Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

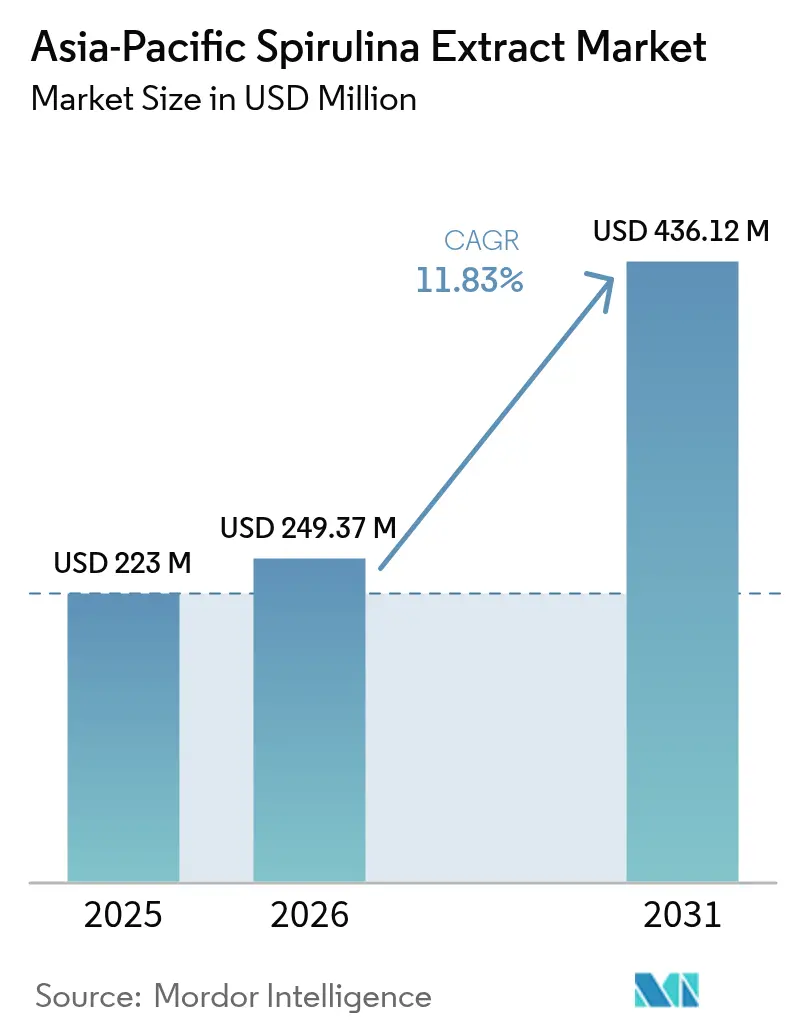

| Base Year Market Size (2025) | USD 223.00 Million |

| Market Size (2026) | USD 249.37 Million |

| Market Size (2031) | USD 436.12 Million |

| Growth Rate (2026 - 2031) | 11.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Spirulina Extract Market Analysis by Mordor Intelligence

The Asia-Pacific spirulina extract market size is expected to grow from USD 223.00 million in 2025 to USD 249.37 million in 2026 and is forecast to reach USD 436.12 million by 2031 at 11.83% CAGR over 2026-2031. The rising demand for clean-label blue colorants, plant-based protein fortification, and sustainability-aligned ingredients continues to drive strong momentum. Regional producers benefit from cost-competitive open-pond cultivation in China and India, expanding photobioreactor investments in South Korea and Japan, and government incentives that de-risk private capital flows into microalgae. Rapid adoption of phycocyanin in ready-to-drink beverages, dairy alternatives, and K-beauty formulations widens end-use diversity, while heat-stable extraction technologies mitigate previous processing barriers. Competitive strategies revolve around vertical integration, patented stabilization methods, and multi-certification portfolios that satisfy diverse import rules across China, India, Japan, South Korea, Australia, and the Association of Southeast Asian Nations (ASEAN) nations.

Key Report Takeaways

- By nature, conventional products captured 77.93% of the Asia-Pacific spirulina extract market share in 2025, whereas organic variants are on track to expand at a 12.22% CAGR through 2031.

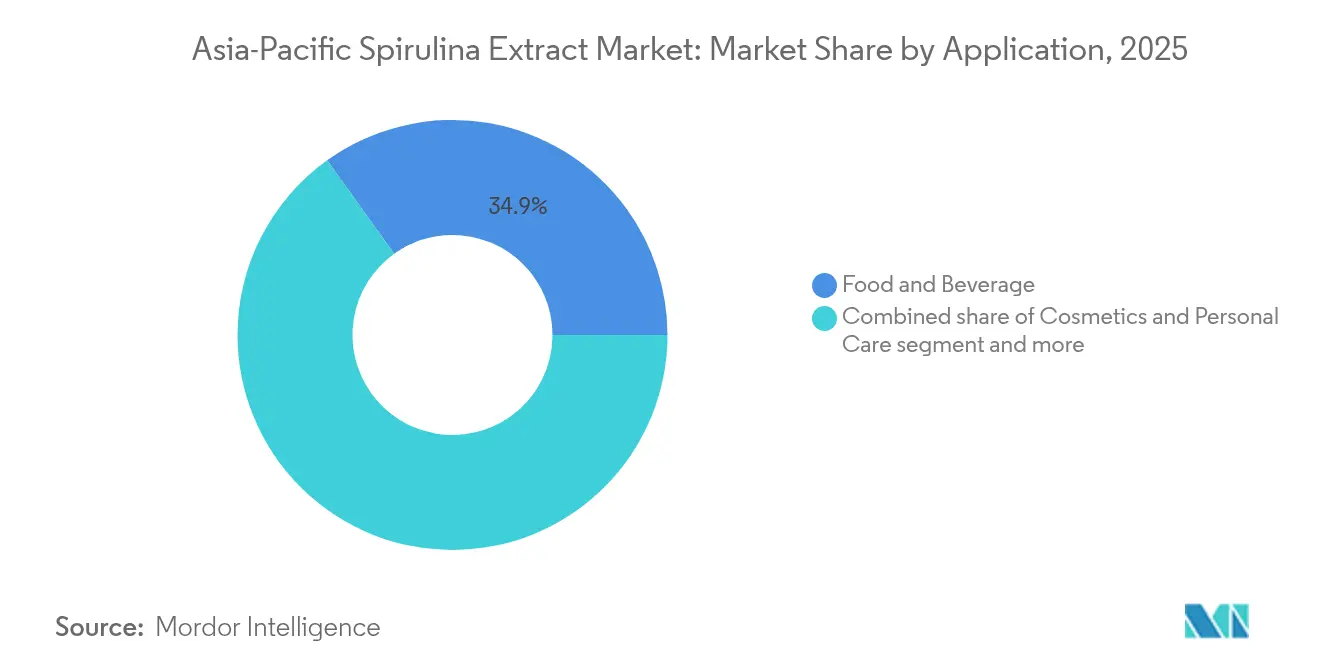

- By application, the food and beverage segment led with 34.91% revenue in 2025; cosmetics and personal care exhibit the highest growth at 13.02% CAGR to 2031.

- By geography, China held 41.07% of 2025 revenues; South Korea is forecast to record a 12.54% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Spirulina Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness focus, with consumers seeking nutrient-dense, antioxidant-rich ingredients | +2.8% | Regional, with the strongest uptake in Japan, South Korea, Australia | Medium term (2-4 years) |

| Expanding use of spirulina extract in functional foods and beverages | +2.5% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Rapid development of plant-based and vegan products where spirulina supports protein, color, and plant-based positioning | +2.3% | South Korea, Japan, Australia, urban China | Short term (≤ 2 years) |

| Government and institutional initiatives in several Asia-Pacific countries | +1.8% | India, China, Indonesia | Long term (≥ 4 years) |

| Ongoing technological advances in extraction and stabilization that improve color intensity and shelf life | +1.6% | Regional, led by Japan, China, South Korea | Medium term (2-4 years) |

| Sustainability and production advantages | +1.2% | Regionwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness focus, with consumers seeking nutrient-dense, antioxidant-rich ingredients

The increasing focus on health and wellness is driving the adoption of spirulina extract as a nutrient-dense, multifunctional ingredient across food, beverage, and supplement applications. With a high protein content of 55–70% and digestibility of 80–95%, spirulina extract serves as a compact nutritional booster for calorie-conscious and portion-controlled products, aligning with preventive health trends. Suppliers like DIC Corporation are enabling brands to fortify snacks, RTD beverages, and supplements with clean-label, whole-food microalgae sources. Standardized to contain 10–15 grams of phycocyanin per 100 grams dry weight, spirulina extract offers a consistent functional pigment that doubles as an antioxidant, supporting visual differentiation and wellness cues. Companies such as Far East Microalgae Industries (FEMICO) and E.I.D. Parry provides phycocyanin-focused portfolios for visually appealing products like blue and teal-toned beverages, jellies, and gummies. Japan and South Korea, with their advanced health and beauty cultures, are key markets where spirulina extract is used in functional foods targeting immunity, eye health, and metabolic support, as seen in DIC’s solutions for aging populations. Clinical evidence highlighting spirulina’s ability to enhance antioxidant enzymes and reduce inflammatory markers strengthens its appeal among consumers seeking measurable health outcomes. Brands like Cyanotech leverage this evidence to market spirulina-based supplements and powders for immunity and metabolic wellness. Additionally, spirulina’s dual role as a natural colorant and bioactive carrier supports reformulation efforts to replace artificial colors while maintaining functionality, with companies like Fuqing King Dnarmsa Spirulina and Jiangshan Comp Spirulina meeting regulatory and sensory demands. The rise of precision nutrition further positions spirulina extract as a versatile ingredient for targeted formulations, such as diabetic-friendly drinks and anti-fatigue shots, offered by specialists like Necton and FEMICO. This convergence of health trends, clinical validation, and natural solutions is transforming spirulina extract into a strategic ingredient for evolving consumer needs.

Expanding use of spirulina extract in functional foods and beverages

Spirulina extract's role as a natural blue colorant and protein enhancer is driving its adoption in functional foods and beverages across the Asia-Pacific region. Companies are leveraging their dual benefits to enhance both the visual appeal and nutritional value of health-focused product lines. The U.S. FDA's progressive expansion of approved applications, covering alcoholic beverages under 20% ABV, non-alcoholic beverages, condiments, sauces, dips, dairy alternatives, salad dressings, and unheated seasoning mixes, provides a strong regulatory framework for Asia-Pacific manufacturers and export-oriented producers, ensuring compliance with global standards. This regulatory support aligns with the increasing consumption of health functional foods in South Korea, where approximately 82–83% of consumers or households purchased such products in 2024, as per the Korea Health Functional Food Association, highlighting the potential for spirulina-based ingredients in beverages, fermented dairy alternatives, and convenient snacks [1]Source: Korea Health Functional Food Association, "The Health Functional Food Market is Estimated to Reach KRW 6.44 Trillion by 2024, With a Purchase Experience Rate of 82.1%", khff.or.kr . Suppliers like Far East Bio-Tec (FEBICO), offering organic spirulina powders and tablets, enable manufacturers to create energy drinks, vegan products, and fortified bakery items, translating these trends into innovative offerings. The ability to incorporate spirulina extract into both low-alcohol RTD cocktails and non-alcoholic wellness beverages allows brands to develop cohesive "better-for-you" portfolios, with the natural blue color serving as a functional marker across diverse product formats. For manufacturers in South Korea and Japan targeting health-conscious consumers, spirulina extract offers opportunities to enhance beverages, sauces, and seasoning mixes with color, protein content, and perceived health benefits, encouraging repeat purchases. These factors collectively position spirulina extract as a cornerstone of functional food and beverage innovation in the Asia-Pacific region.

Rapid development of plant-based and vegan products where spirulina supports protein, color, and “plant-based” positioning

The rapid development and adoption of plant-based and vegan food products are driving demand for spirulina extract in the Asia-Pacific region. Spirulina is increasingly utilized as a key ingredient due to its high-quality protein content, natural coloring properties, and alignment with plant-based preferences, appealing to health-conscious, sustainability-focused, and ethically driven consumers. Governments and non-profit organizations in the region are actively promoting plant-centric diets, with agricultural and nutrition policies in countries such as India and China emphasizing the expansion of sustainable protein sources to improve nutrition and reduce reliance on animal agriculture. These initiatives reflect broader national strategies aimed at encouraging plant-based eating. In India, a significant portion of the population identifies as vegetarian, which naturally increases the demand for alternative proteins and plant-based foods, while urban consumers demonstrate a strong preference for healthier protein options. Similarly, in China, heightened health awareness has led to high levels of plant-protein consumption, with a majority of consumers actively incorporating plant-based proteins into their diets. Non-governmental organizations (NGO), such as the Good Food Fund in China, along with international bodies advocating for plant-based food systems, further underscore the societal shift toward reducing animal product consumption and increasing plant protein intake. These developments highlight the growing recognition of plant-based diets as a means to address health, sustainability, and ethical concerns, positioning spirulina extract as a vital component in meeting the evolving dietary preferences of consumers across the region.

Government and institutional initiatives in several Asia-Pacific countries

Governments are actively supporting the microalgae industry by providing critical infrastructure, research funding, and policy frameworks to mitigate risks for private investors and drive market growth. In India, NITI Aayog has introduced a comprehensive strategy for seaweed and microalgae, while organizations like the Department of Biotechnology-TERI Centre of Excellence and BIRAC are advancing spirulina-based products, including fortified foods and nutraceuticals. Similarly, China's Ministry of Agriculture has incorporated spirulina into its official feed catalog, legitimizing its use in aquaculture and poultry feed and creating a significant demand channel for lower-grade spirulina biomass that does not meet food or pharmaceutical standards. Moreover, Indonesia, the leading global seaweed producer with a 2024 output of 10.80 million tonnes, is focusing on strengthening seaweed and microalgae value chains [2]Source: British Chamber of Commerce in Indonesia, "Indonesia Prioritizes Seaweed Amidst Surging Global Demand", britcham.or.id. The upcoming mandatory halal certification for food products, effective from October 2026, presents both compliance challenges and market opportunities for certified spirulina extract producers. These initiatives collectively reduce cultivation risks, enhance technical quality control, and improve access to essential resources such as land, water, and financing for small and medium-scale producers. Over the long term, government-backed research consortia are expected to play a pivotal role in improving strain selection, optimizing cultivation protocols tailored to local climatic conditions, and developing advanced extraction technologies. These advancements aim to boost phycocyanin yields and lower production costs, further solidifying the market's growth trajectory and fostering innovation across the microalgae sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain inconsistencies and contamination risks | -1.5% | Regional, acute in China, India, Indonesia | Short term (≤ 2 years) |

| Fragmented heavy-metal regulations across Asia-Pacific | -1.2% | Regionwide, export-oriented producers most affected | Medium term (2-4 years) |

| Formulation challenges in cosmetics/supplements | -0.9% | Japan, South Korea, Australia | Short term (≤ 2 years) |

| Limited local research and development | -0.7% | Indonesia, Thailand, Rest of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply chain inconsistencies and contamination risks

Contamination risks from heavy metals such as arsenic, lead, cadmium, and mercury, along with microcystin toxins, continue to present significant quality control challenges, constraining market growth and driving up compliance costs for producers. Spirulina's propensity to bioaccumulate heavy metals from cultivation water, combined with co-contamination risks from toxic cyanobacteria strains, necessitates rigorous testing protocols, particularly for pharmaceutical, infant, and export markets. The U.S. FDA mandates strict specifications for spirulina extracts, including lead ≤2 mg/kg, arsenic ≤2 mg/kg, mercury ≤1 mg/kg, and negative microcystin tests [3]Source: Electronic Code of Federal Regulations (eCFR), "§ 73.1530 Spirulina Extract", ecfr.gov. However, many small-scale producers, especially in the Asia-Pacific region, face difficulties meeting these standards due to limited laboratory infrastructure and inconsistent water quality. Contamination incidents can result in batch rejections, export bans, and reputational damage, as evidenced by periodic import alerts on spirulina products in developed markets. Supply chain inefficiencies, stemming from fragmented cultivation practices, inadequate traceability systems, and insufficient cold-chain logistics, further exacerbate quality variability and increase the risk of product degradation during storage and transport. Larger producers with vertically integrated operations and certifications such as ISO 22000 or FSSC 22000 are better positioned to ensure batch-to-batch consistency and full traceability, enabling them to command premium pricing. However, these capabilities remain concentrated among a minority of regional players. Addressing these contamination risks requires substantial investments in closed photobioreactor systems, water purification technologies, analytical testing equipment, and workforce training. For small and medium enterprises, these capital expenditures are often prohibitive, limiting their ability to compete and slowing market expansion in price-sensitive segments.

Fragmented heavy-metal regulations across Asia-Pacific

Spirulina extract producers face significant compliance challenges and market-access barriers due to regulatory fragmentation across Asia-Pacific countries. Nations such as China, India, Japan, South Korea, Indonesia, Thailand, and Australia enforce distinct standards for spirulina and phycocyanin, including specific purity requirements, permissible uses, labeling guidelines, and testing protocols. This fragmented regulatory environment compels producers to navigate multiple frameworks and reformulate products to meet varying market demands. For example, India's Food Safety and Standards Authority (FSSAI) has established spirulina standards as a dietary supplement, while China's regulatory framework involves food additive approvals and health food filings, which include efficacy-component requirements and unsuitable-population declarations. Export-oriented producers face additional hurdles, such as adhering to the EU's Novel Food Regulation and the U.S. FDA's color additive listings, which often impose stricter purity thresholds or require comprehensive safety dossiers. These complexities increase time-to-market, inflate legal and testing costs, and disproportionately impact smaller producers lacking regulatory expertise. Efforts to harmonize regulations through ASEAN or other regional standards bodies remain in early stages, leaving producers to contend with a patchwork of rules that stifles cross-border trade and limits economies of scale. Until greater regulatory alignment is achieved, compliance challenges will continue to constrain growth opportunities for regional producers, particularly those pursuing export strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Organic Certification Drives Premium Positioning Despite Conventional Dominance

Conventional spirulina extract is projected to maintain a significant 77.93% share of the Asia-Pacific market in 2025, supported by cost efficiency, established supply chains, and adaptability for high-volume applications prioritizing affordability. Leading producers such as Yunnan Green A, Chenghai Paul, and Hainan DIC leverage advanced cultivation techniques and optimized production protocols to deliver consistent output at costs 30-50% lower than organic alternatives. This cost advantage ensures a steady supply for price-sensitive sectors, including animal feed and aquaculture, where spirulina is valued as a natural pigment and immune booster without the need for organic certification. Additionally, in mass-market supplements and industrial food colorants, conventional extracts meet demand for consistent quality at competitive pricing, allowing organic variants to focus on niche, premium markets.

Organic spirulina extract, while holding a smaller market share, is expected to grow at a compound annual growth rate (CAGR) of 12.22% through 2031. This growth is driven by increasing demand for certified products in supplements, functional foods, and cosmetics, where organic certification supports premium pricing and appeals to consumers seeking clean-label products. Certifications such as USDA Organic, EU Regulation 2018/848, and ASEAN's ACT Organic ensure compliance with stringent standards, enabling access to export markets and upscale retail channels. Companies like T Far East Bio-Tec Co., Ltd. (FEBICO) cater to this demand, positioning organic spirulina as a premium ingredient in high-end supplements and vegan functional products. This dual-market structure allows conventional spirulina to address bulk demand while organic spirulina captures growth in lifestyle-focused categories.

By Application: Cosmetics Surge Outpaces Food and Beverage's Volume Leadership

Food and beverage applications are expected to account for 34.91% of spirulina extract demand in 2025, driven by its dual functionality as a natural blue colorant and protein fortifier. These applications span dairy alternatives, beverages, confections, and ready-to-eat cereals, where clean-label preferences influence formulation decisions. For example, Givaudan Sense Colour's COLOR BLUE SPIRU WS10, a water-soluble liquid spirulina extract stabilized with glycerin, trehalose, and sodium citrate, meets regulatory and consumer requirements for transparency. Certified as Halal, Kosher, Non-GMO, and allergen-free, it provides vibrant blue hues for mass-market products. This demand base in food and beverage complements pharmaceutical and supplement uses, where spirulina's antioxidant, anti-inflammatory, and immunomodulatory properties support typical human doses of 1-2 grams per day, with tolerability up to 10 grams, enabling cross-category nutritional fortification strategies.

Animal feed applications further strengthen spirulina's market position by utilizing lower-grade biomass for natural pigmentation in aquaculture, poultry, and livestock, enhancing egg yolk color, fish skin vibrancy, and immune function. China's Ministry of Agriculture's endorsement of spirulina in its official feed catalogue has scaled its integration into conventional production chains, absorbing excess supply and stabilizing pricing for upstream innovations. Meanwhile, the cosmetics and personal care segment is projected to grow at a CAGR of 13.02% through 2031, driven by spirulina's phycocyanin content, which supports anti-aging and skin barrier formulations. Verified suppliers like Algatechnologies provide phycocyanin-rich extracts tailored for premium cosmetics, enabling brands to unify ingredient narratives across beauty-from-within supplements and topical products, further enhancing spirulina's versatility in the Asia-Pacific market.

Geography Analysis

China holds a commanding 41.07% share of the spirulina extract market in the Asia-Pacific region in 2025, driven by its large-scale cultivation infrastructure, cost-efficient production, and strong domestic demand across food, feed, and nutraceutical applications. Major production centers in Yunnan Province (Chenghai Lake), Hainan Island, and Inner Mongolia utilize alkaline lake environments, abundant sunlight, and established supply chains to achieve economies of scale. The Ministry of Agriculture's decision to include spirulina in China's official feed catalogue has significantly increased demand in the aquaculture and poultry sectors. Additionally, government support for biotechnology and natural product industries creates a favorable environment for capacity expansion and technological advancements.

India has emerged as a key production and export hub, led by E.I.D. Parry's vertically integrated operations in Tamil Nadu and supported by government initiatives such as NITI Aayog's seaweed and microalgae strategy, the Department of Biotechnology-TERI Centre of Excellence, and BIRAC's product development programs. In November 2024, Parry Nutraceuticals obtained certification for food and beverage applications, enabling the company to expand its market presence beyond supplements to include functional foods and natural colorants. India's cost advantages in labor and land, combined with FSSAI's regulatory framework for spirulina as a dietary supplement, position the country as a competitive supplier for both organic and conventional segments. However, challenges such as gaps in cold-chain logistics and analytical testing infrastructure continue to impact quality consistency and export growth.

South Korea is projected to be the fastest-growing market, with a 12.54% CAGR forecasted from 2026 to 2031. This growth is attributed to increasing health supplement consumption, the rise of K-beauty trends, and a strong consumer preference for plant-based and clean-label products. Spirulina's natural blue color, high protein content, and proven bioactivity align well with these trends, making it a sought-after ingredient in dietary supplements and cosmetics. Korean brands, known for their innovative use of ingredients and clinical validation, are driving this momentum. Meanwhile, Japan continues to exhibit stable demand, supported by DIC Corporation's long-standing spirulina operations and consumer familiarity with spirulina's health benefits, which are marketed based on nutritional density, antioxidant properties, and natural sourcing.

Regulatory Landscape

Regulation for spirulina extract in Asia-Pacific continues to be shaped by country-specific food additive and supplement frameworks, with additional influence from Codex and major export markets. In China, spirulina blue is governed under the National Food Safety Standard GB 1886.309-2020, which sets product requirements for food additive spirulina blue derived via aqueous extraction. South Korea regulates spirulina-related products under the Health Functional Food Code administered by the Ministry of Food and Drug Safety (MFDS), aligning manufacturing and compositional expectations with the Health Functional Food Act.\n\nCross-border compliance is complicated by contamination controls and differing use-permissions, which pushes suppliers toward multi-standard dossiers for colorant and wellness applications. Internationally, JECFA (95th meeting, 2022) assigned spirulina extract (INS 134) an ADI \"not specified\" and its inclusion in the Codex GSFA provides a reference point for member markets. Regional coordination also gained visibility in June 2026, when MFDS, as chair of the Asia-Pacific Food Regulatory Authority Summit (APFRAS), issued the APFRAS Seoul 2026 Declaration aimed at advancing food regulatory harmonisation, a step that can reduce friction for spirulina-derived colorants and functional ingredients traded across the region.

Value Chain Analysis

The Asia-Pacific spirulina extract value chain spans upstream cultivation (open-pond raceways for cost-advantaged biomass and closed photobioreactors for tighter purity control), followed by harvesting, aqueous extraction, purification, concentration, and stabilization into liquid or powder formats for B2B ingredient supply. China remains a major integrated production base, supported by large-scale cultivation clusters and processors that convert biomass into higher-value extracts, while India has developed export-oriented, vertically integrated models centered on traceability and certification for nutraceutical and food-grade markets (for example, Parry Nutraceuticals operations and certification-driven positioning).\n\nMidstream processing and downstream distribution are strongly shaped by food-safety and contaminant specifications, which increase the need for in-house or partner laboratory testing, quality systems, and documentation aligned to multiple destination-market standards. Export exposure makes suppliers sensitive to changes in major reference markets, highlighted by the U.S. FDA action in March 2026 to delay the effective date of a February 2026 final order on expanded use of spirulina extract as a color additive due to objections and hearing requests. This reinforces the role of regulatory monitoring, application support (stability in beverages, dairy alternatives, and cosmetics), and multi-channel logistics (ingredient distributors, contract manufacturers, and direct-to-brand supply) as key value chain differentiators.

Competitive Landscape

The spirulina extract market in the Asia-Pacific region is moderately fragmented, with multinational ingredient suppliers and regional specialists competing through distinct strengths. Multinational companies such as DIC Corporation, Sensient Technologies, and Givaudan (post-Naturex acquisition) leverage global distribution networks and technical expertise to ensure consistent quality and regulatory compliance. Their diversified natural-color portfolios enable seamless integration of spirulina extract into premium applications, addressing high-end demands. Meanwhile, regional specialists like E.I.D. Parry (India), Zhejiang Binmei, Yunnan Green A, Fuqing King Dnarmsa, and Cyanotech capitalize on proximity to cultivation sites, lower production costs, and local regulatory knowledge to secure bulk supply contracts and cater to price-sensitive segments.

Vertical integration strategies are pivotal for both multinational and regional players, enabling control over quality and costs while meeting application-specific needs such as heat-stable phycocyanin for beverages. Capacity expansions in China and India by companies like Yunnan Green A and E.I.D. Parry enhances supply reliability and supports the transition from raw biomass to value-added extracts, reducing dependency risks. Technological advancements, including microencapsulation for improved stability in cosmetics and beverages, further drive innovation. For instance, Cyanotech’s phycocyanin developments enhance shelf-life and bioavailability, supporting diverse end-use applications.

Collaborative partnerships between suppliers and food and cosmetics brands are central to market strategies. Multinationals like Givaudan work with regional players to develop tailored phycocyanin blends, combining global research and development expertise with local sourcing efficiencies. Similarly, Novonesis' alliances with Asia-Pacific beauty firms for spirulina-based actives link advancements in extraction purity to brand-specific formulations, driving adoption in cosmetics while stabilizing food colorant volumes. These strategic moves, including DIC Corporation’s heat-stable offerings, expand spirulina’s applications from conventional feeds to premium functional products, sustaining innovation and moderate fragmentation in the market.

Asia-Pacific Spirulina Extract Industry Leaders

-

DIC Corporation

-

Fuqing King Dnarmsa Spirulina Co. Ltd.

-

E.I.D. Parry (India) Ltd.

-

Zhejiang Binmei Biotechnology Co. Ltd.

-

Sensient Technologies Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and new cultivation hubs across Asia-Pacific create whitespace for ingredient suppliers that can consistently deliver phycocyanin-rich extracts meeting food, beverage, and cosmetics specifications. Vietnam provides a clear proof point: US Vietnam Algae Technology JSC completed phase one of a Bao Loc spirulina cultivation facility (240-tonne annual capacity) and structured a second phase to add capacity, illustrating how new regional supply nodes can support local and export demand for clean-label blue colorants and protein fortification. China also shows continued cultivation scaling into non-traditional land bases, with DXN Corporation (Ningxia) Co., Ltd. reporting operations at a 1,000 mu production base in Ningxia with annual output of 200 tonnes of spirulina powder, supporting a broader feedstock pool for downstream extraction.\n\nNear-term commercial opportunities are concentrated where regulatory complexity and quality risks screen out smaller suppliers, elevating the value of vertically integrated production, validated contaminant control, and multi-certification portfolios for cross-border trade. Indonesia is another demand-side catalyst through government interest in marine biopharmaceuticals and the upcoming mandatory halal certification for food products effective October 2026, which creates packaging, auditing, and certification demand for compliant spirulina extract inputs used in functional foods and nutraceuticals. In parallel, early-stage scaling in India, such as Novalgae Private Limited's seed funding to expand community spirulina farming in Ballari District, points to local sourcing models that can supply cost-competitive biomass while building traceability and inclusion narratives for consumer brands.

Recent Industry Developments

- June 2026: Outbound shipments of phycocyanin powder to D.D. Williamson Colors, LLC were recorded, highlighting continued cross-border supply into the natural colors value chain. Fuqing King Dnarmsa Spirulina Co. Ltd. reported batch-level consistency and export documentation readiness that support color formulators in beverages and foods. The development underscores the role of established Chinese producers in maintaining upstream supply for multi-market color applications.

- May 2026: E.I.D. Parry (India) Ltd. announced a Disciplined Renewal plan for FY 2026-27, focusing on margin improvement through sharpened portfolio and channel strategies across nutraceuticals including organic spirulina. The initiative signals tighter prioritization of high-value applications and customer segments within spirulina offerings. The plan reinforces the importance of a vertically integrated, compliance-ready supply to serve food, beverage, and wellness formulations.

- March 2025: DIC Corporation reported that its subsidiary Earthrise Nutritionals, LLC commenced operations at a new edible algae cultivation facility in California, supported by an investment of about JPY 1.2 billion to expand production of Spirulina and the natural blue colorant LINABLUE. The added cultivation footprint strengthens supply availability for natural blue solutions used in beverage and food applications. It also raises competitive pressure on regional suppliers by improving scale and consistency at the upstream stage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers sales of spirulina extract ingredients used in food and beverage, supplements, cosmetics and personal care, and feed uses across Asia-Pacific. The sizing is captured in value terms, reflecting regional demand and trade flows for spirulina-derived extracts.

Scope exclusions: Whole spirulina biomass products sold as powders, tablets, or capsules without an extract claim are excluded from this market size.

Segmentation Overview

-

By Nature

- Organic

- Conventional

-

By Application

- Food and Beverage

- Pharmaceutical and Supplements

- Animal Feed

- Cosmetics and Personal Care

- Others

-

By Country

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure for the model and to pin down the Asia-Pacific footprint by end use and country coverage. We leaned on public sources such as national customs portals and UN Comtrade for trade direction checks, FAO for aquaculture and agriculture context, and government food regulator portals for allowed-use and labeling cues around natural colors and supplements.

To avoid relying on one single data stream, the desk work was also supported with company annual reports, investor presentations, association websites, and reported capacity or facility news in reputed press. Where needed, we used paid subscription sources covering company financials and shipment-level import and export data to cross-check volumes and price points in a practical way. These desk research sources are illustrative, and many other public references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating what portion of spirulina extract demand is actually ingredient-led (versus broader spirulina products) and how pricing shifts by application, purity, and certification. We interviewed and surveyed extract suppliers, ingredient distributors, brand-side procurement teams, and formulators across key Asia-Pacific markets, so assumptions could be corrected where desk signals were incomplete.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 34% | |

| Smaller Players: 15% | Managers: 54% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic. From the top-down side, we reconstructed an addressable demand pool by country using application-level adoption signals for spirulina extracts, then applied pricing bands that reflect purity and certification mix before rolling results up to the region.

Those totals were checked using selective bottom-up approximations, such as sampling supplier and distributor revenues where disclosures exist, using channel feedback to sanity-check how much extract is moving into supplements versus food and beverage, and testing implied average selling prices against traded-value ranges. When bottom-up information was missing for smaller markets, we handled the gaps through proxy penetration assumptions anchored to similar countries, then corrected through primary feedback.

For forecasts, scenario analysis was used so expected growth could flex with demand swings in natural colors, supplement launches, and new extraction capacity coming online. Key inputs tracked included phycocyanin and other pigment demand in beverages and dairy alternatives, supplement category growth, organic versus conventional mix, import dependence versus local cultivation, and observed pricing progression by grade and application.

Data Validation & Update Cycle

Validation was done through triangulation across three angles: demand indicators, trade and capacity signals, and what interviewees reported as real purchasing patterns. Outliers were flagged when country totals implied unrealistic per capita consumption, or when price and volume movement did not line up with known product-grade shifts, and then the assumptions were reworked.

Before sign-off, the full model and its drivers were reviewed in steps so calculation errors and inconsistent logic could be caught early. Reports are refreshed annually, and interim updates are made when a material event occurs, such as a major capacity addition or a regulatory change that affects use in foods. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Asia Pacific Spirulina Extract Market Size Versus Other Published Estimates

Published market sizes for Asia-Pacific spirulina extract often do not match because the term extract gets used differently, and because firms apply different year anchors, pricing ladders, and country coverage cutoffs. Differences also come from whether numbers are framed around ingredient trade value, finished-goods retail value, or a mixed approach.

Whole spirulina powders and tablets sit outside Mordor Intelligence's scope here, which removes a large finished-product layer that some estimates appear to blend into extract totals. Other gaps usually come from using aggressive price escalation for high-purity pigments, extending forecasts with limited checks on capacity additions, and applying a single regional average price across very different application mixes and import reliance levels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 249.37 M (2026) | |

| Global Consultancy A | USD 342.80 M (2026) | The estimate appears to use a broader product set and may include more finished-format spirulina products alongside extracts, and it also carries a wider price-upside assumption across the region without fully separating application-grade mix. |

| Industry Research Publisher B | USD 275.00 B (2023) | The published value is orders of magnitude higher, which strongly suggests it is not limited to extract ingredients and likely blends retail-level finished goods or adjacent nutrition categories, plus it uses a different base year and unit scale. |

Taken together, the spread is best explained by scope and unit consistency first, then by how prices and application mix are treated over time. By tying the model back to country demand cues, traded-value checks, and interview-led price bands, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

How large will Asia-Pacific spirulina extract revenues be by 2031?

The Asia-Pacific spirulina extract market is projected to reach USD 436.12 million by 2031, reflecting a 11.83% CAGR.

Which application is growing the fastest across the region?

Cosmetics and personal care lead growth at a 13.02% CAGR through 2031, fueled by phycocyanin’s anti-aging and hydration benefits.

Which country delivers the highest growth rate?

South Korea shows the fastest expansion, registering a 12.54% CAGR on the back of strong supplement uptake and K-beauty innovation.

Why are manufacturers shifting toward organic spirulina?

Certified organic spirulina secures export access and commands 50-100% retail premiums, driving a 12.22% CAGR despite higher production costs.

Page last updated on: