Reading Glasses Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

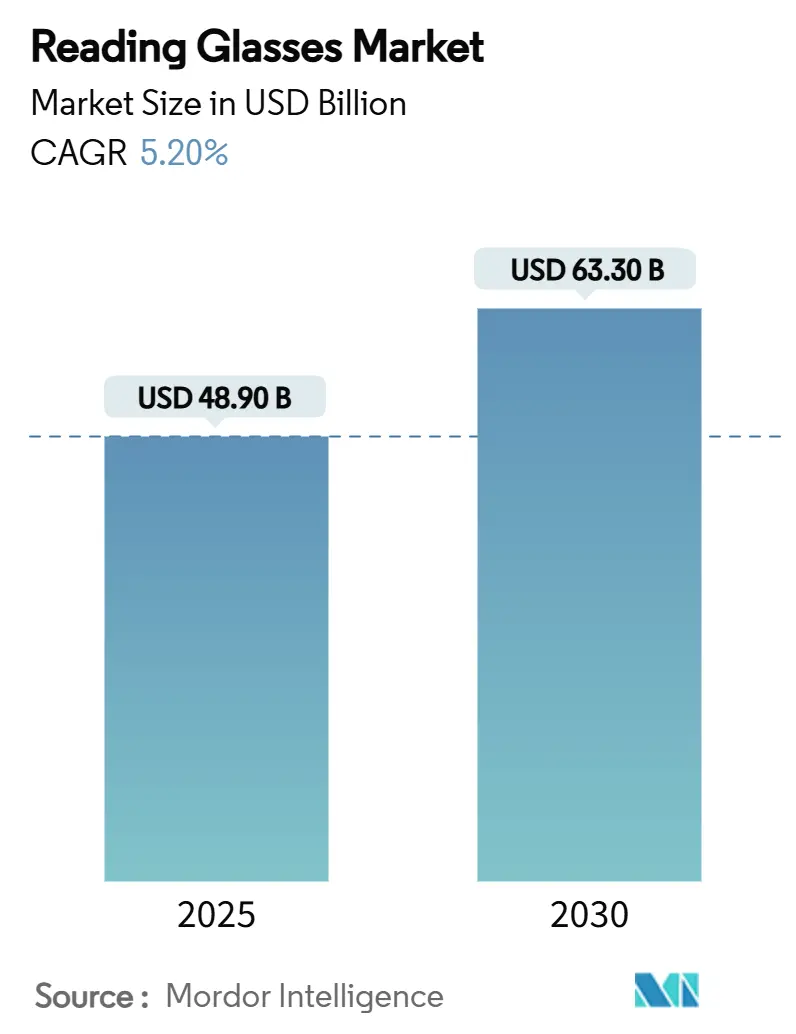

| Market Size (2025) | USD 48.90 Billion |

| Market Size (2030) | USD 63.30 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

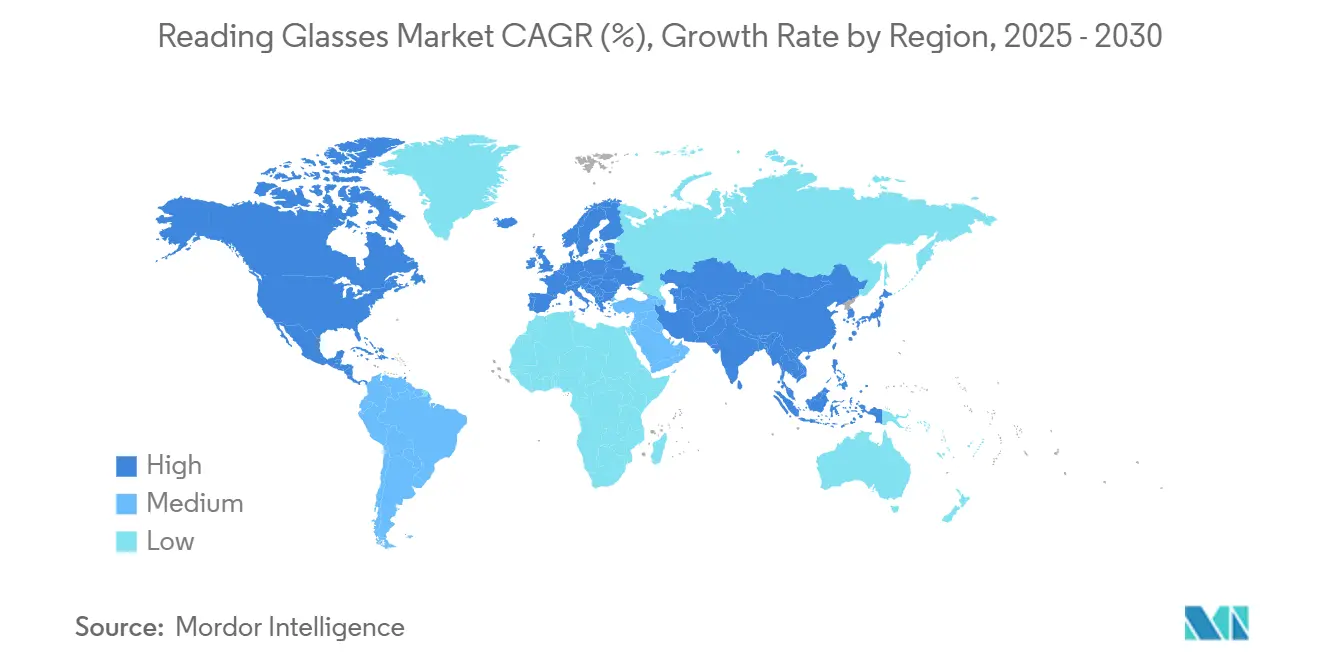

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reading Glasses Market Analysis by Mordor Intelligence

The reading glasses market size stood at USD 48.9 billion in 2025 and is on course to reach USD 63.3 billion by 2030, reflecting a robust 5.20% CAGR through the forecast period. Global presbyopia prevalence now affects 1.8 billion people and will rise to 2.1 billion by 2030, ensuring a steady flow of new consumers into the reading glasses market.[1]British Contact Lens Association, “BCLA CLEAR Presbyopia: Epidemiology and Impact,” sciencedirect.comDemand is reinforced by rising screen exposure, premiumization of frames, and the rapid growth of online direct-to-consumer (D2C) channels. North America retains leadership owing to high disposable incomes and fashion-centric consumers, yet Asia Pacific posts the quickest gains as urbanization, smartphone use, and expanding middle-class spending converge. Meanwhile, technology players are injecting smart-wearable capabilities, creating fresh competitive battlegrounds, and unlocking adjacent revenue streams such as software subscriptions.

Key Report Takeaways

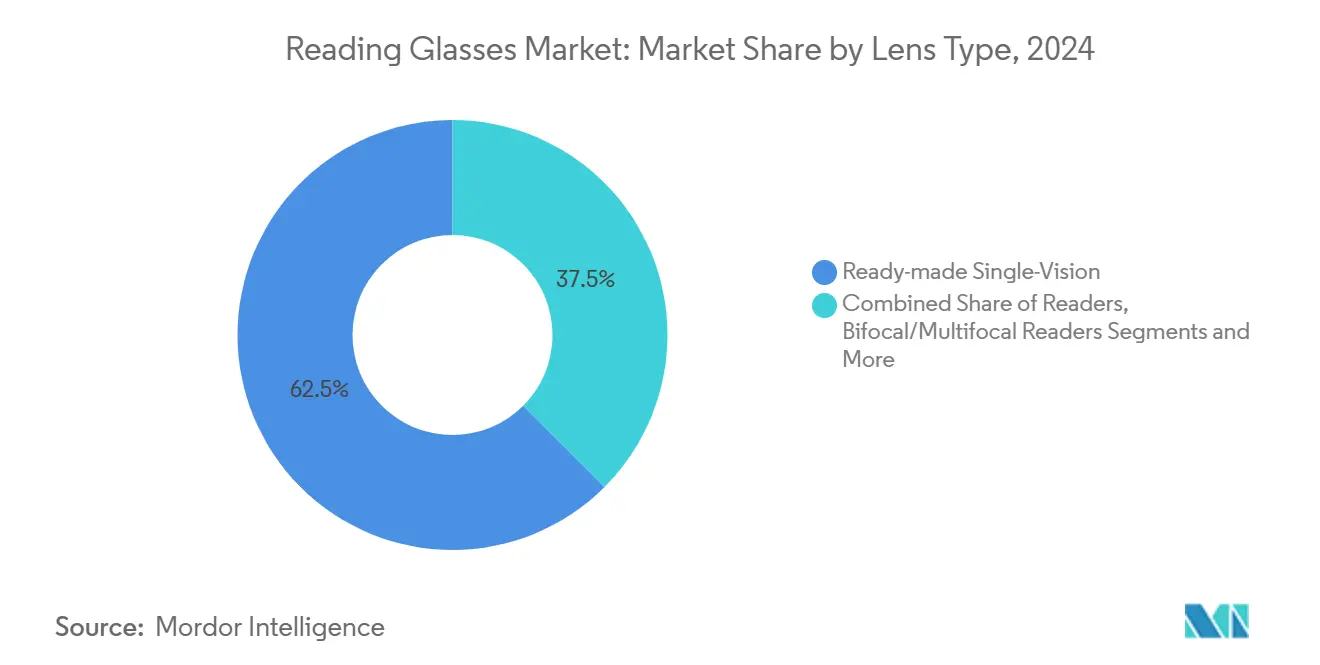

- By lens type, ready-made single-vision readers captured 62.5% of reading glasses market share in 2024, whereas blue-light-blocking readers are forecast to progress at a 7.1% CAGR through 2030.

- By power range, the +2.00 to +2.75 D segment accounted for 44.7% share of the reading glasses market size in 2024, while the +0.75 to +1.75 D band is projected to expand at a 6.8% CAGR to 2030.

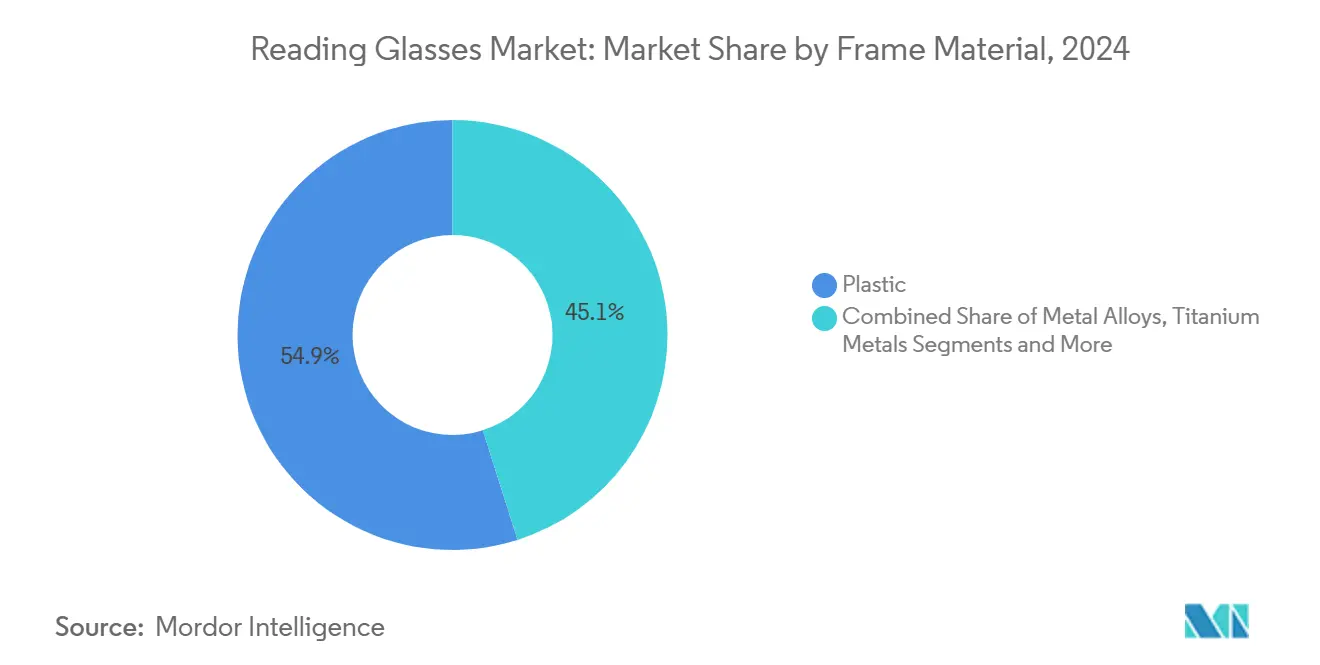

- By frame material, plastic frames dominated with 54.9% share in 2024; bio-based and recycled variants advance at a 5.4% CAGR during the same period.

- By distribution channel, optical retail stores held 38.2% share of the reading glasses market size in 2024 and e-commerce D2C remains the fastest mover at an 8.2% CAGR through 2030.

- By geography, North America led with 37.4% revenue share in 2024, whereas Asia Pacific is poised for a 6.3% CAGR to 2030.

Global Reading Glasses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population with rising presbyopia prevalence | +1.80% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Higher digital-screen time driving earlier onset of near-vision fatigue | +1.20% | Global, strongest in APAC urban centers | Medium term (2 - 4 years) |

| Expansion of low-cost OTC readers in mass-merchandise retail & e-commerce | +0.90% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Fashion-driven premiumisation of reading frames | +0.70% | North America & Europe, emerging in APAC metros | Medium term (2 - 4 years) |

| Workplace safety regulations mandating impact-rated Rx readers in industrial PPE | +0.40% | North America & Europe, selective APAC markets | Long term (≥ 4 years) |

| Emerging “smart-reader” devices integrating eye-strain sensors & AR overlays | +0.30% | North America & Europe early adoption, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population with Rising Presbyopia Prevalence

Presbyopia now impacts 128 million Americans and 2 billion people worldwide, a figure that will continue to climb as global life expectancy rises. The condition’s universal onset near age 40 secures a predictable intake of consumers into the reading glasses market. In the United States, more than 60% of presbyopes rely on reading glasses as the primary correction method, assuring a stable repeat-purchase pattern. Even as progressive lenses or surgical alternatives emerge, functional presbyopia prevalence remains at 24.1%, keeping sheer unit volumes on an upward slope. This demographic swell offsets downward price pressure from mass retail channels and sustains steady revenue growth for both legacy optical players and new entrants.

Higher Digital-Screen Time Driving Earlier Onset of Near-Vision Fatigue

Two-thirds of U.S. adults who spend extended hours on digital devices report glare, discomfort, and blurred vision, symptoms linked to earlier presbyopia onset. Screen fatigue now appears 5 - 10 years ahead of the typical age-related onset, swelling the younger consumer base of the reading glasses market. Blue-light exposure from smartphones and laptops disrupts circadian rhythm, propelling demand for blue-light-blocking lenses that command 20 - 40% premiums over standard readers. Remote-work normalisation post-pandemic further entrenches long-screen habits, especially across Asia Pacific cities with smartphone penetration above 80%. Consequently, specialty computer-specific readers have shifted from niche to mainstream, sustaining double-digit online sales growth for leading D2C brands.

Expansion of Low-Cost OTC Readers In Mass-Merchandise Retail & E-Commerce

Aggressive pricing by mass retailers and online marketplaces reduces barriers to vision correction, widening penetration in underserved regions. Walmart’s network now exceeds 3,000 Vision Centers, enhanced by virtual try-on technology that lets shoppers finalize purchases within minutes. E-commerce platforms compress distribution costs and empower brands to deliver prescription-grade readers at 50 - 70% discounts versus conventional optical stores. Price transparency on Amazon and other marketplaces pressures brick-and-mortar operators to differentiate through eye-care services and curated assortments. For emerging markets where optical infrastructure is thin, low-cost OTC readers fill an essential healthcare gap and add incremental volume to the reading glasses market.

Fashion-Driven Premiumization of Reading Frames

Reading glasses have evolved from mere medical aids into style statements, with premium materials and designer collaborations fetching 200 - 300% premiums over basic products. Affluent baby boomers in North America and Europe treat frames as accessories, often buying several pairs to complement their wardrobes. Luxury brands use celebrity partnerships and social-media campaigns to nurture aspirational positioning, while vertical D2C players exploit quick design cycles to keep collections fresh. Premiumization lifts average selling prices and offsets volume softness in mature markets, bolstering margin resilience for manufacturers that can blend style with optical performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Penetration of multifocal & progressive lens prescriptions replacing OTC readers | -0.80% | North America & Europe primarily, expanding globally | Medium term (2 - 4 years) |

| Growing adoption of refractive surgery & in-office presbyopia treatments | -0.60% | North America & Europe, selective APAC metros | Long term (≥ 4 years) |

| Price pressure from dollar-store/private-label readers | -0.40% | Global, most intense in price-sensitive markets | Short term (≤ 2 years) |

| Environmental pushback against single-use plastic frames escalating compliance | -0.20% | Europe leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Penetration Of Multifocal & Progressive Lens Prescriptions Replacing OTC Readers

Advances in progressive-lens design reduce adaptation discomfort, narrowing the performance gap between prescription eyewear and OTC readers.[2]CORDIS, “Adaptive Eyeglasses Offer Clear Vision for Those With Presbyopia,” cordis.europa.euInsurance coverage often covers a significant portion of prescription lens cost, making a single multifocal pair financially competitive against multiple OTC readers. Optometrists increasingly advocate progressive solutions that correct distance and near vision simultaneously, trimming replacement frequency for standalone readers. Lens innovators such as EssilorLuxottica’s Stellest series further elevate performance, siphoning potential volume from the reading glasses market even as unit economics for prescriptions improve.

Growing Adoption of Refractive Surgery & In-Office Presbyopia Treatments

FDA approval of Vuity eye drops introduces the first pharmaceutical pathway to offset presbyopia, nudging patients toward clinical interventions. Rapid-recovery laser procedures and intraocular lens implants also appeal to active consumers wanting permanent correction. Although cost and surgical risk limit adoption to higher-income groups, growing awareness and clinician marketing erode a slice of future demand. Over time, these therapies may slow growth rates in affluent urban centers, especially where private insurance reimburses elective vision care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lens Type: Premium Filters and Smart Functions Shift Value Creation

Ready-made single-vision readers dominated the 62.5% reading glasses market share in 2024, generating reliable, high-volume sales through drugstores and supermarkets. Blue-light-blocking variants, however, post a 7.1% CAGR because consumers link digital eye strain to productivity and sleep quality. Average selling prices are higher as protective coatings and chic color tints justify a premium. Progressive and adjustable-focus readers remain niche yet benefit from increasing user familiarity with variable-focus optics, while sport-specific and impact-rated lenses extend opportunities in specialized use cases.

E-commerce brands exploit data analytics to launch micro-targeted collections—gamers receive glare-reduction coatings, while remote workers gravitate toward wider intermediate zones. Meanwhile, factories and hospitals migrate to impact-resistant prescription readers to comply with safety codes, favoring suppliers that merge optical precision with durable materials. As tech-native entrants showcase auto-dimming and AR overlay abilities, the reading glasses market is witnessing a shift from purely corrective utility toward multi-function digital accessories.

By Power Range: Early Intervention Expands Lower-Strength Volumes

The +0.75 to +1.75 D band is the fastest-growing cohort at a 6.8% CAGR, reflecting the earlier onset of near-vision fatigue linked to prolonged screen exposure among professionals in their 30s. Mid-range powers from +2.00 to +2.75 D hold the lion’s share at 44.7%, serving consumers in their 50s and 60s, many of whom buy multiple pairs for different tasks. Upper-range powers above +3.00 D address advanced presbyopia but grow modestly as surgical solutions gain traction in high-income brackets.

Manufacturers fine-tune merchandising by clustering SKUs in quarter-diopter steps, minimizing inventory while maximizing fit rates. Some online portals deploy AI engines using webcam-based reading tests to recommend precise powers, lifting conversion, and reducing returns. These digital diagnostics not only widen access but also reinforce consumer trust, cementing brand loyalty in a fragmented, competitive field.

By Frame Material: Sustainability Recasts Product Value Narratives

Plastic frames still accounted for 54.9% of the reading glasses market in 2024, underpinned by low cost and flexible styling options. Yet, regulatory and consumer pressure is forcing a pivot toward bio-based acetates, recycled ocean plastics, and carbon-negative fibers, which together register 5.4% annual growth. Metal alloys and titanium gain favor among premium buyers who value durability and lightweight comfort, particularly when integrated with electronics for smart-reader applications.

Lifecycle assessments now appear in marketing collateral, and retailers prominently label recycled content, swaying eco-aware consumers to pay moderate premiums. Brands experimenting with modular components allow lens swapping without disposing of entire frames, aligning with circular economy mandates in Europe. Suppliers that invest early in sustainable materials enjoy preferential placement in EU optical chains as new extended producer responsibility rules come into force.

By Distribution Channel: Digital Convenience Outpaces Store Footfall

Optical retail outlets captured 38.2% of the reading glasses market size in 2024, leveraging professional eye exams, insurance billing, and instant fulfillment. However, D2C e-commerce is growing 8.2% annually, aided by AI-powered virtual try-on and hassle-free returns. Online vendors bundle protective cases and blue-light coatings, translating higher perceived value into stronger margins despite discount pricing.

Mass merchandisers and drugstores depend on impulse buys and price-sensitive shoppers, though SKU rationalization is tightening shelf space. Department stores and fashion boutiques curate designer frames, positioning readers as lifestyle accessories and generating cross-sales with apparel. Clinics and non-profit vision camps supply basic readers to underserved populations, a model increasingly supported by CSR initiatives from global eyewear groups that seek goodwill and future customer pipelines.

Geography Analysis

North America, with a 37.4% revenue slice in 2024, benefits from affluent older demographics and the region’s early adoption of technology-infused frames. Intense private insurance penetration makes premium progressive readers accessible, while corporate wellness programs reimburse blue-light-blocking glasses for remote employees. Regulatory niches—such as ANSI-certified industrial readers—deliver higher average selling prices and attract B2B partnerships between optical brands and employers.

Europe remains a mature but eco-progressive arena where single-use plastic scrutiny and CE-mark compliance shape product roadmaps. About two-thirds of German adults wear vision aids, anchoring a dependable customer base.[3]Springer Authors, “Sehhilfen, Hörhilfen und Schwerbehinderung,” springer.com Bio-based frames gain traction as retailers align with EU circular-economy directives, and established manufacturers enjoy an advantage given stringent import certification requirements.

Asia Pacific records a vigorous 6.3% CAGR, propelled by urban millennials who juggle intensive screen time with rising disposable income. Japanese firms like JINS showcase hinge innovations that withstand 150 kg of stress, solving durability pain points for active users. China and India provide volume upside thanks to sizeable middle classes, while high myopia prevalence in East Asia ensures a massive pipeline of future presbyopes. Government health schemes that subsidize routine eye exams further enlarge addressability, channeling more consumers toward the reading glasses market.

Competitive Landscape

The reading glasses market exhibits moderate fragmentation, with the top five firms controlling less than 40% of global sales. EssilorLuxottica maintains scale advantages in manufacturing and distribution, yet nimble D2C challengers such as Warby Parker and Zenni Optical erode share through vertical integration and data-driven merchandising. EssilorLuxottica’s 2024 acquisitions of Heidelberg Engineering and youth-oriented Supreme reveal a dual strategy of med-tech expansion and brand diversification.

Technology partnerships are redefining competition. Google’s USD 150 million co-development deal with Warby Parker adds AI and XR capabilities, signaling that future earnings may hinge on software ecosystems as much as optical hardware. Meanwhile, ViXion leverages Nordic Semiconductor chipsets to commercialize lightweight autofocus readers, underscoring how component suppliers are pivotal allies in product differentiation.

Sustainability is the other theatre of rivalry. Eco-Eyewear has achieved carbon-negative operations by adopting castor-seed bio-acetate and transparent supply chains, capturing brand-loyal, eco-conscious consumers. Larger incumbents respond with closed-loop recycling programs and modular designs. Overall, players that combine optical expertise with digital platforms, sustainable materials, and compelling branding stand best poised to extend wallet share in the evolving reading glasses market.

Reading Glasses Industry Leaders

EssilorLuxottica (FGX International)

De Rigo Vision

Specsavers Optical Group

Warby Parker

Zenni Optical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JINS launched the “PLAYFUL METAL” collection featuring four styles and twelve variants at JPY 9,900 (USD 66), marking its push into affordable fashion-forward frames.

- May 2025: Google committed USD 150 million to develop AI-powered smart glasses in partnership with Warby Parker, earmarking USD 75 million for product engineering and the balance linked to milestone delivery.

- April 2025: JINS released “JINS 360°” glasses incorporating all-direction movable hinges tested to 100,000 openings, addressing breakage at temple joints.

- February 2025: SolidddVision unveiled AR glasses at CES 2025 that reroute images to healthy retinal regions for people with macular degeneration, improving reading performance by 50% in clinical trials.

Global Reading Glasses Market Report Scope

| Ready-made Single-Vision Readers |

| Bifocal / Multifocal Readers |

| Blue-Light-Blocking Readers |

| Progressive / Adjustable-Focus Readers |

| Specialty Readers (computer, safety, sports) |

| +0.75 to +1.75 D |

| +2.00 to +2.75 D |

| +3.00 to +3.75 D |

| +4.00 D & above |

| Custom fractional powers |

| Plastic (commodity) |

| Metal Alloys |

| Titanium & Memory Metals |

| Bio-based / Recycled Materials |

| Hybrid & Others |

| Optical Retail Stores |

| Mass-Merchandisers & Drugstores |

| E-commerce Direct-to-Consumer |

| Department & Fashion Boutiques |

| Clinics / Hospitals / Vision Camps |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Lens Type | Ready-made Single-Vision Readers | |

| Bifocal / Multifocal Readers | ||

| Blue-Light-Blocking Readers | ||

| Progressive / Adjustable-Focus Readers | ||

| Specialty Readers (computer, safety, sports) | ||

| By Power Range (Diopters) | +0.75 to +1.75 D | |

| +2.00 to +2.75 D | ||

| +3.00 to +3.75 D | ||

| +4.00 D & above | ||

| Custom fractional powers | ||

| By Frame Material | Plastic (commodity) | |

| Metal Alloys | ||

| Titanium & Memory Metals | ||

| Bio-based / Recycled Materials | ||

| Hybrid & Others | ||

| By Distribution Channel | Optical Retail Stores | |

| Mass-Merchandisers & Drugstores | ||

| E-commerce Direct-to-Consumer | ||

| Department & Fashion Boutiques | ||

| Clinics / Hospitals / Vision Camps | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the reading glasses market in 2025?

The reading glasses market size reached USD 48.9 billion in 2025 and is projected to touch USD 63.3 billion by 2030.

What CAGR is expected for global demand through 2030?

The market is forecast to grow at a steady 5.20% CAGR over the 2025-2030 span.

Which region is expanding the fastest?

Asia Pacific posts the highest regional growth at a 6.3% CAGR, driven by urbanisation and high digital-device penetration.

What lens type is gaining traction most quickly?

Blue-light-blocking readers are advancing at a 7.1% CAGR as screen-related eye-strain awareness rises.

How are smart technologies influencing product development?

Autofocus optics, AR overlays, and AI-powered sensors are transforming readers into multifunction devices, attracting large technology investors.

Are sustainability concerns reshaping material choices?

Yes, bio-based and recycled frames are growing 5.4% yearly as regulations and eco-conscious consumers push for lower environmental impact.

Page last updated on: