GCC Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

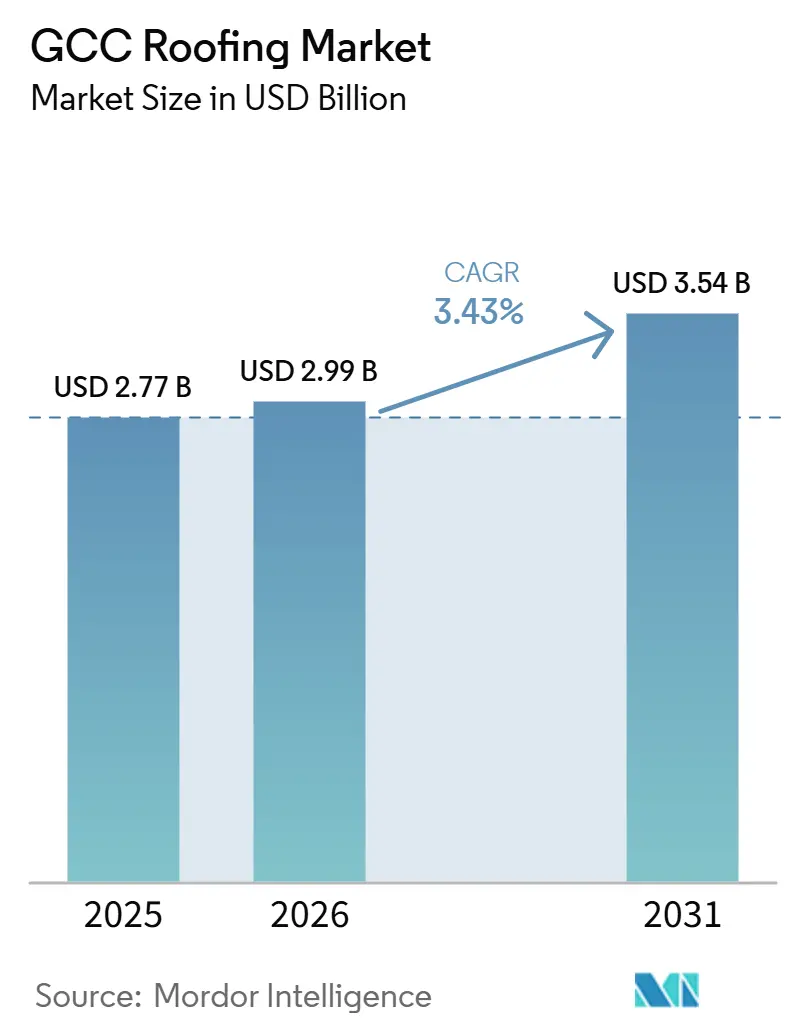

| Base Year Market Size (2025) | USD 2.77 Billion |

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 3.43% CAGR |

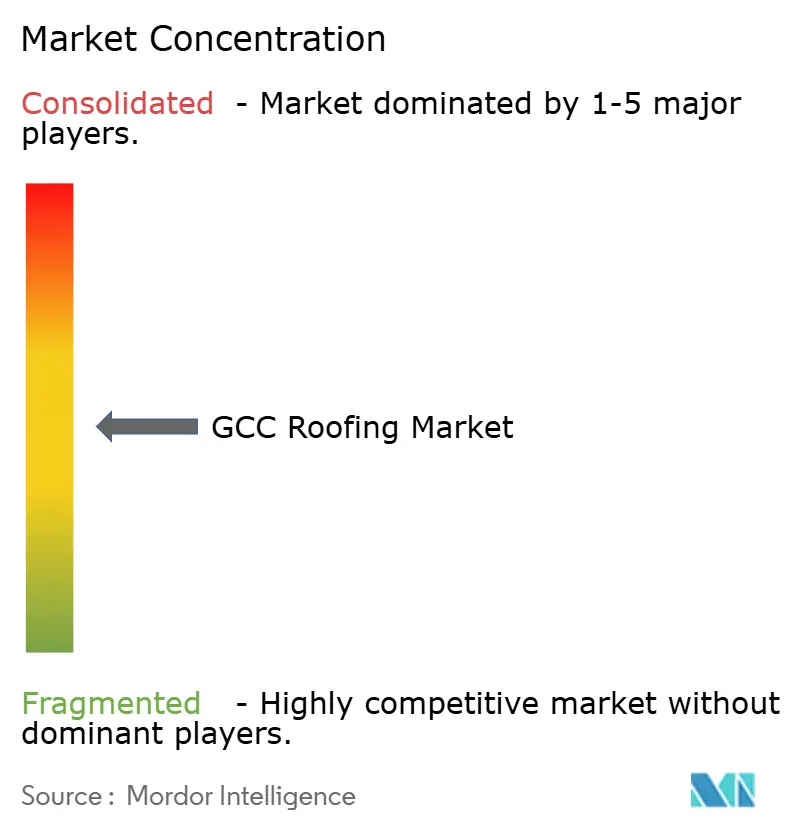

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Roofing Market Analysis by Mordor Intelligence

The GCC Roofing Market size was valued at USD 2.77 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 3.54 billion by 2031, at a CAGR of 3.43% during the forecast period (2026-2031).

The GCC roofing market is being supported more by sovereign-backed construction programs than by short housing cycles, which gives demand a longer planning horizon across the region. Procurement across the GCC roofing market is also moving away from basic roofing selection toward climate-rated, energy-aware assemblies that can withstand high heat, waterproofing stress, and stricter building standards. That change is improving realized pricing because developers are paying more for documented system performance, longer service life, and better compatibility with rooftop solar and thermal-control requirements. Saudi Arabia remains the anchor of the GCC roofing market due to its depth of execution across large tourism, residential, industrial, and mixed-use developments, while the United Arab Emirates (UAE) is adding momentum through green building compliance and dense urban construction activity. These conditions favor suppliers that can offer approved systems, regional manufacturing, dependable delivery, and technical support for large projects rather than only commodity roofing products.

Key Report Takeaways

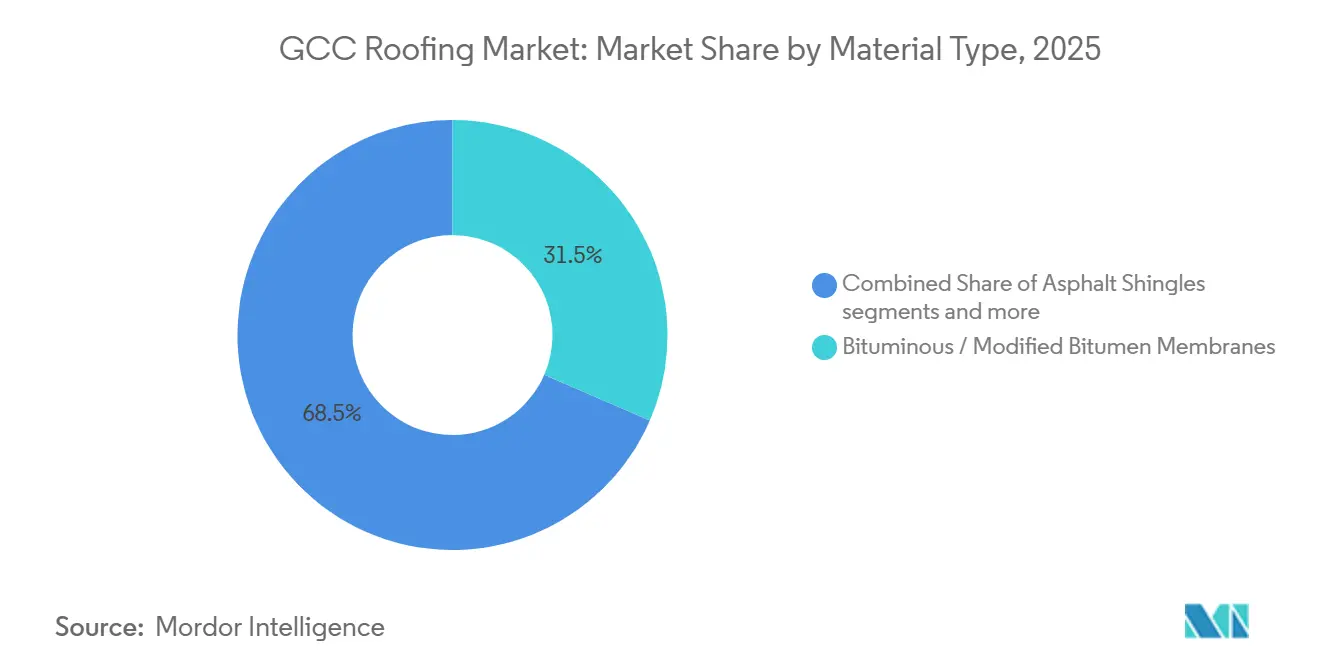

- By material type, bituminous / modified bitumen membranes accounted for 31.5% of the GCC roofing market share in 2025, while metal roofing is projected to grow at a 5.5% CAGR through 2031.

- By construction type, new construction accounted for a 74% share of the GCC roofing market size in 2025, while reroofing & replacement are forecast to expand at 5.98% CAGR through 2031.

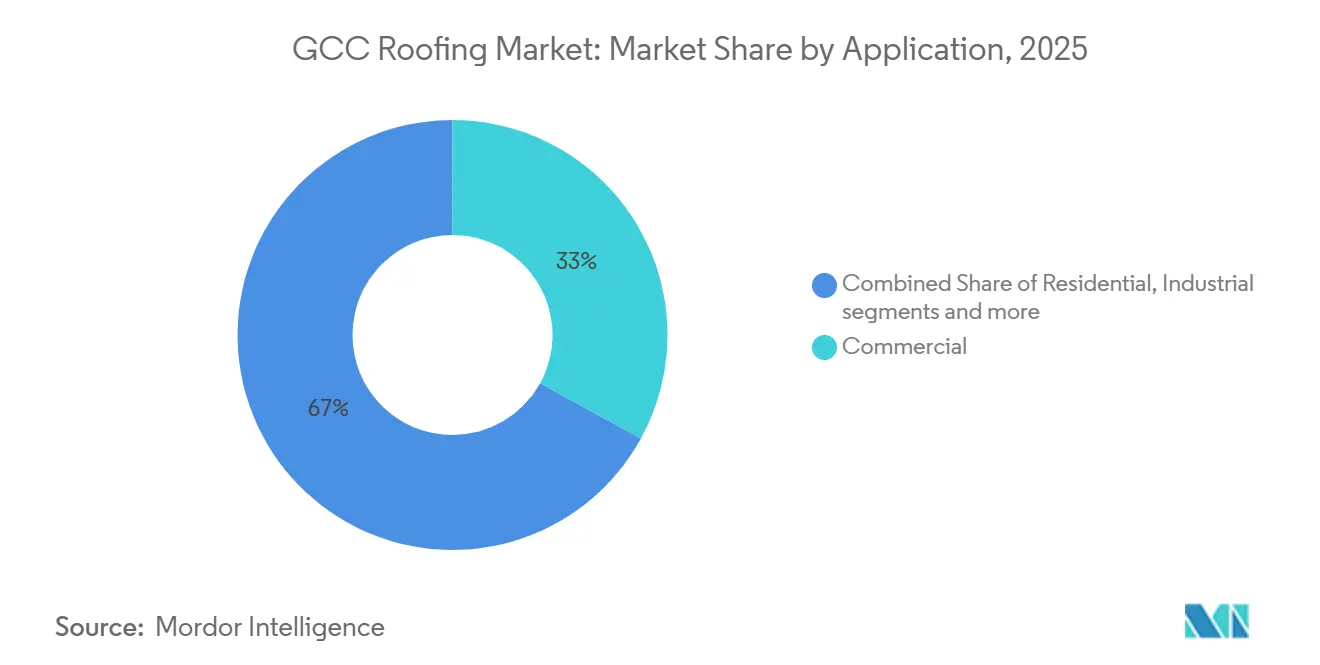

- By application, commercial applications accounted for a 33% share of the GCC roofing market in 2025, while industrial applications are advancing at a 5.7% CAGR through 2031.

- By geography, Saudi Arabia accounted for 45% of the GCC roofing market in 2025, while the United Arab Emirates (UAE) recorded the highest projected CAGR of 5.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC Mega Projects and Infrastructure Growth Boosting Roofing Demand | +1.2% | Saudi Arabia, UAE, Qatar, with spillover to Oman and Kuwait | Medium term (2-4 years) |

| Stricter GCC Green Building and Energy Codes Increasing Demand for Insulated and Reflective Roofing | +0.8% | UAE, Saudi Arabia, Qatar, with wider GCC relevance | Medium term (2-4 years) |

| Harsh GCC Weather Driving Demand for UV-Resistant, Waterproof, and Thermally Stable Roofing | +0.6% | GCC-wide, with acute relevance in inland heat zones and coastal cities | Long term (≥ 4 years) |

| Rising Rooftop Solar Integration Demand | +0.5% | UAE, Saudi Arabia, with expansion into Oman and Qatar | Medium term (2-4 years) |

| Rising Refurbishment and Remediation of Aging Assets Supporting Replacement Roofing Demand | +0.4% | UAE, Saudi Arabia, Qatar, and Kuwait commercial stock | Long term (≥ 4 years) |

| Growing Demand for High-SRI and Re-Coatable Roofing Systems | +0.4% | Saudi Arabia, UAE, and wider GCC commercial districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GCC Mega Projects and Infrastructure Growth Are Boosting Roofing Demand

Mega projects and sovereign infrastructure programs are sustaining the GCC roofing market across housing, tourism, transport, utilities, and industrial corridors. Demand visibility is stronger than in housing-led cycles because flagship programs move through phased procurement and remain tied to state-led diversification agendas. This matters for roofing because projects such as NEOM, Red Sea Global, and Qiddiya require high-reflectance surfaces, solar-ready design, and longer service lives than standard contractor-grade systems. That combination narrows the supplier pool and concentrates more spend among companies that can prove product performance, approvals, and installation support. Large event-linked construction programs also add timing discipline, since delivery deadlines force earlier supplier qualification and capacity planning. The result is a GCC roofing market in which long-cycle infrastructure execution carries more weight than short-term fluctuations in private construction sentiment.

Stricter GCC Green Building and Energy Codes Increasing Demand for Insulated and Reflective Roofing

Stricter building energy rules are moving the GCC roofing market toward insulated panels, reflective membranes, and higher-performance roof assemblies. Dubai's Al Sa'fat 2.0 Silver compliance from 2026, Saudi Arabia's SBC 601, Abu Dhabi's Estidama framework, and Qatar's Global Sustainability Assessment System (GSAS) are all pushing thermal performance to the forefront of roofing specifications. This shift matters because it sets a practical floor for insulation thickness, reflectance performance, and envelope quality in new commercial and industrial projects. It also increases the value of test data, environmental declarations, and formal approvals, which reduces the room for weaker suppliers in large tenders. As these frameworks spread, the GCC roofing market becomes less price-led and more compliance-led, especially in projects backed by public funding or major developers. The GSO’s adoption of Standard 3000:2025 strengthened this direction and gave specifiers a more consistent regional sustainability anchor[1]Gulf Organisation for Research and Development, “GCC Standardization Organization Adopts GSAS as Gulf Green Building Standard With Riyadh Workshop Qualifying 75 Professionals,” GORD, gord.qa.

Harsh GCC Weather Driving Demand for UV-Resistant, Waterproof, and Thermally Stable Roofing

Harsh weather keeps performance risk high across the GCC roofing market because rooftops face intense UV exposure, very high summer heat, sand abrasion, and coastal salinity. These conditions shorten the effective life of lower-grade systems and raise the operating cost of premature failure for building owners. The problem is not limited to heat, because salt crystallization, water exposure, and windblown particles also weaken exposed surfaces and waterproofing layers over time. This is creating replacement demand in assets installed during the earlier construction wave, especially where lower-grade materials were originally selected. It also supports a stronger demand for mineral-surfaced, re-coatable, and more UV-stable systems that can maintain performance over longer service intervals. Research on cool-roof reflectivity degradation supports the case for active maintenance and better-quality exposed roof systems in demanding climates.

Rising Rooftop Solar Integration Demand

Rooftop solar is widening the addressable scope of the GCC roofing market because roof systems now need to support both enclosure performance and on-site power generation. The clearest shift is in industrial and logistics assets, where owners increasingly want roofs that can carry added loads, avoid membrane penetrations, and preserve waterproofing warranties after solar installation. This requirement favors mechanically fastened metal systems and single-ply membranes over legacy systems that are harder to adapt for long-term solar use. It also pushes suppliers to think at system level, since structural support, thermal reflectance, waterproofing, and maintenance access now need to work together. In practice, solar compatibility is becoming part of standard evaluation rather than an optional upgrade in new projects and in reroofing decisions. That is gradually lifting the performance threshold across the GCC roofing market even where the final roofing volume mix changes only in stages.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility and Import Dependence | -0.5% | GCC-wide, with acute relevance in Saudi Arabia and the UAE | Short term (≤ 2 years) |

| High Upfront Cost of Premium Sustainable Roofing | -0.4% | Saudi Arabia mid-tier commercial projects, Oman, Bahrain, Kuwait, and SME buyers | Medium term (2-4 years) |

| Project Delays and Giga-Project Recalibration Risks | -0.4% | Saudi Arabia, with spillover into UAE and Qatar contractor chains | Medium term (2-4 years) |

| Performance Degradation from Dust, Salinity, and Water Exposure | -0.3% | Coastal GCC markets and arid inland zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility and Import Dependence

Raw material volatility remains a restraint on the GCC roofing market because bitumen and steel costs can change quickly and compress fabricator margins. Modified bitumen producers remain exposed to petroleum-linked input pricing, while metal roofing suppliers depend heavily on imported coil and stable shipping conditions. That exposure matters more in the GCC because project pricing is often locked in before installation schedules are fully certain. When logistics disruptions affect freight routes, membrane and metal producers can face rising feedstock cost and delivery risk at the same time. This makes margin protection harder for suppliers without local manufacturing or stronger sourcing flexibility. Producers with domestic supply access or in-country production therefore carry a structural advantage in tender competitiveness, lead time control, and project continuity.

High Upfront Cost of Premium Sustainable Roofing

The higher installed cost of premium sustainable roofing slows parts of the GCC roofing market, especially in smaller projects and cost-sensitive commercial upgrades. Single-ply systems, insulated metal assemblies, and PIR sandwich panels can deliver better lifecycle economics, but many buyers still prioritize initial capital outlay over longer-term savings. The tension is especially evident in reroofing, where owners must balance energy performance, operational continuity, and structural maintenance within limited budgets. Mid-cycle value engineering can therefore downgrade roofing specifications even when a higher-grade system would reduce operating risk over time. Compliance frameworks in the United Arab Emirates (UAE) and Saudi Arabia are reducing the room for those downgrades in some project categories. Even so, smaller GCC markets and mid-tier developments remain more vulnerable to cost-led substitution toward lower-performance roofing options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Membranes Anchor Market While Metal Systems Accelerate

Bituminous/modified bitumen membranes held 31.5% of the GCC roofing market share in 2025, reflecting the dominance of flat roofs across commercial and industrial buildings in the region. Their lead also came from mature contractor familiarity, broad supply availability, and suitability for large low-slope roof decks that dominate many GCC project formats. APP-modified products with softening points above 115°C remain valued because they perform better than unmodified bitumen under harsh temperature cycles and exposed conditions. Metal roofing is projected to expand at a 5.5% CAGR through 2031, helped by logistics parks, manufacturing facilities, and pre-engineered buildings that value speed of installation, long spans, and thermal efficiency.

Standing seam steel systems and insulated sandwich panels are gaining favor because they combine thermal control, structural clarity, and solar-mounting compatibility in a single roof build-up. Single-ply membranes are also gaining ground in commercial and industrial reroofing, especially where white-surface reflectivity, UV resistance, and solar compatibility are being specified together. Asphalt shingles, clay, and concrete tiles remain more limited in the GCC roofing market and are concentrated in villa or residential formats, where sloped rooflines are still common. Wood roofing remains a niche because fire-safety compliance and climate suitability are difficult to achieve across most GCC end uses. The Others category includes spray polyurethane foam systems and elastomeric liquid-applied coatings, which are benefiting from demand for re-coatable flat-roof solutions and easier maintenance cycles. Research on building-integrated photovoltaics in Saudi climate conditions supports the case for cool, UV-stable roof assemblies, thereby strengthening demand for high-SRI metal, TPO, and other advanced systems [2]PLOS One, “Energy Assessment of BIPV System in Code-Compliant Residential Building in Cooling-Dominated Climates,” PLOS One, plos.org .

By Construction Type: New Construction Leads, Reroofing & Replacement Closing the Gap

New construction accounted for a 74% of the GCC roofing market in 2025, reflecting the scale of greenfield housing, tourism, industrial, and mixed-use development across the region. That dominance still coexists with a clear change in purchasing behavior as earlier commercial and industrial stock reaches major maintenance intervals. Reroofing & replacement is forecast to grow at a 5.98% CAGR through 2031, which should increase demand for lighter, mechanically fastened, and cold-applied systems that minimize disruption in occupied buildings. This sub-segment often supports higher selling prices because warranty risk, roof access constraints, and installation complexity are greater than in greenfield work. The primary structural driver behind this shift is straightforward. Numerous buildings constructed during the 1990s and early 2000s are now entering their major replacement window.

New-build demand in the GCC roofing industry is also becoming more segmented by project tier, with mega-projects opting for longer-life systems and mid-market projects still prioritizing lead time and price. Flagship developments tied to national diversification plans are raising the bar for warranty periods, weathering performance, and formal approvals, going beyond standard contractor-grade offers. That split favors international system suppliers in the premium channel while leaving room for local fabricators in standard specifications and repeat-contractor jobs. Contractors on larger projects also increasingly prefer FM-approved or similarly documented roof systems because specification risk is lower and insurance or owner requirements are easier to meet. Kingspan's Dammam facility, which produces locally FM-approved roofing insulation for Saudi projects, demonstrates how suppliers are moving closer to the GCC roofing market to meet local content requirements and shorten delivery cycles.

By Application: Commercial Concentration With Industrial Growth Momentum

Commercial applications accounted for 33% of the GCC roofing market in 2025, supported by concentrated hospitality, retail, office, and mixed-use construction in the region's leading urban centers. Industrial applications are projected to rise at a 5.7% CAGR through 2031, making them the fastest-growing use case in the GCC roofing market. This pattern reflects industrial zone expansion, bonded warehousing, manufacturing localization, and growing data center activity across Saudi Arabia and the United Arab Emirates (UAE). Large-span industrial buildings also require roofing systems that combine waterproofing, thermal control, structural clarity, and solar-readiness at scale. That makes industrial procurement one of the strongest channels for metal panels, insulated assemblies, and higher-performance membrane systems.

Residential demand benefits from housing programs and villa construction, but its lower installed value per square meter limits revenue share compared with commercial and industrial work. Institutional demand remains specification-led because hospitals, schools, and government facilities place greater weight on lifecycle performance, formal approvals, and long-term maintenance certainty. Infrastructure-related applications in transport and utilities add steady baseline demand where flat-roof or low-slope assemblies are common. The others category remains smaller, but it benefits from airport, metro, port, and utility expansion across the GCC. Across the GCC roofing industry, the growth of rooftop solar and tighter sustainability standards is pushing more application segments toward reflective, insulated, and warranty-backed roof systems.

Geography Analysis

Saudi Arabia accounted for 45% of the GCC roofing market in 2025, making it the largest market in the region. Its lead rests on the breadth of Vision 2030 activity across tourism, residential development, sports venues, industrial corridors, and large mixed-use destinations. The Saudi market also benefits from a large installed base of older commercial buildings that will need replacement roofing as energy codes and maintenance standards tighten. Localization is becoming more important because public and large private projects increasingly favor suppliers with in-kingdom production and approval credentials. Sika's acquisition of Riyadh-based Gulf Seal in November 2025 reflected that logic and strengthened access to Saudi membrane and waterproofing demand.

The United Arab Emirates (UAE) is set to record the fastest expansion in the GCC roofing market, with a 5.9% CAGR projected over 2026-2031. Growth is supported by dense construction activity in Dubai and Abu Dhabi, along with tighter sustainability-led specification requirements in new projects. The market is also seeing stronger demand for roofing assemblies that can accommodate rooftop solar without compromising waterproofing performance or roof access. Nakheel's April 2026 award of AED 3.5 billion (approximately USD 953 million) in contracts for 544 villas on Palm Jebel Ali shows the scale of residential construction, which is still feeding roofing demand in Dubai. The United Arab Emirates (UAE) also has one of the more developed reroofing pools in the region because older commercial stock in Dubai and Abu Dhabi is moving deeper into replacement age.

Qatar, Oman, Kuwait, and Bahrain together make up the balance of the GCC roofing market, with Qatar leading this group through industrial and major-project maintenance activity. Qatar's GSAS framework has also influenced the broader regional sustainability standard, GSO 3000:2025, which supports higher-performance roofing specifications across member states. Oman is adding demand for UV- and salt-resistant systems due to its coastal development profile and maritime exposure. Kuwait and Bahrain are smaller markets, but procurement standards are gradually aligning with the same regional push toward better thermal, waterproofing, and durability performance.

Competitive Landscape

The GCC roofing market is moderately consolidated. Multinational suppliers such as Sika GCC, Kingspan UAE, and Saint-Gobain's Izomaks benefit from system warranties, approval depth, and regional manufacturing links that matter in large tenders. Local producers such as TSSC Group, Bitumat, Awazel, SAHARA Insulation Factory, Arkaz, and other established fabricators remain competitive where delivery speed, contractor familiarity, and price discipline are decisive. This creates a two-track competitive structure in which premium projects reward documented system performance, while routine projects still allow room for regional price competition. The GCC roofing market, therefore, does not operate as a winner-takes-all space, but it is becoming more selective at the top end.

A key strategic move came in November 2025 when Sika acquired Gulf Seal in Saudi Arabia, giving it local membrane production, regional export reach, and stronger access to Vision 2030-linked demand[3]Sika AG, “Sika Reports Full-Year 2025 Results, Executing Plan to Accelerate Growth,” Sika, sika.com. Sika's 2025 full-year results then reported double-digit growth in the Middle East and Africa, which supported the case for continued investment in the region. Another important move was Kingspan Insulation's Dammam facility, which added local capacity for roofing insulation and improved supply responsiveness for Saudi projects. TSSC Group also retains structural strength through manufacturing scale and longstanding contractor relationships, supported by Gulf Investment Corporation's 30.7% stake. These examples show that competitive advantage in the GCC roofing market is increasingly tied to local production, approval status, and the ability to serve complex project scopes rather than only product availability.

The next area of competition is likely to center on solar-ready roofs, high-SRI systems, and re-coatable solutions for aging commercial stock. Suppliers that can combine waterproofing, insulation, and solar compatibility within one offer are better positioned as procurement teams ask for integrated roof performance. Compliance requirements under GSO 3000:2025 and similar national frameworks will likely widen the gap between specification-grade suppliers and commodity traders. That should keep the GCC roofing market open to further consolidation at the top even as a wide base of regional installers and fabricators remains active.

GCC Roofing Industry Leaders

TSSC Group

Sika GCC

Bitumat

Izomaks (Saint-Gobain)

Zamil Steel / BCOMS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kingspan Insulation inaugurated its manufacturing facility in Dammam, Saudi Arabia. The newly operational Dammam facility of Kingspan Insulation caters to the Saudi market, producing Heating, Ventilation, and Air Conditioning (HVAC) ductwork insulation, building insulation boards, and FM-approved roofing insulation products. This move not only curtails the nation's reliance on imports but also accelerates delivery timelines for significant projects under the Vision 2030 initiative.

- April 2026: Nakheel, a subsidiary of Dubai Holding Real Estate, has awarded contracts worth over AED 3.5 billion (USD 953 million) to Ginco and UNEC for the construction of 544 villas on Palm Jebel Ali. This significant residential construction initiative is poised to drive a robust demand for premium roofing systems and waterproofing assemblies in Dubai.

- November 2025: Sika has acquired Gulf Seal (Awazil Al Khaleej Industrial Co.), a Riyadh-based manufacturer of bituminous waterproofing membranes with over 20 years of presence in the GCC market. This acquisition strengthens Sika's position to address the growing demand for construction chemicals and roofing membranes driven by Vision 2030 and the FIFA World Cup 2034.

GCC Roofing Market Report Scope

The GCC Roofing Market Report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, and more), Construction Type (New Construction, and Reroofing & Replacement), Application (Residential, Commercial, Industrial, Institutional, and Others), and Geography (United Arab Emirates, Saudi Arabia, Oman, Qatar, Kuwait, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing & Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Oman |

| Qatar |

| Kuwait |

| Bahrain |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing & Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Oman | |

| Qatar | |

| Kuwait | |

| Bahrain |

Key Questions Answered in the Report

What is the expected value of GCC roofing by 2031?

The GCC roofing market is projected to reach USD 3.54 billion by 2031, rising from USD 2.99 billion in 2026 at a 3.43% CAGR over 2026-2031.

Which country leads regional demand?

Saudi Arabia led with 45% share in 2025, supported by its large pipeline of housing, tourism, industrial, and mixed-use projects.

Why is reroofing becoming more important across GCC countries?

Reroofing & replacement is forecast to grow at 5.98% CAGR because many commercial and industrial assets built in earlier cycles are reaching major maintenance intervals.

How are sustainability rules changing roofing selection in the region?

Codes and standards are pushing buyers toward insulated, reflective, solar-ready, and better-documented systems, which is lifting demand for specification-grade roofing assemblies.

Page last updated on: