Tomato Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tomato Powder Market Analysis by Mordor Intelligence

The tomato powder market size is expected to grow from USD 1.61 billion in 2025 to USD 1.71 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at 6.02% CAGR over 2026-2031. This growth is primarily driven by its extensive use in processed foods such as soups, sauces, seasonings, and ready-to-eat meals. Additionally, the longer shelf life and ease of storage compared to fresh tomatoes make it a preferred choice for both manufacturers and consumers. Food manufacturers are increasingly incorporating tomato powder as a natural flavoring and coloring agent, aligning with clean-label trends. Furthermore, the growth of the foodservice industry and expansion of packaged food sectors are contributing to higher consumption levels. Emerging markets are also playing a key role, driven by urbanization and rising disposable incomes. Overall, the market is expected to witness sustained growth, supported by product innovation and expanding application areas.

Key Report Takeaways

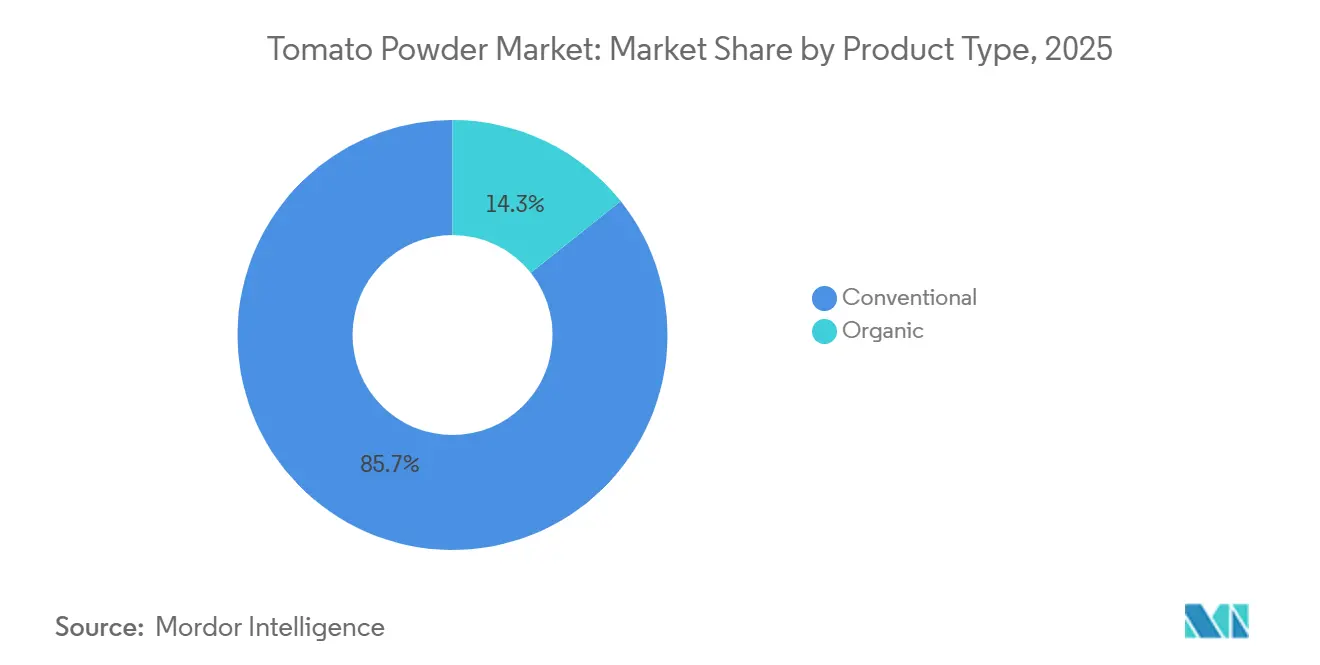

- By product type, conventional powder led with 85.71% tomato powder market share in 2025; the organic segment is advancing at an 8.46% CAGR through 2031.

- By process technology, spray-drying captured 69.97% of tomato powder market share in 2025, while freeze-drying is projected to expand at a 7.21% CAGR to 2031.

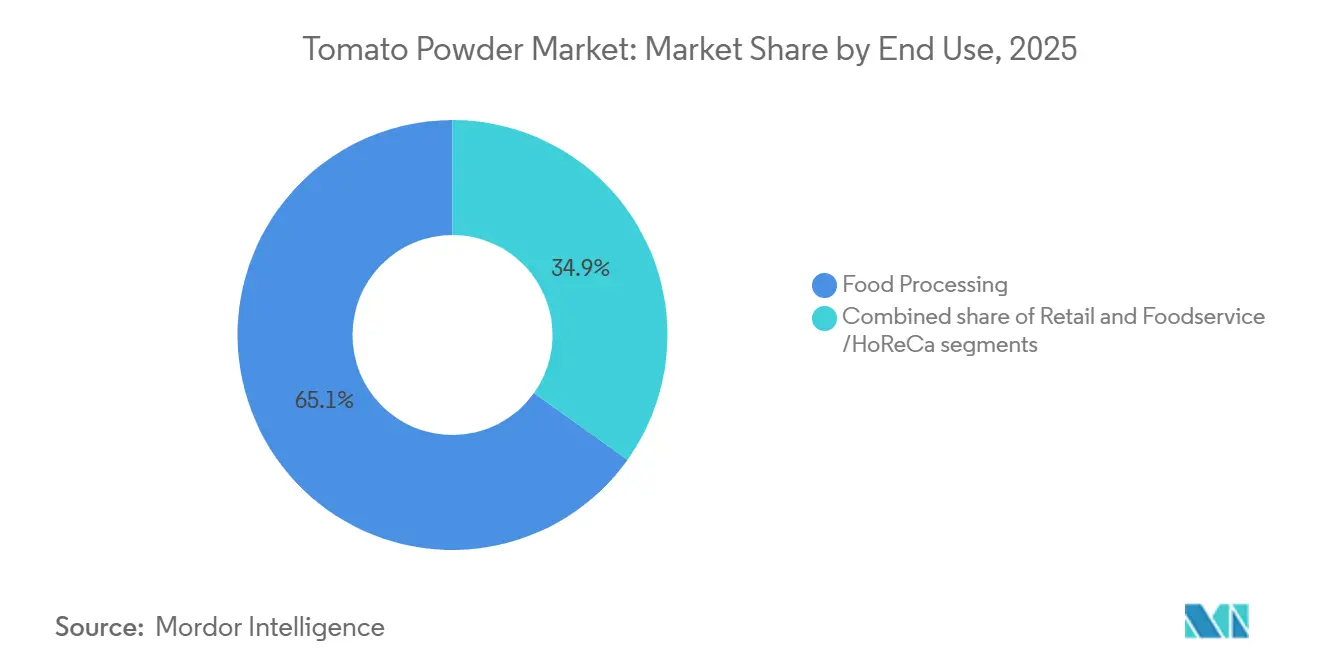

- By end use, food processing held 65.13% tomato powder market size in 2025 and the retail segment is expanding at a 7.22% CAGR over 2026-2031.

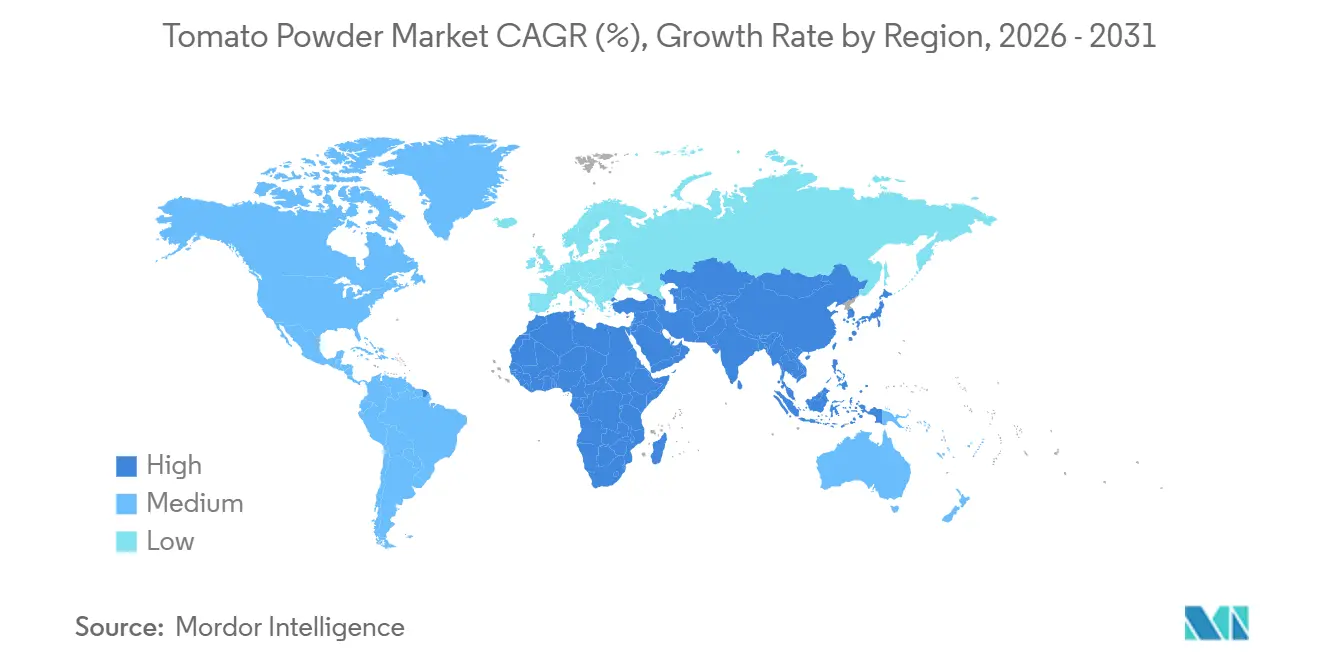

- By geography, Europe commanded 35.65% of the 2025 tomato powder market size, whereas the Middle East and Africa region is advancing at a 7.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tomato Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label and natural food ingredients | +1.2% | Global, with early concentration in North America and Western Europe | Medium term (2-4 years) |

| Increasing consumption of ready-to-eat and convenience foods | +1.5% | Global, led by Asia-Pacific urban centers and North America | Short term (≤ 2 years) |

| Technological advancements in drying and dehydration processes | +0.8% | North America, Europe, and advanced Asia-Pacific facilities (Japan, South Korea) | Long term (≥ 4 years) |

| Surging demand for shelf-stable and long-lasting food ingredients | +1.0% | Global, with accelerated adoption in Middle East, Africa, and food-insecure regions | Medium term (2-4 years) |

| Growing focus on food waste reduction and efficient ingredient utilization | +0.7% | North America and Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of the food processing industry | +1.3% | Middle East and Africa, Asia-Pacific core, spill-over to South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label and natural food ingredients

The rising demand for clean-label and natural food ingredients is a key factor driving the growth of the tomato powder market globally. Consumers are increasingly seeking products with simple, transparent ingredient lists, free from artificial additives, preservatives, and synthetic colors, which positions tomato powder as a favorable natural alternative. Derived from dehydrated tomatoes, it offers a clean-label solution for flavoring, coloring, and nutritional enhancement across various food applications. This shift is particularly evident in processed and convenience foods, where manufacturers are reformulating products to meet evolving consumer expectations. According to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to account for over 70% of product portfolios in 2025 and 2026, up from 52% in 2021, highlighting the rapid transition toward natural ingredients[1]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities”, cbi.eu. According to Kerry Nutrition Report 2025, 50% of Brazilian consumer's preferred natural ingredients[2]Source: Kerry, “Sustainable Nutrition in LATAM: Consumer Insights from Mexico & Brazil”, kerry.com. This growing preference is encouraging food producers to replace artificial tomato-based additives with powdered forms. As a result, tomato powder is gaining traction as a versatile, shelf-stable, and label-friendly ingredient across global markets.

Increasing consumption of ready-to-eat and convenience foods

The growing demand for ready-to-eat and convenience food products is significantly contributing to the expansion of the tomato powder market. As busy lifestyles and increasing urbanization drive the need for quick and easy meal solutions, consumers are relying more on packaged and instant food options. Tomato powder is widely utilized in these products due to its extended shelf life, ease of handling, and ability to quickly reconstitute while maintaining flavor and color. It is commonly incorporated into instant soups, sauces, snack seasonings, and prepared meals, enhancing both taste and visual appeal. Moreover, manufacturers favor tomato powder as it simplifies storage and transportation compared to fresh tomatoes, reducing overall operational costs. The rising popularity of convenience foods across global markets is therefore boosting its demand. Consequently, tomato powder continues to gain importance as a versatile and efficient ingredient in modern food processing.

Technological advancements in drying and dehydration processes

Technological advancements in drying and dehydration processes are significantly driving the growth of the tomato powder market. Innovations such as spray drying, freeze drying, and vacuum drying have improved the efficiency of production while preserving the natural color, flavor, and nutritional content of tomatoes. These advanced techniques enable manufacturers to produce high-quality tomato powder with better solubility, longer shelf life, and enhanced stability. Additionally, modern processing technologies help minimize nutrient loss, particularly vitamins and antioxidants like lycopene, thereby increasing the product’s functional value. Improved drying methods also allow for consistent particle size and quality, which is crucial for large-scale food manufacturing applications. Furthermore, automation and energy-efficient technologies are reducing production costs and improving scalability. As a result, these technological developments are encouraging wider adoption of tomato powder across the global food industry.

Surging demand for shelf-stable and long-lasting food ingredients

The increasing preference for shelf-stable and long-lasting food ingredients is significantly boosting the demand for tomato powder in the global market. With a growing focus on reducing food waste and ensuring product longevity, both consumers and manufacturers are shifting toward ingredients that offer extended usability without compromising quality. Tomato powder, due to its low moisture content, provides excellent stability and minimizes the risk of microbial spoilage, making it an efficient substitute for fresh tomatoes. It can be stored for longer durations without the need for refrigeration, which enhances its suitability for processed and packaged food products. Additionally, it maintains consistent flavor, color, and nutritional value over time, supporting its use in applications such as soups, sauces, and snack seasonings. The rising need for durable ingredients in bulk storage and international trade further supports its adoption. Consequently, tomato powder is gaining traction as a dependable and cost-effective solution in modern food processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in raw tomato prices and seasonal supply instability | -0.6% | Global, acute in California, China, Mediterranean Europe | Short term (≤ 2 years) |

| High production and processing costs (drying technologies, equipment) | -0.4% | Europe (energy-intensive regions), North America | Medium term (2-4 years) |

| Quality consistency challenges due to variability in raw materials | -0.2% | Global, particularly in regions with fragmented smallholder supply | Medium term (2-4 years) |

| Stringent food safety and regulatory compliance requirements | -0.3% | Europe (EU Regulation 2018/848), North America (FDA, USDA), emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in raw tomato prices and seasonal supply instability

Fluctuations in raw tomato prices and seasonal supply instability represent a significant restraint for the tomato powder market. The availability and cost of processing tomatoes are highly dependent on climatic conditions, agricultural inputs, and regional production dynamics, leading to inconsistent supply and pricing volatility. For instance, California processing-tomato acreage contracted to 9.25 million tons in 2025, reflecting an 11% decline from 10.25 million tons in 2024, indicating tightening raw material availability[3]Source: United States Department of Agriculture, “PUTTING AMERICAN FARMERS FIRST”, usda.gov. Furthermore, projections for 2026 suggest that planted area may fall below 200,000 acres for the first time in five decades, driven by water allocation restrictions, labor shortages, and a shift of growers toward more profitable crops such as tree nuts. These structural challenges directly impact the cost of raw tomatoes used in powder production. As a result, manufacturers face margin pressures and potential disruptions in supply continuity. This volatility makes long-term pricing strategies and production planning increasingly complex for industry participants.

High production and processing costs (drying technologies, equipment)

High production and processing costs associated with advanced drying technologies and specialized equipment act as a significant restraint on the tomato powder market. The manufacturing process requires capital-intensive methods such as spray drying, freeze drying, and vacuum drying, which involve substantial investment in machinery and energy consumption. Additionally, maintaining optimal processing conditions to preserve color, flavor, and nutritional value increases operational complexity and costs. Small and medium-scale manufacturers often face challenges in adopting these technologies due to high initial capital requirements. Energy price fluctuations further add to production expenses, particularly in regions with high utility costs. Moreover, the need for skilled labor and regular equipment maintenance contributes to overall cost burdens. These factors collectively impact profit margins and can limit market entry and expansion for new players in the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conventional Dominance Meets Organic Acceleration

Conventional tomato powder held the dominant position in the market in 2025, accounting for 85.71% of the total market share. This strong presence is largely attributed to its cost-effectiveness and widespread availability across global markets. Food manufacturers prefer conventional variants due to their consistent quality, stable supply, and suitability for large-scale production. The segment is extensively used in processed foods such as sauces, soups, snacks, and ready-to-eat meals, where pricing and bulk usage are key considerations. Additionally, well-established supply chains and large-scale tomato cultivation support the continued dominance of conventional products. Its versatility as a flavoring and coloring agent further enhances its adoption across both food processing and foodservice industries.

The organic tomato powder segment is projected to be the fastest-growing category, expanding at a CAGR of 8.46% through 2031. This growth is driven by increasing consumer awareness regarding health, sustainability, and clean-label food products. Consumers are increasingly seeking organic alternatives that are free from synthetic pesticides, fertilizers, and additives. As a result, food manufacturers are incorporating organic tomato powder into premium product lines to cater to this growing demand. The segment is also benefiting from the expansion of organic food retail channels and certifications that build consumer trust. Additionally, rising disposable incomes and a shift toward healthier dietary habits are further supporting its growth.

By Process Technology: Spray-Drying Scale Versus Freeze-Drying Quality

Spray-drying dominated the tomato powder market in 2025, accounting for 69.97% of the total market share. This leadership is primarily due to its cost efficiency and suitability for large-scale production. The process allows manufacturers to convert liquid tomato extracts into fine powder quickly, ensuring high productivity and consistent output. Spray-dried tomato powder is widely used in processed foods such as soups, sauces, snacks, and seasonings due to its uniform texture and ease of blending. Additionally, the technology supports extended shelf life and stable storage, making it highly practical for bulk applications. Its established industrial adoption and lower production costs continue to reinforce its dominance in the global market.

Freeze-drying is expected to be the fastest-growing process technology segment, expanding at a CAGR of 7.21% through 2031. This growth is driven by its ability to preserve the natural color, flavor, and nutritional value of tomatoes more effectively than conventional methods. The process involves removing moisture at low temperatures, which helps retain product quality and enhances rehydration properties. As consumer demand for premium and clean-label products increases, manufacturers are increasingly adopting freeze-drying for high-quality applications. The technology is particularly popular in health-focused and specialty food segments, where product integrity is critical. Although it is more expensive than spray-drying, its superior quality output is attracting growing interest.

By End Use: Food Processing Anchors Demand, Retail Channels Accelerate

The food processing segment dominated the tomato powder market in 2025, accounting for 65.13% of the total market size. This strong position is driven by the extensive use of tomato powder as a key ingredient in processed foods such as sauces, soups, ready meals, snacks, and seasonings. Manufacturers prefer tomato powder due to its long shelf life, ease of storage, and consistent flavor profile, which supports large-scale production. It also serves as a natural coloring and flavoring agent, aligning with clean-label trends in the food industry. Additionally, the growing demand for convenience and packaged foods has significantly increased its adoption among food processors. Established supply chains and bulk purchasing practices further strengthen the dominance of this segment.

The retail segment is projected to be the fastest-growing end-use category, expanding at a CAGR of 7.22% over the forecast period. This growth is fueled by rising consumer demand for convenient cooking ingredients and ready-to-use food products at home. Tomato powder is increasingly being purchased through supermarkets, online platforms, and specialty stores for household use. Its versatility in home cooking, including use in soups, curries, and seasoning blends, is driving consumer adoption. Additionally, increasing awareness of its longer shelf life and minimal wastage compared to fresh tomatoes is supporting demand. The expansion of e-commerce and availability of smaller, consumer-friendly packaging formats are also contributing to growth.

Geography Analysis

Europe held the largest share of the tomato powder market in 2025, accounting for 35.65% of the global market size. This dominance is supported by the region’s well-established food processing industry and high consumption of tomato-based products. Countries such as Italy, Spain, and Germany are key contributors, driven by strong culinary traditions that rely heavily on tomato ingredients. The demand for convenience foods, including ready meals, sauces, and soups, further boosts the use of tomato powder across the region. Additionally, increasing preference for clean-label and natural ingredients is encouraging manufacturers to adopt tomato powder as a natural flavoring and coloring agent. Advanced supply chains, strong retail networks, and high consumer awareness also contribute to sustained market leadership.

The Middle East and Africa region is projected to be the fastest-growing market, expanding at a CAGR of 7.31% through 2031. This growth is driven by rapid urbanization, rising disposable incomes, and increasing demand for processed and convenience foods. Tomato powder is gaining popularity due to its long shelf life and suitability for regions with limited cold storage infrastructure. The expanding foodservice sector, including restaurants and catering services, is also contributing to higher consumption levels. Additionally, population growth and changing dietary patterns are supporting demand for affordable and easy-to-use food ingredients. As distribution networks and retail infrastructure continue to develop, the region is expected to offer significant growth opportunities for market players.

North America and Asia-Pacific represent significant and steadily growing markets for tomato powder, supported by strong demand from both food processing and retail sectors. In North America, the market is driven by the widespread consumption of packaged and convenience foods, along with increasing demand for natural and clean-label ingredients. Asia-Pacific is witnessing rapid growth due to urbanization, expanding food processing industries, and rising adoption of Western-style diets in countries such as China and India. Meanwhile, South America is emerging as a promising market, supported by abundant tomato production and increasing exports of processed food products. Across these regions, the growth of e-commerce, product innovation, and expanding application areas are key factors driving market expansion.

Competitive Landscape

The tomato powder market exhibits fragmentation, with a mix of global ingredient manufacturers, regional processors, and numerous small- to medium-scale players operating across different geographies. While a few established companies hold notable positions due to their scale, technological capabilities, and distribution networks, a large portion of the market remains dispersed among regional suppliers. This fragmentation is largely driven by the widespread availability of raw materials, relatively low entry barriers, and the presence of local processing units in key tomato-producing regions. As a result, competition is intense, with players differentiating themselves based on pricing, quality, and product consistency. The market structure allows both large and small companies to coexist, catering to diverse customer needs across food processing and retail sectors.

Leading players such as Olam International, Ingredion Incorporated, and Kerry Group leverage their strong global presence, advanced processing technologies, and extensive product portfolios to maintain competitive advantage. These companies focus on large-scale production, consistent quality, and long-term supply agreements with food manufacturers. They also invest in research and development to improve product functionality, enhance flavor profiles, and align with clean-label trends. In addition, strategic partnerships, acquisitions, and expansion into emerging markets are common strategies adopted by these players to strengthen their market position.

At the same time, regional and local manufacturers play a significant role in shaping the competitive landscape by offering cost-effective solutions and catering to local demand. These players often benefit from proximity to raw material sources, enabling them to reduce production and transportation costs. Many small-scale producers also focus on niche segments such as organic or specialty tomato powders to differentiate themselves. Furthermore, the rise of private-label brands and increasing penetration of e-commerce platforms have intensified competition by improving market access for smaller companies. This dynamic environment encourages continuous innovation, pricing strategies, and product diversification, ensuring sustained competition and growth within the tomato powder market.

Tomato Powder Industry Leaders

Symrise AG

Kagome Co., Ltd.

Olam International Limited

Aarkay Food Products Ltd.

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Archer Daniels Midland Company announced a USD 26 million expansion at its Erlanger, Kentucky facility to enhance its flavor and color production capacity. This initiative aimed to support the company's brand reformulation efforts in compliance with clean-label mandates and sodium-reduction policies. The investment included the incorporation of advanced spray-drying and extraction technologies.

- March 2025: Symrise AG expanded its water-soluble ingredients portfolio through a partnership with Infusd Nutrition, enhancing its ability to deliver tomato-based natural colors and flavors in beverage and dairy applications. The collaboration leverages Infusd's proprietary encapsulation technology to improve bioavailability and sensory performance.

- January 2025: Agrofusion introduced its new Tomato Powder, Inagro, at Gulfood 2025. This product is made using advanced Filtermat technology, resulting in a rich, dark-red powder. According to the brand, it contains no anti-caking agents, providing a clean-label solution for premium formulations.

- December 2024: Kalsec Inc. broadened its reach in the Asia-Pacific savory category by expanding its exclusive distribution partnership with Connell Caldic in China. As part of this collaboration, Kalsec has set up a state-of-the-art application lab in Shanghai and brought on board technical experts to tailor food solutions. This agreement capitalizes on Caldic's deep-rooted local market knowledge and robust supply-chain infrastructure.

Global Tomato Powder Market Report Scope

Tomato powder is a dehydrated form of tomatoes, produced by removing the moisture content from fresh tomatoes through drying techniques such as spray drying, freeze-drying, or drum drying.The tomato powder market is segmented by product type, processing technology, end use and geography. Based on product type, the market is segmented into conventional and organic. By processing technology, the market is segmented into spray-dried, freeze-dried, vaccum-dried and others. By end use the market is segmented into foodprocessing, retail and foodservice. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Conventional |

| Organic |

| Spray-Dried |

| Freeze-Dried |

| Vacuum-Dried |

| Others (Sun-Dried, Drum Dried) |

| Food Processing | Soups and Sauces |

| Bakery and Snacks | |

| Seasonings and Flavors | |

| Ready Meals and Instant Mixes | |

| Others | |

| Foodservice/HoreCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Conventional | |

| Organic | ||

| By Process Technology | Spray-Dried | |

| Freeze-Dried | ||

| Vacuum-Dried | ||

| Others (Sun-Dried, Drum Dried) | ||

| By End Use | Food Processing | Soups and Sauces |

| Bakery and Snacks | ||

| Seasonings and Flavors | ||

| Ready Meals and Instant Mixes | ||

| Others | ||

| Foodservice/HoreCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the tomato powder market by 2031?

The tomato powder market is forecast to reach USD 2.29 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

It is projected to register a 6.02% CAGR during the 2026-2031 period.

Which region will record the highest growth rate?

The Middle East and Africa region is set to advance at the fastest 7.31% CAGR through 2031.

What share did conventional powder hold in 2025?

Conventional powder captured 85.71% of global consumption in 2025.

Which technology remains dominant in processing?

Spray-drying remains the leading technology, accounting for 69.97% of 2025 output thanks to scalability and cost efficiency.

Page last updated on: