Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

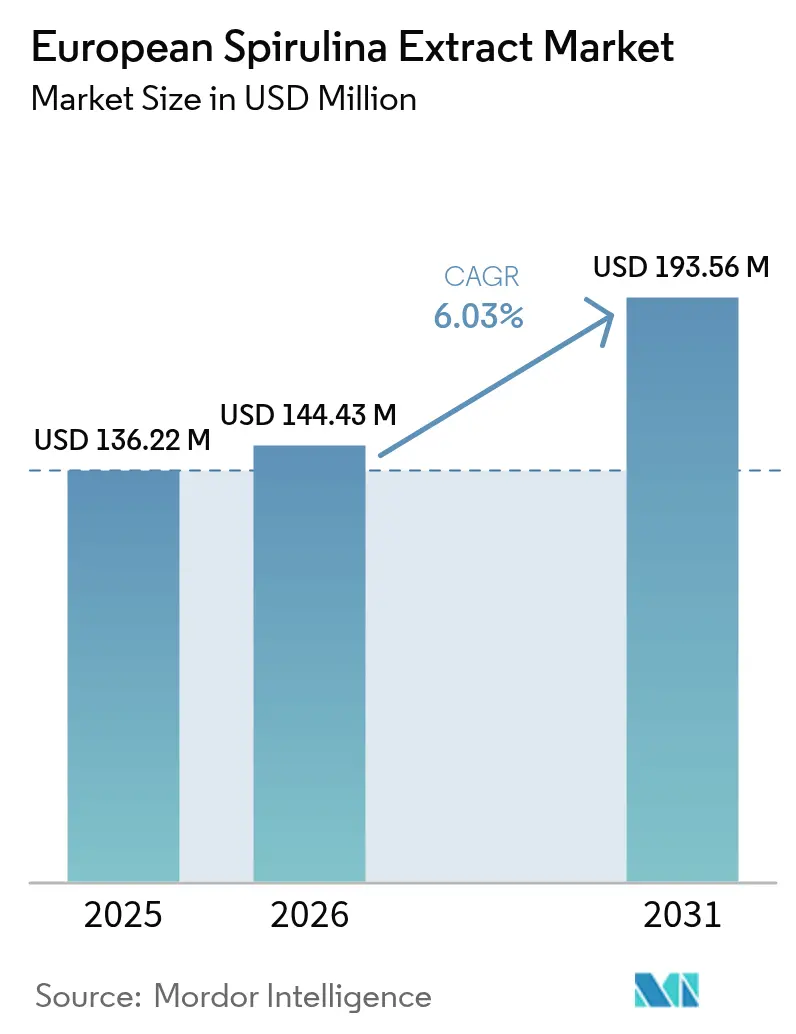

| Base Year Market Size (2025) | USD 136.22 Million |

| Market Size (2026) | USD 144.43 Million |

| Market Size (2031) | USD 193.56 Million |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

European Spirulina Extract Market Analysis by Mordor Intelligence

European Spirulina market size in 2026 is estimated at USD 144.43 million, growing from 2025 value of USD 136.22 million with 2031 projections showing USD 193.56 million, growing at 6.03% CAGR over 2026-2031. This growth is primarily driven by increasing consumer emphasis on health, wellness, and nutrition, as spirulina is recognized for its high protein content, vitamins, minerals, antioxidants, and bioactive compounds. The market is undergoing significant advancements as manufacturers adopt improved cultivation and extraction technologies, including photobioreactors, closed-system farms, and advanced drying or microencapsulation methods, to enhance product quality, stability, and bioavailability. Additionally, rising consumer demand for plant-based, organic, and sustainably sourced ingredients is prompting companies to develop premium spirulina products with clean-label claims and environmentally sustainable production processes.

Key Report Takeaways

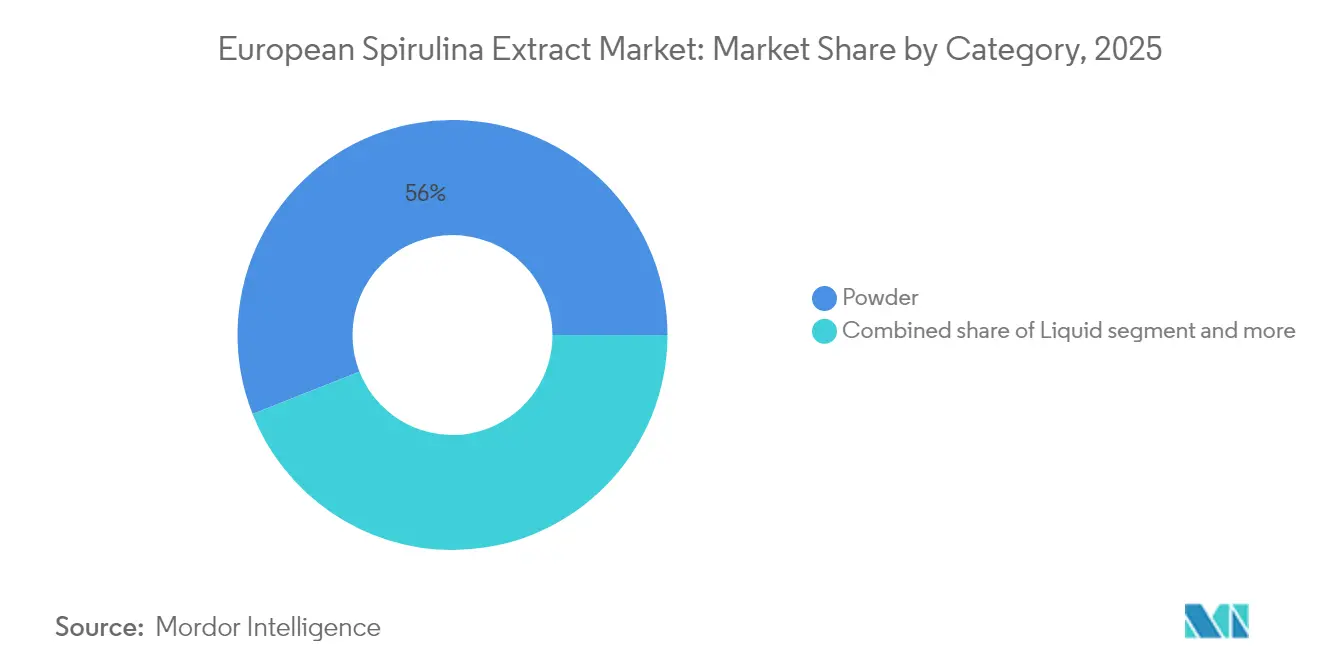

- By category, powder formats captured 55.98% of the European Spirulina market share in 2025; liquid spirulina is advancing at a 6.48% CAGR through 2031.

- By nature, conventional products held 75.10% of demand in 2025, while organic variants are expanding at a 7.34% CAGR through 2031.

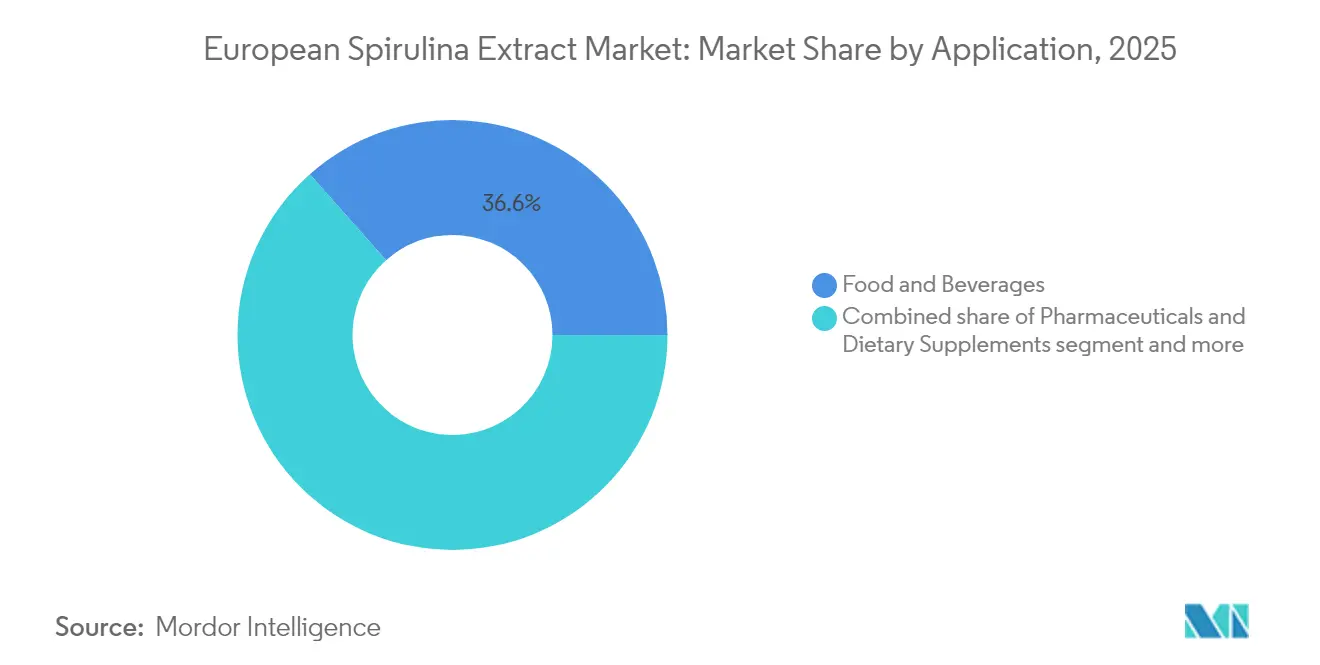

- By application, the food and beverages segment accounted for 36.55% of revenue in 2025. The cosmetics and personal care segment is projected to grow at a CAGR of 7.02% through 2031.

- By geography, Germany led with 22.85% of the European Spirulina market size in 2025, whereas the United Kingdom is set to post a 6.72% CAGR through

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

European Spirulina Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer health and wellness awareness | +1.0% | Pan-European, strongest in Germany, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Advancements in algae farming and extraction technologies | +0.8% | France, Germany, Italy, Spain (production hubs); Netherlands, Belgium (innovation clusters) | Long term (≥ 4 years) |

| Strong nutraceutical sector demand | +0.9% | Germany, United Kingdom, France, and Poland (supplement consumption leaders) | Short term (≤ 2 years) |

| Sustainable and organic product preference | +0.7% | Germany, Netherlands, Sweden, France (organic market leaders); spillover to Belgium, UK | Medium term (2-4 years) |

| Innovative product development | +0.6% | France, Belgium, Netherlands (fresh spirulina innovation); Germany, UK (formulation advances) | Medium term (2-4 years) |

| Use of spirulina as natural blue colorant in beverages and dairy alternatives | +0.7% | Germany, France, Netherlands, Belgium (food manufacturing centers); UK, Spain (beverage innovation) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer health and wellness awareness

The European spirulina extract market is primarily driven by increasing consumer awareness of health and wellness, which has significantly influenced purchasing behavior and product demand across the region. Consumers in Europe are increasingly focusing on nutrient-rich, natural, and functional ingredients in their diets, seeking products that promote immunity, energy, detoxification, and overall well-being. Spirulina, known for its high content of protein, vitamins, minerals, antioxidants, and bioactive compounds like phycocyanin, aligns well with these shifting consumer preferences. The rise of fitness and lifestyle trends, such as plant-based diets, veganism, and preventive healthcare, has further boosted demand for spirulina. It is regarded not only as a dietary supplement but also as a versatile superfood that can be easily integrated into meals, smoothies, and beverages. Moreover, the proliferation of information through social media, health blogs, and wellness platforms has increased consumer awareness of spirulina's functional benefits, driving demand for natural, clean-label, and sustainable products.

Advancements in algae farming and extraction technologies

Advancements in algae farming and extraction technologies are driving the market by improving the quality and scalability of spirulina production. Modern cultivation methods, such as photobioreactors, closed-system farms, and optimized open-pond systems, enable higher yields, controlled nutrient profiles, and reduced contamination risks compared to traditional farming practices. These technological advancements ensure consistent biomass quality, making it possible to meet the increasing demand from industries such as dietary supplements, functional foods, beverages, and cosmetics. On the extraction side, innovations like supercritical CO₂ extraction, enzymatic processing, microencapsulation, and advanced drying techniques enhance the bioavailability, stability, and color retention of spirulina extracts. These advancements allow manufacturers to produce high-purity, standardized ingredients suitable for premium and specialized applications. By improving efficiency, lowering production costs, and enabling value-added formulations, technological progress in algae farming and extraction is significantly enhancing market accessibility, expanding application possibilities, and driving overall growth in the European spirulina extract market.

Strong nutraceutical sector demand

The European spirulina extract market is primarily driven by strong demand from the nutraceutical industry, which has been growing rapidly due to increasing consumer emphasis on preventive healthcare and dietary supplementation. Spirulina's rich nutritional composition, including high-quality protein, vitamins, minerals, antioxidants, and bioactive compounds, positions it as a key ingredient in dietary supplements, functional foods, and fortified beverages. Nutraceutical manufacturers are incorporating spirulina extracts into various formats such as capsules, powders, tablets, and ready-to-drink formulations to meet the needs of health-conscious consumers seeking benefits like immunity support, energy enhancement, detoxification, and overall wellness. For example, data from Synadiet, the French national trade association for food supplements, indicates that 61% of people in France consumed food supplements in 2024, underscoring the widespread adoption of nutraceutical products [1]Source: Synadiet, "Share of people having consumed food supplements in France", synadiet.org. This strong market penetration reflects a well-established consumer base increasingly inclined toward natural and plant-based ingredients.

Sustainable and organic product preference

Consumer preference for sustainable and organic products is driving market growth, reflecting a broader shift toward environmentally responsible consumption and clean-label ingredients. Spirulina meets this demand by offering a natural, chemical-free, and nutrient-rich option. Manufacturers are increasingly prioritizing organic certification, traceability, and sustainable production practices to differentiate their products and cater to environmentally conscious consumers. This trend is influenced by both health considerations and a growing awareness of sustainability and ethical sourcing, which have become significant factors in purchasing decisions across Europe. For example, according to the Research Institute for Organic Agriculture (FiBL), Norway recorded the highest volume of organic aquaculture production in 2023, with approximately 54.1 thousand metric tons, followed by Ireland with 34.3 thousand metric tons [2]Source: Research Institute for Organic Agriculture (FiBL), "Volume of organic aquaculture production in Europe", fibl.org. These figures underscore the region’s strong commitment to sustainable and organic production practices. Such advancements highlight the growing capacity and acceptance of organic aquaculture and related sectors, fostering a favorable environment for the adoption of organically produced spirulina.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and processing costs | -0.5% | Pan-European, most acute in Northern Europe (Sweden, Poland, Germany, UK) | Short term (≤ 2 years) |

| Taste and sensory challenges | -0.3% | United Kingdom, Germany, Spain, Poland (markets with lower spirulina familiarity) | Medium term (2-4 years) |

| Limited awareness in certain regions | -0.3% | Poland, Spain, Italy, Belgium, Rest of Europe (emerging markets) | Medium term (2-4 years) |

| Supply chain vulnerability | -0.4% | Pan-European, particularly affecting United Kingdom, Germany, Netherlands (high import dependency) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production and processing costs

A key restraint for the European spirulina extract market is the high production and processing costs involved in its cultivation and extraction. Spirulina cultivation requires controlled conditions, including precise light, temperature, and nutrient management, particularly in closed systems or photobioreactors, which demand significant capital and operational investments. Furthermore, while advanced extraction techniques enhance product quality and bioavailability, they also contribute to higher production costs. These elevated costs are often reflected in the final product price, reducing accessibility for price-sensitive consumers and limiting adoption in cost-competitive segments such as mass-market food and beverages. The combination of labor-intensive cultivation processes, high energy requirements, and complex downstream processing poses a financial challenge for smaller manufacturers, potentially hindering market growth despite increasing demand. This remains a significant obstacle to the wider adoption of spirulina products in Europe.

Taste and sensory challenges

Taste and sensory challenges are significantly hindering market growth. Spirulina possesses a naturally strong, earthy, and algae-like flavor, coupled with a deep green-blue color, which many consumers find unappealing, particularly in food and beverage applications. These pronounced sensory characteristics limit its direct incorporation into mainstream products without the use of masking or flavor-modification techniques. Although powder, liquid, and encapsulated forms offer diverse usage options, the inherent taste often necessitates additional formulation steps, such as blending with flavors, sweeteners, or other masking agents, thereby increasing production complexity and costs. Consumer reluctance driven by these sensory attributes can substantially slow adoption in functional foods, beverages, and certain nutraceutical products, posing significant challenges for manufacturers aiming to expand spirulina’s appeal among European consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Fresh Formats Challenge Powder's Processing Dominance

In 2025, powder spirulina held a dominant 55.98% share of the European spirulina extract market, highlighting its widespread adoption and significant contribution to market growth. The powder form's versatility makes it the preferred choice for various applications, including dietary supplements, functional foods, beverages, and nutraceutical products. It can be easily incorporated into formulations without significantly altering taste, texture, or nutritional content. Its convenience and precise dosage control are particularly valued in supplements and clinical formulations, ensuring consistent delivery of essential nutrients such as proteins, antioxidants, and immune-supporting compounds. Additionally, the segment benefits from the growing emphasis on organic, clean-label, and sustainable products, aligning with regulatory standards and consumer expectations for transparency and environmentally responsible production.

The liquid spirulina segment is experiencing steady growth in the European spirulina extract market, with a CAGR of 6.48% projected through 2031. This growth reflects its increasing adoption in functional beverages, nutraceuticals, and liquid supplement formulations. The segment's inherent convenience and ready-to-use format enable manufacturers and consumers to incorporate spirulina directly into drinks, smoothies, shots, and other liquid-based wellness products without additional preparation. Liquid spirulina is valued for its enhanced bioavailability and ease of mixing, ensuring consistent nutrient intake. This makes it particularly appealing to health-conscious consumers seeking quick and efficient supplementation. Furthermore, advancements in formulation technologies, such as flavor masking, stabilization techniques, and fortified blends, address the strong algae taste and improve shelf life. These innovations enhance the palatability and commercial viability of liquid spirulina products.

By Nature: Organic Certification Reshapes Value Chains

Conventional spirulina accounted for 75.10% of the European spirulina extract market in 2025, highlighting its strong presence and broad acceptance among manufacturers and consumers. This dominance is primarily due to its lower production costs and extensive availability, making it the preferred option for mass-market applications such as dietary supplements, functional foods, beverages, and nutraceutical formulations. Manufacturers often choose conventional spirulina because it can be produced at scale using established open-pond and controlled cultivation methods. These methods ensure a consistent supply and quality at competitive prices, which is essential to meet the increasing demand across Europe. Additionally, the versatility of conventional spirulina in various formulations and its compatibility with existing production processes further solidify its position as a key ingredient in the market.

The organic spirulina segment is projected to grow at a CAGR of 7.34% through 2031, driven by increasing consumer demand for natural, sustainably produced, and clean-label products in Europe. This growth is attributed to heightened awareness of health, environmental sustainability, and ethical sourcing, making organic ingredients a priority for both consumers and manufacturers. For example, according to the Federal Ministry of Food and Agriculture, as of December 2024, Germany had 109,567 products carrying organic labels, reflecting strong market penetration and consumer acceptance of organic-certified products . This widespread adoption of organic labeling underscores the growing preference for certified natural products, fostering a favorable environment for the growth of organic spirulina. With organic certification ensuring transparency, traceability, and adherence to sustainable practices, manufacturers are increasingly incorporating organic spirulina into dietary supplements, functional beverages, and food formulations to align with regulatory standards and consumer expectations.

By Application: Cosmetics Outpaces Food as Margin Driver

In 2025, the food and beverages segment accounted for a notable 36.55% share of the European spirulina extract market, highlighting its importance as a primary application area for this ingredient. This strong market presence is driven by spirulina’s versatility and nutritional benefits, enabling its incorporation into various products such as functional beverages, smoothies, snack bars, bakery items, dairy alternatives, and ready-to-drink health shots. Its high protein content, antioxidants, vitamins, and minerals make it a valuable fortification ingredient for food and beverage products targeting health-conscious and fitness-oriented consumers. Additionally, the segment benefits from increasing consumer demand for functional and plant-based foods, as European consumers increasingly favor clean-label, natural, and nutrient-rich products.

The cosmetics and personal care segment is projected to grow at a CAGR of 7.02% through 2031, making it the fastest-growing application in the European spirulina extract market. This growth is driven by spirulina’s rich composition of antioxidants, vitamins, minerals, and bioactive compounds, which deliver anti-aging, skin-nourishing, and protective benefits that are highly valued in personal care formulations. The increasing consumer preference for clean-label, sustainable, and plant-based ingredients in the beauty industry is also a significant factor. For example, according to Cosmetica Italia, the consumption value of cosmetics and personal care products in Europe reached EUR 95.7 billion in 2023, underscoring the market’s potential for innovative ingredients like spirulina extract. European consumers’ growing focus on natural and eco-friendly products has led brands to incorporate spirulina into serums, creams, masks, shampoos, and other formulations to meet this demand.

Geography Analysis

This dominance is attributed to the country’s well-developed health and wellness industry, strong consumer awareness of dietary supplements, and the widespread availability of functional foods and nutraceuticals. Germany’s advanced regulatory framework, high-quality standards, and robust retail infrastructure, including pharmacies, specialty health stores, and e-commerce platforms, create a favorable environment for spirulina products. Manufacturers often prioritize Germany for new product launches due to its large, health-conscious consumer base and high willingness to pay for premium, organic, and functional ingredients.

The United Kingdom is projected to grow at the fastest rate, with a CAGR of 6.72% through 2031. This growth reflects increasing consumer adoption of plant-based and superfood supplements, heightened interest in immune-supporting products, and the expanding trend of functional beverages. France combines its leadership in production with strong domestic consumption, leveraging its established nutraceutical and food supplement manufacturing capabilities. Italy demonstrates steady growth, driven by rising awareness of health and wellness trends, the popularity of functional foods, and the integration of spirulina into dietary supplements and fortified food products.

Other European markets are developing at varying rates. Spain’s spirulina sector remains relatively nascent, with adoption primarily concentrated in specialty health stores and e-commerce, indicating significant untapped growth potential. Poland has experienced a surge in dietary supplement consumption, creating opportunities for spirulina extract as part of the growing interest in vitamins, proteins, and natural nutraceuticals. The Netherlands serves as a key hub for distribution and trade, benefiting from a strong logistics network and high export potential, facilitating both domestic consumption and access to neighboring European markets.

Competitive Landscape

The European spirulina extract market is moderately fragmented, with a wide range of participants, including large multinational corporations and small- to medium-sized enterprises, competing across various product forms and applications. This fragmentation is driven by the diverse end-use applications, such as dietary supplements, functional foods and beverages, cosmetics, and nutraceutical ingredients. Consequently, no single company dominates the market, enabling multiple players to capture niche segments and regional markets. The competitive environment fosters continuous product innovation, strategic partnerships, and differentiation through quality, certifications, and specialty offerings, such as organic and high-phycocyanin extracts.

Prominent players in the market include globally recognized companies such as Sensient Technologies Corporation, Givaudan S.A., DIC Corporation, Cyanotech Corporation, and Botanic Healthcare, among others. These firms leverage their strong Research and Development (R&D) capabilities, extensive distribution networks, and established brand recognition to sustain their market presence. They focus on developing value-added products, including standardized extracts, fortified powders, and stabilized liquid formulations, to meet the increasing demand from functional foods, beverages, and cosmetics sectors. Additionally, these companies are investing in sustainable cultivation practices and obtaining organic certifications to address the growing consumer preference for environmentally responsible and natural ingredients, further enhancing their competitive positioning in the market.

Technological advancements are creating a divide within the market, distinguishing traditional players from those adopting advanced extraction, drying, and stabilization technologies. Companies utilizing innovative techniques, such as supercritical CO₂ extraction, enzymatic processing, and microencapsulation, are able to offer products with enhanced bioavailability, improved color stability, and extended shelf life, allowing them to command premium pricing. In contrast, players relying on conventional cultivation and processing methods face challenges in differentiation and often compete primarily on price and scale.

European Spirulina Extract Industry Leaders

-

Sensient Technologies Corporation

-

Givaudan S.A.

-

DIC Corporation (Earthrise Nutritionals)

-

Cyanotech Corporation

-

Botanic Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Givaudan introduced a new range of active botanical extracts under its Vibrant Collection, aimed at enhancing make-up formulations. The Spirulina 2183 Brightening algae extract is derived from Spirulina platensis G.

- April 2024: Edonia, a producer of protein ingredients derived from microalgae such as spirulina and chlorella, has completed its first financing round, raising EUR 2 million. This funding will support the industrialization of its technology and the expansion of its Research and Development (R&D) efforts.

- March 2024: Probelte introduced Spirunol, a biostimulant derived from microalgae. The product contains vitamins and antioxidant compounds, including plant pigments, polyphenols, amino acids, prebiotic proteins, and polysaccharides.

European Spirulina Extract Market Report Scope

The European spirulina extract market is segmented by application and geography. On the basis of application, the market is segmented into nutraceuticals, food, cosmetics, agriculture, animal feed, and other applications. The report covers regional trends across major countries in Europe.

By Category

| Powder |

| Liquid |

| Others |

By Nature

| Conventional |

| Organic |

By Application

| Food and Beverages |

| Pharmaceuticals and Dietary Supplements |

| Animal Feed |

| Cosmetics and Personal Care |

| Others |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Category | Powder |

| Liquid | |

| Others | |

| By Nature | Conventional |

| Organic | |

| By Application | Food and Beverages |

| Pharmaceuticals and Dietary Supplements | |

| Animal Feed | |

| Cosmetics and Personal Care | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe Spirulina market in 2026?

The Europe Spirulina market size is USD 144.43 million in 2026 and is projected to reach USD 193.56 million by 2031.

Which format leads European demand?

Powder spirulina leads with 55.98% market share in 2025 due to well-established tableting and encapsulation lines.

Which application will grow the fastest through 2031?

Cosmetics and personal care shows the highest CAGR at 7.02%, driven by clean-beauty demand for natural actives.

Which country is forecast to expand most rapidly?

The United Kingdom is forecast to grow at 6.72% CAGR through 2031, supported by a strong plant-based sector and online supplement sales.

Page last updated on: