Frame Grabber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.75 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

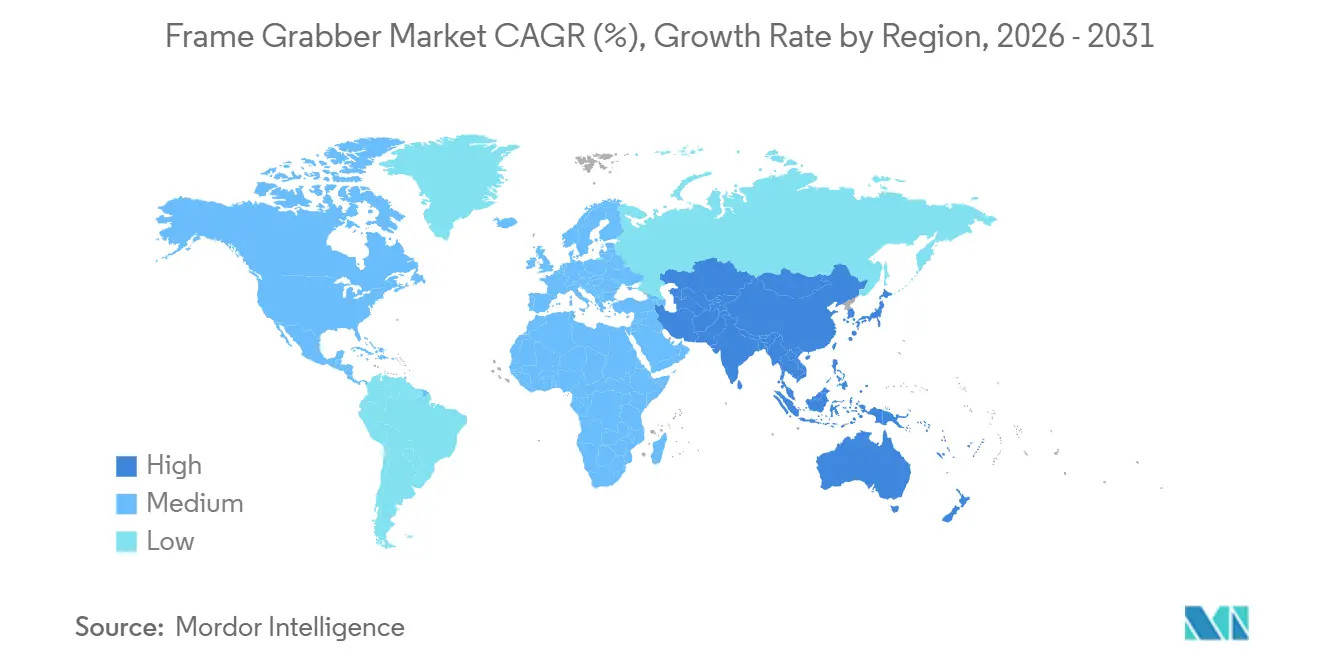

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

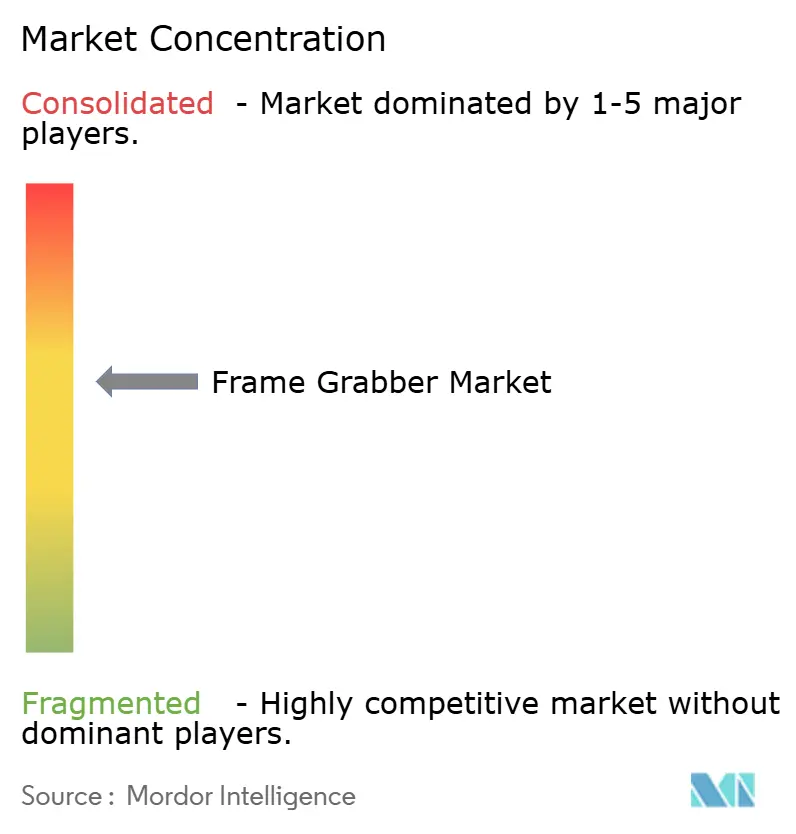

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frame Grabber Market Analysis by Mordor Intelligence

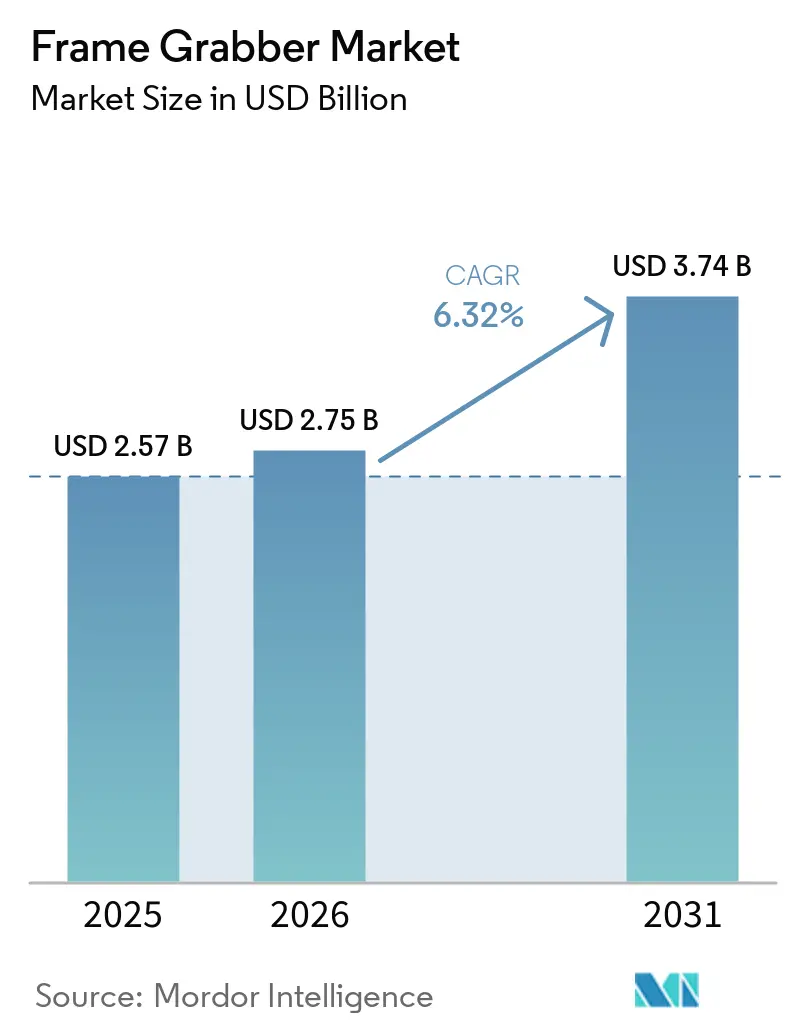

The frame grabber market size is expected to increase from USD 2.57 billion in 2025 to USD 2.75 billion in 2026 and reach USD 3.74 billion by 2031, growing at a CAGR of 6.32% over 2026-2031. The advance is propelled by manufacturing lines migrating to sensors exceeding 50 megapixels, Industry 4.0 initiatives that demand deterministic imaging, and the pairing of CoaXPress 2.0 with PCIe 4.0 host interfaces, which together clear an aggregate bandwidth ceiling above 50 gigabits per second. Vendors are responding with PCIe Gen4 cards capable of 13.2 gigabytes per second sustained host transfer, seven-lane Camera Link HS capture, and cable reaches beyond 30 meters, capabilities that ease installation in semiconductor fabs and automotive paint-booth cells. Concurrently, smart-camera alternatives with embedded AI accelerators are squeezing the low-to-mid performance tiers, while legacy Camera Link and GigE Vision deployments linger where deterministic latency is less critical. In this environment, the frame grabber market continues to balance the pull of high-throughput inspection against the push from integrated vision devices, resulting in steady mid-single-digit growth and a technology cadence tied to sensor and host-bus upgrades.

Key Report Takeaways

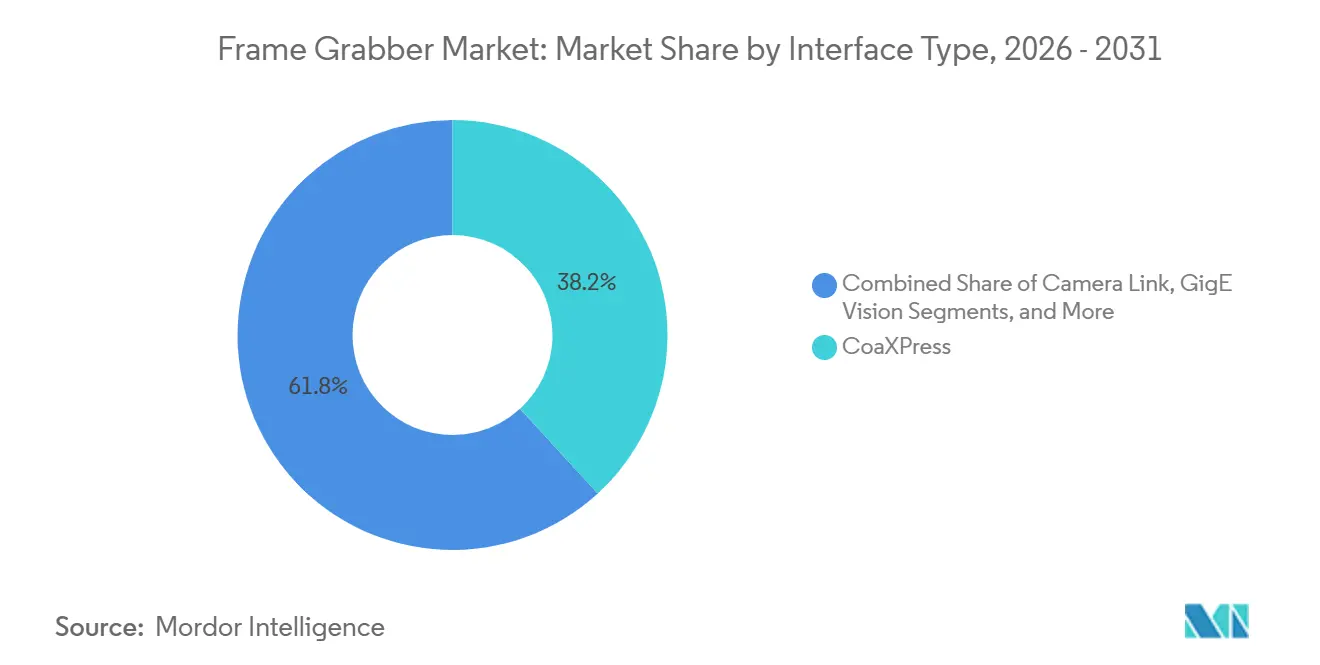

- By interface type, CoaXPress commanded 38.19% of the frame grabber market share in 2025 and is expanding at a 6.97% CAGR through 2031, reflecting its power-over-cable advantage and a forthcoming 25-gigabit specification.

- By host-bus and form factor, PCIe and PCI cards led with 46.52% of the frame grabber market share in 2025, while M.2 and Thunderbolt modules are advancing at a 7.03% CAGR toward 2031 as capture logic migrates into compact edge appliances.

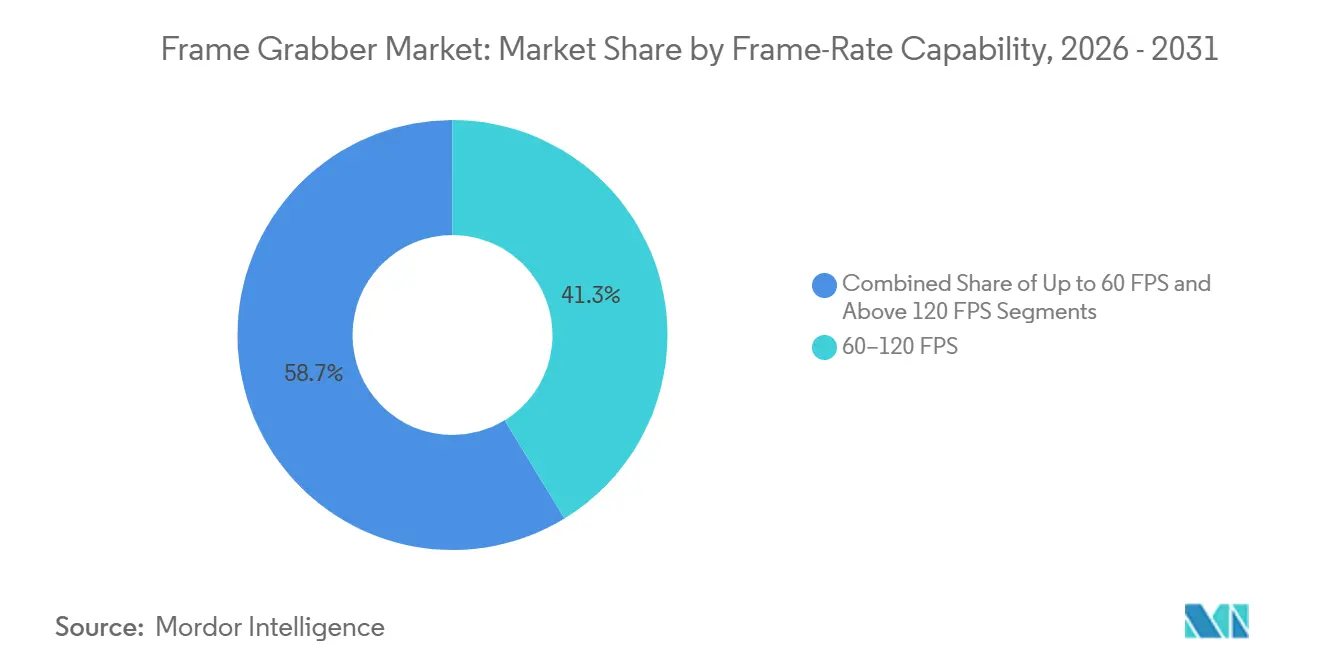

- By frame-rate capability, the 60-120 FPS tier held 41.27% of the frame grabber market share in 2025, whereas above-120 FPS configurations are projected to grow at a 7.11% CAGR on the strength of high-speed line-scan demand.

- By application industry, industrial and manufacturing accounted for 34.74% of the frame grabber market share in 2025; medical and life sciences is the fastest mover, tracking a 6.91% CAGR that mirrors the adoption curve of surgical robotics.

- By geography, Asia-Pacific captured 32.43% of the frame grabber market share in 2025 and outpaces all regions with a forecast 7.88% CAGR, bolstered by China’s localization drive and India’s expanding computer-vision ecosystem.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Frame Grabber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of >50 MP Image Sensors | +1.4% | Asia-Pacific semiconductor fabs, European automotive plants | Medium term (2-4 years) |

| Industry 4.0 Roll-Outs Requiring Real-Time Imaging | +1.2% | Germany, United States, China, Japan | Medium term (2-4 years) |

| Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth | +1.1% | Early uptake in North America and Europe, rapid Asia-Pacific scale | Short term (≤ 2 years) |

| Growth of Automated Optical Inspection in Electronics | +0.9% | China, South Korea, Taiwan, wider Southeast Asia | Medium term (2-4 years) |

| AI-enabled FPGA preprocessing on grabbers | +0.9% | Global, concentrated in advanced manufacturing regions | Medium term (2-4 years) |

| Surgical-robot demand for deterministic video | +0.5% | North America and EU, expanding to developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of >50 MP Image Sensors on Production Lines

Canon's 410-megapixel CMOS sensor and Sony's IMX927 105-megapixel sensor running at 100 frames per second exemplify the resolution escalation that forces production-line integrators to replace legacy Camera Link Base or GigE Vision interfaces with CoaXPress 2.0 or Camera Link HS. A single 105-megapixel frame at 100 frames per second generates approximately 10.5 gigabytes per second of raw Bayer data, exceeding the 1 gigabit per second ceiling of standard GigE Vision by an order of magnitude. This bandwidth mismatch compels manufacturers to deploy frame grabbers with aggregate throughput beyond 10 gigabytes per second, driving demand for PCIe Gen4 cards and CoaXPress multi-link configurations. STMicroelectronics' 5-megapixel hybrid global-rolling-shutter sensor further illustrates the trend toward application-specific imaging that requires flexible frame-grabber architectures capable of switching between global-shutter and rolling-shutter modes midstream.[1]Source: STMicroelectronics, “VD56G3 5 MP Hybrid Global-Rolling Shutter Sensor,” st.com The shift to >50-megapixel sensors is most pronounced in semiconductor wafer inspection, flat-panel-display defect detection, and automotive body-in-white measurement, where sub-micron resolution directly correlates with yield improvement and warranty-cost reduction.

Industry 4.0 Roll-Outs Requiring Real-Time Imaging

Industry 4.0 architectures mandate closed-loop control with sub-10-millisecond latency between image acquisition and actuator response, a requirement that favors frame grabbers with FPGA-based pre-processing over software-only pipelines running on general-purpose CPUs. Gidel's Proc1C10N frame grabber integrates 143 tera-operations per second of INT8 inference capacity directly on the capture card, enabling real-time defect classification without round-tripping pixel data to a host GPU. This on-board intelligence reduces network congestion in multi-camera cells and ensures deterministic latency even when other workloads contest host resources. Basler's November 2023 partnership with Siemens embedded the pylon SDK into Siemens Industrial Edge devices, allowing factory operators to deploy vision applications as containerized microservices that scale horizontally across production lines. The convergence of time-sensitive networking protocols, OPC UA for machine-to-machine communication, and deterministic frame grabbers positions imaging as a first-class citizen in the industrial Internet of Things stack, rather than a bolt-on inspection step.

Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth

CoaXPress 2.0 delivers 12.5 gigabits per second per link and supports power-over-cable at 13-17 watts, eliminating separate power supplies for cameras in space-constrained enclosures and reducing cabling complexity in multi-camera arrays. The specification's use of Micro-BNC connectors and 75-ohm coaxial cable extends reach to 40 meters without active repeaters, a critical advantage in automotive paint-booth inspection where electromagnetic interference from high-voltage curing lamps degrades twisted-pair signals. PCIe Gen4's doubling of per-lane bandwidth to approximately 2 gigabytes per second allows a single x8 card to sustain 16 gigabytes per second of host transfer, sufficient to stream four 105-megapixel cameras at 30 frames per second with headroom for metadata and error correction. Teledyne DALSA's Xtium3 leverages this headroom to implement lossless compression and GPU-direct DMA, bypassing system memory and reducing latency by 2-3 milliseconds in time-critical applications. The CoaXPress 3.0 specification, currently in draft, targets 25 gigabits per second per link and will enable single-cable solutions for 200-megapixel sensors, further consolidating the interface's position in high-throughput inspection.

Growth of Automated Optical Inspection in Electronics

ViTrox's V510i automated optical inspection system pairs a 12-megapixel CoaXPress camera with a frame grabber capable of 64 square centimeters per second throughput, inspecting printed-circuit-board solder joints at line speeds that match modern surface-mount-technology placement rates. Delvitech's Horus multi-camera AOI platform aggregates six camera heads into a single inspection station, generating over 40 gigabytes per second of raw data that only a multi-link frame grabber can ingest without frame drops. The electronics industry's migration to 01005 passive components and 0.3-millimeter ball-grid-array pitches demands sub-pixel registration accuracy, driving adoption of line-scan cameras with 32,000-pixel resolution and line rates exceeding 400 kilohertz. Teledyne's Linea HS camera family, designed for Camera Link HS interfaces, exemplifies this trend by delivering time-delay-integration scanning at speeds that outpace area-scan alternatives by a factor of five. Asia-Pacific's dominance in electronics manufacturing, particularly China's role in assembling 70 percent of global smartphones and South Korea's leadership in memory-chip packaging, concentrates AOI frame-grabber demand in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Cameras Replacing Discrete Frame Grabbers | -0.9% | Most pronounced in North America and Europe | Short term (≤ 2 years) |

| High Up-Front Cost of CoaXPress Cards for SMEs | -0.6% | Acute in South America, Africa, and Southeast Asia | Medium term (2-4 years) |

| Thermal-Management Issues Beyond 25 Gbps | -0.4% | Global high-throughput installations | Long term (≥ 4 years) |

| FPGA Supply-Chain Tightness | -0.3% | All regions that rely on Xilinx and Intel Altera devices | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart Cameras Replacing Discrete Frame Grabbers

Allied Vision's Alecs smart camera integrates an NVIDIA Jetson Orin NX module with 100 tera-operations per second of AI performance, enabling on-device inference for defect classification, optical character recognition, and dimensional measurement without a separate frame grabber or host PC.[2]Source: Allied Vision, “Alecs Smart Camera,” alliedvision.com Teledyne's BOA3 AI camera similarly embeds a neural network accelerator that processes images at the edge, transmitting only metadata or alarm signals over GigE or USB3, thereby reducing network bandwidth by two orders of magnitude. This architectural shift appeals to applications where a single camera suffices, installation space is constrained, and the cost of a dedicated frame grabber and host PC cannot be justified. However, smart cameras struggle in multi-camera synchronization scenarios, deterministic-latency applications such as surgical robotics, and high-throughput inspection cells where uncompressed pixel data must be archived for traceability. The frame-grabber ecosystem retains an advantage in these niches by offering hardware-triggered acquisition across dozens of cameras with sub-microsecond jitter, FPGA-based real-time processing that bypasses operating-system scheduling latency, and direct GPU memory access for accelerated inference pipelines.

High Up-Front Cost of CoaXPress Cards for SMEs

CoaXPress frame grabbers with four-link support and PCIe Gen4 host interfaces command premium pricing that can exceed USD 3,000 per card, a barrier for small and medium enterprises operating on capital-expenditure budgets measured in tens of thousands of dollars rather than millions. This cost structure forces SMEs to extend the service life of legacy Camera Link or GigE Vision infrastructure, accepting lower frame rates and resolution rather than migrating to CoaXPress 2.0. The economic calculus shifts when production volumes justify the investment: a semiconductor fab processing 10,000 wafers per month can amortize a USD 50,000 multi-camera inspection cell over six months, but a contract manufacturer assembling 500 units per month faces a multi-year payback period. Vendors are responding with entry-level CoaXPress cards that support one or two links and PCIe Gen3 host interfaces, sacrificing aggregate bandwidth to hit sub-USD 1,500 price points, yet these products still cost more than GigE Vision frame grabbers by a factor of three. The pricing gap narrows when total system cost is considered: CoaXPress's power-over-cable eliminates the need for separate camera power supplies, and longer cable runs reduce the need for intermediate junction boxes, but these savings are often invisible to procurement teams focused on line-item component costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Interface Type: CoaXPress Strengthens its High-Bandwidth Foothold

The frame grabber market size for interface-type solutions shows CoaXPress occupying 38.19% revenue share in 2025, a share projected to climb steadily through 2031 as its 6.97% CAGR outpaces that of Camera Link and GigE alternatives. CoaXPress fusion of 12.5 Gbps per link and power delivery translates into simplified cable harnesses and extended reach, attributes crucial in semiconductor wafer inspection and automotive paint booths. Camera Link’s entrenched base in aerospace and medical X-ray keeps it relevant for retrofit projects, yet new installations prefer the headroom and future-proofing of CoaXPress 2.0 and Camera Link HS. GigE Vision, while cost-friendly, suffers from packet loss and CPU overhead that undermine deterministic inspection, relegating it to distributed or cost-sensitive tasks.

Forward-looking demand centers on the draft CoaXPress 3.0 standard, which targets 25 Gbps per link, clearing the way for single-cable 200-MP cameras in flat-panel display metrology. Camera Link HS retains a specialized following where radiation-hard components are required, but engineering mindshare is pivoting toward CoaXPress. USB3 Vision maintains a foothold in handheld scanners and laboratory instruments thanks to its ubiquity and plug-and-play elegance, yet its 5 Gbps ceiling limits it to resolutions under 20 MP at moderate frame rates. Consequently, CoaXPress will remain the flagship of the frame grabber market, defining both performance expectations and competitive roadmaps.

By Host-Bus and Form Factor: Edge-Friendly M.2 Modules Take Share

PCIe and PCI cards supplied 46.52% of 2025 revenue, a testament to the dominance of tower and rackmount workstations in legacy vision architectures. The rise of compact edge appliances now lifts M.2 and Thunderbolt modules, forecast to log a 7.03% CAGR through 2031. M.2 modules mate directly to PCIe lanes in a footprint smaller than a credit card, enabling fanless designs that mount behind robot arms or inside panel PCs. Thunderbolt 4 provides 40 Gbps aggregate bandwidth, daisy-chaining, and hot-plug convenience, features that improve installation economics for portable inspection rigs.

Embedded boards in PC/104 and CompactPCI formats persist in aerospace and defense, where shock and vibration requirements exceed commercial PC tolerances. USB external capture units meet entry-level needs when a single camera suffices, but their reliance on host USB controllers introduces latency variability, disqualifying them for deterministic inspection. High-density lines still lean on full-height PCIe cards that pool FPGA resources across four or more camera links, underscoring a bifurcated demand curve inside the frame grabber market. The outcome is a gradual, not abrupt, form-factor transition driven by the rise of edge AI deployments.

By Frame-Rate Capability: Above-120 FPS Tier Accelerates

The 60-120 FPS tier commanded 41.27% of 2025 revenue because it aligns with conveyor speeds and robotic cycle times in much of discrete manufacturing. Yet the above-120 FPS category is clocking a faster 7.11% CAGR as line-scan and high-speed area-scan cameras gain traction. Line-scan solutions that push 32,000 pixels at 400 kHz generate torrents of data that only multi-link CoaXPress or Camera Link HS boards can capture without dropped frames, making high-end frame grabbers indispensable to web inspection and semiconductor wafer metrology.

Area-scan platforms are also nudging frame rates upward. Sony’s 105-MP sensor runs at 100 FPS, enabling automotive body-in-white stations to image a full vehicle in 2 seconds.[3]Sony Semiconductor, “IMX927 CMOS Image Sensor,” sony-semicon.com Aerospace test labs seek 1,000 FPS or more for turbine blade vibration and ballistic impact studies, motivating cards with 16 GB on-board SDRAM that buffer burst captures before NVMe offload. Consequently, while mid-speed tiers still dominate by volume, the high-speed slice exerts outsized influence over roadmap priorities and margins within the frame grabber market.

By Application Industry: Surgical Robotics Drives Medical Uptake

Industrial and manufacturing applications retained the largest 2025 slice at 34.74%, owing to electronics AOI, automotive paint inspection, and general parts verification. Medical and life sciences, however, chart the highest CAGR at 6.91%. Surgical robots depend on deterministic, hardware-time-stamped video streams to synchronize haptic feedback with imagery, a need best met by FPGA-enabled frame grabbers. Regulatory burdens under IEC 60601-1 reward vendors with mature quality systems, creating a barrier that cushions pricing power.

Electronics and semiconductor inspection will remain another cornerstone, underwritten by Asia-Pacific’s leadership in smartphone assembly and memory packaging. Security and surveillance segments gravitate to smart cameras and NVRs that sidestep capture cards, muting growth potential there. Aerospace and defense buyers gravitate toward rugged cards with conformal coating and MIL-STD-810 certification, sustaining a profitable, though niche, revenue stream. The interplay of fast-growing medical demand and entrenched industrial volume cements a balanced application mix for the frame grabber market size outlook.

Geography Analysis

Asia-Pacific accounted for 32.43% of the global frame grabber market revenue in 2025 and is projected to register a 7.88% CAGR through 2031. China’s semiconductor localization mandates, South Korea’s leadership in memory packaging, and India’s production-linked incentives for electronics combine to anchor regional momentum. Western vendors, as illustrated by Basler’s 76% purchase of Alpha TechSys Automation India, are deepening local footprints to keep pace with agile domestic competitors. Japan’s aging workforce and the imperative of automation likewise propel adoption in factory retrofits that demand deterministic imaging.

North America and Europe jointly contributed roughly half of 2025 revenue, supported by mature industrial bases, stringent automotive quality standards, and robust demand in aerospace and defense. The United States continues to specify ruggedized capture cards for MIL-STD-qualified programs, while Germany’s automotive tier-ones favor multi-camera inspection cells wired through CoaXPress 2.0 links. Harmonized FDA and IEC pathways streamline vendor compliance in medical imaging, yet the pending IEC 60601-1 Edition 4 upgrade will raise cybersecurity and software lifecycle bars, tilting the advantage toward incumbents with established QMS infrastructures.[4]U.S. FDA, “Standards and Conformity Assessment Program,” fda.gov

South America, the Middle East, and Africa together generated less than 15% of 2025 revenue. Brazil’s automotive hubs offer the largest parcel, but currency swings and capex constraints temper ordering patterns for advanced frame grabbers. Middle Eastern oil and gas complexes deploy machine vision for pipeline inspection and component verification, yet volumes remain modest compared to those in Asia-Pacific fabs. African mining operations adopt vision-based ore sorting where ROI is immediate, though infrastructure and skills gaps slow pervasive rollout. Collectively, these regions require vendor financing models and close integration partnerships to unlock latent demand.

Competitive Landscape

The frame grabber market shows moderate fragmentation: the top five suppliers hold a meaningful but not dominant slice, while niche specialists innovate around FPGA firmware and emerging interface standards. Teledyne DALSA’s Xtium3 PCIe Gen4 card, launched in December 2025, highlights the playbook of leveraging Gen4 throughput and Camera Link HS support to meet the bandwidth demands of semiconductor and flat-panel display inspection. Euresys, BitFlow, and Active Silicon compete on similar high-link-count CoaXPress boards that pair power-over-cable with GPU-direct DMA to shave milliseconds from inference pipelines.

Geographic expansion complements product differentiation. Basler’s Indian acquisition brings local engineering and after-sales support, an advantage as the Asia-Pacific region becomes the fastest-growing market for frame grabbers. KAYA Instruments and Gidel pursue vertical integration by bundling cameras or AI accelerators onto capture cards, pitching a single-vendor solution that trims integration risk. Meanwhile, disruptive pressure comes from smart camera suppliers such as Allied Vision and Zebra Technologies; their embedded Jetson modules suit single-camera stations where a discrete card is overkill. Traditional grabber makers, therefore, emphasize deterministic multi-camera synchronization, FPGA-level pre-processing, and compliance with standards like GenICam to preserve their edge.

Supply-chain resilience is a competitive differentiator. The Atlantic Council’s 2024 study underscored 40-plus-week lead times for certain Xilinx parts, prompting several board vendors to dual-source with Intel Altera devices or lock in long-term supply agreements. Thermal management is another arena; cards aggregating four CXP-12 links now ship with heat-pipe coolers or blower kits to keep FPGA junctions below 80 °C under sustained loads. Vendors that solve these practical hurdles while staying ahead on interface bandwidth will retain a premium share as the frame grabber market evolves.

Frame Grabber Industry Leaders

Teledyne DALSA Inc.

Matrox Electronic Systems Ltd.

BitFlow, Inc.

Euresys SA

Active Silicon Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Teledyne DALSA began volume shipments of the Xtium3 Camera Link HS frame grabber, bundling GPU-direct DMA support for NVIDIA RTX 5000-class cards.

- October 2025: Basler acquired a 76% stake in Alpha TechSys Automation India, securing local systems-integration capacity in the subcontinent.

- June 2025: Euresys released firmware supporting CoaXPress 2.1 cameras at 12.5 Gbps per link and GPU-direct transport.

- February 2025: KAYA Instruments launched the Komodo-III dual-CXP-12 frame grabber with Intel Arria 10 FPGA and PCIe Gen3 x8 host interface.

Global Frame Grabber Market Report Scope

The Frame Grabber Market Report is Segmented by Interface Type (Camera Link, CoaXPress, GigE Vision, USB3 Vision, LVDS and Parallel Digital), Host-Bus and Form Factor (PCIe and PCI Cards, USB External Capture Units, Embedded Boards, M.2 and Thunderbolt Modules), Frame-Rate Capability (Up to 60 FPS, 60-120 FPS, Above 120 FPS), Application Industry (Industrial and Manufacturing, Electronics and Semiconductor Inspection, Medical and Life Sciences, Security and Surveillance, Aerospace and Defense), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Camera Link |

| CoaXPress |

| GigE Vision |

| USB3 Vision |

| LVDS and Parallel Digital |

| PCIe / PCI Cards |

| USB External Capture Units |

| Embedded Boards (PC/104, cPCI) |

| M.2 / Thunderbolt Modules |

| Up to 60 FPS |

| 60 - 120 FPS |

| Above 120 FPS |

| Industrial and Manufacturing |

| Electronics and Semiconductor Inspection |

| Medical and Life Sciences |

| Security and Surveillance |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Interface Type | Camera Link | |

| CoaXPress | ||

| GigE Vision | ||

| USB3 Vision | ||

| LVDS and Parallel Digital | ||

| By Host-Bus / Form Factor | PCIe / PCI Cards | |

| USB External Capture Units | ||

| Embedded Boards (PC/104, cPCI) | ||

| M.2 / Thunderbolt Modules | ||

| By Frame-Rate Capability | Up to 60 FPS | |

| 60 - 120 FPS | ||

| Above 120 FPS | ||

| By Application Industry | Industrial and Manufacturing | |

| Electronics and Semiconductor Inspection | ||

| Medical and Life Sciences | ||

| Security and Surveillance | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the frame grabber market growing from 2026 to 2031?

It is forecast to expand at a 6.32% CAGR, climbing from USD 2.75 billion in 2026 to USD 3.74 billion by 2031.

Which interface standard is gaining the most revenue share?

CoaXPress leads the shift, holding 38.19% share in 2025 and growing at a 6.97% CAGR as 12.5 Gbps-per-link cards proliferate.

What role do smart cameras play in reshaping demand?

Integrated cameras with embedded AI accelerators replace entry-level grabbers in single-camera cells, trimming near-term unit volumes but leaving high-throughput, multi-camera niches intact.

Why is Asia-Pacific the fastest-growing region?

China's semiconductor localization, South Korea's memory packaging, and India's incentive-backed electronics output push regional revenue toward a 7.88% CAGR through 2031.

How does CoaXPress 3.0 influence future hardware roadmaps?

By targeting 25 Gbps per link, CoaXPress 3.0 enables single-cable connections for 200 MP sensors, reinforcing the need for next-generation frame grabbers with PCIe Gen5 or higher host buses.

What differentiates premium frame grabbers from cost-optimized models?

High-end cards integrate FPGA pre-processing, GPU-direct DMA, multi-link synchronization, and on-board memory, whereas entry models focus on basic capture at lower link counts and host-side processing only.

Page last updated on: