Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

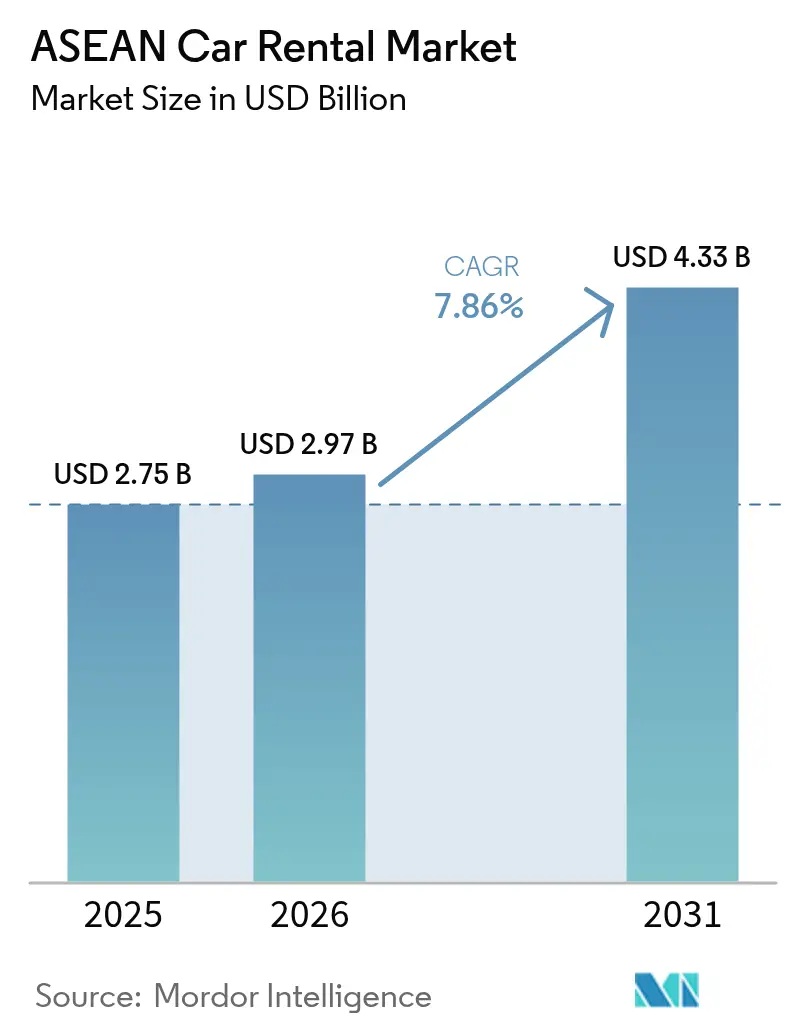

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.97 Billion |

| Market Size (2031) | USD 4.33 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

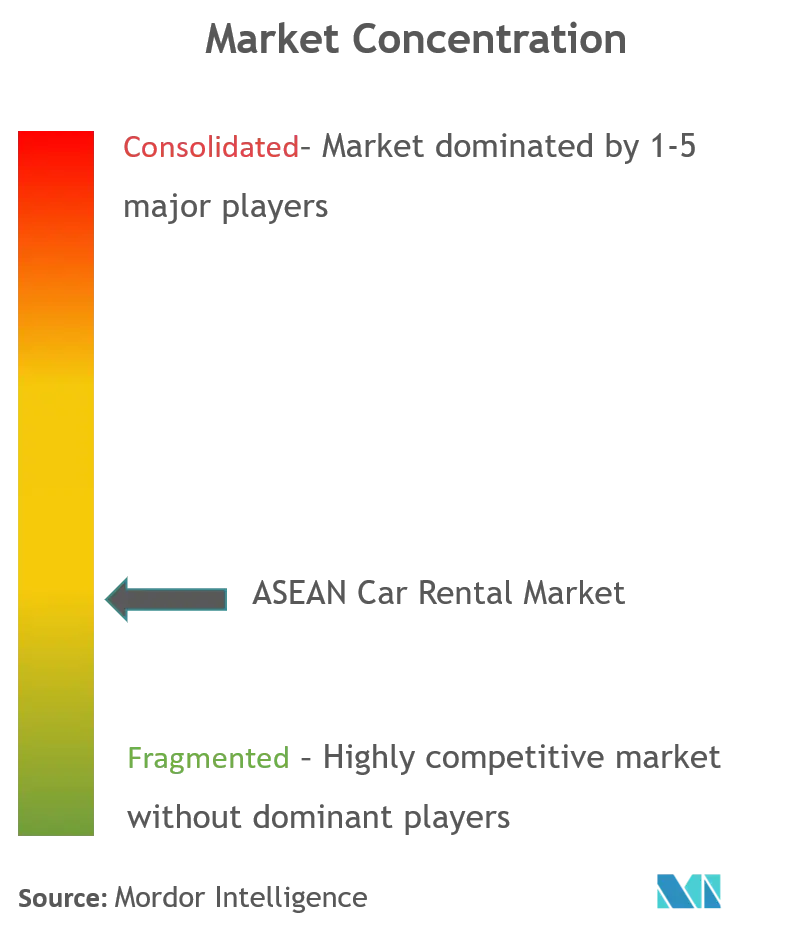

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Car Rental Market Analysis by Mordor Intelligence

The ASEAN Car Rental Market size in 2026 is estimated at USD 2.97 billion, growing from 2025 value of USD 2.75 billion with 2031 projections showing USD 4.33 billion, growing at 7.86% CAGR over 2026-2031. Tourism rebound, the rapid shift to digital booking channels, and steady corporate mobility demand are the primary growth engines. Fleet operators benefit from pricing power as tourist arrivals scale faster than vehicle additions, while super-apps convert ride-hailing audiences into rental users through one-click upselling. Businesses across Southeast Asian urban hubs increasingly substitute fleet ownership with service contracts, steering stable long-term revenue to providers.

Key Report Takeaways

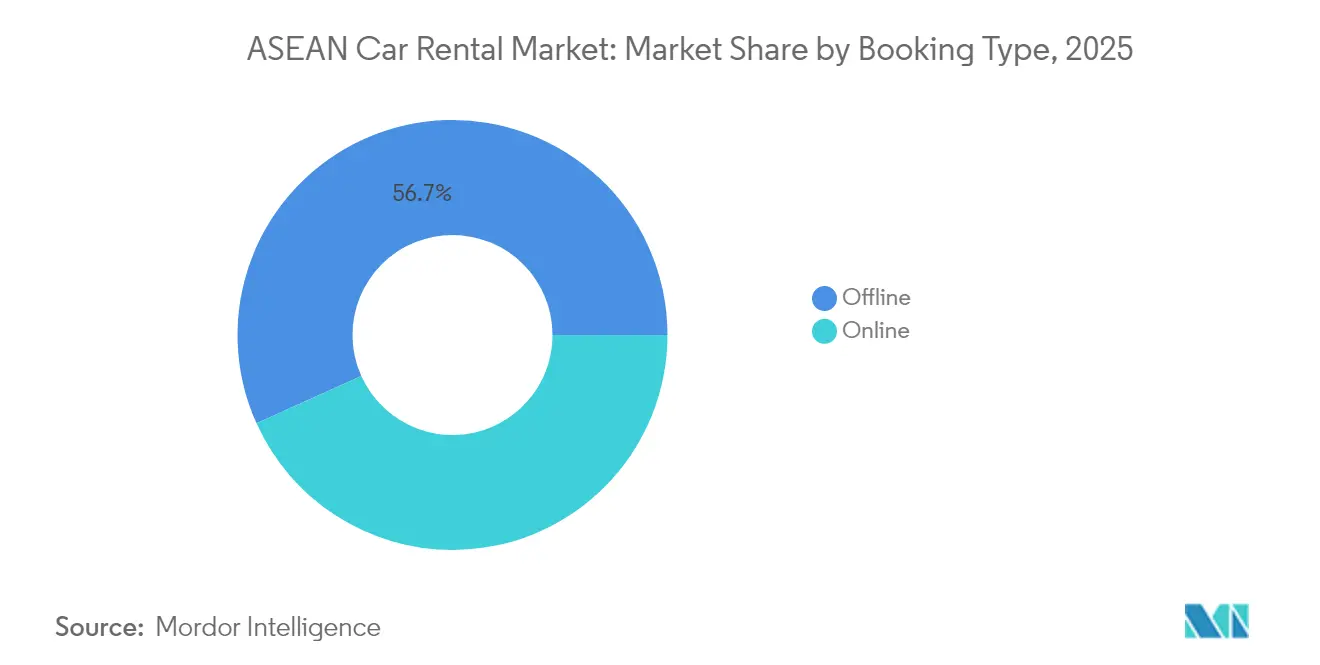

- By booking type, offline channels still held 56.74% revenue share in 2025, but online channels are growing at 8.31% CAGR to 2031.

- By rental duration, short-term contracts accounted for 80.62% of the ASEAN car rental market size in 2025, while subscription models are climbing at 7.75% CAGR.

- By service type, self-drive captured 65.89% revenue share in 2025; peer-to-peer car-sharing is the fastest-growing at 8.29% CAGR.

- By vehicle type, economy and mini cars commanded 33.74% of the ASEAN car rental market size in 2025; SUVs are charting the highest 8.37% CAGR.

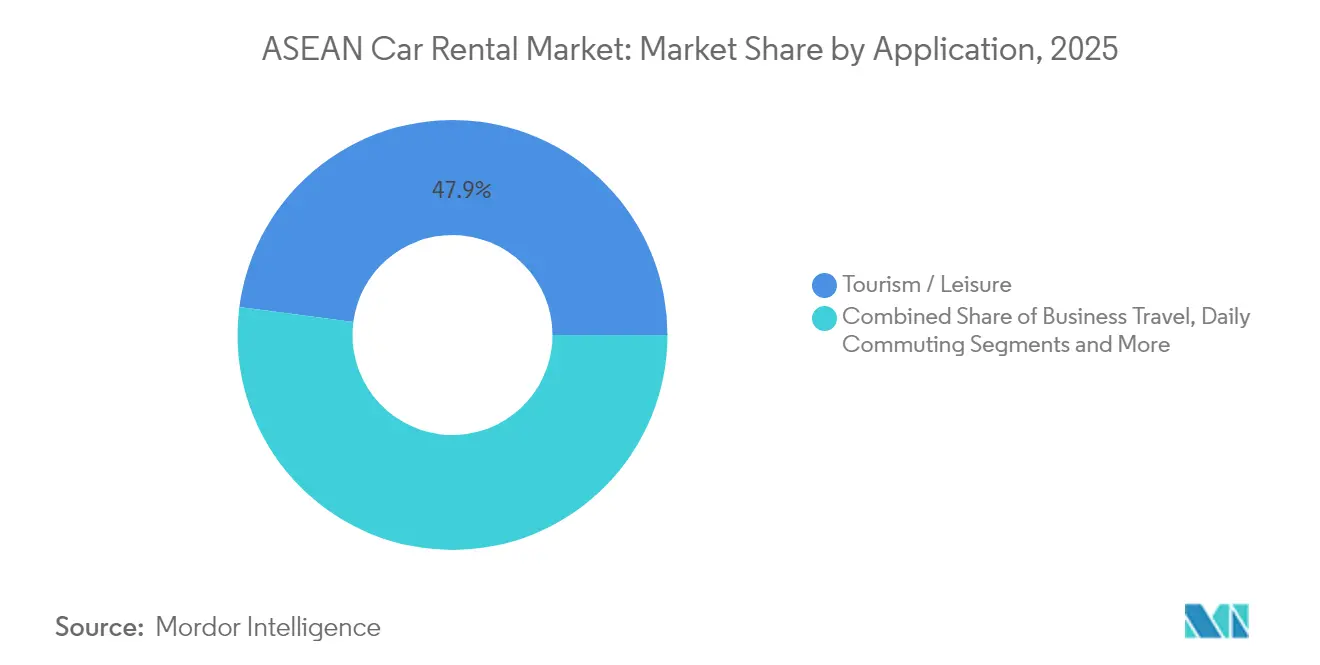

- By application, tourism and leisure held 47.92% share of the ASEAN car rental market size in 2025, whereas ride-hail driver rentals register an 8.05% CAGR.

- By end-customer, individuals formed 54.58% share in 2025; corporates and SMEs are pacing ahead at 8.73% CAGR to 2031.

- By country, Indonesia led with 25.31% of ASEAN car rental market share in 2025; Vietnam is projected to expand at a 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound | +2.1% | Indonesia, Thailand, Malaysia, Singapore | Medium term (2-4 years) |

| Surge in OTA Bookings | +1.8% | Global ASEAN, strongest in Singapore, Malaysia | Short term (≤ 2 years) |

| Corporate Demand for Mobility-as-a-Service | +1.5% | Singapore, Malaysia, Thailand urban centers | Medium term (2-4 years) |

| EV-Ready Government Incentives | +1.2% | Indonesia, Thailand, Singapore | Long term (≥ 4 years) |

| P2P Platforms Unlock Idle Supply | +0.9% | Singapore, Malaysia, urban Vietnam | Short term (≤ 2 years) |

| Harmonising ASEAN Digital Trade | +0.6% | Regional cross-border operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound Out-Paces Fleet Growth

International arrivals surpassed 100 million in 2023, equal to 70% of pre-pandemic flows, yet rental fleets grew at a markedly slower pace.[1]“Tourism Statistics 2024,” ASEAN Secretariat, asean.org Utilization now exceeds 85% at peak seasons, compared with 65% before the pandemic, allowing operators to implement dynamic pricing and redeploy vehicles across borders for yield optimization. Thailand’s new rail and road corridors connecting secondary cities magnify the strain on limited fleets, particularly in Laos-bound tourist circuits. Established providers with existing inventory therefore enjoy higher margins and faster payback on new vehicles. Investors channel capital toward fleet expansion, but lengthy order backlogs for new cars, especially EVs, curtail immediate supply relief.

Surge in OTA / Super-App Bookings

Heavy smartphone penetration and a payment-ready digital economy propel online reservation volumes. Grab, Traveloka, and Agoda embed rental offers next to flights and hotels, raising conversion by bundling discounts and loyalty points. For operators, platform distribution trims branch overheads and supports real-time revenue management. Corporate self-booking portals further widen digital adoption as finance teams demand integrated expense workflows. The share of web- and app-based reservations in the ASEAN car rental market climbed to 42.7% in 2024 and is on course to overtake offline transactions before 2028.Enhanced data visibility empowers insurers to price usage-based products, improving coverage availability for short-term renters.

Corporate Demand for Mobility-as-a-Service Contracts

Businesses streamline capital allocation by shifting from owned fleets to monthly mobility subscriptions that bundle insurance, maintenance, and telematics dashboards. Singapore’s professional‐services firms were early adopters, but SMEs across Bangkok, Kuala Lumpur, and Ho Chi Minh City are now driving the 9.16% CAGR corporate segment. Operators dispatch dedicated account managers and analytics to optimize fleet mix by trip profile, ensuring higher vehicle rotation and longer asset life. Subscription revenue also cushions providers against seasonal tourism swings. Marubeni’s PrimeMobility alliance with local Thai dealerships illustrates how diversified conglomerates are entering service-led models to capture downstream value.

EV-Ready Government Incentives

Indonesia and Thailand subsidize battery-electric vehicle purchases, waive import duties, and build charging corridors that cut operator payback periods. Blue Bird, the region’s largest taxi group, will field 1,000 EVs by end-2025, lowering fuel and maintenance outlays while marketing a green brand proposition[2]“Blue Bird Accelerates EV Fleet Expansion,” Blue Bird Group, bluebirdgroup.com. Rental firms collaborate with utilities to install depot fast-chargers, and fleet-size commitments earn bulk discounts from Chinese OEMs keen on Southeast Asian footholds. In parallel, regulators pilot zero-emission zones in Jakarta and Bangkok that could eventually restrict combustion rental fleets, nudging demand toward electric offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented licensing | -1.4% | Cross-border operations, rural areas | Medium term (2-4 years) |

| Ride-hailing substitutes | -1.1% | Urban centers, Singapore, Malaysia | Short term (≤ 2 years) |

| Vehicle supply & financing | -0.9% | Indonesia, Philippines, Vietnam, emerging markets | Medium term (2-4 years) |

| Slow charger roll-out | -0.7% | Indonesia, Thailand, Malaysia EV adoption zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Licensing and Insurance

ASEAN nations retain divergent permit classes, liability ceilings, and taxation triggers, forcing operators to run discrete legal entities for each jurisdiction. Malaysia’s July 2025 8% sales and service tax on rentals raises headline prices compared with duty-free Singapore, complicating regional rate transparency. Insurance carriers apply different excess thresholds, limiting cross-border rentals and curbing tourist convenience. Smaller firms lack the compliance resources of larger incumbents, slowing new-entrant expansion and local competition, especially in secondary cities where consumer choice is already thin.

Ride-Hailing Substitutes

Grab’s dominance, alongside Gojek and increasingly robust taxi apps, lures short-distance travelers away from daily or weekend self-drive bookings. The ride-hailing sector exceeded USD 30 billion in gross merchandise value by 2025, siphoning urban demand that once underpinned compact-car rentals[3]“Grab Financial Report Q1 2025,” Grab Holdings, grab.com.Potential Grab–GoTo consolidation could widen network effects, enabling lower fares that further erode rental share for intra-city mobility. Operators respond by repositioning self-drive offerings for multi-day tourism and corporate contracts rather than point-to-point trips.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Platforms Accelerate Adoption

Offline Channel reservations contributed 56.74% of 2025 revenues share in the ASEAN car Rental Market, whereas Online Channel is set to grow at 8.31% CAGR. Offline branches still dominate rural markets and legacy corporate accounts, but branch-light models lower fixed costs and extend geographic reach via pickup lockers at airports and malls. Super-apps funnel traffic by bundling vouchers with food delivery and payments, ensuring high engagement. Corporate self-booking tools integrate policy controls that improve compliance and automate expense reconciliation. For operators, richer data flows enable predictive maintenance scheduling and AI-driven price elasticity testing, boosting both uptime and yield.

The share of app-based reservations in the ASEAN car rental market is expected to surpass 54.60% by 2031 as younger digital-native travelers mature into higher-spending cohorts. Travel resellers embed direct-connect APIs, shortening booking flows to two taps. Blockchain-secured smart contracts gain traction for P2P transactions, promising faster settlements and tamper-proof damage logs. To mitigate digital fraud, industry associations collaborate on shared blacklists, enhancing platform trust and minimizing chargebacks.

By Rental Duration: Subscription Gains Momentum

Short-term rentals dominated the ASEAN car rental market with 80.62% revenue share in 2025, while subscription models are climbing at 7.75% CAGR, buoyed by tourism rebounds and sporadic local demand. Operators deploy variable-rate engines that adjust instantly to flight arrival patterns and hotel occupancy data. Corporations adopt plans that bundle multiple car classes, enabling flexible fleet rightsizing without residual-value risk.

In Singapore, the Certificate of Entitlement system inflates ownership costs, making subscriptions an economically viable substitute. Consumers value all-inclusive monthly pricing that covers insurance, servicing, roadside assistance, and often home charging for EVs. Providers leverage telemetry to monitor driving behavior and vary renewal terms accordingly, reducing loss ratios and rewarding safe usage. Regional banks partner with fleets to extend inventory financing lines, underwriting asset purchases backed by locked-in subscription cash flows.

By Service Type: Peer-to-Peer Models Scale

Self-drive retained 65.89% of the ASEAN car rental market revenue in 2025, yet P2P car-sharing is on track for 8.29% CAGR as asset-light models resonate with millennial cost sensitivities. SOCAR’s expansion beyond Malaysia’s Klang Valley into Kota Kinabalu illustrates the concept’s adaptability to new catchments without large branch footprints. The ASEAN car rental market size for chauffeur-drive services remains steady because premium business travelers and high-net-worth tourists value productivity and status.

Hybrid strategies emerge: rental incumbents list idle fleet units on P2P marketplaces during low-season windows, extracting incremental yields. Liability management remains a hurdle as insurers calibrate risk models for intermittent, multi-driver usage, but usage-based premiums gradually close the protection gap. Governments support shared mobility through dedicated parking bays and congestion-pricing rebates, tilting consumer calculus toward shared rather than owned transport.

By Vehicle Type: SUVs and EVs Lead Mix Shift

Economy and mini segments collectively earned 33.74% of the ASEAN Car Rental Market's market share, whereas Sport Utility Vehicle bookings are expected to grow at 8.37% CAGR due to increasing family group travel and improved inter-city roads. Chinese automakers flood the market with competitively priced compact crossovers, widening consumer choice and compressing rental acquisition costs. The ASEAN car rental market size for electrified SUVs could grow significantly in the upcoming years as operators accelerate fleet electrification to align with government incentives.

Luxury electric sedans enter fleets to serve executive travelers and high-spending tourists. Telematics-linked pay-per-use insurance models unlock premium pricing that reflects lower EV maintenance frequency. Suburban charging infrastructure lags city centers, prompting operators to co-invest with energy providers for depot superchargers to sustain fleet uptime. Vans and MPVs remain vital in markets with constrained public transit, supplying group transfers from airports to resorts.

By Application: Tourism Dominates but Gig-Trips Rise

Tourism and leisure retained 47.92% of the ASEAN car rental market revenue in 2025, anchored by island-hopping itineraries and cultural tours. Yet ride-hail driver rentals are the fastest-growing at 8.05% CAGR, as gig-economy workers without vehicle access rent cars by the week. Operators craft “driver-partner” programs with discounted rates and zero-deposit options in exchange for telematics data that tracks trip earnings.

Business-travel recovery lifts premium sedan demand, particularly in manufacturing hubs like Ho Chi Minh City and industrial estates near Kuala Lumpur. Daily commuting packages attract expatriates and local professionals priced out of car ownership by rising loan rates and fuel costs. Airport transfer rentals face downward pressure from ride-hailing flat fares, prompting operators to bundle GPS, child seats, and all-risk insurance for value differentiation.

By End-Customer: Corporate Wallets Grow Fastest

Individuals still accounted for 54.58% of the ASEAN car rental market revenue in 2025, but corporate and SME contracts, advancing at 8.73% CAGR, underpin long-term fleet stability. Mobility-as-a-service bundles resonate with CFOs tasked with cost containment, substituting capex-heavy company cars. Operators deploy dashboards that aggregate usage across multiple employees, simplifying tax reporting. Government contracts require tender compliance and security vetting, offering margin-accretive business, albeit with lengthy procurement cycles.

Expats and diplomats represent a niche but profitable customer set because they demand multi-year leases, premium maintenance standards, and cross-border allowances. Providers allocate multilingual support teams and vehicle swap options to minimize downtime. Subscription bundles for corporate employees include driver training modules that insurers reward with lower rates, reinforcing retention.

Geography Analysis

Indonesia contributed 25.31% of ASEAN car rental market revenue in 2025, leveraging a 270 million-strong population, revived domestic tourism, and the archipelago’s dispersed geography that favors self-drive trips. Government policy anchors fleet electrification by offering duty waivers and manufacturing tax holidays, aiming for 600,000 battery-electric vehicles by 2030. Rental operators tap local nickel supply chains to negotiate favorable battery replacement contracts, smoothing the total cost of ownership. Jakarta’s Low Emission Zone pilot attracts ESG-minded corporate clients who now specify electric vehicle classes in RFQs. Bali remains the premium leisure node, where SUV and MPV categories dominate bookings for family groups moving between resorts and surf spots.

Vietnam is the fastest-expanding market, recording a 8.95% CAGR outlook as new highways from Hanoi to Haiphong and Ho Chi Minh City to the Mekong Delta cut drive times. Manufacturing FDI inflows trigger executive travel and supplier site visits, boosting premium sedan demand. Local ride-hail competitors Gojek and BeGroup push into four-wheel segments, raising consumer awareness of flexible mobility. The Ministry of Transport’s digital licensing portal streamlines operator entry, curbing informal rentals and expanding tax-compliant fleets. Rising middle-class incomes support weekend leisure drives to coastal retreats such as Da Nang and Quy Nhon, sustaining utilization in non-metro areas.

Thailand, Malaysia, and Singapore make up the mature tier of the ASEAN car rental market. Thailand’s 2024 infrastructure upgrades, financed partially by China’s Belt and Road Initiative, unlocked secondary tourist circuits into Chiang Rai and Isan, boosting one-way rental demand. Enterprise Mobility’s joint venture with Thai Rent a Car demonstrates that global brands win by pairing international reservation systems with local regulatory navigation. Malaysia’s July 2025 8% SST on car rentals may temper short-term leisure demand, but corporate contracts commonly reclaim taxes, softening the blow. Singapore maintains the region’s highest daily rental tariffs due to tight vehicle quotas and high COE costs, yet utilization remains robust because branchless operators deploy smart lockers for after-hours collection. The Philippines, Cambodia, Laos, and Myanmar represent nascent pockets where informal rentals dominate; formal operator entry hinges on clearer insurance legislation and stable economic growth trajectories.

Regulatory Landscape

Regulation affecting car rental operations across ASEAN remains country-specific across licensing, insurance liability and taxation, which limits seamless cross-border rental products. Malaysia implemented an 8% sales and service tax on rentals in July 2025, directly affecting retail pricing versus lower-tax or duty-structured markets such as Singapore. At the regional level, ASEAN frameworks that target cross-border facilitation, such as the ASEAN Framework Agreement on the Facilitation of Cross-Border Transport of Passengers by Road Vehicles and related protocols, provide a formal basis for harmonized procedures, but implementation is uneven. Operators still typically structure compliance through separate in-country entities.

Electrification-linked policy is an increasingly important compliance and fleet-planning variable. Indonesia used fiscal instruments to support battery electric vehicle uptake, including Ministry of Finance Regulation 9/2024 (PPnBM incentives for specific BEVs during 2024) and Regulation 12/2025 extending government-borne VAT and PPnBM incentives for specific four-wheeled BEVs and buses in 2025. Regulatory definitions and registration processes also evolve. In Indonesia, KBLI 2025 taxonomy adoption in its Online Single Submission system began in June 2026, changing how mobility and rental-related business activities are categorized for licensing. In Thailand, the Department of Land Transport published a draft amendment for consultation in May 2026 to allow juristic persons to register vehicles as electronic ride-hailing cars subject to minimum fleet conditions, shaping how fleets can be deployed across rental and mobility use cases.

Value Chain Analysis

The ASEAN car rental value chain starts with vehicle sourcing (OEMs and dealer networks), followed by fleet financing (banks, captive finance, leasing companies), fleet operations (registration, insurance placement, telematics, and branch or locker-based distribution), and downstream lifecycle services (maintenance, repair, tires, parts, remarketing and disposal). The regional automotive production ecosystem is governed by multinational OEMs and depends heavily on Northeast Asian supply for key components and inputs, transmitting availability and pricing volatility into fleet acquisition cycles. Within ASEAN, Thailand and Indonesia are more integrated in motor-vehicle supply chains than markets such as the Philippines and Vietnam.

For uptime and operating-cost control, rental operators rely on standardized aftermarket service coverage, supported by regional players such as Valeo Service ASEAN, alongside local workshops and dealership service bays. Demand capture and fulfillment increasingly run through digital distribution and corporate procurement workflows. OTAs and super-apps (for example, Grab, Traveloka and Agoda) function as high-volume customer-acquisition layers, while corporate accounts are handled through master service agreements and self-booking tools that integrate policy controls and expense management. Key cost and performance levers sit in insurance underwriting (particularly for self-drive and P2P use cases), telematics-enabled risk scoring, and maintenance network density, with asset utilization and residual-value realization tied to used-vehicle channels and dealer remarketing partnerships.

Competitive Landscape

The ASEAN car rental industry displays moderate fragmentation. International majors such as Enterprise Mobility, Avis Budget, and Hertz piggyback on franchise or equity partnerships to mitigate regulatory risk and accelerate fleet localization. Enterprise Mobility has partnered with Thai Rent a Car as part of its ongoing global expansion. This move is a segment of a broader strategy targeting the Asia-Pacific, with fresh branches set to debut in Japan, South Korea, and New Zealand.

Peer-to-peer platforms SOCAR, DriveLah, and Trevo focus on tech-enabled asset sharing. They differentiate on flexible durations—hourly to monthly—and zero counter pickups. Insurance underwriters build bespoke products for P2P fleets, gradually maturing risk profiling. Electric mobility specialists like BlueSG (Singapore) and PrimeMobility (Thailand) carve out niches with all-EV portfolios and subscription bundles targeted at ESG-conscious corporates.

Strategic moves underscore evolving playbooks. Blue Bird is committed to 1,000 EV taxis by end-2025, aiming for a 10% zero-emission fleet mix. SOCAR acquired platform rival Buddy Car to consolidate Malaysian market share and widen fleet access in East Malaysia. Avis Budget launched a chatbot-enabled booking experience in 2024, integrating airport pickup locker codes into WhatsApp notifications to compress queue times. Competitive intensity pivots increasingly on tech stack sophistication, fleet electrification speed, and ability to lock long-term corporate contracts that secure predictable vehicle utilization.

ASEAN Car Rental Industry Leaders

Avis Budget Group

Sixt SE

Hertz Global Holdings

Europcar Mobility Group

Enterprise Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Brand expansion via local franchise and dealer-backed operating platforms stands out as a whitespace lever in ASEAN, particularly where regulatory navigation and service infrastructure favor partnerships. In Singapore, Enterprise Mobility signed a franchise agreement with Eurokars Leasing in April 2026 to introduce Enterprise Rent-A-Car, National Car Rental and Alamo, with services scheduled to launch in October 2026. This adds fresh capacity and supports product differentiation around international-standard reservation, service and corporate-accounting workflows. In Malaysia, Avis Malaysia introduced the Budget brand to broaden its retail mobility portfolio ahead of Visit Malaysia 2026, positioning rental offerings alongside a specific tourism program timeline rather than relying only on traditional counter sales.

Operational digitization and fleet intelligence also support near-term execution, especially around damage assessment, safety and utilization optimization. Lumens in Singapore adopting generative AI to automate vehicle damage documentation (August 2025) and Geotab unveiling an AI-powered telematics roadmap for Southeast Asian fleets (February 2026) both support faster turnarounds and standardized inspection evidence for self-drive, subscription and corporate fleets. Platform consolidation and multi-service MaaS builds remain an opportunity area, supported by Sagtec Global's January 2026 disclosure of a US$4.0 million software development agreement for an AI-driven mobility platform spanning e-hailing, car rental and subscription across Malaysia, Indonesia, Singapore and the Philippines, reflecting continued integration of rental into broader app-based mobility ecosystems.

Recent Industry Developments

- April 2026: Enterprise Mobility and Eurokars Leasing signed a franchise agreement to introduce Enterprise Rent-A-Car, National Car Rental and Alamo in Singapore, with services launching in October 2026. The move uses an established local automotive partner to accelerate market entry and service coverage while aligning global reservation and corporate-account capabilities for a high-yield hub market.

- June 2025: Baidu announced plans to roll out Apollo Go robotaxi services in Singapore and Malaysia via alliances with local operators. The planned deployment raises the competitive bar for urban point-to-point mobility and can reshape how travelers compare chauffeur-drive rentals with short-duration transport alternatives in major cities.

- February 2024: Indonesia's Ministry of Finance issued Regulation 9/2024 providing government-borne PPnBM incentives for specific battery electric vehicle imports and sales for the 2024 fiscal year. This lowered effective acquisition costs for qualifying EVs and strengthened the economics for rental and subscription operators considering electrified fleet additions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from renting passenger cars in ASEAN through self-drive and chauffeur-driven formats, for both leisure and business uses. This includes bookings made online and offline.

Scope exclusions: The market size excludes automotive sales, vehicle financing, and repair-only services that do not include a paid rental period.

Segmentation Overview

- By Booking Type

- Offline

- Online

- By Rental Duration

- Short-term (Less than 30 days)

- Long-term / Subscription (More than or equal to 30 days)

- By Service Type

- Self-Drive

- Chauffeur-Drive

- Peer-to-Peer Car-Sharing

- Corporate Fleet Leasing

- By Vehicle Type

- Economy & Mini

- Compact & Mid-size

- Sport Utility Vehicle

- Multi-Purpose Vehicle

- Luxury & Premium

- By Application

- Tourism / Leisure

- Business Travel

- Daily Commuting

- Airport Transport

- Ride-hail Driver Rentals

- By End-Customer

- Individuals

- Corporates & SMEs

- Government & Public Sector

- Expat / Diplomat

- By Country

- Indonesia

- Thailand

- Malaysia

- Singapore

- Vietnam

- Philippines

- Rest of the ASEAN Countries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping how rental demand forms in ASEAN, then checking what can be tracked each year using public reporting. We referenced public sources such as ASEANstats and national statistics offices, tourism arrivals and receipts from ministries of tourism, airport passenger throughput updates from airport authorities, and central bank or IMF inflation and exchange-rate series.

To keep assumptions grounded, we also reviewed transport and road safety agencies for fleet and licensing context, plus customs and trade portals for vehicle import signals where relevant. Company annual reports, investor presentations, and reputable press were used to understand pricing direction and channel shifts. In a few cases, we used paid subscriptions for company financials and intelligence, news and financials, and shipment-level import and export checks to cross-verify directional trends. These examples are indicative only, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk sources cannot explain well, especially utilization patterns, seasonality around peak travel months, and discounting behavior by booking channel. We spoke with operators, fleet partners, travel intermediaries, and corporate mobility buyers across the main ASEAN markets, then reconciled differences by country and booking channel.

Inputs from these discussions helped refine typical rental length, the mix of self-drive versus chauffeur-driven demand, and how pricing changes when supply tightens and vehicles become less available.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 59% | Functional/Unit leaders: 42% | |

| Smaller Players: 16% | Managers: 44% |

Market-Sizing & Forecasting

The core model starts from a top-down demand pool build tied to travel and mobility activity across ASEAN, then converts it into rental revenue using traceable inputs. Practical starting points include inbound and domestic tourism volumes, airport passenger throughput, urban mobility intensity, and the active fleet available for rent, which are then translated into paid rental days and expected pricing.

To make sure totals are not drifting, the results are corroborated with selective bottom-up approximations, such as sampled average daily rates by country, utilization ranges observed through interviews, and revenue run-rate checks from a set of visible operators. Where direct data is missing for smaller markets, gaps are filled using proxy indicators like tourism growth, vehicle availability, and relative price levels, and then re-checked with local respondents.

For forecasting, we used scenario analysis supported by regression checks on the strongest drivers, mainly tourism demand, inflation-linked price movement, and fleet availability constraints. The scenarios were tuned with expert views on how online bookings, long-term rentals, and corporate demand are likely to rebalance through the forecast window.

Data Validation & Update Cycle

Validation is done through several passes so assumptions do not slip into the final numbers unnoticed. We compare model outputs against independent signals such as tourism trends, airport traffic changes, and observable pricing movement, and then investigate any large variance by country or rental type before sign-off.

If a mismatch is detected, respondents are re-contacted and inputs are adjusted with a clear audit trail so the change can be explained. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory shifts, sharp currency moves, or major travel disruptions. Before delivery, an analyst completes a fresh review pass so clients receive the most current view.

Mordor Intelligence's Asean Car Rental Market Estimate Compared With Other Published Estimates

Published market values for ASEAN car rental can look far apart because counted services, timing, and currency handling are not the same across studies. Differences usually come from what is treated as rental revenue versus adjacent mobility services, and from how pricing and utilization are normalized across countries.

Peer-to-peer car sharing is kept inside Mordor Intelligence's scope only when it is a paid vehicle rental transaction, which removes a lot of casual cost-sharing activity that some estimates appear to include. Other gaps come from whether long-term corporate leasing is treated as part of rentals, whether rates are modeled using peak-season prices, and how FX conversion is timed when local currencies move quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.97 B (2026) | |

| Regional Consultancy A | USD 3.35 B (2026) | Uses a broader mobility basket that can blend rentals with adjacent services, and applies higher blended daily rates without fully normalizing for utilization differences by country. |

| Industry Publisher B | USD 2.71 B (2022) | Older base year and partial country coverage can understate the rebound period, and FX conversion and inflation updates are not clearly refreshed to the current cycle. |

The spread in the table is mainly explained by scope items around car sharing and leasing, plus how pricing and FX are updated by year. With demand and price inputs tied to visible travel and fleet signals, the final number stays easy to trace and repeat when market conditions change.

Key Questions Answered in the Report

How large is the ASEAN car rental market in 2026?

The ASEAN car rental market size stands at USD 2.97 billion in 2026 and is projected to reach USD 4.33 billion by 2031.

Which country leads the market?

Indonesia commands the largest share at 25.31% of ASEAN car rental market share in 2025, propelled by strong domestic tourism and EV incentives.

What booking channel is growing fastest?

Online reservations through OTAs and super-apps are expanding at 8.31% CAGR, outpacing offline branches as smartphone adoption rises.

Why are subscriptions becoming popular?

Corporates and urban professionals favor fixed monthly payments that cover insurance and maintenance, helping subscription models grow at 7.75% CAGR.

How are electric vehicles influencing the sector?

Government subsidies and corporate sustainability goals push operators to electrify fleets; Indonesia alone targets 600,000 EVs by 2030, underpinning new rental revenue streams.

Who are the key competitors?

Enterprise Mobility, Avis Budget, Hertz, Grab, SOCAR, and Blue Bird lead the field, each focusing on tech integration, fleet electrification, or peer-to-peer sharing to differentiate.

Page last updated on: