ASEAN Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

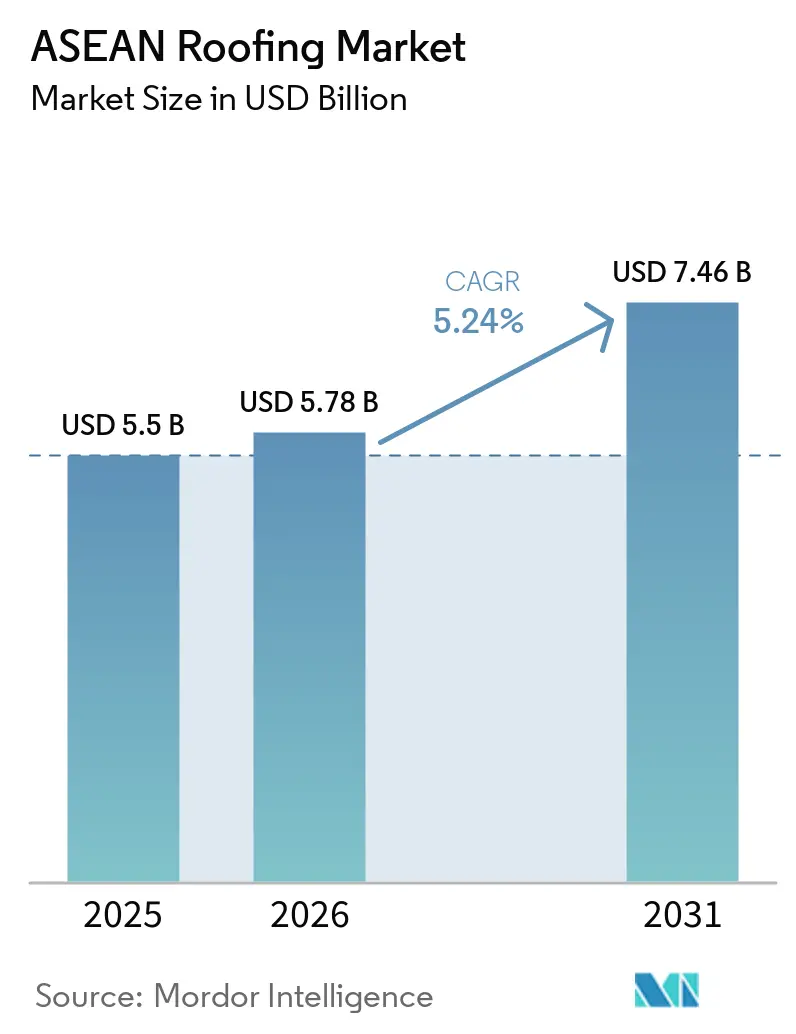

| Base Year Market Size (2025) | USD 5.5 Billion |

| Market Size (2026) | USD 5.78 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Roofing Market Analysis by Mordor Intelligence

The ASEAN Roofing Market size is projected to be USD 5.5 billion in 2025, USD 5.78 billion in 2026, and reach USD 7.46 billion by 2031, growing at a CAGR of 5.24% from 2026 to 2031.

The ASEAN roofing market is being supported by two steady demand pools, mass residential construction and expanding industrial and logistics real estate, while public infrastructure spending is adding a firm base of project activity across the region. Indonesia is keeping demand stable through a state-backed renovation drive for 2 million substandard homes, supported by Rp 43.6 trillion (USD 2.65 billion), which is turning housing policy into a direct volume for roofing replacements. Vietnam is adding another layer of support with 158,723 social housing units targeted for 2026 and a wider 973,471-unit pipeline through 2030, while public investment disbursements are rising and construction output is expected to strengthen in parallel. Lower intra-ASEAN trade barriers and the 2026 Passive Cooling Roadmap are also pushing the ASEAN roofing market toward higher-value reflective, insulated, and system-based products instead of basic commodity sheets in many public and institutional projects. At the same time, steel, bitumen, and petrochemical price swings are keeping the ASEAN roofing market split between volume suppliers competing on price and premium suppliers defending margins through warranty, performance, and specification support.

Key Report Takeaways

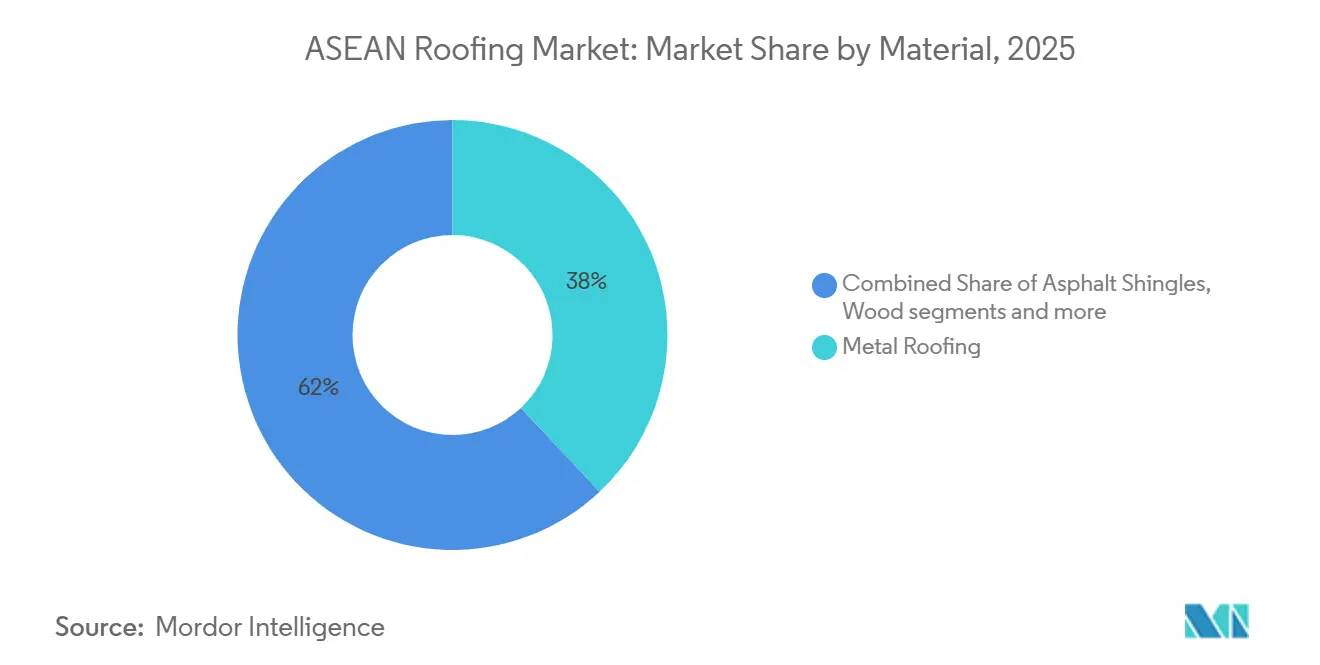

- By material type, metal roofing accounted for 38% of revenue in 2025, while single-ply membranes are projected to expand at a 6.4% CAGR through 2031.

- By construction type, new construction accounted for 64% of 2025 revenue and also leads growth with a 5.9% CAGR through 2031.

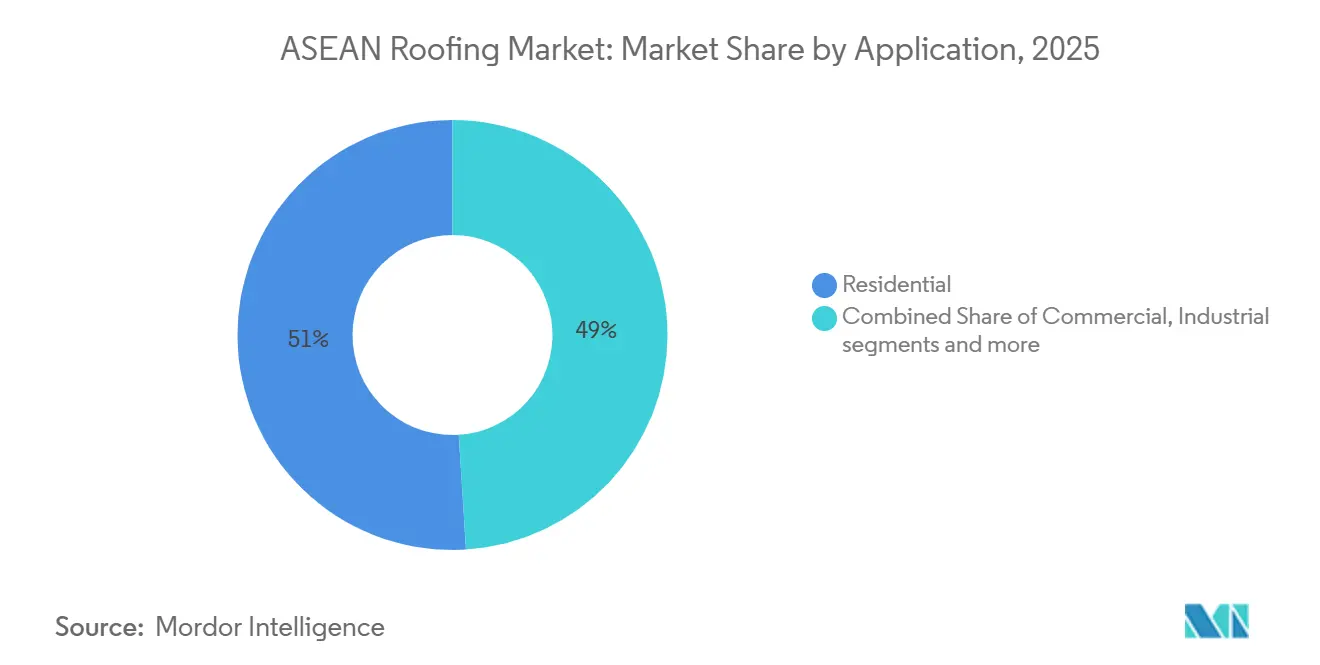

- By application, residential accounted for 51% of the ASEAN roofing market size, while commercial is forecast to record the fastest growth at a 6.0% CAGR through 2031.

- By geography, Indonesia held 35% of the ASEAN roofing market share in 2025, while Vietnam is expected to grow at the fastest pace with a 6.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Housing and Infrastructure Pipelines Expanding Roofing Demand | +1.4% | Indonesia, Vietnam, Philippines, Thailand | Short term (≤ 2 years) |

| Green Building and Thermal Performance Rules Supporting Cool and Insulated Roofs | +0.9% | ASEAN-wide, with strongest compliance in Singapore, Vietnam, Thailand | Medium term (2-4 years) |

| Industrial, Logistics, Cold Chain, and Data Center Build Out Increasing Demand for Insulated Panels and Membranes | +0.8% | Indonesia, Thailand, Vietnam, Singapore | Medium term (2-4 years) |

| Tropical Humidity, Monsoon Exposure, and Leakage Risk Lifting Waterproofing Intensity | +0.6% | Philippines, Indonesia, Vietnam | Short term (≤ 2 years) to Medium term (2-4 years) |

| Green Roofs, Siphonic Drainage, and Stormwater Features Adding Premium Content | +0.3% | Singapore, Thailand, Vietnam urban centers | Long term (≥ 4 years) |

| Lower Intra-ASEAN Trade Barriers Improving Access to Premium Roofing Inputs | +0.3% | ASEAN-wide | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Housing and Infrastructure Pipelines Expanding Roofing Demand

Government-backed housing schemes are providing a reliable support base for the ASEAN roofing market as private construction moves unevenly. In Indonesia, the renovation of 2 million substandard dwellings by the end of 2025, backed by Rp 43.6 trillion (USD 2.65 billion), is directly driving roofing replacement demand in provinces with large housing deficits such as West Java, Banten, and Central Java. In Vietnam, more than 102,600 social housing units were completed in 2025, which exceeded the annual plan, and the 2026 target rises to 158,723 units, with stronger public investment disbursement behind it. These programs matter because they sustain roofing volume even when private housing starts slow, and they create clearer order visibility for manufacturers and contractors. They also encourage the use of certified, standardized materials in mass housing, gradually reducing the role of informal or recycled roofing inputs and broadening the formal, addressable base of the ASEAN roofing market.

Green-Building and Thermal-Performance Regulation Tightening Roof Specifications

Regulations around building envelope performance are steadily changing product choice in the ASEAN roofing market. The International Energy Agency (IEA) roadmap for energy-efficient buildings in ASEAN identifies roofs as the critical thermal boundary in tropical climates. It highlights cool roofs, green roofs, and passive ventilation as practical measures to reduce cooling demand. The Passive Cooling Roadmap launched by the ASEAN Centre for Energy (ACE) and the United Nations Environment Programme (UNEP) in April 2026 goes further by recommending mandatory passive cooling requirements in national building codes and identifying reflective roofs as a leading intervention[1]ASEAN Centre for Energy and United Nations Environment Programme, “ACE and UNEP Launch Passive Cooling Roadmap to Protect Communities and Cities from Rising Heat Risks in ASEAN,” ASEAN Centre for Energy, aseanenergy.org. Once green certification systems become a practical requirement for project financing or public procurement, buyers tend to purchase compliant roof assemblies rather than isolated low-cost components. That dynamic supports reflective, insulated, and integrated roof systems and moves the ASEAN roofing market away from purely commodity purchasing in institutional and commercial projects.

Industrial, Logistics, and Data Centre Build Out Driving Insulated Metal Panel Demand

Industrial expansion is changing the product mix of the ASEAN roofing market, not just lifting total volume. Large logistics sheds, cold-chain assets, and data centers require roofing systems that span wide areas, manage heat, and minimize operational disruption during installation or replacement. That requirement is favoring insulated sandwich panels for temperature-sensitive buildings and low-downtime single-ply membrane systems for highly specified facilities in Singapore, Jakarta, and Kuala Lumpur. The result is a structural ceiling on the role of uninsulated corrugated sheet in these projects, especially where thermal conductivity and fire-rating thresholds are built into the design brief. This shift is important because it lifts average revenue per square meter above residential levels and gives premium suppliers a stronger position in the ASEAN roofing market.

Tropical Climate and Monsoon Exposure Reinforcing Premium Waterproofing Specification

Climate exposure remains a basic but powerful demand driver in the ASEAN roofing market. The Philippines faces repeated typhoon landfalls, Indonesia records heavy annual rainfall in major population centers, and Vietnam’s coastal provinces deal with storm surges that test standard roof detailing, all of which raise the cost of under-specification in roofing systems. These conditions shorten the effective performance window of conventional bituminous and metal systems when waterproofing and penetration detailing are weak. ACE-linked passive cooling guidance also references findings that higher solar reflectance on residential roofs can reduce cooling loads by 18% to 93% and cut peak cooling demand in air-conditioned buildings by 11% to 27%. That overlap between thermal control and moisture protection is encouraging buyers to source integrated roofing systems rather than separate waterproofing and insulation packages, which benefits suppliers with full-system offerings in the ASEAN roofing market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Cost Volatility in Bitumen, Resin, and Petrochemical Inputs Pressuring Margins | -1.2% | ASEAN-wide, most acute in Indonesia and Vietnam | Short term (≤ 2 years) |

| Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption | -0.8% | Indonesia, Philippines, Rest of ASEAN | Medium term (2-4 years) |

| Competition from Lower Cost Substitute Materials Capping Pricing Power | -0.6% | Indonesia, Philippines, Vietnam rural and peri-urban | Short term (≤ 2 years) to Medium term (2-4 years) |

| Import Dependence and Uneven Regional Standards Complicating Supply Decisions | -0.5% | Philippines, Rest of ASEAN | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Cost Volatility Compressing Project Economics and Supplier Margins

Input cost volatility is still one of the clearest brakes on the ASEAN roofing market. Bitumen, Polyvinyl Chloride (PVC) resin, Thermoplastic Polyolefin (TPO) compounds, and steel coil are exposed to global commodity cycles that often move out of step with local construction schedules and tender timelines. According to the Organisation for Economic Co-operation and Development's (OECD) 2025 Steel Outlook, fluctuations in pricing for strip and coil buyers, crucial for metal roofing manufacturers in ASEAN, may arise from capacity additions and inconsistent demand growth. In 2024 and 2025, those swings compressed supplier margins and pushed some contractors toward downgraded material choices when protecting bids became difficult. Manufacturers without hedging capacity, long-term sourcing arrangements, or some level of input integration remain more exposed during long project cycles in the ASEAN roofing market.

Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption

Installer availability is limiting how quickly the ASEAN roofing market can shift toward advanced roofing systems. Single-ply membranes, vegetated roofs, and siphonic drainage assemblies depend on trained crews and correct installation methods, especially where warranty protection is tied to seam quality or manufacturer certification. This gap is most evident in Indonesia, the Philippines, and parts of Vietnam, where the design intent of a premium roof system does not always align with the local execution capacity. In practice, that can delay projects or force substitutions to simpler, lower-value materials during value engineering. The companies that can build installer networks, training partnerships, and easier-to-install product formats are therefore in a stronger position to capture the premium side of the ASEAN roofing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Metal Roofing Anchors Revenue While Membranes Close the Gap

Metal roofing accounted for 38% of the ASEAN roofing market in 2025, making it the largest material category across the region. Its position is tied to broad use in industrial warehousing, peri-urban housing, and public projects where speed of installation and cost per square meter remain central buying criteria. The category also benefits from the region’s manufacturing and logistics build-out, as large-span, low-slope roofs commonly default to profiled metal sheets, sometimes paired with insulated composite layers. The OECD’s 2025 steel outlook reinforces this backdrop by identifying ASEAN as one of the few regions where steel demand is expected to grow strongly through 2030. In the ASEAN roofing market, this gives metal roofing manufacturers a material supply base that remains strategically important even when prices are volatile.

Single-ply membranes are projected to grow at a 6.4% CAGR in the ASEAN roofing market through 2031, making them the fastest-growing material group in the forecast period. Their demand is being led by data centers and high-specification commercial roofs in Singapore, Jakarta, and Ho Chi Minh City, where heat-welded systems are chosen for low seam-failure risk and short replacement shutdown windows. Clay and concrete tiles still retain cultural and architectural relevance in Thai and Vietnamese housing. Still, they face pressure to be replaced by lighter fiber-cement and metal options in multi-story applications. Asphalt shingles remain more concentrated in premium residential pockets in Thailand, Malaysia, and the Philippines. At the same time, bituminous membranes continue to serve flat commercial and industrial roofs because they have a familiar installer base and lower equipment needs than welded systems. Wood roofing is declining, while polycarbonate, uPVC, and fiber-cement sheets are gaining traction in affordable housing renovation, especially where certified heat-reflective, low-maintenance products align with state-backed renovation demand.

By Construction Type: New Construction Dominates but Replacement Economics Are Improving

New construction accounted for 64% of the ASEAN roofing market in 2025 and is forecast to expand at a 5.9% CAGR through 2031. That combination shows that the region is still driven more by first-time build activity than by mature replacement cycles. Indonesia’s large housing agenda and Vietnam’s social housing pipeline continue to support fresh roof installations at a scale that keeps new construction well ahead of reroofing in the ASEAN roofing market. This matters to suppliers because project capture depends heavily on contractor relationships, access to specifications, and fast delivery during the original build phase. It also explains why many manufacturers still organize their commercial strategy around broad distribution and first-install wins rather than repair-led aftermarket demand.

The replacement segment is smaller today, but it generates higher revenue per square meter when owners upgrade entire systems rather than replacing like-for-like sheets. The large installed base of metal roofs from 2005–2015 is nearing its renewal cycle, creating favorable conditions for replacement demand growth in the late 2020s and beyond. Commercial owners in markets such as Thailand and Singapore are paying closer attention to total ownership costs, which strengthens the case for more efficient reroofing systems. In the same direction, SCG reported that roofing lines within its Smart Value Product portfolio generated more than THB 993 million (USD 28.4 million) in Q1 2026, showing that premium performance at accessible price points can widen the replacement base without waiting for a large income step-up among end users.

By Application: Residential Scale Meets Commercial Momentum

Residential construction accounted for 51% of the 2025 value in the ASEAN roofing market, supported by the sheer number of housing units moving through state-backed programs across the region. Indonesia’s renovation and new-build housing programs, Vietnam’s expanding social housing pipeline, and similar residential construction activity across ASEAN collectively underpin a large and consistent base of annual roof installations. That scale makes residential demand less sensitive to short-term sentiment changes or financing cycles than many commercial categories. It also keeps volume-oriented product lines relevant even as more advanced systems gain traction in other parts of the ASEAN roofing market. Residential roofing, therefore, remains the broadest demand base, even when growth is faster elsewhere.

Commercial roofing is forecast to expand at a 6.0% CAGR through 2031, making it the fastest-growing application in the ASEAN roofing market. Office, retail, hospitality, and especially digital infrastructure projects are pushing this segment toward higher thermal, waterproofing, and durability standards than basic housing projects. Industrial and institutional applications are also meaningful because factories, cold-chain sites, schools, hospitals, and public buildings often need insulated or reflective assemblies rather than basic sheet products. Thailand’s building energy code framework for non-residential buildings has helped reinforce that direction by linking roof thermal performance to compliance expectations in public and private projects[2]Thailand Building Energy Code Reference, “Passive Cooling Strategies Practitioner Handbook,” Climate Technology Centre and Network, ctc-n.org. As a result, the ASEAN roofing industry is seeing faster value growth in applications where roof systems are purchased as part of whole-building performance rather than as stand-alone materials.

Geography Analysis

Indonesia held 35% of the ASEAN roofing market share in 2025, making it the largest market in the region. Its scale rests on a housing delivery agenda that combines new-build targets with subsidized renovation, creating both volume demand and a shift toward more formal materials channels in lower-income housing segments. The renovation of 2 million substandard homes with Rp 43.6 trillion (USD 2.65 billion) in funding is especially important because it turns public spending into immediate reroofing demand rather than only future pipeline potential. Indonesia also stands out because premium roofing demand is moving beyond cold-chain uses into pharmaceutical, institutional, and data-center projects. In the ASEAN roofing market, the combination of very large basic housing demand and rising specification-led industrial demand gives Indonesia a scale and value that other countries do not match.

Vietnam is forecast to expand at a 6.7% CAGR through 2031, making it the fastest-growing country in the ASEAN roofing market. The growth case is tied to a strong social housing pipeline, rising public investment disbursement, and a broader manufacturing hub strategy that is supporting industrial and infrastructure construction. Vietnam also has stronger pull for premium roofing systems because major projects and technical standards are raising the requirement for insulated and compliant roof assemblies. SCG’s PRIME subsidiary is expanding GP tile capacity from 19 million square meters in 2025 to a planned 25.6 million square meters in 2026, signaling confidence in both domestic demand and export opportunities from Vietnam into nearby markets.

Thailand remains a more mature part of the ASEAN roofing market, where growth is steadier, and product premiumization matters more than pure volume expansion. That is evident in SCG’s launch of the LumaX Series in Thailand, aimed at design-sensitive projects that value leak resistance, detailing, and integrated system performance over price alone. The Philippines is facing softer near-term conditions in the construction sector. However, residential permits still point to underlying housing demand that can continue to support basic roofing volume. The rest of ASEAN, led by Malaysia and Singapore, remains smaller in volume but remains important for premium membranes, green roofs, and other specialist systems, as product standards and specification practices in these markets often influence the wider ASEAN roofing market.

Competitive Landscape

The ASEAN roofing market is fragmented overall, as no company controls all major material categories across the region. Regional manufacturers such as SCG, Swissma Building Technologies, and Le Nam Megasheet are most visible in metal roofing and related products, where competition centers on price, fabrication capacity, and delivery speed. Global specialists such as Sika, SOPREMA, and Kingspan are stronger in membranes, waterproofing, and insulated panel systems, where technical approval, specification access, and installer certification matter more than simple volume reach. This split keeps the ASEAN roofing market competitive across a wide product perimeter and prevents a single supplier from dominating both commodity and premium roofing demand. It also means that market leadership often depends on the product segment under discussion rather than on a single clear regional winner.

Sika’s acquisition of Elmich Pte Ltd in February 2025 is a clear example of how premium players are using targeted deals to widen their roofing system offer. Elmich brought urban greening and green-roof capabilities that fit directly with Sika’s existing waterproofing and membrane portfolio in Singapore and the wider Asia Pacific region[3]Sika AG, “Sika Acquires Leading Green Roof Provider in Singapore,” Sika AG, sika.com. Kingspan made a similar move in March 2025 by acquiring Hao Wei in Malaysia, which gave it a local XPS insulation production base and reduced its dependence on imported supply for Southeast Asia. In a price-sensitive region, that type of local manufacturing step can narrow the landed-cost gap between high-performance systems and lower-cost alternatives.

SCG has also strengthened its position through product development and portfolio expansion in the ASEAN roofing market. The company launched the LumaX Series in Thailand in 2025 to target higher-value design requirements and reported more than THB 993 million (USD 28.4 million) in Q1 2026 revenue from roofing lines within its Smart Value Product portfolio. SCG Cement-Building Materials also acquired an 80% stake in Siam Coating Innovation Co., Ltd. in 2025, thereby improving its access to high-performance coating capabilities for fiber-cement, metal, and concrete roofs. As the ASEAN roofing market moves toward stronger specification requirements in Vietnam and Indonesia, the pressure on domestic volume players, regional champions, and global specialists is likely to intensify rather than ease.

ASEAN Roofing Industry Leaders

SCG

Thung Hing

Swissma Building Technologies

Le Nam Megasheet

LCP Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The ASEAN Centre for Energy (ACE) and the United Nations Environment Programme (UNEP) jointly launched the Passive Cooling Roadmap for the ASEAN Region in Manila, calling for mandatory passive-cooling and reflective-roof requirements in national building codes aligned with the ASEAN Plan of Action for Energy Cooperation (APAEC) 2026–2030. The roadmap's adoption by national planning ministries is expected to improve roof thermal performance specifications across public-sector construction procurement in all ASEAN-5 markets.

- December 2025: SCG positioned Vietnam as a key production and export hub within its Regional Optimization strategy, with its PRIME subsidiary announcing plans to expand glazed porcelain (GP) tile capacity from 19 million square meters in 2025 to 25.6 million square meters in 2026 through investments at the Pho Yen facility. The expansion strengthens domestic tile supply capacity for Vietnam's social housing, residential, and infrastructure construction pipeline.

- March 2025: Kingspan Group acquired Hao Wei, a Malaysia-based XPS insulation manufacturer, establishing Kingspan Insulation's first local manufacturing facility in Asia. The acquisition includes a polystyrene recycling facility aligned with Kingspan's Planet Passionate sustainability targets and immediately lowers supply-chain costs for flat-roof and cold-store applications across Southeast Asia.

ASEAN Roofing Market Report Scope

The ASEAN Roofing Market is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, Single-Ply Membranes, Wood, and Others), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, Industrial, and more), and Geography (Indonesia, Vietnam, Thailand, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| Indonesia |

| Vietnam |

| Thailand |

| Philippines |

| Rest of ASEAN |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | Indonesia |

| Vietnam | |

| Thailand | |

| Philippines | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the current outlook for ASEAN roofing demand through 2031?

The ASEAN roofing market stands at USD 5.78 billion in 2026 and is forecast to reach USD 7.46 billion by 2031 at a 5.24% CAGR, supported by housing, industrial projects, and public infrastructure.

Which material category leads roofing demand in ASEAN today?

Metal roofing leads with 38% of 2025 revenue because it suits industrial sheds, peri-urban housing, and public works where cost and installation speed matter most.

Which roofing materials are growing the fastest across ASEAN?

Single-ply membranes are the fastest-growing material segment with a 6.4% CAGR through 2031, driven by data centers, cold-chain assets, and other highly specified buildings.

Why is Vietnam growing faster than other ASEAN countries in roofing?

Vietnam is forecast to grow at a 6.7% CAGR through 2031 because of its social housing pipeline, rising public investment, and its role as a regional manufacturing hub.

Page last updated on: