Lightweight Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

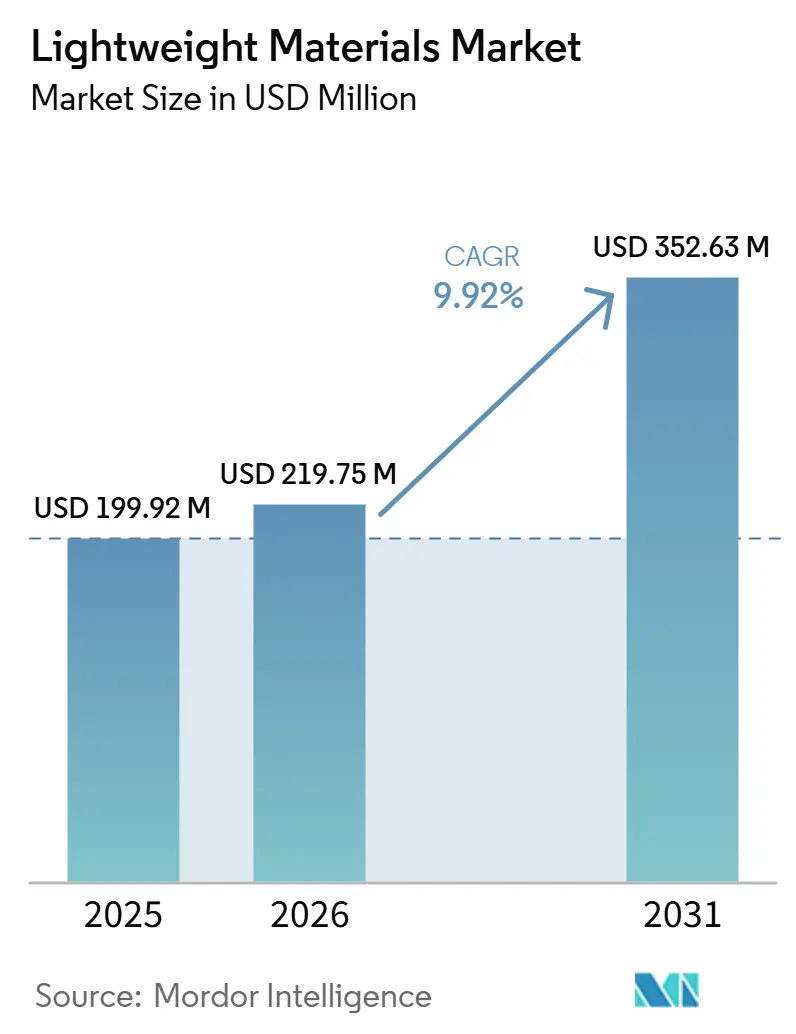

| Market Size (2026) | USD 219.75 Million |

| Market Size (2031) | USD 352.63 Million |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lightweight Materials Market Analysis by Mordor Intelligence

The Lightweight Materials Market size was valued at USD 199.92 million in 2025 and is estimated to grow from USD 219.75 million in 2026 to reach USD 352.63 million by 2031, at a CAGR of 9.92% during the forecast period (2026-2031). Amid increasing cost, regulatory, and performance pressures, automakers, energy developers, and aerospace companies are working to reduce unnecessary weight from their vehicles, infrastructures, and launch systems. The European Union’s Carbon Border Adjustment Mechanism (CBAM) and similar embedded-carbon tariffs provide low-carbon aluminum and steel with a 15-25% cost advantage, driving the adoption of lightweight alloys. China's 2025 action plan mandates magnesium wheels, motor housings, and structural castings in new-energy vehicles (NEVs), with an expected demand increase of 120,000 tons annually by 2028. Hydrogen infrastructure developers are adopting carbon-fiber-reinforced polymer (CFRP) tanks to meet strict weight requirements, while reusable launch economics benefit from every kilogram reduced in second-stage structures. These trends position the lightweight materials market as a key component in multi-sector decarbonization initiatives over the next decade.

Key Report Takeaways

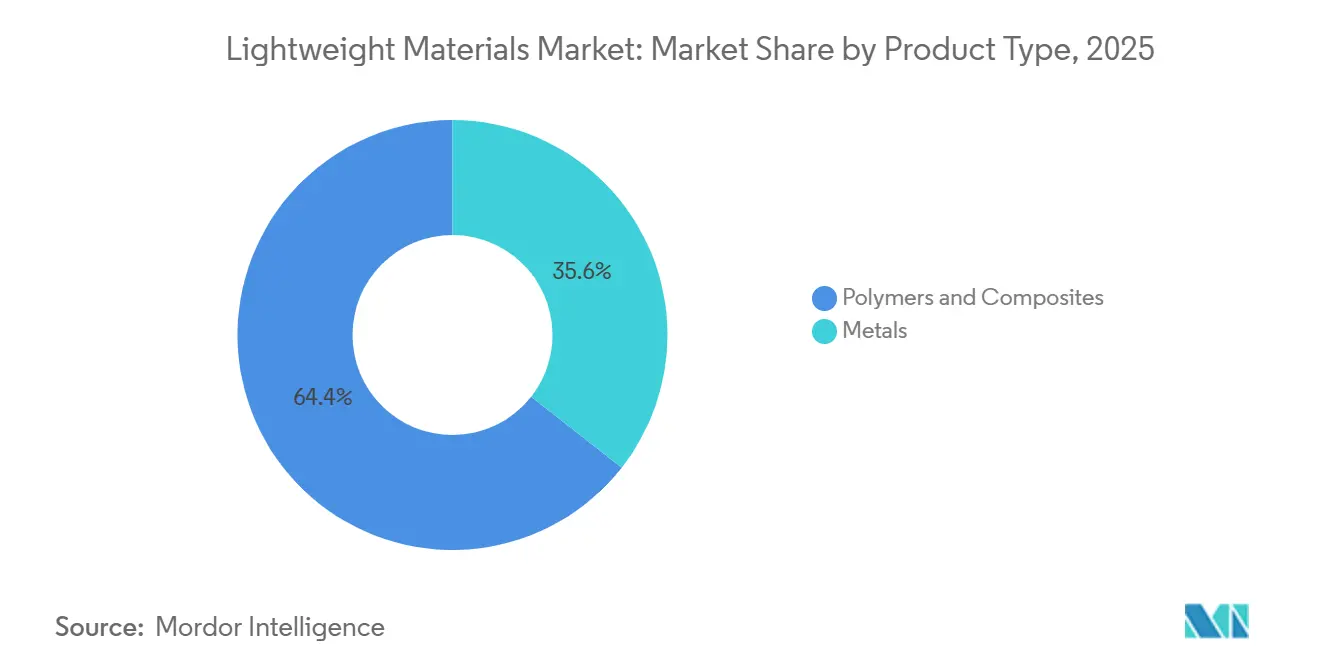

- By product type, polymers and composites led with 64.42% of the lightweight materials market share in 2025; metals are projected to expand at a 9.28% CAGR through 2031.

- By manufacturing process, extrusion and rolling accounted for 30.78% of the lightweight materials market size in 2025, while additive manufacturing posted the fastest projected 9.67% CAGR to 2031.

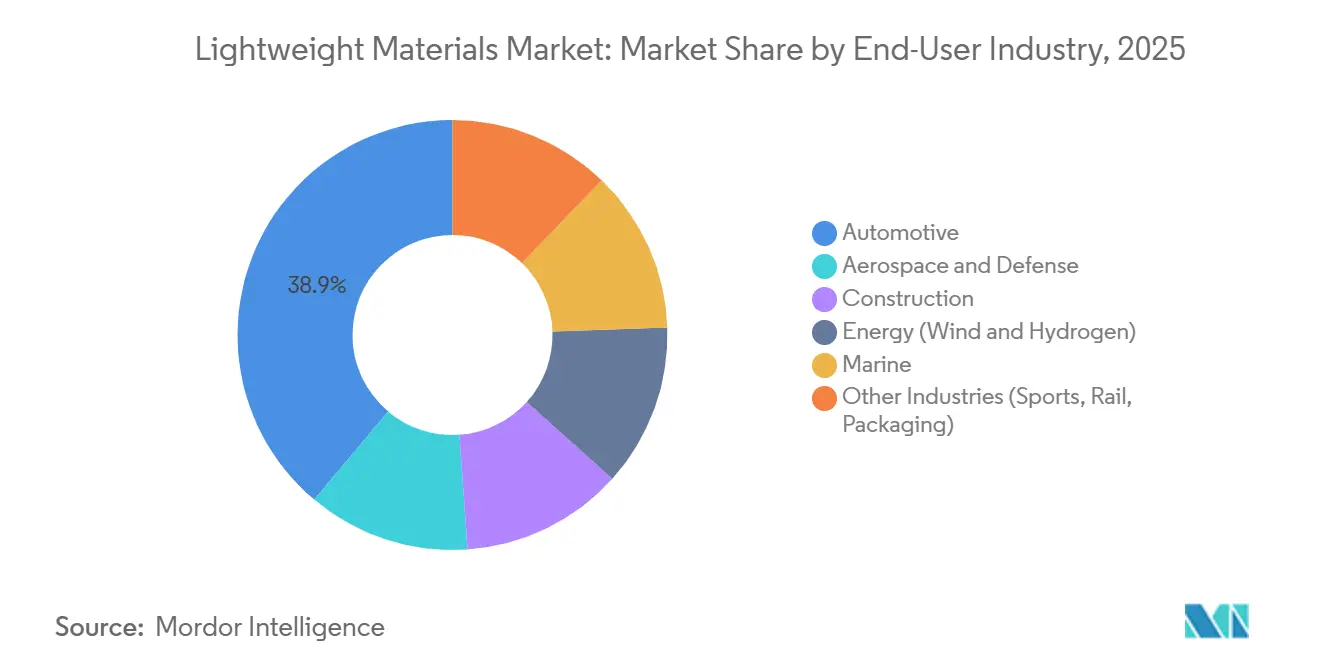

- By end-user industry, automotive held 38.88% of 2025 revenue; the energy segment is forecast to expand at a 9.81% CAGR through 2031.

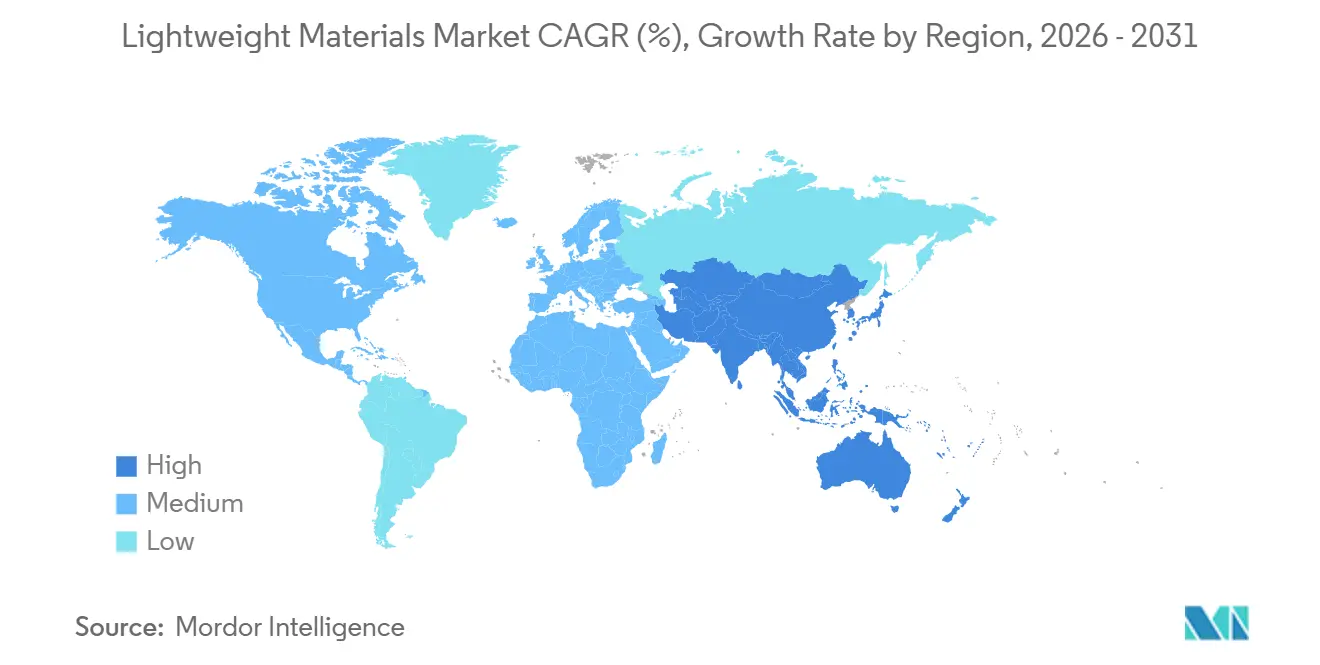

- By geography, Asia-Pacific captured 41.12% lightweight materials market share in 2025 and is tracking the highest 9.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lightweight Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global CO₂ / fuel-economy regulations | +2.8% | Global, with EU and China leading enforcement | Medium term (2-4 years) |

| Hydrogen storage and distribution weight limits | +1.6% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Rapid aerospace and reusable-launch adoption | +1.9% | North America, Europe, China | Medium term (2-4 years) |

| AI-driven generative-design mass optimization | +1.4% | Global, concentrated in automotive and aerospace hubs | Short term (≤ 2 years) |

| Carbon border-adjustment incentives for low-embodied-carbon metals | +2.2% | EU primary, spillover to ASEAN and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Global CO₂ and Fuel-Economy Regulations

Fleet-average carbon ceilings set by the European Union (EU), China, and the United States (U.S.) are prompting automakers to reduce 100-150 kilograms (kg) from every new platform[1]European Commission, “Circular Economy Action Plan,” EUROPA.EU. The EU imposes penalties of EUR 95 for each gram of excess CO₂ per car. As a result, lightweight closures, subframes, and seat structures have become essential compliance measures. China's updated dual-credit scheme provides bonus credits for New Energy Vehicles (NEVs) consuming below 11 kilowatt-hours (kWh)/100 kilometers (km), a target that is challenging to meet without aluminum body-in-white and magnesium interior castings. The U.S. Environmental Protection Agency's (EPA) 2024 directive for model years 2027-2032 targets a 56% reduction in fleet-wide CO₂ emissions from 2026 levels. This regulation is driving Original Equipment Manufacturers (OEMs) to adopt high-strength aluminum and Carbon Fiber Reinforced Polymer (CFRP) to offset battery mass. Consequently, the lightweight materials market is positioned at the intersection of vehicle design and regulatory compliance.

Hydrogen Storage and Distribution Weight Limits

The Department of Energy (DOE) mandates that light-duty fuel-cell vehicles must store 5.5 weight percent (wt%) hydrogen at 700 bar. This performance is achievable only with Type IV CFRP vessels, which weigh between 90 and 110 kg for a 5 kg hydrogen payload[2]U.S. Department of Energy, “Wind Energy Research and Development,” ENERGY.GOV. Heavy-duty trucks face similar requirements: Nikola's eight-tank module carries 70 kg of hydrogen while keeping the total assembly mass under 500 kg, ensuring compliance with U.S. axle-weight limits. Japan has allocated USD 250 million in 2025 subsidies for hydrogen stations, each requiring 15-20 storage modules. This initiative is expected to increase domestic carbon-fiber demand by 8,000 tons annually. The structural demand for CFRP tanks provides a stable foundation for the lightweight materials market, independent of fluctuations in the aerospace or automotive industries.

Rapid Aerospace and Reusable-Launch Adoption

Organizations such as SpaceX, Blue Origin, and national programs are adopting mass-optimized composites and titanium to enhance payload and fuel efficiency. Blue Origin's 7-meter (m) carbon-composite fairing reduces weight by 2.3 tons compared to an aluminum counterpart, directly increasing customer payload capacity. In civil aviation, Boeing's 787 and Airbus's A350 families incorporate 50-53% composites by weight. This reduces structural mass by approximately 20% and improves fuel efficiency by 20-25% per seat-mile. These efficiencies translate into significant operating-cost reductions for carriers, particularly amid high jet-fuel prices. These advancements ensure the lightweight materials market remains closely aligned with increasing commercial build rates.

AI-Driven Generative-Design Mass Optimization

Advancements in generative-design software enable engineers to evaluate thousands of load cases within hours. This process can reduce component mass by up to 60%, achieving geometries that are not feasible with traditional machining. For example, a General Motors seat bracket redesigned in Autodesk Fusion 360 reduced its weight from 3.4 kg to 1.4 kg and is now in low-volume production using selective-laser-melted Aluminum Silicon 10 Magnesium (AlSi10Mg). Similarly, Airbus achieved a 40% weight reduction and a 30% decrease in part count for a titanium engine-pylon fitting optimized through Siemens NX. These AI-driven efficiencies are accelerating the adoption of additive manufacturing and expanding the lightweight materials market's potential.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-intensive extraction and processing routes | -1.8% | Global, acute in coal-dependent regions (China, India, Middle East) | Medium term (2-4 years) |

| Mixed-material end-of-life separation hurdles | -1.2% | Europe and North America leading regulatory pressure | Long term (≥ 4 years) |

| Joining incompatibilities in giga-cast multi-material BIW | -0.9% | Automotive hubs (Germany, China, U.S., Japan) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Intensive Extraction and Processing

Primary aluminum smelting consumes 15-16 MWh per ton and is subject to electricity cost fluctuations. This was demonstrated in 2023 when European power price increases led to 800 kilotons of capacity being taken offline. Producing carbon fiber requires 80-110 MWh per ton during precursor oxidation and carbonization. The Kroll process for titanium production demands 60-80 MWh per ton and generates magnesium-chloride waste. High power requirements increase costs and scope-1 carbon emissions, potentially impacting the lightweight materials market unless technologies like inert-anode aluminum (ELYSIS) and electrified titanium processes achieve large-scale commercialization.

Mixed-Material End-of-Life Separation Hurdles

In Europe, wind-turbine blades weighing 40,000-50,000 tons retire annually. These blades, made with thermoset epoxy, are resistant to mechanical recycling. As a result, fewer than 10% of these blades enter recovery streams because the energy costs of pyrolysis exceed the market value of reclaimed fiber. The European Union's (EU) updated End-of-Life Vehicles Directive requires 95% recovery by weight and 85% closed-loop recycling by 2028. This creates challenges for platforms that combine aluminum giga-castings, carbon fiber-reinforced polymer (CFRP) panels, and steel subframes. Without scalable recycling solutions, the lightweight materials market may face increasing waste-management costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Composites Lead, Metals Accelerate on Electrification

In 2025, carbon-fiber-reinforced and glass-fiber-reinforced polymers accounted for 64.42% of the revenue, supported by a 1.2 million tons annual demand for wind blades and a near-recovery of Boeing 787 and Airbus A350 production rates to pre-pandemic levels. Glass fiber remains prevalent in cost-sensitive construction, while high-temperature polymers like polyether ether ketone (PEEK) and polyetherimide (PEI) are gaining traction in battery housings and electric motor insulators, particularly where flame-smoke toxicity regulations exclude metals. The market for composite lightweight materials is expected to grow further, driven by thermoplastic tapes enabling 3-4 minute cycle times suitable for automotive lift gates.

Metals are projected to grow at a 9.28% compound annual growth rate (CAGR) through 2031, driven by aluminum giga-casting, China's magnesium mandate, and advancements in titanium additive manufacturing. Closed-loop aluminum, with 90% recycled content and a carbon dioxide (CO₂) footprint of 2.3 tons CO₂/ton, complies with Carbon Border Adjustment Mechanism (CBAM) thresholds, enabling original equipment manufacturers (OEMs) to label products as near-carbon-neutral. The market share for magnesium in lightweight materials is expected to increase as corrosion-resistant plasma-electrolytic-oxidation coatings become more cost-effective, potentially dropping below USD 8/kg. Titanium remains specialized, but Norsk Titanium's rapid-plasma-deposition technology reduces buy-to-fly ratios from 10-20% to under 2%, lowering aerospace alloy costs by 30-40%.

By Manufacturing Process: Additive Gains, Extrusion Holds Volume

Extrusion and rolling contributed 30.78% of the 2025 demand, reflecting low conversion costs and 10-15 second sheet-forming cycle times that align with automotive production requirements. Novelis, with a global rolling capacity of 4.2 million tons, has secured multi-year contracts with Ford and General Motors (GM) for 5000 and 6000 series closures, while hydroforming offers an additional 20-30% weight reduction at a premium cost.

Additive manufacturing, currently holding a mid-single-digit market share, is forecast to grow at a 9.67% CAGR. General Electric's (GE) LEAP engine demonstrates its potential, featuring 19 printed fuel nozzles that consolidate 20 brazed parts, achieving a 25% weight reduction. Companies such as Desktop Metal, Velo3D, and Markforged are scaling binder-jetting and laser-powder-bed rates by 10-20 times, making components like door panels, seat anchors, and battery-tray brackets cost-competitive for printing at under USD 150/kg. As machines surpass the 100-kg/hour threshold, the adoption of additive methods in the lightweight materials market is expected to expand beyond aerospace into short-run automotive platforms.

By End-User Industry: Energy Outpaces Automotive

The automotive sector accounted for 38.88% of the market in 2025, but its growth is anticipated to slow to single digits. This is primarily due to aluminum body-in-white penetration stabilizing at 25-30% of global builds and magnesium remaining below 5% due to fire-safety and salt-spray challenges. In contrast, the energy sector is projected to grow at a 9.81% CAGR through 2031. Offshore turbines, now averaging 12-15 megawatts (MW), require 80-100 meter blades that combine carbon spars with glass skins, achieving a 15-20% mass reduction and lowering nacelle loads by one-fifth. Additionally, hydrogen mobility is incorporating 25-30 kilograms (kg) of carbon fiber per passenger car and up to 200 kg for heavy trucks. As a result, the lightweight materials market is expected to grow in tandem with offshore wind and hydrogen fleet developments.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.12% of the lightweight materials market. Projections indicate this share will grow at a 9.77% compound annual growth rate (CAGR), extending to 2031. China's eight-ministry magnesium initiative is expected to increase domestic automotive demand by 5.3 times, reaching 80,000 tons by 2028. In Japan, subsidies for hydrogen refueling stations are anticipated to raise carbon-fiber precursor capacity by 8,000 tons annually. South Korea's KRW 450 billion (USD 0.29 billion) joint venture between Toray and SK is set to produce 3,000 tons of carbon fiber, catering to aerospace and fuel-cell vehicles.

Europe contributes significantly to global demand. In 2025, German original equipment manufacturers (OEMs) consumed nearly 200 kilotons of aluminum sheets. Looking ahead, ArcelorMittal's hydrogen-driven direct reduced iron (DRI) line in Dunkirk is projected to supply 1.5 million tons of low-carbon steel for European electric vehicle (EV) battery enclosures starting in 2026. However, Brexit-induced customs frictions have shifted 15% of the United Kingdom's (UK) composite wing production to continental plants, highlighting the industry's sensitivity to policy changes.

North America is experiencing steady growth, supported by Novelis's 600 kiloton recycling expansion in Kentucky and Tesla's adoption of giga-casting at its Monterrey and Austin facilities. While Canada's composite fuselage sector is facing challenges due to declining business-jet volumes, the decrease is largely offset by demand for United States (U.S.) launch vehicles. Mexico is benefiting from Tier-1 relocations aligning with the United States-Mexico-Canada Agreement (USMCA) rules-of-origin requirements for battery supply chains, enhancing the region's share in the lightweight materials market.

Competitive Landscape

The lightweight materials market is lowly fragmented. With a combined share of approximately 35-40%, the top 10 suppliers create a balanced landscape in the lightweight materials market, blending large-scale players with regional specialists. Toray, Hexcel, Mitsubishi Chemical, and SGL Carbon command nearly 70% of the capacity for aerospace-grade carbon fiber. SGL’s recycled fiber achieves a recovery of 80-85% of virgin strength and reduces costs by 40%. This development facilitates carbon fiber-reinforced polymer (CFRP) integration into automotive lift gates and wind-blade spars, priced at USD 10-12 per kilogram. In the aluminum segment, Novelis and Constellium lead in closed-loop sheets, while Alcoa and Rio Tinto advance inert-anode smelting through their ELYSIS joint venture.

Strategically, vertical integration enhances margins. For example, Toray's operations span precursor, fiber, and prepreg lines. In contrast, specialists like Hexcel focus on aerospace prepregs, avoiding exposure to commodity market cycles. Companies such as Covestro in thermoplastic composites and Desktop Metal, along with Velo3D in high-throughput metal additive manufacturing, are introducing innovations aimed at reducing cycle times, making products suitable for automotive applications. Additionally, blockchain traceability pilots with Airbus are streamlining material qualification timelines to 9-12 months, offering a competitive advantage in securing next-generation fuselage contracts.

Lightweight Materials Industry Leaders

Novelis Inc.

ARCELORMITTAL

TORAY INDUSTRIES, INC.

Alcoa Corporation

Hexcel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SGL Carbon received the German Sustainability Award for developing a recycled carbon-fiber process that retains 80-85% of its original strength. The company plans to scale this process to a production capacity of 2,000 tons by 2027. This advancement aligns with the growing demand for lightweight materials in various industries, including automotive and aerospace, where reducing weight without compromising strength is critical.

- January 2025: Gestamp inaugurated a USD 45 million hot-stamping facility in Tennessee, manufacturing 1,500 MPa (megapascal) battery enclosures. These enclosures reduce weight by 25% compared to mild steel, aligning with the growing demand for lightweight materials in the automotive industry.

Global Lightweight Materials Market Report Scope

Lightweight materials are substances designed to have a lower density compared to traditional materials, such as steel or cast iron, while maintaining or improving their strength, durability, and overall performance.

The lightweight materials market is segmented by product type, manufacturing process, end-user industry, and geography. By product type, the market is segmented into polymers and composites, and metals. By manufacturing process, the market is segmented into extrusion and rolling, additive manufacturing, resin transfer molding, hot stamping, and hydroforming. By end-user industry, the market is segmented into automotive, aerospace and defense, construction, energy (wind and hydrogen), marine, and other industries (sports, rail, and packaging). The report also covers the market size and forecasts for the lightweight materials in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Polymers and Composites | CFRP |

| GFRP | |

| Thermoplastic Composites | |

| High-performance Polymers (PEEK, PEI) | |

| Metals | Aluminium |

| Magnesium | |

| Titanium | |

| High-strength Steel |

| Extrusion / Rolling |

| Additive Manufacturing |

| Resin Transfer Molding |

| Hot Stamping and Hydroforming |

| Automotive |

| Aerospace and Defense |

| Construction |

| Energy (Wind, Hydrogen) |

| Marine |

| Other Industries (Sports, Rail, Packaging) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Mexico | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Polymers and Composites | CFRP |

| GFRP | ||

| Thermoplastic Composites | ||

| High-performance Polymers (PEEK, PEI) | ||

| Metals | Aluminium | |

| Magnesium | ||

| Titanium | ||

| High-strength Steel | ||

| By Manufacturing Process | Extrusion / Rolling | |

| Additive Manufacturing | ||

| Resin Transfer Molding | ||

| Hot Stamping and Hydroforming | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Construction | ||

| Energy (Wind, Hydrogen) | ||

| Marine | ||

| Other Industries (Sports, Rail, Packaging) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Mexico | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the lightweight materials market by 2031?

It is forecast to reach USD 352.63 million by 2031, reflecting a 9.92% CAGR from 2026 to 2031.

Which region will see the fastest growth in lightweight materials demand?

Asia-Pacific is expected to post the highest 9.77% CAGR through 2031, led by China’s magnesium mandate and Japan’s hydrogen rollout.

Which end-use segment is growing quickest?

The energy segment, driven by offshore wind blades and hydrogen tanks, is projected to expand at a 9.81% CAGR.

Why are carbon-fiber composites critical for hydrogen vehicles?

They enable 700-bar Type IV tanks that achieve 5.5 wt% hydrogen storage while keeping system mass below 110 kg.

Page last updated on: