Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

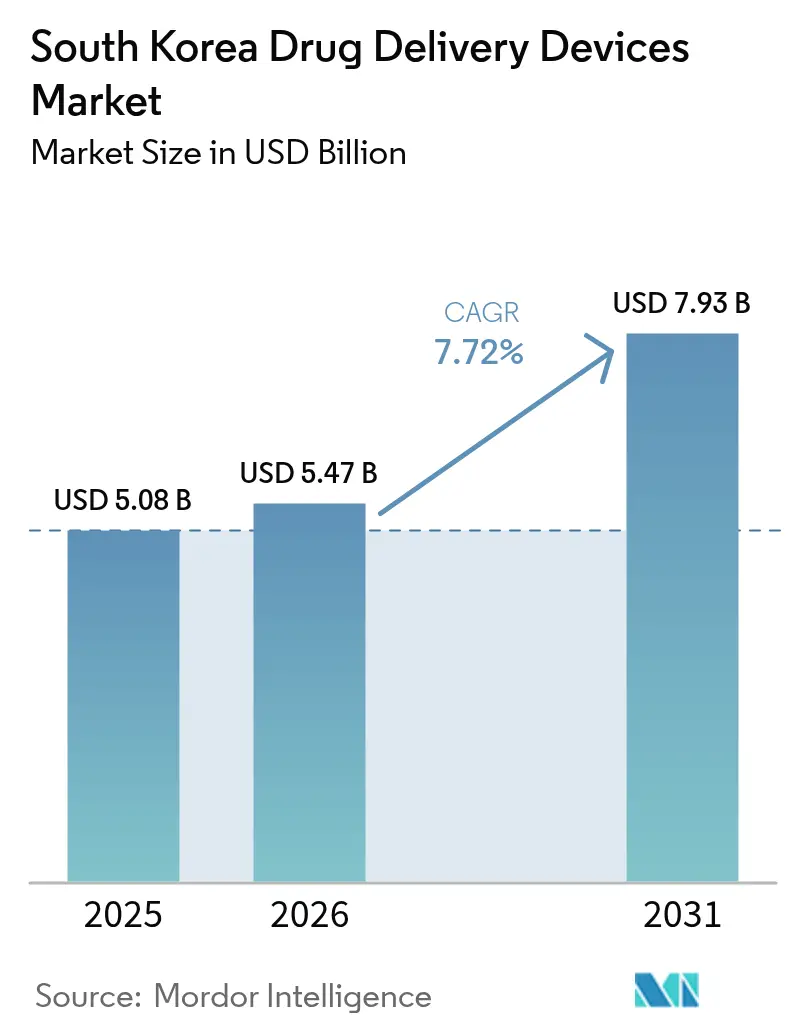

| Base Year Market Size (2025) | USD 5.08 Billion |

| Market Size (2026) | USD 5.47 Billion |

| Market Size (2031) | USD 7.93 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Drug Delivery Devices Market Analysis by Mordor Intelligence

The South Korea drug delivery devices market size was valued at USD 5.08 billion in 2025 and estimated to grow from USD 5.47 billion in 2026 to reach USD 7.93 billion by 2031, at a CAGR of 7.72% during the forecast period (2026-2031). Rising life expectancy, rapid urbanization, and strong domestic production underpin this growth. A national policy focus on chronic disease management, coupled with high digital‐health adoption, is accelerating uptake of connected pumps, smart inhalers, and other patient-centric technologies. Government fast-track approvals for breakthrough devices shorten launch timelines, while a broad biologic pipeline pushes demand for advanced injectable platforms. Competitive intensity is increasing as domestic innovators align with global leaders to commercialize novel formats across oncology, diabetes, and pain care.

Key Report Takeaways

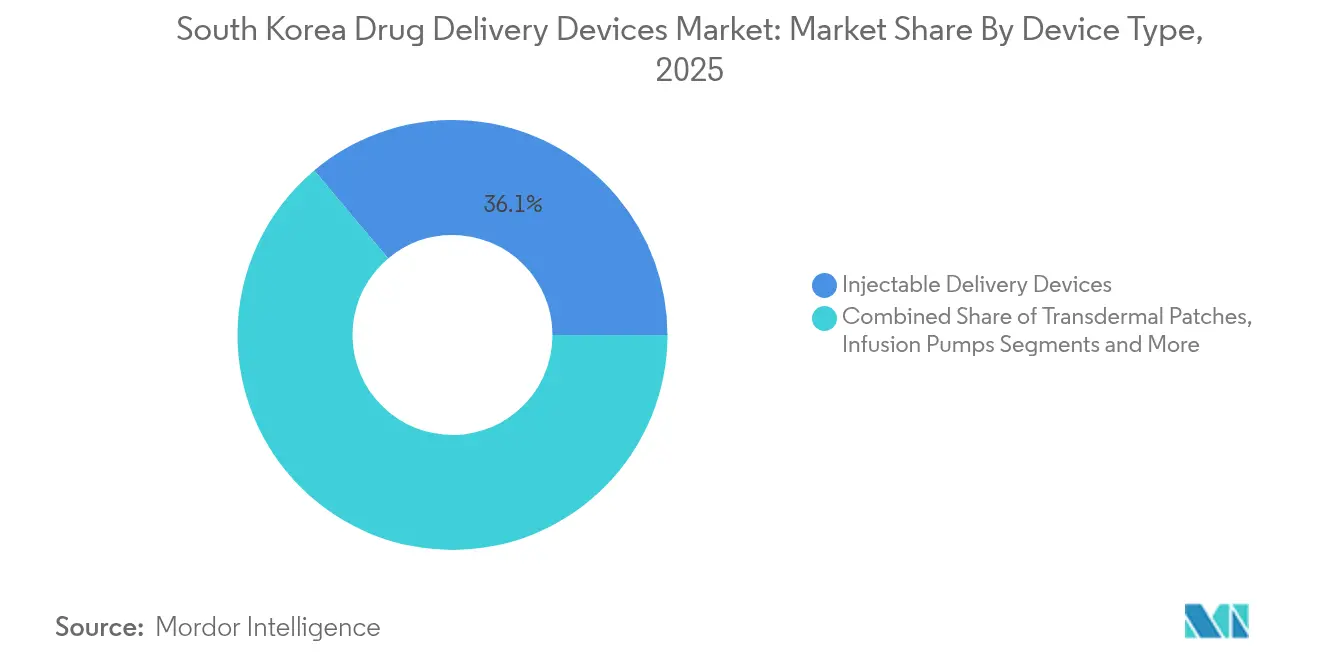

- By device type, injectable delivery devices held 36.12% of South Korea drug delivery devices market share in 2025; implantable systems are projected to expand at a 10.31% CAGR through 2031.

- By route of administration, injectables commanded 56.19% share of the South Korea drug delivery devices market size in 2025, while oral mucosal delivery is forecast to grow at 10.55% CAGR to 2031.

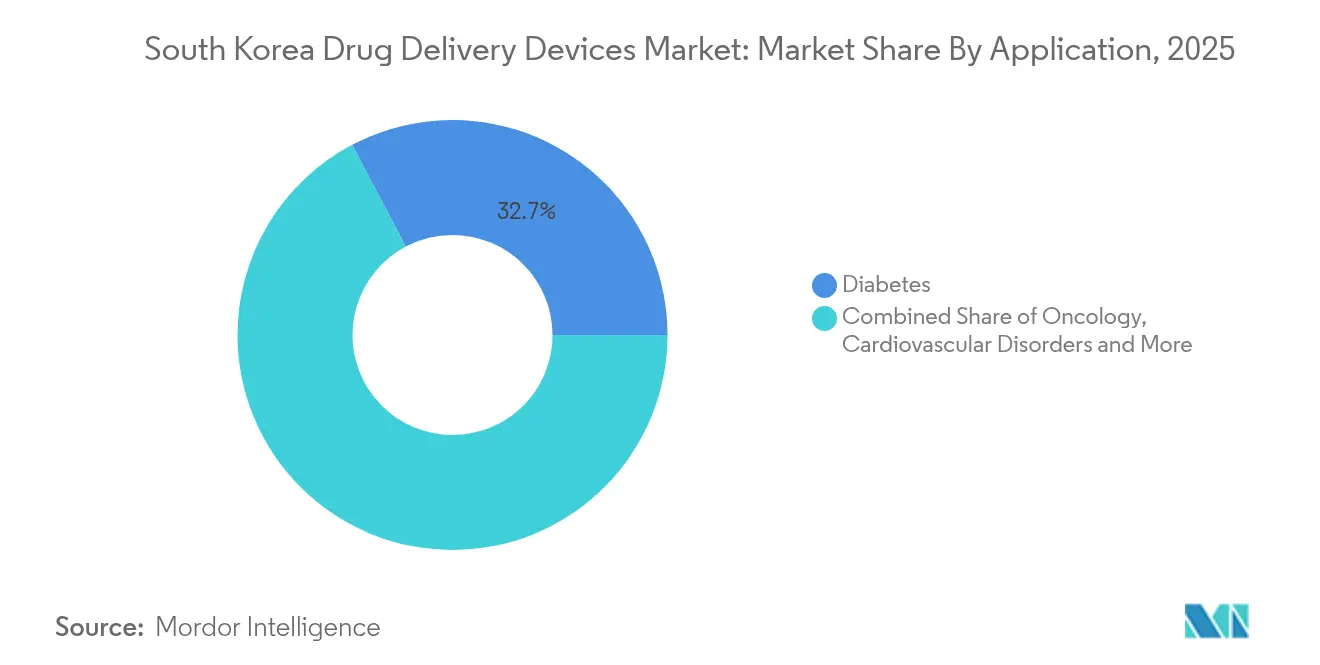

- By application, diabetes accounted for 32.73% of the South Korea drug delivery devices market size in 2025 and oncology is advancing at an 10.96% CAGR through 2031.

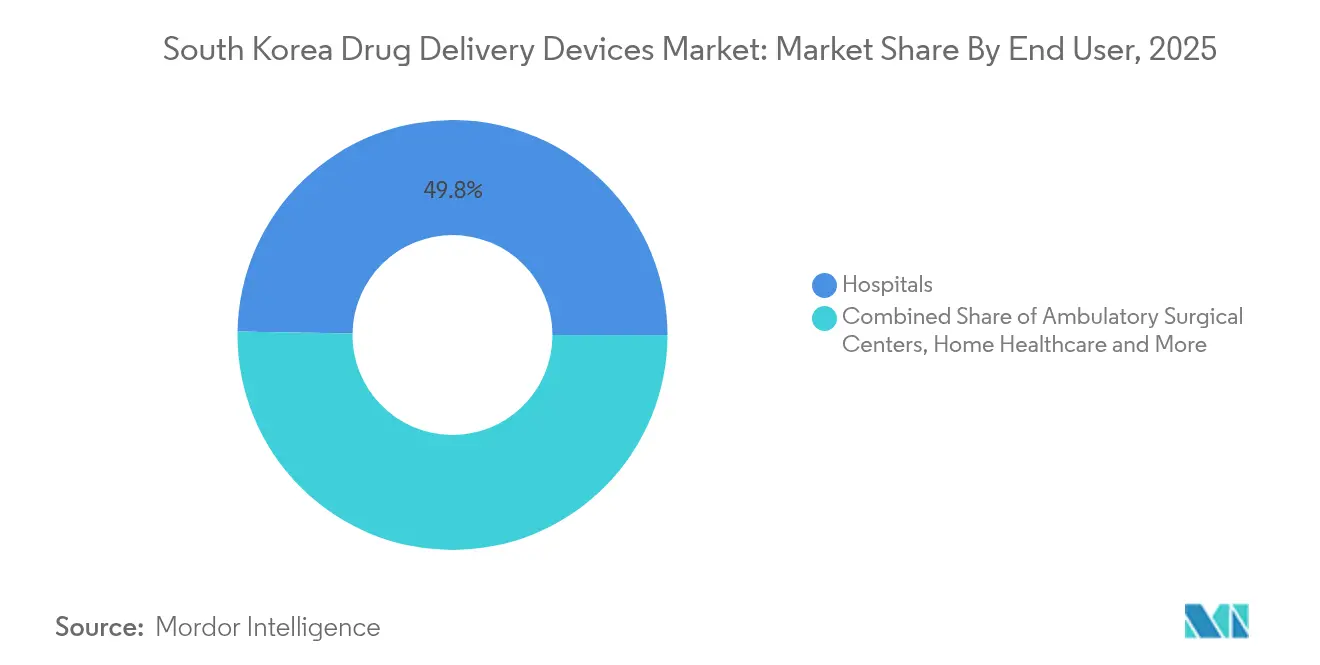

- By end user, hospitals captured 49.75% revenue share in 2025; home healthcare is set to expand at an 10.62% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population Coupled with High Burden Chronic Disease Burden | +1.8% | National, with concentrated impact in Seoul, Busan, and Daegu metropolitan areas | Long term (≥ 4 years) |

| Technological Advancement and Supportive Government Policies | +1.5% | National, with early adoption in Seoul National University Hospital and Samsung Medical Center networks | Medium term (2-4 years) |

| High Digital Health Adoption Supporting Smart Pumps & Connected Inhalers | +1.2% | National, with accelerated penetration in urban centers and tech-forward healthcare systems | Short term (≤ 2 years) |

| Expanding Domestic Biosimilar & Biologic Pipeline Requiring Injectable Formats | +1.0% | National, with manufacturing hubs in Songdo, Ochang, and Osong bioclusters | Medium term (2-4 years) |

| Expansion of Home Healthcare | +0.9% | National, with early gains in Seoul, Incheon, and Gyeonggi Province | Short term (≤ 2 years) |

| Initiatives for Manufacturing and Infrastructure Boost for Drug Delivery Devices | +0.7% | National, with focused development in K-Bio Belt regions and industrial complexes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Coupled with High Chronic Disease Burden

More than 20% of citizens will be 65 or older by end-2025, and 54.8% of these older adults manage multiple chronic conditions.[1]Source: Mi-Sun Lee & Hooyeon Lee, “Chronic Disease Patterns and Their Relationship With Health-Related Quality of Life Among Korean Older Adults,” JMIR Public Health and Surveillance, publichealth.jmir.orgComplex medication schedules heighten demand for user-friendly devices that deliver several drugs with minimal disruption. Frequent comorbid clusters, such as cardiometabolic and arthritis, are steering suppliers toward combination systems tailored to specific patient groups. Out-of-pocket costs nearly triple for multimorbid individuals, motivating insurers to endorse efficient delivery tools that improve adherence and lower total care expenditure.

Technological Advancement and Supportive Government Policies

National programs like the High-Tech Bio Initiative and the 1st Master Plan for Fostering and Supporting the Medical Device Industry provide funding, testbeds, and accelerated reviews that shorten commercialization cycles.[2]Source: Ministry of Health and Welfare, “A Policy Package to Bring Essential Healthcare Back from the Brink of Collapse,” mohw.go.kr Reforms at the Ministry of Food and Drug Safety (MFDS) carve dedicated pathways for breakthrough devices, shrinking approval windows and encouraging early market entry.[3] Nanotechnology-enabled carriers, now progressing through clinical pipelines, demonstrate improved drug loading and targeted release, reinforcing South Korea’s ambition to lead AI-integrated, patient-centric healthcare.

High Digital Health Adoption Supporting Smart Pumps & Connected Inhalers

Nationwide 5G coverage and high smartphone penetration underpin rapid rollout of connected drug delivery devices. MFDS has cleared more than 100 ICT-based medical devices, creating a robust regulatory precedent.[3]Source: Ministry of Food and Drug Safety, “Reform of an Approval and Review System of the MFDS Medical Products,” mfds.go.kr Companies integrate Bluetooth and cloud analytics to track dosing, deliver alerts, and feed population-level datasets that guide public-health policy. Wearable insulin pumps capable of seven-day operation showcase the shift toward passive, always-on administration that reduces user burden and improves glycemic control.

Expanding Domestic Biosimilar & Biologic Pipeline Requiring Injectable Formats

Local manufacturers are scaling up monoclonal antibodies and other large-molecule drugs, amplifying demand for high-precision injectors and sustained-release implants. Partnerships such as the oral antibody capsule collaboration between Celltrion and Rani Therapeutics illustrate how firms convert hospital-delivered injectables into self-administered oral therapies, easing adoption barriers for patients while maintaining drug integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Approval & Vigilance Delaying Novel Device Launches | -1.3% | National, with regulatory bottlenecks concentrated at MFDS headquarters in Cheongju | Medium term (2-4 years) |

| Risks and Safety Concerns Related to Devices | -0.8% | National, with heightened scrutiny in major hospital networks and academic medical centers | Short term (≤ 2 years) |

| HIRA Price Caps Compressing Premium Device Margins | -1.1% | National, affecting all healthcare providers under National Health Insurance coverage | Long term (≥ 4 years) |

| Hospital Tender Bias Toward Domestic Vendors Limiting Foreign Manufacturers | -0.9% | National, with strongest impact on public hospitals and government-affiliated medical institutions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Approval and Vigilance Delaying Novel Device Launches

MFDS classifies devices by risk, and Classes II–IV undergo extensive dossier reviews, including quality, safety, and sometimes clinical data.[3]Source: Ministry of Food and Drug Safety, “Reform of an Approval and Review System of the MFDS Medical Products,” mfds.go.kr For foreign firms, the mandatory Korean License Holder adds administrative layers. Post-market surveillance lists track 52 device categories, imposing ongoing reporting that can deter small entrants.

Risks and Safety Concerns Related to Devices

Complex electromechanical formats introduce failure points in pumps and implants. MFDS requires manufacturers to institute traceability and field correction protocols, prolonging development timelines. User errors during home use lead suppliers to invest in intuitive interfaces, automated shutoffs, and tamper-proof packaging, adding cost and design constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Injectable Platforms Lead Innovation Wave

Injectable platforms account for 36.12% of South Korea drug delivery devices market share in 2025, reflecting their versatility across diabetes, oncology, and autoimmune therapy. Demand remains steady as biologics dominate development pipelines. Implantable systems, posting a 10.31% CAGR to 2031, benefit from biocompatible polymers that release drugs over months, lowering dosing frequency for chronic pain and hormone disorders. Clinical data from domestic cohorts confirm reduced opioid exposure when intrathecal pumps replace systemic analgesics.

Wearable injectors, fixed‐dose autoinjectors, and on-body pumps enhance self-management. Transdermal patches broaden options for neurological and pain conditions, with twice-weekly rivastigmine patches easing caregiver workloads. Inhalers, now integrating dose-tracking chips, link to mobile apps for personalized coaching. Nasal and ocular inserts remain niche but attract R&D interest for CNS drugs and ophthalmic biologics. Growing acceptance of these alternatives signals ongoing diversification within the South Korea drug delivery devices market.

By Route of Administration: Patient Preference Shifts

Injectables cover 56.19% of administration routes in 2025, favored for their proven bioavailability and compatibility with complex molecules. Oral mucosal formats show the fastest 10.55% CAGR, drawing traction for rapid onset and ease of use. Thin films dissolving in seconds avoid first-pass metabolism, helping dysphagic patients adhere to regimens. The South Korea drug delivery devices market size for mucosal routes is projected to expand steadily alongside R&D investments that improve permeability enhancers and taste-masking agents.

Transdermal technology advances through micro‐needle arrays that painlessly breach the stratum corneum and deliver steady plasma levels over several days. Respiratory applications hold a stable share as chronic obstructive pulmonary disease and asthma prevalence rises. Ocular and nasal routes gain strategic importance for vaccines and neuro-active peptides that target the brain, bypassing systemic clearance barriers.

By Application: Diabetes Management Drives Demand

Diabetes commands 32.73% of the South Korea drug delivery devices market size in 2025, propelled by rising prevalence and a push for automated insulin delivery. Closed-loop pump-sensor ecosystems capture continuous glucose data and adjust basal rates in real time, cutting hypoglycemia risk. Oncology, expanding at 10.96% CAGR, leverages sustained-release depots and antibody-drug conjugate injectors to localize therapy, minimizing systemic toxicity.

Cardiovascular applications leverage polymer-based stents and bioresorbable depots to deliver antithrombotics. Respiratory disease management capitalizes on smart inhalers that upload adherence metrics to clinician dashboards. Infectious disease programs seek room-temperature–stable patches and oral vaccines suitable for mass campaigns. Auto-immune disorders round out the market, drawing on self-injectable biologics and novel oral platforms for patient-controlled therapy at home.

By End User: Hospitals Retain Core Role

Hospitals hold 49.75% of 2025 revenue, supported by resources to manage complex infusion and implant procedures. They adopt integrated pump fleets that link with electronic medical records for dose logging and pharmacovigilance. The South Korea drug delivery devices market is pivoting as home healthcare, growing at 10.62% CAGR, absorbs routine chronic care through plug-and-play devices optimized for non‐clinical settings. Urban patients embrace video consultations combined with connected pumps that alert nurses to anomalies.

Ambulatory surgical centers gain relevance by using long-acting local anesthetic depots that shorten recovery times, enabling same-day discharge. Specialty clinics, particularly endocrinology and oncology units, trial novel injectors and patches before home rollout. Seamless transition of devices across sites underscores the integrated care model encouraged by national policy.

Geography Analysis

South Korea’s highly urbanized corridor stretching from Seoul through Incheon to Suwon anchors the largest share of the South Korea drug delivery devices market. High broadband penetration and tertiary hospitals support early adoption of smart pumps and AI-enabled inhalers. Rural provinces face physician shortages; remote-monitoring devices bridge gaps by transmitting adherence and biometric data to regional care teams. Government grants for telemedicine kiosks in county clinics further expand reach for chronic disease tools.

Coastal cities such as Busan and Ulsan show growing demand driven by aging populations employed in industrial sectors with elevated respiratory conditions. Local governments subsidize COPD management programs that bundle connected inhalers and virtual coaching. In central regions, provincial hospitals implement implantable depots for cancer pain, reducing travel frequency for elderly residents.

Jeju’s medical tourism initiatives attract regional patients seeking advanced biologic therapies administered through long-acting injectables. The island’s special regulatory zone expedites studies on micro-needle patches for traveler vaccinations, broadening exposure for device manufacturers. Across all regions, national reimbursement policies equalize patient out-of-pocket costs, sustaining unified growth momentum for the South Korea drug delivery devices market.

Competitive Landscape

The market hosts a balanced mix of global multinationals and innovative domestic firms. LG Chem advances biologic-compatible prefilled syringes and collaborates with start-ups on AI algorithms that predict dosing schedules. Yuhan Corporation invests in micro-needle patch production lines that promise higher yields and sterile integrity. International leaders supply electromechanical pump assemblies, while local firms customize software and language interfaces, strengthening stickiness with Korean hospitals.

Strategic alliances multiply. Celltrion’s joint work on oral antibody capsules illustrates convergence between pharmaceutical formulation and device engineering, reducing injection frequency. EOFlow pilots seven-day wearable insulin pumps, positioning for overseas licensing. Overseas players set up R&D hubs in Seoul to tap skilled engineers and access MFDS fast-track reviews.

Price pressure from the Health Insurance Review and Assessment Service (HIRA) sparks innovation on materials and manufacturing efficiency. Firms streamline supply chains and shift toward modular pump designs that share components across therapeutic indications. Robust patent portfolios, backed by universities and public research institutes, sustain a pipeline of nanocarriers and biodegradable implants, keeping the South Korea drug delivery devices market competitive and technology-focused.

South Korea Drug Delivery Devices Industry Leaders

Baxter International

Johnson & Johnson

Terumo Corporation

Becton, Dickinson and Company

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SHL Medical will join COPHEX 2025 on April 22–25 at KINTEX in Goyang, South Korea, where it plans to showcase its newest injectable-device platforms to stakeholders focused on advanced drug-delivery, healthcare industrialization, and high-volume production

- January 2025: Evonik and ST Pharm agreed to integrate ST Pharm’s active-pharmaceutical-ingredient capabilities for gene therapy with Evonik’s lipid-nanoparticle expertise to speed development of RNA and other nucleic-acid therapeutics.

- January 2025: Eli Lilly launched Ebglyss, a 250 mg pre-filled autoinjector containing lebrikizumab, for the treatment of atopic dermatitis in South Korea.

- February 2024: Luye Pharma granted Myung In Pharm exclusive South Korean marketing rights for the twice-weekly rivastigmine transdermal patch that treats mild to moderate Alzheimer’s dementia.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study regards the South Korea drug delivery devices market as the annual sales value of purpose-built medical devices that release a therapeutic agent through injectable, inhalation, transdermal, implantable, ocular, nasal, oral-mucosal, and infusion routes inside the country, wherever the primary intent is controlled or targeted drug administration for human use.

Scope Exclusions: Diagnostic catheters, drug-eluting stents, and purely pharmaceutical formulations without an integrated delivery mechanism fall outside Mordor's scope.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- By Application

- Diabetes

- Oncology

- Cardiovascular Disorders

- Respiratory Diseases

- Infectious Diseases

- Auto-immune & Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare Settings

- Specialty Clinics

Detailed Research Methodology and Data Validation

Primary Research

Interview rounds with hospital pharmacy chiefs, device product managers, and reimbursement specialists across Seoul, Busan, and Jeju validated adoption rates, typical selling prices, and route-of-administration splits. Follow-up surveys with home-health practitioners and community endocrinologists helped our team confirm rapid uptake of wearable injectors and refine growth assumptions around diabetes care outside tertiary centers.

Desk Research

We collected baseline supply, price, and utilization clues from open statistics issued by the Ministry of Food and Drug Safety, the Korea Health Industry Development Institute, customs trade dashboards, and disease prevalence datasets released under the Korean National Health & Nutrition Examination Survey. Complementary trend signals came from peer-reviewed clinical journals, Korea Medical Device Industry Association briefs, and large hospital purchasing disclosures.

To strengthen company-level calibration, Mordor analysts extracted audited sales lines from SEC or KRX filings, sifted local press articles via Dow Jones Factiva, and sampled device registrations filed under MFDS's Medical Device Information Service. These publicly available anchors are then cross-checked against subscription sources such as D&B Hoovers and Questel for any patent-driven pipeline shifts. The list above is illustrative; many other trusted sources were referenced for data gathering and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with MFDS production plus net import statistics, which are then value-adjusted using median ex-factory prices sourced from tender databases before being further filtered through device-specific penetration rates among key disease cohorts. Select bottom-up checks, such as sampled ASP × volume roll-ups at three distributor clusters, provide reality checks against the national totals. Variables that drive the model include diagnosed diabetes population, oncology biologic prescription counts, home-health enrollment, per-capita healthcare spend, average price ceilings set by HIRA, and patent expiry timelines. A multivariate regression, stress-tested under optimistic and conservative uptake scenarios, projects demand to 2030; gaps in granular input are bridged by weighted averages from nearest comparable device classes.

Data Validation & Update Cycle

Outputs pass anomaly scans against historical series, peer ratios, and prior editions. Senior reviewers flag variances above two standard deviations for re-contact. Reports refresh every twelve months, with interim updates triggered by regulatory shocks or landmark product launches; an analyst re-validates figures again just before client delivery.

Why Our South Korea Drug Delivery Devices Baseline Commands Reliability

Published estimates differ because firms choose dissimilar device baskets, price bases, or refresh cadences.

Key gap drivers include divergent inclusion of low-priced disposable syringes, contrasting ASP escalation paths, and less frequent model refreshes in some studies, which tend to overstate the current-year value relative to Mordor's disciplined 2025 baseline anchored to verified MFDS trade data and most recent hospital tender prices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.08 B | Mordor Intelligence (2025) | - |

| USD 8.04 B | Regional Consultancy A (2024) | Aggregates Asia-Pacific averages, uses list prices, refreshes biennially |

| USD 8.20 B | Trade Journal B (2024) | Includes drug-eluting stents and diagnostic catheters, applies flat 6 % annual growth from 2019 base |

In summary, the tighter scope, annual refresh, and price reality checks help Mordor deliver a balanced, transparent baseline that decision-makers can retrace to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the South Korea drug delivery devices market?

The market is valued at USD 5.47 billion in 2026 and is set to grow to USD 7.93 billion by 2031.

Which device type holds the largest share?

Injectable platforms lead with 36.12% share in 2025 due to their broad applicability in diabetes, oncology, and autoimmune conditions.

Which segment is growing the fastest?

Implantable systems are advancing at a 10.31% CAGR as biocompatible materials enable longer-acting therapies with fewer interventions.

Why is home healthcare gaining momentum?

Government incentives to reduce hospitalization costs and widespread digital infrastructure support remote monitoring, driving an 10.62% CAGR in home-use devices.

How are regulations influencing innovation?

MFDS fast-track pathways and the New Bio-Health Industry Regulation Innovation Plan shorten approval times, encouraging rapid introduction of breakthrough technologies.

What role do domestic companies play in the market?

Firms such as LG Chem, Yuhan, and Celltrion are partnering with technology specialists and investing in R&D to compete head-to-head with global multinationals across injectable, patch, and implant platforms.

Page last updated on: