South Korea Die Casting Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

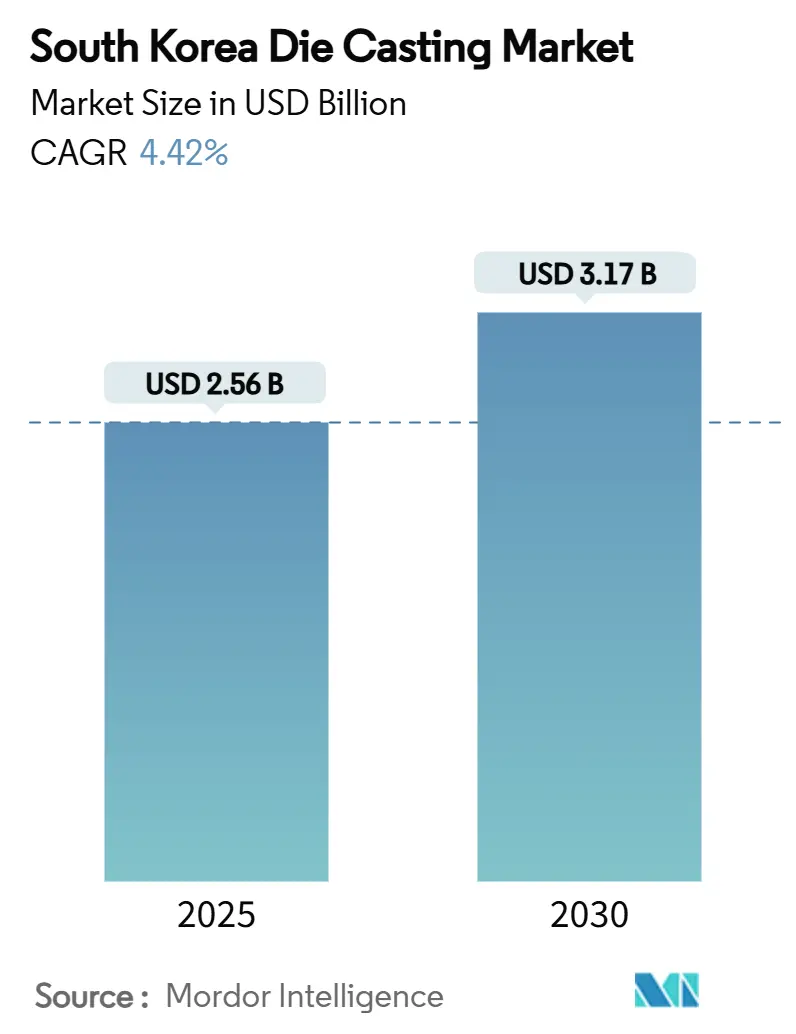

| Market Size (2025) | USD 2.56 Billion |

| Market Size (2030) | USD 3.17 Billion |

| Growth Rate (2025 - 2030) | 4.42% CAGR |

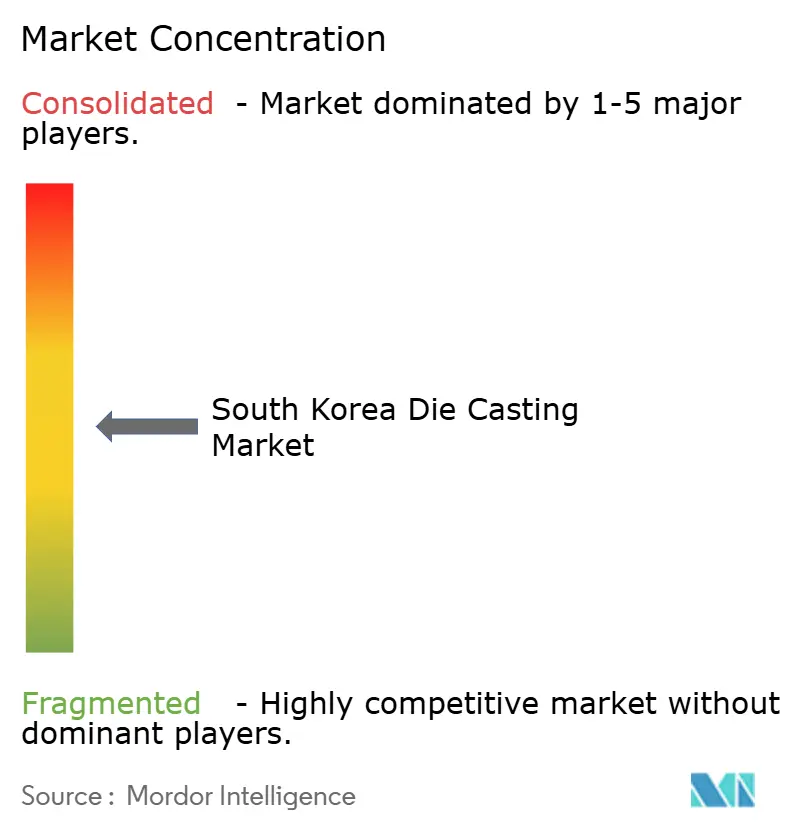

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Die Casting Market Analysis by Mordor Intelligence

The South Korea Die Casting Market size is estimated at USD 2.56 billion in 2025, and is expected to reach USD 3.17 billion by 2030, at a CAGR of 4.42% during the forecast period (2025-2030). This momentum reflects the country’s strategic push toward electric mobility, sustained investment in smart-factory upgrades, and the rapid scale-up of semiconductor fabrication capacity. Tier-one automakers are rolling out structural “hypercasting” programs, electronics majors are demanding tighter thermal tolerances, and government incentives offset upfront capital costs for new capacity. Together, these forces are broadening end-use diversity, elevating quality requirements, and opening white-space opportunities in hydrogen vehicle components and circular-economy feedstock streams, reinforcing long-term growth visibility for the South Korea die casting market.

Key Report Takeaways

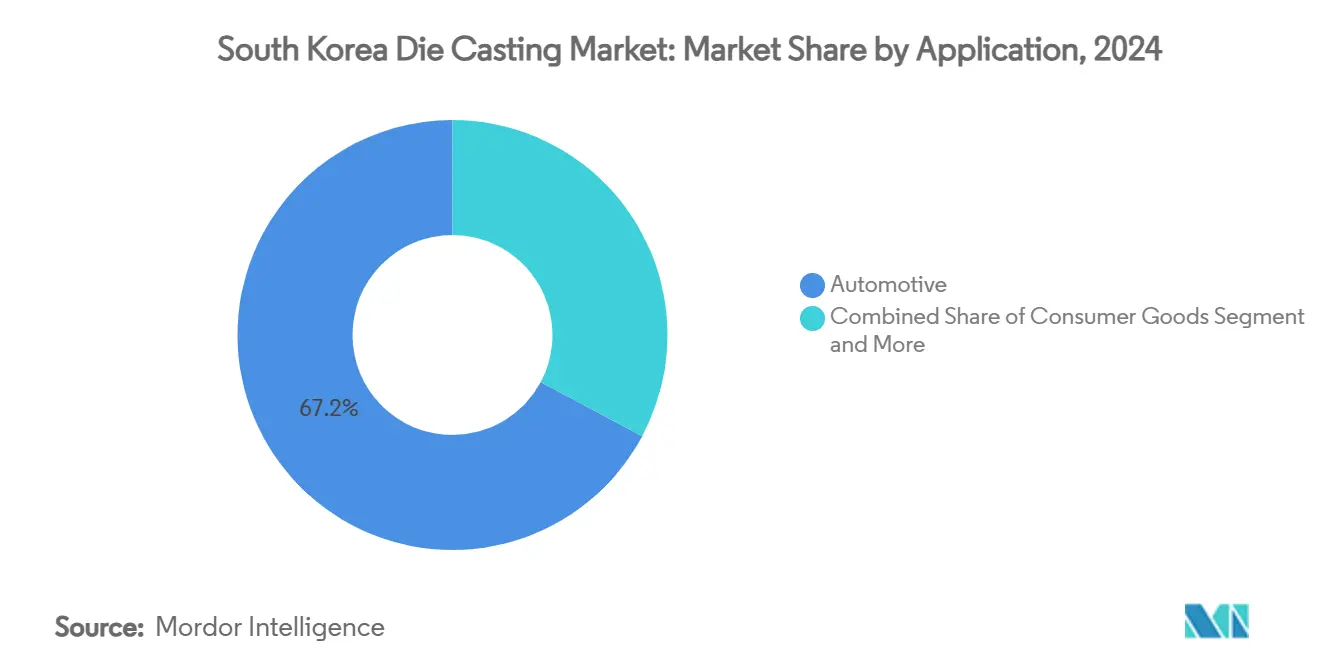

- By application, the automotive segment captured 67.17% of the South Korea die casting market share in 2024, and electronics & communication is projected to expand at the fastest 4.61% CAGR between 2025 and 2030.

- By process, high-pressure die casting held 52.28% revenue share in 2024, while vacuum die casting is set to record a 4.56% CAGR through 2030.

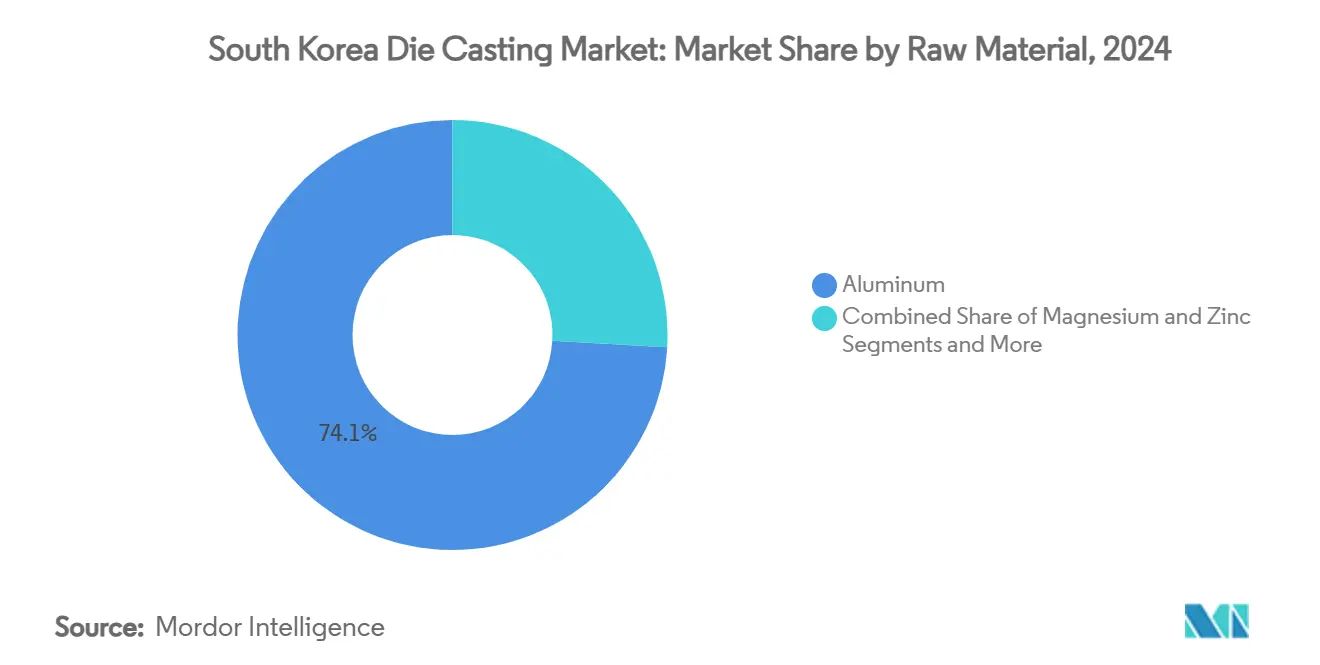

- By raw material, aluminum accounted for 74.14% of the South Korea die casting market size in 2024; magnesium is on track for the quickest 4.53% CAGR.

- By tonnage class, the 401-800 ton machinery class led with 35.13% share in 2024, whereas presses above 2,000 tons are forecast to post a 4.47% CAGR.

- By province, Gyeonggi-do province commanded 36.57% of 2024 revenues, and Gyeongsang Region is projected to rise at a 4.51% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with South korea representing one among them. The global report on die casting market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

South Korea Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Led Lightweighting | +1.1% | National, with concentration in Gyeonggi-do and Ulsan automotive hubs | Medium term (2-4 years) |

| Surge in Complex Electronic Housings | +0.8% | Gyeonggi-do semiconductor cluster, Seoul metropolitan area | Short term (≤ 2 years) |

| Design-Flexibility Demands | +0.7% | National automotive manufacturing regions | Medium term (2-4 years) |

| Government Smart-Foundry Subsidies | +0.5% | National, with priority zones in industrial complexes | Short term (≤ 2 years) |

| Hydrogen-Vehicle Component Build-out | +0.4% | Ulsan hydrogen industrial complex, Gyeonggi-do | Long term (≥ 4 years) |

| Circular-Economy Scrap-Utilisation Mandate | +0.4% | National, with focus on metal recycling hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-led Lightweighting Boom

Electric-vehicle adoption forces every automaker to trim mass to protect range, and integrated “gigacasting” now replaces dozens of stamped parts with a single structural node that cuts body-in-white weight by up to 40%. Hyundai plans to commission a domestic hypercasting line in 2026, while its suppliers line up multi-cavity tools capable of injecting 120 kg aluminum shots in one cycle. The charging network is set to quintuple the units by 2030, ensuring demand visibility for battery EV platforms that rely on large die-cast subframes. Early adopters have validated thirty-plus-minute takt times per gigacast, encouraging wider industry migration. Equipment orders above 2,000 tons have already risen, and local press makers are partnering with AI start-ups to stabilise melt flow, unlocking deeper penetration of the South Korean die casting market.

Surge in Complex Electronic Housings

The USD 471 billion semiconductor mega-cluster in Gyeonggi-do will house sixteen fabs producing 7.7 million wafers monthly by 2030. Fab equipment requires hermetic chambers, fluid manifolds, and heat spreaders machined to single-digit micron tolerances, tasks now migrating to vacuum die casting lines outfitted with melt-quality sensors. Samsung and SK Hynix demand 50% local sourcing of mechanical parts to derisk their supply chains, translating into multi-year blanket contracts for domestic foundries. AI accelerator chips deploy dense packaging that generates heat flux above 1,000 W/cm², compelling adopters to specify thin-wall aluminum housings with integrated vapor chambers. These technical stipulations elevate average selling prices and lengthen tooling lifecycles, adding profitable backlog for specialists in the South Korean die casting market.[1]“Fab Expansion Plan 2030,” Samsung Electronics, samsung.com

Design-Flexibility Demands in Auto Body Panels

Vehicle model lifecycles are shrinking to meet bespoke consumer preferences, so OEMs now seek body panels that can navigate late-stage engineering changes without re-cutting entire tool stacks. Die-cast structures allow quicker CAD-to-press transition because additive-manufactured cores incorporate conformal cooling paths that cut cycle times by 10% and permit intricate aesthetic cues. Hyundai and Kia plan thirty-one EV models on modular skateboard platforms by 2030, each leveraging common gigacast nodes with variant-specific styling ribs. Die casting lowers part counts, accelerates launch calendars, and reduces cost variance across trims, an attractive trifecta for OEM CFOs. Consequently, design-for-casting becomes mandatory coursework across Tier-one engineering teams.

Government Smart-Foundry Subsidies

Through the Manufacturing Industry Innovation 3.0 program, the Ministry of Trade, Industry, and Energy reimburses up to 75% of capital outlays for AI-enabled monitoring, robotic sprayers, and closed-loop melt furnaces. Tax holidays extend seven years for advanced casting lines, and interest-free loans backfill working-capital gaps for small and midsize foundries. Pilot plants in Busan report a decent amount of scrap reduction within six months of sensor retrofits. This public-private model hastens the diffusion of Industry 4.0 playbooks, locking in productivity gains that cushion wage inflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -0.70% | National, with supply chain dependencies on China and global markets | Short term (≤ 2 years) |

| Advanced-Skilled Labour Shortage | -0.50% | National, particularly acute in traditional manufacturing regions | Medium term (2-4 years) |

| Stringent Foundry-Emission Regulations | -0.40% | National, with stricter enforcement in metropolitan areas | Medium term (2-4 years) |

| Grid-Power Instability | -0.30% | National, affecting energy-intensive die casting operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

South Korea relies on imports for 95% of its raw minerals, mainly routed through Chinese brokers, making exchange-rate gyrations an additional pain point. Strategic reserves will expand from fifty-four to one hundred days, though those buffers soften rather than eliminate shocks. Zinc demand grew 26.1% locally in 2024 even as Chinese consumption fell, reflecting divergent industrial cycles and increasing premiums on the London Metal Exchange. Forward-buying strategies and alloy substitutions provide partial relief, yet small foundries with thin balance sheets remain exposed.

Advanced-Skilled Labour Shortage

Registrations for regional skills competitions in machine trades have dropped by half over ten years, and every second tool-room supervisor is above fifty-five years old. Younger graduates gravitate toward software and digital-content roles, leaving vacancies on CNC lines untouched for months. Shipyards report a 72% decline in engineering designers, signalling a broader drain that spills into die casting. While government programs aim to train 40,000 shop-floor specialists and 150,000 chip engineers by 2031, lead times to competency stretch beyond immediate production needs. In response, foundries accelerate robotics adoption, yet capital barriers restrict smaller operators, creating a bifurcated landscape of tech-enabled leaders and resource-strapped laggards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Automotive Dominance Drives Market

The automotive segment generated 67.17% of revenue in 2024, underscoring the importance of power-train housings, structural gigacasts, and steering components in the South Korean die casting market. EV penetration intensifies casting demand because battery packs multiply the need for thermal management plates and lightweight chassis nodes. While only a fifth of sales today, electronics and communication exhibit a 4.61% CAGR, benefiting from the semiconductor cluster’s ramp-up and a national 5G roll-out that requires heat-dissipating base-station housings. Consumer goods leverage aesthetic aluminium finishing capabilities, whereas packaging skews toward precision zinc parts for aerosol valves. Growth vectors differ, but all segments draw from a common tool-making ecosystem that spreads fixed costs and raises collective competitiveness.

Hyundai Mobis’s KRW 90 billion EV module complex in Ulsan will consume up to 20,000 tons of aluminium annually once fully operational in 2026, translating into steady batch orders for local die casters.[2]“Ulsan EV Module Plant Groundbreaking,” Hyundai Mobis, hyundaimobis.com Electronics assemblers specify tighter porosity ceilings to protect high-frequency signal integrity, a shift that propels vacuum casting equipment upgrades. Across consumer goods, demand for decorative finishes drives investment in duplex nickel-chrome plating lines attached to die casting cells, proving how downstream integration enhances margin. These diverse end-uses cushion cyclical swings as a portfolio, supporting sustained South Korea die casting market expansion.

By Process: High-Pressure Leadership with Vacuum Innovation

High-pressure technology captured a 52.28% share in 2024 because of its high throughput and established operator base. Its dominance in producing transmission housings and laptop frames ensures order visibility in the South Korean die casting market. Vacuum die casting, while only one-sixth of revenue, logs a 4.56% CAGR because OEMs impose stricter X-ray criteria on EV chassis gigacasts where porosity undermines crashworthiness. Low-pressure and gravity methods survive in decorative fixtures and aerospace hubs where thinner walls or premium alloys matter more than cycle time.

Additive manufacturing of conformal-cooled dies shrinks cycle times, enabling vacuum presses to match output formerly exclusive to high-pressure lines, thus widening adoption. Government smart-foundry subsidies reimburse up to 75% of sensor retrofits, lowering barriers for mid-tier firms to install vacuum systems. Meanwhile, squeeze casting gains niche traction for high-silicon magnesium alloys used in thermal-shock-resistant components. Process diversification, therefore, enhances resilience and collectively accelerates the South Korean die casting market.

By Raw Material: Aluminum Prevalence with Magnesium Momentum

Aluminum’s 74.14% share derives from an extensive recycling chain that slashes energy consumption to 3% of primary smelting levels, aligning with OEM Scope 3 decarbonisation targets. The South Korean die casting market size for aluminum components benefited from record scrap recovery, buoyed by the “Valuable Recycling” project that funds sensor-equipped collection bins. Magnesium blossoms at a 4.53% CAGR because each kilogram removed from an EV chassis extends range, reducing battery cost per kilometer. Zinc serves decorative and dimensional-accuracy products like camera housings, while copper-rich alloys solve electromagnetic shielding challenges in 5G modules.

Raw-material volatility forces hedging tactics, prompting OEMs to standardise alloy families across programs to secure economies of scale. Magnesium uptake faces flammability concerns, yet newly developed rare-earth infusions raise ignition temperatures above 600 °C, unlocking broader use avenues. Foundries are trialling rheo-casting to tame turbulence and reduce oxide film defects that plague magnesium. Such technical gains cement long-run substitution potential while aluminium retains baseline dominance.

By Tonnage Class: Mid-Range Strength with Heavy-Duty Expansion

Presses rated 401-800 tons delivered 35.13% of 2024 sales, striking an optimal balance between part envelope and capital outlay. They churn out medium-sized differential cases, smartphone mid-frames, and drone brackets. Machines above 2,000 tons, though still niche, post the fastest 4.47% CAGR. They enable gigacasting of single-piece rear underbodies weighing up to 100 kg, which is essential for EV structural simplification. Equipment below 400 tons continues to supply miniature lens mounts and medical devices, sustaining specialist job shops.

Heavy-duty expansion coincides with OEM moves to internalise chassis casting, creating captive demand for partnered suppliers to operate plants onsite. Press manufacturers embed real-time shot-curve analytics, cutting scrap by 5% and validating the ROI of high-tonnage systems despite their hefty price tags. Mid-tonnage units evolve into flexible cells with automatic die-change carts, allowing four model variants per shift. Such modularity complements mega-presses, giving the South Korean die casting market a balanced capacity pyramid.

Geography Analysis

Gyeonggi-do retained its leadership in 2024 with 36.57% of national revenue, sustained by Tier-one automotive plants and new-build fabs that anchor continuous order flows together. Government designation of the USD 471 billion semiconductor mega-cluster cements a decade-long pipeline for heat-sink plates, wafer handling arms, and vacuum pump bodies. Tax abatements and a pledge to train 150,000 chip engineers ensure the technical workforce matches tooling sophistication, reinforcing the South Korea die casting market.

Gyeongsang Region is charting a 4.51% CAGR to 2030. Shipyards diversify into offshore wind and hydrogen carriers, each requiring large aluminium tank brackets produced on presses above 2,000 tons. Ulsan’s hydrogen corridor secures early purchase agreements for fuel-cell truck fleets, translating into forecastable order books for lightweight stack casings.[3]“Hydrogen Economy Roadmap,” Ulsan Metropolitan City, ulsan.go.kr The regional government pairs smart-factory grants with rent reductions inside industrial parks to lure component suppliers, further bolstering local die casting capacity.

Chungcheong and Jeolla contribute complementary strengths. Chungcheong’s inland hubs leverage highway interchanges to deliver just-in-time lots to both coasts, while Jeolla’s new 550,000 m² complex near Geodu channels a massive amount toward AI-enabled machining centers, which in turn raise demand for precision cast housings. These developments distribute production risk, stimulate supplier diversity, and strengthen national supply resilience.

Competitive Landscape

The South Korean die casting market is moderately fragmented, with domestic specialists and multinational entrants splitting large OEM programs. The top five suppliers hold roughly around half of revenue, leaving room for niche players that excel in proprietary alloys, custom surface finishing, or rapid prototype delivery. Established firms deepen vertical integration, adding powder-bed fusion printers for mould inserts and in-house anodising lines to capture more value per kilogram.

Technology stewardship separates leaders from followers. Early adopters install vision-guided robots for trimming and deburring cells and connect melt furnaces to digital twins that forecast dross accumulation. Intellectual-property filings on conformal cooling geometries jumped 18% in 2024, revealing an arms race for cycle-time reduction. Some firms form joint ventures with global press builders to co-develop 3,500-ton “Giga” cells, aligning with OEM chassis strategies.

White-space opportunities include hydrogen-ready alloys, semiconductor clean-room housings, and recycled magnesium feedstock. Start-ups exploit this terrain by offering lot sizes under 1,000 pieces per month while guaranteeing sub-1% reject rates through full-part CT scanning. Consolidation is plausible once those innovators scale, yet current M&A volume remains low due to high valuation expectations and divergent niche focus.

South Korea Die Casting Industry Leaders

Seojin System Co., Ltd.

Samkee Corp.

Castec Korea Co., Ltd.

Dynacast International (Korea)

Ryobi Ltd. (Korea)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Hyundai Mobis allocated KRW 90 billion (USD 65 million) for an EV module plant in Ulsan, which is due online in late 2025. This will boost regional demand for structural die-cast parts.

- January 2024: The Ministry of Trade, Industry, and Energy confirmed a KRW 622 trillion (USD 471 billion) semiconductor mega-cluster in Gyeonggi-do alongside Samsung Electronics and SK Hynix, unlocking capacity for 7.7 million wafers per month by 2030 and large volumes of precision die-cast equipment components.

South Korea Die Casting Market Report Scope

| Automotive |

| Electronics & Communication |

| Consumer Goods |

| Packaging & Others |

| High-Pressure Die Casting |

| Low-Pressure Die Casting |

| Vacuum Die Casting |

| Squeeze Die Casting |

| Gravity & Others |

| Aluminum |

| Magnesium |

| Zinc |

| Others |

| Up to 400 Ton |

| 401-800 Ton |

| 801-2,000 Ton |

| Above 2,000 Ton |

| Gyeonggi-do |

| Chungcheong Region |

| Gyeongsang Region |

| Jeolla & Others |

| By Application | Automotive |

| Electronics & Communication | |

| Consumer Goods | |

| Packaging & Others | |

| By Process | High-Pressure Die Casting |

| Low-Pressure Die Casting | |

| Vacuum Die Casting | |

| Squeeze Die Casting | |

| Gravity & Others | |

| By Raw Material | Aluminum |

| Magnesium | |

| Zinc | |

| Others | |

| By Tonnage Class | Up to 400 Ton |

| 401-800 Ton | |

| 801-2,000 Ton | |

| Above 2,000 Ton | |

| By Province | Gyeonggi-do |

| Chungcheong Region | |

| Gyeongsang Region | |

| Jeolla & Others |

Key Questions Answered in the Report

How large is the South Korean die casting market in 2025?

The South Korean die casting market size is USD 2.56 billion in 2025 and is projected to reach USD 3.17 billion by 2030.

What is the expected growth rate for die casting in South Korea?

The market is forecast to expand at a 4.42% CAGR from 2025 to 2030.

Which application segment contributes the most revenue?

Automotive accounts for 67.17% of 2024 revenue due to strong domestic vehicle production and rising EV gigacasting orders.

Which province is growing the fastest in die casting activity?

Gyeongsang Region leads provincial growth with a 4.51% CAGR through 2030, supported by hydrogen-vehicle and shipbuilding diversification.

What material is gaining share most rapidly?

Magnesium is the fastest-growing raw material, advancing at a 4.53% CAGR as EV lightweighting intensifies.

How fragmented is the competitive landscape?

The top five vendors command roughly around half of sales, signalling moderate fragmentation and leaving room for niche specialists.

Page last updated on: