South America Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

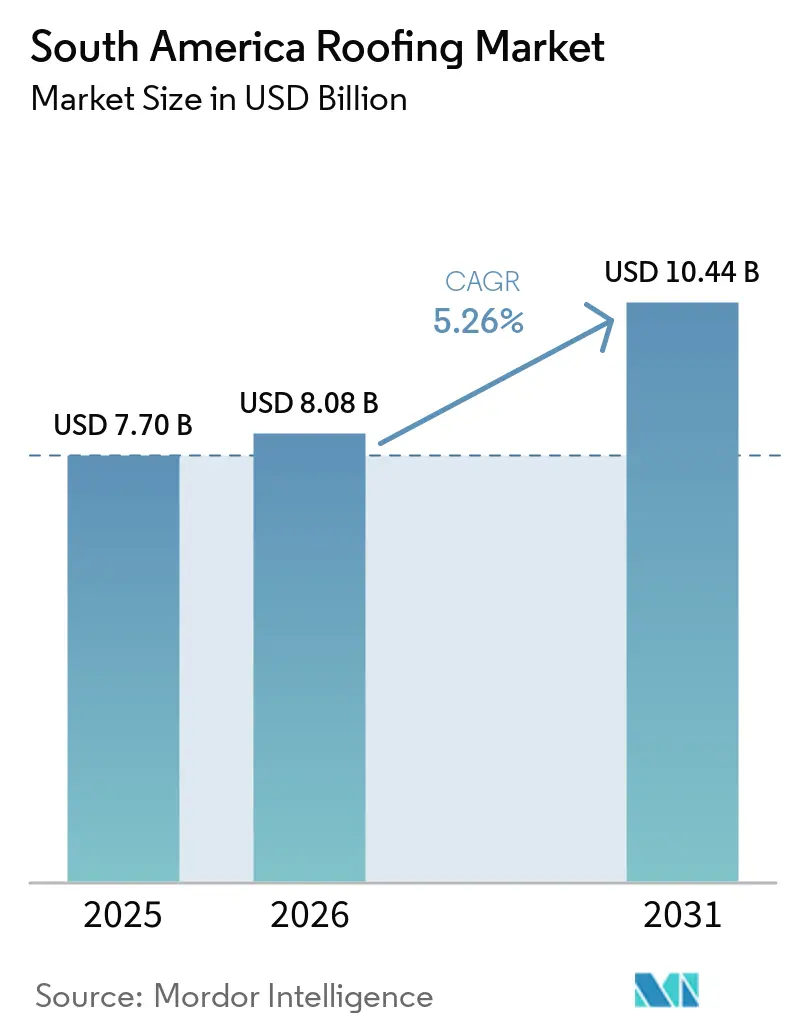

| Base Year Market Size (2025) | USD 7.70 Billion |

| Market Size (2026) | USD 8.08 Billion |

| Market Size (2031) | USD 10.44 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Roofing Market Analysis by Mordor Intelligence

The South America Roofing Market size is projected to be USD 7.70 billion in 2025, USD 8.08 billion in 2026, and reach USD 10.44 billion by 2031, growing at a CAGR of 5.26% from 2026 to 2031.

The South America roofing market is being supported by a persistent housing shortage in Brazil, Colombia, and Peru, while the region’s older tile-heavy housing stock is also moving deeper into a replacement cycle. Brazil’s Minha Casa, Minha Vida program selected 130,000 new housing units in May 2025, keeping a meaningful pipeline of roofing projects in place for suppliers even when private financing conditions remain tight. This pattern matters because subsidized housing acts as a buffer for the South America roofing market when higher interest rates slow commercial and middle-income private construction. At the same time, tighter thermal performance rules in Chile and Colombia, and growing industrial demand for insulated metal systems are lifting the value mix toward more technical roofing products. The main short-term pressure on the South America roofing market comes from Brazil’s 15% Selic rate in early 2026 and steel cost increases tied to anti-dumping duties, both of which weigh on private project starts and metal roofing margins.

Key Report Takeaways

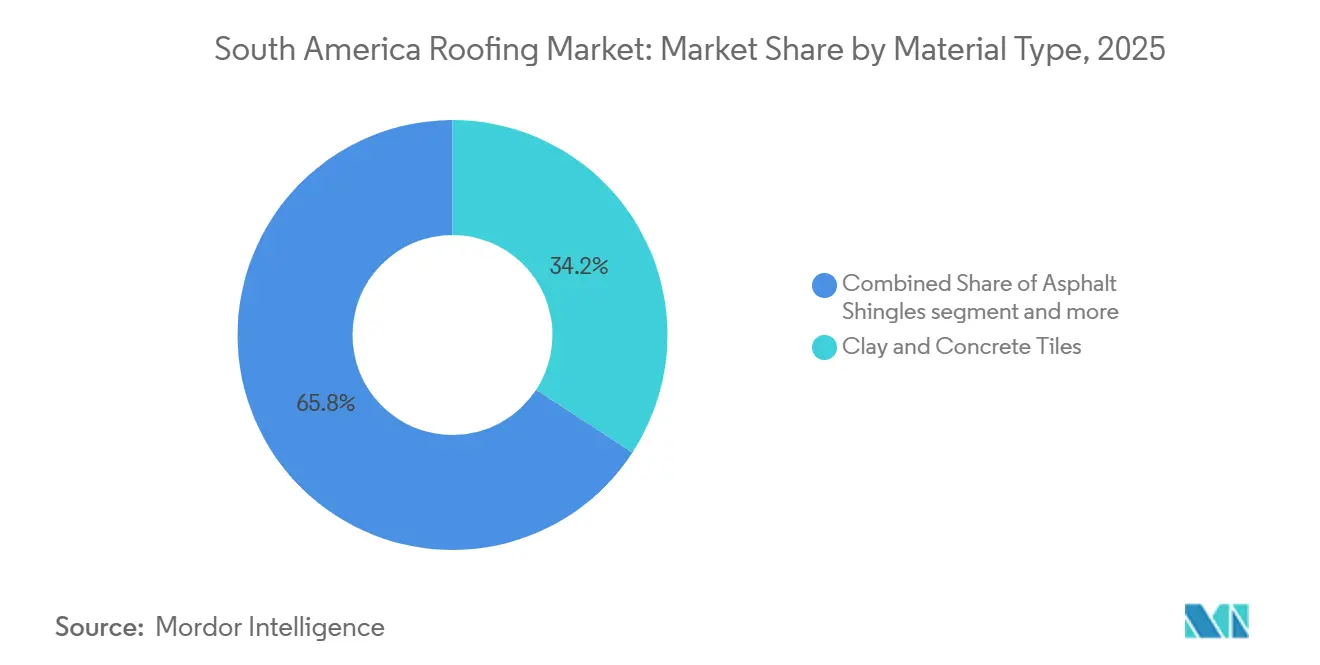

- By material type, clay & concrete tiles led with 34.2% of the South America roofing market share in 2025, while metal roofing recorded the highest projected CAGR at 6.4% through 2031.

- By construction type, reroofing and replacement held 55.7% of the South America roofing market size in 2025, while new construction is forecast to expand at a 5.9% CAGR through 2031.

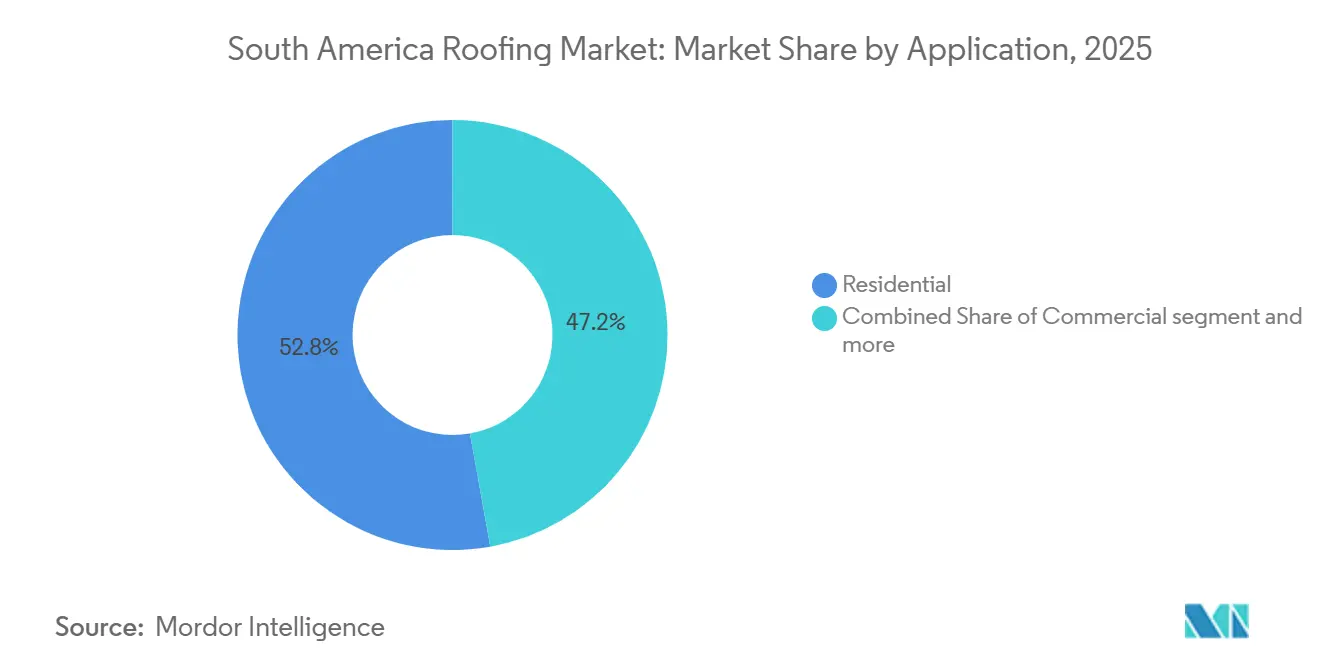

- By application, residential roofing accounted for a 52.8% share of the South America roofing market size in 2025, while industrial roofing is advancing at a 6.1% CAGR through 2031.

- By geography, Brazil held 48.6% of the South America roofing market share in 2025, while Colombia is forecast to post the fastest regional growth at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized Housing Pipelines and Housing Backlog | +1.4% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| Replacement Demand from Aging Tile-Heavy Roof Stock | +1.1% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Metal and Insulated Roofing Adoption in Industrial Buildings | +0.8% | Brazil, Peru, Argentina, Chile | Short term (≤ 2 years) |

| Tightening Roof Thermal Efficiency Standards | +0.7% | Chile, Colombia, Brazil | Medium term (2-4 years) |

| Climate-Resilience Reroofing After Extreme Weather Events | +0.6% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Cool-Roof Retrofit Economics in Hot-Climate Cities | +0.5% | Brazil, Colombia, Ecuador | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidized Housing Pipelines and Housing Backlog

Brazil’s Minha Casa Minha Vida program selected 130,000 new housing units in May 2025 for families with a monthly gross income below BRL 2,850 (USD 502)[1]Secretaria de Comunicação Social, “Governo Federal Anuncia a Seleção de 130 Mil Novas Unidades Habitacionales Pelo Minha Casa, Minha Vida,” Brazilian Federal Government, gov.br. The same announcement set per-unit subsidy ceilings at BRL 140,000 (USD 24,659.6) to BRL 180,500 (USD 31,793.3). This structure keeps a demand corridor open for the South America roofing market because a large share of roofing demand in subsidized housing is not tied to standard mortgage availability. Comparable affordable housing channels in Colombia and Peru create a broader regional base for entry-level residential roofing demand within the South America roofing market. The mix in this channel is also shifting, with tighter unit sizes and cost ceilings favoring fiber-cement and flat concrete systems over traditional ceramic clay tiles. Manufacturers that already expanded capacity for this tier are in a stronger position, and Eternit’s BRL 187 million (USD 32.9 million) Caucaia plant completed its first full year of nominal-capacity operation in 2024, reinforcing that supply-side advantage.

Replacement-Led Demand from Aging Tile-Heavy Roof Stock

A large share of South America’s residential buildings were erected before 2000, when roofing durability and thermal performance were not consistently addressed as they are today. As clay and ceramic roofs installed during the 1980–2000 building cycle age past 30 years, replacement demand is becoming more systematic across Brazil, Argentina, and Colombia. This matters for the South America roofing market because homeowners replacing old roofs are increasingly choosing fiber cement, coated metal, or lightweight concrete instead of direct ceramic replacements. That trade-up pattern is already visible in Brazil, where Eternit’s Q1 2025 fiber-cement roofing panel sales rose 15.1% year on year to 167,600 tonnes, with gains linked in part to North and Northeast Brazil, where older roofs are being replaced. The replacement cycle also expands the revenue pool for the South America roofing market because reroofing projects often include underlayments, ridge capping, and improved fastening systems rather than only the visible roof covering.

Metal and Insulated Roofing Adoption in Industrial Buildings

The adoption of metal and insulated roofing in industrial buildings is supporting growth in the South American roofing market across Brazil, Peru, Argentina, and Chile. As logistics warehouses, cold-storage facilities, agro-industrial buildings, and mining-support assets demand faster installation, greater durability, and superior thermal control, a noticeable shift is occurring. These requirements often surpass what traditional corrugated sheet systems can offer. In industrial projects, operators are increasingly opting for insulated polyisocyanurate and expanded polystyrene core panel systems over basic metal roofing to reduce heat loads and achieve more consistent indoor conditions. Chile’s tighter thermal rules are also reinforcing this move by making roof performance more important at the design and permit stage in regulated building categories. Supplier investments support the same direction, with Kingspan opening a USD 20 million insulated panel factory in Paraguay in June 2025 to serve nearby markets, including Brazil and Argentina, while Etex committed EUR 65 million (USD 74 million) across Peru, Chile, and Argentina to expand capacity for construction solutions. As more industrial tenants prioritize energy performance and compliance, metal and insulated systems are gaining share because they offer a clearer value proposition than commodity roofing in high-use buildings.

Tightening Roof Thermal Efficiency Standards

Chile’s updated thermal regulation under Article 4.1.10 of the Ordenanza General de Urbanismo y Construcciones (OGUC) took effect on November 28, 2025, and set stricter thermal transmittance and resistance requirements for roofs, walls, and ventilated floors in new residential, education, and health buildings. Colombia reinforced this direction with Resolution 194 of 2025, which introduced minimum energy-efficiency requirements and a sustainable construction guide that includes roof insulation measures for new buildings. These rules are reshaping the South America roofing market because compliance is assessed at permit submission, so roofing systems now have to be specified correctly before projects enter construction. That shifts purchase decisions away from simple price comparisons and toward documented thermal performance, which supports insulated panels, reflective metal systems, and higher-mass tile solutions. Manufacturers that provide technical documents and installer guidance are gaining more influence in the South America roofing market, and Cintac has already turned Chile’s new standard into a customer-facing compliance support theme.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest Rates Limiting Private Construction Starts | -1.5% | Brazil, Argentina | Short term (≤ 2 years) |

| Input-Cost Volatility in Steel, Membranes, and Asphaltic Products | -0.8% | Brazil, Chile, Colombia, regional spill-over | Medium term (2-4 years) |

| Installer Capability Gaps for Advanced Roofing Systems | -0.5% | Bolivia, Ecuador, Venezuela, rural Brazil | Long term (≥ 4 years) |

| Informal Self-Build Channel Slows Premium-System Adoption | -0.4% | Brazil Northeast, Bolivia, Paraguay, Venezuela | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest Rates Limiting Private Construction Starts

Brazil’s Selic rate stood at 15% in early 2026, which was the highest level since 2006 and a clear constraint on private construction activity[2]Valor Internacional, “Construction Sector Bets on Boost From Lower Interest Rates,” Valor Internacional, valorinternacional.globo.com. New construction starts fell by 6.2% through mid-2025 across all Brazilian regions, keeping pressure on mid-income private construction projects. Developers are also dealing with financing costs at Selic plus 3% to 3.5% and with household purchasing power that has not kept pace with construction cost inflation. In the South American roofing market, that means slower order conversion in private housing and longer project timelines for developers targeting middle-income buyers. Even so, the Central Bank’s Focus survey in March 2026 pointed to a year-end Selic rate of 12.13%, suggesting some easing risk if rate cuts materialize later in the period.

Input-Cost Volatility in Steel, Membranes, and Asphaltic Products

Brazil imposed anti-dumping duties in 2026 ranging from USD 284.98 to USD 709.63 per tonne on flat-steel imports, which immediately lifted galvanized coil and galvalume prices by USD 10 to USD 30 per tonne. That matters because metal roofing sheet producers in the South America roofing market often bid fixed-price contracts well before material purchases are locked in. Regional steel supply has also tightened, and Latin America’s output in 2025 was materially below 2010 levels, leaving less domestic buffer when global pricing shifts. Modified bitumen and related membrane products face similar pressure because petrochemical inputs move with crude oil and natural gas prices. These cost swings are a direct restraint on the South American roofing market because passing through higher prices is more difficult in residential channels, where low-cost alternatives and informal supply remain active.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Metal Roofing Accelerates as Industrial Demand Reshapes the Mix

Clay & concrete tiles held a 34.2% value share in 2025, making them the largest material group in the South American roofing market. Their leading position remains strongest in Brazil, Argentina, and Colombia, where ceramic roofing continues to align with local building practices and entry-level residential budgets. Metal roofing is the fastest-growing material segment with a 6.4% CAGR through 2026-2031, and that rate is closely tied to logistics warehouses, cold storage, mining-support assets, and agro-industrial buildings. The South America roofing market size for clay & concrete tiles remained anchored by mass-market residential demand. At the same time, the growth premium shifted toward coated and insulated metal systems in non-residential projects. Thermal regulations in Chile and Colombia are reinforcing this move, as industrial and institutional buyers now need better-documented roof performance from the outset of project design.

Fiber cement remains the main affordable residential roofing alternative in the South America roofing market, with Brazil representing one of the largest and most established fiber-cement roofing markets in the region. As one of the leading manufacturers, Eternit reported full-year fiber-cement sales volume of 633,242 tonnes in 2024, highlighting the significant scale and depth of the segment in Brazil. Bituminous and modified bitumen membranes continue to dominate many flat commercial roofs, while single-ply systems, especially Thermoplastic Polyolefin (TPO), are gaining adoption in newer projects that prioritize solar reflectivity and seam reliability. Ethylene Propylene Diene Monomer (EPDM) remains relevant in premium commercial applications, while Polyvinyl Chloride (PVC) continues to be important in environments where chemical resistance is required. Asphalt shingles and wood roofing keep smaller positions in the South America roofing market, with shingles tied to urban renovation niches and wood limited by fire-risk concerns in broader adoption.

By Construction Type: Reroofing and Replacement Dominance Reflects Retrofit and Upgrade Dynamics

Reroofing and replacement held a 55.7% value share in 2025, making this the largest construction-type segment in the South America roofing market. That lead reflects old building stock, growing repair needs, and tighter thermal compliance in Chile, Colombia, and parts of Brazil. New construction is the faster-growing segment with a 5.9% CAGR through 2031, supported by social housing, industrial buildouts, and logistics investment. The South America roofing market size linked to replacement work is especially valuable because reroofing contracts usually include tear-off labor, underlayment repair, and better-performing materials rather than simple like-for-like replacement. This gives the replacement segment more pricing depth per square meter than its headline share alone suggests.

Bundling behavior is also boosting spending in the South American roofing market because many owners now treat reroofing as an opportunity to add insulation, waterproofing improvements, or solar mounting readiness. That trend broadens suppliers' revenue mix by allowing them to sell complete systems rather than just roof coverings. New construction still matters because Peru, Chile, Brazil, and Colombia continue to show investment activity in industrial, logistics, and public-use buildings that are less tied to household mortgage cycles. The South America roofing industry also benefits from compliance-led replacement triggers in formal urban markets, where performance standards are becoming harder to avoid during property upgrades and regulated transactions. Insurance-led storm repairs after events in Rio Grande do Sul and Catamarca should keep supporting replacement demand even when private new-build activity stays uneven.

By Application: Industrial Emerges as the Premium Growth Frontier

Residential roofing retained a 52.8% application share in 2025, which kept it as the largest use case in the South America roofing market. The base remains broad because social housing, self-build activity, and replacement cycles continue to drive large roof-area volumes across Brazil and Colombia. Industrial roofing is the fastest-growing application with a 6.1% CAGR through 2031, supported by warehousing, food processing, agro-industry, cold storage, energy infrastructure, and data-oriented facilities. The South America roofing market size for industrial projects is gaining value faster than volume because insulated polyisocyanurate and expanded polystyrene panel systems carry a higher price per square meter than most residential materials. That pricing gap is one reason industrial roofing is closing ground on residential value share, even though residential remains larger today.

Commercial roofing remains the second-largest non-residential outlet, supported by retail, office, and hospitality projects in large metropolitan areas. Institutional demand also stays durable because schools, hospitals, and public facilities increasingly require roofing systems that meet energy, durability, and documentation standards. Etex’s USD 74 million investment plan across Peru, Chile, and Argentina signals confidence in those medium-term building categories. Kingspan’s USD 20 million factory opening in Paraguay in June 2025, along with its planned Leme, Brazil plant, shows that suppliers are preparing for longer industrial demand depth in the South America roofing market[3]Kingspan Isoeste, “Kingspan Inaugura Nova Fábrica em Itá e Fortalece Presença Industrial na América do Sul,” Kingspan Isoeste, kingspan-isoeste.com.br. Single-ply membranes and modified bitumen remain strong in commercial and institutional flat roofs. At the same time, metal panel systems dominate industrial projects and are moving into large-format mixed-use projects where energy efficiency matters more.

Geography Analysis

Brazil held 48.6% of the South America roofing market share in 2025, which made it the clear anchor for regional demand. That position reflects the combination of social housing deliveries, replacement demand, cold-chain expansion, and agro-industrial construction. The South America roofing market is especially deep in Brazil because demand is spread across low-cost residential, industrial sheds, logistics assets, and retrofit work rather than depending on one narrow end use. Brazil also remains the country where policy support and financing stress coexist most clearly, since subsidized housing supports volume while high interest rates still suppress part of the private pipeline.

Colombia is the fastest-growing geography in the South America roofing market with a 6.8% CAGR through 2031. Its growth profile is being shaped by urban housing demand, industrial expansion, and tighter building performance requirements, which make better roof specification more important in new projects. Chile adds a different layer because the OGUC thermal rule now requires stronger roof performance in regulated building types, which is raising the minimum quality threshold in new construction. Cintac has already responded with technical guidance tied to the updated rule, showing how local manufacturers can turn regulation into a commercial tool. Peru is emerging as a logistics and industrial roofing node, and Sika’s Lima plant commissioned in April 2024 supports a wider construction supply footprint in the Andean corridor.

Argentina remains important because its Pampas agro-industrial base and large urban centers continue to support demand for metal, tile, and membrane systems. Paraguay is becoming more relevant to the South America roofing market as a manufacturing base, with Kingspan’s Itá plant giving the country a stronger role in insulated panel supply for both domestic and neighboring markets. Uruguay continues to function as a smaller but higher-specification destination for premium metal and membrane products. Venezuela, Guyana, Suriname, Ecuador, and Bolivia are smaller contributors, but they still provide pockets of demand tied to reconstruction, import substitution, and resource-linked infrastructure.

Competitive Landscape

The South America roofing market is moderately consolidated at the manufacturing level, with a mix of established regional and international producers competing alongside numerous local manufacturers, distributors, and installers. Large companies compete through scale of production, technical expertise, product innovation, and broad distribution networks. At the same time, local firms maintain their positions through regional presence, pricing flexibility, faster delivery, and strong customer relationships. Fiber cement remains a key roofing material across the region, particularly in the residential sector, supporting the presence of major manufacturers such as Eternit.

Leading companies continue to strengthen their positions through capacity expansion, product diversification, and investments in manufacturing and distribution infrastructure. Saint-Gobain is expanding its focus on industrial, commercial, and specification-driven projects, while Kingspan is increasing its regional footprint through investments in manufacturing facilities in South America. Etex is reinforcing its presence through investments across multiple countries in the region, while Sika continues to broaden its reach through distribution and channel development initiatives. As technical standards and performance requirements become more important, manufacturers that provide engineering support, documentation, warranties, and installer training are gaining a competitive advantage.

Despite the presence of large manufacturers, domestic companies such as Imbralit, Ternium, Cintac, Viapol, Dânica, Rooftec Telhas Metálicas, and Brastetto continue to play an important role through strong local coverage and established customer relationships. Growth opportunities remain in cool-roof retrofits, broader adoption of single-ply membrane systems across the region, and Building-Integrated Photovoltaic (BIPV) roofing solutions for industrial and commercial applications. As a result, the market remains moderately consolidated, with leading manufacturers holding strong positions while local participants continue to influence competition across distribution and installation activities.

South America Roofing Industry Leaders

Eternit

Saint-Gobain Brasilit

Imbralit

Etex

Kingspan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saint-Gobain inked a deal to divest its Brazilian construction materials distribution chain, Telhanorte, to Tauá Partners. This sale marks Saint-Gobain's full retreat from Brazil's distribution scene, following its prior divestment of Tumelero. The decision underscores Saint-Gobain's pivot towards bolstering its industrial building-material operations, notably roofing brands like Brasilit, all while refining its portfolio in Latin America.

- March 2026: Saint-Gobain unveiled its latest innovations in roofing and lightweight construction at Expo Revestir 2026. The company, through its brands Brasilit, Isover, and Placo, showcased a suite of integrated roofing, insulation, and sustainable construction systems. The exhibition underscored a growing emphasis on energy-efficient roofing and integrated envelope systems across South America.

- March 2026: Holcim completed the acquisition of a majority stake in Cementos Pacasmayo, marking Holcim’s largest Latin American acquisition to date. The deal strengthens Holcim’s construction materials and roofing solutions footprint in Peru and supports broader regional expansion under its NextGen Growth 2030 strategy.

South America Roofing Market Report Scope

The South America Roofing Market is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and more), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, and more), & Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is driving roofing demand in South America through 2031?

Demand is being supported by a housing backlog, strong reroofing activity, and industrial demand for insulated metal systems. The market is expected to reach USD 10.44 billion by 2031 at a 5.26% CAGR.

Which roofing material is growing fastest in South America?

Metal roofing is the fastest-growing material segment, with a 6.4% CAGR through 2031. Growth is tied to warehouses, cold storage, mining-support buildings, and thermal compliance needs.

Why does reroofing hold such a large share of regional demand?

Reroofing and replacement accounted for 55.7% of value in 2025 because a large part of the region’s roof stock is aging and many projects now combine replacement with insulation and waterproofing upgrades.

Which application is creating the highest-value opportunities for suppliers?

Industrial roofing is creating the premium growth opportunity, with a 6.1% CAGR through 2031. Insulated panel systems used in logistics and industrial buildings carry a higher value per square meter than most residential materials.

Page last updated on: