Central and Eastern Europe Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

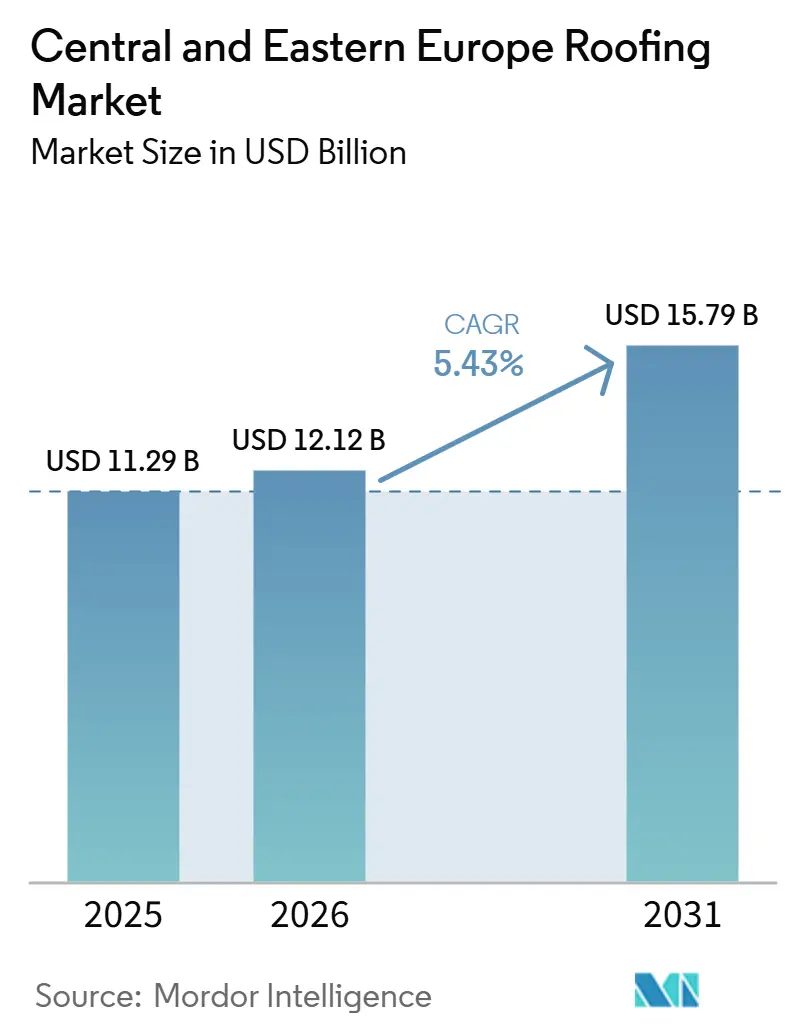

| Base Year Market Size (2025) | USD 11.29 Billion |

| Market Size (2026) | USD 12.12 Billion |

| Market Size (2031) | USD 15.79 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central and Eastern Europe Roofing Market Analysis by Mordor Intelligence

The Central And Eastern Europe Roofing Market size was valued at USD 11.29 billion in 2025 and is estimated to grow from USD 12.12 billion in 2026 to reach USD 15.79 billion by 2031, at a CAGR of 5.43% during the forecast period (2026-2031).

The Central and Eastern Europe roofing market is being shaped by the revised Energy Performance of Buildings Directive (EPBD), which has tightened renovation requirements for inefficient buildings and made solar-ready roof design a standard consideration in new construction and major renovation projects following its implementation in May 2026. Demand is also being supported by public thermal renovation programs, a broader shift toward nearshoring-led industrial construction, and more frequent hail and convective storm events that are shortening replacement cycles across parts of the region. At the same time, the Central and Eastern Europe roofing market faces persistent execution pressure from roofer shortages, uneven renovation quality, and volatility in steel and bitumen prices, all of which affect installation schedules and margin stability. Competition is moving beyond basic product supply, as manufacturers that can offer lightweight systems, faster installation, solar compatibility, and documented compliance support are gaining a clearer advantage in both renovation and new-build projects. This leaves the Central and Eastern Europe roofing market with a stronger medium-term opportunity set than a simple replacement cycle would suggest, because policy, weather exposure, and building performance needs are now moving in the same direction.

Key Report Takeaways

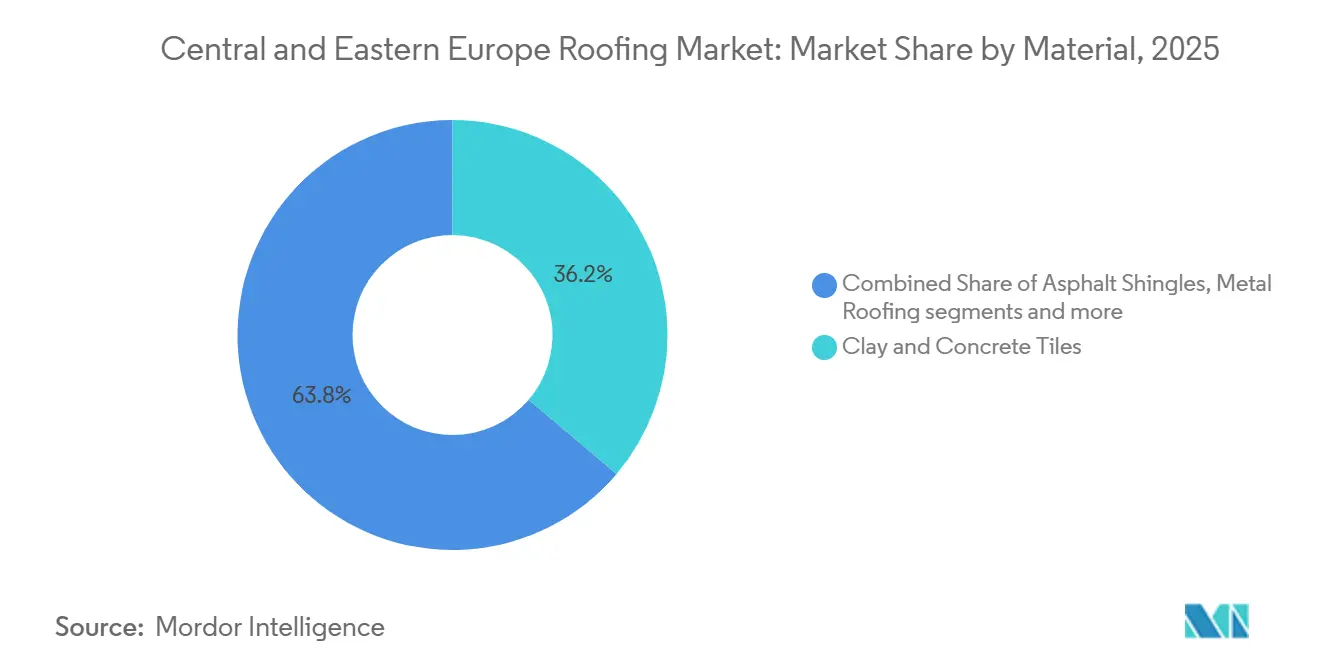

- By material type, clay & concrete tiles held a 36.20% market share in 2025, while metal roofing is forecast to expand at a 6.40% CAGR through 2031.

- By construction type, reroofing and replacement captured 57.40% of the Central and Eastern Europe roofing market share in 2025, while new construction is projected to grow at a 6.00% CAGR through 2031.

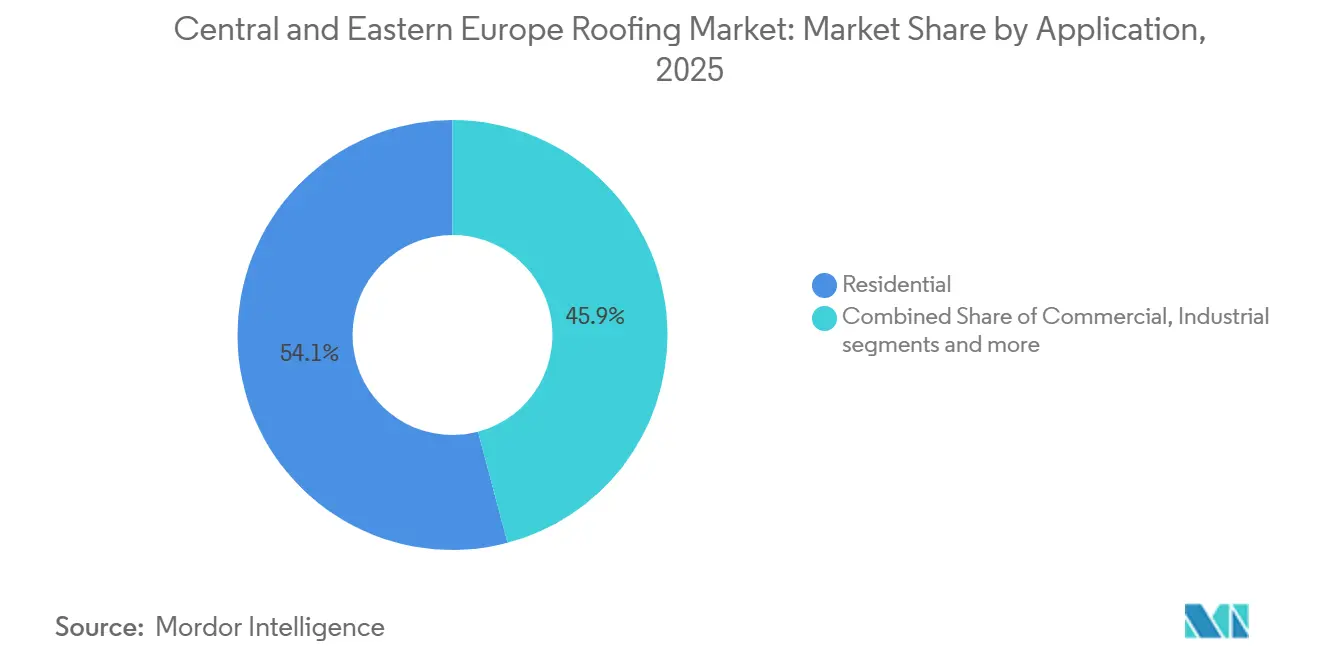

- By application, residential accounted for 54.12% of the Central and Eastern Europe roofing market size in 2025, while the industrial segment is advancing at a 6.10% CAGR through 2031.

- By geography, Poland held 34.61% of the Central and Eastern Europe roofing market share in 2025, while Romania recorded the highest projected CAGR at 6.30% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Central and Eastern Europe Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPBD-Led Deep Renovation of Worst-Performing Buildings | +1.4% | EU-wide, concentrated in Poland, Czech Republic, Hungary, and Romania | Medium term (2-4 years) |

| Thermal Modernization Subsidies Supporting Reroofing Demand | +1.0% | Poland, Czech Republic, and Hungary | Short term (≤ 2 years) |

| Nearshoring-Led Warehouse and Light-Industrial Roof Build-Out | +0.9% | Poland, Czech Republic, Hungary, and Romania | Short term (≤ 2 years) to Medium term (2-4 years) |

| Metal Roofing Substitution in Renovation for Lightweight, Faster Installation | +0.6% | Poland, Romania, and Rest of CEE | Short term (≤ 2 years) to Medium term (2-4 years) |

| Solar-Ready and Rooftop PV Permit Triggers Increasing Roof-System Upgrades | +0.5% | EU-wide, strongest in Poland and Czech Republic | Medium term (2-4 years) to Long term (≥ 4 years) |

| Hail and Convective Storm Damage Accelerating Reroofing Cycles | +0.5% | Poland, Czech Republic, and Hungary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EPBD Renovation Mandates Create a Durable, Policy-Anchored Demand Pipeline

The Central and Eastern Europe roofing market is being reshaped by the recast of the Energy Performance of Buildings Directive (EPBD), which is one of the strongest policy drivers influencing roof renovation decisions over the forecast period[1]European Commission, “Energy Performance of Buildings Directive (EU/2024/1275),” Energy, energy.ec.europa.eu. The directive requires renovating the 16% worst-performing non-residential buildings by 2030 and 26% by 2033, while also targeting a 16% reduction in average primary energy use in residential buildings by 2030. This matters more in Central and Eastern Europe because more than 50% of the building stock does not meet current performance expectations, and much of the residential base predates 1990. In practice, many properties will not be able to comply solely through minor repairs, so roof replacement, insulation upgrades, and related envelope work will increasingly be specified together. That bundling effect makes roofing demand less discretionary and more tied to mandatory compliance schedules, which improves visibility for suppliers and installers serving the Central and Eastern Europe roofing market. It also raises the value of technically certified systems, because buyers now need proof that the finished roof meets energy performance targets rather than just restoring weather protection.

Thermal Modernization Subsidy Programs Activate Household Reroofing at Scale

Household subsidy programs are expanding the addressable base for renovation work and making the Central and Eastern European roofing market more resilient to short-term price pressure. Poland's Czyste Powietrze program secured PLN 10 billion (USD 2.5 billion) from the European Union (EU) Modernization Fund in March 2025, including support for roof insulation as part of wider household energy upgrades. In the Czech Republic, the New Green Savings Programme directly supports roof and ceiling insulation for family houses and apartment buildings, which helps convert policy demand into actual roof replacement activity. The effect is especially strong at the lower-income end, where high grant coverage reduces the sensitivity of repair decisions to movements in metal or bitumen prices. That keeps reroofing pipelines more stable than they would be in a purely unsubsidized consumer market, particularly in countries with older housing stock and low heating efficiency. As a result, the Central and Eastern Europe roofing market is seeing more projects where insulation, covering replacement, and future solar compatibility are considered in a single homeowner decision rather than in separate phases.

Nearshoring Industrial Construction Sustains Single-Ply and Panel Roofing Demand

The Central and Eastern Europe roofing market is also benefiting from a broader industrial construction cycle, driven by nearshoring, logistics expansion, and light manufacturing investment across the region. These projects typically require high-insulation roof systems, large-span flat roof solutions, and better integration with rooftop energy systems than older warehouse formats demanded. That supports demand for single-ply membranes, insulated panels, and other system-led products that perform well in terms of speed, drainage, and solar readiness. The project mix is important because industrial roofs are increasingly procured as part of a wider building performance package rather than as a low-cost standalone input. This raises unit specification and gives suppliers who can document compliance, detailing, and warranty support an advantage over those serving larger roof areas. The same shift is helping the Central and Eastern Europe roofing market move toward more technically complex products, even before all national rules fully catch up with the newest EU framework.

Metal Roofing Substitution in Renovation for Lightweight, Faster Installation

Metal roofing is gaining ground in renovation projects across the Central and Eastern Europe roofing market because it places less structural load on aging roof frameworks and can be installed faster than heavier traditional systems. This matters in a region where much of the housing stock predates modern energy standards, making lightweight replacement solutions more practical during deep renovation work. Faster installation is also becoming a more important buying factor because roofer shortages are limiting how quickly projects can be completed across many EU member states. In this setting, metal systems help contractors reduce on-roof labor time, improve scheduling, and manage more projects with constrained installer capacity. Product development is already reflecting this shift, as Ruukki Construction launched its wider 510 mm Classic Pro standing seam sheet for the Central and Eastern Europe markets in October 2025 to reduce joint count and labor time per roof.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel, Bitumen, and Energy Input Costs | -0.7% | Global, strongest transmission in Poland, Romania, Czech Republic, and Hungary | Short term (≤ 2 years) to Medium term (2-4 years) |

| Skilled Roofer Shortages and Ageing Installer Base | -0.6% | EU-wide, acutely felt in Czech Republic, Poland, and Romania | Long term (≥ 4 years) |

| Renovation Underperformance and Weak Building-Level Execution Controls | -0.3% | Poland, Romania, and Bulgaria | Medium term (2-4 years) |

| Fragmented Installer Quality and Uneven Code Enforcement | -0.2% | Rest of CEE, Romania rural areas, and Balkan sub-markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel, Bitumen, and Energy Input Costs

Steel and bitumen price volatility remains a direct headwind for the Central and Eastern Europe roofing market, particularly in product groups that depend on imported feedstock or energy-intensive production. EUROMETAL reported late May 2026 hot-rolled coil prices at EUR 700 to EUR 770 per tonne, equivalent to USD 756 to USD 831.6 per tonne, while the July 2026 safeguard changes are expected to keep pricing for steel-based products uncertain. That uncertainty affects metal roofing manufacturers, fabricators, and distributors because quoting windows and procurement timing become harder to manage. Bitumen-related pressure also matters for flat roofing systems, as disruptions in raw material availability can delay project schedules and compress margins. Energy costs add another layer of strain on clay tile, membrane, and other manufactured roofing products that depend on stable plant economics. The burden falls more heavily on smaller regional players, which may accelerate share gains for larger businesses with broader sourcing options and stronger balance sheets.

Skilled Roofer Shortages and Ageing Installer Base

Skilled roofer shortages are limiting how quickly projects can move through the Central and Eastern Europe roofing market, even as renovation demand and new specification requirements continue to rise. The European Employment Services (EURES) identifies roofers among the European Union's critical shortage occupations, indicating that the labor shortage is structural and affects multiple member states rather than being limited to a single local market. The aging installer base adds to this pressure because retirements are reducing available site capacity faster than new skilled workers are entering the trade. The European Construction Industry Federation stated in November 2025 that the EU construction sector will need 2 million additional workers by 2030, reflecting a weak replacement pipeline after years of declining enrollment in skilled trades. For roofing manufacturers and contractors, this raises labor costs, extends project lead times, and increases the appeal of systems that reduce installation complexity and time on the roof. The result is a persistent execution bottleneck that can slow the conversion of policy-led renovation demand into completed roofing volumes across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Clay & Concrete Tiles Lead Value, Metal Roofing Drives Growth

Clay & Concrete Tiles held a 36.20% market share in 2025, making them the largest material category in the Central and Eastern Europe roofing market. This leading position reflects long-established preferences for pitched roofs across Poland, Hungary, and the Czech Republic, where tile roofs remain closely tied to mainstream residential construction. The category also benefits from replacement demand, as many renovated homes were originally built with pitched roofs that are well-suited to tile systems. In practical terms, that installed base keeps tile relevant even as performance expectations rise. End-2025 investment also showed that manufacturers still view this category as strategically important, with Wienerberger commissioning a new concrete roof tile plant in Hungary with an annual capacity of 3 million square meters and an investment of EUR 30 million (USD 32.4 million)[2]BFT International, “CO2-Neutral Concrete Roof Tile Production Facility in Hungary Successfully Commissioned,” BFT International, bft-international.com. The decision supports the view that scale, product continuity, and regional supply remain important in the Central and Eastern Europe roofing industry.

Metal Roofing is the fastest-growing material segment, with the Central and Eastern Europe roofing market size for this category projected to expand at a 6.40% CAGR from 2026 to 2031. Its growth is tied to two practical advantages that matter more each year: lighter structural loading on older buildings and faster installation under tight labor conditions. That makes metal especially attractive in renovation projects where legacy roof frames cannot easily support heavier replacement systems. It also fits projects where installers need to complete more area in fewer site days because certified labor is limited. Bituminous and modified bitumen membranes remain essential for flat commercial roofs, although cost and supply volatility can complicate procurement planning. Single-ply membranes are gaining ground in large industrial applications due to their compatibility with drainage design and rooftop solar integration. At the same time, asphalt shingles retain a niche role, and wood remains concentrated in heritage and premium uses. Across the Central and Eastern Europe roofing industry, the shift toward certified system solutions is becoming clearer as owners place more value on compliance, service life, and integration than on low-end material substitution alone.

By Construction Type: Reroofing and Replacement Dominance Deepens as Policy Mandates Converge

Reroofing and Replacement accounted for 57.40% of the market share in 2025, indicating that the Central and Eastern Europe roofing market is still led by an aging building stock rather than pure new-build momentum. That profile is rooted in the region's large share of pre-1990 buildings and the slow historical pace of energy renovation. Roof work is also being pulled forward by building performance rules, because compliance often requires more than patch repairs and favors deeper renovation packages. Weather exposure adds another layer, as severe hail events across Central Europe in 2024 damaged roofs and increased repair pressure in affected zones. Munich Re also reported in 2025 that severe hail losses are rising in Europe, supported by greater storm frequency and larger hailstone sizes. This combination of aging stock, policy pressure, and weather-related damage keeps replacement activity structurally important rather than cyclical.

New construction is the fastest-growing construction segment and is forecast to advance at a 6% CAGR from 2026 to 2031. Logistics facilities, light manufacturing sites, residential program restarts, and broader investment in modern building stock across the region support the growth base. Unlike simple replacement work, these projects increasingly call for roof systems that are designed with insulation, solar-readiness, and compliance documentation from the outset. That supports higher-value specification in industrial and commercial buildings, especially where multinational occupiers want stronger performance standards in leased assets. For manufacturers, the implication is not that renovation loses importance, but that the Central and Eastern Europe roofing market is developing two parallel demand engines, one built on replacement necessity and one built on more technical new-build standards. Product lines that can bridge both conditions, especially with accessories, detailing support, and matched system components, are likely to capture a larger share of the upgrade cycle over time.

By Application: Residential Anchors Volume While Industrial Gains Fastest

Residential applications held a 54.12% market share in 2025, making Central and Eastern Europe the roofing market with the largest volume base in single-family and small multi-family structures. This position is closely linked to the housing profile of countries such as Poland, where pitched roofs remain common, and the stock of older homes creates recurring replacement demand. It is also supported by public energy renovation programs that make roof insulation and covering upgrades more financially accessible for households. Residential demand, therefore, combines routine maintenance, storm-related repairs, efficiency retrofits, and selective new housing activity to provide broad market depth. That is why the Central and Eastern Europe roofing market keeps a strong residential bias even as industrial construction grows faster. The category also favors suppliers that can offer a wide range of designs, compatible accessories, and products that fit partial or phased replacement work.

Industrial is the fastest-growing end-use segment, and the Central and Eastern Europe roofing market size for this segment is projected to increase at a 6.10% CAGR through 2031. Nearshoring, logistics expansion, and manufacturing relocation are pushing demand toward flat and low-slope systems that can handle insulation, drainage, and rooftop solar requirements in a single design package. These projects are more likely to use single-ply membranes, insulated panels, and engineered assemblies with stronger documentation and warranty support. Commercial and institutional demand remains relevant, especially for public buildings and non-residential properties that need upgrades to align with new performance rules. Industrial projects also raise the average specification level because large occupiers and investors tend to assess roof systems within broader building performance targets, not only on first-cost terms. This makes the Central and Eastern Europe roofing market more favorable for suppliers that can serve integrated project needs rather than only commodity material demand. The result is a gradual increase in the share of projects in which roof selection affects energy strategy, operating costs, and lease appeal simultaneously. That shift is especially visible in new logistics and manufacturing facilities designed for future rooftop photovoltaic installation.

Geography Analysis

Poland accounted for 34.61% of the Central and Eastern Europe roofing market in 2025, making it the largest country market in the region. Poland combines scale in residential demand with a strong manufacturing base and a policy backdrop that is supportive of renovation activity. The PLN 10 billion (USD 2.5 billion) Modernization Fund (MF) allocation to Czyste Powietrze in March 2025 reinforced support for household energy renovation and roof insulation upgrades. This gives Poland a stronger renovation pipeline than a simple maintenance cycle would imply, because subsidy-backed projects can continue even when material prices remain unsettled. Poland is also well placed to benefit from the EPBD and solar-ready requirements, as its large stock of older buildings provides a broad base for roof performance upgrades.

Romania is forecast to grow at a 6.30% CAGR from 2026 to 2031, the fastest pace within the Central and Eastern Europe roofing market. The country's faster expansion reflects a mix of structural underinvestment, rising renovation needs, and better alignment with EU-backed renovation planning. Romania was among the first EU member states to submit a draft National Building Renovation Plan by the December 2025 deadline, which supports the view that policy implementation will increasingly support on-ground activity. That planning progress matters because roofing demand in Romania is closely tied to the broader modernization of building performance and the need to improve aging stock rather than serving only new construction. Romania, therefore, stands out in the Central and Eastern Europe roofing market as the geography where catch-up renovation and policy implementation are most likely to work together during the forecast period.

The remaining Central and Eastern Europe roofing market is shared across the Czech Republic, Hungary, and the Rest of Central and Eastern Europe, where distinct subsidy support, labor constraints, and manufacturing investment shape demand. In the Czech Republic, the New Green Savings Programme directly supports roof and ceiling insulation, which helps sustain household renovation demand and improves the commercial case for deeper roof upgrades. Hungary adds an important manufacturing dimension, as Wienerberger's new concrete tile plant strengthens the country's role in regional supply and reflects continuing confidence in tile-based demand across neighboring markets. Across the wider region, the shared challenge is execution capacity, because roofer shortages and uneven installer quality can slow project delivery even when demand fundamentals are supportive. Even so, the Central and Eastern Europe roofing market outside Poland is not weak. It is simply more varied, with some countries led by subsidy-backed residential renovation and others supported by manufacturing, logistics, or cross-border product supply. Over time, EU performance standards are likely to narrow some of those differences by raising minimum roof specifications more consistently across member states. That should gradually make the regional opportunity more balanced, even if country-level demand patterns remain distinct.

Competitive Landscape

The Central and Eastern Europe roofing market remains fragmented, with pan-European groups such as BMI Group, Kingspan Group, Wienerberger, Soprema, and Ruukki Construction competing alongside strong regional manufacturers including Pruszyński, Balex Metal, Metigla, Wetterbest, ROVA Group, and Terrán Group. No single supplier appears to dominate the region across all materials, applications, and geographies, which keeps competition active in both product breadth and country-level execution. Large groups offer wider product portfolios, stronger compliance support, and broader distribution. At the same time, national specialists often compete on channel access, familiarity with local roof types, and faster response times for renovation work. This structure means the share is spread across multiple formats, including metal systems and tiles, membranes, and insulated panels. It also means the Central and Eastern Europe roofing market rewards companies that can align product design with labor efficiency, solar integration, and local installation practice rather than relying on scale alone.

Strategic moves in 2025 and 2026 show that competition is increasingly focused on capability building. Ruukki Construction launched the Ruukki Classic Pro standing seam sheet in a wider 510 mm format for CEE markets in October 2025, with the clear goal of reducing joint count and lowering installation time per roof[3]Ruukki Construction, “New Ruukki Classic Pro Standing Seam Sheet for CEE Markets,” Ruukki Construction, ruukki.com. Balex Metal launched its PIR ROOF panel with an oblique joint in April 2026, targeting industrial and commercial roofs with a gravity-based sealing approach that removes the need for polymer seals and supports higher fire and smoke performance. Wienerberger also reinforced its regional roofing presence by commissioning a new concrete roof tile plant in Hungary at end-2025, which points to continued confidence in tile demand and regional supply optimization. These moves indicate that the Central and Eastern Europe roofing market is not only expanding, but also becoming more demanding in how products are engineered and delivered.

Operational strategy is also changing alongside product strategy. Kingspan reported improved performance in Central and Eastern Europe in 2025 and noted healthy European roofing backlogs entering 2026, suggesting that regional demand has remained constructive despite cost and labor challenges. BMI Group completed a major SAP Cloud ERP Private consolidation in March 2026, moving from 44 legacy systems to a single platform, indicating a stronger focus on operating discipline and standardized execution. The competitive implication is clear. As EPBD compliance, solar readiness, and documentation requirements rise, suppliers with stronger systems, cleaner installation logic, and better support tools are likely to gain ground. That makes the Central and Eastern Europe roofing market increasingly favorable to companies that can combine product performance with execution reliability. It also creates room for regional consolidation if smaller players struggle to manage raw-material volatility, installer scarcity, and certification costs simultaneously.

Central and Eastern Europe Roofing Industry Leaders

BMI Group

Wienerberger

Pruszyński

BP2

ROVA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kingspan Group acquired Duggan Profiles, an Irish manufacturer of single-skin steel construction sheets, purlins, profiled steel sheeting, and flashings serving the agricultural and industrial sectors. The acquisition deepens Kingspan's vertical integration across steel roofing and façade components.

- April 2026: Balex Metal launched the PIR ROOF panel with an oblique joint for industrial and commercial roofing. The gravity-based sealing mechanism eliminates polymer seals, achieves fire class RE 60 and smoke class s1, and is designed to reduce installation failure points on warehouse and logistics roofs.

- January 2026: Wienerberger announced in 2026 the expansion of its roofing and solar-integrated solutions portfolio across Central and Eastern Europe, including increased rollout of its in-roof photovoltaic systems (such as Wevolt) in markets like Poland, Hungary, and the Czech Republic. The initiative reflects growing demand for energy-generating roofing systems and positions Wienerberger to capture rising residential renovation and sustainability-driven roofing upgrades across the region.

- January 2026: 7R delivered a warehouse with integrated 350 kWp PV for Profile VOX in Pobiedziska, Poland, covering more than 20,000 square meters, demonstrating that solar-ready industrial roofing specifications are becoming standard for Central and Eastern Europe build-to-suit logistics facilities.

Central and Eastern Europe Roofing Market Report Scope

The Central and Eastern Europe Roofing Market is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and more), Construction Type (New Construction, Reroofing), Application (Residential, and more), and Geography (Poland, Romania, Czech Republic, Hungary, and Rest of Central and Eastern Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| Poland |

| Romania |

| Czech Republic |

| Hungary |

| Rest of Central and Eastern Europe |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | Poland |

| Romania | |

| Czech Republic | |

| Hungary | |

| Rest of Central and Eastern Europe |

Key Questions Answered in the Report

What is the expected value of Central and Eastern Europe roofing demand by 2031?

The sector is projected to reach USD 15.79 billion by 2031, rising from USD 12.12 billion in 2026 at a 5.43% CAGR over 2026 to 2031.

Which material category leads sales across the region?

Clay & concrete tiles led in 2025 with a 36.20% share, supported by the large installed base of pitched residential roofs across Poland, Hungary, and the Czech Republic.

Which roofing material is growing the fastest in Central and Eastern Europe?

Metal roofing is the fastest-growing material segment, with a projected 6.40% CAGR from 2026 to 2031, helped by lower structural load and faster installation.

Why is replacement work larger than new construction in this region?

Reroofing and replacement held 57.40% of demand in 2025 because the building stock is older, energy performance standards are tightening, and storm damage is shortening replacement cycles.

Page last updated on: