Eyewear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

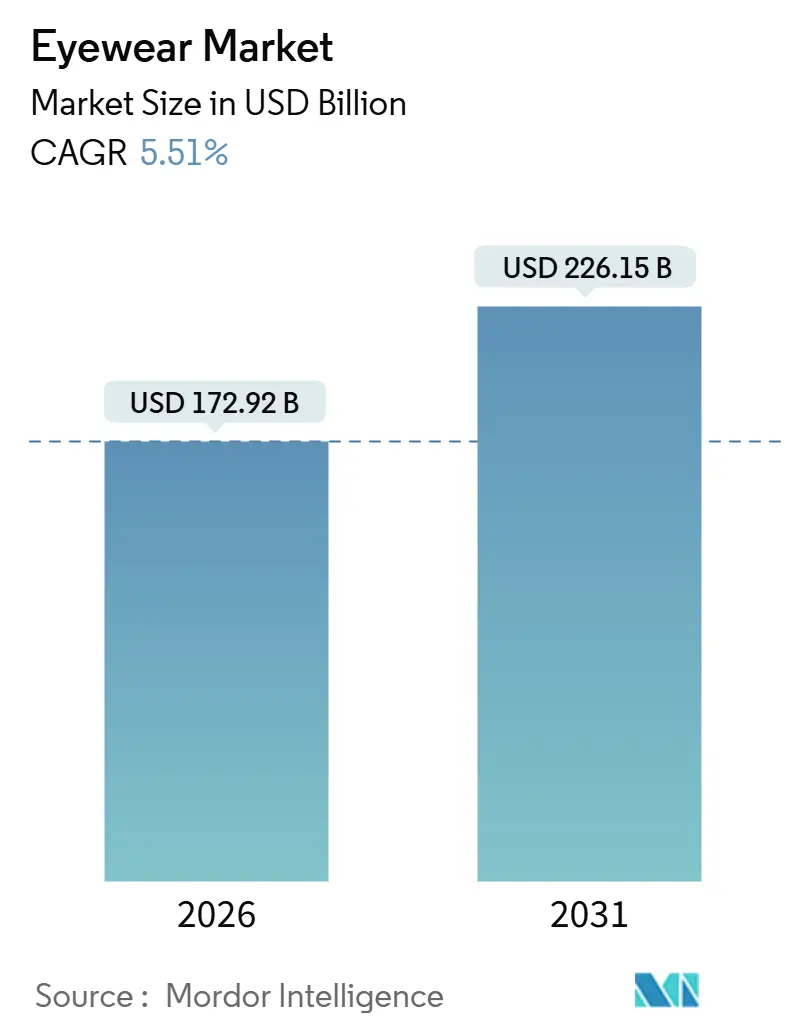

| Market Size (2026) | USD 172.92 Billion |

| Market Size (2031) | USD 226.15 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

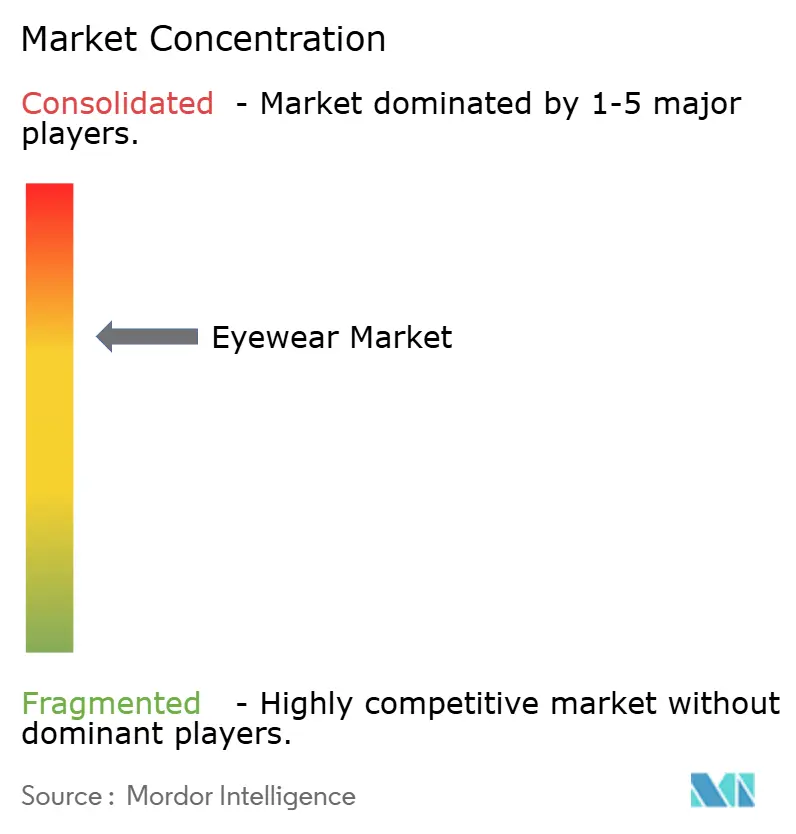

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Eyewear Market Analysis by Mordor Intelligence

The eyewear market reached USD 172.92 billion in 2026 and is forecast to climb to USD 226.15 billion by 2031, reflecting a 5.51% CAGR and confirming a sturdy growth runway for the global market size. Fueled by medical, lifestyle, and technological trends, the eyewear market is witnessing robust growth. The rising prevalence of refractive errors, such as myopia and presbyopia, is driving demand. Factors like extended screen time, an aging population, and urbanization are impacting billions worldwide. As digital eye strain becomes more common, there's an increased demand for blue-light blocking lenses and more frequent eyewear replacements. Beyond vision correction, eyewear has evolved into a fashion statement. Consumers, especially women, Gen Z, and millennials, are gravitating towards designer frames and luxury sunglasses. Their choices, often updated seasonally, are heavily influenced by social media and celebrity endorsements. With growing awareness about UV protection and the pursuit of active lifestyles, segments like sunglasses and sports eyewear are seeing a surge. Smart glasses are carving a niche, merging fashion with technology. The collaboration between Ray-Ban and Meta underscores that wearable AI can harmoniously blend with aesthetics. Additionally, the consolidation of luxury brands, workplace mandates emphasizing blue-light protection, and stringent actions against counterfeit goods are amplifying demand signals while simultaneously raising entry barriers.

Key Report Takeaways

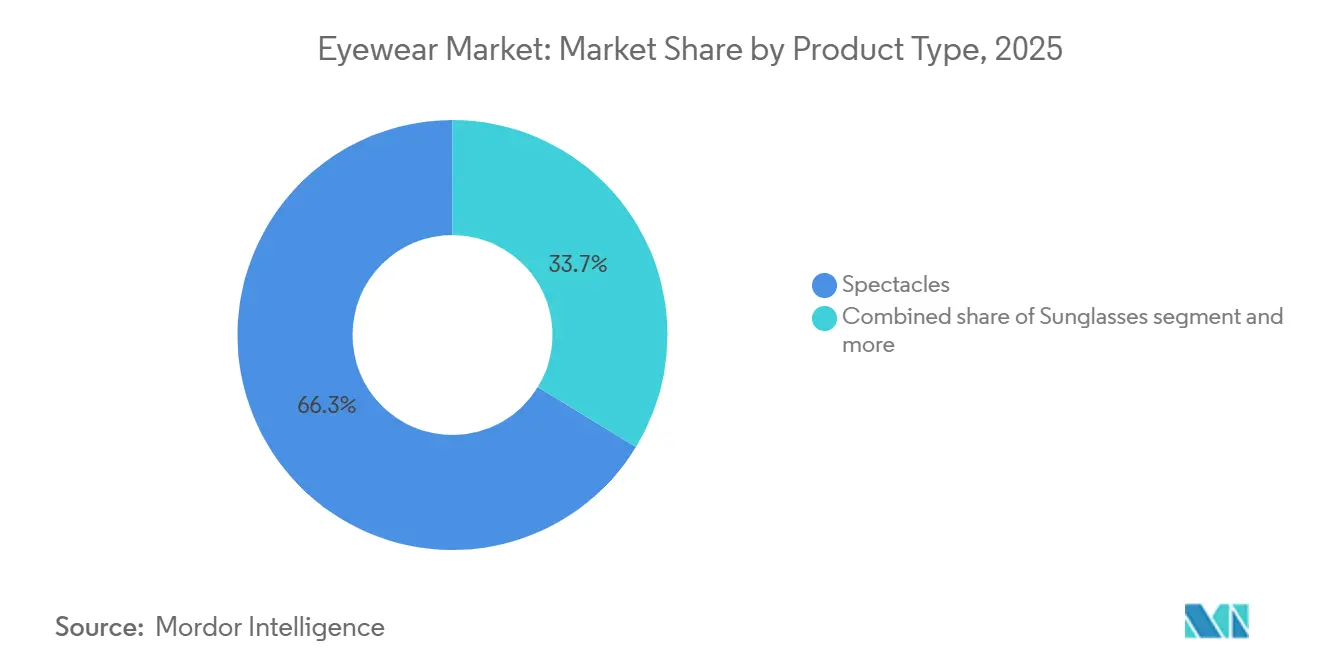

- By product type, spectacles led with 66.28% revenue share in 2025, while sunglasses are projected to expand at a 6.72% CAGR through 2031.

- By category, the mass segment held 67.54% of the eyewear market share in 2025, whereas premium eyewear is expected to grow at a 6.12% CAGR to 2031.

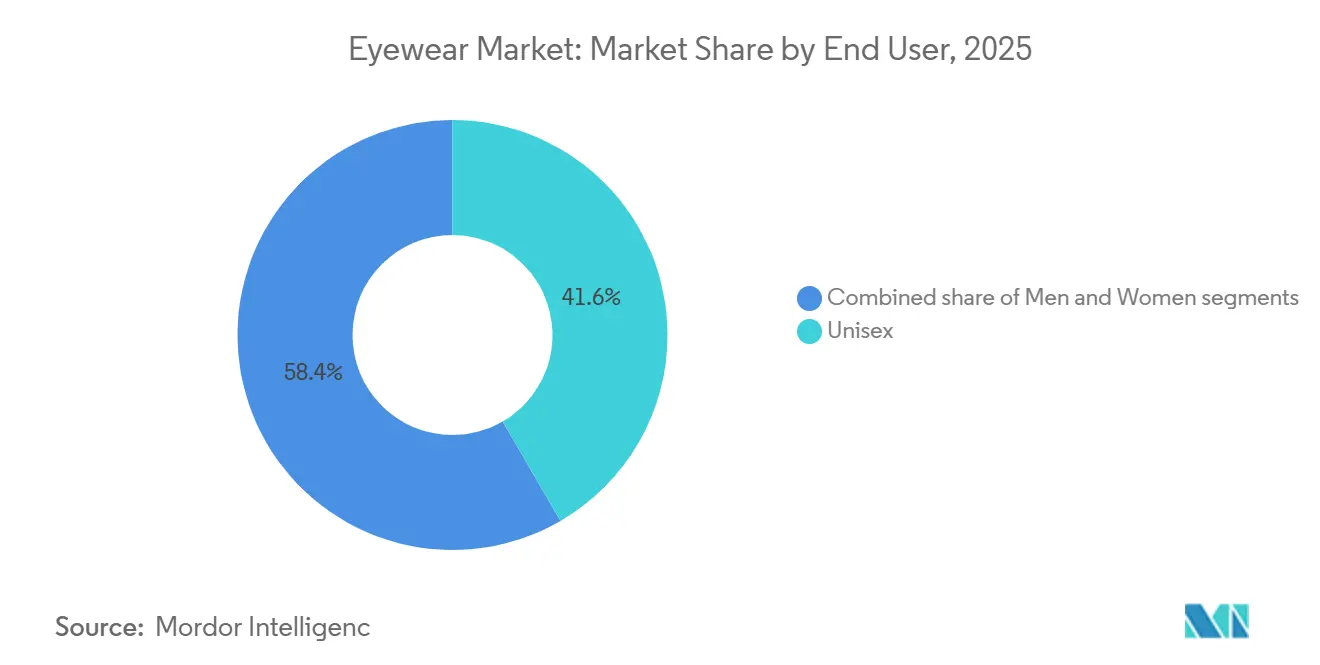

- By end user, unisex frames accounted for 41.63% of the eyewear market size in 2025, yet women’s eyewear is advancing at a 5.88% CAGR through 2031.

- By distribution channel, offline stores represented 83.11% of sales in 2025, while online channels are predicted to post a 6.85% CAGR to 2031.

- By geography, North America held 32.96% of 2025 revenue, and Asia-Pacific is poised for the quickest expansion at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Eyewear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for luxury and premium sunglasses | +1.2% | Global, concentrated in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing prevalence of vision problems | +1.8% | Global, acute in Asia-Pacific (China, India) and Sub-Saharan Africa | Long term (≥4 years) |

| Technological advancements and smart eyewear | +0.9% | North America, Europe, early adoption in Japan and South Korea | Short term (≤2 years) |

| Growing awareness of UV protection and eye health | +0.7% | Global, regulatory-driven in North America and Europe | Medium term (2-4 years) |

| Influence of celebrity endorsements and social media | +0.6% | Global, strongest in North America, Europe, and urban Asia-Pacific | Short term (≤2 years) |

| Blue-light protection mandates in workplaces | +0.4% | North America, Europe, emerging in Asia-Pacific corporate sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for luxury and premium sunglasses

Premium sunglasses are increasingly marketed as a lifestyle choice, emphasizing UV protection not just as a necessity but as a statement. This trend is underscored by EssilorLuxottica's USD 1.5 billion acquisition of Supreme in July 2024, a move that melds streetwear's allure with optical retail. LVMH's November 2023 acquisition of Barton Perreira further underscores the industry's tilt towards vertical integration. Established players, equipped with in-house testing labs, find an advantage in navigating regulatory hurdles like ISO 12312-1:2022, which sets stringent UV transmittance and impact resistance standards for sunglasses. As disposable incomes rise, a broader swath of consumers can now indulge in premium and luxury sunglasses, transcending mere functionality. Data from the U.S. Bureau of Economic Analysis, accessed via FRED, highlighted that the Real Disposable Personal Income in the U.S. reached USD 18,040.2 in September 2025 [1]Source: Federal Reserve Bank, "Real Disposable Personal Income", fred.stlouisfed.org. With this financial flexibility, consumers are leaning towards quality craftsmanship, exclusivity, and brand prestige. This shift fuels a heightened demand for limited-edition collections, sustainable materials, and technologically advanced lenses, sidelining mass-market alternatives.

Increasing prevalence of vision problems

The global rise in refractive errors, including myopia, hyperopia, and astigmatism, is fueling the demand for prescription sunglasses that provide both vision correction and UV protection. According to the World Health Organization, at least 2.2 billion people worldwide experience near or distance vision impairments, emphasizing the substantial market potential for vision correction solutions [2]Source: World Health Organization, "Blindness and Vision Impairment", who.int. . Myopia, in particular, has surged dramatically, especially in Asia. In nations such as China, Japan, Singapore, and South Korea, 80-90% of teenagers and young adults are now myopic, making it a significant public health concern [3]Source: American Academy of Ophthalmology, "Sharp Rise in Myopia Around the World", aao.org. Advancements in photochromic lens technology are driving growth in the prescription sunglasses market by improving functionality. In April 2024, Indizen Optical Technologies of America (IOT America) introduced Neochromes FT-28 flat-top polycarbonate photochromic lenses, enhancing the bifocal lens segment with improved light-adaptive features and durability. Increasing screen time has led to a rise in digital eye strain, boosting the adoption of blue light filtering lenses. Additionally, aging populations in developed markets are sustaining demand for specialized vision correction products in the eyewear market.

Technological advancements and smart eyewear

In July 2024, Meta, in partnership with EssilorLuxottica, introduced AI-powered Ray-Ban smart glasses. These glasses combine fashion with wearable technology, offering features like voice assistants and hands-free photography. To strengthen this collaboration, Meta is considering acquiring an equity stake in EssilorLuxottica. Similarly, Snap Inc. launched its Spectacles 5 in September 2024. With a USD 99 monthly developer subscription, these glasses feature augmented reality displays. However, Snap is targeting enterprise applications such as retail visualization and remote assistance, rather than the mass market. The United States Food and Drug Administration approved 12 new contact lens designs for 2024-2025. Key approvals include Johnson and Johnson Vision's Acuvue Oasys Max 1-Day with TearStable Technology and CooperVision's MiSight 1-day for myopia control. These approvals reflect a regulatory focus on incremental innovations rather than disruptive smart lens technologies. Furthermore, blue-light filtering coatings, now widely included in North American prescription lenses, comply with ISO 12312-1:2022 and ANSI Z80.3-2018 standards. Their adoption, primarily driven by optometrist recommendations instead of consumer demand, underscores the influence of professionals in shaping technology adoption over marketing efforts.

Growing awareness of UV protection and eye health

The World Health Organization identifies UV exposure as a contributing factor in 20% of cataract cases. This has prompted national health agencies to promote UV400-rated lenses in public health campaigns. However, compliance remains largely voluntary outside Australia and New Zealand, where the Therapeutic Goods Administration mandates UV transmittance labeling on all sunglasses. In the United States, the Food and Drug Administration enforces 21 CFR Part 886.5844, which requires impact resistance for prescription lenses but does not establish specific UV protection thresholds. This regulatory gap allows premium brands to market UV400 as a distinguishing feature. Additionally, the ISO 12312-1:2022 standard has reduced UV transmittance limits for Category 2-4 sunglasses to below 5% and introduced impact resistance testing at speeds of 162 kilometers per hour. These changes have increased compliance costs, particularly for manufacturers without in-house testing capabilities. Clinical evidence linking UV exposure to conditions such as pterygium and macular degeneration supports optometrists' recommendations for polarized lenses, which are priced higher than non-polarized alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.8% | Global, concentrated in Asia-Pacific (China, Hong Kong) and distributed via e-commerce | Short term (≤2 years) |

| Vision correction surgeries | -0.5% | North America, Europe, urban Asia-Pacific with high disposable income | Medium term (2-4 years) |

| Fluctuating raw material prices | -0.6% | Global, acute in regions dependent on imported acetate, polycarbonate, titanium | Short term (≤2 years) |

| High costs of research, design, and technology | -0.4% | Global, disproportionately affects smaller brands without R&D scale | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

In 2024, the European Union seized 112 million counterfeit items with an estimated value of EUR 3.8 billion, emphasizing the persistent challenges in combating counterfeiting activities. The European Union's Regulation 608/2013 grants member states the authority to detain suspected counterfeit goods at borders; however, enforcement practices differ significantly across the region, leading to varying levels of effectiveness. The World Intellectual Property Organization's 2024 report highlights that eyewear ranks as the fourth most valuable category among seized counterfeit goods, following pharmaceuticals, electronics, and apparel. This ranking reflects counterfeiters' strategic exploitation of low manufacturing costs to produce and distribute fake products. To address this issue, EssilorLuxottica has implemented an e-Recordation program in collaboration with U.S. Customs and Border Protection. This program facilitates real-time alerts whenever shipments matching registered trademarks are detected entering the U.S., thereby reducing the infiltration of counterfeit goods. Nonetheless, this initiative requires substantial investments in legal frameworks and compliance infrastructure to ensure its success.

Vision correction surgeries

The United States Food and Drug Administration states that LASIK and photorefractive keratectomy procedures reduce reliance on distance-vision eyewear but do not fully address presbyopia, which typically develops between ages 40 and 45. This limitation mitigates the long-term risk of spectacle demand erosion. Refractive surgery adoption is primarily concentrated in high-income markets, with North America and Europe accounting for a significant share of procedures. In contrast, regions such as Asia-Pacific, Latin America, and the Middle East experience lower adoption rates due to cost-related barriers. The American Academy of Ophthalmology's 2025 guidelines recommend against LASIK for individuals with thin corneas, autoimmune disorders, or unstable prescriptions, excluding approximately 30% of myopic candidates and maintaining a baseline demand for corrective eyewear. Meanwhile, contact lens manufacturers like Johnson and Johnson Vision and CooperVision promote myopia control lenses such as Acuvue Oasys Max and MiSight 1 day as alternatives to refractive surgery for pediatric patients. This approach addresses parental concerns about surgical risks while fostering early brand loyalty that extends into adulthood.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spectacles Anchor Volume, Sunglasses Capture Premiumization

In 2025, spectacles dominated the market with a substantial 66.28% share. This dominance is primarily driven by the global need for distance-vision correction and the increasing demand for presbyopia lenses. The rising prevalence of myopia, presbyopia, and digital eye strain, largely caused by prolonged exposure to screens, has significantly boosted the demand for prescription lenses. Additionally, contact lenses are witnessing growth due to the Food and Drug Administration approvals aimed at controlling myopia, further diversifying the eyewear market. Other product categories, such as sports eyewear and safety goggles, remain niche, catering to specific consumer needs. The updated ISO 12870:2024 standard for spectacle frames has introduced durability testing for bio-based acetate materials. This advancement enables brands like Warby Parker and Fielmann to highlight their sustainability efforts while maintaining price competitiveness with traditional petroleum-based alternatives.

The sunglasses segment, however, is projected to grow at a robust 6.72% CAGR through 2031. This growth is largely attributed to the consolidation of luxury brands within the market. Key developments include EssilorLuxottica's USD 1.5 billion acquisition of Supreme in July 2024 and LVMH's USD 80 million purchase of Barton Perreira in November 2023. These strategic acquisitions underscore the profitability of the premium sunglasses segment, which boasts gross margins of 50-70%, significantly higher than the 30-40% margins associated with prescription spectacles. The trend of premiumization, driven by the appeal of designer brands, the influence of social media, and technological innovations such as polarized and smart lenses, has encouraged frequent upgrades. This is particularly evident among younger demographics and affluent consumers, who are drawn to the combination of functionality and luxury offered by these products.

By Category: Mass Dominates Volume, Premium Captures Margin Expansion

In 2025, the mass segment secures a dominant 67.54% share of the market. This segment thrives on the high-volume production of standardized eyewear designs, which allows for cost-efficient manufacturing. The resulting affordability appeals strongly to price-sensitive consumers across both urban and rural regions, making it the primary driver of global demand. The mass segment primarily serves emerging markets, addressing the needs of a broad consumer base that relies on essential prescription glasses for conditions such as myopia and presbyopia, as well as for daily use. In these regions, middle- and lower-income groups often prioritize functionality and affordability over aesthetic appeal, further solidifying the segment's position in the market.

Conversely, premium eyewear is projected to grow at a 6.12% CAGR through 2031. This growth is fueled by EssilorLuxottica's strategic licensing agreements with luxury brands such as Prada, Chanel, and Versace. These collaborations capitalize on red-carpet exposure, supporting retail prices ranging from USD 300-800 for frames that cost USD 30-80 to produce. Additionally, LVMH's Thélios division, following its November 2023 acquisition of Barton Perreira, now manufactures eyewear for high-end brands like Dior, Fendi, and Celine. This shift eliminates royalty payments, previously 8-12% of wholesale revenue, and accelerates design-to-market timelines from 18 months to 12 months. Furthermore, compliance with ISO 12312-1:2022 standards, which incurs costs of USD 50,000-200,000 per product line for UV transmittance and impact resistance testing, poses a significant challenge for mass-market players. Premium brands, equipped with in-house laboratories, easily meet these regulatory requirements, creating a substantial barrier for new entrants.

By End User: Unisex Frames Dominate, Women's Segment Outpaces Growth

In 2025, unisex eyewear accounts for 41.63% of the market share, driven by minimalist designs such as aviators, wayfarers, and round frames. These styles appeal to cost-conscious consumers who value versatility. Brands like Warby Parker and Zenni Optical focus on unisex SKUs to streamline inventory management. Unisex frames accommodate various face shapes and styles, enabling retailers to eliminate the need for separate men's and women's lines. This broad appeal targets consumers seeking adaptable, minimalist eyewear. By incorporating neutral colors, classic shapes, and timeless designs, brands cater to shared family purchases and style-fluid consumers, boosting sales volumes. The growing emphasis on inclusivity, gender fluidity, and social media-driven trends supports the demand for unisex products, particularly among younger generations, such as Gen Z and millennials, who prioritize comfort over traditional gender norms.

On the other hand, women's eyewear is experiencing significant growth, with a 5.88% CAGR projected through 2031. This growth is driven by gender-specific designs, including cat-eye and oversized frames, which command a 20-30% price premium compared to unisex alternatives. EssilorLuxottica's Ray-Ban and Oakley Women's lines are expected to generate USD 2.5 billion in revenue in 2024. Celebrity endorsements play a pivotal role in the success of women's eyewear. For example, Lenskart's expansion in India heavily relies on Bollywood partnerships. Actress Katrina Kaif's endorsement has contributed to 25% of the brand's new customer acquisitions in 2024, highlighting the influence of regional celebrities over global brand recognition in emerging markets. However, challenges persist. The U.S. Federal Trade Commission updated its endorsement disclosure guidelines in 2024, requiring influencers to clearly label paid partnerships. While this initiative enhances transparency, it also increases compliance costs for brands managing multi-tier influencer networks.

By Distribution Channel: Offline Retains Dominance, Online Accelerates Disruption

In 2025, offline stores hold an 83.11% market share, supported by optician-led consultations, streamlined insurance reimbursements, and quick lens fittings. The hands-on nature of eyewear, requiring precise fittings for comfort and functionality, ensures the dominance of physical stores. Opticians enhance this experience by providing on-site eye exams, customized adjustments, and immediate product trials, which build consumer confidence for significant purchases. On the other hand, online stores are experiencing growth, with a 6.85% CAGR projected through 2031. This growth is driven by features such as virtual try-ons, wide product ranges, competitive pricing, and the convenience of home delivery, which appeal to tech-savvy younger consumers.

Lenskart illustrates this trend with its omnichannel strategy, integrating online orders with offline fittings. This approach highlights the importance of physical touchpoints in emerging markets, addressing consumer concerns about purchasing eyewear online. Similarly, Fielmann is expanding across Europe by strategically opening flagship stores in high-traffic urban areas like Berlin, Paris, and Milan. These stores combine retail with in-store optometry and lens grinding services, reducing fulfillment times from the standard 7-10 days to same-day delivery, providing a competitive edge over online-only players. Additionally, the U.S. Federal Trade Commission updated its Contact Lens Rule in 2024, requiring prescribers to provide patients with copies of their prescriptions. This change enables online retailers such as 1-800 Contacts and Lens.com to capture a significant 30% share of the U.S. contact lens market.

Geography Analysis

In 2025, North America accounted for 32.96% of the revenue, supported by Food and Drug Administration mandates on impact resistance that increased the costs of imported lenses. Strong enforcement against counterfeiting further protected premium pricing. In Canada, provincial subsidies, along with Mexico's growth in developing markets, contributed to volume growth. Although LASIK demand moderated growth, it did not hinder it entirely. High disposable incomes, extensive vision insurance coverage, and a preference for premium brands like Ray-Ban and Oakley drove higher per-capita spending, strengthening the region's value share compared to volume-driven regions.

Asia-Pacific is projected to achieve the fastest regional CAGR of 6.67%. India's policy changes increasingly support local production, while China's accelerated approval processes create opportunities for new market entrants. Japan's aging population continues to fuel repeat purchases, particularly for presbyopia-related products. Lenskart's rapid store expansions underscore the growing success of omnichannel retailing. Europe shows consistent growth despite uneven enforcement against counterfeiting. In the United Kingdom, NHS voucher programs support demand for basic spectacles. Germany's Fielmann differentiates itself with same-day fulfillment services. Meanwhile, medical device companies like Carl Zeiss focus on high-margin diagnostic equipment, intensifying competition in the consumer eyewear market.

South America is progressing, with Brazil's ANVISA registration rules protecting established brands. In Argentina, inflation is pushing consumers toward mass-market frames, but installment plans help sustain sales volumes. Chile's free school spectacle programs are building brand familiarity that persists into adulthood. The Middle East and Africa present growth opportunities, driven by Saudi Arabia's healthcare funding and the United Arab Emirates's ISO 13485 import regulations that ensure quality. Despite ongoing fragmentation in South Africa and Nigeria, chain expansions and local sourcing are beginning to reduce consumer prices. These varied geographical trends not only mitigate risks in the eyewear market but also ensure diversified revenue streams across regions.

Competitive Landscape

The eyewear market exhibits moderate consolidation, with established companies strengthening their positions through strategic partnerships. These major players leverage their vast distribution networks, diverse brand portfolios, and robust manufacturing capabilities to maintain a competitive edge. Such partnerships not only bolster joint research efforts but also promote technology sharing and synchronized market expansion. Key players in the market include Safilo Group S.p.A., Fielmann AG, EssilorLuxottica SA, The Cooper Companies, Inc., and Johnson & Johnson.

Technology giants are reshaping the competitive dynamics. Meta and Apple, vying for dominance in augmented reality (AR), are weaving their ecosystems into eyewear, featuring virtual displays, gesture controls, and seamless device connectivity. Meanwhile, regional player Lenskart is broadening its horizons with omnichannel strategies, highlighted by its Owndays acquisition in Japan. This expansion spans physical retail, e-commerce, and innovative digital try-on solutions. Mid-tier brands are carving out niches with sustainable materials, 3-D printing, and AI-driven sizing, offering biodegradable frames and bespoke designs. To counteract counterfeiting, companies are adopting blockchain tracking and micro-engraving, a move that, while elevating operational costs, bolsters consumer trust.

Luxury titans LVMH and Kering view eyewear as a lucrative extension, snapping up design houses and licenses to maximize value. Regional players like Fielmann, Devlyn, and Specsavers are consolidating fragmented markets with their omnichannel approaches, intensifying competition for independent retailers. The threat of counterfeits drives continuous investments in authentication tech and collaboration with customs, incurring compliance costs but safeguarding brand integrity.

Eyewear Industry Leaders

-

Safilo Group S.p.A.

-

Fielmann AG

-

EssilorLuxottica SA

-

The Cooper Companies, Inc.

-

Johnson and Johnson AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rokid, a Chinese augmented reality (AR) glasses manufacturer, launched new AR Spatial eyewear globally through AliExpress, Alibaba Group Holding's e-commerce platform, as it expands internationally amid increasing market competition.

- May 2025: Lawaken launched three new AI smart glasses models in Hefei: the Lawaken City AI Glasses (Fashion Edition), the Lawaken City Air AI Glasses (Business Edition), and the Lawaken View AI Glasses (Travel Edition).

- April 2025: Finnish eyewear company IXI secured USD 36.5 million in Series A funding to introduce autofocus glasses. The company aims to transform traditional prescription eyewear into technology-enhanced accessories for contemporary users.

- February 2025: Lenskart, a manufacturer of prescription glasses and sunglasses, introduced its first smartglasses with Bluetooth audio capabilities in India. The new Phonic smartglasses enable users to listen to music, interact with voice assistants, and make voice calls without the need for separate audio devices, such as headphones or earphones.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the global eyewear market as the value of all new spectacles, sunglasses, and contact lenses sold through retail and e-commerce channels for vision correction or eye protection, inclusive of prescription and plano lenses, across consumer and professional end users in more than forty countries. Guided by that definition, we track revenues in USD from 2020 and model forward to 2030.

Scope Exclusion: This assessment does not include aftermarket accessories such as cases, cleaning solutions, or smart-glasses electronics sold separately.

Segmentation Overview

-

By Product Type

- Spectacles

- Sunglasses

- Contact Lenses

- Other Product Types

-

By Category

- Mass

- Premium

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Offline Stores

- Online Stores

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with optometrists, optical retailers, pure-play e-commerce operators, and lens-material suppliers across North America, Europe, and Asia-Pacific let us confirm unit-demand swings, online penetration, and promotional pricing trends. Surveys of spectacle owners verified replacement cycles and lens-upgrade rates, enabling our team to refine preliminary desk estimates.

Desk Research

We pulled population-weighted prevalence of refractive errors, cataract-surgery backlogs, and age-cohort projections from sources such as the WHO Vision Atlas, United Nations DESA, and national health surveys. Trade statistics from UN Comtrade, retail scanner data released by Eurostat, and price indices issued by the U.S. Bureau of Labor Statistics anchored volumes and average selling prices. Company 10-Ks, investor presentations, and news retrieved via our D&B Hoovers and Dow Jones Factiva subscriptions revealed channel mix shifts and brand pricing ladders. The sources noted are illustrative; many additional publications informed data collection, validation, and clarifications.

Market-Sizing & Forecasting

Mordor analysts apply a top-down and bottom-up blend. We size the addressable pool by multiplying country-level vision-impairment cohorts with eyewear-penetration rates, which are then reconciled against import, production, and channel-revenue tallies. Inputs include myopia prevalence, per-capita disposable income, lens-replacement intervals, sunglass seasonality indices, and online share of optical spend. A multivariate regression model links demand to those drivers; exponential smoothing projects each driver, while scenario analysis tests high and low adoption of premium coatings. Gaps in bottom-up brand roll-ups are bridged by regional channel checks and sampled ASP × volume validations.

Data Validation & Update Cycle

Triangulation runs through every step. Anomalous variances trigger expert re-contact, and senior reviewers audit formulas before sign-off. Reports refresh annually, with interim updates when currency shocks or regulatory shifts materially alter growth outlooks.

Why Mordor's 2025 Eyewear Baseline Earns Decision-Makers' Trust

Published estimates often diverge because product baskets, price definitions, and refresh cadences vary. Our analysts disclose scope choices up-front and keep currency conversions fixed to IMF averages, limiting noise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 162.26 B | Mordor Intelligence | |

| USD 181.75 B | Global Consultancy A | Includes goggles and safety frames; uses list prices, not net sales |

| USD 221.90 B | Industry Journal B | Assumes aggressive premium mix and higher e-commerce markups |

| USD 162.80 B | Regional Consultancy C | Excludes contact-lens revenues, counts only spectacles and sunglasses |

Differing inclusions or price treatments can inflate or deflate totals. By anchoring estimates to transparent drivers and repeatable checks, Mordor Intelligence provides a balanced, dependable baseline for strategic decisions.

Key Questions Answered in the Report

What is the predicted value of the global eyewear market in 2031?

The market is forecast to reach USD 226.15 billion by 2031, expanding at a 5.51% CAGR.

Which product type is expected to grow fastest over the next five years?

Sunglasses are set to record the highest growth, with a 6.72% CAGR through 2031.

Why is Asia-Pacific considered the most attractive growth region?

Policy incentives for local production, rapid store rollouts, and heightened vision-care awareness underpin a 6.67% CAGR outlook.

How are smart glasses influencing competitive dynamics?

Partnerships like Ray-Ban Meta blend fashion with AR functionality, creating a new premium segment that established optical players are well-placed to serve.

Page last updated on: