South Asia Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Volume (2025) | 2.95 Billion liters |

| Market Volume (2030) | 3.34 Billion liters |

| Growth Rate (2025 - 2030) | 2.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Asia Automotive Lubricants Market Analysis by Mordor Intelligence

The South Asia automotive lubricants market size is estimated at 2.95 billion liters in 2025, and is expected to reach 3.34 billion liters by 2030, at a CAGR of 2.52% during the forecast period (2025-2030). Sustained vehicle parc expansion, dedicated freight corridor roll-outs, and rising synthetic adoption underpin this measured trajectory, even as electrification slowly gains ground. India anchors regional demand with 84.90% volume share, while Bangladesh, Pakistan, and Sri Lanka deliver incremental growth through infrastructure modernization, policy liberalization, and renewed OEM activity. Engine oil leadership at 66.72% mirrors the region’s two-wheeler dominance and aging commercial fleets; yet, automatic-transmission fluids post the quickest gains as passenger and light-commercial models shift to automatic gearboxes. Competitive intensity remains moderate, characterized by international majors and domestic refiners establishing extensive distribution networks, pursuing OEM tie-ups, and defending margins against counterfeit incursions and fluctuations in the base-oil price.

Key Report Takeaways

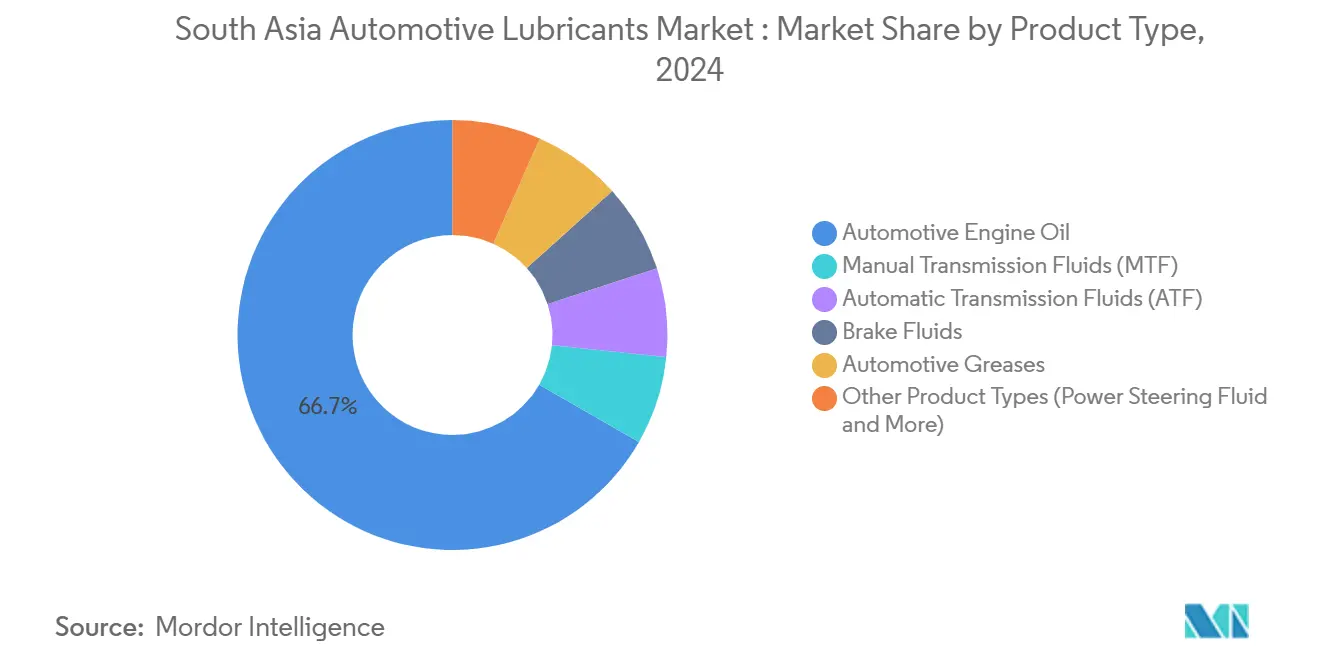

- By product type, automotive engine oil accounted for 66.72% of the South Asian automotive lubricants market share in 2024. Automatic transmission fluids are forecast to expand at a 2.67% CAGR and represent the fastest-growing product category to 2030.

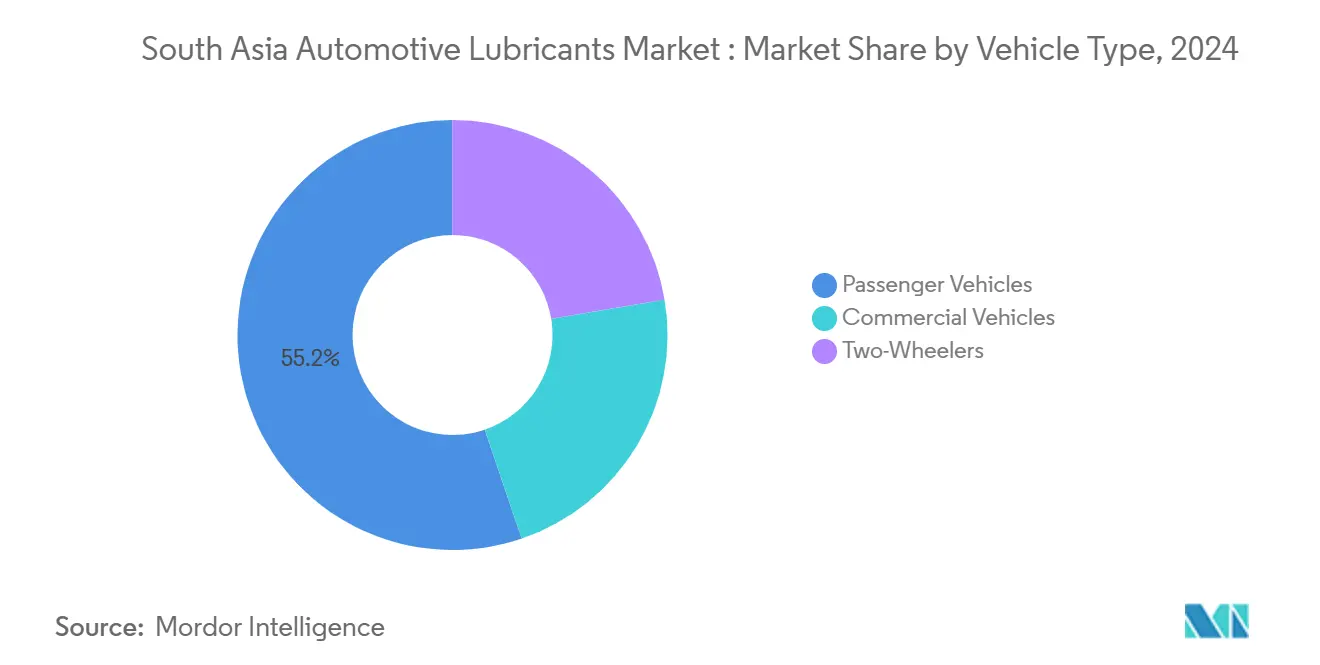

- By vehicle type, passenger vehicles accounted for 55.23% of consumption in 2024, while commercial vehicles are projected to advance at a 2.73% CAGR through 2030.

- India accounted for 84.90% of regional volume in 2024, and is expected to advance at a 2.55% CAGR through 2030.

South Asia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mobility corridors and freight demand | +0.8% | India core, spillover to Bangladesh and Pakistan | Medium term (2-4 years) |

| Expanding two-wheeler parc | +0.6% | India dominant; Bangladesh, Nepal emerging | Long term (≥4 years) |

| Premium-synthetic adoption | +0.4% | India urban centers, gradual regional spread | Medium term (2-4 years) |

| OEM service tie-ups | +0.3% | India and Pakistan primary markets | Short term (≤2 years) |

| Rural e-commerce distribution | +0.2% | India rural; early Bangladesh uptake | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Mobility Corridors and Freight Demand

Dedicated freight corridors in India, including the Eastern and Western alignments, are driving the deployment of heavy-duty trucks and increasing average route distances. Commercial-vehicle lubricant demand is therefore growing at a 2.73% CAGR, higher than the overall South Asia automotive lubricants market. Bangladesh’s industrial clusters and Pakistan’s CPEC projects replicate this push, creating secondary demand nodes that reinforce regional volume resilience. Higher-capacity trucks require longer drain cycles, accelerating fleet adoption of premium synthetic blends that promise fuel economy gains and downtime reduction. Multinational suppliers and domestic refiners are leveraging OEM telematics data to position long-drain formulations that align with fleet TCO benchmarks. The ensuing product-mix shift elevates average selling prices and cushions margin compression from import-linked base-oil costs.

Expanding Two-Wheeler Parc in India, Bangladesh, and Nepal

India’s 2025 GST cut on sub-350cc motorcycles catalyzes fresh demand among price-sensitive rural households, reinforcing the South Asia automotive lubricants market’s two-wheeler bedrock. Bangladesh reports 5 million motorcycles out of an 8.5 million vehicle fleet, while Nepal’s mountainous terrain entices commuters toward light, agile two-wheelers. These patterns sustain high-frequency oil-change cycles because of dusty environments and air-cooled engines that degrade lubricant viscosity. Suppliers respond with shear-stable, JASO-MA2-compliant blends tailored for urban stop-and-go riding and elevated operating temperatures. Over the long term, synthetic and semi-synthetic penetration in two-wheelers is expected to increase margins and reduce counterfeit volumes by leveraging QR-coded pack authentication schemes[1]Government of India, “GST Council Notification Reducing Motor-Cycle Rate,” gst.gov.in.

Premium-Synthetic Adoption for Fuel-Economy and Drain Extension

BS-VI emissions norms mandate the use of low-sulfur fuels and after-treatment compatibility, prompting OEMs to recommend Group III and poly-alpha-olefin base stocks. Synthetic formulations extend drain intervals to 15,000 km in many passenger-car and light-truck platforms, compared with 7,500 km for mineral oils. Fleets benchmark total cost of ownership and now calculate lubricant spend as a minor line item relative to downtime savings, supporting price premiums in an otherwise frugal market. Suppliers with in-house hydro-cracking facilities are integrating upstream to secure base-oil availability and hedge against import volatility. The South Asian automotive lubricants market, therefore, witnesses a gradual yet definitive shift toward higher-value blends[2]Ministry of Petroleum and Natural Gas, “Auto Fuel Vision Policy 2025,” petroleum.nic.in.

OEM-Service Tie-ups Steering Brand Choice

Lubricant marketers are increasingly relying on factory-fill contracts and branded service-center programs to secure repeat purchases. Gulf Oil’s extended partnership with Piaggio India, through 2030, deepens the brand's presence in the two- and three-wheeler ecosystem by embedding approved oils into dealer service menus. Such alliances ensure warranty compliance and simplify consumer choice, while enabling premium-tier pricing. In Pakistan, OEM endorsements help reinforce consumer trust amid rising cases of counterfeit products and quality concerns. Suppliers utilize shared digital platforms for service scheduling and oil-change reminders, thereby reinforcing loyalty and creating data-driven cross-selling opportunities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit/adulterated products | -0.4% | India, Bangladesh primary; Pakistan emerging | Short term (≤2 years) |

| Imported base-oil dependency | -0.3% | Bangladesh, Pakistan high exposure; India moderating | Medium term (2-4 years) |

| Foreign-exchange volatility | -0.2% | Pakistan, Bangladesh concentrated | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Counterfeit / Adulterated Products in Informal Retail

Seizures in West Bengal and Hyderabad have uncovered organized counterfeit rings selling sub-standard oils at discounts that tempt cash-constrained motorists. Bangladesh faces a 60% penetration of substandard products, which undermines engine life and erodes consumer trust in branded lubricants. Such proliferation drags the South Asia automotive lubricants market by 0.4 percentage points of forecast CAGR, mainly by depressing premium-segment uptake. OEMs now affix tamper-proof holograms, while enforcement agencies increase raids and impose harsher penalties. Genuine suppliers collaborate with e-commerce channels to trace product provenance and promote QR-based validation at the point of sale

Imported Base-Oil Dependency and Price Swings

Limited domestic refining in Bangladesh and Pakistan forces blenders to import Group I and II base stocks, exposing them to fluctuations in freight and currency. Asian refinery turnarounds in 2024-2025 tightened supplies, elevating Group I spot quotes to USD 800-900 per metric ton and squeezing blender gross margins. India partially offsets the risk through upcoming 0.5-2.4 million barrels per day refining additions, which could turn it into a regional export hub. Suppliers adopt hedging and term contracts; however, the cost pass-through to end-users remains constrained by price-sensitive demand, which mutes overall market value expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Leadership Sustains Volume Momentum

Automotive engine oil consumption accounted for 66.72% of South Asia's automotive lubricants market share in 2024, underscoring its criticality across the region’s two-wheeler and light-commercial vehicle fleets. Rising vehicle complexity, notably turbocharged gasoline direct-injection engines and BS-VI after-treatment systems, has led to a shift in viscosity grades toward 5W-30 and 0W-20 synthetic blends. Meanwhile, automatic-transmission fluids are the fastest-growing category, advancing at a 2.67% CAGR to 2030, reflecting the gradual diffusion of AT gearboxes into mid-segment passenger cars. Conventional manual-transmission fluids and automotive greases continue to maintain steady demand due to the entrenched dominance of manual gearboxes and the need for heavy-equipment lubrication in infrastructure construction.

OEM-driven viscosity shifts and extended drain intervals create scope for premium synthetic positioning and product differentiation. Formulators invest in high-VI Group III base-oil back-integration to secure supply and enhance additive package compatibility. Brake-fluid demand benefits from the proliferation of anti-lock braking systems, while niche products like power-steering fluids track the electrification trend that slowly reduces hydraulic systems but introduces new coolant needs for electric drivetrains. Overall, product-mix evolution supports upward movement in average selling prices, cushioning volume growth that trails the broader automotive sector.

By Vehicle Type: Commercial-Vehicle Growth Outpaces Passenger-Car Volumes

Passenger vehicles retained 55.23% volume leadership in 2024, yet commercial vehicles registered a 2.73% CAGR through 2030, outstripping the broader South Asia automotive lubricants market. Dedicated freight corridors, e-commerce logistics, and infrastructure projects are placing larger, higher-horsepower trucks on increasingly longer routes, thereby raising lubricant demand per vehicle. Fleets adopt premium long-drain heavy-duty engine oils and low-viscosity driveline fluids to minimize service downtime. Two-wheelers, although mature, remain a critical anchor segment, particularly in rural and peri-urban regions, where motorcycles serve as the primary mode of mobility.

Synthetic penetration in passenger-car and commercial-vehicle segments rises under OEM warranty conditions that mandate specific API and ACEA performance tiers. For two-wheelers, upgrades from monograde mineral to semi-synthetic multigrade drive modest but meaningful value uplift. The combined effect of more sophisticated formulations and heightened fleet-maintenance standards sustains the South Asia automotive lubricants market size trajectory, even as electrification nibbles at long-term demand for ICE lubricants.

Geography Analysis

India’s 84.90% volume dominance in 2024 cements its role as the epicenter of South Asia's automotive lubricants market development. Domestic refining expansions, including planned additions of up to 2.4 million barrels per day by 2028, enhance self-sufficiency and pave the way for export positioning to smaller neighbors. BS-VI norms, widespread two-wheeler ownership, and progress on dedicated freight corridors are expected to uphold a 2.55% CAGR, while rural e-commerce channels extend authentic product reach to deepen penetration in smaller towns and villages. Counterfeit-control initiatives and QR-coded packaging shift consumer confidence toward branded synthetics, expanding premium uptake.

Bangladesh offers the next-largest opportunity pocket, albeit from a smaller base, as industrialization accelerates and vehicle registrations climb. The sizable presence of sub-standard oil—estimated at 60% of market volume—creates headroom for quality-assured brands to gain traction through awareness campaigns and stricter port inspections. OEM workshops and hyperlocal e-commerce delivery address authenticity concerns, steering a gradual migration toward API SP-grade formulations suited to hotter climates and stop-and-go traffic.

Pakistan’s lubricant landscape is in transition following Shell’s divestment announcement in June 2024. Consolidation prospects favor domestic energy giants and agile regional players equipped to navigate deregulated fuel pricing and volatile forex markets. Government crackdowns on illegal solvent imports seek to stem engine-damage incidents and rebuild trust in certified products. Sri Lanka, though smaller, presents targeted opportunities in two-wheeler and three-wheeler fleets, where Ceylon Petroleum Corporation competes against Sinopec and Indian Oil for share gains. The nation’s post-crisis economic stabilization and port expansion could augment heavy-vehicle lubricant demand in coming years.

Regional connectivity via SAARC trade initiatives and bilateral agreements smooths cross-border movement of finished lubricants and base oils. India’s refining overhang positions it as a future supply hub, mitigating Bangladesh’s and Pakistan’s import vulnerabilities, and supporting the South Asia automotive lubricants market’s long-term resilience.

Competitive Landscape

The South Asia automotive lubricants market is moderately consolidated. Domestic majors, such as Indian Oil, leverage integrated refining, extensive retail networks, and public-sector vehicle contracts to maintain their share. Multinational companies compete through differentiated synthetic portfolios and OEM endorsements. Distribution reach remains the decisive battleground. E-commerce channels, from Flipkart’s automotive category to specialized platforms like myTVS Hypermart, open direct-to-consumer pathways that favor brands capable of managing rapid logistics and tamper-proof packaging. Product innovation centers on extended-drain synthetics, BS-VI compliant low-ash formulations, and emerging e-fluid lines for hybrid and electric vehicles. Counterfeit mitigation underscores the importance of track-and-trace technology, with several players adopting blockchain-enabled serial number authentication. Quality-led consolidation could raise entry barriers for smaller blenders dependent on imported Group I base oils, further tilting the field toward vertically integrated refiners and global specialty formulators.

South Asia Automotive Lubricants Industry Leaders

Indian Oil Corporation Ltd

BP p.l.c.

Bharat Petroleum Corporation Limited

Hindustan Petroleum Corporation Limited

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Gulf Oil renewed its partnership with Piaggio India through 2030, expanding BS-VI–compliant oils and new electric-vehicle fluid lines

- June 2024: Shell announced the sale of its 77.42% stake in Shell Pakistan, signaling a strategic market exit and facilitating sector consolidation

South Asia Automotive Lubricants Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| India |

| Bangladesh |

| Sri Lanka |

| Pakistan |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | India | |

| Bangladesh | ||

| Sri Lanka | ||

| Pakistan | ||

Key Questions Answered in the Report

How big is the South Asia automotive lubricants market in 2025?

The market stands at 2.95 billion liters in 2025 and is projected to climb to 3.34 billion liters by 2030.

Which product type leads regional demand?

Automotive engine oil dominates the market with a 66.72% share, driven by the vast two-wheeler and light-commercial vehicle fleets in India and neighboring markets.

What segment is growing the fastest?

Automatic-transmission fluids register a 2.67% CAGR through 2030 as automatic gearboxes gain traction in passenger and light-commercial vehicles.

Why are synthetic lubricants gaining ground?

OEM BS-VI requirements, extended drain intervals of up to 15,000 km, and fleet fuel economy targets are driving the adoption of synthetic oils, despite higher price points.

How does counterfeit activity affect the market?

Counterfeit oils erode consumer trust and suppress premium uptake, dragging forecast CAGR by an estimated 0.4 percentage points until enforcement and authentication measures curb illicit trade.

What impact will India’s refinery expansions have?

An additional 0.5-2.4 million barrels-per-day capacity by 2028 will reduce import dependence, stabilize base-oil supply, and position India as a potential export hub for neighboring countries.

Page last updated on: