Strep Throat Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

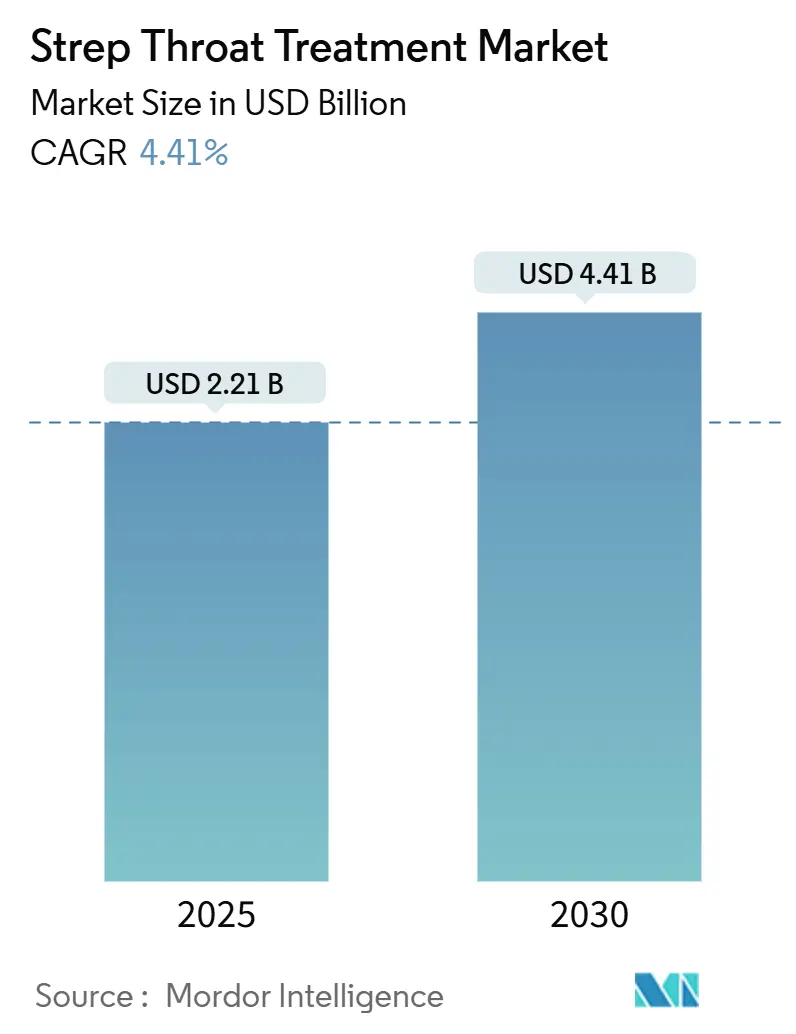

| Market Size (2025) | USD 2.21 Billion |

| Market Size (2030) | USD 4.41 Billion |

| Growth Rate (2025 - 2030) | 4.41% CAGR |

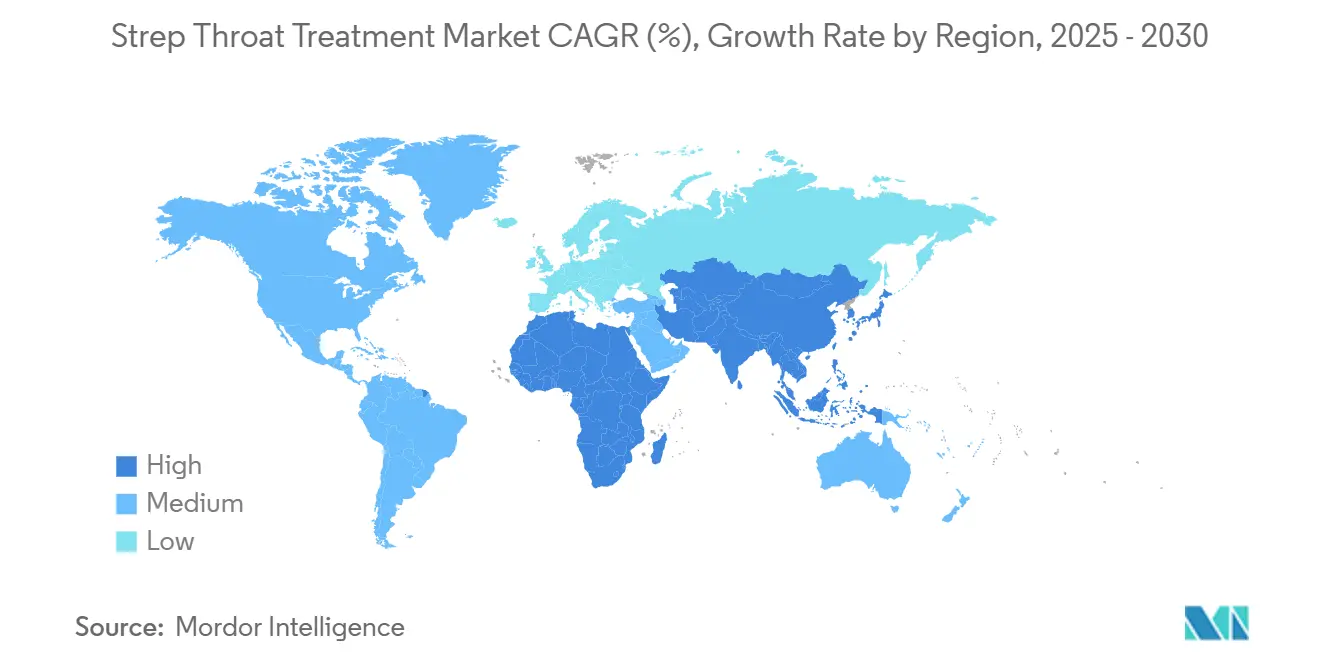

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Strep Throat Treatment Market Analysis by Mordor Intelligence

The strep throat treatment market size stood at USD 2.21 billion in 2025 and is forecast to reach USD 2.74 billion by 2030, reflecting a 4.41% CAGR. This growth is underpinned by persistently high Group A Streptococcus (GAS) pharyngitis incidence, supply-chain diversification into India, and a steady flow of product innovation. Rising pediatric caseloads, narrow-spectrum prescribing mandates, and expanding e-pharmacy networks collectively bolster demand, whereas macrolide resistance and benzathine penicillin shortages temper momentum. Competitive activity now centers on fermentation capacity additions, next-generation antibiotic launches, and vaccine-linked diagnostic solutions. North America remains the revenue leader, but Asia-Pacific—supported by fresh API investments and rapid digital health adoption—exhibits the fastest acceleration.

Key Report Takeaways

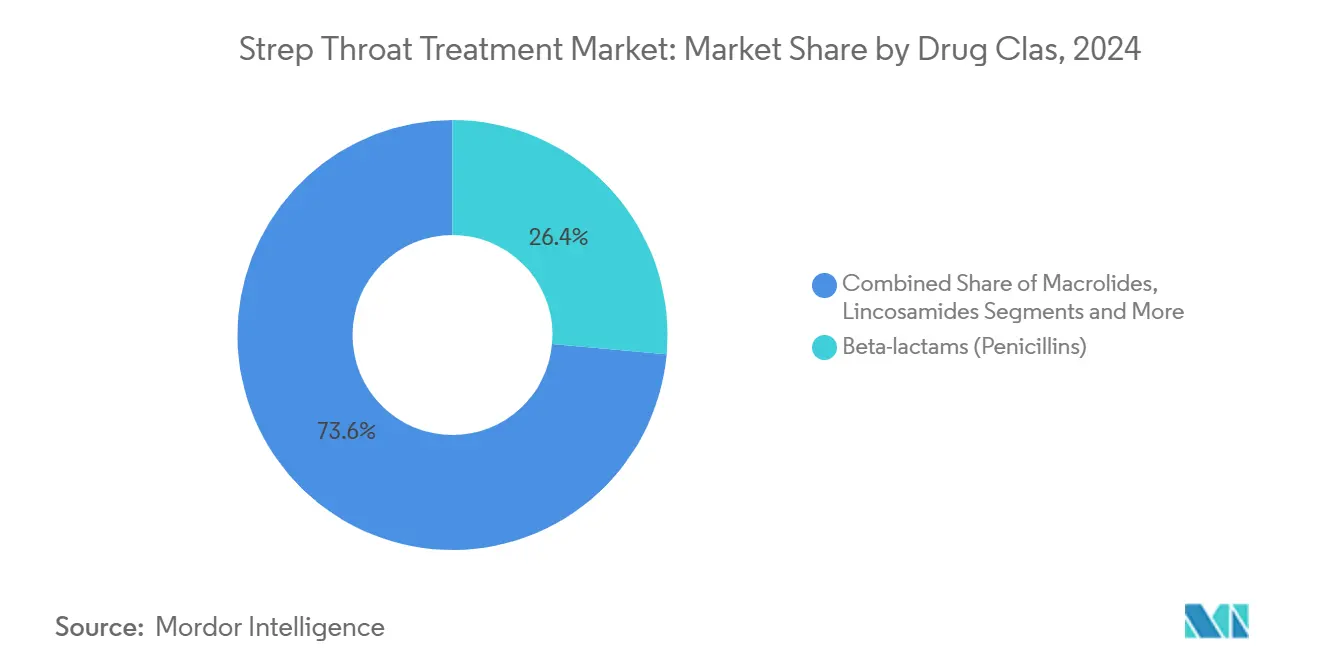

- By drug class, beta-lactams (Penicillins) held 26.42% of strep throat treatment market share in 2024; cephalosporins are advancing at a 7.21% CAGR through 2030.

- By route of administration, oral formulations commanded 61.22% of the strep throat treatment market size in 2024, while parenteral options are expanding at a 7.96% CAGR to 2030.

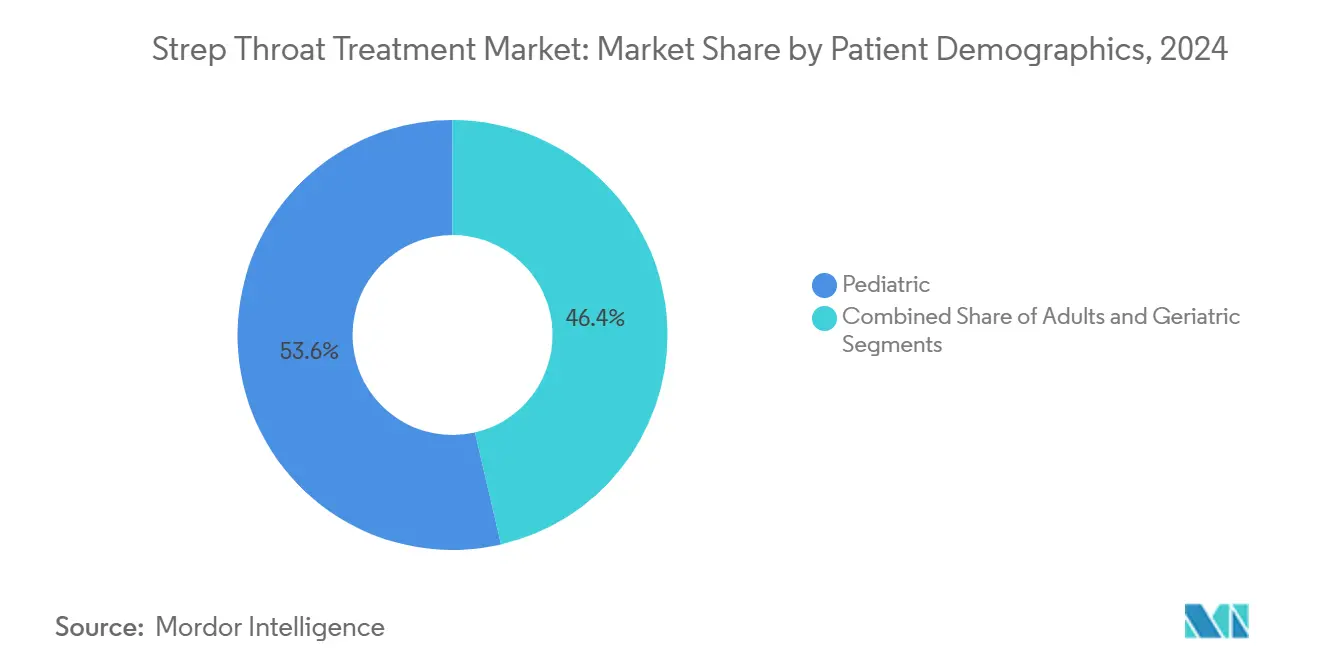

- By patient demographic, the pediatric cohort accounted for 53.63% of the strep throat treatment market size in 2024, whereas adults are registering the highest forecast CAGR at 6.02%.

- By distribution channel, hospital pharmacies captured 58.74% of strep throat treatment market share in 2024; online pharmacies are growing fastest at 8.48% CAGR.

- By geography, North America led with 31.21% market share in 2024, and Asia-Pacific is poised for a 6.73% CAGR during the outlook period.

Global Strep Throat Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of GAS pharyngitis in children | +1.2% | North America, Europe, global school-age populations | Medium term (2-4 years) |

| Mandated use of narrow-spectrum penicillins | +0.8% | Developing regions, global guideline adoption | Long term (≥ 4 years) |

| Expanding e-pharmacy reach in emerging markets | +1.5% | Asia-Pacific core, Latin America, MEA | Short term (≤ 2 years) |

| Growth in Asian generic-API capacity | +0.9% | Asia-Pacific, global export markets | Medium term (2-4 years) |

| Hospital stock-piling of benzathine penicillin | +0.6% | North America, European Union, Australia | Short term (≤ 2 years) |

| Accelerating Strep A vaccine R&D | +0.4% | High-income economies, global diagnostics market | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of GAS Pharyngitis Among School-Age Children

Surveillance programs recorded a 40% rise in Canadian invasive GAS cases during 2023, while U.S. figures climbed to a two-decade high of 20,000–27,000 infections with about 2,000 deaths, trends traced to reduced immunity post-lockdown and the virulent M1UK strain.[1]Donald R. Walkinshaw, “Invasive Group A Streptococcal Disease: a Resurging Menace?” Cepheid, cepheid.com Children under 10 remain the most affected, mirroring their 53.63% treatment volume share. Heightened school-based screening, rapid antigen testing, and prophylactic protocols sustain therapeutic demand and spur diagnostic procurements.

Guideline-Mandated Use of Narrow-Spectrum Penicillins to Prevent Rheumatic Fever

CDC and WHO guidelines continue to endorse penicillin as first-line therapy, preserving its 26.42% segment lead and pre-empting acute rheumatic fever. The UK’s January 2025 “Access” list update broadened first-generation cephalosporin options yet upheld stewardship goals.[2]UK Health Security Agency, “Antibiotic ‘Access’ List Updated for the UK,” gov.ukSustained regulatory backing ensures durable demand for traditional penicillin formulations.

Expanding E-Pharmacy Penetration in Emerging Economies

Online pharmacies are spreading fast across emerging economies, led by India, where digital storefronts have been growing at an 8.48% CAGR—well ahead of traditional chemists. The habit took hold during the pandemic and has since turned into a mainstream option as patients appreciate the ease of ordering antibiotics from home. Policymakers now accept electronic prescriptions and have set clear quality-control rules, giving the channel formal legitimacy. Real-time inventory tools and responsive delivery networks allow rural households to receive verified medicines without long trips to urban centers. Faster access helps curb complications from untreated infections and supports better adherence with automatic refill reminders. All told, e-pharmacy is shifting from a niche experiment to a pillar of antibiotic distribution across the developing world.

Growth in Asian Generic-API Capacity Lowering Treatment Cost

Aurobindo Pharma’s 15,000-tonne Penicillin G facility, operational since November 2024, punctures decades-long dependence on Chinese fermentation output and signals wider regional cost advantages. Similar capacity builds by Sandoz in Austria and Germany inject redundancy into global supply chains and compress finished-dose prices, benefiting cost-sensitive markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antimicrobial resistance to macrolides & clindamycin | −1.1% | China, broader Asia-Pacific, global surveillance zones | Medium term (2-4 years) |

| Poor adherence to 10-day oral regimens | −0.8% | Pediatric cohorts worldwide | Short term (≤ 2 years) |

| Hospital stewardship programs cutting prophylaxis | −0.6% | North America, Europe, advanced Asia-Pacific | Long term (≥ 4 years) |

| API supply crunch & price spikes for penicillin | −0.9% | Import-dependent regions, North America, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Antimicrobial Resistance to Macrolides & Clindamycin

Chinese surveillance reports erythromycin resistance exceeding 90%, eroding fallback options for penicillin-allergic patients.[3]Jialin Li et al., “Severe Problem of Macrolide Resistance to Common Pathogens in China,” Frontiers in Cellular and Infection Microbiology, frontiersin.org Spain shows lower yet notable rates, underscoring geographic variability. Hospitals now trial linezolid for toxin suppression, but pricing limits widescale substitution.

Poor Adherence to 10-Day Oral Regimens

Placebo-controlled studies question extended courses, revealing similar symptomatic relief yet heightened complication risk without antibiotics. Single-dose benzathine injections and twice-daily amoxicillin regimens seek to offset early discontinuation common in children.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Penicillins Remain Core While Cephalosporins Advance

Beta-lactams (Penicillins) accounted for 26.42% of the strep throat treatment market share in 2024, validated by persistent first-line guideline status. Cephalosporins led growth at a 7.21% CAGR as newly reclassified “Access” agents gained favor for penicillin-allergic cases. Macrolides and lincosamides struggle amid resistance, whereas novel β-lactam/enzyme combinations expand “Others.”

Cephalosporin adoption strengthens physician flexibility and may marginally compress penicillin volumes, yet universal GAS susceptibility ensures penicillin’s structural dominance. Regulatory harmonization under WHO AWaRe targets keeps broad-spectrum creep in check, sustaining narrow-spectrum demand across developed and emerging markets alike.

By Route of Administration: Oral Regimens Prevail Yet Parenteral Uptake Climbs

Oral formats captured 61.22% of the strep throat treatment market in 2024, reflecting outpatient care norms. Intravenous and intramuscular options, however, posted a 7.96% CAGR as invasive GAS episodes rose and benzathine injections offered adherence insurance.

Parenteral expansion aligns with hospital stewardship that favors assured pharmacokinetics in severe disease. Single-shot intramuscular benzathine mitigates pill fatigue in children, and shorter IV courses trimmed to seven days reduce bed-day costs while maintaining outcomes.

By Patient Demographic: Pediatric Dominance Sustained as Adult Volume Builds

Children generated 53.63% of treatment revenues in 2024, correlating with incidence peaks of 1,764 cases per 100,000 and updated school health mandates. Adults record the sharpest expansion at 6.02% CAGR, propelled by improved diagnostic coding and post-pandemic clinic attendance.

Geriatric cohorts remain niche yet clinically complex, often requiring renal-adjusted dosing and multidrug interaction checks. Telemedicine triage coupled with rapid antigen testing broadens disease recognition across all age brackets, further enlarging the total addressable population.

By Distribution Channel: Hospital Pharmacies Lead While Digital Dispense Accelerates

Hospital pharmacies retained 58.74% revenue share in 2024 through stewardship oversight and emergency inventory roles. Online outlets, scaling at 8.48% CAGR, integrate telehealth consults and same-day delivery, attracting remote consumers and younger demographics.

Retail community pharmacies remain central to routine script fulfillment, yet face price competition and digital convenience advantages. Blended omnichannel offerings—click-and-collect or hospital-to-home delivery—emerge as defensive strategies for brick-and-mortar operators.

Geography Analysis

North America generated 31.21% of 2024 revenue, supported by widespread rapid testing and reimbursement coverage. Persistent benzathine shortages prompted FDA emergency imports, yet robust insurance frameworks preserved treatment access.

Asia-Pacific exhibits a 6.73% CAGR, energized by Aurobindo’s Penicillin G restart and accelerating e-pharmacy penetration. China’s 44.5% share of global antibiotic API exports and India’s PLI-driven capacity surge jointly reinforce the region’s supply clout. Concurrent public-sector programs broaden rural diagnostic reach.

Europe maintains steady uptake via stewardship-aligned prescribing and coordinated resistance surveillance. Middle East & Africa increasingly participate in WHO rheumatic-heart-disease prevention schemes, though logistics hurdles persist. South America’s outlook remains moderate as Brazil and Argentina scale local generics and expand primary-care infrastructure.

Competitive Landscape

Global supply shocks and resistance trends shape a moderately concentrated arena where scale manufacturing, R&D pipelines, and digital integrations define leadership. Pfizer invested AUD 150 million to modernize its Melbourne plant with AI-driven robotics and purchased AstraZeneca’s antibiotics unit for USD 1.5 billion to deepen its infectious-disease franchise.

Shionogi merged with Qpex Biopharma in April 2024, establishing a San Diego hub that targets resistant pathogens within BARDA-backed programs. Sandoz and Aurobindo pursue cost leadership through fresh penicillin lines in Europe and India, respectively, enhancing redundancy and price competitiveness.

Competitive differentiation now extends to point-of-care diagnostics, AI-guided prescription platforms, and blockchain-verified supply chains. Firms with robust compliance track records and diversified API sources are better positioned to navigate future shortages and stewardship restrictions.

Strep Throat Treatment Industry Leaders

Pfizer Inc.

GlaxoSmithKline plc

Sandoz

Abbott Laboratories

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Shionogi finalized its Qpex Biopharma merger, expanding U.S. R&D capacity

- April 2024: Aurobindo Pharma activated a 15,000-tonne Penicillin G plant in Andhra Pradesh, ending India’s 30-year production hiatus

Global Strep Throat Treatment Market Report Scope

| Beta-lactams (Penicillins) |

| Cephalosporins |

| Macrolides |

| Lincosamides |

| Others |

| Oral |

| Intramuscular |

| Intravenous |

| Pediatric (0-17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (65+ yrs) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Beta-lactams (Penicillins) | |

| Cephalosporins | ||

| Macrolides | ||

| Lincosamides | ||

| Others | ||

| By Route of Administration | Oral | |

| Intramuscular | ||

| Intravenous | ||

| By Patient Demographic | Pediatric (0-17 yrs) | |

| Adults (18-64 yrs) | ||

| Geriatric (65+ yrs) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the strep throat treatment market?

The strep throat treatment market size reached USD 2.21 billion in 2025 and is projected to grow to USD 2.74 billion by 2030.

Which drug class dominates prescription volumes for strep throat?

Penicillins remain the leading class with 26.42% market share, driven by consistent guideline endorsements.

Why is Asia-Pacific the fastest-growing region?

The region benefits from expanded generic API capacity, strong e-pharmacy uptake, and improving healthcare access, yielding a 6.73% CAGR.

How are supply shortages influencing hospital procurement?

Hospitals are stock-piling benzathine penicillin and diversifying suppliers to mitigate a 15.6% antibacterial shortage rate.

What role do online pharmacies play in treatment access?

Online channels, growing at 8.48% CAGR, integrate telehealth and home delivery, improving adherence and rural reach.

Are vaccine developments expected to disrupt the therapeutic market?

Multiple Strep A vaccine candidates are advancing, and widespread adoption could eventually curb treatment demand while boosting diagnostic testing volumes.

Page last updated on: