Southeast Asia And Oceania Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

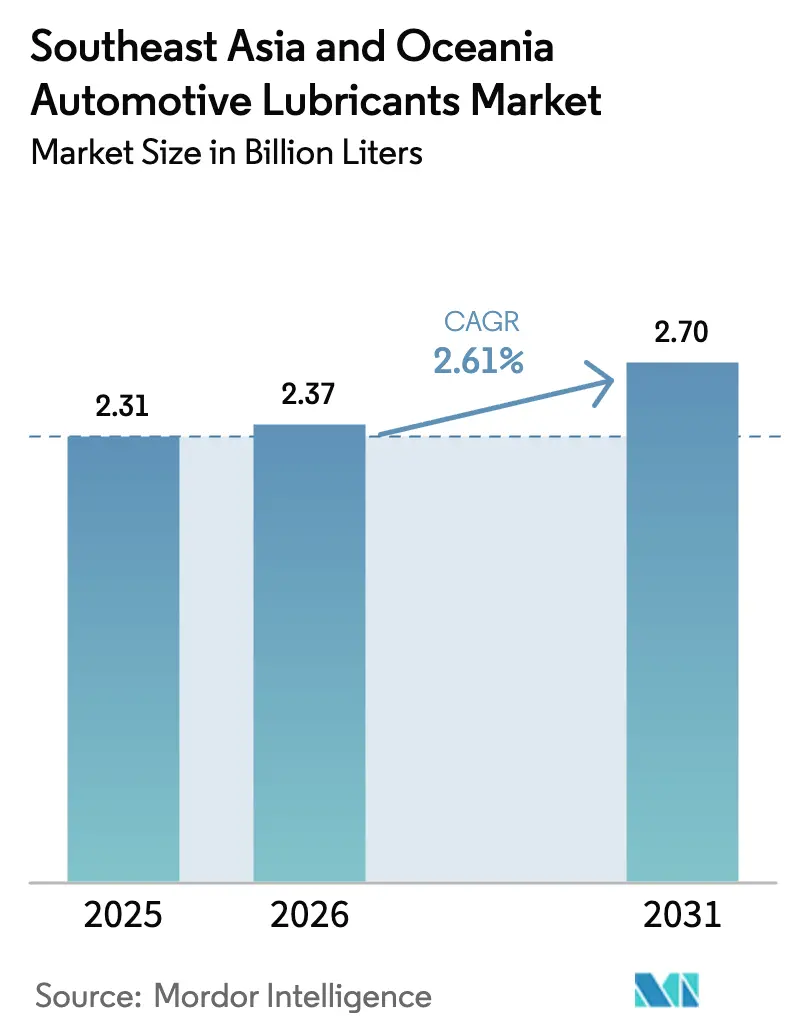

| Base Year Market Size (2025) | 2.31 Billion liters |

| Market Volume (2026) | 2.37 Billion liters |

| Market Volume (2031) | 2.7 Billion liters |

| Growth Rate (2026 - 2031) | 2.61% CAGR |

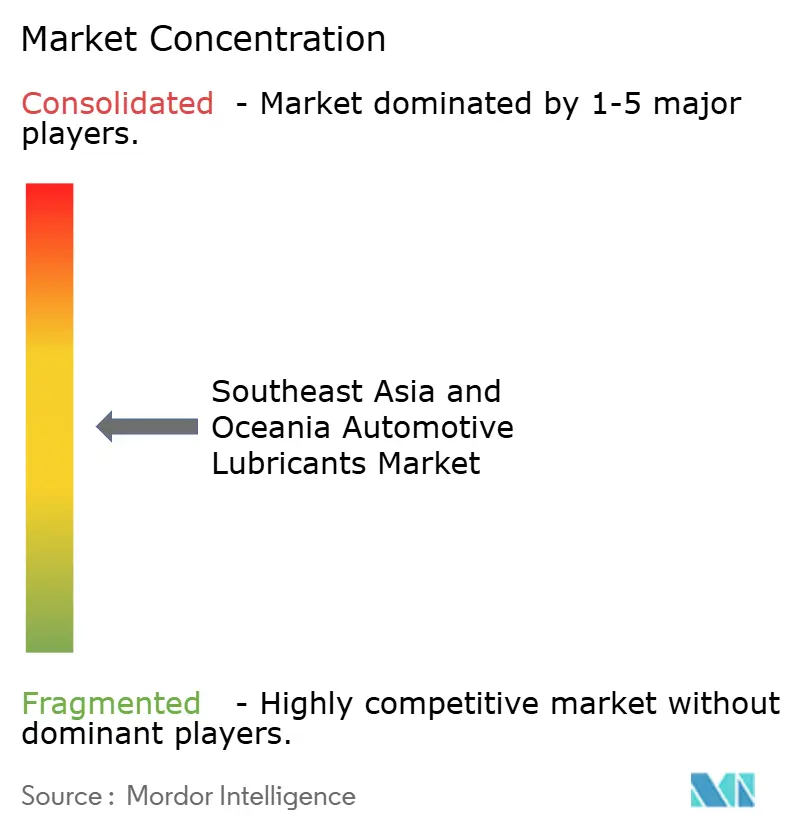

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia And Oceania Automotive Lubricants Market Analysis by Mordor Intelligence

The Southeast Asia and Oceania Automotive Lubricants Market size was valued at USD 2.31 billion in 2025 and estimated to grow from USD 2.37 billion in 2026 to reach USD 2.7 billion by 2031, at a CAGR of 2.61% during the forecast period (2026-2031). Moderate growth reflects a region where rising vehicle ownership coincides with early adoption of electric vehicles, sophisticated fleet management, and uneven economic development. Indonesia leads demand, driven by refinery upgrades, a growing middle class, and resilient internal-combustion engine sales. Vietnam delivers the fastest growth pace, supported by a government roadmap that targets domestic manufacturing self-sufficiency and export capacity. Thailand remains the regional production hub, while Malaysia tightens quality oversight through mandatory SIRIM certification that takes effect in April 2025. On the product front, the penetration of synthetic and semi-synthetic products is rising as OEMs push for longer drain intervals and tighter emissions limits. Consolidation among multinational suppliers continues, with players reallocating capital toward local blending and specialty manufacturing as retail divestments accelerate.

Key Report Takeaways

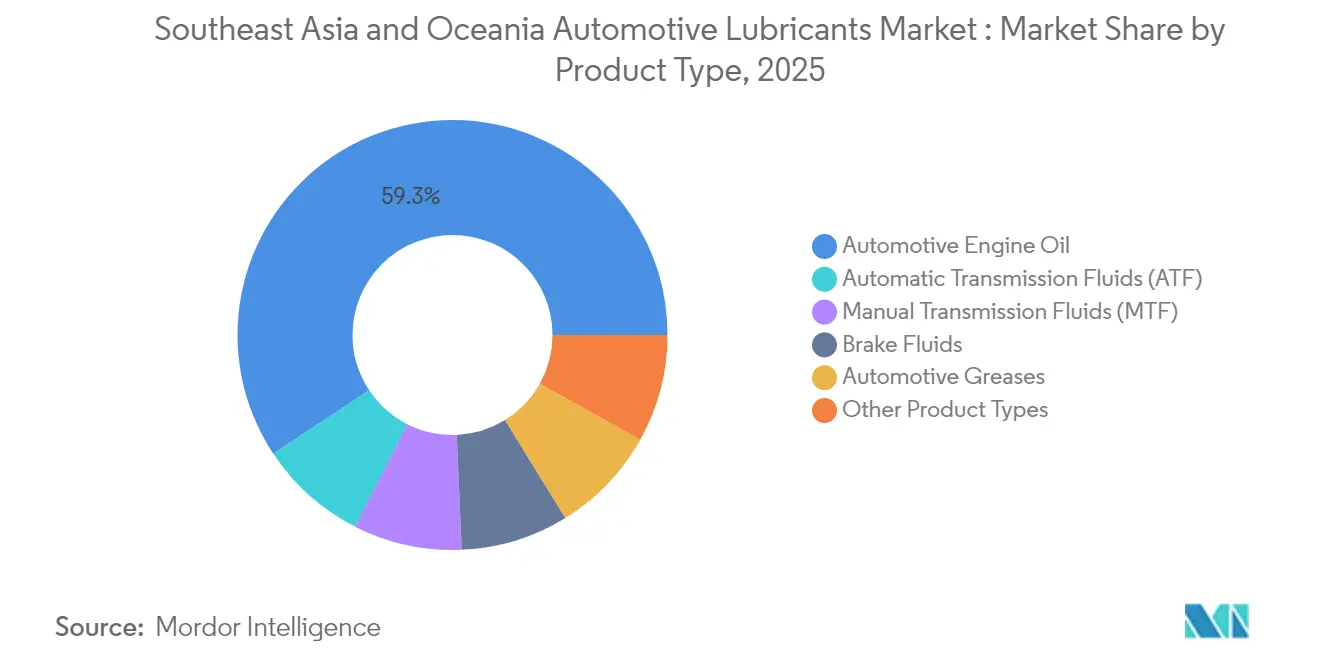

- By product type, automotive engine oil led with a 59.32% share of the Southeast Asia and Oceania automotive lubricants market in 2025, while automatic transmission fluids posted the fastest growth rate of 2.78% through 2031.

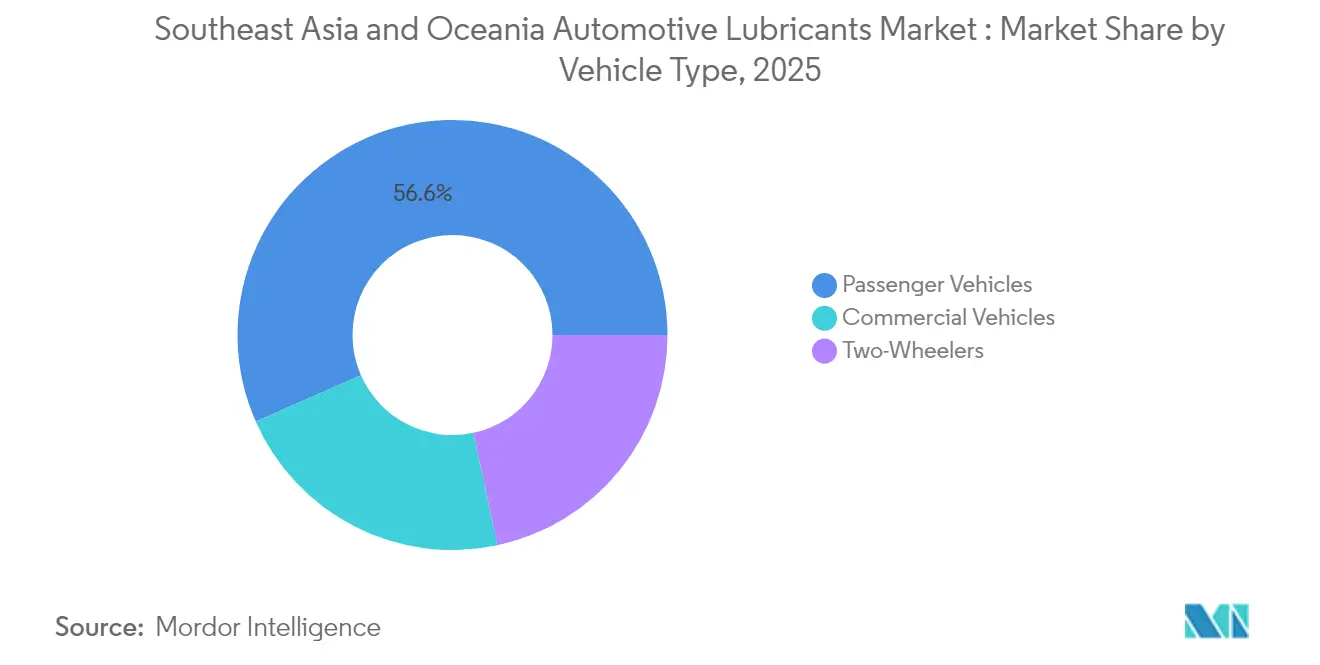

- By vehicle type, passenger cars accounted for 56.60% of the Southeast Asia and Oceania automotive lubricants market size in 2025, yet commercial vehicles delivered the highest 2.92% CAGR between 2026 and 2031.

- By geography, Indonesia held 28.40% of the Southeast Asia and Oceania automotive lubricants market share in 2025, whereas Vietnam is forecast to grow at a 4.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia And Oceania Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of e-commerce and logistics fleets | +0.8% | Indonesia, Vietnam, Thailand, Malaysia | Medium term (2-4 years) |

| Growing two-wheeler and ride-sharing parc | +0.6% | Indonesia, Vietnam, Thailand, Philippines | Short term (≤ 2 years) |

| Rising adoption of synthetic grades | +0.5% | Singapore, Malaysia, Thailand, Australia | Long term (≥ 4 years) |

| OEM co-branding partnerships | +0.4% | Thailand, Indonesia | Medium term (2-4 years) |

| Income growth and vehicle sales | +0.7% | Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of e-commerce and logistics truck fleets

Commercial logistics is reshaping the Southeast Asia and Oceania automotive lubricants market. Indonesia’s national logistics upgrades push commercial-vehicle lubricant demand to a 3.05% CAGR, well above headline growth, as fleet owners adopt high-performance synthetics to reduce downtime and fuel use. Vietnam’s 2030–2045 auto-sector blueprint aligns with similar fleet modernization, driving specification upgrades that favor extended-drain formulations. Cross-border e-commerce routes increase average haul length, exposing lubricants to higher thermal stress. Suppliers are responding by establishing regional hubs that shorten delivery cycles while tailoring viscosity packages to meet the specific operating conditions of tropical environments.

Growing two-wheeler and ride-sharing parc

Motorcycles dominate personal mobility in Indonesia, Vietnam, Thailand, and the Philippines, and riders clock higher annual mileage under app-based ride-sharing platforms. Two-wheeler lubricants require more frequent drain intervals resulting in a higher volume per vehicle compared to passenger cars. Platform operators now specify branded synthetics to minimize unplanned maintenance, raising average selling prices and boosting supplier margins.

Rising adoption of synthetic and semi-synthetic grades

Stringent emissions rules in Singapore and Malaysia, as well as tightening OEM warranties across Thailand, accelerate the uptake of synthetic fuels. Price premiums over mineral oils are mitigated by 1.5-2× service-interval extensions, attracting fleets focused on total cost of ownership. PETRONAS’s 2024-2026 activity outlook highlights a downstream pivot toward cleaner mobility solutions, mirroring the momentum of consumer and regulatory trends[1]PETRONAS, “PETRONAS Activity Outlook 2024-2026,” petronas.com . Australia’s mature aftermarket adds further pull as independent workshops promote mid-SAPs formulations to meet Euro 6 equivalents.

OEM co-branding and service-fill partnerships

Thailand’s dense assembly footprint enables lubricant manufacturers to secure volume through factory-fill agreements. PTT Lubricants leverages a domestic market share to secure after-sales contracts, thereby deepening customer loyalty throughout the vehicle lifecycle. Similar tie-ups in Indonesia channel automatic transmission fluid demand, which is growing at a 2.89% CAGR as automatic gearboxes penetrate mass-market segments. Co-branding also rolls out digital maintenance records that prompt timely lubricant changes, reinforcing repeat purchases.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Early EV uptake | −0.3% | Singapore, Australia, urban Malaysia | Medium term (2-4 years) |

| Counterfeit and unorganized retail channels | −0.2% | Indonesia, Philippines, Vietnam, Malaysia | Short term (≤ 2 years) |

| Import dependence for Group III/IV base-oils and additives | −0.4% | Thailand, Malaysia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Early EV uptake in Singapore and Australia

Battery-electric models displace engine oil demand in Singapore’s urban fleet and among Australian suburban commuters, trimming regional volumes. The heavy-duty and off-road sectors remain combustion-centric, which limits their overall impact. The shift, however, seeds opportunities in EV-specific greases and dielectric coolants, partially offsetting the loss of engine oil barrels. Suppliers are piloting low-viscosity fluids tailored to electric drivetrains, positioning themselves to capture value as EV penetration widens in the late 2020s.

Counterfeit and unorganized retail channels

Unlicensed brands erode consumer trust and depress legitimate sales, particularly in Indonesia and the Philippines. Malaysia’s SIRIM certification, which becomes mandatory from April 2025, introduces tamper-proof labels and penalties for violators. Enforcement raids have already seized a million worth of fake products since 2019. While compliance costs may squeeze smaller distributors, a cleaner retail environment should benefit branded players after the short-term adjustment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: engine oil dominance amid ATF uptrend

Automotive engine oil retained a 59.32% share of the Southeast Asia and Oceania automotive lubricants market in 2025, underscoring the region’s continued reliance on combustion powertrains. Synthetic and semi-synthetic blends captured incremental market share as OEMs mandated lower viscosities to meet fuel economy rules. Tropical climates accelerate oxidation, resulting in a high annual change frequency despite the use of longer drain technologies. Fleet managers are increasingly valuing extended-drain packages that reduce workshop downtime, thereby increasing premium penetration.

Automatic transmission fluids are forecast to post a 2.78% CAGR, the fastest among product categories. Rising automatic-vehicle uptake in Indonesia’s mass-market passenger segment and Thailand’s OEM assembly lines accelerates volume. Factory-fill contracts deepen penetration, while ride-hailing fleets refresh fluid more often to safeguard gearbox warranties. Manual transmission fluids and brake fluids notch steady single-digit growth, whereas grease demand benefits from industrial project pipelines.Shell tripled Thai grease capacity to 15,000 t per year in 2024, enough to supply over half of domestic needs and export to 40 regional markets [2]Shell Thailand, “Shell Enhances Production Capacity at Grease Manufacturing Plant,” shell.co.th.

By Vehicle Type: commercial fleet acceleration

Passenger cars accounted for 56.60% of the total volume in 2025, while commercial vehicles are expected to expand at the fastest rate, with a 2.92% CAGR through 2031. Logistics operators optimize the total cost of ownership by adopting low-ash synthetics, which lengthen oil intervals. Regional free-trade corridors spur cross-border trucking, intensifying lubricant duty cycles. Two-wheelers remain a distinct demand pillar in Indonesia and Vietnam, where motorcycle fleets surpass passenger car fleets. Frequent oil changes and high utilization rates amplify per-vehicle consumption, reinforcing baseline growth. The structural tilt toward fleet buyers channels sales through organized workshops, thereby boosting the share of branded multinationals with field engineering support.

Geography Analysis

Indonesia commanded 28.40% of Southeast Asia and Oceania's automotive lubricants market share in 2025, driven by its large population and indigenous refining capacity. Pertamina’s Balikpapan upgrade bolsters domestic base-oil supply and export potential. Jakarta’s push for biodiesel and Euro 4 compliance further accelerates the adoption of synthetic fuels.

Vietnam is projected to log the highest 4.23% CAGR from 2026 to 2031. Hanoi’s 2030–2045 automotive roadmap prioritizes local assembly, part localization, and supplier park development, expanding lubricant demand in both OE and aftermarket segments. Rising household incomes boost private vehicle sales, while infrastructure projects, such as the North–South Expressway, stimulate commercial vehicle utilization.

Thailand maintains steady growth as the regional manufacturing nexus. OEM proximity enables lubricant firms to embed factory-fill products and secure after-sales contracts. PTT Lubricants leverages its domestic share to penetrate ASEAN neighbors, underscoring Thailand’s role as a redistribution hub. Shell’s Thai grease plant supplies both domestic and export markets, highlighting the strength of intra-ASEAN supply chains.

Malaysia’s SIRIM mandate should shift volumes toward compliant brands, curbing grey-market leakage. Singapore, though tiny in volume, acts as a trading and blending hub thanks to Jurong Island’s additive cluster. Australia’s mature fleet favors synthetics and low-SAPs blends to satisfy Euro 6-equivalent standards, while New Zealand, Cambodia, and Myanmar represent still-nascent opportunities that hinge on broader economic development.

Competitive Landscape

The Southeast Asia and Oceania automotive lubricants market is moderately fragmented. Multinational majors continue to rationalize retail footprints while expanding high-margin blending and grease facilities. Shell’s negotiations to divest its Malaysian station network to Saudi Aramco illustrate the pivot toward upstream value pools. ExxonMobil’s Indonesian expansion and TotalEnergies’ PFAS-free grease launch demonstrate product-innovation bets aligned with regulatory trends. Strategically, suppliers emphasize: (1) proximity blending to cut lead times and hedge freight volatility; (2) specialty formulations that meet OEM drain and emissions requirements; and (3) sustainability credentials that resonate with corporate fleet tenders. Emerging digital supply-chain tools—such as QR-coded authenticity seals—further differentiate brands in markets plagued by counterfeit risks.

Southeast Asia And Oceania Automotive Lubricants Industry Leaders

Shell plc

BP p.l.c.

Exxon Mobil Corporation

PETRONAS Lubricants International

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TotalEnergies’ Lubrilog unveiled PFAS-free Plastogrease for automotive actuator applications, anticipating global regulatory curbs on PFAS compounds.

- June 2025: BP p.l.c. initiated the sale process for its Castrol lubricants division, valued at up to USD 10 billion, under a broader USD 20 billion divestment program aimed for completion by 2027.

Southeast Asia And Oceania Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| Malaysia |

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Philippines |

| Australia |

| Others (New Zealand, Cambodia and Myanmar) |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| By Geography | Malaysia | |

| Singapore | ||

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Philippines | ||

| Australia | ||

| Others (New Zealand, Cambodia and Myanmar) |

Key Questions Answered in the Report

How large will lubricant demand in Southeast Asia and Oceania be by 2031?

Volumes are projected to reach 2.7 billion litres by 2031, up from 2.37 billion litres in 2026.

Which product type grows fastest through 2031?

Automatic transmission fluids lead with a 2.78% CAGR, driven by the shift toward automatic gearboxes and OEM factory-fill contracts.

Why are commercial vehicles critical to future growth?

Logistics and e-commerce fleets expand at a 2.92% CAGR, exceeding overall market growth and boosting demand for high-specification synthetics.

Which country offers the highest volume opportunity today?

Indonesia holds 28.40% share in 2025 thanks to population scale and refinery upgrades that ensure secure domestic supply.

How will EV adoption affect lubricant suppliers?

EV uptake in Singapore and Australia trims engine-oil demand but opens niche opportunities in thermal-management fluids and EV-specific greases.

Page last updated on: