Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

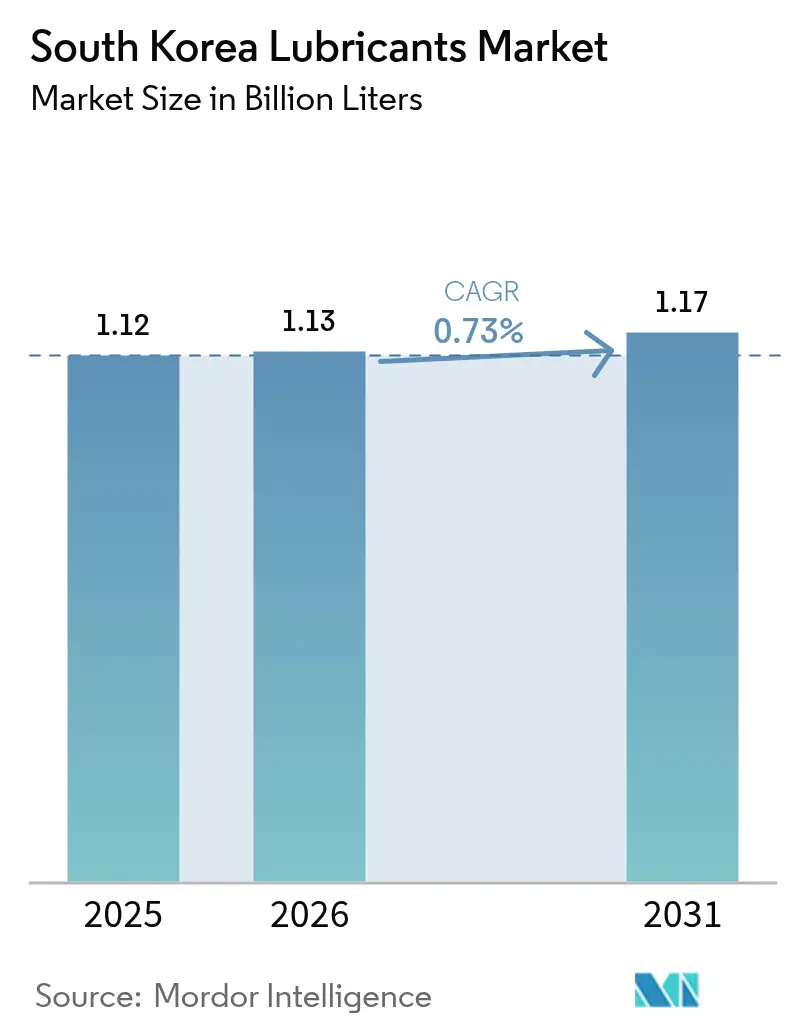

| Base Year Market Size (2025) | 1.12 Billion Liters |

| Market Volume (2026) | 1.13 Billion Liters |

| Market Volume (2031) | 1.17 Billion Liters |

| Growth Rate (2026 - 2031) | 0.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Lubricants Market Analysis by Mordor Intelligence

South Korea Lubricants Market size in 2026 is estimated at 1.13 Billion Liters, growing from 2025 value of 1.12 Billion Liters with 2031 projections showing 1.17 Billion Liters, growing at 0.73% CAGR over 2026-2031. The growth path remains subdued because electric-vehicle penetration is replacing conventional engine oil volumes, while industrial buyers are tightening their efficiency targets and sustainability criteria. Government incentives for EV-oriented lubricant R&D, rapid data center expansion, and resilient premium base oil exports cushion volumes, yet cannot fully offset demand erosion in legacy automotive segments. Refiners are therefore shifting portfolios toward high-margin synthetic, bio-based, and specialty fluids to defend profitability amid volatile base-oil spreads. At the same time, improved enforcement against counterfeit products is removing low-cost options, nudging users toward branded formulations with verified performance credentials.

Key Report Takeaways

- By product type, automotive engine oil accounted for 37.62% of the market share in 2025. The market size of transformer oil is expected to increase with a CAGR of 1.83% during the forecast period (2026-2031).

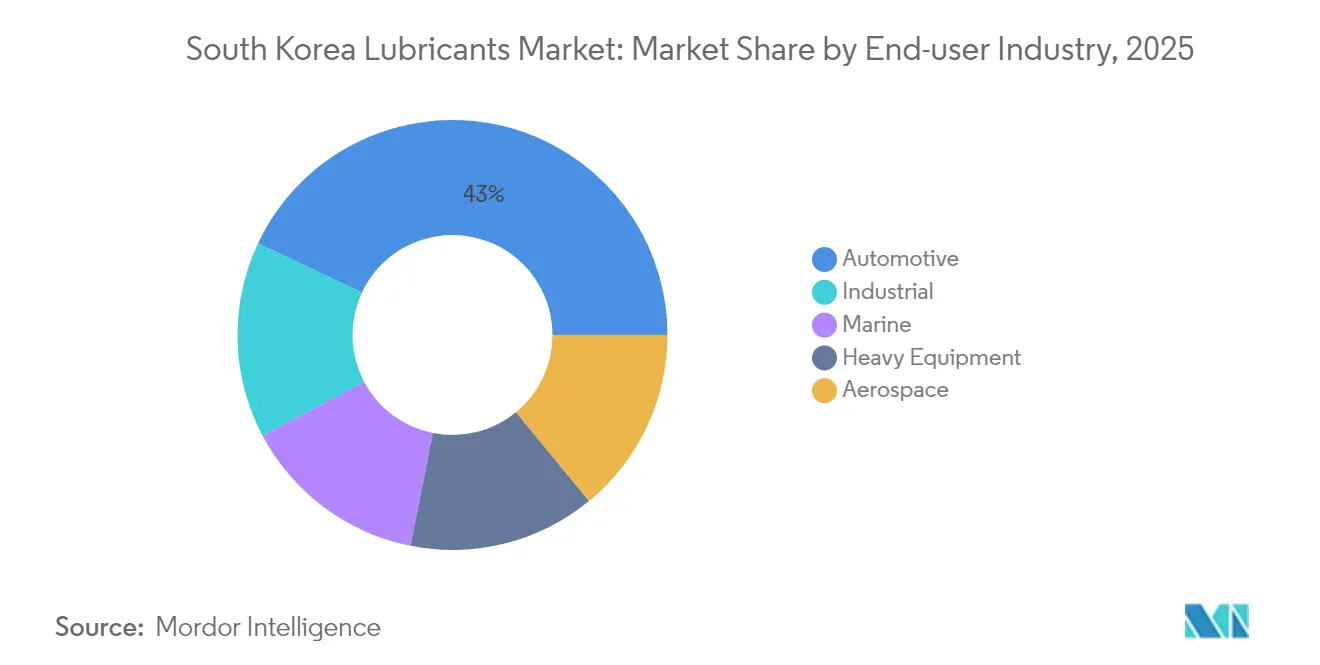

- By end-user industry, the automotive sector held a 43.00% market share in 2025, and during the forecast period (2026-2031), the industrial sector's share is expected to increase at a CAGR of 0.98%.

- By base stock type, the market share of the mineral oil-based lubricants was 67.40% in 2025, and the share of bio-based lubricants is expected to increase with a CAGR of 2.14% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-specific lubricant R&D incentives | +0.2% | National (Seoul-Incheon belt) | Medium term (2-4 years) |

| Data-center immersion-cooling fluid uptake | +0.15% | Pangyo and Bundang tech hubs | Short term (≤2 years) |

| Premium base-oil export profitability | +0.1% | Ulsan and Yeosu refining complexes | Long term (≥4 years) |

| Rising synthetic penetration in passenger cars | +0.05% | Urban markets nationwide | Medium term (2-4 years) |

| Stricter fuel-economy and emission norms | +0.08% | Nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV-specific lubricant R&D incentives empower rapid portfolio diversification

The Ministry of Trade, Industry, and Energy earmarked KRW 1 trillion (USD 750 million) in 2024 to accelerate next-generation lubricant development focused on EV drivetrains and thermal management[1]Ministry of Trade, Industry and Energy, “Petrochemical Restructuring Initiatives,” motie.go.kr. Funding priority for copper-compatible fluids, high-dielectric coolants, and extended-interval greases gives domestic formulators a head start in emerging niches. Large refiners partner with battery and power-electronics suppliers to co-design fluids that enhance drivetrain efficiency, while small specialty chemists gain access to grants that would be unattainable under normal capital-intensive R&D models. Portfolio renewal reduces reliance on declining engine oil barrels and positions the South Korean lubricants market for export of proprietary EV fluid technology. Intellectual-property creation also builds barriers against lower-cost overseas blenders attempting to enter the segment.

Data-center immersion-cooling fluid uptake reinforces digital-economy alignment

Hyperscale operators have accelerated the rollout of liquid cooling to curb energy intensity, driving new demand for specialty dielectric fluids. SK Enmove opened a dedicated production line in 2024 that delivers high-thermal-stability single-phase fluids, while GS Caltex integrated service contracts covering coolant supply, monitoring, and disposal. Early projects in Pangyo demonstrate power-usage effectiveness gains of up to 30%, making immersion cooling an attractive option under tighter energy regulations. The premium chemistry involved, including narrow-range base stocks and robust antioxidant packages, generates unit margins several times higher than commodity hydraulic oils. Because fluid change-outs follow strict quality protocols, suppliers can secure long-term, annuity-like revenue streams.

Premium base-oil export profitability offsets domestic volume stagnation

Korea Customs Service reported USD 2.1 billion in base-oil export receipts for 2024, with Group II and III cuts commanding sturdy premiums over regional spot prices. Technological advantages, such as advanced hydro-cracking and wax isomerization, enable tight viscosity-index control, meeting OEM demands for extended-drain lubricants that enhance fuel efficiency. The Shaheen project adds 340,000 barrels per day of capacity, oriented toward high-grade base stocks, reinforcing the country as a reliability hub in the Asia-Pacific region. Shorter lead times and strong technical support enhance stickiness with foreign blenders, allowing for sustained pricing even when crude spreads compress. Export resilience, therefore, stabilizes refinery utilization and supports cash flow needed for domestic sustainability investments.

Rising synthetic penetration in passenger cars meets performance mandates

Synthetic lubricants covered roughly 35% of passenger-car fills in 2024 as OEMs pursued fuel-efficiency gains and longer service intervals[2]Ministry of Environment, “Euro 7 Transition Roadmap,” env.go.kr . Hyundai adopted full-synthetic factory fills across its domestic models, boosting demand for low-viscosity formulations, such as SAE 0W-20, that reduce friction losses. Consumer awareness campaigns emphasize the importance of warranty retention and reduced maintenance downtime, persuading owners to pay premiums. The trend also aligns with Euro 7 readiness, which requires tighter control of particulate emissions. As synthetics often command double the margin of mineral products, refiners view penetration gains as a hedge against volume attrition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV adoption cutting engine-oil volumes | -0.25% | Seoul-Incheon and nationwide | Medium term (2-4 years) |

| Counterfeit lubricant distribution crackdown | -0.12% | Rural and small-town networks | Short term (≤2 years) |

| Volatile base-oil spreads squeezing margins | -0.1% | Integrated refineries nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid EV adoption erodes legacy engine-oil demand

Electric vehicles captured 35% of new registrations in 2024 and are projected to achieve a 100% share by 2035, resulting in a reduction of roughly 4–5 liters of annual engine oil consumption per vehicle. The effect compounds through the fleet as early-cycle EVs age, translating into a structural headwind for the South Korea lubricants market. Commercial fleets are mirroring the shift to electric buses and light-duty delivery vans, accelerating the decline in diesel engine oil use. Although EV-specific fluids generate new revenue streams, their per-unit volume is significantly lower. This forces marketers to pursue higher-value synthetics and services to preserve top-line stability while rightsizing blending capacity.

Volatile base-oil spreads pressure refinery economics

Base-oil crack spreads narrowed sharply in late 2024 as China brought new capacity online, squeezing margins for Korean producers with high operating costs. Spread volatility complicates feedstock procurement planning and undermines the economics of long lead-time export contracts. Integrated refiners respond by throttling production toward higher-value Group III stocks or diverting feed to fuel production when spreads turn negative. Smaller standalone blenders face sudden cost shocks that erode competitiveness against majors with captive supply. The uncertainty also discourages capital allocation to specialty upgrades, slowing innovation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-oil supremacy confronts emerging specialty gains

The automotive engine oil segment retained a 37.62% share of the South Korean lubricants market in 2025, driven by a 25 million-unit internal combustion fleet that still requires routine drain intervals. Volume slippage becomes evident from 2026 onward as EV registrations accelerate; yet, the absolute scale keeps the segment central to revenue. Transformer oil is the fastest-growing product, with a 1.83% CAGR, driven by national grid upgrades and renewable energy integration, which demand high-dielectric fluids resistant to oxidative stress.

Industrial engine oils and hydraulic fluids sit in a mid-growth corridor tied to advanced manufacturing and construction cycles. Transmission fluids gain relevancy through wider adoption of multi-speed automatics and hybrid transmissions that rely on low-viscosity, high-shear-stability fluids. Gear oils maintain steady demand from shipbuilding and offshore equipment, driven by stringent OEM warranty requirements. Brake-fluid sales are slowly shrinking as regenerative braking curbs usage frequency, although fluid specifications are growing more complex to suit electronic stability controls. Greases maintain niche importance across bearings and chassis components, often functioning as entry points for specialty manufacturers targeting performance-critical applications.

By End-User Industry: Automotive bulk challenged by smarter factories

Automotive consumption accounted for 43.00% of the South Korea lubricants market in 2025, anchored by domestic production from Hyundai, Kia, and GM Korea as well as a sizable aftermarket. However, the industrial sector posts the highest growth at a 0.98% CAGR, reflecting expanded semiconductor fabrication, petrochemical upgrades, and investments in precision machinery. These plants require low-evaporation, ultra-clean, and thermally stable lubricants that permit extended service intervals and minimal downtime. The South Korea lubricants market size for industrial users is projected to climb from 0.34 billion liters in 2026 to 0.36 billion liters in 2031 as smart-factory rollouts widen.

Marine demand benefits from shipyard activity in Ulsan, Geoje, and Busan, where newbuilds and overhauls need engine oils, stern-tube greases, and wire-rope lubricants. Aerospace volumes remain modest yet technically demanding due to stringent fire-resistance and oxidation thresholds. Heavy-equipment usage is linked to infrastructure budgets and urban redevelopment, sustaining hydraulic and gear oil flows. Power-generation subsegments grow alongside offshore wind farms and gas-turbine repowering projects, boosting turbine-oil and transformer-oil needs. Together these shifts signify a gradual pivot away from vehicle reliance toward diversified, specialty-rich industrial orders.

By Base Stock Type: Mineral dominance gives ground to low-carbon alternatives

Mineral oils supplied 67.40% of total volumes in 2025, driven by integrated refining economics that have kept delivered costs low. Bio-based lubricants are projected to expand at a 2.14% CAGR through 2031, spurred by tax credits, government procurement preferences, and brand-owner sustainability pledges.

Semi-synthetics appeal where full synthetics overshoot cost thresholds, providing a balanced value proposition. Regulatory frameworks such as Korean Industrial Standards (KS) definitions and International Sustainability and Carbon Certification (ISCC) labels increase transparency, giving importers confidence in renewable-c, such as Korean Industrial Standards (KS) definitions and International Sustainability and Carbon Certification (ISCC) labels, increase transparency, giving importers confidence in renewable content claims. Refiners with hydrocracking flexibility can co-process waste cooking oil or plastic pyrolysis feed to generate low-carbon Group III+ base oils without requiring major equipment overhauls, thereby enhancing competitiveness as carbon accounting becomes tighter.

Geography Analysis

Lubricant demand is concentrated in the Seoul-Incheon corridor, which accounted for roughly 34.70% of national volumes in 2025, due to high vehicle density, semiconductor fabs, and hyperscale data centers. This urban cluster leads in synthetic grades and EV-specific fluids, thanks to higher income levels and early regulatory adoption. The Ulsan-Busan axis ranks second, anchored by petrochemical complexes, automotive plants, and the world’s largest shipyards. Here, industrial oils, marine lubricants, and process oils dominate the blend mix.

The Yeosu-Gwangyang region supports large steel mills, petrochemical crackers, and bulk chemical exports that demand heavy-duty hydraulic and gear oils. Government restructuring funds worth KRW 3 trillion, announced in 2024, aim to upgrade these facilities toward low-carbon processes, thereby expanding opportunities for bio-based and high-efficiency lubricants. In contrast, rural provinces show lower penetration of synthetics and EV fluids, relying on mineral-based engine oils for agricultural machinery and aging vehicle fleets. Distribution logistics focus on hub-and-spoke models where regional service centers consolidate inventory and technical support.

Spatial variations widen as data-center clusters emerge in Gyeonggi Province and Busan’s Eco-Delta industrial complex, catalyzing demand for immersion-cooling fluids produced by SK Enmove and GS Caltex. Metro governments enforce stricter low-emission zones, quickening the shift to low-viscosity oils within city limits, while coastal regions prioritize marine fuels with higher TBN detergency. These divergent patterns underline the need for location-specific portfolio mixes to sustain share in the South Korea lubricants market.

Regulatory Landscape

South Korea's lubricant and additive supply chains are increasingly shaped by chemicals management rules under the Ministry of Environment (K-REACH and the Chemical Control Act). These tighten substance identification, hazard communication, and import documentation requirements that apply to lubricant additives and specialty fluids. Major revisions implemented in August 2025 replaced the broad "toxic substance" label with a more granular classification for human acute, human chronic, and environmental hazardous substances, increasing compliance workloads across formulation, labeling, and customer documentation.

In 2026, operational compliance deadlines and inventories became more stringent. The grace period for old MSDS templates ended on June 30, 2026 under MOEL Public Notice 2025-50, and July 1, 2026 marked a deadline tied to substance confirmation (LOC), hazard labeling, and import declaration for newly designated hazardous substances. Separately, an April 28, 2026 official notice revised the Existing Chemical Substances List and restored original names for 136 substances previously masked for confidential business information protection, requiring companies to recheck registrations and exemptions against updated naming and identification references.

Value Chain Analysis

The value chain runs from base-oil production at integrated refining complexes through blending and formulation, and packaging, to distribution through OEM channels and a large aftermarket. Domestic refiners such as SK Enmove, S-OIL, GS Caltex, and HD Hyundai Oilbank anchor upstream supply of Group II and Group III base oils, while blending plants and technical centers tailor additive packages for automotive oils, industrial lubricants, and emerging thermal-management fluids for EVs and data centers. Downstream, branded networks and service partners distribute through dealerships, quick-lube outlets, industrial MRO suppliers, and direct B2B contracts where condition monitoring and used-oil handling are increasingly bundled with supply.

In 2026, public-sector oversight added another layer to channel discipline and operating risk. The Ministry of Trade, Industry and Energy initiated interagency inspections with local governments and the Korea Petroleum Quality and Distribution Authority to check manufacturers and distributors, alongside weekly price monitoring of automotive lubricants and marine fuels intended to stabilize supplies. Competitive conduct risk also rose after the Korea Fair Trade Commission began formal deliberations involving 10 lubricant companies for alleged price-fixing and bid-rigging in industrial lubricants and metalworking fluids (covering January 2018 to October 2024), increasing due-diligence demands for procurement, tendering practices, and distributor governance across midstream and industrial end-user nodes.

Competitive Landscape

The South Korea Lubricants Market is moderately consolidated. The South Korea lubricants market exhibits oligopolistic traits with three integrated majors, S-Oil, GS Caltex, and SK Innovation, controlling more than two-thirds of volumes through captive base-oil supply, proprietary blending plants, and nationwide distribution. Regulatory compliance and brand trust act as formidable barriers for foreign entrants, given stringent Korean Industrial Standards and rigorous counterfeit enforcement. Majors invest in QR-code authentication and blockchain traceability to maintain customer confidence, while AI-enabled demand forecasting curbs overproduction. As a result, market contestability hinges less on new capacity and more on innovation pipelines and sustainability narratives.

South Korea Lubricants Industry Leaders

ExxonMobil Corporation

GS Caltex

S-OIL Corporation

HD Hyundai

SK inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity area is the shift from commodity automotive oils toward specialty, higher-margin fluids tied to electrification and digital infrastructure. Government programs and policy signals are steering chemicals and materials R&D toward advanced applications: MOTIE allocated KRW 1 trillion in 2024 for next-generation lubricant development focused on EV drivetrains and thermal management, and in February 2026 announced the 2026 Materials and Components Technology Development Project with KRW 1.291 trillion for R&D (including funding lines for chemicals and automotive-related materials). On the demand side, data-center liquid cooling is already moving into commercial rollout, and suppliers in South Korea have introduced dedicated production and product lines for dielectric and direct-liquid-cooling fluids. That supports a premium niche where service contracts and strict quality protocols create more durable supplier relationships.

Another opportunity is operational and portfolio upgrading in the base-oil and blending ecosystem, shaped by oversupply pressures in the wider region and tighter customer qualification needs for Group II and Group III and specialty base stocks. Corporate and plant-level modernization is also visible in the sector, including GS Caltex completing a large Yeosu plant turnaround in July 2026 with an investment of 200 billion won and use of AI-driven maintenance approaches, which supports reliability and more consistent quality in supply. At the same time, stronger enforcement and monitoring for pricing and distribution practices is pushing buyers toward traceable, compliant products, creating whitespace for suppliers that can document formulations under updated MSDS rules and meet increasingly formal procurement requirements in industrial accounts.

Recent Industry Developments

- May 2026: Lubrizol and HD Hyundai Oilbank signed a memorandum of understanding to collaborate on lubricant innovation, technical development, and market insight sharing across Korea and the Asia-Pacific region. The agreement strengthens additive-formulation and base-oil alignment, supporting faster development cycles for premium and specialty lubricants. It also reinforces Korea-based capability building for differentiated products as legacy engine-oil volumes face structural pressure.

- October 2025: GS Caltex launched Kixx DLC Fluid PG25, a direct liquid cooling fluid for data centers, expanding its thermal-management portfolio beyond immersion cooling fluids introduced earlier. The move targets a fast-growing buyer set among hyperscale and enterprise data center operators seeking higher heat-removal performance. It also broadens lubricant marketers into serviceable fluids with monitoring and replacement protocols that favor longer-term supply relationships.

- August 2025: GS Caltex introduced the Kixx GX7 synthetic engine oil lineup certified under the API SQ specification for gasoline engines. The launch positioned the brand around higher-performance, low-viscosity formulations aligned with newer vehicle requirements and extended drain intervals. Upgrading product tiers helps defend margins in the automotive segment as consumers and OEMs raise performance and warranty-compliance expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers finished lubricants consumed within South Korea, measured in volume, across automotive and industrial use where oils and greases are used to reduce wear, heat, and friction in equipment.

Scope exclusions: This sizing does not include fuels, base oils traded as feedstock, or non-lubricant process chemicals that are sometimes bundled into refinery product discussions.

Segmentation Overview

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil & White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy & Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the country demand pool using public data that can anchor activity levels, before any pricing or share assumptions are applied. Sources reviewed include government and official statistics such as Korea Customs Service trade releases, Statistics Korea (KOSTAT) industrial output series, and Ministry of Land, Infrastructure and Transport vehicle registration tables, which help frame the in-use vehicle and equipment base.

Next, the supply and application picture is refined using technical and industry references such as KSA standards notes, SAE and API lubricant service category updates, and open publications from KOTRA and trade bodies covering manufacturing and shipbuilding. We also cross-check with company annual reports, investor decks, and reputable business press to validate capacity additions, product positioning, and channel shifts. To close gaps on company-level splits and historic financials, we selectively used paid databases for company financials and for lubricants specific market information. This desk list is not exhaustive, and many other public sources were also consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to validate consumption patterns and to keep the volume model aligned with what is actually being sold into automotive workshops, fleets, factories, and marine and industrial maintenance channels. We spoke with lubricant blenders, distributors, service providers, and large end users across key demand centers in South Korea, and then rechecked assumptions where interview feedback differed from desk indications.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | |

| Mid tier: 47% | Functional/Unit leaders: 27% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs lubricant demand from the South Korea vehicle parc and industrial activity indicators, which are then translated into lubricant consumption rates by application. To keep it practical, we modeled the market in liters first and only used value proxies as supporting checks, because product mix and drain intervals can shift volumes even when spending looks stable.

Inputs used in the model include the in-use vehicle population by major type, annual mileage and service frequency, estimated drain intervals by lubricant grade, industrial output trends in lubricant-intensive sectors (such as machinery and shipbuilding), and the share shift toward synthetics that can reduce liters per service. Where a data series was missing, we filled it with bounded ranges from interviews and aligned it to observable signals like import-export direction and maintenance intensity.

For forecasting, scenario analysis was applied around a base case so the model stays transparent when EV penetration, manufacturing cycles, and maintenance behavior move faster or slower than expected. We then corroborated totals with selective bottom-up approximations, including sampled average liters per change multiplied by service events and channel checks on distributor throughput, and we adjusted only when the two views stayed consistently apart across multiple checkpoints.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including vehicle stock changes, production cycles in key industries, and whether implied per-unit consumption remains realistic versus service norms shared by practitioners. When a number looks unusual, it is traced back to the driver layer, and the assumption is either corrected or validated through a follow-up touchpoint.

Before sign-off, the work goes through a multi-step analyst review where calculations, unit conversions, and year-on-year movements are rechecked for consistency. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp changes in industrial output, major regulatory shifts, or visible disruptions in supply. Just before delivery, we run a final update pass so the dataset reflects the latest available public releases and verified market signals.

Mordor Intelligence's South Korea Lubricants Market Size Compared Against Other Published Estimates

Published market sizes for South Korea lubricants often do not match because authors use different units, include different product baskets, and apply different assumptions for drain intervals and synthetic mix. Timing also matters since some estimates are built on older parc data or on a different base year.

Base oils sold as refinery feedstock are a common inclusion in some write-ups, but they sit outside Mordor Intelligence's scope here, which stays on finished lubricants consumed in-country and expressed in liters. Gaps also come from whether marine and industrial maintenance volumes are modeled from activity indicators, or simply grown using a headline CAGR, and from how imports are netted out when re-exports or blending flows are present.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.12 B (2025) | |

| Trade Journal A | USD 0.86 B (2025) | Uses a narrower demand pool that leans on automotive service volumes and applies conservative drain-interval assumptions, which can undercount industrial maintenance and marine-related consumption. |

| Industry Association B | USD 1.00 B (2025) | Aggregates finished lubricants with selected adjacent fluids and uses a blended growth rate without fully rechecking implied liters against vehicle parc and industrial output movements. |

Overall, the spread is explained mostly by what gets counted as a lubricant and how liters are rebuilt from real activity drivers. By keeping the inputs tied to parc, service intensity, and industrial production checks, our estimate stays traceable to clear steps that can be repeated and stress-tested when conditions change.

Key Questions Answered in the Report

How large is the South Korea lubricants market in 2026?

It totals 1.13 billion liters, with a forecast uptick to 1.17 billion liters by 2031.

What CAGR is expected for lubricant demand through 2031?

The overall market is projected to post a modest 0.73% CAGR during 2026-2031.

Which product type currently dominates sales?

Automotive engine oil leads with 37.62% share of national volumes in 2025.

Which segment is growing fastest?

Transformer oil is set to rise at a 1.83% CAGR as grid modernization accelerates.

How is electric-vehicle adoption affecting lubricant demand?

Each EV removes 4–5 liters of annual engine-oil volume, creating a structural decline offset by growth in specialized EV fluids.

Page last updated on: