Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

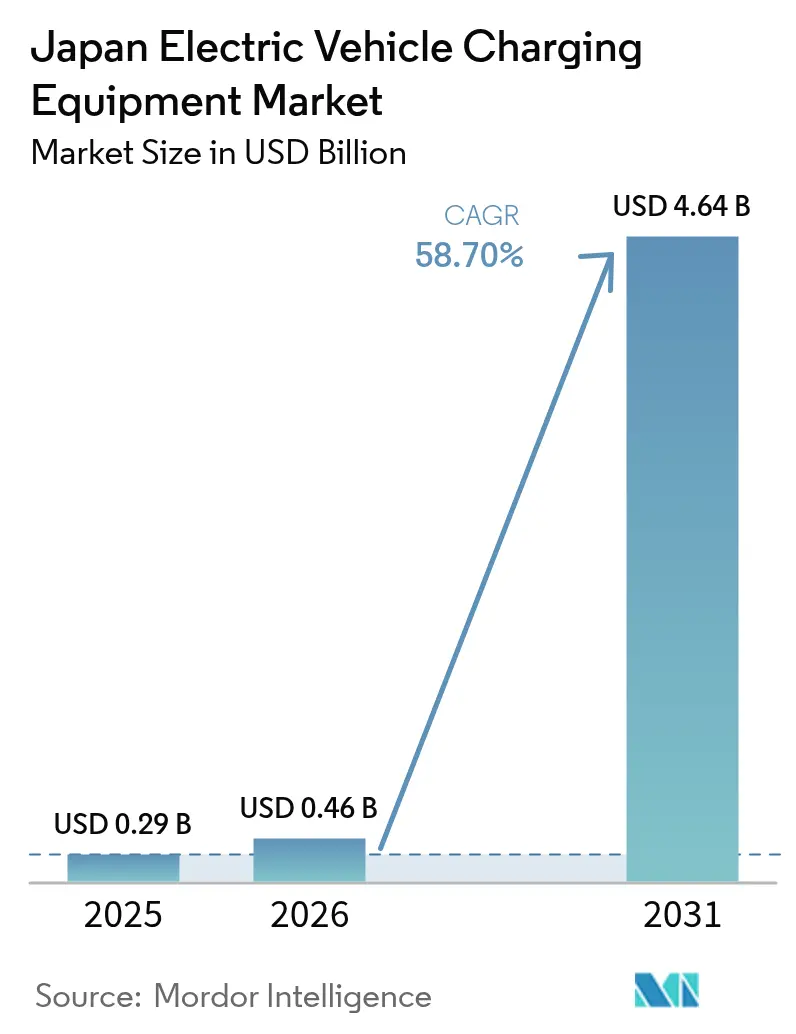

| Base Year Market Size (2025) | USD 0.29 Billion |

| Market Size (2026) | USD 0.46 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 58.70% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

The Japan EV charging equipment market size was valued at USD 0.29 billion in 2025 and estimated to grow from USD 0.46 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 58.70% during the forecast period (2026-2031). The Japan EV charging equipment market is propelled by the 2035 gasoline-vehicle sales ban, heavy green-growth spending, and nationwide integration of bidirectional chargers into the power system. Corporate electrification mandates issued by major keiretsu groups give the Japan EV charging equipment market an unusually predictable demand base, allowing faster network build-outs and earlier scale economies than consumer-led models. Technology advances—especially liquid-cooled cords, composite cables, and next-generation CHAdeMO/ChaoJi protocols—position equipment as grid assets rather than simple refueling hardware. Policy coherence between ministries and prefectures sustains subsidy pipelines that narrow payback periods, while component innovation drives total cost of ownership down. Although the Japan EV charging equipment market remains moderately fragmented, utilities have emerged as pivotal ecosystem orchestrators that unlock new revenue through demand-response programs

Key Report Takeaways

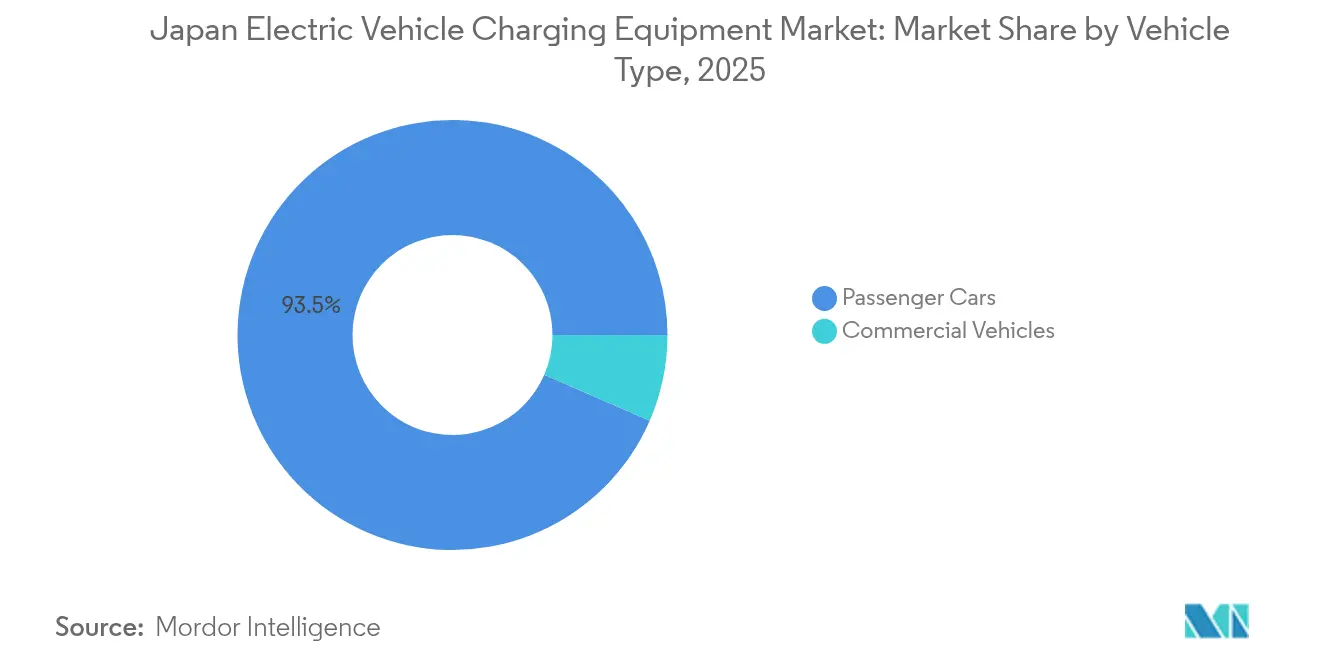

- By vehicle type, passenger cars led the Japan electric vehicle charging equipment market with 93.48% market share in 2025, while commercial vehicles are projected to expand at a 64.30% CAGR through 2031.

- By charging equipment, the Others category charging equipment (terminal blocks, energy meters, safety mechanisms, etc.) held a 33.62% share of the Japan electric vehicle charging equipment market in 2025, and cords & cables are slated for the fastest 63.90% CAGR to 2031.

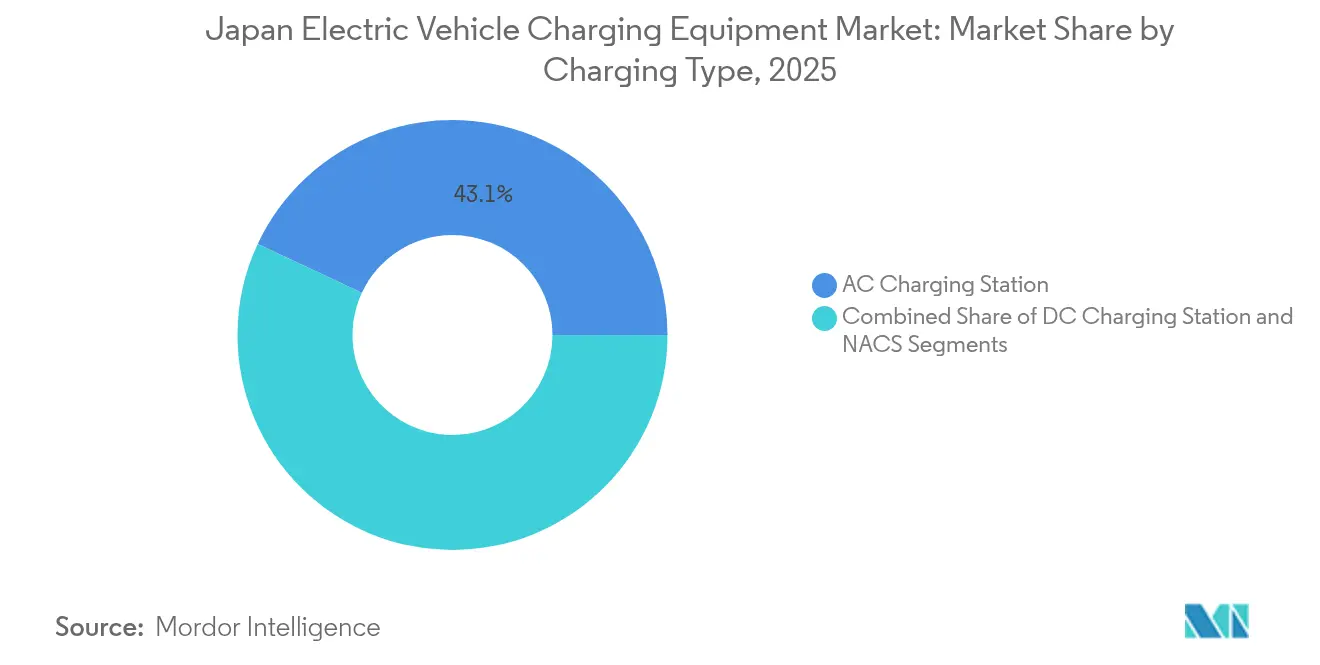

- By charging type, AC stations captured a 43.05% of the Japan electric vehicle charging equipment market in 2025 and are forecast to grow at a 64.70% CAGR through 2031.

- By application type, home charging commanded an 82.95% of the Japan electric vehicle charging equipment market share in 2025, whereas public charging is anticipated to surge at a 91.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2035 Gasoline-Car Sales Ban | +12.8% | Tokyo, Kanagawa, Osaka, Aichi | Long term (≥ 4 years) |

| ESG-Fleet Electrification Mandates | +8.5% | Tokyo, Kanagawa, Osaka | Medium term (2-4 years) |

| METI's Green Growth Fund | +6.2% | Tokyo, Kanagawa, Aichi, Fukuoka | Short term (≤ 2 years) |

| V2H (Vehicle-To-Home) Tariff | +4.1% | Tokyo, Kanagawa, Chiba, Saitama | Medium term (2-4 years) |

| Demand for Bidirectional Chargers | +3.9% | Yamanashi, Miyazaki, Kochi, Tokushima | Long term (≥ 4 years) |

| On-Street Charger Pilots | +2.7% | Osaka, Kyoto, Hyogo | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV-Shift Stimulus From Japan’s 2035 Gasoline-Car Sales Ban

The ban removes policy ambiguity and accelerates equipment investment because Japanese EV charging equipment market suppliers can confidently model ten-year cash flows. The Japanese government has earmarked trillions for charging build-outs and set a 300,000-public-port target by 2030, an almost eight-fold expansion. Commercial fleets must also comply, triggering immediate depot-charging demand that underpins the Japan EV charging equipment market’s significant CAGR. Tokyo and adjacent prefectures attract the bulk of early funding, reflecting population density and corporate head-office concentration.

Corporate ESG-Fleet Electrification Mandates By Keiretsu Groups

In Japan, the distinctive keiretsu system shifts electric vehicle (EV) adoption from mere consumer choices to unified corporate strategies, leading to unique infrastructure demand patterns not seen in Western markets. Some Japanese companies have pledged to have fully electrified commercial fleets by 2030, locking in long-term charger contracts at factories and logistics hubs. Scale advantages lower per-port installation costs and accelerate return on investment, especially in the Kanto and Kansai economic belts.

Subsidized High-Power Charger Grants Under METI’s Green Growth Fund

Japan’s subsidy program for FY2024-2025 specifically targets high-power charging infrastructure, addressing the critical gap between current AC-dominant installations and future fast-charging requirements. The program's focus on 150kW+ installations signals Japan's strategic shift toward supporting longer-distance travel and commercial vehicle operations, areas where current infrastructure remains inadequate. Grant rules demand grid-integration functions, giving domestic power-electronics makers a head start. Concentrated subsidies in Tokyo, Aichi, and Fukuoka lift utilization and shorten payback to under four years.

V2H Tariff Premiums from Power Utilities

Power utilities treat EV batteries as distributed storage that can feed the grid when wholesale spot prices spike. Under new dynamic-pricing plans, households with bidirectional chargers earn significantly per kWh exported during evening peaks. The arbitrage opportunity shortens payback on a residential 7 kW wall box to under three years, strengthening the consumer business case for the Japanese EV charging equipment market. Utilities also avoid costly gas-turbine starts by tapping aggregated vehicle capacity, which helps them meet carbon-intensity caps without investing in standalone batteries. Prefectures around Tokyo lead subscription growth because they combine high rooftop-solar penetration with stringent grid-stability targets[1]“CHAdeMO Protocol Development Roadmap,” CHAdeMO Association, chademo.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow Condominium Retrofit Approvals | -3.2% | Tokyo, Kanagawa, Osaka, Kyoto | Long term (≥ 4 years) |

| High Land-Lease Costs | -2.8% | Tokyo, Kanagawa, Osaka, Aichi | Medium term (2-4 years) |

| CHAdeMO / CCS / NACS Standard Fragmentation | -1.9% | Tokyo, Kanagawa, Osaka, Aichi | Medium term (2-4 years) |

| Low Rural Utilization Rates | -1.4% | Hokkaido, Tohoku, Kyushu rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Condominium Retrofit Approvals Under the Building Management Act

Japan's Building Management Act mandates unanimous consent from all condominium owners for major electrical modifications. This requirement poses significant hurdles for installing residential charging stations, especially in urban areas dominated by condominium living. While the Act was crafted for traditional building modifications, it fails to address the nuances of EV infrastructure deployment. Here, decisions made by individual owners can have far-reaching implications on the building's overall electrical capacity and safety systems. As EV adoption surges, these constraints intensify, leading to infrastructure bottlenecks. Consequently, many new EV owners are pushed towards public charging solutions, which inflate operational costs and dampen the appeal of EV adoption.

High Land-Lease Costs for Public Fast-Charging Sites Near Expressways

Prime spots for public fast-charging stations, especially those close to expressways and urban hubs, come with steep land lease rates. These premiums challenge the profitability of charging operators, even with high utilization rates. In metropolitan areas, costs soar even higher. This financial strain nudges operators towards secondary locations that lack visibility and accessibility. Such a shift diminishes network convenience and hampers adoption rates, especially among consumers wary of range limitations. This challenge is most pronounced in the deployment of DC fast-charging stations. Their higher power demands lead to heftier infrastructure investments, which operators must recoup over fewer charging sessions than AC installations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Corporate Fleets Reshape Equipment Demand

Passenger cars held a 93.48% Japan EV charging equipment market share in 2025, furnishing the baseline load for most public networks. Commercial vehicles, however, post a 64.30% CAGR that pulls equipment makers toward depot-grade DC blocks and advanced load-scheduling software. Fleet electrification contracts are typically multi-year, letting suppliers lock in recurring maintenance revenue and forecast parts demand more accurately. Logistics firms like Yamato and Sagawa deploy megawatt hubs that double as micro-grids, using stationary batteries to shave peak demand and sell ancillary services to utilities. These large installations create spillover benefits for retail drivers when operators open excess nighttime capacity to the public.

The corporate pivot also drives connector durability and payment integration innovation because fleet use cases require thousands of mating cycles and centralized billing. Higher throughput accelerates hardware replacement cycles, expanding the aftermarket for cables, seals, and switchgear. Suppliers that bundle hardware with SaaS fleet dashboards gain margin insulation because software churn remains low once integrated into logistics workflows. As corporate adoption scales, the commercial share of the Japan EV charging equipment market size is expected to rise, even if passenger cars remain numerically dominant.

By Charging Equipment: Cords & Cables Outpace Legacy Pillars

The Others (terminal blocks, energy meters, safety mechanisms, etc.) category held 33.62% of the Japan EV charging equipment market share in 2025, but cords and cables are forecast to grow at a 63.90% CAGR. Lightweight composite sheathing cuts cable mass by 40%, mitigating ergonomic strain and reducing maintenance calls linked to dropped connectors. Domestic firms co-develop these designs with resin suppliers, securing exclusive supply contracts that shore up margins. Component scale economies lower per-unit cost significantly, widening adoption among small independent operators.

Traditional pedestal pillars face urban footprint constraints, prompting vendors to roll out slimline wall-mounts that bolt onto existing parking-lot lighting poles. Power supplies and control boards track the overall growth of Japan's EV charging equipment market size but gain an incremental bump from silicon-carbide MOSFET adoption, significantly improving conversion efficiency. Interoperability upgrades follow CHAdeMO’s ChaoJi roadmap, ensuring new hardware remains backward-compatible with earlier vehicles. Suppliers that offer end-to-end hardware suites win municipal tenders because bundling simplifies procurement audits. The component race thus underscores how incremental engineering tweaks can swing large revenue pools in a fast-scaling market.

By Charging Type: AC Dominance Reinforced By Bidirectional Value

AC stations commanded 43.05% of Japan's EV charging equipment market share in 2025 and will expand at a 64.70% CAGR as household V2H use cases multiply. Residential units now ship with factory-flashed firmware enabling 20 kW export, enough to cover peak evening loads for a typical Japanese apartment building’s common areas. Utilities reward bidirectional participation, offsetting longer charge durations than DC. The extra functionality increases equipment utilization even when vehicles are parked, turning idle time into revenue for both owner and operator. In suburban prefectures, builders integrate AC wall boxes into new-home packages, adding only around 1% to construction cost yet boosting property value.

DC fast chargers retain primacy along expressways and fleet depots, where turnaround time dictates route economics. Silicon-carbide power modules and liquid-cooled cables allow significant throughput that recharges next-gen 100 kWh packs in under 10 minutes. However, grid upgrades lag in historic downtowns, funneling investment toward outer-ring logistics parks with ample capacity. The NACS protocol remains under evaluation; pilot adapters from Panasonic achieve a reliable handshake but await government approval. Thus, DC growth, while rapid, stays tethered to infrastructure realities that AC units sidestep through lower amperage draws.

By Application Type: Public Networks Close the Urban Gap

Home installations accounted for 82.95% of Japan's EV charging equipment market size in 2025, favored by single-family owners who can access low overnight tariffs. Yet condominium retrofit headwinds shift urban drivers toward public or workplace chargers, igniting a 91.80% CAGR for public applications. Retail landlords deploy eight-bay clusters to monetize parking dwell times, reporting ancillary sales uplifts as EV drivers linger during charging sessions. Municipalities integrate curbside AC posts into smart-city upgrades, using IoT sensors to adjust parking fees dynamically based on grid load. This policy blueprint spreads from Tokyo’s wards to Osaka and Fukuoka, expanding public-network density.

Workplace charging emerges as a hybrid model: employees reserve AC slots via mobile apps, while unused midday capacity feeds energy back to the building under an internal tariff. The dual-use case improves payback periods and aligns with corporate sustainability audits. Destination sectors like hospitality and big-box retail join the wave, installing chargers to capture eco-conscious travelers. Hardware makers respond with modular designs ranging from two to sixteen heads without new transformers, easing capex decisions. By 2031 the public slice of the Japan EV charging equipment market share is expected to rival the home segment, signaling a mature two-channel ecosystem.

Geography Analysis

Tokyo’s metropolitan cluster dominates the Japan EV charging equipment market, which is supported by a dense population, high GDP per capita, and progressive municipal climate plans. The metro area benefits from overlapping subsidies: Tokyo prefecture covers significant charger hardware costs for small businesses, while national METI grants handle grid-connection fees. Corporate HQs in Marunouchi and Shinjuku mandate workplace charging, accelerating equipment penetration in commercial towers. High utilization rates ensure robust cash flows that attract infrastructure funds.

Industrial champions Toyota and Nissan spur equipment demand in the Chubu and Kansai by electrifying logistics arms. Aichi and Kanagawa prefectures cooperate with utilities to pre-permit transformer upgrades, shrinking construction timelines significantly. These areas double as testbeds for ChaoJi ultra-fast prototypes, giving domestic vendors a home-field advantage. Manufacturing clusters also integrate chargers with rooftop solar and cogeneration plants, creating micro-grids that sell frequency-control services to the main grid. Consequently, regional governments position EV infrastructure as both an industrial policy lever and an energy-transition tool, widening the reach of the Japanese EV charging equipment market.

Rural prefectures, especially Yamanashi, Miyazaki and Kochi, adopt chargers primarily to soak up midday solar surpluses. Battery-buffered AC posts smooth intermittency and provide emergency power during typhoons and earthquakes, a critical resilience feature. Low traffic volumes depress standalone profitability, so local governments bundle chargers with tourism campaigns that highlight eco-routes and green lodging. Though each rural site contributes modest revenue, together they ensure national coverage and lift the Japan EV charging equipment market’s social license to expand.

Competitive Landscape

The Japan EV charging station market exhibits moderate fragmentation, indicating significant consolidation opportunities as the industry matures. The competitive dynamics favor companies combining hardware capabilities with software platforms, enabling integrated solutions that address vehicle charging and grid management requirements. This integration becomes valuable as utilities seek partners for demand response programs and grid stabilization services.

Strategic partnerships multiply: Utilities such as Tokyo Electric Power ink revenue-sharing pacts that give equipment vendors preferential tariff windows in exchange for demand-response participation. Start-ups like PowerX introduce containerized battery-integrated chargers, lowering peak draw and carving a niche in land-scarce ports. Cross-border M&A accelerates; Hitachi Energy’s acquisition of eks Energy secures advanced power electronics that shorten installation timeframes to a great extent.[2]Kelsey Misbrener, "Hitachi completes full acquisition of eks Energy", Solar Power World, solarpowerworldonline.com

Innovation focus shifts from pure hardware to full-stack ecosystems encompassing payment, authentication, and energy-trading modules. Vendors embedding AI-based predictive maintenance cut downtime significantly, a differentiator in franchise tenders. Competitive pressure pushes price per installed kilowatt down by around 8% annually, yet service contracts cushion margin erosion. Investors favor firms offering end-to-end solutions because vertical integration simplifies risk assessment. As consolidation continues, the Japan EV charging equipment market heads toward an oligopoly of hardware-plus-software champions able to underwrite multi-gigawatt rollouts.

Japan Electric Vehicle Charging Equipment Industry Leaders

-

ABB

-

Delta Electronics Inc.

-

Toyota Connected Corporation

-

ENECHANGE Ltd.

-

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PowerX opened the first location in its high-power network built with Mercedes-Benz High Power Charging Japan. The Mercedes-Benz Charging Hub Chiba Park runs around the clock, welcomes every EV model and supplies up to 150 kW per port.

- October 2024: Mitsubishi Motors Corporation, MC Retail Energy, Kaluza Japan and Mitsubishi Corporation launched a connected smart-charging service that lets Outlander PHEV owners schedule and control charging through a cloud platform tied to the vehicle’s onboard systems.

- September 2024: Panasonic Energy began mass producing 4680 cylindrical batteries at its Wakayama plant, with full-scale output targeted for FY2025 Q2. The cells serve both vehicle and stationary storage markets and are engineered for easy integration with chargers that support grid balancing and demand management.

Japan Electric Vehicle Charging Equipment Market Report Scope

A charging station, also known as electric vehicle charging station, electric recharging point, charging point, charge point, electronic charging station (ECS), and electric vehicle supply equipment (EVSE), is a machine that supplies electric energy to charge plug-in electric vehicles, including cars, trucks, buses, and others. Charging stations provide connectors that conform to a variety of standards. For common direct current rapid charging, chargers are equipped with multiple adaptors such as combined charging system (CCS), CHAdeMO, and AC fast charging.

The Japanese electric vehicle charging infrastructure is segmented by end use and charging station type. By end use, the market is segmented into home charging and public charging. By charging station type, the market is segmented into AC charging station and DC charging station.

For each segment, market sizing and forecast have been done on the basis of value (USD billion).

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Charging Equipment

| Pillar |

| Cord and Cable |

| Control Boards |

| Charging Controllers |

| Power Supplies |

| Others |

By Charging Type

| AC Charging Station |

| DC Charging Station |

| NACS (North American Charging System) |

By Application Type

| Home Charging |

| Public Charging |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Charging Equipment | Pillar |

| Cord and Cable | |

| Control Boards | |

| Charging Controllers | |

| Power Supplies | |

| Others | |

| By Charging Type | AC Charging Station |

| DC Charging Station | |

| NACS (North American Charging System) | |

| By Application Type | Home Charging |

| Public Charging |

Key Questions Answered in the Report

How large is Japan’s EV charging equipment market in 2026?

It is valued at USD 0.46 billion and is projected to reach USD 4.64 billion by 2031 at a 58.70% CAGR.

What share of equipment uses AC technology today?

AC units account for 43.05% of installed capacity, favored for bidirectional V2H functionality.

Which application type is growing fastest?

Public charging is forecast to surge at a 91.80% CAGR through 2031 as urban drivers rely on curbside and retail hubs.

Why are cords and cables expanding so quickly?

Liquid-cooled, lightweight designs enable higher power delivery, driving a 63.90% CAGR for the component category.

What blocks home-charger adoption in cities?

Condominium retrofit rules under the Building Management Act require unanimous consent, delaying approvals.

Page last updated on: