Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

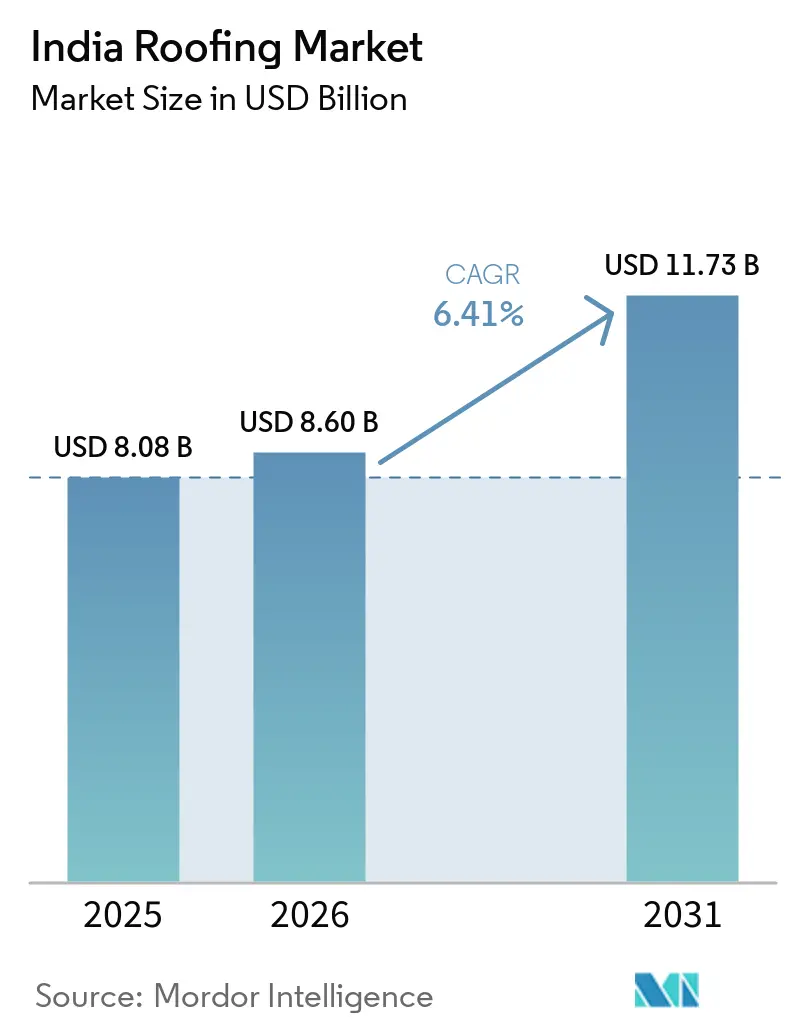

| Base Year Market Size (2025) | USD 8.08 Billion |

| Market Size (2026) | USD 8.60 Billion |

| Market Size (2031) | USD 11.73 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

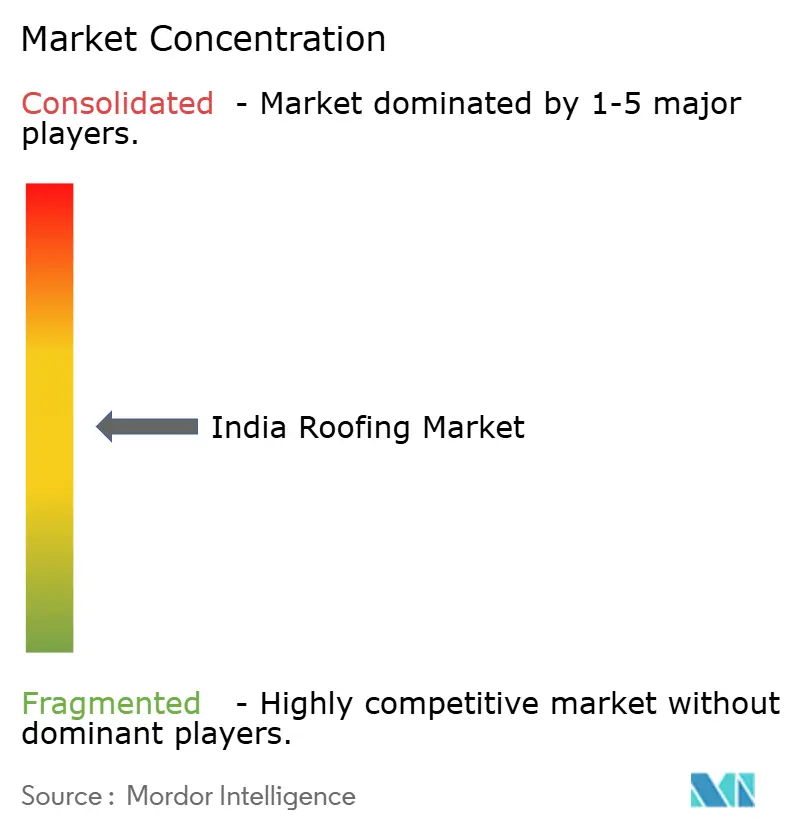

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Roofing Market Analysis by Mordor Intelligence

The India Roofing Market size is expected to grow from USD 8.08 billion in 2025 to USD 8.6 billion in 2026 and is forecast to reach USD 11.73 billion by 2031 at 6.41% CAGR over 2026-2031. The growth trajectory reflects simultaneous momentum from rapid urbanization, government infrastructure mandates, and climate-adaptation policies that are changing material preferences and adoption patterns. Residential construction remains the leading demand center, but technology-rich commercial, industrial, and infrastructure projects are accelerating the shift toward premium membranes and solar-ready solutions. Manufacturers are responding through vertical integration, capacity additions, and direct-forming innovations that shorten lead times and improve cost control. Competitive intensity is rising as new entrants expand metal sheet capacity while established players enrich portfolios with cool-roof coatings and energy-efficient assemblies.

Key Report Takeaways

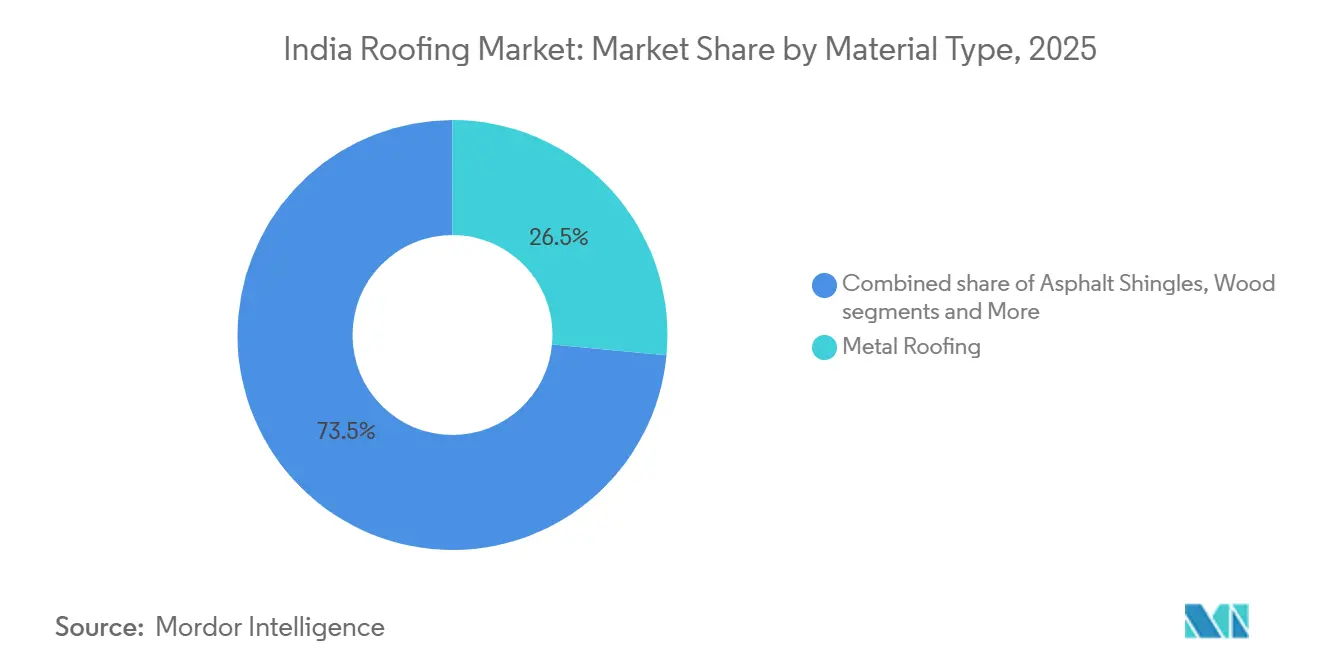

- By material type, Metal Roofing led with 26.5% share in 2025, while Bituminous / Modified Bitumen Membranes is forecast to expand at 8.20% CAGR through 2031.

- By construction type, New Construction held 71% share in 2025, while Reroofing and Replacement is projected to grow at 7.44% CAGR through 2031.

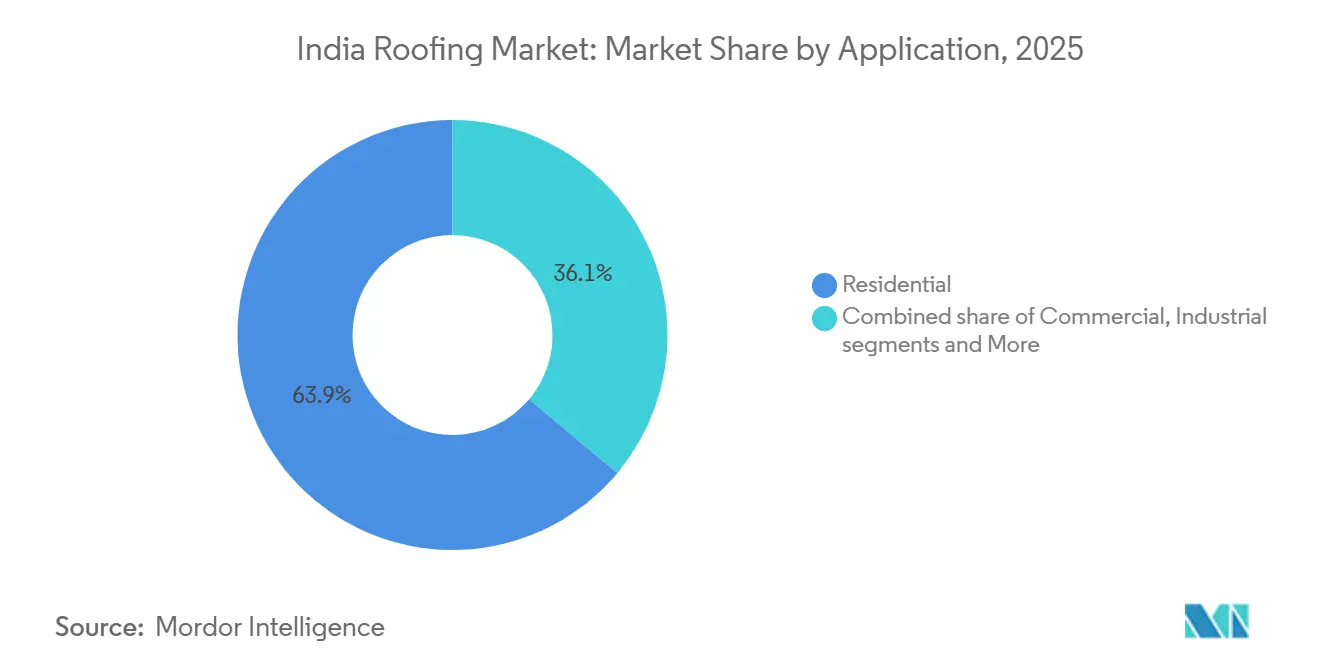

- By application, Residential accounted for a 63.92% share in 2025 and is also the fastest-growing application, with an 8.59% CAGR through 2031.

- By geography, South India held 31.5% share in 2025, while North India is projected to grow at 7.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & middle-class expansion | +1.2% | National, with early gains in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Rapid urbanization & construction boom | +0.8% | North India, West India, with spillover to South India | Short term (≤ 2 years) |

| Government infrastructure initiatives (Smart Cities Mission, PMAY) | +0.6% | National, concentrated in mission cities and PMAY beneficiary states | Medium term (2-4 years) |

| Solar-rooftop subsidies accelerating metal sandwich demand | +0.4% | National, with early adoption in Gujarat, Rajasthan, Maharashtra | Short term (≤ 2 years) |

| Climate-resilience mandates in coastal states | +0.3% | Coastal states (Gujarat, Maharashtra, Tamil Nadu, Odisha, West Bengal) | Long term (≥ 4 years) |

| State-level "cool roof" policies for urban heat mitigation | +0.2% | Urban centers in North India and West India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Middle-Class Expansion

Higher disposable income is steering homeowners toward premium membranes that promise extended service life and lower cooling costs. The government’s PMAY program has delivered 1.18 crore homes under its urban component and 2.95 crore under its rural arm, creating a large installed base ready for upgrades. Tier-2 and Tier-3 cities now account for a growing share of specification-rich projects where thermoplastic polyolefin (TPO) and EPDM membranes displace commodity asphalt sheets. Manufacturers are amplifying dealer training to capture this latent demand, while financiers are piloting easy EMI plans that ease the adoption of costlier but more durable systems[1]Pratima Joshi, “PMAY-Urban: Houses Completed as on March 2025,” Ministry of Housing & Urban Affairs, mohua.gov.in.

Government Infrastructure Initiatives (Smart Cities Mission, PMAY)

PMAY’s standardized roofing templates allow scale-driven manufacturers to amortize investments in automated roll-forming lines. Simultaneously, Smart Cities projects impose green-building scorecards that popularize cool-roof pigments and solar-ready fasteners. Vendors able to localize specifications for climate zones, humid coastal, dry arid, or temperate northern win repeat orders from state agencies. The convergence of mass housing and smart municipal assets, therefore, gives the India roofing market multiple predictable revenue streams and an incentive to upgrade digital sales channels that track subsidy availment for end users.

Solar-Rooftop Subsidies are Accelerating Metal Sandwich Demand

The PM Surya Ghar rooftop program has already disbursed INR 4,770 crore (USD 572 million) and targets 1 million installations by March 2025. Metal sandwich panels with pre-punched mounting rails simplify photovoltaic (PV) placement, cutting installer time by up to 30%. Brands that certify load-bearing parameters jointly with PV inverter suppliers now secure preferential listings with state nodal agencies. Because the scheme extends to 10 million households by 2027, demand visibility for solar-compatible roofing remains high, nudging even cost-sensitive buyers toward zinc-aluminum coated sheets with anti-corrosion warranties[2]Rakesh Gupta, “PM Surya Ghar Rooftop Subsidy Disbursement Update,” Press Information Bureau, pib.gov.in.

Climate-Resilience Mandates in Coastal States

Cyclone-prone coastal states have begun enforcing wind-uplift ratings and salt-spray resistance in their building bylaws. As a result, polymer-modified membranes with reinforced scrims gain traction over unbranded tar felt. Gujarat’s 2024 Coastal Resilience Code, for example, requires Class C fire-rating and 150 km/h wind resistance on all public buildings; similar norms are pending in Odisha and Tamil Nadu. Manufacturers investing in FM-approved product lines, therefore, position themselves for long-term procurement cycles tied to schools, hospitals, and ports[3]Deepak Mehta, “Coastal Resilience Building Code 2024,” Government of Gujarat Urban Development Department, gujarat.gov.in.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit / sub-standard materials prevalence | -0.5% | National, with higher concentration in unorganized markets | Short term (≤ 2 years) |

| Skilled-labor shortage | -0.4% | National, with acute impact in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Imported bitumen & metal price volatility (₹ depreciation) | -0.3% | National, with higher impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Municipal approval delays for innovative systems | -0.2% | Urban centers, particularly in North India and West India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit/Sub-Standard Materials Prevalence

Up to 30% of low-ticket roofing rolls in informal retail channels fail IS 15965 tensile tests, eroding consumer trust and compressing average selling prices. Warranty claims surge when counterfeit logos masquerade as premium brands, forcing genuine companies to spend more on hologram labels and QR-based verification. Organized players leverage mobile apps that allow dealers to scan batch numbers and instantly confirm authenticity, thereby locking in repeat orders. Regulatory raids, though increasing, remain uneven across states, leaving compliance-paying firms at a 3-5% cost disadvantage.

Imported Bitumen & Metal Price Volatility

The rupee’s 8% slide against the USD between 2023 and 2024 raised landed costs for polymers, aluminum, and galvanizing chemicals. Manufacturers reported margin compression of 50-100 basis points, prompting staggered price hikes that distributors resisted. Hedging through forward contracts offsets only part of the exposure because special-grade bitumen is sourced from the Middle East and premium TPO resins from Europe. Frequent list-price changes also slow procurement decisions, elongating sales cycles in the India roofing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Metal Systems Lead, Membrane Products Accelerate

Metal Roofing held 26.5% of the India roofing market share in 2025, keeping it ahead of all other material categories, driven by industrial warehousing, commercial buildings, and Pre-Engineered Buildings (PEBs). Across the India roofing industry, metal systems continue to benefit from faster installation, long service life, and stronger acceptance in large-span applications where structural reliability matters as much as appearance. The dealer footprint of large suppliers also matters because broader last-mile reach helps branded coated steel move into non-metro construction markets where local procurement still drives many roofing decisions. Clay and concrete tiles still retain a clear place in South India residential construction, especially where sloped roofs are part of local building practice. Even so, metal systems are steadily taking share in commercial and institutional projects where corrosion resistance, speed, and lower maintenance carry more weight than traditional appearance.

Bituminous/Modified Bitumen Membranes are forecast to grow at a 8.20% CAGR through 2031, making them the fastest-growing material line in the India roofing market. This growth is tied to flat-roof commercial buildings, organized retail projects, logistics parks, and institutional assets where waterproofing performance is a hard requirement rather than a discretionary feature. Single-ply membranes such as Thermoplastic Polyolefin (TPO), Ethylene Propylene Diene Monomer (EPDM), and Polyvinyl Chloride (PVC) are also becoming more visible in higher-specification commercial roofs where thermal and maintenance performance have gained importance. Wood roofing remains limited to premium and niche uses. At the same time, corrugated fiber cement, Unplasticized Polyvinyl Chloride (UPVC), and polycarbonate products continue to serve rural, agricultural, and temporary-structure demand at lower price points. In the India roofing market, the material mix is therefore widening at both ends, with premium performance products growing in specification-led projects and basic alternatives holding steady where upfront affordability still dominates.

By Construction Type: New Build Dominates, Reroofing Cycle Emerges

New Construction accounted for 71% of total demand in 2025, giving it the largest share of the India roofing market. That share reflects the combined impact of public housing, industrial building programs, transport infrastructure, logistics expansion, and private real estate development, all of which require new roof installations. The breadth of new-build demand is one of the defining features of the India roofing market, encompassing affordable housing, manufacturing sheds, office developments, transit infrastructure, and utility-linked structures. Roofing suppliers, therefore, do not depend on a single construction category, and that helps keep demand more stable across the cycle. New build demand also supports several material groups, from value-added coated steel to membranes and tile systems, because each end use has its own specification mix.

Reroofing and replacement are projected to grow at a 7.44% CAGR through 2031, making it the fastest-rising construction opportunity after new build scale. Much of the urban building stock added during the late 1990s and 2000s is now entering replacement cycles, especially where older galvanized, asphalt, or fiber-cement roofs were installed under less demanding performance standards. That creates room for owners to upgrade to Galvalume (zinc-magnesium-aluminum-coated steel) and better-finished systems with greater durability and aesthetics. Across the India roofing industry, this is attractive because reroofing buyers often accept higher unit pricing when the replacement clearly improves longevity, heat performance, or solar readiness. The India roofing market is therefore not only expanding through new structures, but it is also beginning to benefit from an upgrade cycle within the existing built stock.

By Application: Residential Leads Broadly, Commercial and Industrial Diversify Mix

Residential accounted for 63.92% of the India roofing market in 2025 and was also the fastest-growing application, with an 8.59% CAGR through 2031. That combination is important because it shows that the largest demand pool in the India roofing market is still gaining momentum rather than maturing. Housing delivery under the Pradhan Mantri Awas Yojana, ongoing rural completions, and the need for additional urban homes are keeping the residential pipeline broad and visible. The PM Surya Ghar program is adding another layer by prompting households to consider roof strength, fastener compatibility, and reflective performance before selecting a roof for new construction or replacement. This is lifting interest in engineered metal panels, standing-seam systems, and thermally efficient products that can support rooftop solar without substantial retrofitting.

Commercial and industrial demand still plays an important balancing role in the India roofing market even though residential remains dominant. Commercial roofs are benefiting from office parks, organized retail, mixed-use projects, and institutional buildings, where flat-roof membranes and reflective systems better align with modern design and operating needs. Industrial demand continues to come from warehousing, manufacturing sheds, and logistics facilities that need large clear-span structures and quick installation, which supports metal roofing and insulated sandwich panels. Institutional demand is also taking shape through government procurement, especially as cool-roof requirements and energy efficiency standards become part of the build specification. As a result, the India roofing market has a residential core. Still, its revenue mix is becoming more diversified as commercial, industrial, and public-use buildings ask for higher-performance systems.

Geography Analysis

South India held a 31.5% share in 2025, making it the largest regional cluster in the India roofing market. Karnataka, Tamil Nadu, Telangana, and Andhra Pradesh continue to support industrial corridors, technology parks, electronics and manufacturing investments, and data center construction, which often favor metal roofing for its speed, span capability, and corrosion resistance. South India also benefits from deeper acceptance of higher-specification systems in both industrial and residential projects, which keeps branded suppliers active across several price tiers. Telangana has moved further than most states on policy, with its Cool Roof Framework requiring high Solar Reflective Index materials in targeted building categories and linking compliance to the building approval process. Kerala and Tamil Nadu have also advanced cool-roof action through state-led programs and public-building pilots, which gives the India roofing market a stronger specification base in the South than in many other regions.

North India is forecast to grow at a 7.76% CAGR through 2031, making it the fastest-growing regional block in the India roofing market. A stronger housing cycle, wider infrastructure activity, and logistics-related construction across the Delhi National Capital Region, Haryana, Punjab, Rajasthan, and Uttar Pradesh are supporting the region. Demand is not limited to urban housing, as warehouse, industrial shed, and transport-linked construction are also increasing the addition of roof area across the region. Public action on heat mitigation is beginning to influence roof specifications as well, with reflective roof pilots becoming part of formal city planning in Delhi. In the India roofing market, this combination of residential growth and logistics-led non-residential construction is making North India a more balanced growth engine than before.

West India remains a critical industrial and solar-linked demand center in the India roofing market, led by Maharashtra and Gujarat. Coastal risk management and resilience planning are becoming increasingly relevant here, and the National Cyclone Risk Mitigation Project supports greater attention to wind-resistant, durable roof systems in exposed districts. Gujarat also stands out for solar-integrated roofing demand, where coated metal systems that work well with photovoltaic mounting are gaining importance. East and North East India still form the smallest regional cluster. Still, government-backed rural housing completions and increased assistance for special category states are creating a clearer upgrade path from traditional roof materials to more formal, durable systems. The India roofing market therefore shows distinct regional logics in each zone: the South, led by industrial depth and policy action; the North, by growth speed; and the West and East, by resilience, solar adoption, and housing formalization.

Competitive Landscape

Market structure is moderately fragmented, with the top five players accounting for roughly 45% of 2024 revenue, leaving room for regional challengers. Tata BlueScope and Hindalco leverage integrated steel value chains to buffer metal price swings, while midsize firms such as Shyam Metalics deploy new 400,000-tonne capacity to chase volume. Value propositions center on higher SRI coatings, factory-attached insulation, and patented clip-lock seams that halve onsite labor.

Direct-forming technology is replacing one-pass corrugators, enabling just-in-time customization of rib heights and panel widths. Forward integration into installation services is rising as customers seek single-warranty accountability; UltraTech’s 2025 entry into cables and wires complements its building envelope ambitions and underscores supply-chain convergence. Capital markets reward scale plays: JTL Industries raised USD 36 million in 2024 to bankroll Raigad expansion and then acquired Nabha Steels, securing coil self-sufficiency.

Digital engagement is a new frontier: QR-coded coils enable traceability from mill to roof, and cloud-based thermal simulation tools help architects model savings in real time. Manufacturers offering such digital stack integration differentiate beyond price, a critical edge as the India roofing market matures. Logistics footprint also matters: vendors with Eastern depots promise 72-hour delivery, crucial for infrastructure projects on tight milestones.

India Roofing Industry Leaders

Tata BlueScope Steel

Hindalco Industries Ltd

JSW Steel Coated Products

CK Birla Group (HIL Ltd)

Everest Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tata Steel Limited gained sole control of Tata BlueScope Steel Private Limited by acquiring the remaining 50% equity stake from BlueScope Steel Asia Holdings Pty Limited for up to USD 130 million. The transaction converted a 50-to-50 joint venture established in 2005 into a wholly owned Tata Steel subsidiary and consolidated the DURASHINE and LYSAGHT roofing brand portfolios.

- December 2025: Tata Steel Limited approved the establishment of a 0.7 million metric ton per year rolled pickling and galvanizing line at its Maharashtra cold rolling mill through the Tata BlueScope network. The move deepens downstream capacity for color-coated steel products used in roofing and construction.

- June 2025: Hindalco Industries commissioned a USD 145 million aluminum coil-coating plant in Sambalpur, Odisha, adding 250,000 t of corrosion-resistant roofing-sheet capacity; first commercial shipments are slated for Q4 2025.

- May 2025: Tata BlueScope Steel launched PRISMA, a next-generation pre-painted 55% aluminum-zinc alloy-coated steel coil for roofing and cladding applications, with Cool Comfort Technology intended to maintain cooler interiors. The product carries Bureau of Indian Standards certification and is targeted at Tier 2 and Tier 3 construction markets.

India Roofing Market Report Scope

The Indian roofing industry encompasses the manufacturing, distribution, installation, and maintenance of roofing systems. These systems play a crucial role in shielding buildings from weather elements and enhancing energy efficiency. With the rapid pace of urbanization and infrastructure development, there's a surging demand for diverse and sustainable roofing solutions across residential, commercial, and industrial sectors.

A complete background analysis of the India Roofing Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and the impact of Geopolitics and Pandemics on the Market, is covered in the report.

The India Roofing Market is segmented by sector (commercial, residential, and industrial construction) as well as by material (tiles, bricks, metal roofing) .The report offers market size and forecasts for all the above segments in value (USD).

By Material Type

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

By Construction Type

| New Construction |

| Reroofing and Replacement |

By Application

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

By Geography

| North India |

| South India |

| West India |

| East and North East India |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | North India |

| South India | |

| West India | |

| East and North East India |

Key Questions Answered in the Report

What is the 2031 outlook for roofing demand in India?

The India roofing market is expected to reach USD 11.7 billion by 2031 from USD 8.6 billion in 2026, with a forecast CAGR of 6.4%.

Which material category leads demand today?

Metal Roofing led with a 26.5% share in 2025 because it fits industrial sheds, warehouses, and large commercial buildings where installation speed and durability matter.

Which roofing application is growing the fastest?

Residential is both the largest and the fastest-growing application, with 63.92% share in 2025 and an 8.59% CAGR through 2031.

Why is rooftop solar important for roof selection in India?

Rooftop solar is changing roof-buying decisions, as households now consider structural load, corrosion resistance, and mounting compatibility, favoring engineered metal systems and standing-seam profiles.

Which region offers the strongest near-term growth opportunity?

North India is projected to grow the fastest at 7.76% CAGR through 2031, supported by housing, logistics, and infrastructure activity.

What is the biggest risk for suppliers and contractors?

The main risks are imported input cost volatility, installer shortages, and counterfeit or sub-standard materials, all of which can pressure margins and reduce trust in product performance.

Page last updated on: