Bronchitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

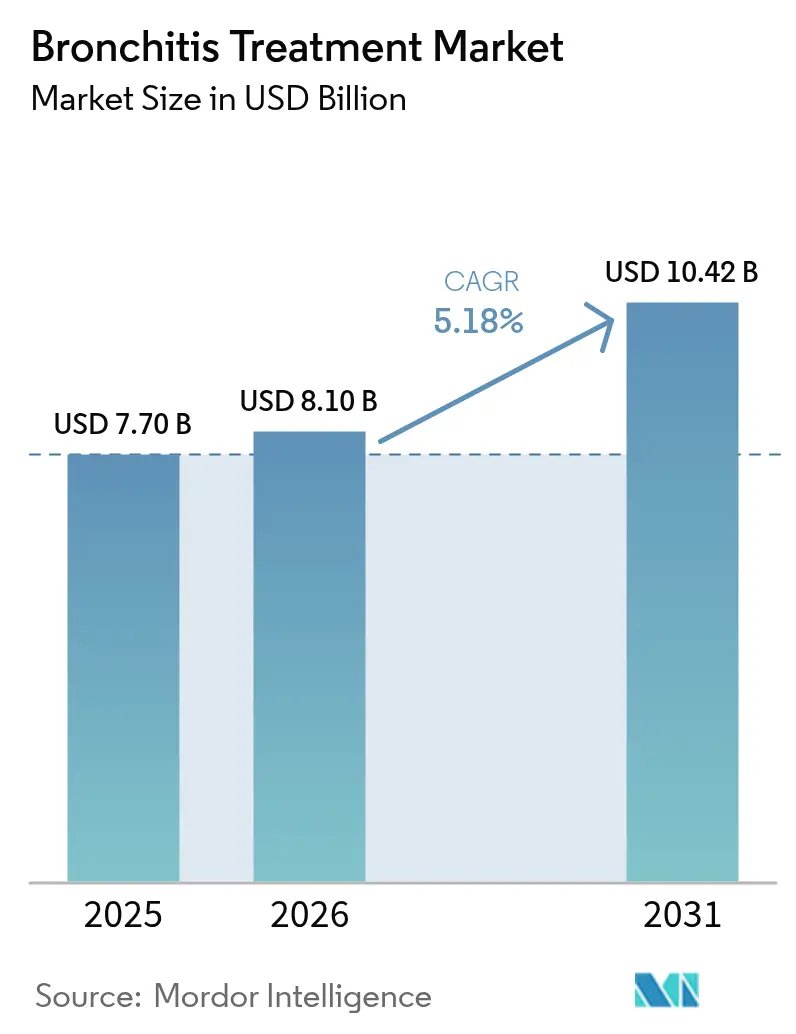

| Market Size (2026) | USD 8.1 Billion |

| Market Size (2031) | USD 10.42 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bronchitis Treatment Market Analysis by Mordor Intelligence

The bronchitis treatment market size is expected to grow from USD 7.70 billion in 2025 to USD 8.10 billion in 2026 and is forecast to reach USD 10.42 billion by 2031 at 5.18% CAGR over 2026-2031. Increasing life expectancy, sustained urban air-pollution exposure, and the wider adoption of long-acting inhaled combination therapies are reshaping commercial opportunity. A steady rise in chronic obstructive pulmonary disease (COPD) prevalence, especially among aging populations, keeps patient volumes high, while megacity nano-particle concentrations continue to elevate symptomatic caseloads[1]Keck School of Medicine, “Air Pollution Exposure During Childhood Linked Directly to Adult Bronchitis Symptoms in New Research,” keck.usc.edu. Digital health integration further broadens treatment access through home-monitoring platforms that improve adherence and reduce costly exacerbations. Supply-side pressure persists, however, as antibiotic active-ingredient sourcing remains concentrated in a few Asian hubs, leading firms to diversify manufacturing footprints to reinforce resilience.

Key Report Takeaways

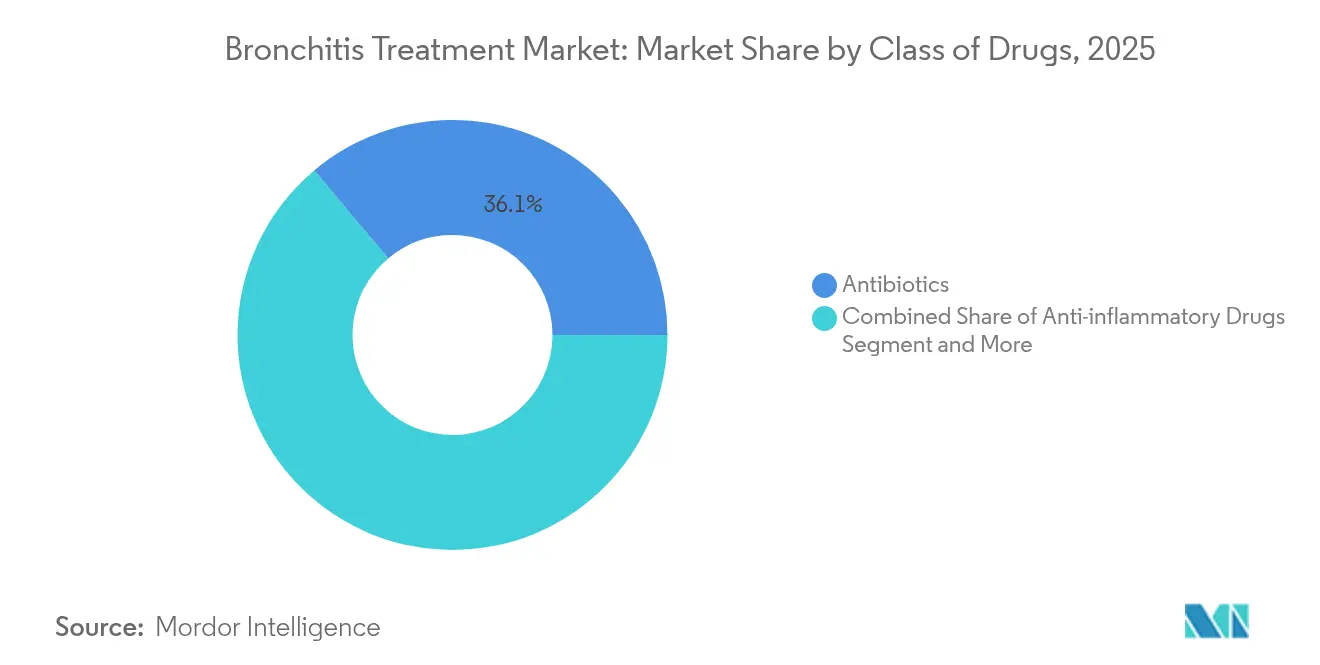

- By class of drugs, antibiotics led with 36.12% of bronchitis treatment market share in 2025; bronchodilators are projected to expand at a 6.98% CAGR through 2031.

- By disease type, acute bronchitis accounted for 58.96% of bronchitis treatment market size in 2025, while chronic bronchitis is progressing at a 8.96% CAGR to 2031.

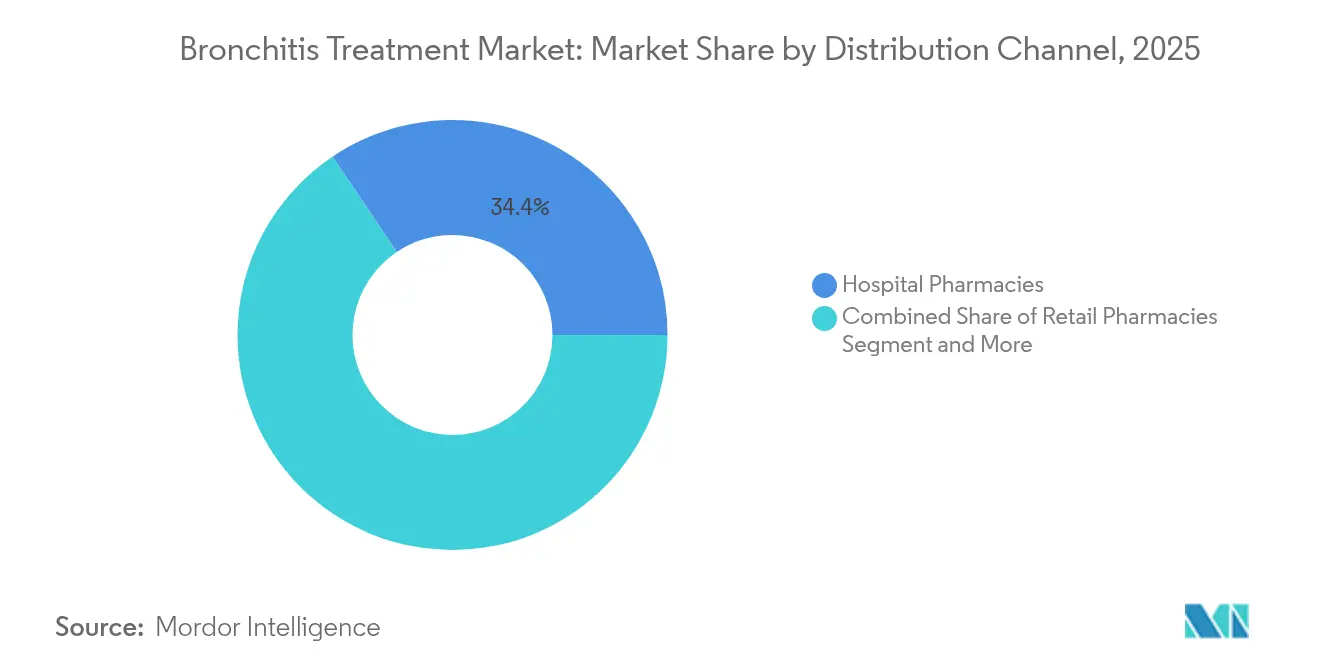

- By distribution channel, hospital pharmacies held 34.41% revenue share in 2025; online and mail-order pharmacies record the fastest growth at 9.74% CAGR through 2031.

- By route of administration, parenteral delivery commanded 44.25% share of bronchitis treatment market size in 2025, whereas inhalation routes are rising at a 10.18% CAGR through 2031.

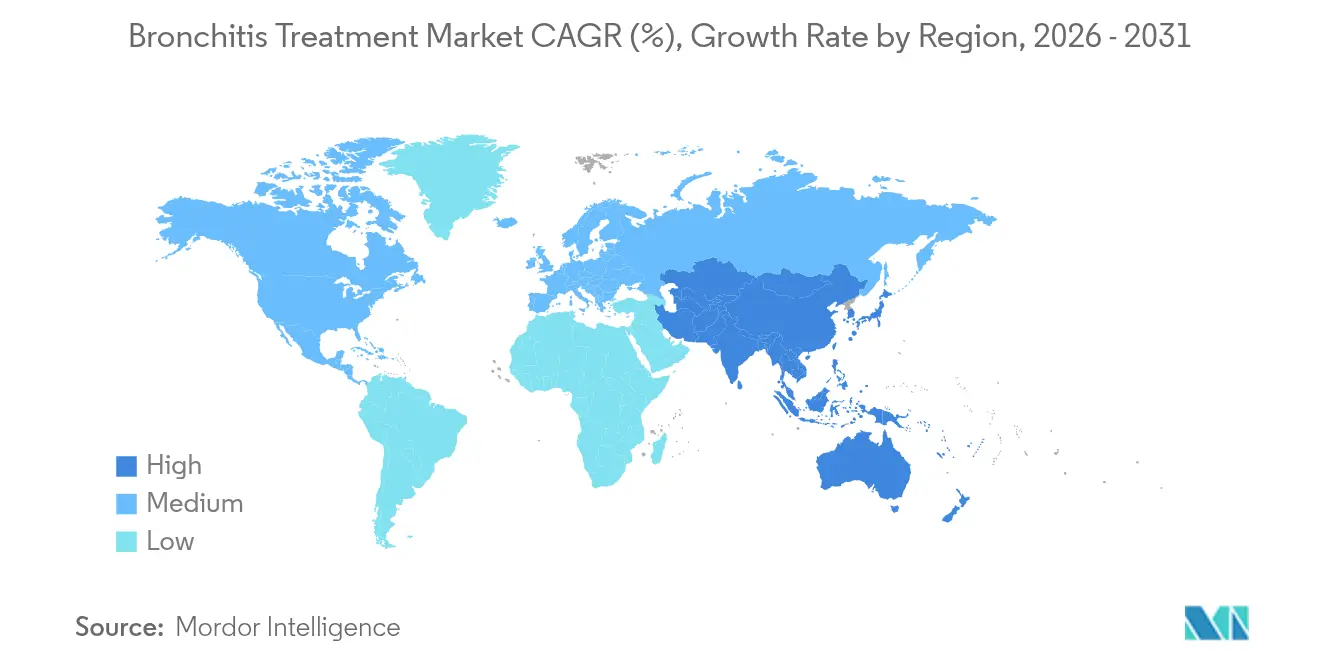

- By geography, North America captured 35.40% bronchitis treatment market share in 2025; Asia-Pacific is the fastest-growing region at a 10.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bronchitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Geriatric Population With Higher Bronchitis Incidence | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Escalating COPD Prevalence Worldwide | +1.8% | Global, particularly APAC and emerging markets | Medium term (2-4 years) |

| Rising Air-Pollution Nano-Particle Exposure In Megacities | +0.9% | APAC core, spill-over to MEA urban centers | Medium term (2-4 years) |

| Expanding Tele-Pulmonology Platforms Improving Therapy Adherence | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Government Push For AMR-Conscious Antibiotic Stewardship | +0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population With Higher Bronchitis Incidence

People aged 65 and above now account for an unprecedented share of the global population, and molecular hallmarks of lung aging—oxidative stress and cellular senescence—reduce mucociliary clearance and impair immune function. As a result, elderly patients present with more frequent bronchitis episodes requiring intensive pharmacologic support. Health systems are responding by rolling out age-specific care pathways, geriatric pulmonary clinics, and home-based monitoring to avoid hospital readmissions. Drug developers are tailoring dosing regimens and delivery devices to accommodate declining inspiratory flow, further stimulating the bronchitis treatment market.

Escalating COPD Prevalence Worldwide

Global COPD prevalence continues to climb, especially in middle-income economies where tobacco exposure and indoor biomass fuel use remain common. Because chronic bronchitis is a core COPD phenotype, escalating COPD caseloads translate directly into sustained demand for long-acting bronchodilators and dual anti-inflammatory therapies. The 2024 FDA approval of ensifentrine, the first dual PDE3/4 inhibitor for maintenance therapy in over two decades, signals industry commitment to novel mechanisms that reduce exacerbations and enhance quality of life.

Rising Air-Pollution Nano-Particle Exposure In Megacities

Particulate-matter (PM2.5) and nano-particle concentrations in fast-growing urban centers are damaging airway epithelial integrity and triggering oxidative injury. Longitudinal evidence links childhood NO₂ exposure to adult bronchitis symptoms, even after adjusting for childhood asthma. Regulatory lag in emerging economies means millions remain exposed to unhealthy air, pushing treatment volumes upward. Pharmaceutical marketers are targeting high-pollution clusters with direct-to-consumer awareness campaigns and inhaler adherence programs.

Expanding Tele-Pulmonology Platforms Improving Therapy Adherence

Remote spirometry, smart inhalers, and AI-driven symptom trackers surged following the COVID-19 pandemic and now anchor hybrid care models. Studies show that telemedicine visits for COPD patients reduce exacerbation-related hospitalizations by enabling early intervention. Leading drug manufacturers partner with digital-health start-ups to bundle medications with connected devices, thereby differentiating brands and elevating the bronchitis treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Drug-Approval Timelines & Costs | -0.8% | Global, most pronounced in developed markets | Medium term (2-4 years) |

| Volatile API Supply Chains For Macrolides & Quinolones | -0.6% | Global, concentrated risk in Asia-dependent markets | Short term (≤ 2 years) |

| Growing Consumer Preference For Antibiotic-Free Herbal Remedies | -0.4% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Drug-Approval Timelines & Costs

Securing a new respiratory therapy can require close to USD 1 billion in R&D outlay and nearly eight years of clinical development, while a single FDA application with clinical data now commands a USD 4.31 million fee. Such economics discourage smaller innovators and slow the refresh rate of first-in-class molecules, tempering the pace at which groundbreaking options reach the bronchitis treatment market.

Volatile API Supply Chains For Macrolides & Quinolones

Antibiotic supply reliability remains under threat as 67% of antimicrobial Drug Master Files are lodged in India and China. Regulatory disruptions, geopolitical frictions, and pricing pressure on low-margin generics heighten the risk of shortages for frontline bronchitis therapies[2]Quality Matters, “Supply Chain Vulnerabilities Exist for Antimicrobial Medicines: USP Medicine Supply Map Analysis,” qualitymatters.usp.org. Manufacturers are investing in dual-sourcing strategies and near-shoring initiatives, yet the capital intensity and long lead times dilute near-term impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Class of Drugs: Antibiotics Lead Despite Bronchodilator Surge

Antibiotics held 36.12% of bronchitis treatment market share in 2025, reflecting their entrenched role for bacterial exacerbations. The bronchitis treatment market size for antibiotics reached USD 2.78 billion and expanded modestly as stewardship programs temper unnecessary use. Concurrently, bronchodilators registered a 6.98% CAGR, buoyed by the launch of dual-mechanism inhalers and triple fixed-dose combinations. The bronchodilator segment of bronchitis treatment market size is forecast to surpass USD 2.38 billion by 2031 as payers increasingly recognize their exacerbation-prevention value.

Regulatory tailwinds favor long-acting formulations: the June 2024 FDA approval of ensifentrine reinvigorated R&D pipelines. Antibiotic innovators counter by reformulating macrolides for once-daily dosing and rapid-onset parenteral options. In parallel, herbal alternatives such as ivy-leaf extract achieve guideline endorsements for acute bronchitis relief, reflecting growing consumer interest in antibiotic-sparing therapies.

By Disease Type: Chronic Bronchitis Gains Momentum

Acute bronchitis contributed 58.96% to 2025 revenue yet grows slowly as viral etiology awareness restricts antibiotic prescribing. Chronic bronchitis, however, is advancing at a 8.96% CAGR and will close the gap by the end of the decade, underpinned by the aging population and mounting COPD burden. Payers increasingly reimburse maintenance therapies that curb hospitalizations, bolstering the chronic segment’s share of bronchitis treatment market size.

Guideline updates now stress early introduction of inhaled anti-inflammatory combinations for chronic cases, a shift mirrored by rising uptake of smart inhalers capable of logging real-world adherence and inspiratory flow metrics. Acute bronchitis care continues migrating toward symptomatic relief, with rapid diagnostics supporting delayed antibiotic scripts that meet antimicrobial stewardship targets.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies captured 34.41% of 2025 revenue by virtue of specialist oversight and formulary integration, but their share is gradually ceded to emerging e-commerce models. Online and mail-order channels clocked a 9.74% CAGR as teleconsults surged and chronic patients demanded doorstep delivery. Retail chains respond by adding point-of-care spirometry and disease-state clinics to maintain footfall, keeping them integral to the bronchitis treatment market.

Digital pharmacies partner with adherence-support apps and automated refill engines that alert users ahead of prescription lapses. Regulators strive to balance consumer convenience with safety, imposing e-pharmacy accreditation standards while encouraging electronic prescriptions. Drug makers now craft multi-channel launch plans, bundling drug starter kits with QR-linked education portals for seamless onboarding.

By Route of Administration: Inhalation Innovation Drives Growth

Parenteral therapies led with 44.25% share owing to their indispensability in severe inpatient cases. Nevertheless, inhalation routes are outpacing all others at a 10.18% CAGR as device miniaturization and formulation science deliver higher lung deposition. The bronchodilator segment of inhalation-focused bronchitis treatment market size is projected to add USD 914 million between 2026 and 2031.

Advanced systems such as Aerami’s soft-mist AFINA inhaler deposit nearly 80% of payload in distal airways. Nanogrid carriers and mRNA-loaded nanoparticles, still in early trials, promise targeted anti-inflammatory effects with extended dwell time. Oral routes remain vital for outpatient antibiotic courses but face rising competition from inhaled antibiotics designed for on-target delivery with fewer systemic effects.

Geography Analysis

North America controlled 35.40% of 2025 revenue thanks to cutting-edge drug availability, comprehensive reimbursement frameworks, and high telehealth penetration. Recent FDA approvals of biologics such as mepolizumab for eosinophilic COPD have widened the therapeutic arsenal, supporting premium pricing in the United States. Canada’s single-payer system negotiates lower list prices yet drives volume through national COPD screening programs, while Mexico benefits from cross-border generic importation that reduces out-of-pocket costs.

Asia-Pacific is expanding fastest at a 10.11% CAGR as governments boost healthcare outlays and encourage local production of complex inhaled formulations. China’s Healthy China 2030 agenda increases diagnosis rates, and India’s Ayushman Bharat scheme enlarges insurance coverage, collectively lifting treatment uptake. Singapore’s 2024 clearance of Trelegy Ellipta underscores the region’s growing role as a launchpad for inhaled triple therapies. However, regulatory heterogeneity across ASEAN markets necessitates tailored filing pathways, elongating time-to-launch.

Europe maintains steady growth, propelled by universal coverage and robust antimicrobial stewardship that nudges prescribers toward non-antibiotic options. The EU’s heightened focus on clean-air directives indirectly supports preventive treatment demand as cities struggle to meet PM2.5 targets. Eastern European states observe rapid uptake of generic bronchodilators, while Western markets embrace biologic add-ons for severe phenotypes. Elsewhere, South America and the Middle East & Africa offer long-term upside but grapple with volatile currency environments and patchy insurance coverage, prompting multinational firms to partner with local distributors for wider reach.

Competitive Landscape

Moderate concentration characterizes the bronchitis treatment market. AstraZeneca, GSK, and Boehringer Ingelheim collectively command well over half of branded inhaled therapy sales, leveraging deep pipelines and global detailing forces. Strategic acquisitions reinforce scale; AstraZeneca’s USD 2 billion purchase of Almirall’s respiratory franchise in 2024 added established brands and a late-stage biologic candidate. GSK’s USD 1.4 billion buyout of Aiolos Bio in early 2024 secured a next-generation anti-IL-33 antibody, broadening its immunology portfolio.

Emerging players inject novelty. Verona Pharma’s ensifentrine recorded USD 42 million in first-year sales and attracted significant formulary coverage owing to its dual-mechanism efficacy. Insmed’s brensocatib, with a December 2025 PDUFA date, could become the first DPP1 inhibitor for bronchiectasis, opening an adjacent submarket. Device specialists such as Phillips-Medisize (Molex) and Bespak augment competition through innovative inhaler platforms that improve dose accuracy and patient ergonomics.

Technology collaborations differentiate value propositions: AstraZeneca’s tie-up with ArtiQ embeds AI-driven lung-function analytics into home spirometry kits, while Flagship Pioneering aligns with GSK to co-discover novel respiratory biologics. Patent cliffs for leading bronchodilators begin mid-decade, inviting generic entrants that will pressure price points yet expand patient reach, especially in cost-sensitive markets.

Bronchitis Treatment Industry Leaders

Boehringer Ingelheim International GmbH

AstraZeneca PLC

GSK PLC

Novartis AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GSK received FDA approval for Nucala (mepolizumab) as add-on maintenance therapy for adults with inadequately controlled COPD and blood eosinophil count ≥ 150 cells/µL, introducing the first biologic for eosinophilic COPD phenotypes.

- April 2025: Insmed’s brensocatib achieved significant efficacy in Phase 3 bronchiectasis trials, with 48.5% of patients remaining exacerbation-free at week 52 versus 40.3% for placebo, supporting its FDA submission with a December 8 2025 action date.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bronchitis treatment market as prescription or over-the-counter drugs, antibiotics, anti-inflammatory agents, bronchodilators, mucolytics, expectorants, and oxygen therapy sold through hospital, retail, and online channels for acute and chronic bronchitis across 17 country clusters.

Scope exclusion: Diagnostic devices, rehabilitation equipment, and herbal supplements lie outside this scope.

Segmentation Overview

- By Class of Drugs

- Antibiotics

- Anti-inflammatory Drugs

- Bronchodilators

- Mucolytics & Expectorants

- Other Drugs

- By Disease Type

- Acute Bronchitis

- Chronic Bronchitis

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online & Mail-order Pharmacies

- Other End Users

- By Route of Administration

- Oral

- Inhalation

- Parenteral

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with pulmonologists, pharmacists, payor advisers, and manufacturing managers in North America, Europe, and Asia to validate therapy mix, refill behavior, and mark-ups before final modeling.

Desk Research

We extracted disease incidence, hospital admissions, and import data from the World Health Organization, CDC, Eurostat, national customs portals, and trade dashboards. Drug price curves and pipeline shifts were refined with 10-K filings, peer journals, and the Questel patent repository. These inputs set prevalence, unit volume, and average selling price baselines; other sources were also reviewed.

Market-Sizing & Forecasting

We open with a top-down prevalence-to-treated-cohort build, multiplying country bronchitis incidence, treatment-seeking rates, and standard course costs to reach revenue pools. Supplier roll-ups for key molecules test these totals. Core variables include COPD prevalence, air-quality indices, antibiotic stewardship rules, retail pharmacy penetration, and inflation-adjusted drug ASPs. Multivariate regression underpins the 2025-2030 outlook, while scenario checks dampen extremes. Bottom-up gaps, such as untracked private-label sales, are filled by channel share proxies agreed in interviews.

Data Validation & Update Cycle

Two analysts run variance screens; anomalies trigger follow-ups, and every model refreshes yearly, with mid-cycle updates for material regulatory or supply shifts.

Why Mordor's Bronchitis Treatment Baseline Commands Reliability

Published estimates often diverge because firms pick different drug baskets, patient funnels, currencies, and refresh cadences. Our disciplined scope, dual-path model, and annual updates keep the baseline steady yet responsive.

Some providers merge asthma inhalers or equipment revenue; others rely on straight inflation factors instead of epidemiologic controls. Mordor adjusts every driver each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.70 Bn (2025) | Mordor Intelligence | |

| USD 6.90 Bn (2024) | Regional Consultancy A | Includes devices alongside drugs |

| USD 8.67 Bn (2025) | Global Consultancy B | Counts COPD and asthma therapeutics together |

| USD 5.94 Bn (2025) | Industry Tracker C | Uses limited hospital data and linear price escalators |

These comparisons show that Mordor's figures sit within the observable range yet rest on transparent variables and repeatable steps, giving decision-makers a balanced, dependable starting point.

Key Questions Answered in the Report

What is the current value of the bronchitis treatment market?

The bronchitis treatment market is valued at USD 8.10 billion in 2026 and is projected to reach USD 10.42 billion by 2031.

Which drug class is growing fastest in bronchitis care?

Bronchodilators exhibit the highest growth, advancing at a 6.98% CAGR through 2031 due to uptake of dual- and triple-mechanism inhalers.

Why is Asia-Pacific the most attractive growth region?

Rapid urbanization, rising healthcare investment, and growing middle-class awareness are driving a 10.11% regional CAGR, the highest globally.

How are tele-pulmonology platforms influencing the market?

Connected inhalers and remote spirometry improve adherence and early exacerbation detection, adding new revenue streams and reducing hospital readmissions.

What challenges threaten bronchitis drug supply?

API manufacturing is heavily concentrated in India and China, making antibiotics vulnerable to geopolitical and regulatory disruptions.

Page last updated on: