Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

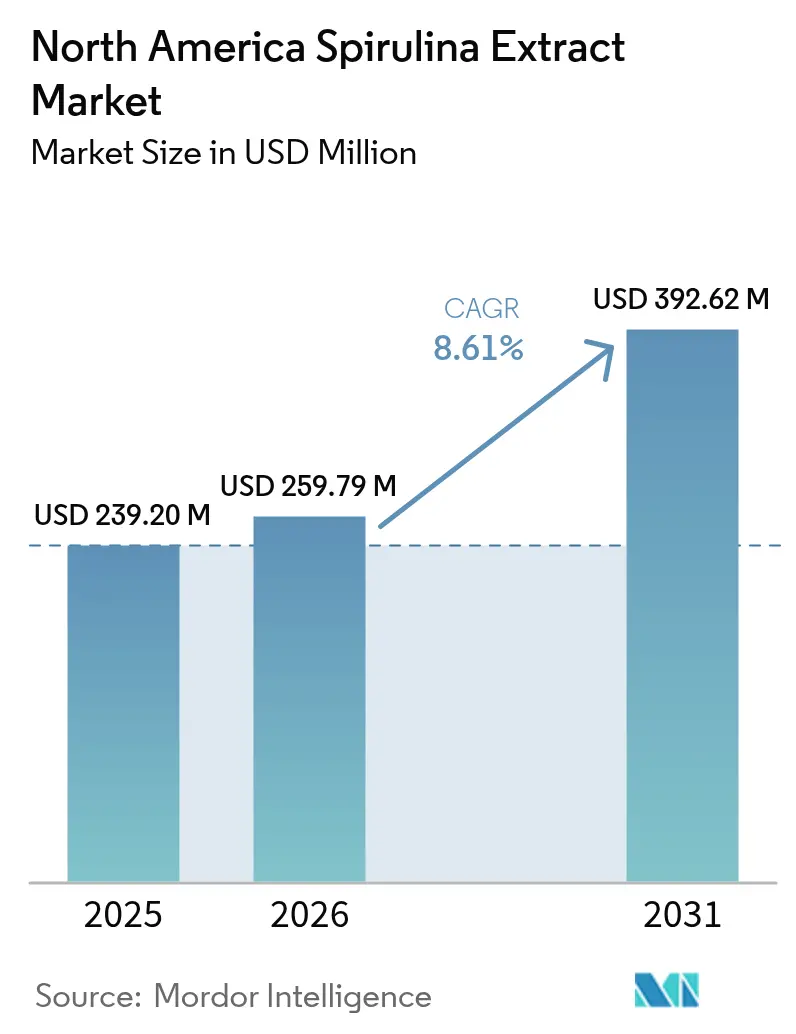

| Base Year Market Size (2025) | USD 239.20 Million |

| Market Size (2026) | USD 259.79 Million |

| Market Size (2031) | USD 392.62 Million |

| Growth Rate (2026 - 2031) | 8.61% CAGR |

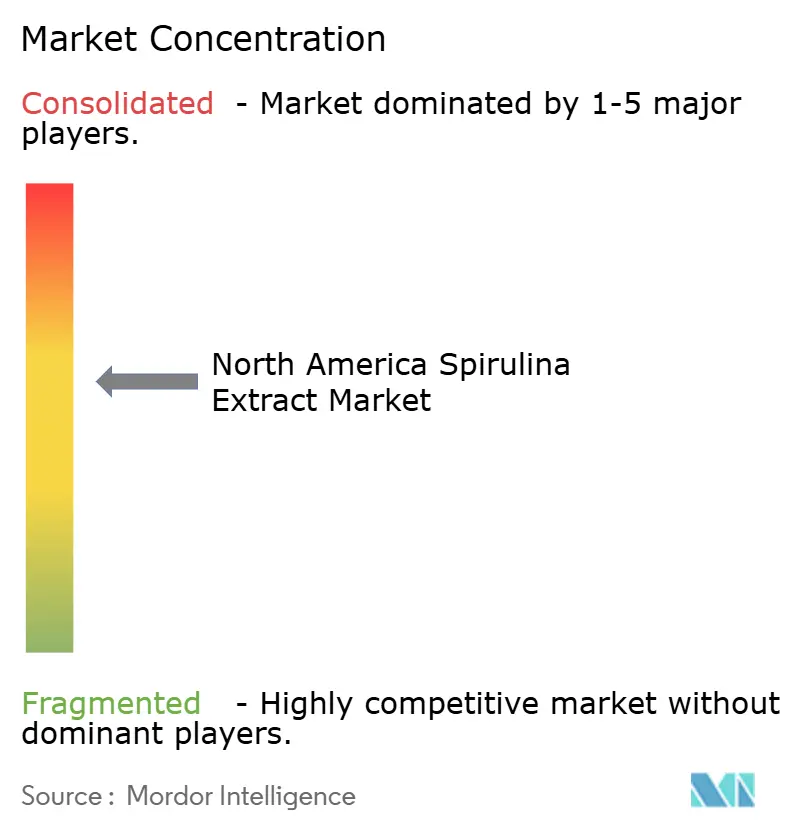

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Spirulina Extract Market Analysis by Mordor Intelligence

The spirulina ingredient market size in North America in 2026 is estimated at USD 259.79 million, growing from 2025 value of USD 239.20 million with 2031 projections showing USD 392.62 million, growing at 8.61% CAGR over 2026-2031. This growth path is anchored in spirulina’s dual roles as a vibrant natural colorant and a rich source of complete protein, aligning with the growing trend of plant-based eating habits. Formulators are adopting micro-algae to simplify ingredient decks, replace synthetic blues, and meet the rising demand for preventive health solutions. Regulatory approvals covering broader food categories, third-party safety verifications, and continuous process innovation jointly expand commercial headroom. At the same time, vertically integrated suppliers are scaling extraction technologies that lower unit costs and free up capacity for premium applications.

Key Report Takeaways

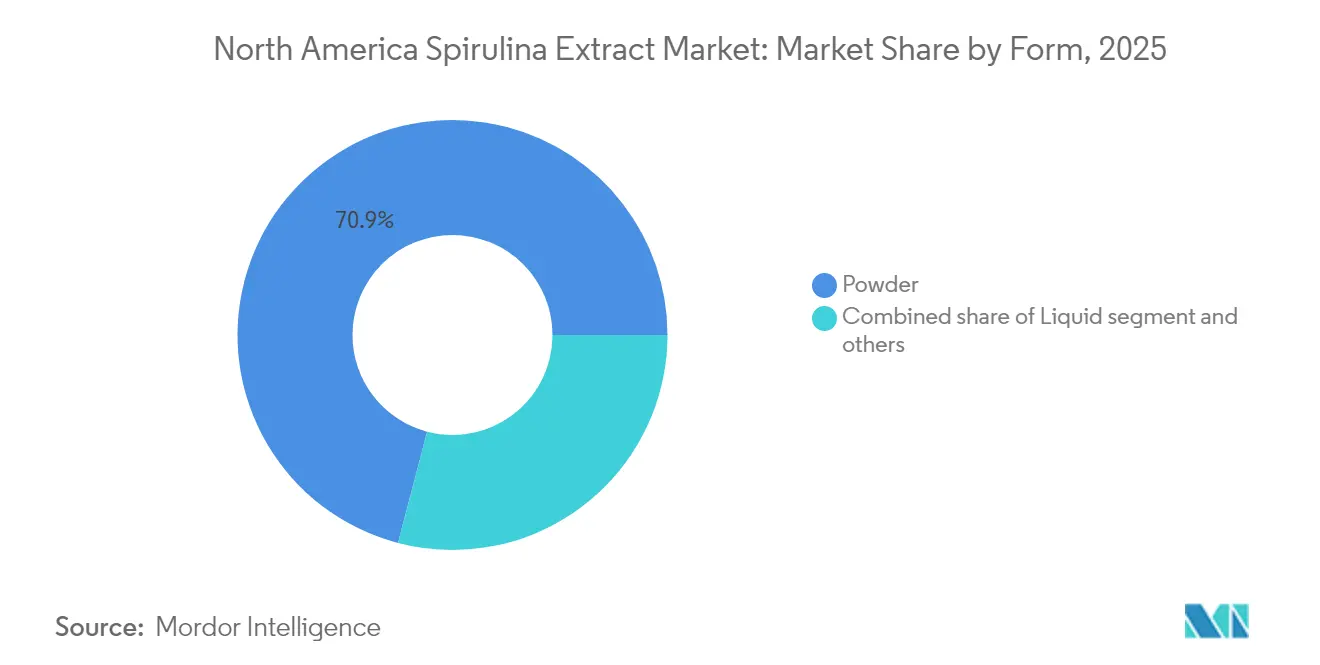

- By form, powder captured 70.92% of the spirulina ingredient market share in 2025, while liquid extracts are forecast to expand at a 10.65% CAGR to 2031.

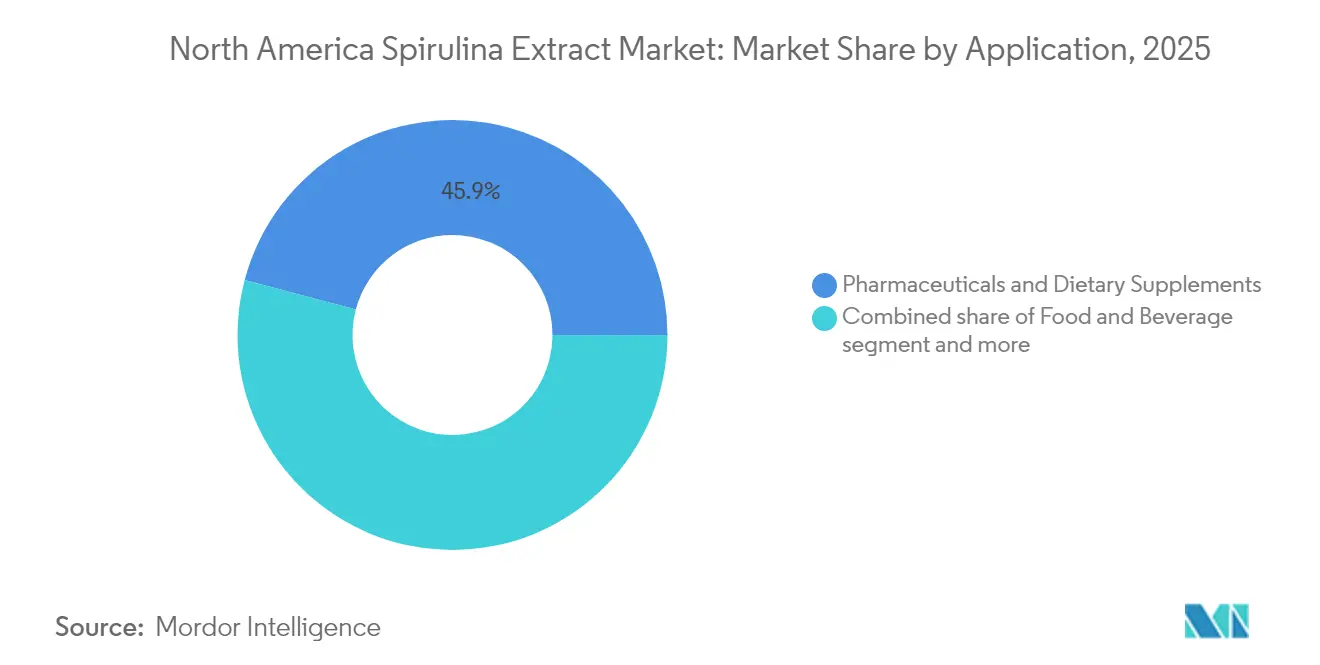

- By application, pharmaceuticals and dietary supplements held a 45.88% revenue share in 2025; the food and beverage sector is projected to advance at a 9.89% CAGR through 2031.

- By geography, the United States accounted for 78.02% of regional demand in 2025, whereas Mexico is projected to record the fastest growth of 9.44% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Spirulina Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use of spirulina in dietary supplements and functional foods | +1.8% | United States, Canada; emerging in Mexico | Medium term (2-4 years) |

| Expansion of clean-label and organic product formulations | +1.5% | United States, Canada | Short term (≤ 2 years) |

| Rising demand for plant-based and natural nutritional ingredients | +1.6% | North America-wide, strongest in urban US markets | Medium term (2-4 years) |

| Increasing consumer focus on preventive healthcare and immunity support | +1.4% | United States, Canada | Short term (≤ 2 years) |

| Advancements in spirulina cultivation and extraction technologies | +1.2% | United States (California, Hawaii production hubs) | Long term (≥ 4 years) |

| Favorable regulatory acceptance of spirulina-based ingredients | +1.0% | United States (FDA), Canada (CFIA) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Use of Spirulina in Dietary Supplements and Functional Foods

Spirulina’s high protein content (55–70% dry weight) makes it an efficient, sustainable source of amino acids, supporting the growing US organic supplement market, which reached USD 5.9 billion in 2023[1]Source: U.S. Department of Agriculture, “Organic Supplement Sales Data,” usda.gov. A 2025 meta-analysis confirmed the benefits for body composition, providing formulators with clinical evidence for labeling and marketing. E.I.D. Parry’s USP Dietary Ingredient Verification highlights the rising importance of third-party quality assurance, while Lonza’s 2025 Organicaps pullulan capsules enable fully organic spirulina supplements without gelatin, opening premium retail shelf space. The market is also shifting toward multi-ingredient blends that include ashwagandha, turmeric, or omega-3 fatty acids, thereby expanding overall volume despite the fragmentation of SKUs.

Expansion of Clean-Label and Organic Product Formulations

Clean-label trends are driving the growth of spirulina, whose single-ingredient profile provides transparency that synthetic colorants cannot. The FDA’s 2025 updates to the “healthy” claim and GNT USA’s 2022 approval for dairy alternatives and plant-based beverages position spirulina for front-of-pack nutrition messaging and 15–20% price premiums. Canada’s SFC traceability rules favor local producers with farm-to-facility documentation, limiting offshore imports. While organic certification adds USD 0.50–1.00/kg in costs, certified organic spirulina commands wholesale prices 40–60% higher, making it attractive for mid-sized premium brands.

Rising Demand for Plant-Based and Natural Nutritional Ingredients

Plant-based diets are driving demand for spirulina, valued for its complete amino acid profile and allergen-free properties. SimpliiGood’s 2025 launch of spirulina-based smoked salmon shows its potential in whole-food analogs, while its natural blue-green color is now a selling point in vibrant smoothies and functional beverages. In Mexico, the wellness food market grew 14.7% CAGR to USD 33.8 billion (2019–2023), with fortified foods gaining traction. Rising incomes and the Canada-Mexico Organic Equivalency Arrangement enable Canadian producers to expand spirulina-fortified products into Mexico without duplicative certification.

Increasing Consumer Focus on Preventive Healthcare and Immunity Support

Spirulina’s immunomodulatory benefits, driven by phycocyanin and polysaccharides, are becoming a key commercial selling point as consumers prioritize clinically supported immune ingredients. Its antioxidant activity, at phycocyanin levels of 10–15 g per 100 g biomass, supports claims of reducing oxidative stress, aligning with post-pandemic wellness trends. Spirulina’s Class A safety rating allows formulators to recommend higher daily doses (3–5 g) with regulatory confidence, setting it apart from newer botanicals that lack long-term safety data[2]Source: United States Pharmacopeia, “Verification Program Participants,” usp.org. Canada’s 2024 update to the Natural Health Product framework has shortened licensing timelines, enabling faster launches of immunity-focused blends during peak seasonal demand. However, substantiating structure-function claims remains a challenge, as the FDA requires NDI filings for novel extracts with concentrated phycocyanin, which can delay responses to trending formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and input-price volatility | -0.9% | United States (California, Hawaii), Canada | Short term (≤ 2 years) |

| Complex FDA/CFIA compliance for novel ingredients | -0.6% | United States, Canada | Medium term (2-4 years) |

| Taste, odor, and color challenges in food and beverage applications | -0.7% | North America-wide | Medium term (2-4 years) |

| Limited scalability of premium extraction technologies | -0.5% | United States (production hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Input-Price Volatility

Spirulina cultivation is energy- and cost-intensive, with fluctuations in electricity prices directly affecting margins. Open-pond systems in California benefit from sunlight but face rising water costs, while Hawaii’s Cyanotech facility contends with peak electricity rates exceeding USD 0.30/kWh. Nutrient inputs, such as sodium bicarbonate and nitrogen, are subject to commodity cycles; a 20% increase in bicarbonate can reduce gross margins by 3–5 points[3]Source: Cyanotech Corporation, “Investor Presentation Q3 FY2025,” cyanotech.com. Closed photobioreactors offer contamination control and year-round output but require USD 2–5 million per hectare, limiting access for smaller producers and concentrating production among integrated firms. Labor for harvesting, drying, and quality control accounts for 15–25% of costs, with wage inflation prompting producers to consider automation or margin erosion. The market is bifurcated between commodity powder (USD 8–12/kg) and pharmaceutical-grade extracts (USD 40–60/kg), forcing producers to focus on either volume or premium supply chains, which limits flexibility and exacerbates fluctuations in electricity prices.

Complex FDA/CFIA Compliance for Novel Ingredients

The FDA’s NDI pathway requires manufacturers of novel spirulina products, such as fermented spirulina, concentrated phycocyanin, or hydrolysates, to submit safety dossiers 75 days prior to launch, at a cost of USD 50,000-150,000 per ingredient. In Canada, CFIA licensing now includes GMP audits and site inspections, adding 6-12 months to development and requiring dedicated regulatory staff. Mexico’s COFEPRIS permits must be filed through a local entity, which can delay foreign launches by 12–18 months. Established spirulina powders benefit from GRAS status, while innovative extracts face stricter scrutiny, which slows market entry and favors incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominates, Liquid Extracts Gain in Beverages

Sensient’s March 2024 launch of a heat-stable spirulina ingredient is opening up high-temperature applications that were previously unavailable, including baked snacks and UHT beverages. In 2025, powder dominated the market with a 70.92% share, primarily due to its compatibility with tablets, capsules, and protein blends. In contrast, liquid extracts are projected to grow at a 10.65% CAGR through 2031, offering water-dispersible solutions that eliminate the gritty mouthfeel associated with powders. Tablets remain popular for dosing convenience, but demand is shifting toward capsules, especially pullulan-based organic options like Lonza’s 2025 Organicaps, that avoid gelatin and synthetic polymers. Fresh, texturized spirulina, exemplified by SimpliiGood’s 2025 smoked salmon analog, preserves heat-sensitive nutrients and delivers whole-food texture, appealing to flexitarian consumers.

Other innovative forms, including gummies, chews, and “candyceuticals,” are capturing younger consumers who prefer fun, convenient formats, though these require premium extracts with minimal off-flavors. Liquid spirulina products, such as YANGGE BIOTECH’s blue honey-like extract, target beverage manufacturers seeking natural blue colorants that comply with FDA 21 CFR 73.530 standards. While powder maintains volume leadership at USD 8–12/kg wholesale, liquid and fresh formats are carving out premium niches, commanding 2–3× price premiums due to superior sensory performance and clean-label appeal.

By Application: Pharma/Supplements Lead, Food/Beverage Accelerates

Pharmaceuticals and dietary supplements accounted for 45.88% of spirulina extract applications in 2025, driven by its USP Class A safety rating, clinical evidence supporting improvements in body composition, and compatibility with multi-nutrient blends targeting immunity, energy, and cognitive health. Food and beverage applications, although smaller in volume, are growing at a 9.89% CAGR through 2031, supported by the FDA’s 2022 approval, which expands the use of spirulina as a natural colorant in confections, ice cream, yogurt, cereals, and ready-to-drink beverages. This enables formulators to replace synthetic Blue 1 while adding protein and micronutrients. Animal feed applications, particularly in aquaculture and poultry, benefit from research showing improvements in growth performance and partial to full replacement of soybean meal, although adoption is largely limited to premium operations due to cost sensitivity.

Industrial applications, including cosmetics, biofuels, and biostimulants, remain niche but are attracting R&D investment as producers seek to monetize byproducts and improve biorefinery economics. For example, DIC Corporation’s investment in Back of the Yards Algae Sciences’ zero-waste platform demonstrates how extracting colorants, biostimulants, and heme analogs from the same biomass can diversify revenue streams. Overall, while supplements provide stable demand, the fastest growth is in food and beverage, where spirulina’s dual functionality, nutrition plus natural color, supports clean-label positioning. Regulatory clarity, such as FDA approval for specific coloring uses, is critical for market expansion, whereas animal feed growth remains constrained by inconsistent offshore quality and the lack of standardized dosing guidelines.

Geography Analysis

The United States dominated North America’s spirulina ingredient market in 2025, accounting for 78.02% of regional revenue. Key production hubs include California’s Earthrise facility (108 acres in Calipatria) and Hawaii’s Cyanotech operation (96 acres in Kona), both of which benefit from year-round sunlight, established supply chains, and proximity to downstream nutraceutical formulators in Southern California and the Pacific Northwest. Cyanotech reported Q3 FY2025 net sales of USD 6.172 million, up 10.6% year-over-year, reflecting strong demand from contract manufacturers for USP-verified, GMP-certified spirulina for private-label supplements and functional foods. The FDA’s 2022 approval, which expands the use of spirulina as a natural colorant in confections, ice cream, yogurt, cereals, and beverages, has further opened up margin-rich food and beverage applications. High production costs in California and Hawaii, driven by electricity (USD 0.15–0.30/kWh), labor, and environmental compliance, push producers to compete on quality, traceability, and regulatory alignment rather than price.

Canada’s spirulina market is shaped by CFIA regulations, which require site licensing, GMP audits, and product-specific approvals, adding 6–12 months to commercialization but creating a quality moat that protects compliant producers. The Canada Organic Regime (COR) mandates certification for organic spirulina, while the February 2023 Canada-Mexico Organic Equivalency Arrangement enables Canadian producers to access Mexico’s growing middle-class market without duplicative audits. Canada’s 2024 modernization of its self-care framework has accelerated Natural Health Product licensing, allowing faster launches of spirulina-based immunity blends to capitalize on seasonal demand peaks. Though smaller than US producers, Canadian companies such as C.B.N. Spirulina Canada Co. leverage regulatory alignment and proximity to US markets to serve cross-border supply chains for both organic and non-GMO formulations.

Mexico is the fastest-growing North American market, projected to expand at a 9.44% CAGR through 2031, supported by a health-and-wellness packaged food sector valued at USD 33.8 billion in 2023. Fortified and functional foods account for 30.4% of this market, creating opportunities for spirulina-fortified tortillas, protein bars, and beverages. Rising population and per capita income, alongside COFEPRIS regulations and NOM-051 labeling requirements, shape market entry, often favoring partnerships with US and Canadian producers. Currently, Mexico receives a significant portion of processed food exports from the US (65.2%), suggesting spirulina ingredients are largely imported through US-based formulators and contract manufacturers. Other North American regions, primarily Caribbean markets, remain limited in size due to low local production, high import costs, and nascent consumer awareness.

Competitive Landscape

The North American spirulina ingredient market is moderately concentrated, with the top five players being Cyanotech Corporation, DIC Corporation/Earthrise Nutritionals, Sensient Technologies, and Chr. Hansen, and DDW–The Color House, accounting for an estimated 55–65% of regional revenue. These companies leverage vertical integration strategies that span cultivation, extraction, and ingredient sales. Cyanotech’s 96-acre Hawaiian facility and DIC’s 108-acre California operation anchor domestic supply, while Sensient and DDW focus on downstream value capture through heat-stable extracts and application-specific color solutions that command 2–3× premiums over commodity powder. DIC’s 2022 investment in Back of the Yards Algae Sciences illustrates a shift toward zero-waste biorefineries, which extract food colorants, biostimulants, and spirulina-based heme analogs from the same biomass, thereby lowering effective production costs and reshaping competitive dynamics. Sensient’s Q3 2025 Color Group revenue of USD 178.2 million, up 9.9%, reflects the prioritization of spirulina-derived phycocyanin as a growth vector, intensifying competition for cultivation capacity and potential M&A among mid-sized producers[4]Source: Sensient Technologies Corporation, “Heat-Stable Spirulina Launch,” sensient.com .

White-space opportunities exist in fresh and texturized spirulina formats, as evidenced by SimpliiGood’s April 2025 EU approval for spirulina-based smoked salmon, which bypasses the sensory limitations of powders while commanding premium pricing. Fermented spirulina is another emerging segment, with preliminary research indicating enhanced bioavailability and reduced off-flavors. Technology is a key differentiator: investments in photobioreactor automation, real-time contamination monitoring, and advanced extraction methods such as ultrasonication and membrane filtration allow producers to achieve pharmaceutical-grade purity at near-commodity costs, compressing margins for open-pond incumbents. Third-party quality assurance, exemplified by E.I.D. Parry’s USP Dietary Ingredient Verification, is increasingly essential for contract manufacturers serving risk-averse multinational brands.

Regulatory compliance further shapes market dynamics. FDA NDI notifications, CFIA site licensing, and COFEPRIS sanitary permits impose fixed costs that favor larger players with dedicated regulatory teams, while simultaneously protecting incumbents from low-cost offshore suppliers unable to meet North American purity and traceability standards. As competition intensifies, success in the market will depend on the ability to combine technological innovation, high-quality verification, and regulatory alignment, particularly for companies seeking to expand into high-margin food, beverage, and specialty supplement applications.

North America Spirulina Extract Industry Leaders

Cyanotech Corporation

DIC Corporation- Earthrise Nutritionals

Sensient Technologies Corporation

Chr. Hansen A/S

Givaudan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Lonza launched Organicaps, USDA organic-certified pullulan capsules for the North American market, addressing a supply-chain bottleneck for fully organic spirulina supplements by eliminating gelatin and synthetic polymers. The launch enables brands to claim 100% organic formulations, unlocking shelf space in natural-products retailers and premium e-commerce channels.

- March 2024: Sensient Technologies introduced a proprietary heat-stable spirulina ingredient that can withstand baking, extrusion, and pasteurization without color degradation. The innovation enables spirulina to enter high-temperature food applications, including extruded snacks, baked goods, and UHT beverages, which were previously inaccessible due to thermal instability, thereby expanding the addressable markets for natural blue colorants.

North America Spirulina Extract Market Report Scope

Spirulina extract, obtained through specialized extraction processes, offers higher potency and functionality than whole spirulina biomass and is available in various formats, including powder, liquid, and other specialized forms, to suit diverse formulation needs. The market scope encompasses its use in food and beverage products as a natural colorant and functional ingredient, in pharmaceuticals and dietary supplements for immune, antioxidant, and metabolic support, in animal feed to enhance nutrition and performance, as well as in select industrial and personal care applications. Geographically, the scope encompasses the United States, the dominant market, Canada with its regulated natural health product framework, Mexico, a rapidly developing consumer base, and the rest of North America, where demand is driven by growing interest in plant-based, sustainable, and clean-label ingredients.

By Form

| Powder |

| Liquid |

| Others |

By Application

| Food and Beverage |

| Pharmaceuticals and Dietary Supplements |

| Animal Feed |

| Other Industrial Uses |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Food and Beverage |

| Pharmaceuticals and Dietary Supplements | |

| Animal Feed | |

| Other Industrial Uses | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the spirulina ingredient market in North America today?

The market reached USD 259.79 million in 2026 and is projected at USD 392.62 million by 2031, representing an 8.61% CAGR.

Which form of spirulina captures the highest market share?

Powder formats account for 70.92% of 2025 revenue because they fit existing supplement and food manufacturing lines.

What is driving food and beverage adoption of spirulina?

FDA approval for expanded color uses lets brands replace synthetic blue dyes while adding protein and micronutrients.

Why is Mexico the fastest-growing geography?

Rising disposable income and a USD 33.8 billion health-and-wellness food sector are opening retail space for spirulina-fortified products.

Which companies dominate supply?

Cyanotech, DIC Corporation’s Earthrise, Sensient Technologies, Chr. Hansen, and DDW collectively control about 55%-65% of regional revenue.

Page last updated on: