Oman EV Charging Station Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

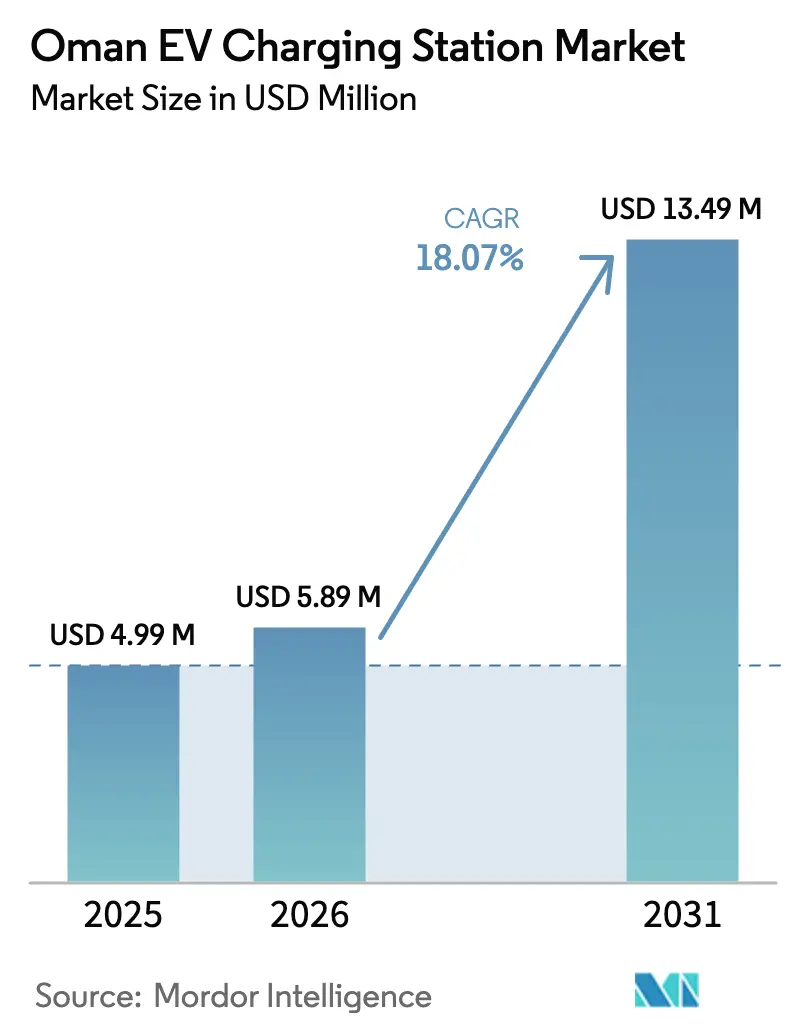

| Base Year Market Size (2025) | USD 4.99 Million |

| Market Size (2026) | USD 5.89 Million |

| Market Size (2031) | USD 13.49 Million |

| Growth Rate (2026 - 2031) | 18.07% CAGR |

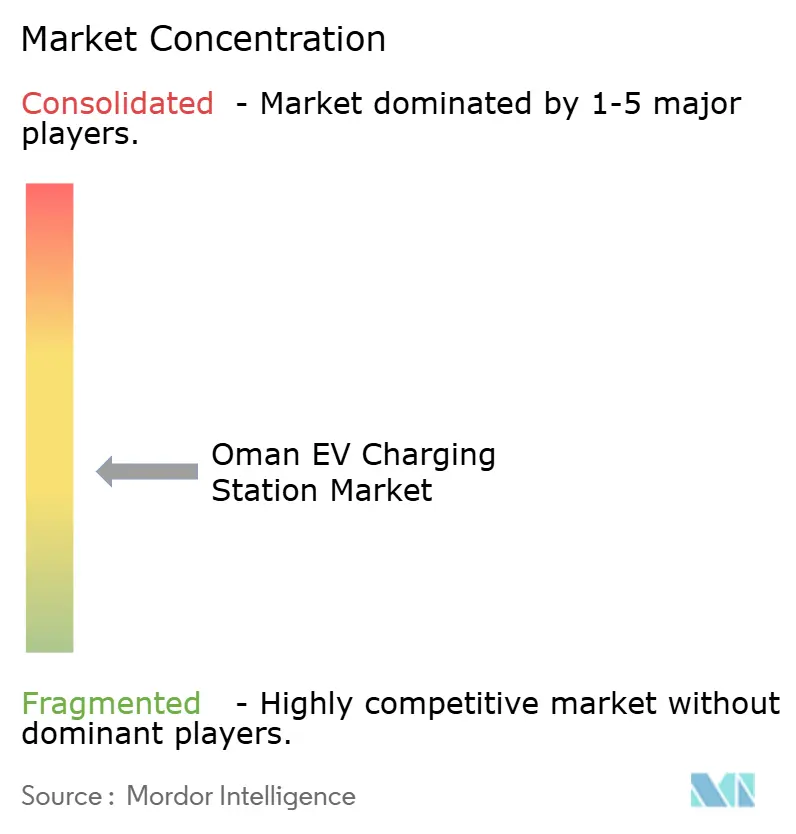

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman EV Charging Station Market Analysis by Mordor Intelligence

Oman EV Charging Station Market size in 2026 is estimated at USD 5.89 million, growing from 2025 value of USD 4.99 million with 2031 projections showing USD 13.49 million, growing at 18.07% CAGR over 2026-2031. Strong policy direction under Vision 2040, obligatory chargers at all commercial fuel stations, and fast‐growing renewable power capacity converge to lift near-term deployment. Early build-out focuses on urban hubs where Muscat Electricity Distribution Company’s grid upgrades intersect with robust passenger-car uptake. At the same time, the Authority for Public Services Regulation’s Mode 4 guidance nudges investors toward high-power DC systems. Fleet electrification by oil-and-gas operators, cross-border tourism corridors, and GCC interconnection financing broaden the business case, yet rural grid constraints and high capex temper the pace in remote districts. Public–private joint ventures such as OOMCO-Synergy’s EVO network and Siemens-OTE Group roll-outs illustrate how asset-light technology partners gain rapid market access through incumbent fuel retailers and dealership chains.

Key Report Takeaways

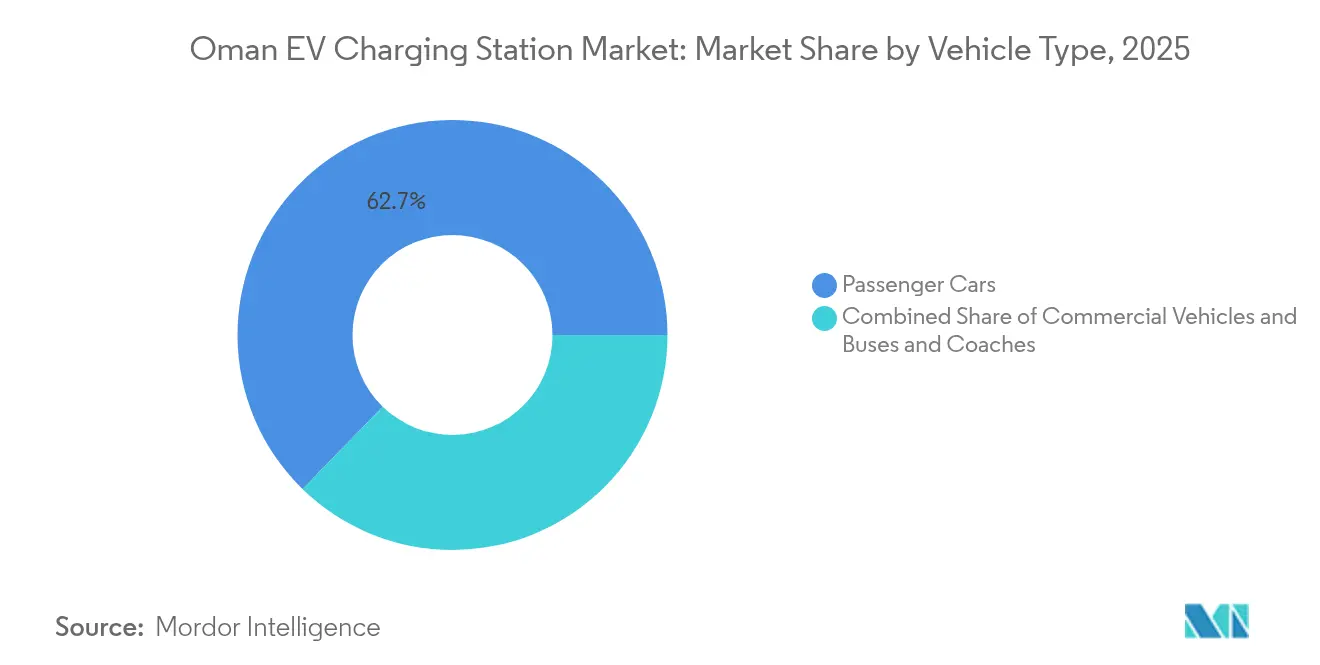

- By vehicle type, passenger cars led with 62.71% of the Oman EV charging station market share in 2025; buses & coaches are projected to grow at an 18.22% CAGR to 2031.

- By charger type, AC units held 73.55% of the Oman EV charging station market share in 2025, while DC fast chargers are set to expand at an 18.18% CAGR through 2031.

- By ownership model, public networks accounted for 54.02% of the Oman EV charging station market share in 2025; private installations are on track for an 18.26% CAGR through 2031.

- By installation site, destination/retail locations captured 45.12% of the Oman EV charging station market share in 2025, whereas highway/transit sites will rise at an 18.21% CAGR to 2031.

- By connector, CCS dominated with a 57.32% of the Oman EV charging station market share in 2025, and Tesla NACS is forecast to advance at an 18.29% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman EV Charging Station Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies & Vision 2040 EV | +4.2% | National, concentrated in Muscat, Salalah, Duqm | Medium term (2-4 years) |

| Declining Battery Prices | +3.8% | Global impact, regional adoption acceleration | Short term (≤ 2 years) |

| Renewable-Energy Integration | +3.1% | National, priority in solar-rich regions | Long term (≥ 4 years) |

| Tourism-Driven Demand For EV Taxis | +2.7% | Muscat, Salalah, tourism corridors | Medium term (2-4 years) |

| Oil-&-Gas ESG Commitments Transitioning | +2.4% | Industrial zones, Duqm, oil field operations | Medium term (2-4 years) |

| Planned GCC Cross-Border Fast-Charging Corridors | +2.0% | Border regions, major highways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies & Vision 2040 EV Targets

Vision 2040 anchors Oman’s net-zero pledge by 2050 and sets a significant electric-vehicle fleet goal by 2035, pushing ministries to streamline licensing and harmonize Gulf standards [1]“Technical Guidelines for Electric Vehicle Charging,” Authority for Public Services Regulation, apsr.om. The November 2023 decree requiring every fuel station to host at least one charger converted more than 270 legacy forecourts into ready-made sites and underwrote initial network density. Future Fund Oman earmarked for e-mobility projects, supplying relatively low-cost capital that de-risks early installations. Multi-agency alignment cuts permitting lead times and gives suppliers confidence that demand volumes will materialize.

Declining Battery Prices Lowering TCO of EV Ownership

Argonne National Laboratory shows lithium-ion pack prices sliding below USD 140 /kWh in 2025 and tracking toward USD 86 /kWh by 2035, compressing the total cost of ownership gap between EVs and internal-combustion vehicles [2]“Lithium-Ion Battery Cost and Performance Projections to 2035,” Argonne National Laboratory, anl.gov . LFP chemistry now exceeds two-fifths of global cell output, offering heat tolerance vital for Oman’s 50 °C summer peaks. Falling pack costs encourage larger battery formats, extending range and heightening demand for 150 kW-plus roadside fast chargers.

Renewable-Energy Integration Enabling Green Charging

Nama Power & Water plans 2 GW of additional solar and wind capacity by 2028, with 1.55 GW already online. OQ Alternative Energy has locked in a quarter equity stake in each new project [3]“Renewable Energy Capacity Expansion Plan 2025-2028,” Nama Power & Water Procurement, namaoman.om . The 500 MW Manah 1 solar plant, operational since January 2025, offsets 780,000 tCO₂ each year—enough to power a statewide network of 1,200 DC fast chargers on fully renewable electricity. New utility-scale projects are coupled with dedicated EV tariffs, letting operators hedge tariff volatility and market chargers as genuinely “green.”

Tourism-Driven Demand for EV Taxis & Rental Fleets

In 2024, tourism arrivals reached a significant post-pandemic milestone, prompting Mwasalat to pilot the country’s first battery-electric bus under sponsorship from Al Maha Petroleum and Sohar International Bank [4]“Sustainable Mobility Initiatives 2024,” Mwasalat, mwasalat.com . The expansion of ride-hailing and rental fleets along the Muscat-Salalah-Duqm corridors highlights the need for high-capacity highway chargers, strategically spaced at regular intervals, a recommendation endorsed at the UITP MENA Conference in Salalah in July 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex & Limited Project-Finance Options | -3.2% | National, affecting private investments | Short term (≤ 2 years) |

| Rural Grid-Capacity Constraints | -2.8% | Rural areas, remote highways | Medium term (2-4 years) |

| Low Petrol Prices | -2.1% | National, stronger in rural areas | Medium term (2-4 years) |

| Charger Derating Under Extreme Summer Temperatures | -1.5% | National, peak impact in interior regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex & Limited Project-Finance Options

A 180 kW charger plus interconnection can cost significantly, yet utilization rarely tops in the first two years. Local banks provide infrastructure loans but seldom ring-fence revenues solely from charging; the exception is Sohar International Bank’s line for the GCC interconnection deal, which illustrates the scale domestic lenders can muster. Absent guaranteed off-take or anchor fleet contracts, many private operators rely on fuel-retailer partnerships to achieve acceptable internal rates of return.

Rural Grid-Capacity Constraints for High-Power DC Sites

Oman Electricity Transmission Company plans multiple projects that are highly worth reinforcing 400 kV backbones, yet distribution feeders in sparsely populated governorates remain undersized for more than 150 kW chargers. Developers frequently resort to solar-plus-storage hybrids to trim peak draws, but that upsizes capex by a quarter and prolongs payback. The North-South Interconnector Phase 2, due Q4 2026, will ease systemic constraints, though localized bottlenecks may linger for several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Infrastructure Scale

Passenger cars controlled 62.71% of the Oman EV charging station market share in 2025. Yet, the buses and coaches category is forecast to record an 18.22% CAGR through 2031, reinforcing a strategic pivot toward depot-oriented charging. The Oman EV charging station market size for passenger-car applications is expected to grow significantly through 2031. Still, double-shift duty cycles mean heavy vehicles already consume a disproportionate share of delivered kilowatt-hours.

Fleet operators gain pricing leverage by aggregating demand and can capitalize on predictable dwell windows to run chargers during off-peak grid hours, shrinking energy costs. Omani state-owned Mwasalat plans to add 4,000 taxis and trial additional e-buses, creating anchor tenants for new DC hubs. Oil-field service fleets in Duqm and Fahud similarly eye electrification to satisfy corporate net-zero pledges, encouraging suppliers to pre-wire yards for megawatt-scale charging when grid capacity permits.

By Charger Type: DC Fast Charging Gains Strategic Priority

AC chargers retained 73.55% of the Oman EV charging station market share in 2025 on pure unit count, but DC installations are accelerating at an 18.18% CAGR as investors chase higher energy throughput and differentiated service levels. The Oman EV charging station market size attached to DC units is expected to grow fairly steadily until 2031. It is anticipated to triple by 2031, due partly to Mode 4 compliance mandates and the spillover from long-haul freight electrification.

Temperature derating poses a significant challenge: power output can drop significantly at high ambient temperatures. In response, vendors are turning to liquid-cooled cables and remote monitoring to mitigate thermal throttling. In a strategic move, Siemens has teamed up with OTE Group, integrating station management software that prompts cabinets to reduce current when cell temperatures reach critical levels. This not only prolongs hardware life but also curbs warranty claims. While AC wall-boxes are prevalent in residential and hospitality sectors due to extended dwell times, mall developers are shifting gears. They're now favoring split AC/DC architectures, setting up multiple sockets complemented by a shared DC post, effectively serving short- and long-stay visitors.

By Ownership Model: Private Sector Accelerates Investment

Publicly owned networks held a 54.02% of the Oman EV charging station market share in 2025, but private players are forecast to expand at 18.26% CAGR as companies embed chargers into ESG roadmaps. Corporate landlords in Muscat’s knowledge hubs install workplace chargers to retain talent. At the same time, upstream oil-and-gas majors retrofit service fleets to shrink Scope 1 emissions, frequently co-locating PV canopy arrays to hedge grid tariffs.

The regulatory mandate covering every commercial fuel outlet further blurs the line between public and private because, despite universal access, ownership often remains with the oil company. Capital recycling strategies, such as carving out charger portfolios into infrastructure funds, emerge as popular ways to unlock liquidity and scale deployment without overstretching balance sheets.

By Installation Site: Highway Corridors Emerge as Growth Priority

Destination and retail venues captured 45.12% of the Oman EV charging station market share in 2025, but highway/transit sites are marching ahead at an 18.21% CAGR on the back of GCC-wide corridor plans. It will rise quickly as the North-South Interconnector energizes 400 kV nodes close to service areas. The average journey distance between Muscat and Salalah is 1,030 km; installing more than 200 kW chargers every 80 km would require at least 13 sites, each drawing 400 kW peak.

Developers are therefore co-locating battery storage to clip peaks, enhancing grid friendliness. Retail-anchored chargers remain indispensable because shoppers routinely park for over two hours, providing sufficient dwell to add 120 km of range from a 22 kW socket. Airports and seaports follow a hybrid model, combining 50 kW posts for public taxis with 350 kW dispensers dedicated to trucks and heavy equipment.

By Connector Standard: Tesla NACS Gains Momentum

CCS retained a 57.32% of the Oman EV charging station market share in 2025, yet Tesla’s NACS is advancing at an 18.29% CAGR as multiple OEMs adopt the interface for 2026 model years. Operators now minimize stranded-asset risks, with many new DC orders opting for dual-cable dispensers that house both connectors. While Japanese OEM imports plateau, eroding CHAdeMO’s installed base, China’s GB/T carves out a niche, finding application in company fleets that import right-hand-drive vans. The GCC Standardization Organization oversees interoperability testing, bolstering cross-border roaming. This feature gains prominence as the UAE-Oman highway corridors gear up for a future launch.

Looking ahead, wireless inductive pads might find favor in depot operations, especially where buses align over embedded coils. However, with efficiency limitations, they lag behind cabled alternatives, particularly in Oman, where high summer temperatures lead to notable energy losses.

Geography Analysis

With its dense population and high EV adoption, Muscat Governorate is at the forefront of grid reinforcement efforts. Recently, Muscat Electricity Distribution implemented a smart meter rollout, enabling time-of-use tariffs that substantially reduce peak pricing for late-night EV charging. This initiative is expected to encourage customers to adopt electric vehicles by making charging more cost-effective during off-peak hours. Siemens-OTE strategically places branded chargers at every dealership in the capital's showroom network, ensuring visibility for potential buyers. This approach enhances customer convenience and integrates after-sales servicing into maintenance contracts, creating a seamless experience for EV owners and fostering long-term customer relationships.

Duqm Special Economic Zone emerges as a key player, driven by the electrification of heavy industries and a strong focus on renewable energy development. In the coming years, OETC plans to connect renewable and conventional energy sources, creating dual supply routes that reduce energy curtailment risk during low renewable energy generation periods. A memorandum between the Port of Duqm and OOMCO also aims to introduce solar-powered charging islands, positioning the port as a green logistics hub.

Dhofar Governorate, centered around Salalah and heavily reliant on tourism, is making significant strides in enhancing grid stability through wind-power expansion and the completion of interconnectors. This improved stability is paving the way for the installation of high-capacity roadside chargers along the coastal highway, which is expected to support the growing number of electric vehicles in the region. Local taxi operators are planning a phased transition to electric vehicles, although this shift remains dependent on securing adequate financing.

Competitive Landscape

The field remains moderately fragmented; however, OOMCO (Oman Oil Marketing Company) controls many forecourts, equipping a substantial portion with chargers. Its joint venture, Electric Vehicles One, facilitates an accelerated rollout while maintaining financial stability. Siemens, in collaboration with OTE Group, integrates hardware with managed-services contracts, ensuring high uptime levels, a critical factor for fleet operators who prioritize service reliability and transparency.

Kempower, a global charger specialist, has adopted a distribution-plus-service model through TEAMS International. This approach enables rapid market entry while delegating civil works execution to local contractors with expertise navigating permitting protocols. Following a strategy similar to Tesla, Chinese OEMs are exploring the development of captive charger networks to attract and retain buyers. Meanwhile, utility Nama focuses on enhancing grid reliability instead of owning downstream assets, creating opportunities for third-party network operators to expand their presence.

Technological competition is centered on advancements in thermal management and dynamic power sharing, moving beyond the focus on kilowatt ratings alone. Cabinets capable of reallocating current to a single cable during reduced simultaneous usage improve efficiency and reduce waiting times. The long-term leaders in the industry are expected to excel in lifecycle economics, offering innovative power-by-the-hour subscription models that align operational costs with energy consumption.

Oman EV Charging Station Industry Leaders

Electric Vehicles One LLC

CITA group

Legend Green Energy Solutions LLC

Shell Charge Solutions (Shell PLC),

ZEROVA Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kempower entered an exclusive sales and service partnership with TEAMS International to deploy modular DC fast chargers across service stations and fleet hubs.

- April 2025: OQ Alternative Energy secured up to 25% stakes in all renewable projects procured by Nama Power & Water Procurement through 2028, ensuring green electricity supply for future charging hubs.

- March 2025: Port of Duqm Company and OOMCO signed an MoU to co-develop solar systems, EV charging infrastructure, and biofuels within the port precinct.

Oman EV Charging Station Market Report Scope

EV charging stations provide electric energy to recharge a variety of plug-in vehicles, from electric cars and neighborhood electric vehicles to plug-in hybrids.

The Oman EV Charging Station Market is segmented by vehicle type, charger type, and charging ownership type. By Vehicle Type, the market is segmented into passenger cars and commercial vehicles. By charger type, the market is segmented into AC Charging Stations and DC Charging Stations. By Charging Ownership Type, the market is segmented into public and private. For each segment, the market size and forecast have been done based on the value (USD).

| Passenger Cars |

| Commercial Vehicles |

| Buses and Coaches |

| AC Charging Station |

| DC Charging Station |

| Public |

| Private |

| Home |

| Destination/Retail |

| Highway/Transit |

| Fleet Depot |

| CCS |

| CHAdeMO |

| GB/T |

| Tesla NACS |

| Wireless |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Buses and Coaches | |

| By Charger Type | AC Charging Station |

| DC Charging Station | |

| By Ownership Model | Public |

| Private | |

| By Installation Site | Home |

| Destination/Retail | |

| Highway/Transit | |

| Fleet Depot | |

| By Connector Standard | CCS |

| CHAdeMO | |

| GB/T | |

| Tesla NACS | |

| Wireless |

Key Questions Answered in the Report

What is the forecasted value of Oman’s EV charging station network by 2031?

The market is projected to reach USD 13.49 million by 2031, growing at 18.07% CAGR.

How many public chargers are currently located at OOMCO service stations?

OOMCO has equipped 86 of its forecourts with EV charging points, with 12 sites powered by onsite solar arrays.

Which charger type is expected to record the quickest growth in Oman?

DC fast chargers are set to expand at an 18.18% CAGR through 2031 as fleet operators demand rapid turnaround.

Why are highway corridors a strategic focus for new installations?

Planned GCC cross-border corridors and the long Muscat–Salalah route require high-power chargers every 80 km to support intercity travel.

Which connector standards dominate Oman’s new DC deployments?

CCS leads, but Tesla’s NACS is gaining swiftly as multiple OEMs migrate to the interface from 2026 model years.

Page last updated on: