Armor Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

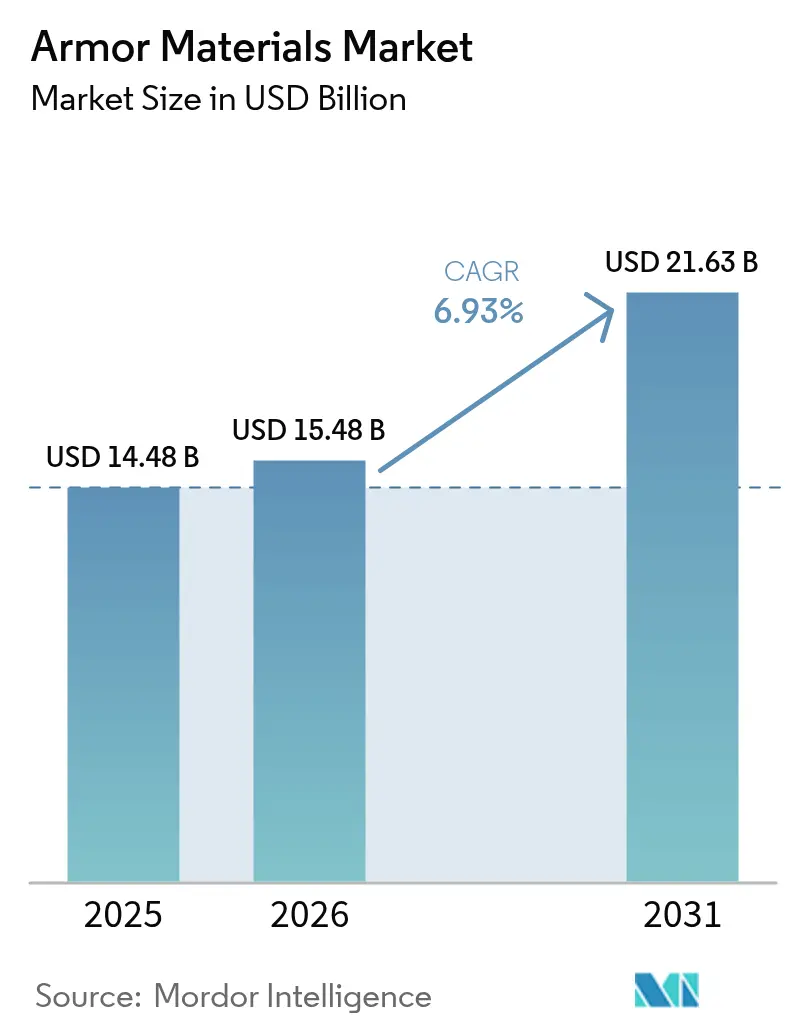

| Market Size (2026) | USD 15.48 Billion |

| Market Size (2031) | USD 21.63 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

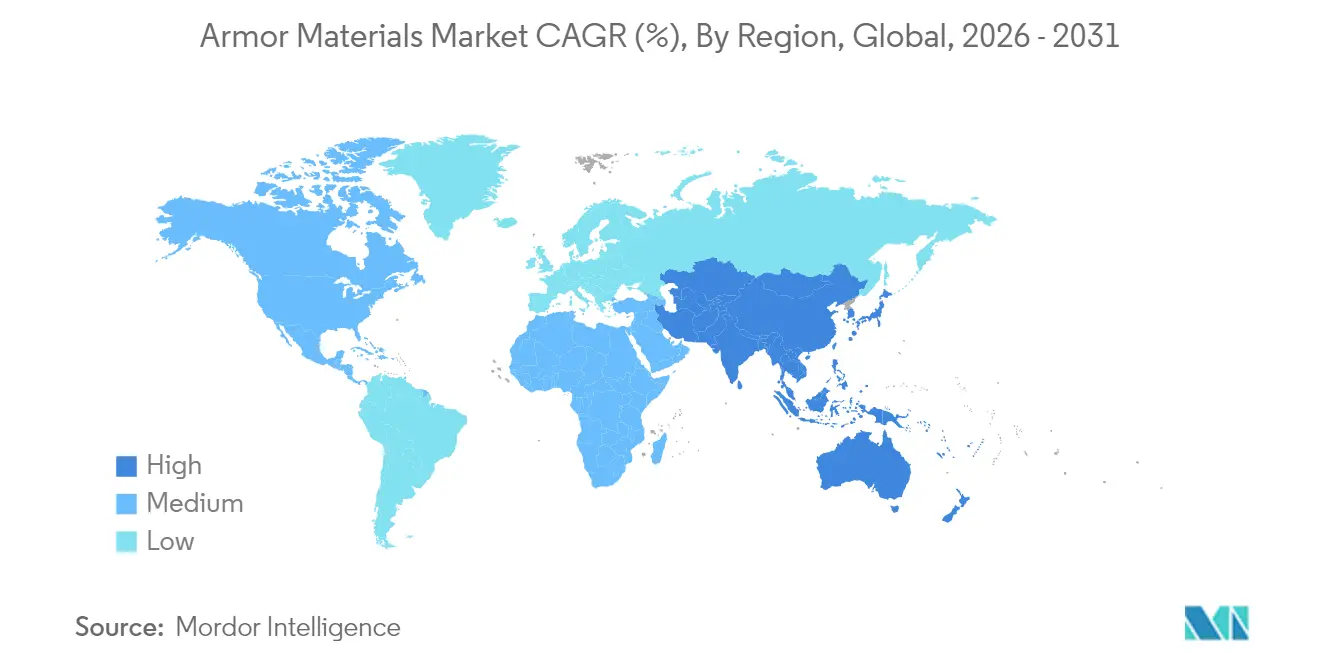

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

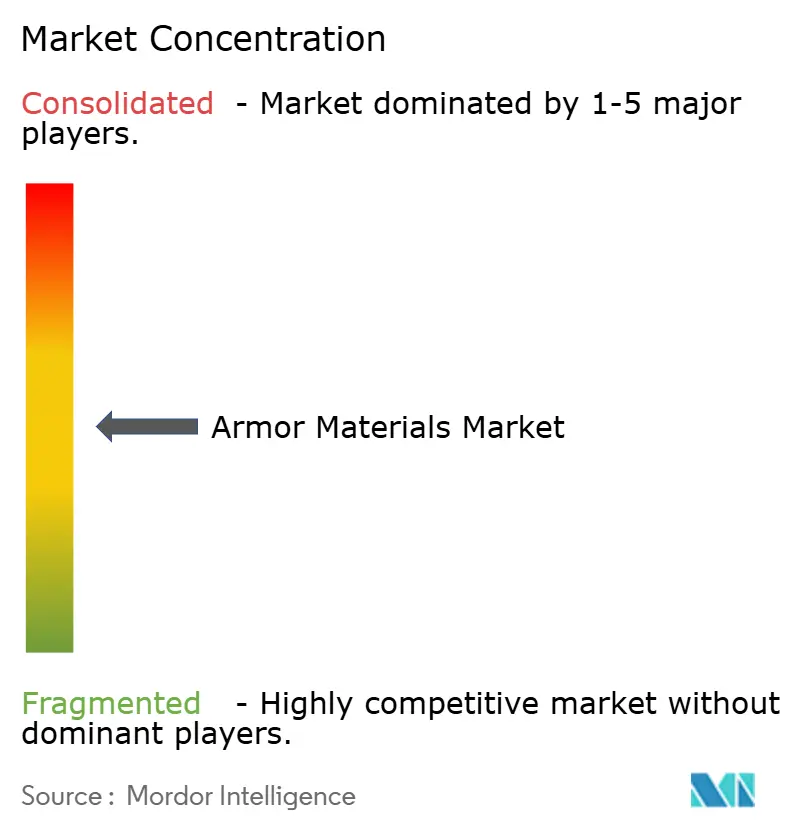

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Armor Materials Market Analysis by Mordor Intelligence

The armor materials market size is expected to grow from USD 14.48 billion in 2025 to USD 15.48 billion in 2026 and is forecast to reach USD 21.63 billion by 2031 at 6.93% CAGR over 2026-2031. Current demand is driven by higher threat levels across military, law enforcement, and critical-infrastructure settings, alongside rapid advances in ceramics, metal matrix composites, and ultra-high-molecular-weight polyethylene (UHMWPE). Faster adoption of lightweight hybrid solutions, government programs that subsidize protective gear for police officers, and accelerated naval and space programs all contribute to rising procurement budgets. Meanwhile, supply insecurity for strategic minerals such as titanium and boron carbide forces buyers to redesign material portfolios and build contingency stocks, opening niche opportunities for recyclers and secondary processors. Competitive activity is moderate; large chemical and advanced-materials companies still dominate, but start-ups that specialize in nano-enhanced ceramics are gaining traction, especially where sustainability credentials and circular-economy services matter.

Key Report Takeaways

- By product type, metal & alloys led with 51.30% revenue share in 2025, while ceramic & composite materials are projected to advance at a 7.05% CAGR to 2031.

- By application, body armor accounted for 41.40% of the armor materials market share in 2025 and is set to expand at a 7.01% CAGR through 2031.

- By end user, defense dominated with 66.20% of the armor materials market size in 2025; homeland security & law-enforcement demand is rising fastest at 7.08% CAGR to 2031.

- By geography, North America held 37.40% of 2025 revenues, whereas Asia-Pacific is the fastest-growing region at a 7.20% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Armor Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development of body armor and advanced weapons | +0.19% | Global, with concentration in North America and Europe | Medium term (3-4 yrs) |

| Increasing homeland security concerns | +0.14% | Global, particularly in North America, Europe, and Asia-Pacific | Short term (≤ 2 yrs) |

| Rising incidence of asymmetric warfare & IED threats elevating demand for blast-resistant vehicle armor | +0.23% | Middle East, Africa, Asia-Pacific, with spillover to global markets | Medium term (3-4 yrs) |

| Expansion of commercial spaceflight & near-space tourism requiring micrometeoroid-shielding materials | +0.12% | North America, Europe, with emerging interest in China and UAE | Long term (≥ 5 yrs) |

| Accelerated modernization of naval fleets driving need for corrosion-resistant armor steels | +0.17% | Asia-Pacific, North America, Europe | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Development of body armor & advanced weapons

Angel Armor’s 2024 Truth SNAP plate system demonstrated how magnetic couplings deliver modularity while plates as light as 0.65 lb keep operators agile. Hybrid lay-ups such as UHMWPE/carbon-fiber reinforced plastic (CFRP) now achieve 28% lower back-face deformation than legacy laminates, proving that multi-material stacks can equal Level IV protection at lower mass. Field trials confirm that ceramic-UHMWPE hybrids survive multiple hits, while aluminum–titanium-carbide metal-matrix composites boost ballistic-limit velocity by 30% versus rolled homogeneous armor. These innovations increase the performance ceiling of the armor materials market and push procurement toward lighter configurations without sacrificing survivability.

Increasing homeland-security concerns

Federal and state funding flows directly to local agencies. The FBI Legacy Body Armor Program has already transferred nearly USD 700,000 in plates and vests to small departments where 41% of officers previously had no mandatory-wear policy. The U.S. Department of Homeland Security is requesting USD 107.4 billion for FY 2025, including grants that earmark USD 1.008 billion for protective equipment upgrades[1]U.S. Department of Homeland Security, “Future Years Homeland Security Program Fiscal Years 2025-2029 Executive Summary,” dhs.gov . Similar schemes in Europe and parts of Asia accelerate purchase cycles and sustain volume growth for the armor materials market.

Rising incidence of asymmetric warfare & IED threats

Vehicle builders are adopting four-layer armor stacks that combine Ti-6Al-4V skins, titanium-carbide reinforced metal-matrix cores, and energy-absorbing porous layers. In ballistic tests against 7.62 mm AP rounds, these systems absorbed the projectile’s kinetic energy while keeping areal density to 2.82 g/cm³, relevant for mine-resistant vehicles that must meet stringent weight ceilings. Strong demand from Middle Eastern and African defense ministries propels the armor materials market in blast-protection niches.

Accelerated Modernization of Naval Fleets

Global naval modernization programs are driving increased demand for specialized marine armor materials. The U.S. Navy's FY 2025 budget allocates USD 32.38 billion for shipbuilding and conversion, with significant funding directed toward the COLUMBIA Class submarines and Arleigh Burke-class destroyers. This investment highlights the growing importance of advanced armor materials in naval operations.

Recent advancements in marine armor technology include the development of hexagonal boron nitride (hBN) coatings. These coatings, applied to stainless steel and other metal alloys, significantly enhance durability, reduce friction, and improve resistance to corrosion and high-temperature oxidation. Such innovations are particularly critical in naval applications, where corrosion resistance is as vital as ballistic protection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile titanium & boron-carbide feedstock prices inflating production costs | -0.21% | Global, with severe impact in Europe and North America | Short term (≤ 2 yrs) |

| Stringent export-control regulations limiting cross-border technology transfer | -0.18% | Global, particularly affecting emerging markets | Medium term (3-4 yrs) |

| Recycling & end-of-life challenges for composite armor materials | -0.15% | Europe, North America, with growing concern in Asia-Pacific | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Volatile titanium & boron-carbide feedstock prices

The 2025 U.S. Geological Survey summaries note frequent spot-price swings for strategic metals, including titanium sponge, caused by concentrated supply in a handful of producers[2]U.S. Geological Survey, “Mineral Commodity Summaries 2025,” usgs.gov . Meanwhile, GAO data show that the Department of Defense recorded 99 material shortfalls, a 167% jump versus 2019, with boron-carbide repeatedly flagged as “single-source”. As suppliers impose surcharges, armor makers wrestle with cost-plus contracts that seldom adjust quickly, eroding margins across the armor materials market.

Stringent export-control regulations

ITAR revisions (January 2025) lock down cross-border transfers of ballistic-grade fibers and ceramics. Parallel frameworks in the UK and the EU require licenses even for dual-use abrasion-resistant panels. Compliance costs raise barriers for new entrants from emerging economies and can delay joint-development programs by several quarters, curbing the armor materials market’s speed of international rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceramic & Composite Materials Gain Ground on Metals

Metals and alloys retained 51.30% of sales in 2025, yet ceramic & composite lines are pacing the overall armor materials market at a 7.05% CAGR. Silicon-carbide tiles now deliver like-for-like ballistic resistance at densities below 3.2 g/cm³, trimming war-fighter loadouts by several kilograms per torso kit. Study results on staggered half-lap joint designs confirm that optimized ceramic shapes yield full compliance with U.S. military protocols at lower thickness. Consequently, procurement agencies recalibrate specifications toward lighter plates, a trend that reshapes supplier mix within the armor materials market.

Structural ceramics partner well with UHMWPE backings, producing multi-hit capability gains of 35%. Parallel research into Kevlar/UHMWPE laminates using Elium thermoplastic resin recorded 25% higher energy absorption and a 22.44% weight reduction, helping law-enforcement agencies extend patrol duration without fatigue penalties. Growth in para-aramid fiber adoption remains steady, but UHMWPE fibers now post the fastest uptake due to superior tensile strength and improved thermal aging properties. Together, these dynamics shift investment from traditional steel to hybrid stacks, cementing the armor materials market’s pivot toward advanced composites.

By Application: Body Armor Advances, Vehicle Protection Evolves

The armor materials market size for body armor retained 41.40% of sales in 2025 and is on track for a 7.01% CAGR, buoyed by individual-protection mandates and new NIJ Standard 0101.07 test regimes. Products like the ExoM exoskeleton redistribute 70% of the carried load while stopping 7.62 mm rounds, proving that ergonomic gains and ballistic capability can coexist. Female-specific panel geometry, driven by the revised NIJ threat levels, opens an underserved customer cohort, and incremental sales flow directly into the armor materials market.

Nano-reinforced aluminum-nickel-phosphorus bronze matrices, infused with titanium carbonitride and yttria, slash mass by up to 45% relative to rolled homogeneous armor while complying with NATO STANAG blast benchmarks. Adoption in mine-resistant ambush-protected (MRAP) fleets demonstrates how lighter systems unlock payload, range, and modular sensor kits. The armor materials market share for aerospace applications stays small but moves swiftly as commercial spaceflight accelerates. Micrometeoroid shield demand grows around reusable capsules, where impedance-graded Ti/Al bumpers arrest particle clouds and cut repair cycles between missions.

By End User: Defense Dominant, Homeland Security Rising

Defense procurement comprised 66.20% of the armor materials market size in 2025. The U.S. FY 2025 defense request allocates USD 849.8 billion, with explicit funds for advanced materials, keeping front-line demand steady. Similar modernization programs in Japan, India, and Australia accelerate composite-armor adoption, particularly for next-generation destroyers and infantry fighting vehicles.

Homeland security & law-enforcement orders rise at a 7.08% CAGR as urban agencies refresh ballistic vests and tactical shields. Eligibility for DHS grants accelerates turnover cycles from seven to four years, which significantly enlarges lifetime volumes flowing into the armor materials market. Civil & commercial buyers—spanning private security, construction blasting crews, and high-risk logistics—remain niche but steady, often preferring modular plate carriers that can upgrade to Level III+ when threat levels rise.

Geography Analysis

North America captured 37.40% of 2025 revenue, anchored by the U.S. defense budget and vigorous R&D. Ongoing Air Force Research Laboratory programs funnel breakthroughs in high-entropy alloys and nano-engineered ceramics straight into production, shortening technology-transition timelines. Federal Buy-American statutes further insulate regional suppliers and stabilize the armor materials market.

Asia-Pacific is the fastest-growing cluster at a 7.20% CAGR. China funnels substantial resources into indigenous silicon-carbide sintering, while India’s DRDO advances fiber-reinforced polymer composites tailored for hot climates. Parallel naval procurement in South Korea and Australia boosts demand for corrosion-resistant armor steels and composite bow inserts, broadening the regional customer base.

Europe grapples with strategic-mineral access. The EU Critical Raw Materials Act targets 40% domestic processing and 15% recycling rates by 2030, prompting fresh investment in boron-carbide recovery and titanium-scrap upgrading. Cross-border collaboration under the Permanent Structured Cooperation (PESCO) framework accelerates next-generation helmet programs, keeping the armor materials market innovative despite tight budgets.

The Middle East and Africa record mid-single-digit growth. Procurement centers on counter-IED vehicle kits and perimeter fortifications for energy installations. Nations such as the UAE also fund micrometeoroid shielding research for planned near-space tourism, extending the armor materials market into emergent aerospace domains.

Competitive Landscape

Established multinationals retain scale advantages, but innovation has tilted toward agile specialists. DuPont uses its Kevlar EXO platform to cut felt-package thickness by 30% while maintaining legacy stopping power; the firm also reports a 58% reduction in Scope 1 & 2 emissions between 2019 and 2024. Morgan Advanced Materials posted GBP 1.10 billion in 2024 revenue and reinvests 8.7% of sales in capacity for reaction-bonded silicon-carbide tiles, underscoring the long-term margin potential of premium armor ceramics.

SINTX Technologies acquired boron-carbide assets to accelerate commercial sales of 100% B4C plates, illustrating how focused IP positions carve profitable niches. On the metals side, Norsk Titanium pushes plasma-arc deposition of Ti-6Al-4V armor nodes, achieving near-net shapes that lower machining scrap by 30%. Collaboration structures dominate: prime contractors bundle chemistry experts with robotics firms to meet sustainability mandates and ITAR compliance. As a result, the armor materials market rewards enterprises that mesh R&D vigor, domestic production, and end-of-life services.

Regulatory levers also shape rivalry. The U.S. FY 2024 National Defense Authorization Act encourages multiyear sourcing of domestically processed critical minerals, favoring vertically integrated producers. European exporters, conversely, focus on downstream recycling to meet stricter extended-producer-responsibility rules. Across all regions, corporate positioning now hinges on the capacity to deliver validated, lightweight systems and credible recycling pathways.

Armor Materials Industry Leaders

3M

BAE Systems

CeramTec GmbH

DuPont

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DSM firmenich (Avient) introduced Dyneema HB330/332, its third-generation UHMWPE sheets, which enable weight reductions of up to 45% in hard inserts, helmets, and vehicle appliqué panels. This innovation is expected to drive advancements in the armor materials market.

- January 2025: CPS Technologies won a Phase I SBIR contract from the U.S. Army to design ultra-low-temperature sintered ceramic armor that maintains high compressive strength while trimming thermal budgets in production.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the armor materials market as the value of newly produced metals, ceramics, composites, aramid fibers, ultra-high-molecular-weight polyethylene, fiberglass, and other engineered formulations that are purposely designed, certified, and supplied for ballistic, blast, or stab protection across body, vehicle, aerospace, marine, and civil platforms worldwide.

Scope exclusion: aftermarket repair kits and recycled scrap are left outside the valuation.

Segmentation Overview

- By Product Type

- Metal and Alloy

- Ceramic and Composite

- Para-aramid Fiber

- Ultra-high-molecular-weight Polyethylene (UHMWPE)

- Other Product Types (e.g., fiberglass, carbon, nano-enhanced)

- By Application

- Body Armor

- Vehicle Armor

- Aerospace

- Marine Armor

- Civil Armor

- By End User

- Defense

- Homeland Security and Law‐Enforcement

- Civil and Commercial

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and short surveys are run with armor-plate fabricators, ballistic-lab managers, procurement officers, and frontline users across North America, Europe, Asia-Pacific, and the Middle East.

Their firsthand views help us validate cost pass-throughs, adoption rates of hybrid ceramic-UHMWPE panels, and typical replacement intervals, which in turn refine assumption ranges inside our model.

Desk Research

Mordor analysts start with open data streams such as SIPRI defense-spending tables, UN Comtrade shipment codes for HS-class 6811 and 7326, United States NIJ ballistic standards, European Defence Agency procurement statistics, and patent families retrieved through Questel.

Company filings, investor decks, and respected trade journals complement those baselines, while D&B Hoovers and Dow Jones Factiva provide cost curves and deal activity.

The public sources cited above are illustrative only and do not exhaust the full set of documents screened during desk work.

Market-Sizing & Forecasting

A top-down build begins with country-level defense and homeland-security spending, which is then linked to armor budget share and historical penetration into individual soldier, vehicle, and airframe programs.

Select bottom-up checks, supplier revenue roll-ups, and sampled average selling price multiplied by unit demand provide reality tests before final calibration.

Key variables tracked include titanium and boron-carbide prices, troop modernization counts, rotorcraft deliveries, police officer population, and weight-saving targets specified in open tenders.

A multivariate regression blended with scenario analysis projects how those drivers influence demand out to 2030.

Missing datapoints are bridged with region-specific proxy indicators that have been stress-tested through earlier cycles.

Data Validation & Update Cycle

Outputs pass two rounds of analyst peer review, automated anomaly flags, and senior sign-off.

We refresh every twelve months and issue mid-cycle amendments when material contract awards, regulatory shifts, or raw-material price spikes alter baseline logic.

Why Mordor's Armor Materials Baseline Inspires Confidence

Published values often diverge because research houses choose different scope boundaries, currency conversions, refresh cadences, and risk scenarios.

Key gap drivers here include whether aftermarket refurbishment is counted, how aggressively future composite adoption is assumed, and the year used for currency normalization.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.48 B | Mordor Intelligence | - |

| USD 13.68 B | Global Consultancy A | Omits UHMWPE and fiberglass; uses defense spend only, ignoring civil armor demand |

| USD 17.43 B | Regional Consultancy B | Adds retrofit and repair services, inflating base year; mixes 2024 and 2025 exchange rates |

| USD 13.14 B | Research Boutique C | Focuses mainly on body armor; applies uniform price inflation without material-specific indices |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual-path validation, and annual refresh deliver a balanced, transparent baseline that decision-makers can replicate with publicly traceable inputs.

Key Questions Answered in the Report

What is the current size of the armor materials market?

The market stood at USD 15.48 billion in 2026 and is projected to reach USD 21.63 billion by 2031.

Which segment grows fastest within the armor materials market?

Ceramic & composite products are expanding at a 7.05% CAGR, outpacing metals and polymers.

Why is Asia-Pacific the fastest-growing region?

Defense modernization, rising homeland-security budgets, and local R&D into lightweight composites give Asia-Pacific a 7.20% CAGR to 2031.

How do supply-chain risks affect prices?

Limited sources for titanium and boron carbide lead to price swings that shave 0.21 percentage points off the forecast CAGR.

What standards govern new body armor products?

NIJ Standard 0101.07, released in late 2024, introduces updated threat levels and testing protocols that all U.S. law-enforcement plates must meet.

Are recycling solutions available for composite armor?

Early-stage chemical processes can now recover some fibers and resins, but large-scale recycling remains in development, prompting manufacturers to design for easier disassembly.

Page last updated on: