Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

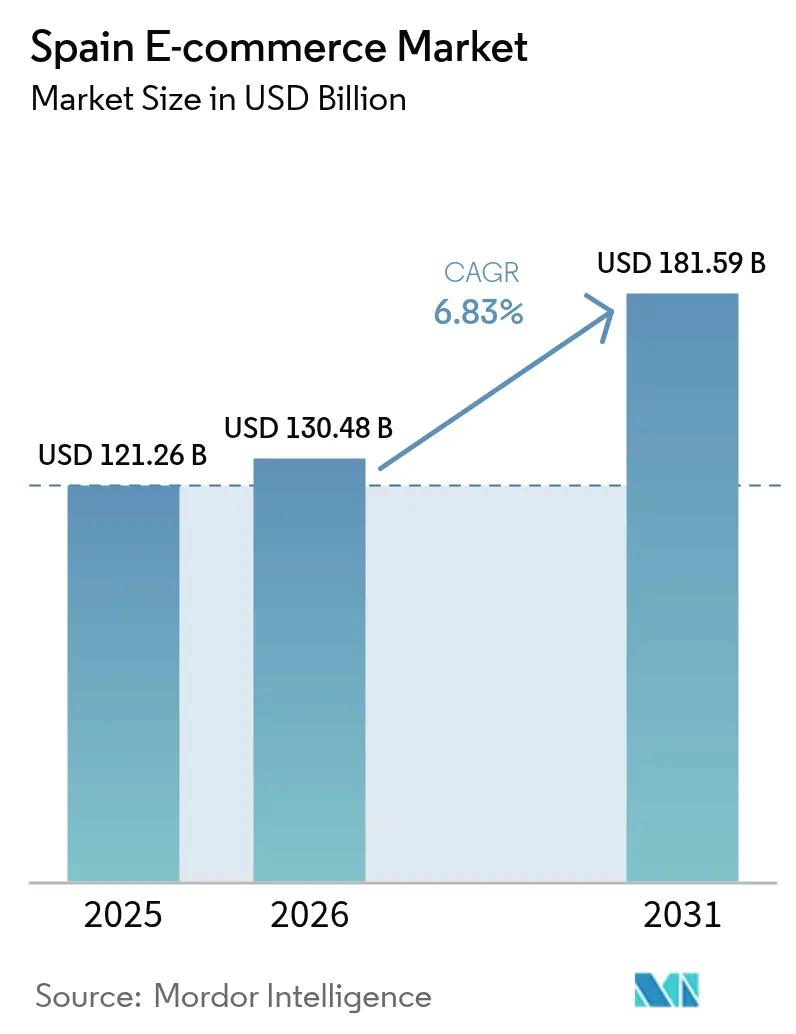

| Base Year Market Size (2025) | USD 121.26 Billion |

| Market Size (2026) | USD 130.48 Billion |

| Market Size (2031) | USD 181.59 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

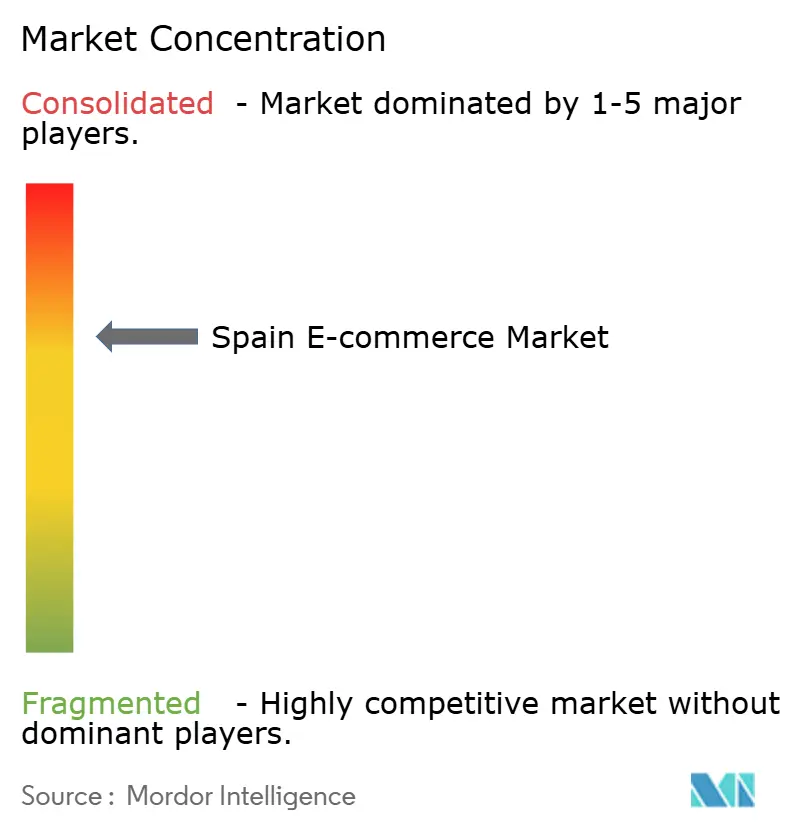

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain E-commerce Market Analysis by Mordor Intelligence

The Spain e-commerce market size was valued at USD 121.26 billion in 2025 and estimated to grow from USD 130.48 billion in 2026 to reach USD 181.59 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). Mobile-first shopping has become mainstream as 5G coverage reaches 96% of urban areas, while Bizum’s one-click account-to-account payments shorten checkout time and lower merchant fees. Kit Digital vouchers worth EUR 3.067 billion (USD 3.46 billion) ease capital constraints for small firms, prompting tens of thousands of new online storefronts. Same-day delivery capability has expanded beyond Madrid-Barcelona corridors, narrowing the service-level gap between local retailers and Amazon. Cross-border demand from Latin American consumers, attracted by Spanish-language sites and euro pricing, adds a second growth engine.

Key Report Takeaways

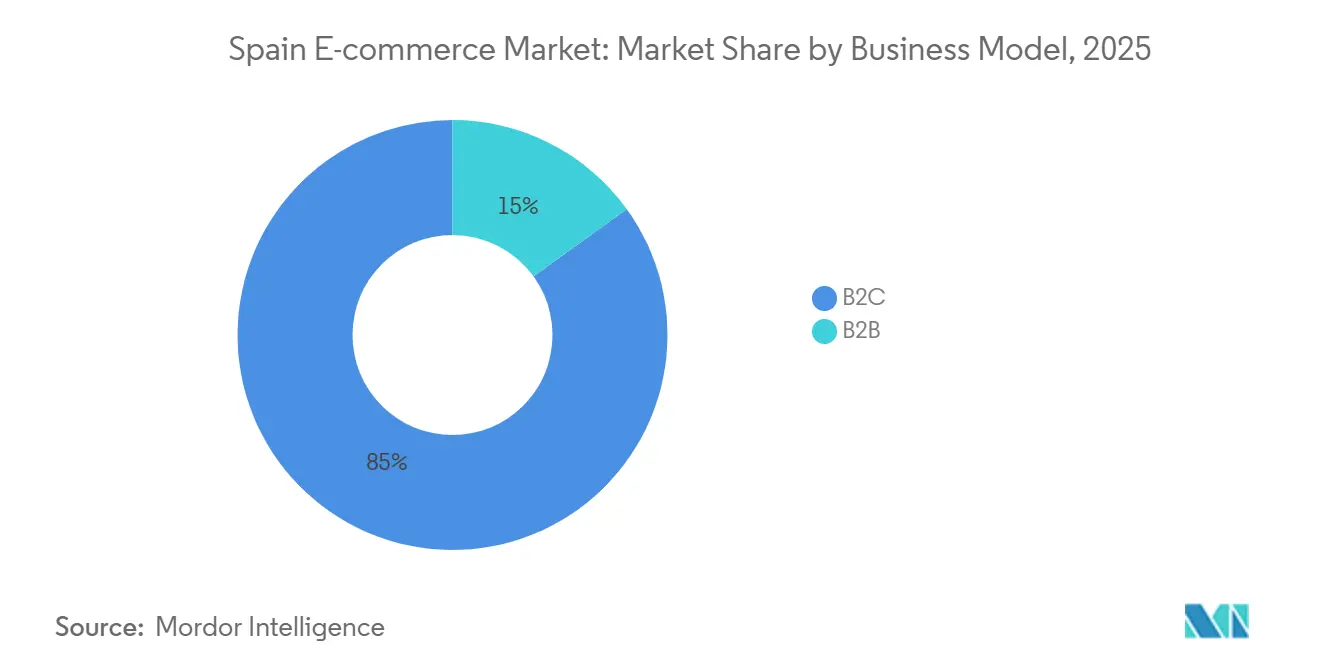

- By business midel, business-to-consumer transactions commanded 84.97% of 2025 value, while business-to-business is projected to grow at a 7.43% CAGR through 2031.

- By device type, smartphones drove 69.67% of B2C traffic in 2025; desktop and laptop channels are forecast to expand at a 7.26% CAGR as larger screens support considered purchases.

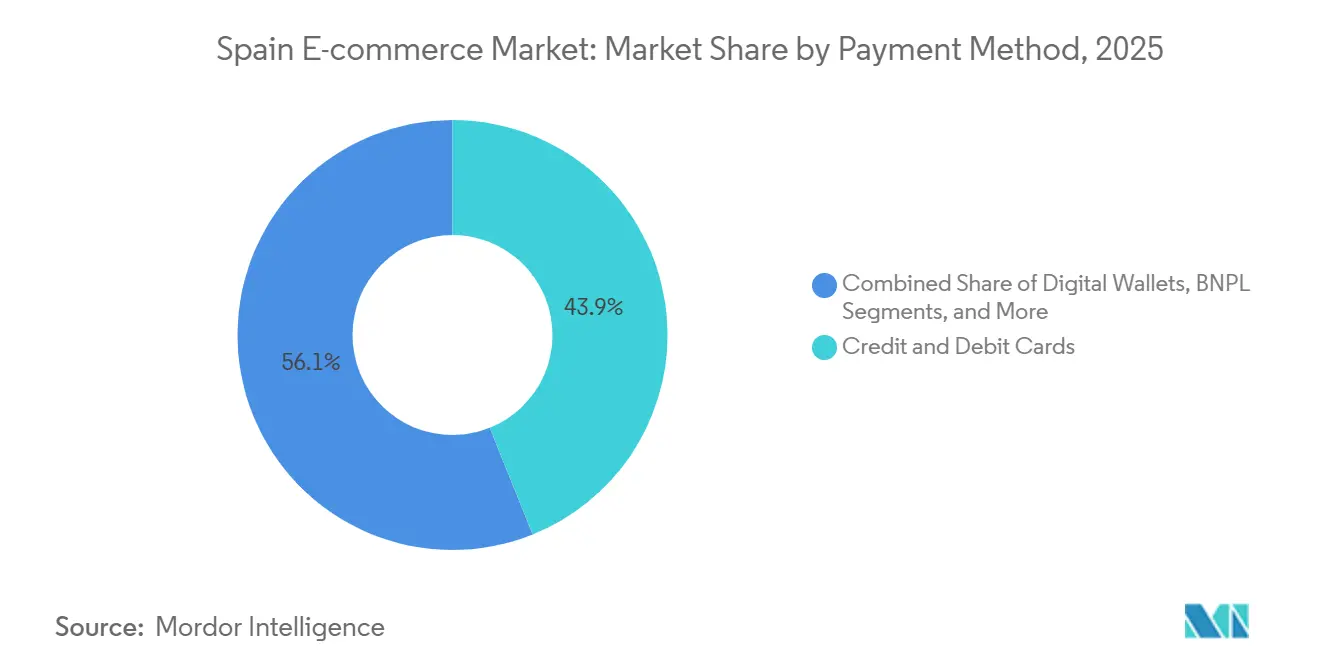

- By payment method, credit and debit cards held 43.92% of payment share in 2025, whereas buy-now-pay-later solutions are advancing at a 8.37% CAGR to 2031.

- by product category, fashion and apparel accounted for 29.49% of category spending in 2025, yet beauty and personal care is expected to expand at a 7.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Penetration of Bizum Instant-Payment System | +1.1% | National, strongest in Madrid, Catalonia, Basque Country | Short term (≤ 2 years) |

| Government Kit Digital Grants Accelerating SME Digitalization | +1.3% | National, early gains in Andalusia, Valencian Community, Galicia | Medium term (2-4 years) |

| Expansion of Same-Day Delivery Networks by Correos and SEUR | +0.9% | Madrid, Barcelona, Valencia, Seville metro areas | Short term (≤ 2 years) |

| 5G-Driven Surge in Mobile-First Shopping | +1.2% | National, earlier in large urban centers | Long term (≥ 4 years) |

| Cross-Border Demand from Latin-American Spanish-Speaking Shoppers | +0.7% | Nationwide, concentrated in fashion, beauty, electronics | Medium term (2-4 years) |

| Rising Adoption of Sustainable Delivery and Reverse-Logistics Solutions | +0.4% | Primary and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Penetration of Bizum Instant-Payment System

Bizum’s 20 million-strong user base enables one-tap checkout that bypasses card rails, cutting interchange fees for merchants and boosting repeat purchase rates.[1]Bizum, “About Us,” bizum.es The service processed 763 million transactions in 2023 and plans NFC point-of-sale functionality in 2025, unifying online and offline payment experiences. Bank-consortium governance guarantees interoperability across institutions, limiting fragmentation that hindered digital wallets elsewhere in Europe. Regulatory alignment with PSD2 simplifies cross-border compliance as Spanish sellers target Latin America. Together, these factors lift conversion rates and widen the addressable base for the Spain e-commerce market.

Government Kit Digital Grants Accelerating SME Digitalization

Funded by EU recovery resources, Kit Digital provides vouchers of EUR 12,000 (USD 14,300), EUR 6,000 (USD 7,100), and EUR 2,000 (USD 2,400) that subsidize e-commerce platforms, cloud inventory tools, and digital marketing for smaller firms. By 2024, tens of thousands of SMEs had claimed grants, sharply raising online product variety and competition. Adoption is notably strong in Andalusia and Galicia, regions historically behind Madrid and Catalonia in digital maturity. Certified-provider bundles encourage integrated point-of-sale and logistics solutions, cutting order errors and reconciliation costs. This policy backdrop underpins longer-term infrastructure investment in broadband and cybersecurity, reinforcing growth prospects for the Spain e-commerce market.

Expansion of Same-Day Delivery Networks by Correos and SEUR

Correos has earmarked EUR 1.8 billion (USD 2.03 billion) for parcel-network upgrades, including electric vans and 2,400 click-and-collect points, extending same-day service across major metros. SEUR’s micro-fulfillment hubs use bike couriers to navigate low-emission zones. Faster delivery elevates customer satisfaction: global surveys show same-day options can lift conversion by up to 20%. Sustainability mandates in Madrid and Barcelona further reward carriers that decarbonize early. Collectively, these efforts raise service parity, fueling incremental demand for the Spain e-commerce market.

5G-Driven Surge in Mobile-First Shopping

Spain’s Digital 2026 agenda pushed 5G to 96% urban and 80% rural coverage by 2024.[2]Ministry of Economic Affairs and Digital Transformation, “5G Deployment in Spain,” mineco.gob.es Lower latency supports video-based product demos and augmented-reality try-ons, enhancing engagement on mobile devices. Retailers deploy progressive web apps that load quickly even on congested networks, keeping bounce rates low. Enhanced coverage also brings underserved rural shoppers into the Spain e-commerce market, narrowing the urban-rural gap. Over the forecast horizon, 5G will underpin immersive shopping formats such as live-stream commerce and interactive gaming tie-ins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Last-Mile Logistics in Rural Provinces Raising Fulfillment Costs | -0.7% | Castilla y León, Extremadura, Castilla-La Mancha, Aragón, rural Galicia | Medium term (2-4 years) |

| Persistent Cash-on-Delivery Culture Limiting Online Payment Conversion | -0.9% | Nationwide, higher in older demographics and rural areas | Short term (≤ 2 years) |

| Strict LOPDGDD / GDPR Enforcement Elevating SME Compliance Costs | -0.3% | National, heavier on micro-enterprises | Long term (≥ 4 years) |

| High Product-Return Rates in Fashion Segment Eroding Margins | -0.6% | National, concentrated in online-only fashion retailers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Cash-on-Delivery Culture Limiting Online Payment Conversion

Cash represented 36% of Spain’s physical point-of-sale transactions in 2025, the highest share in Europe. Cash-on-delivery complicates reconciliation, lifts return-to-origin risk, and adds courier handling costs. Older consumers distrust digital payment security, a sentiment reinforced by the 367 fines totaling EUR 30 million (USD 33.8 million) issued by the Spanish Data Protection Agency in 2023.[3]Spanish Data Protection Agency, “Annual Report 2023,” aepd.es While Bizum and digital wallets attract younger cohorts, merchants still incur operational drag until cash preference recedes. This headwind restrains the full potential of the Spain e-commerce market.

Fragmented Last-Mile Logistics in Rural Provinces Raising Fulfillment Costs

Delivery expenses in low-density provinces can run 30%-50% above urban rates as route optimization is difficult. Rural residents make up 20% of Spain’s population yet generate a much smaller share of e-commerce orders, inhibiting network scale. Correos is extending coverage, but same-day promises remain economically unfeasible in many areas. Limited parcel lockers and reliance on legacy van routes lengthen transit times, diminishing customer satisfaction. Unless drone or autonomous-vehicle pilots prove viable, rural logistics will cap upside for the Spain e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Procurement Digitization Reshapes Corporate Buying

Business-to-consumer transactions owned 84.97% of 2025 value, but business-to-business sales are forecast to outpace with a 7.43% growth rate through 2031. Catalysts include Kit Digital grants that fund ERP integrations, allowing wholesalers to automate ordering and inventory syncing. Larger average order values improve working-capital efficiency, while digital catalogs simplify compliance with public-sector procurement rules. Cross-border B2B flows from Latin America leverage shared language and Spain’s EU trade advantages, injecting resiliency during consumer down-cycles.

Omnichannel retailers continue to refine click-and-collect, turning store networks into micro-fulfillment nodes. Inditex uses real-time stock visibility to pick online orders from local Zara stores, cutting last-mile distance and reinforcing loyalty. Amazon’s 40-site fulfillment grid intensifies price competition but also elevates customer expectations, prompting domestic players to match speed and free-return policies. B2B platforms cope with tiered pricing, negotiated credit terms, and regulatory documentation, but once digitized, these complexities create high switching costs and deepen the Spain e-commerce market moat.

By Device Type: Large Screens Support Considered Purchases

Mobile devices generated 69.67% of traffic and a majority of transactions in 2025. Desktop traffic, however, is projected to grow at a 7.26% CAGR as shoppers research high-ticket electronics and furniture that benefit from larger displays. The Spain e-commerce market share of desktop channels could exceed 35% in revenue terms by the late forecast period, despite lower visit counts. Rich-media configurators, side-by-side spec comparisons, and finance calculators remain easier to use on laptops, nurturing higher average order values.

Retailers deploy responsive websites so that saved carts travel seamlessly between devices, ensuring shoppers who browse on phones can complete checkout on desktops. 5G reduces mobile latency, but battery limits and notification overload still push some buyers to larger screens for final payment. Voice shopping via smart assistants holds niche appeal, mainly for repeat grocery orders, but improved natural-language processing may lift its role over time. Device diversity obliges merchants to maintain consistent branding and functionality across all touchpoints, safeguarding growth for the Spain e-commerce market.

By Payment Method: Installment Flexibility Gains Momentum

Cards controlled 43.92% of checkout share in 2025, yet their dominance is shrinking as buy-now-pay-later (BNPL) adoption accelerates. BNPL volumes expanded more than 8% year-on-year in 2025, capturing younger demographics that favor transparent installments without revolving interest. Spain's e-commerce market size for digital-wallet payments, which include Bizum, PayPal, and Apple Pay, reached USD 27 billion in 2025. Bizum alone drove 21% of e-commerce transactions, the highest penetration of bank-based instant payments in Western Europe.

Regulators are weighing stricter BNPL rules to align creditworthiness checks with banking standards. Merchants, meanwhile, appreciate higher conversion rates and larger baskets when BNPL is available. Cash-on-delivery continues to decline in relative terms but lingers where broadband and card penetration lag. Payment diversification reduces dependency on any single rail, insulating the Spain e-commerce market from systemic outages or fee hikes.

By Product Category: Beauty Outpaces Fashion’s Scale

Fashion led with 29.49% of 2025 spending, reflecting Spain’s strong fast-fashion heritage. Beauty and personal care is forecast to compound at 7.18%, narrowing the gap as influencer marketing drives trial and replenishment. Online beauty shoppers favor video tutorials and virtual try-ons that 5G makes smoother, shortening discovery-to-purchase cycles. Consumer electronics remain cyclical but benefit from 5G handset replacement and demand for work-from-anywhere hardware. Online food and beverages still account for a single-digit share of grocery sales, but rise quickly with 30-minute delivery promises in dense cities.

High return rates, up to 37.5% for premium apparel, pressure margins, and increase carbon footprints. Retailers respond with size-recommendation algorithms and paid-membership models that offset logistics costs. Subscription services for DIY and pet supplies build recurring revenue streams. Category diversification cushions sellers against fashion volatility and strengthens the Spain e-commerce market’s overall resilience.

Geography Analysis

Madrid and Catalonia produced the lion’s share of online spending in 2025, aided by dense logistics assets, higher disposable incomes, and early Bizum adoption. Amazon’s capital outlays intensified same-day coverage across both metros, while Inditex leveraged store networks for two-hour click-and-collect. The Community of Madrid’s corporate concentration boosts B2B procurement, and Catalonia’s manufacturing base underpins export-led transactions.

Andalusia and the Valencian Community, although smaller today, are forecast to be the fastest growers through 2031. Same-day delivery has extended to Seville, Málaga, and Valencia, narrowing service disparities. Kit Digital vouchers accelerate SME onboarding in these regions, expanding product variety and local employment. 5G rural coverage, now at 80%, enables mobile shopping in previously underserved municipalities, enlarging the Spain e-commerce market footprint.

Other autonomous communities display mixed dynamics. The Basque Country’s industrial clusters drive B2B demand, while Galicia contends with scattered settlements that lift delivery costs. Castilla y León and Aragón face 30%-50% higher per-parcel expenses, forcing platforms to levy surcharges or limit service levels. Public-sector broadband investments aim to close the gap, yet physical logistics remain the binding constraint on nationwide parity.

Competitive Landscape

The Spain e-commerce market features a triad of heavyweights, Amazon, El Corte Inglés, and Inditex, that collectively command a sizable but not dominant share, leaving ample room for niche specialists. Amazon operates more than 40 logistics sites, providing an unmatched assortment and same-day reach. El Corte Inglés is converting stores into fulfillment nodes and scaling its marketplace to onboard 5,000 third-party sellers by 2026. Inditex, with EUR 10.2 billion (USD 11.5 billion) in online sales, merges store stock and digital demand, cutting last-mile distances and improving sell-through.

Quick-commerce players such as Glovo partner with grocers for sub-30-minute delivery, testing the limits of urban density economics. Specialty retailers like MediaMarkt and PcComponentes compete on expert advice and bundled services, differentiating beyond price. Compliance overhead from strict data-protection enforcement favors larger platforms with legal resources, nudging smaller sellers toward marketplace aggregation. Investment priorities span artificial intelligence for personalized search, augmented reality for product visualization, and blockchain for supply-chain transparency, all enabled by ubiquitous 5G bandwidth.

White-space opportunities remain in rural coverage and Latin American cross-border flows. Logistics innovation, including parcel lockers at fuel stations and scheduled drone trials, could unlock new cohorts of shoppers. As sustainable delivery mandates tighten, carriers with electrified fleets will enjoy early-mover advantages, cementing their role in the evolving Spain e-commerce market.

Spain E-commerce Industry Leaders

Amazon EU S.à r.l.

El Corte Inglés S.A.

PC Componentes y Multimedia S.L.

Centros Comerciales Carrefour S.A.

Zara Spain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amazon Spain opened two fulfillment centers in Zaragoza and Seville, adding 500,000 square meters of capacity and 1,500 permanent jobs.

- December 2024: Inditex completed nationwide deployment of real-time inventory management, reducing click-and-collect lead times to under two hours in major metros.

- November 2024: Carrefour Spain partnered with Glovo to launch 30-minute grocery delivery in Madrid, Barcelona, and Valencia.

- October 2024: Correos rolled out 500 electric delivery vehicles in Madrid and Barcelona as part of its EUR 1.8 billion fleet decarbonization plan.

Spain E-commerce Market Report Scope

The Spain E-commerce Market Report is Segmented by Business Model (B2B, B2C), Device Type for B2C E-commerce (Smartphone and Mobile, Desktop and Laptop, Other Device Types), Payment Method for B2C E-commerce (Credit and Debit Cards, Digital Wallets, Buy Now Pay Later, Other Payment Methods), Product Category for B2C E-commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Other Product Categories), and Geography (Community of Madrid, Catalonia, Andalusia, Valencian Community, Rest of Spain). The Market Forecasts are Provided in Terms of Value (USD).

By Business Model

| B2B |

| B2C |

By Device Type for B2C E-Commerce

| Smartphone and Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method for B2C E-Commerce

| Credit and Debit Cards |

| Digital Wallets |

| Buy Now Pay Later |

| Other Payment Methods |

By Product Category for B2C E-Commerce

| Beauty and Personal Care | Hair Care |

| Skin Care | |

| Cosmetics and Beauty | |

| Other Beauty and Personal Care Product Categories | |

| Consumer Electronics | Mobile |

| PC and Laptops | |

| Audio Devices | |

| Gaming Devices | |

| Other Consumer Electronics Product Categories | |

| Fashion and Apparel | Clothing |

| Footwear | |

| Fashion Accessories | |

| Other Fashion and Apparel Product Categories | |

| Food and Beverages | Packaged Food |

| Bakery and Confectionery | |

| Meat, Poultry, and Seafood | |

| Other Food and Beverages Product Categories | |

| Furniture and Home | Home Furniture |

| Office Furniture | |

| Outdoor Furniture | |

| Other Furniture and Home Product Categories | |

| Other Product Categories |

| By Business Model | B2B | |

| B2C | ||

| By Device Type for B2C E-Commerce | Smartphone and Mobile | |

| Desktop and Laptop | ||

| Other Device Types | ||

| By Payment Method for B2C E-Commerce | Credit and Debit Cards | |

| Digital Wallets | ||

| Buy Now Pay Later | ||

| Other Payment Methods | ||

| By Product Category for B2C E-Commerce | Beauty and Personal Care | Hair Care |

| Skin Care | ||

| Cosmetics and Beauty | ||

| Other Beauty and Personal Care Product Categories | ||

| Consumer Electronics | Mobile | |

| PC and Laptops | ||

| Audio Devices | ||

| Gaming Devices | ||

| Other Consumer Electronics Product Categories | ||

| Fashion and Apparel | Clothing | |

| Footwear | ||

| Fashion Accessories | ||

| Other Fashion and Apparel Product Categories | ||

| Food and Beverages | Packaged Food | |

| Bakery and Confectionery | ||

| Meat, Poultry, and Seafood | ||

| Other Food and Beverages Product Categories | ||

| Furniture and Home | Home Furniture | |

| Office Furniture | ||

| Outdoor Furniture | ||

| Other Furniture and Home Product Categories | ||

| Other Product Categories | ||

Key Questions Answered in the Report

How large will online retail spending in Spain be by 2031?

It is projected to reach USD 181.59 billion, reflecting a 6.83% CAGR from 2026.

Which Spanish regions show the fastest e-commerce growth?

Andalusia and the Valencian Community are set to outpace national averages as same-day delivery expands and SMEs adopt Kit Digital solutions.

What payment methods are gaining share among Spanish shoppers?

Buy-now-pay-later and Bizum account-to-account payments are the fastest-growing options, especially with younger demographics.

Why is business-to-business e-commerce accelerating in Spain?

Kit Digital subsidies and ERP integrations allow wholesalers and industrial buyers to shift complex procurement workflows online, driving a 7.43% CAGR.

How are Spanish retailers reducing high fashion return rates?

They deploy size-recommendation algorithms, virtual try-ons, and membership models to lower fit-related returns that can reach 37.5%.

What logistics innovations are improving rural delivery?

Correos is expanding parcel lockers and testing electric vehicles, while drone pilots aim to cut the 30%-50% cost premium of rural last-mile service.

Page last updated on: