Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

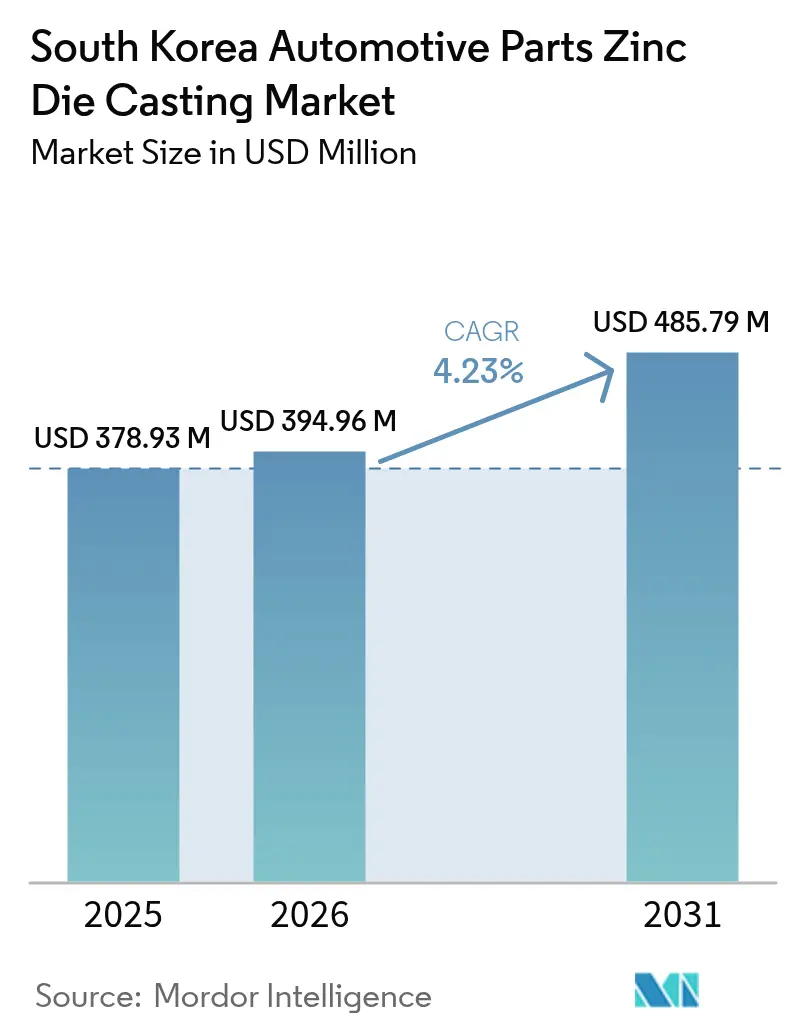

| Base Year Market Size (2025) | USD 378.93 Million |

| Market Size (2026) | USD 394.96 Million |

| Market Size (2031) | USD 485.79 Million |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

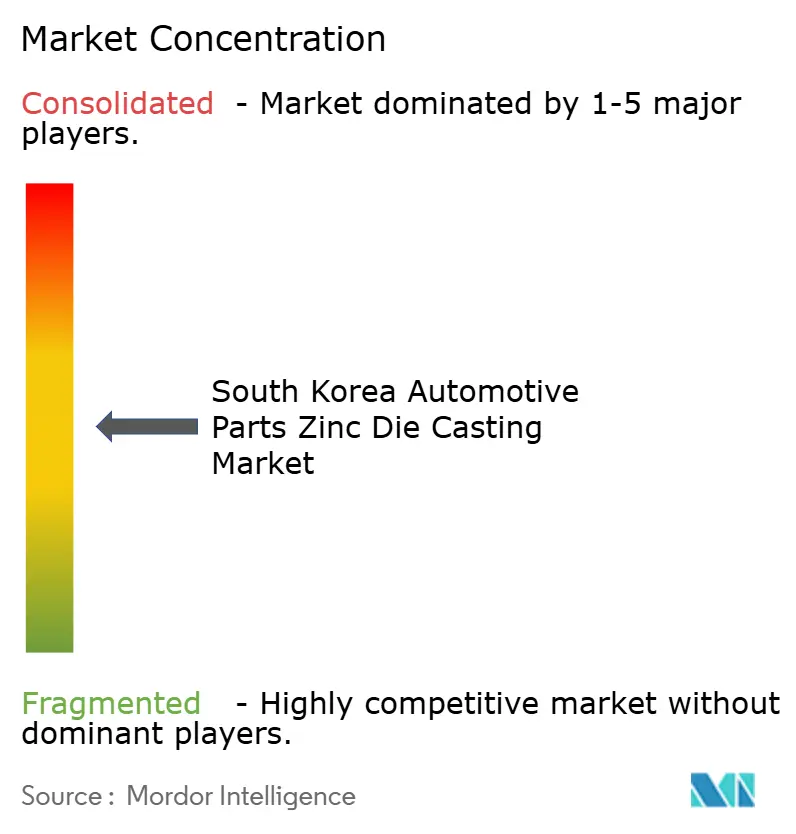

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Automotive Parts Zinc Die Casting Market Analysis by Mordor Intelligence

South Korea Automotive Parts Zinc Die Casting Market size in 2026 is estimated at USD 394.96 million, growing from 2025 value of USD 378.93 million with 2031 projections showing USD 485.79 million, growing at 4.23% CAGR over 2026-2031. The market size momentum rests on the rebound of domestic vehicle assembly volumes, steady electrification targets, and ongoing OEM localization programs. Recovery funding for automotive manufacturers, announced in 2024, underpins new capacity additions and keeps order books healthy despite lingering tariff uncertainties. Simultaneously, lightweighting mandates and the migration to higher‐value thermal-management components are shifting alloy choices toward higher-strength formulations. Process-level upgrades, especially smart-factory retrofits in Ulsan, Changwon, and Gyeonggi, are improving yield and mitigating energy-cost headwinds. Competitive intensity remains moderate, with mid-sized die casters adopting real-time process analytics to secure long-term supply agreements with Hyundai Motor Group and other global OEMs.

Key Report Takeaways

- By production process type, pressure die casting led with 66.42% of the South Korea automotive parts zinc die casting market share in 2025, while semi-solid die casting is projected to advance at a 4.27% CAGR to 2031.

- By alloy type, zamak 3 accounted for 41.78% of the South Korea automotive parts zinc die casting market share in 2025, whereas ZA alloys record the highest forecast CAGR at 4.36% through 2031.

- By application, body assemblies captured 35.92% of the South Korea automotive parts zinc die casting market share in 2025; electrical & electronics housings post the strongest growth outlook at a 4.31% CAGR.

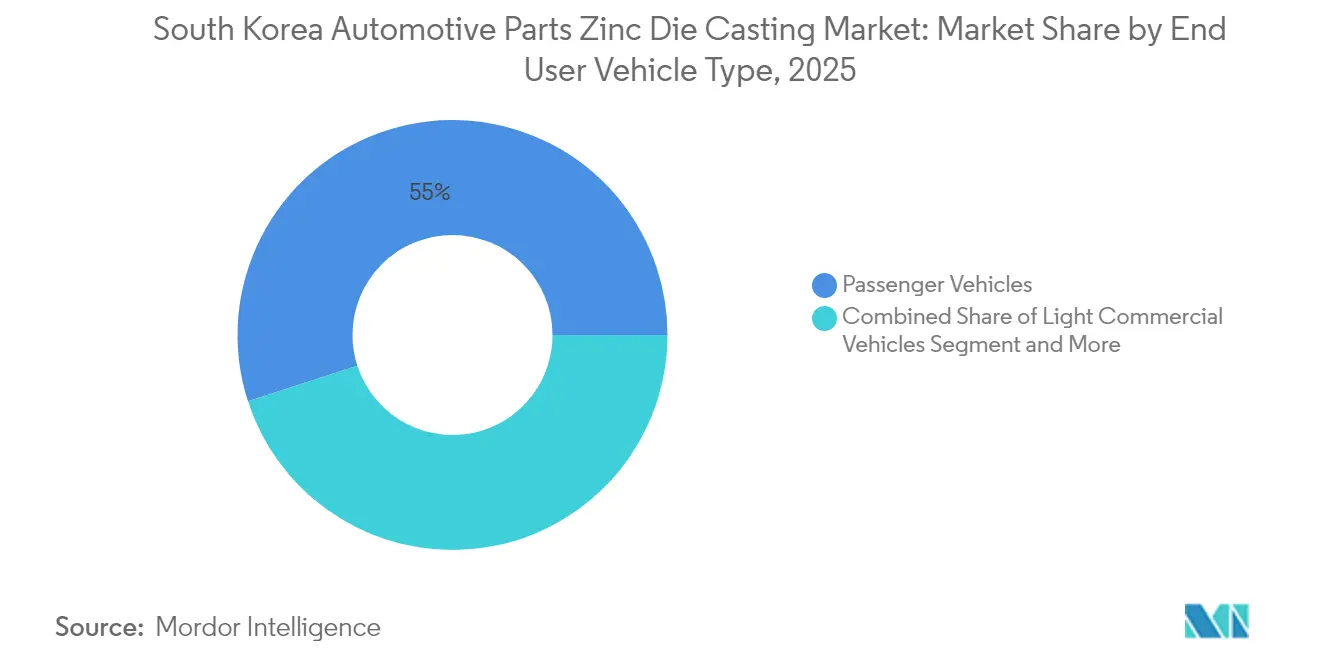

- By end-user vehicle type, passenger vehicles represented 54.98% of the South Korea automotive parts zinc die casting market share in 2025 and are expanding at a 4.29% CAGR to 2031.

- By sales channel, the OEM channel controlled 82.61% of the South Korea automotive parts zinc die casting market share in 2025 and is set to rise at a 4.27% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Automotive Parts Zinc Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery In Domestic Automotive Production Volumes | +1.2% | National, concentrated in Ulsan and Changwon industrial complexes | Short term (≤ 2 years) |

| Rapid EV Adoption | +1.0% | National, with concentration in EV manufacturing hubs | Long term (≥ 4 years) |

| Weight-Reduction Targets | +0.8% | National, with spillover to export markets | Medium term (2-4 years) |

| OEM Localization Push | +0.7% | National, with focus on reducing import dependency | Medium term (2-4 years) |

| Government Incentives | +0.6% | National, focused on industrial complexes in Gyeonggi and South Gyeongsang | Medium term (2-4 years) |

| Korea Zinc Supply-Chain Realignment | +0.4% | National supply chain optimization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recovery In Domestic Automotive Production Volumes Post-2024

Annual vehicle assembly at Hyundai’s Ulsan complex has returned to pre-pandemic rhythm, and a KRW 2 trillion EV-dedicated expansion scheduled for 2025 reinforces part procurement visibility[1]“Ulsan Plant Expansion Update,” Hyundai Motor Company, hyundai.com . More than 300 tier-1 and tier-2 suppliers clustered in the region have restored three-shift operations, raising order flow for precision zinc castings used in door hinges, wiper systems, and seat frames. The national export surge creates additional pull for export-oriented die casters servicing mixed-model platforms. Volumetric rebound helps amortize tooling investments and offsets energy-cost escalation, keeping margins intact for high-volume parts. Suppliers now co-engineer castings at the design stage, shortening time-to-market for model-year 2026 launches.

Rapid EV Adoption Creating New Thermal-Management Parts

The pivot to battery-electric vehicles multiplies zinc casting demand for power-electronics housings, battery-pack frames, and integrated coolant manifolds. Hyundai WIA’s commercial roll-out of a one-piece EV thermal-management module in 2023 validated zinc’s superior thermal conductivity for compact under-hood packaging[2]“Integrated Thermal Management Module,” Hyundai WIA, en.hyundai-wia.com . Unlike combustion-engine radiators, EV modules regulate three heat zones—battery, inverter, and e-motor—necessitating intricate internal flow paths best formed through high-pressure zinc casting. Domestic suppliers exporting to U.S. and European EV brands gain from Korea’s robust EMC testing infrastructure, positioning zinc die casting as a premium solution for thermal and electromagnetic compliance. As EV volumes climb toward the 4.2 million-unit national target by 2030, order frequency for these complex parts is expected to scale faster than overall vehicle builds.

Weight-Reduction Targets Driving Thinner-Wall Zinc Castings

Regulatory push for carbon-neutral fleets drives OEMs to shave every unnecessary gram. Process controls now maintain wall thickness near 1.5 mm while retaining dimensional stability, delivering up to around one-fifth component weight savings versus 2022 designs. Advanced ZA alloys, containing up to 8% aluminum, elevate tensile strength to offset the thinner cross-sections. Investment in conformal-cooling die inserts improves solidification rates and reduces porosity, giving Korean suppliers a reputation for zero-rework batches. Lightweight compliance premiums negotiated with export OEMs add a new revenue layer for mid-sized casters.

Government Incentives For Smart-Factory Upgrades

The Ministry of SMEs and Startups subsidized digital retrofits for 950 companies in 2025, funding sensors, MES integration, and AI-based scrap monitoring. Die casting shops using inline thermal cameras report one-tenth scrap reduction and miminum cycle-time gains. The Banwol-Sihwa Smart Green Complex offers shared logistics ERP and green-transport links, further squeezing overhead costs. Smart-factory accreditation also serves as a qualification badge in global RFQs, enhancing export competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy and Processing Costs | -0.9% | National, particularly affecting energy-intensive operations | Short term (≤ 2 years) |

| Zinc-Price Volatility | -0.6% | Global supply chain with national impact | Medium term (2-4 years) |

| Shortage Of Experienced Tool-And-Die Designers | -0.5% | National, concentrated in industrial regions | Long term (≥ 4 years) |

| Urban Environmental Permitting Hurdles | -0.3% | Urban industrial areas, particularly Seoul metropolitan region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy & Processing Costs vs. Aluminum

Industrial electricity tariffs climbed more than three-fifth between 2022 and 2024, hitting energy-intensive hot-chamber lines especially hard. Although zinc melts at lower temperatures than aluminum, the continuous hold temperature and frequent reheats boost net kWh per kilogram. Some mid-tier foundries are experimenting with induction furnaces powered by PV-backed microgrids, but capital outlays remain daunting. Immediate pressure is visible in thinner operating margins for small contract casters, prompting consolidation.

Zinc-Price Volatility From Global Supply Disruptions

Benchmark zinc hovered near USD 2,600 per ton in 2024 with day-to-day swings touching USD 500, upsetting contract costings. Korea’s reliance on imported concentrates exposes buyers to shipping route disruptions in the Red Sea and South China Sea. Korea Zinc’s equity in The Metals Company aims to diversify nickel and cobalt supply, yet near-term zinc spot stability is still elusive. Hedge programs and strategic stockpiles cushion short shocks but raise working-capital commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process Type: Semi-Solid Casting Gains Momentum

Pressure die casting holds 66.42% of the South Korea automotive parts zinc die casting market share in 2025. Whereas, semi-solid casting is anticipated to post a 4.27% CAGR, The emerging technique combines thixotropic slurry control and high fill rates, producing structural parts with fewer voids and superior fatigue resistance. Automakers allocating budgets to battery-tray reinforcement panels prefer semi-solid due to tighter dimensional tolerances. Pressure die casting keeps scale economies intact for door handles and window regulators, maintaining high OEE on legacy lines. Continuous shot monitoring and servo-driven plungers are pushing CTQ yields beyond 97%. South Korea automotive parts zinc die casting market participants blend both technologies to balance volume economics with premium applications.

Despite its high share, pressure die casting is under process-optimization pressure to stay cost-competitive. Investments in vacuum venting and dual-plunger gates lift mechanical properties closer to semi-solid outputs, blurring traditional boundaries. OEM engineers now specify micro-porosity levels measured via computed tomography, nudging casters toward hybrid tooling solutions. Overseas customers visiting Changwon facilities often contract parallel pilot runs in both technologies before line-side deployment, elongating quoting cycles but locking in multi-year volumes once qualified.

By Alloy Type: ZA Alloys Challenge Traditional Formulations

Zamak 3 alloys, though representing 41.78% of the South Korea automotive parts zinc die casting market share in 2025, are primarily used in door-lock housings, hood latches, and interior bezels. Zamak 5, with its copper booster, is used for styling parts requiring elevated corrosion resistance. ZA alloys are forecast to clock a 4.36% CAGR, the fastest among alloy categories. Their aluminum content above one-tenth provides tensile strengths exceeding 400 MPa, allowing thinner cross-sections without creep. Suppliers report machining-time savings of up to 18% due to improved chip breakage, offsetting marginal raw-metal price premiums.

Material spec shifts often follow joint cost-down workshops held by Hyundai Mobis and tier-1 die casters. Lifecycle simulations now factor vibration frequency spectra unique to battery-electric platforms, driving migration to ZA alloy variants. As OEMs commit to global recycling targets, the superior recyclability of traditional Zamak blends ensures baseline volumes, securing foundry capacity utilization. South Korea automotive parts zinc die casting market size growth therefore reflects parallel demand vectors across traditional and advanced alloys.

By Application: Electronics Housings Drive Innovation

Body assemblies, holding 35.92% share of South Korea automotive parts zinc die casting market size in 2025, remain vital because seat frames, roof-rail brackets, and crash-energy absorbers still rely on zinc’s damping properties. Interior trim brackets benefit from zinc’s decorative plating compatibility, sustaining niche demand. Electrical & electronics housings are projected to grow at 4.31% CAGR, overtaking engine-centric parts that lose share in an electrified fleet. Die casters are shipping shielded inverter boxes with integrated busbar channels, minimizing assembly steps on EV lines.

Engine and transmission parts maintain relevance in hybrid vehicles shipped to export markets with slower electrification trajectories. Casters re-tool legacy molds with conformal cooling inserts, squeezing faster cooling cycles, offsetting volume declines. As in-car compute power escalates, EMC compliance drives fresh usage of zinc housings with integrated gasket grooves. Suppliers winning this new business often provide concurrent engineering to align mounting bosses with OEM PCB stack-ups.

By End-User Vehicle Type: Passenger Vehicles Lead Across Metrics

Passenger vehicles commanded 54.98% of South Korea automotive parts zinc die casting market size in 2025 and will expand at a 4.29% CAGR. Model proliferation, particularly in compact EV crossovers, inflates component count per unit. Heavy commercial vehicles have limited penetration for zinc due to extreme duty cycles favoring steel or ductile iron; however, cabin trim and step brackets still use zinc for corrosion protection. Light commercial vehicles maintain steady demand driven by e-grocery delivery fleets in Seoul and Busan. Two-wheelers represent an emerging export niche to Southeast Asia; compact ABS housings and handlebar clamps are frequently sourced from Korean die casters.

Growth in passenger vehicles benefits from Korea’s free-trade pacts that ease outbound shipments to the EU and Canada. Local content rules inside those pacts favor Korean castings, augmenting export volumes. Platform modularity allows a single zinc bracket family to fit three vehicle models, driving economies of scale that smaller regional competitors struggle to match.

By Sales Channel: OEM Dominance Reflects Integration Trends

OEM contracts represented 82.61% of 2025 revenue, underscoring the collaborative design culture between Korean die casters and automakers and also growing at a CAGR of 4.27% through 2031. Integrated APQP processes mean casting suppliers attend early design reviews, embedding manufacturability insights before tooling kick-off. Aftermarket channels, supplying collision repair centers and performance tuners, grow at muted rates due to improved vehicle durability. Nevertheless, specialty tuners ordering small-batch dress-up components keep a subset of job-shop casters viable. South Korea automotive parts zinc die casting market players seek diversified OEM bases, supplying both Hyundai Motor Group and overseas OEMs such as Renault Korea and GM Korea to balance platform risk.

OEMs tightening PPAP standards compel suppliers to implement automated X-ray and CT scanning. Compliance costs are offset by longer contract tenures and dual-source avoidance. Casters that achieve zero-PPM status often negotiate price escalators indexed to metal surcharges, preserving margins in volatile zinc markets.

Geography Analysis

Production clusters concentrate along the southeast corridor from Ulsan to Changwon, accounting for more than half of national zinc casting output. Ulsan hosts Hyundai’s unit assembly plant and multiple dedicated die casting cells supplying door-handle frames and battery-tray fittings. Upgraded logistics channels through the Port of Ulsan anchor export flows to North America and the EU. Changwon’s industrial complex, established in 1974, integrates upstream machining and post-processing shops, enabling just-in-sequence deliveries to heavy-industry OEMs and vehicle assemblers in nearby Geoje shipyards. The site’s Advanced Transportation Machinery Parts Zone reserves 692,000 m² for automotive casting expansion, with recent tenants adopting low-carbon melting furnaces funded by provincial eco-credit programs.

Gyeonggi’s Banwol-Sihwa Smart Green Industrial Complex provides digital twins and shared ERP for SMEs, trimming lead times for prototype tooling orders by up to one-fifth. Proximity to Seoul’s R&D institutes fosters collaborative alloy development, accelerating migration to ZA variants. Peripheral zones like Wonju’s Foreign Investment Zone in Gangwon-do offer tax holidays and subsidized land to attract global tier-1 suppliers, distributing economic activity beyond legacy hubs.

South Gyeongsang’s incentive package secured expansions from Wurth Korea and other international tool makers, bolstering local die design capabilities. This multi-hub geography mitigates supply disruptions while nurturing specialized talent pools in each region.

Competitive Landscape

Market concentration remains moderate: the top five companies collectively hold an estimated more than half of South Korea automotive parts zinc die casting market share. Hyundai WIA leads thermal-management castings and leverages vertical integration with Hyundai Motor Group. Dynacast Korea focuses on precision micro-components, supplying global EV inverter makers. Ryobi Die Casting Korea adapts proprietary vacuum gate technology imported from Japan to secure drivetrain brackets destined for Europe. Ahresty Korea emphasizes structural parts and collaborates with OEMs on crush-zone optimization projects. Smaller firms such as Seohan Auto and Sungwoo Hitech invest in robotic trimming and cell automation to climb the value ladder.

The technology race centers on smart-factory maturity, with leading firms deploying AI-enabled melt-temperature prediction and predictive die lubrication. Intellectual property protection in die design grows in importance as alloys diversify.

M&A activity is picking up: a domestic private-equity consortium acquired almost two-fifths stake in JYC Foundry in early 2025 to finance ZA alloy line upgrades. Compliance with K-REACH chemical norms and carbon-footprint disclosure is fast becoming a bid qualifier for export programs, pushing laggard firms toward partnerships or exit.

South Korea Automotive Parts Zinc Die Casting Industry Leaders

Ashok Minda Group

Brillcast Manufacturing LLC

Dynacast

Pace Industries

Sandhar Technologies Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Korea Zinc invested USD 85.2 million in The Metals Company to secure critical minerals for EV supply chains, reducing reliance on Chinese imports.

- May 2024: Hyundai Mobis committed KRW 90 billion to an EV module plant in Ulsan set for completion in late 2025, focusing on chassis and driver’s-seat modules.

- May 2024: SeAH Group allocated USD 155.3 million for the first Korean special-alloy plant in the United States to serve aerospace and defense clients.

South Korea Automotive Parts Zinc Die Casting Market Report Scope

Die casting is the process of pouring molten metal into a mold cavity under high pressure to produce a part in a specific shape. Zinc metal is easy to cast as compared to aluminum and magnesium metal. Zinc die casting offers a high level of production efficiency, superior quality, and cost-effectiveness. Zinc die casting is used to manufacture vehicle products such as seat belts, windshield wipers, sunroofs, and chassis.

The study on the South Korean automotive parts zinc die-casting market offers the latest trends and technological developments, as well as the demand by production process type and application type.

Based on the production process type, the market is segmented into pressure die casting, vacuum die casting, and other production process types. Based on the application type, the market is segmented into body assemblies, engine parts, transmission parts, and other application types. For each segment, the market sizing and forecasts will be provided based on value (USD).

By Production Process Type

| Pressure Die Casting |

| Vacuum Die Casting |

| Squeeze Die Casting |

| Semi-Solid Die Casting |

By Alloy Type

| Zamak 3 |

| Zamak 5 |

| ZA Alloys |

| Others |

By Application

| Body Assemblies |

| Engine Parts |

| Transmission Parts |

| Electrical & Electronics Housings |

| Interior & Trim Components |

By End-User Vehicle Type

| Passenger Vehicles |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

By Sales Channel

| OEM |

| Aftermarket |

| By Production Process Type | Pressure Die Casting |

| Vacuum Die Casting | |

| Squeeze Die Casting | |

| Semi-Solid Die Casting | |

| By Alloy Type | Zamak 3 |

| Zamak 5 | |

| ZA Alloys | |

| Others | |

| By Application | Body Assemblies |

| Engine Parts | |

| Transmission Parts | |

| Electrical & Electronics Housings | |

| Interior & Trim Components | |

| By End-User Vehicle Type | Passenger Vehicles |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Two-Wheelers | |

| By Sales Channel | OEM |

| Aftermarket |

Key Questions Answered in the Report

What is the current value of the South Korea automotive parts zinc die casting market?

The market is valued at USD 394.96 million in 2026, reflecting post-pandemic production recovery.

How fast is the South Korea automotive parts zinc die casting market expected to grow?

It is projected to expand at a 4.23% CAGR, reaching USD 485.79 million by 2031.

Which alloy category is growing the quickest in South Korean zinc casting?

ZA alloys show the fastest growth at a 4.36% CAGR because of superior strength and lightweight potential.

Why are electronics housings a high-growth application?

Electrification elevates demand for zinc castings that provide electromagnetic shielding and thermal management for EV power electronics.

How significant is OEM sourcing compared with aftermarket channels?

OEM contracts represent 82.61% of 2025 revenue, underscoring integrated design partnerships with major automakers.

What is the biggest operational challenge facing die casters today?

Escalating industrial electricity prices, up more than three-fifth since 2022, put pressure on hot-chamber processing economics.

Page last updated on: