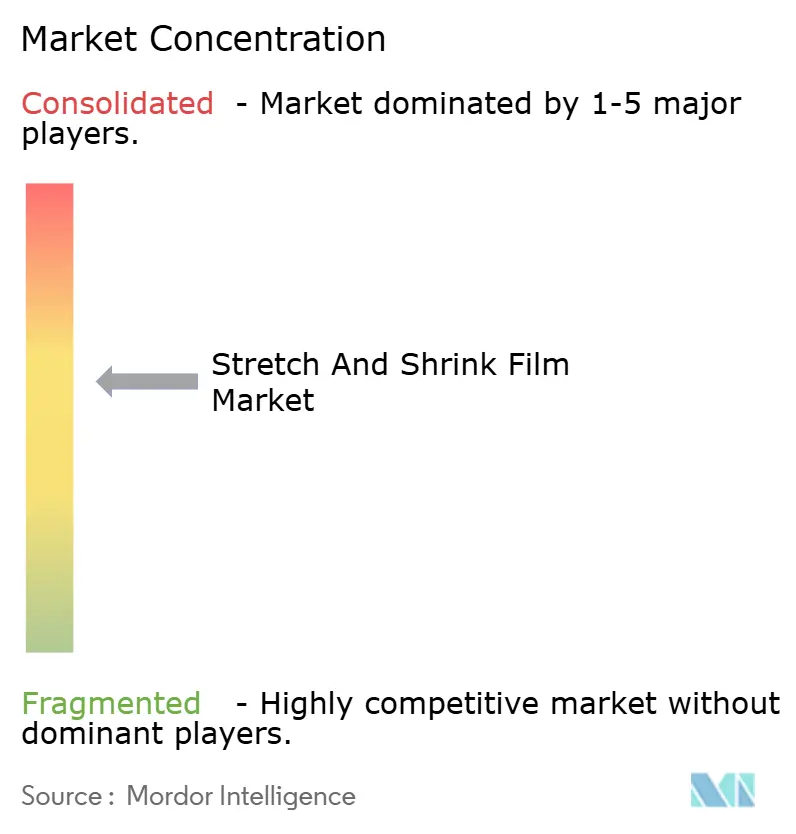

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stretch And Shrink Film Market Analysis by Mordor Intelligence

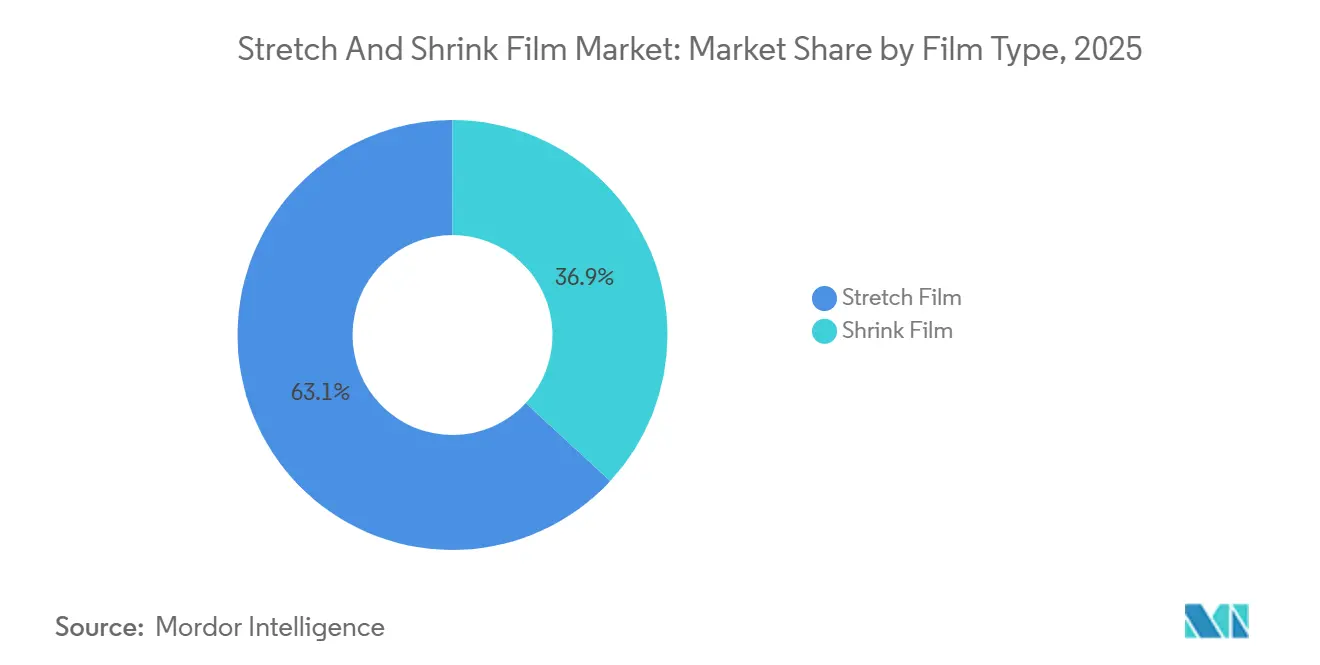

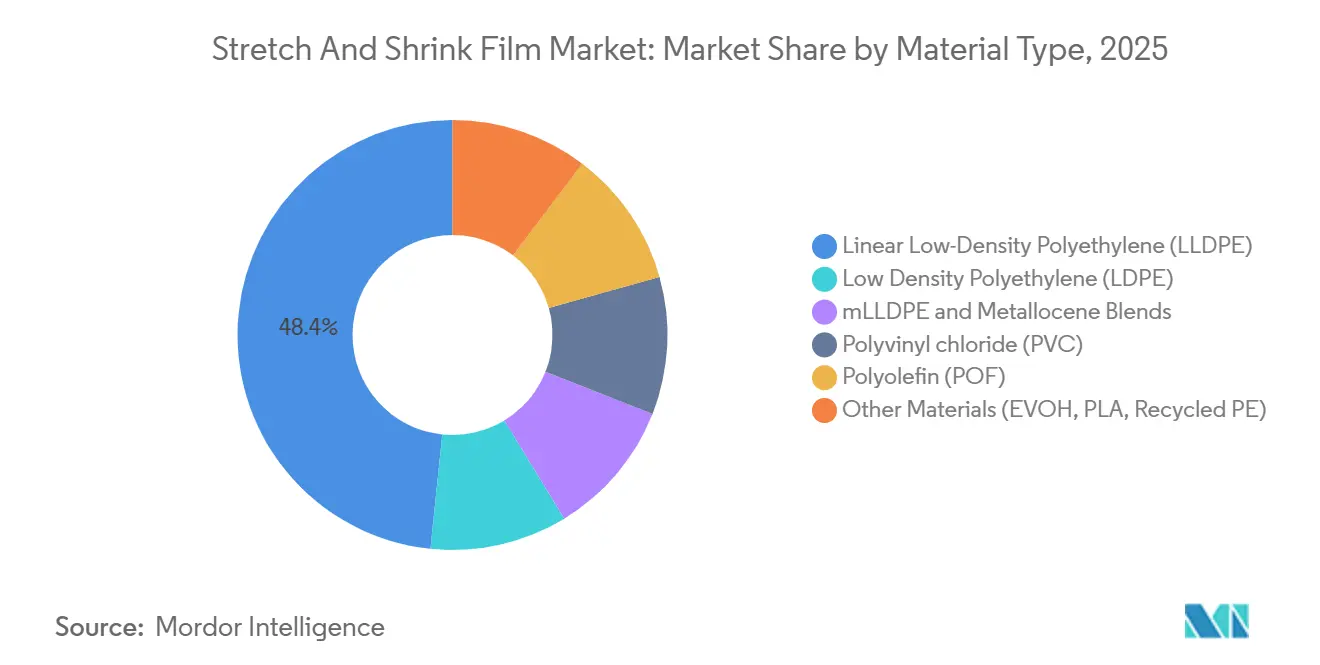

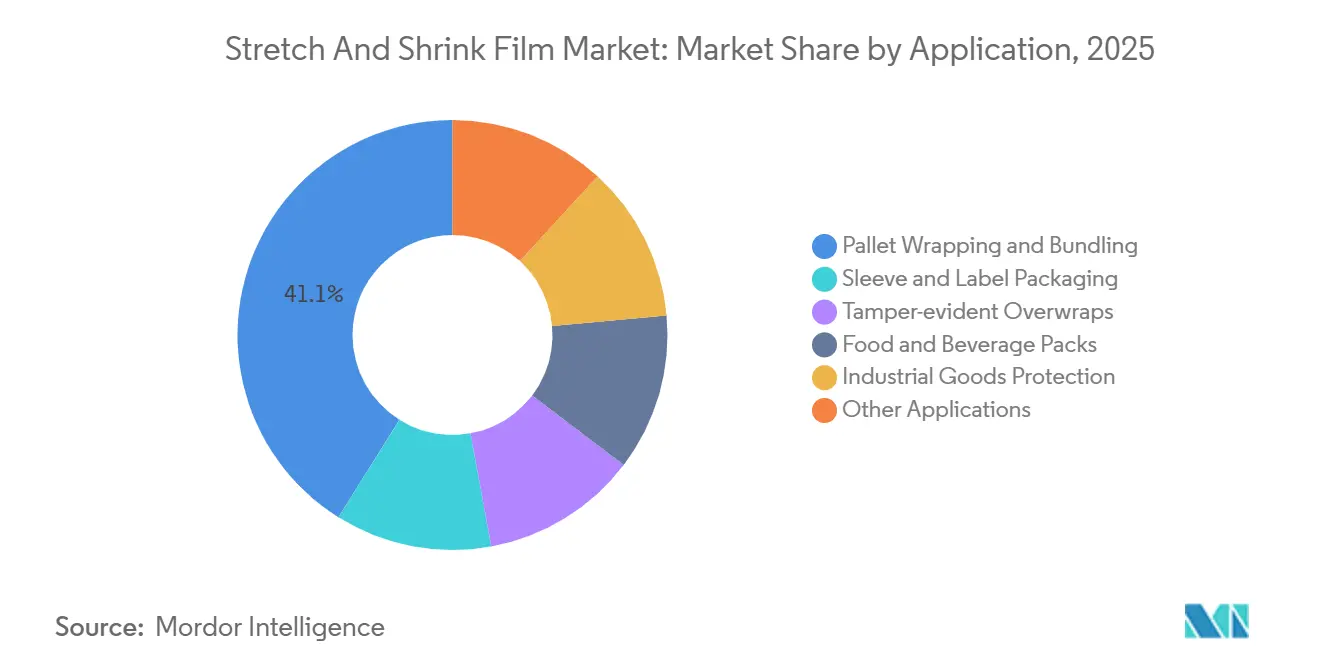

The Stretch And Shrink Film Market size is expected to grow from USD 17.93 billion in 2025 to USD 18.92 billion in 2026 and is forecast to reach USD 24.74 billion by 2031 at 5.51% CAGR over 2026-2031. Converters are achieving efficiency gains by utilizing metallocene-catalyzed resins, reducing material use by 10-20%. These resins also align with the European Union's 2030 mandate of 35% recycled content in flexible packaging. The market is witnessing a reshaping of supply dynamics, highlighted by the completion of the Amcor-Berry Global transaction in 2025, valued at USD 8.4 billion. This merger has positioned the combined entity as North America's leading platform for polyethylene shrink films. While linear low-density polyethylene (LLDPE) commanded a 48.36% material share in 2025, metallocene blends are gaining traction. Their advantage lies in producing thinner gauges without compromising puncture resistance, a feature that aids e-commerce shippers in reducing both freight costs and carbon emissions. In 2025, pallet wrapping accounted for 41.11% of the revenue, driven by a surge in demand for tamper-evident, high-clarity wraps, a trend accelerated by nearshoring. Meanwhile, sleeve and label packaging is projected to grow at 6.01% through 2031. This growth is attributed to the beverage industry's transition from PVC to polyolefin shrink sleeves, which are eligible for store drop-off recycling programs. In 2025, the Asia-Pacific region captured 41.25% of global revenue and is poised for a 6.19% growth, bolstered by new capacities in India catering to export corridors heading to the Gulf Cooperation Council and Southeast Asia.

Key Report Takeaways

- By film type, stretch films commanded 63.11% of 2025 revenue, while shrink films are projected to post the fastest growth at a 5.89% CAGR from 2026 to 2031.

- By material, LLDPE represented 48.36% of 2025 revenue, and metallocene-based blends are expected to expand at a 5.76% CAGR from 2026 to 2031.

- By thickness, conventional 15-25 µm gauges held 44.27% of 2025 sales, whereas the ultra-thin segment (≤15 µm) is forecast to grow at 5.83% CAGR from 2026 to 2031.

- By application, pallet wrapping captured 41.11% of 2025 revenue; sleeve and label packaging is the fastest-growing application at a 6.01% CAGR from 2026 to 2031.

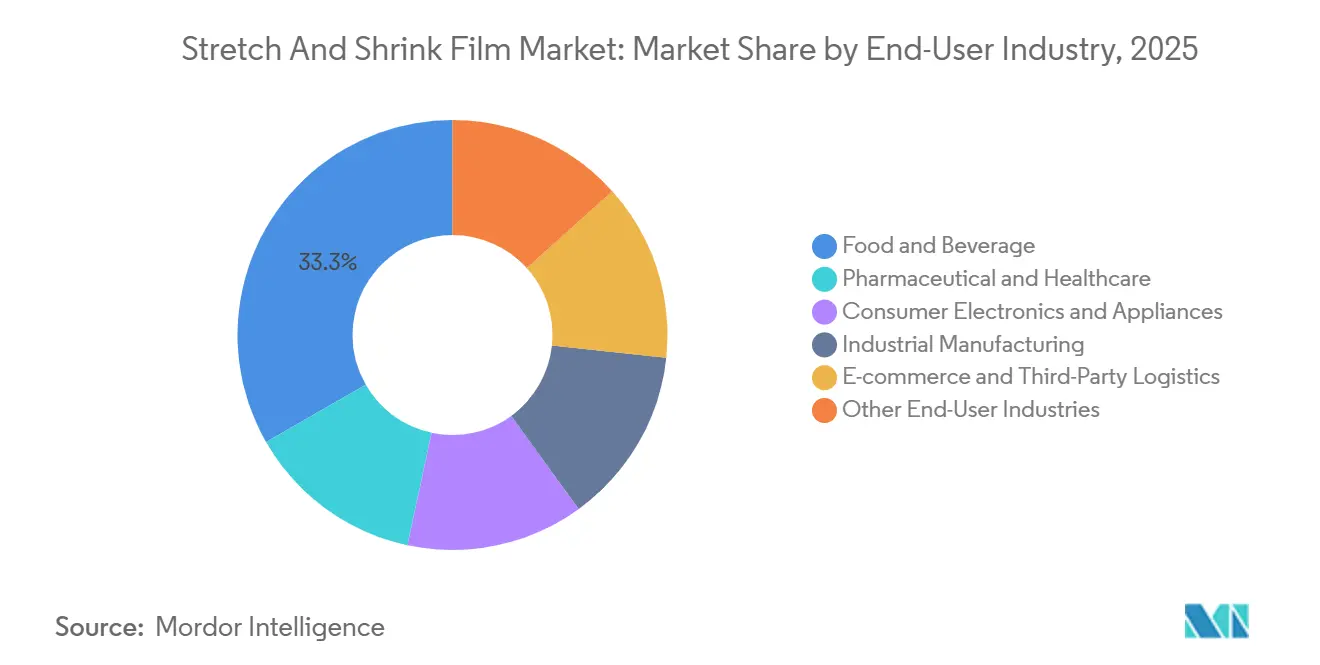

- By end user, food and beverage led with 33.28% of 2025 demand, yet e-commerce logistics is expected to register a 6.13% CAGR from 2026 to 2031.

- By geography, Asia-Pacific led with 41.25% of 2025 demand, and the region is also expected to be the fastest growing with a 6.19% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stretch And Shrink Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for pallet unitization and tamper-proof loads | +1.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability push for downgauged and recyclable films | +1.5% | Europe and North America; APAC uptake rising | Long term (≥4 years) |

| Expansion of cold-chain food and beverage logistics | +0.9% | Asia-Pacific core; Middle East spill-over | Medium term (2-4 years) |

| Automation of stretch-hooding lines in emerging markets | +0.8% | Asia-Pacific and Latin America | Short term (≤2 years) |

| Growth of pharma low-temperature distribution channels | +0.6% | Global, led by North America, Europe, India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pallet Unitization and Tamper-Proof Loads

As light manufacturing was reshored to Mexico and the U.S. Southeast, the volume of palletized freight increased, driven by the need for secure multi-modal transport to prevent edge tears and load shifting. In 2026, parcel traffic in North America exceeded 25 billion units. A shift of just one percentage point from loose cartons to palletized shipping is projected to reduce damage claims by approximately 10%. The demand for tamper-evident wraps with tear strips is growing, particularly among pharmaceutical and electronics shippers, due to compliance requirements with the FDA's 21 CFR Part 11 electronic-records regulations. In India, the installation of automated stretch-hooding systems, with a capacity of 200 pallets per hour, is addressing export lane challenges where temperature and humidity fluctuations require improved load retention. The transition from manual to automated lines is driven by the potential to lower labor costs by up to 60% per pallet and reduce film usage by as much as 35%, offering a return on investment within two years, even in regions with lower wage scales.

Sustainability Push for Downgauged and Recyclable Films

By 2030, the European Union's Packaging and Packaging Waste Regulation requires flexible packaging to contain 35% recycled content and be fully recyclable. Non-compliance could lead to penalties of up to 3% of a company's annual turnover[1]European Commission, “Packaging and Packaging Waste Regulation,” europa.eu. In response, converters are turning to a 12-micron metallocene-based stretch film, which offers puncture resistance while using nearly 50% less resin. Additionally, the seven-layer coextrusion technology has allowed for a reduction in stretch-hood film gauges from 100 µm to 80 µm, maintaining corner-hold strength. Meanwhile, in the U.S., California's SB 54 mandates a 25% cut in single-use plastic packaging by 2032[2]California Department of Resources Recycling and Recovery, “SB 54 Plastic Pollution Prevention,” calrecycle.ca.gov . The state also imposes fees, potentially reaching USD 500 million annually, to bolster recycling infrastructure. This intensifies the push on brands to choose recyclable and lighter films.

Expansion of F&B Cold-Chain Requiring High-Clarity Shrink Film

Films that maintain optical clarity are required for pharmaceutical and perishable supply chains, operating within temperatures of −20 °C to +40 °C. High-clarity polyolefin shrink films, activating at 200-275 °F, are replacing PVC in beverage multipacks. Their ability to comply with store drop-off recycling protocols, certified by the Association of Plastic Recyclers, drives their adoption. In 2025, India’s National Cold Chain Development Program allocated USD 1.8 billion for refrigerated warehousing, which is expected to increase the demand for shrink-sleeve labels capable of withstanding multiple condensation cycles.

Automation of Stretch-Hooding Lines in Emerging Markets

In India, Vietnam, and Thailand, contract packagers are increasingly adopting automated stretch-hooders. These machines use 30-50% less film compared to traditional spiral wrapping while providing five-sided coverage. Facilities shipping over 50,000 pallets monthly can recover the capital investment of USD 250,000-500,000 within approximately 18 months. Additionally, a 22% increase in packaging machinery imports to India in 2025 highlights the growing focus on automation driven by the need for consistent pallet appearance and recyclable mono-material films.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polyolefin and PVC feedstock prices | -0.9% | Global, with acute pressure in import-dependent regions (Europe, Southeast Asia) | Short term (≤2 years) |

| Contamination in mechanical-recycled PE stream | -0.5% | North America and Europe, where PCR mandates are strictest | Medium term (2-4 years) |

| High capex for multilayer thin-gauge extrusion upgrades | -0.4% | Emerging markets (India, Latin America, MEA) with limited access to equipment financing | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Contamination in Mechanical-Recycled PE Streams

Retail stretch-film bales often include labels and adhesives, which reduce the yield of clean flake to 60-75%. Even small amounts of PVC or polypropylene can form gels in new film, causing melt-flow indices to fall outside acceptable limits. While closed-loop initiatives such as the SYNDIGO facility in Indiana have achieved yields above 85% through strict sorting protocols, much of the mechanical-recycling network continues to face variability. These inconsistencies limit the proportion of recycled content suitable for food-contact or high-clarity applications.

High Capex for Multilayer Thin-Gauge Extrusion Upgrades

Producing films of ≤15 µm thickness, while achieving puncture resistance similar to 20-23 µm gauges, requires investment in seven-to-eleven-layer nano-layer lines, each costing between USD 5-12 million. For family-owned converters in India and Latin America, financing these lines at interest rates of 8-12% extends the payback period beyond five years. Furthermore, a lack of skilled process engineers increases the challenges, resulting in ultra-thin capacity being primarily held by global companies with access to low-cost capital and centralized R&D.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Stretch Strength Remains, Shrink Gains Momentum

In 2025, stretch film dominated the market, accounting for 63.11% of total revenue, largely due to its widespread use in automated wrappers capable of processing up to 200 pallets per hour. This growth is driven by the rising demand from e-commerce warehouses and nearshored factories for high-clarity, tamper-evident unitization. Innovations like pre-oriented nano-layer films, which offer a remarkable 300% pre-stretch ratio while minimizing resin usage, are fueling this expansion. Additionally, end users are increasingly favoring perforated stretch films, especially for produce distribution, as they facilitate moisture dissipation.

While shrink film accounted for the 36.89% market share in 2025, it's projected to surpass stretch film, growing at an annual rate of 5.89% until 2031. This surge is attributed to the shift from PVC to polyolefin in beverage multipacks and sleeve labels. Polyolefin's activation window of 200-275 °F not only reduces tunnel residence times but also addresses dioxin concerns associated with PVC, especially in light of state-level bans set to take effect in 2025. Furthermore, high-clarity formulations are now compliant with store drop-off recycling protocols, prompting a swift conversion among brands. The demand for shrink films is also bolstered by the cold-chain infrastructure developments in Southeast Asia and the Middle East, ensuring seal integrity amidst temperature fluctuations.

By Material Type: Metallocene Blends Narrow the Gap

LLDPE held 48.36% of 2025 sales due to its 15-25% cost edge and broad compatibility with legacy extruders. The stretch and shrink film market share for LLDPE is expected to fall modestly as metallocene blends climb at a 5.76% CAGR through 2031, benefiting from downgauging that shaves freight weight by up to 30%. Global metallocene capacity topped 26 million tpa in 2025, and converters in India are adopting the resin at 6.15% yearly growth to serve export lanes that require superior load retention.

Polyolefin shrink films, traditionally a niche, are scaling quickly as recycling mandates bite in Europe and North America. Low-density polyethylene remains important in hand-film applications that rely on its high cling and gloss, while PVC’s share continues to decline except in certain industrial sleeves where optics and stiffness are critical. Recycled polyethylene is gaining momentum as brand owners commit to 25-30% post-consumer content by 2030; SYNDIGO recycled LLDPE is already displacing virgin grades in non-food wraps after proving parity in puncture testing.

By Thickness: Ultra-Thin Gauges Win Premium Positioning

In 2025, conventional gauges measuring 15-25 µm accounted for 44.27% of the turnover, striking a balance between cost, equipment compatibility, and mechanical strength. Ultra-thin films, measuring 15 µm or less, are witnessing a 5.83% annual growth, thanks to nano-layer dies that enhance tear strength with over 100 alternating micro-layers. A newly commercialized stretch film, transitioning from 23 to 12 µm in 2025, achieved a 48% reduction in material usage and a 20% decrease in Scope 3 emissions per pallet, all while maintaining load integrity on fully automated lines.

Films exceeding 25 µm continue to play a crucial role in heavy-duty applications, from construction and steel coils to agricultural silage. Here, the emphasis on UV stability and puncture resistance takes precedence over mere weight savings. While their growth is more gradual, it's consistently supported by capital projects in infrastructure and renewables, both of which demand corrosion-resistant packaging for extended outdoor storage.

By Application: Logistics Diversifies Beyond Pallet Wrapping

Pallet wrapping retained 41.11% of application revenue in 2025 thanks to a vast installed base of rotary and orbital wrappers that secure billions of pallets each year. The stretch and shrink film market size for pallet wrapping is forecast to reach USD 10.4 billion by 2031, although its share will erode slightly as newer uses expand. Tamper-evident overwraps and stretch-hoods providing five-sided coverage with 30-50% less film are scaling quickly in pharmaceutical and electronics supply chains.

Sleeve and label packaging is the fastest-growing application at a 6.01% CAGR through 2031, propelled by beverage brands retiring PVC sleeves in favor of polyolefin alternatives that meet recycling protocols. Food and beverage multipacks continue to rely on shrink bundles that deliver high shelf-impact clarity, while industrial goods protection and agriculture favor thicker films with UV stabilizers.

By End-user Industry: Food & Beverage Dominance Amid E-commerce Surge

Food and beverage held 33.28% of 2025 demand as canned foods, beverages, and fresh produce rely on clear, strong overwraps for visual inspection and tamper evidence. E-commerce logistics is rising at a 6.13% CAGR to 2031, fueled by North American parcel traffic exceeding 25 billion units in 2026. Automated lines running 200 pallets per hour demand downgauged film with 300% pre-stretch that slashes resin consumption without compromising load security.

Pharmaceutical and healthcare use is expanding on parallel timelines as biologics and vaccines need films retaining flexibility at −80 °C. Temperature-indicator and RFID-enabled wraps ensure chain of custody under serialization laws in the European Union and the United States. Consumer electronics, appliances, and industrial manufacturing round out demand with modest but steady growth linked to durable-goods output.

Geography Analysis

Asia-Pacific generated 41.25% of 2025 revenue and is projected to grow at 6.19% to 2031. Capacity additions worth Rs 2,240 crore (USD 251 million) in Gujarat and Karnataka will feed exports to Gulf and Southeast Asian corridors. China supplies the largest volume but slower domestic consumption is pushing converters toward overseas markets, while India, Vietnam, and Thailand are adding automated stretch-hooding to meet multinational client specifications. Developed economies such as Japan, South Korea, and Australia focus on recycling-ready mono-films and line automation upgrades.

North America ranked second in 2025, supported by the Amcor-Berry merger that created the region’s largest shrink-film platform. Sigma Plastics Group’s USD 39 million Georgia expansion will add 150,000 square feet of stretch-film capacity by December 2026, closing a supply gap between Kentucky and California operations. The United States demands benefits from e-commerce parcel volumes and Southeast nearshoring, while Mexico and Canada ride USD 40 billion of announced manufacturing investments since 2024 that favor stretch-hood adoption for automotive and electronics.

Europe’s trajectory is anchored by its Packaging and Packaging Waste Regulation, which sets a 35% recycled-content requirement by 2030. Germany, the United Kingdom, France, Italy, and Spain dominate consumption thanks to mature recycling infrastructure and ambitious brand pledges. Eastern European countries attract greenfield film plants leveraging lower labor costs and proximity to manufacturing clusters. Coveris invested USD 10.5 million in Halle, Germany in 2025 to expand recyclable mono-film capacity and medical-grade production lines.

Competitive Landscape

The stretch and shrink film market is moderately concentrated, with top players such as AEP Industries Inc., Amcor plc, Sealed Air, Mondi, Sigma Plastics Group. Private-equity-backed consolidation accelerated in 2025-2026 as investors sought scale to offset feedstock volatility and finance costly downgauging technology. Sealed Air’s USD 10.3 billion acquisition by Clayton, Dubilier & Rice (a private investing fund) in February 2026 highlights the premium assigned to companies with automation service contracts and consumables annuities.

Tier-one players deploy nano-layer coextrusion and metallocene resins to capture premium margins in the ultra-thin segment, where line costs of USD 5-12 million deter many regional converters. Technology-driven majors have also equipped plants with industrial IoT sensors and high-speed vision inspection, lifting overall equipment effectiveness by more than 200 basis points. In contrast, family-owned converters relying on legacy equipment struggle to match the tight thickness tolerances needed for 12-15 µm gauges.

Circular-economy initiatives are a growing battleground. Brand owners such as Procter & Gamble are signing multiyear supply agreements to meet 25% recycled-content targets. Collaborative projects such as Revoloop, launched by Dow and RKW Group, are commercializing shrink films containing up to 100% recycled polyethylene, bypassing the contamination pitfalls of mixed-stream mechanical recycling.

Stretch And Shrink Film Industry Leaders

AEP Industries Inc.

Amcor plc

Inteplast Group

Sealed Air

Sigma Plastics Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dow and RKW Group released the first commercial run of Revoloop shrink film using 100% post-consumer recycled polyethylene for beverage multipacks.

- April 2026: Sigma Plastics Group broke ground on its USD 39 million Columbus, Georgia plant, scheduled to open in December 2026 with 48,000 tpa of stretch-film capacity focused on ultra-thin gauges.

Global Stretch And Shrink Film Market Report Scope

Stretch films (elastic, used for palletizing/load stability) and shrink films (heat-activated, used for wrapping/bundling items) are essential, distinct plastic packaging materials. Stretch film wraps around items using elastic tension. Shrink film, often polyolefin or PVC, shrinks upon heating, providing a tight, protective, and often clear, tamper-evident seal for retail.

The market is segmented by film type, material type, thickness, application, and end-user industry. By film type, the market is segmented into stretch film and shrink film. By material type, the market is segmented into linear low-density polyethylene (LLDPE), low-density polyethylene (LDPE), mLLDPE and metallocene blends, polyvinyl chloride (PVC), polyolefin (POF), and other materials (including EVOH, PLA, and recycled PE). By thickness, the market is segmented into less than or equal to 15 µm, 15–25 µm, and greater than 25 µm. By application, the market is segmented into pallet wrapping and bundling, sleeve and label packaging, tamper-evident overwraps, food and beverage packs, industrial goods protection, and other applications. By end-user industry, the market is segmented into food and beverage, pharmaceutical and healthcare, consumer electronics and appliances, industrial manufacturing, e-commerce and third-party logistics, and other end-user industries. The report also covers the market size and forecasts for stretch and shrink films in 18 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Stretch Film |

| Shrink Film |

| Linear Low-Density Polyethylene (LLDPE) |

| Low Density Polyethylene (LDPE) |

| mLLDPE and Metallocene Blends |

| Polyvinyl chloride (PVC) |

| Polyolefin (POF) |

| Other Materials (EVOH, PLA, Recycled PE) |

| Less than or Equal to 15 µm |

| 15–25 µm |

| Greater than 25 µm |

| Pallet Wrapping and Bundling |

| Sleeve and Label Packaging |

| Tamper-evident Overwraps |

| Food and Beverage Packs |

| Industrial Goods Protection |

| Other Applications |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Consumer Electronics and Appliances |

| Industrial Manufacturing |

| E-commerce and Third-Party Logistics |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Film Type | Stretch Film | |

| Shrink Film | ||

| By Material Type | Linear Low-Density Polyethylene (LLDPE) | |

| Low Density Polyethylene (LDPE) | ||

| mLLDPE and Metallocene Blends | ||

| Polyvinyl chloride (PVC) | ||

| Polyolefin (POF) | ||

| Other Materials (EVOH, PLA, Recycled PE) | ||

| By Thickness | Less than or Equal to 15 µm | |

| 15–25 µm | ||

| Greater than 25 µm | ||

| By Application | Pallet Wrapping and Bundling | |

| Sleeve and Label Packaging | ||

| Tamper-evident Overwraps | ||

| Food and Beverage Packs | ||

| Industrial Goods Protection | ||

| Other Applications | ||

| By End-user Industry | Food and Beverage | |

| Pharmaceutical and Healthcare | ||

| Consumer Electronics and Appliances | ||

| Industrial Manufacturing | ||

| E-commerce and Third-Party Logistics | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What value will the stretch and shrink film market reach by 2031?

Forecasts put the market at USD 24.74 billion by 2031, expanding from USD 18.92 billion in 2026 at a 5.51% CAGR over 2026-2031.

Which film type is expected to grow the fastest through 2031?

Shrink film is projected to rise 5.89% annually as polyolefin grades replace PVC in beverage multipacks and sleeve labels.

Why are metallocene-based resins gaining share in stretch film?

They allow 10-20% downgauging without losing puncture strength, cutting freight weight and helping converters meet 35% recycled-content rules.

How is Asia-Pacific shaping overall demand?

The region held 41.25% of 2025 revenue and is set to climb at 6.19% through 2031 thanks to new capacity in India that targets GCC and Southeast Asian export lanes.

Page last updated on: