United States Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

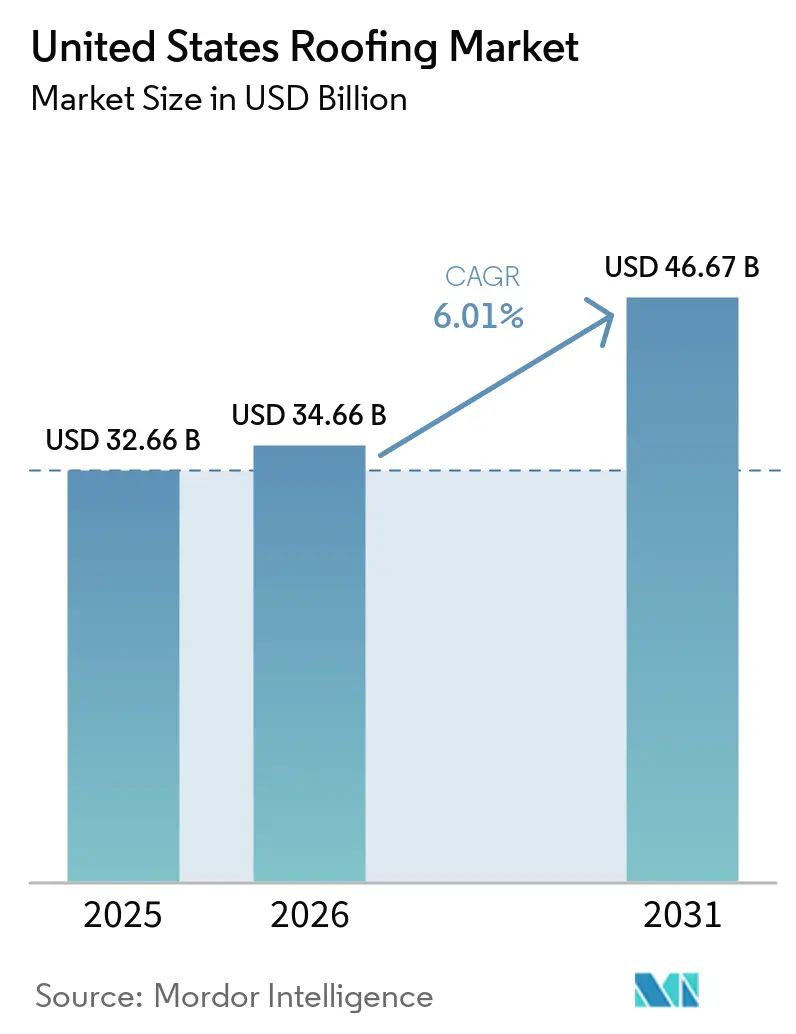

| Base Year Market Size (2025) | USD 32.66 Billion |

| Market Size (2026) | USD 34.66 Billion |

| Market Size (2031) | USD 46.67 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Roofing Market Analysis by Mordor Intelligence

The United States Roofing Market size is expected to grow from USD 32.66 billion in 2025 to USD 34.66 billion in 2026 and is forecast to reach USD 46.67 billion by 2031 at 6.01% CAGR over 2026-2031. Intensifying climate volatility, stricter building codes, and a compressing replacement cycle are sustaining demand even as residential permits ebb and flow. Hail and hurricane losses, together with insurance carriers shortening acceptable roof ages to 15-20 years, are driving a steady stream of re-roofing contracts. Infrastructure Investment and Jobs Act (IIJA) funds are enlarging the public-building pipeline, insulating contractors from private-sector cyclicality. At the same time, single-ply membranes are eating into asphalt’s share on commercial retrofits because they install faster, meet cool-roof mandates, and qualify for federal tax credits. Competitive dynamics are also tilting—vertically integrated material makers hold pricing power while private-equity platforms are stitching regional installers into national chains to secure volume discounts and roll out labor-saving installation technology.

Key Report Takeaways

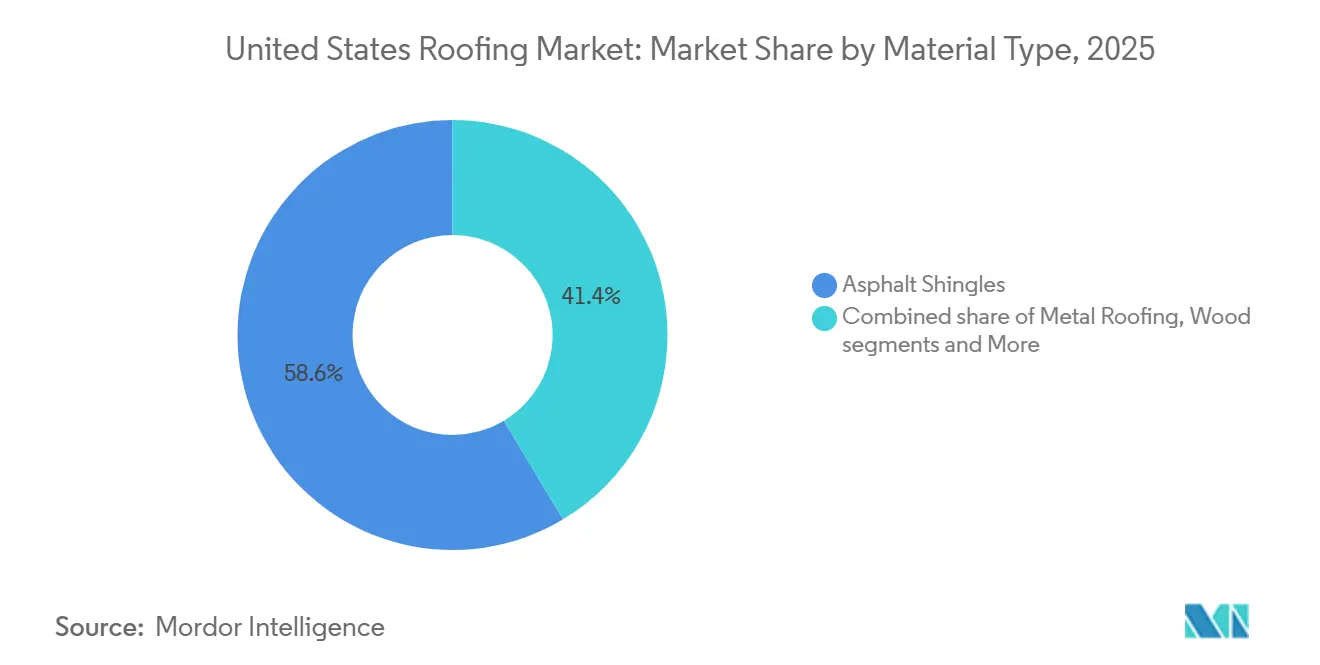

- By material type, asphalt shingles held 58.6% revenue share in 2025, while single-ply membranes are forecast to expand at a 7.69% CAGR through 2031.

- By construction type, reroofing and replacement accounted for 63.5% of revenue in 2025, while new construction is projected to grow at a 6.97% CAGR through 2031.

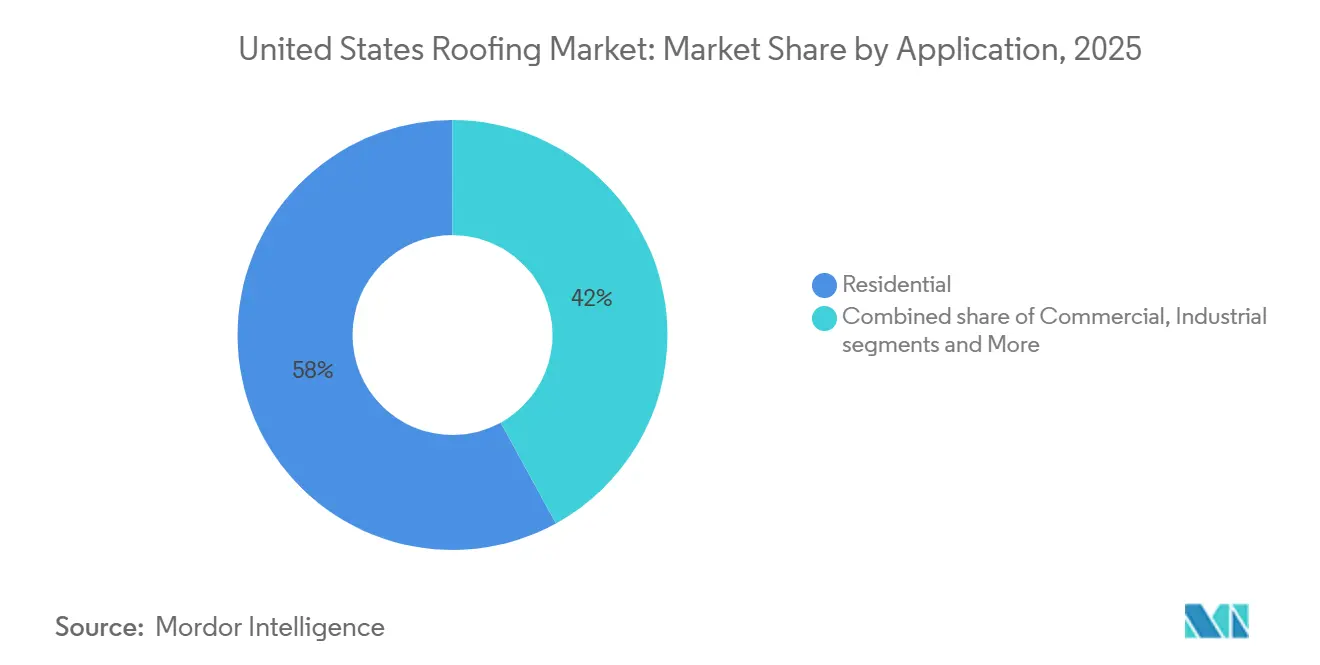

- By application, residential roofing captured 58% share in 2025, while commercial roofing is expected to advance at an 8.05% CAGR through 2031.

- By geography, the Southeast held 28.5% of revenue in 2025, while the Southwest is forecast to record the fastest regional growth at a 7.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging roof stock and higher replacement cycles | +1.8% | National, especially the Northeast and the Midwest | Long term (≥ 4 years) |

| Storm and hail events are raising insurance-funded reroofs | +1.5% | Southeast, Midwest, Southwest | Short term (≤ 2 years) |

| Energy-efficiency upgrades boosting cool-roof demand | +1.2% | Southwest, West, Southeast | Medium term (2–4 years) |

| Growth in logistics warehouses and data centers | +1.0% | Southwest, Southeast, Midwest | Medium term (2–4 years) |

| Solar-ready and PV-integrated roofing adoption | +0.9% | West, Southwest, and emerging Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Roof Stock and Higher Replacement Cycles Sustaining Reroofing Demand

More than one-third of U.S. owner-occupied homes were built before 2000, and the median roof age exceeded 17 years in 2025, moving millions of coverings beyond their typical service life. This demographic swell assures baseline work for contractors even when housing starts slow. Homeowners often upgrade to laminated shingles or metal during tear-offs, lifting ticket values by double digits. Insurers now request roof inspections when policies renew on homes older than 15 years, shortening the lag between failure and action. As a result, consistent replacement volume underpins the United States roofing market [1]U.S. Census Bureau, “American Housing Survey 2025,” census.gov.

Storm and Hail Events Increasing Insurance-Funded Roofing Activity

Severe convective storms generated more than USD 15 billion in roof-related claims across Texas, Oklahoma, and Iowa during 2024-2025. Carriers responded by insisting on impact-resistant shingles certified to UL 2218 Class 4 in high-risk zones. These premium products cost around 18% more but earn homeowners sizable premium credits, directing spend toward higher-margin materials. Florida’s revised wind codes after Hurricane Ian are also forcing early replacements of non-compliant roofs. Collectively, these conditions accelerate reroof cycles and elevate value per square.

Energy-Efficiency Upgrades Boosting Demand for Cool Roofs and Better Insulation Systems

The 2024 International Energy Conservation Code sets a solar-reflectance index minimum of 75 for low-slope roofs in warmer zones, while California’s Title 24 now requires reflective membranes on most commercial reroofs larger than 2,000 square feet. Utilities in Arizona and Nevada pay USD 0.10-0.15 per square foot for cool-roof installs, offsetting roughly 10% of material cost. Building owners record double-digit cuts in peak A/C loads, reaching payback in about four years. These gains reinforce the shift toward white TPO and PVC sheets that already meet reflectance targets out of the box.

Growth in Logistics Warehouses and Data Centers Expanding Commercial Roofing Installations

Warehouse ground-breaks rose to 450 million square feet in 2025, a 14% lift year over year, concentrated in Phoenix, Dallas, Atlanta, and Southern California. Each building spans acres of low-slope area that must support future solar arrays and heavy mechanicals, pushing specs toward thick-gauge TPO with 20-year warranties. Data-center power additions above 500 MW in Nevada alone translated into roughly 25 million square feet of new roof surface. Developers favor membranes that combine puncture resistance, reflectivity, and heat-welded seams to guard uptime, helping the United States roofing market to diversify beyond housing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages are raising installation costs | -0.8% | National, acute in the Northeast & the Midwest | Medium term (2–4 years) |

| Volatile asphalt, metal, and insulation prices | -0.6% | National, hits smaller firms harder | Short term (≤ 2 years) |

| Permitting, insurance, and warranty hurdles | -0.4% | Southeast, West, select metros | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages Limiting Contractor Capacity and Raising Costs

Roofing firms recorded vacancy rates of 12% in 2025 despite wage hikes to USD 28 per hour. Scarcity is sharpest in colder regions where an aging workforce lacks replacements. Contractors are buying robotic applicators and material lifts to offset head-count gaps, but equipment costs raise overhead. Extended lead times of eight to twelve weeks push some owners to defer projects, trimming near-term volume and tempering growth for the United States roofing market[2]National Roofing Contractors Association, “Annual Market Outlook 2026,” nrca.org.

Volatility in Asphalt, Metal, and Insulation Input Prices Pressuring Margins

Asphalt-shingle pricing swung by nearly one-fifth during 2024-2025 as oil and refinery outages disrupted supply. Coil-steel quotes moved between USD 800 and USD 1,100 per ton, and polyiso board climbed 8% alongside petrochemical feedstocks. Large contractors hedge with annual caps, but smaller firms pass surges to customers after 30-day lags, dulling competitiveness. Manufacturers have begun adding index clauses tied to commodities, introducing complexity to bids and stretching negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Asphalt Shingles Hold the Base While Membranes Lead the Next Value Shift

Asphalt shingles held 58.6% of the United States roofing market share in 2025, keeping them firmly in the lead across materials. Their scale reflects a wide installer network, familiar installation methods, strong residential distribution, and a reroofing cycle that still leans heavily toward shingle replacement. Owens Corning stated that the U.S. asphalt shingle market totaled 160 million squares in 2024, with 135 million squares from reroof and repair activity, indicating how much of the material base is tied to recurring replacement work rather than new construction. Owens Corning also noted in 2025 that laminate products accounted for 95% of shingle demand, indicating that the United States roofing market has already shifted away from standard 3-tab products toward higher-value laminated systems. That mix matters because laminates support better selling prices, stronger impact ratings, and better alignment with insurer preferences in hail-prone states.

The United States roofing market for single-ply membranes is forecast to grow at a 7.69% CAGR through 2031, making that group the fastest-growing material category. This expansion reflects stronger code alignment in low-slope commercial work, where reflective Thermoplastic Polyolefin, Ethylene Propylene Diene Monomer, and Polyvinyl Chloride systems better meet efficiency and maintenance requirements than many legacy alternatives. California’s current code direction and federal efficiency standards are helping move reroof specifications toward those systems, especially where owners want compliance and lower cooling loads in the same project. GAF’s 425,000-square-foot Thermoplastic Polyolefin plant in Valdosta, Georgia, which began production in September 2024, demonstrates that manufacturers are adding real capacity to this shift. Metal, modified bitumen, tile, wood, and other materials remain important in specific regional niches. However, the United States roofing market still relies on asphalt shingles for volume and on membranes for the strongest forward growth.

By Construction Type: Replacement Keeps the Core Stable, While New Build Adds Upside

Reroofing and replacement accounted for 63.5% of the United States roofing market in 2025, confirming that the largest revenue pool still comes from the installed roof base rather than from fresh starts. That position reflects storm repair, code compliance, insurer requirements, and the age profile of homes and commercial buildings, all of which keep work moving even when broader construction cycles weaken. Owens Corning stated in 2025 that more than 80% of its U.S. roofing demand came from nondiscretionary reroofing and storm activity, which aligns with the broader structure of the U.S. roofing industry. The replacement side of the United States roofing market also provides manufacturers and distributors with better demand visibility, as repair cycles repeat across regions each year. This makes reroofing the main volume anchor and the main stabilizer for channel throughput.

The United States roofing market for new construction is projected to grow at a 6.97% CAGR through 2031, putting it ahead of replacement in growth rate, even though it starts from a smaller base. The source draft tied this momentum to data centers, logistics facilities, and multifamily projects, which are all roof-intensive formats with larger roof spans and stricter performance requirements than much of the single-family market. U.S. data center construction spending above USD 31.5 billion in 2024 supports that view because it signals continued demand for large low-slope systems, insulation layers, and code-compliant accessories. This part of the United States roofing industry usually offers higher specification value per project, so it creates pricing opportunities even when volume remains lower than in reroofing. The result is a two-speed market in which replacement delivers steadier base demand and new construction creates selective upside where commercial activity is strongest.

By Application: Residential Dominates Revenue While Commercial Expands the Fastest

Residential roofing accounted for 58% of the United States roofing market share in 2025, keeping housing-related work at the center of overall demand. This reflects the scale of the single-family housing stock and the fact that many homes are moving into the first or second major replacement window for roof coverings installed years ago. Owens Corning’s investor materials pointed to a large U.S. single-family base and an aging roof stock, which support repeat-replacement demand even as mortgage affordability weakens and new home turnover declines. Residential demand in the United States roofing market is also shifting within the shingle mix, because Class 4 impact-resistant laminate products are gaining ground in hail-prone states where insurers reward stronger roof performance. keeps residential roofing broad, stable, and closely linked to maintenance and risk reduction rather than to discretionary exterior upgrades alone.

Commercial roofing is expected to grow at an 8.05% CAGR through 2031, making it the fastest-growing application in the United States roofing market. The strongest demand is coming from data centers, e-commerce fulfillment buildings, healthcare properties, and other large-footprint assets where low-slope membrane systems dominate the design. TopBuild’s July 2025 acquisition of Progressive Roofing for USD 810 million, with Progressive generating USD 438 million in annual revenue, 70% of which from nondiscretionary reroofing and maintenance, showed that strategic buyers see durable value in this space. Commercial work also benefits from tighter energy codes and higher owner focus on service life, reflectance, and maintenance planning, which raises the average system value per project. This is why the United States roofing market is seeing its fastest growth in commercial roofing, even as residential roofing remains the larger revenue base.

Geography Analysis

The South East accounted for 28.5% of the United States roofing market in 2025, making it the largest regional revenue contributor. Its lead comes from a combination of dense housing stock, repeated storm exposure, and strong logistics and data center development across states such as Georgia, Virginia, and Louisiana. Hurricane and wind exposure also push more owners toward stronger installation standards, and the Insurance Institute for Business and Home Safety has continued to promote the FORTIFIED Roof program to improve resilience and support insurance eligibility. That matters because higher resilience standards can lift both average project value and product quality in reroofing work. It also helps explain why the United States roofing market in the Southeast stays active across both residential replacement and commercial installations.

The South West is forecast to grow at a 7.27% CAGR through 2031, making it the fastest-growing region in the United States roofing market. Population inflows into Phoenix, Dallas-Fort Worth, Las Vegas, and the wider Texas corridor are supporting both new roof demand and the first replacement cycle for earlier suburban housing growth. Local code adoption is also important here, as warm-climate jurisdictions are placing greater weight on solar reflectance and thermal emittance in low-slope roofing. -Readiness adds another layer, and the Solar Energy Industries Association showed in December 2025 that Texas and California led the country in cumulative solar capacity, which lines up with more interest in photovoltaic-ready roofing systems.

The Midwest remains a key reroofing zone because hail frequency keeps replacement activity elevated, with State Farm reporting that Missouri ranked second nationally in 2025 hail claim payouts and the Kansas Insurance Department reporting USD 879 million in severe storm claims in Kansas during 2025. The North East continues to benefit from older housing stock, and Verisk identified states such as Massachusetts, Connecticut, New Jersey, and West Virginia in 2025 as having some of the highest shares of homes with less than 4 years of remaining shingle life. The West follows a different demand pattern because wildfire resilience, seismic requirements, and reflective roof compliance matter more in roofing decisions, especially in California. This balance across regions means no single area controls the full growth story, leaving the United States roofing market with several durable regional demand engines rather than a single narrow driver.

Competitive Landscape

A handful of vertically integrated manufacturers dominate materials, while contractors consolidate quickly. GAF Materials, Owens Corning, CertainTeed, and Carlisle together control more than 60% of asphalt shingle and single-ply membrane output. Their captive asphalt refineries and polymer plants buffer input volatility, allowing stable list pricing even when crude prices swing. Owens Corning posted USD 1.1 billion in Q3 2024 roofing revenue, up 8% year over year, while Carlisle logged USD 1.5 billion in its Construction Materials arm, up 11%.

Private equity reshaped distribution when QXO closed a USD 11 billion Beacon deal in January 2025, instantly controlling over 550 branches. Subsequent roll-ups by Shore Capital, Sun Capital, Percheron, and Brightstar extended similar scale plays into contracting, adding centralized procurement and drone inspections that cut bid times. These moves give large platforms tiered rebates and preferential freight terms from the big four manufacturers, widening the gap versus family-owned independents.

Innovation pivots on impact-resistant asphalt and labor-saving membranes. Standard Industries bought Malarkey Roofing in 2024 to acquire recycled-rubber Class 4 shingles commanding 20-30% premiums in hail zones. Manufacturers race to issue Environmental Product Declarations to qualify for GSA and IIJA work—GSA logged a 300% EPD jump in a single year. On the tech front, leading contractors deploy AI take-off software and autonomous drones while smaller firms still rely on manual tape pulls. Solar-integrated shingles remain niche because installed costs run USD 30,000-50,000, roughly quadruple conventional asphalt, though federal 25D credits may narrow that delta over time.

United States Roofing Industry Leaders

GAF Materials Corporation

Owens Corning

CertainTeed Corporation

Carlisle Companies Inc.

IKO Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Construction company Allstate reported USD 1.24 billion in Q1 2026 pretax catastrophe losses, including USD 925 million in March alone from 15 wind and hail events; the scale of losses is accelerating insurer requirements for impact-resistant roofing upgrades across policy renewals in storm-exposed states.

- February 2026: McElroy Metal acquired Fabral to consolidate standing-seam capability and widen Southeast and Midwest coverage.

- January 2026: Cornerstone Building Brands introduced SunSteel metal panels with factory PV rails, offering sub-seven-year payback in sunny farm belts.

- November 2025: Owens Corning closed a USD 3.9 billion deal for Masonite, broadening its exterior-envelope lineup .

United States Roofing Market Report Scope

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| North East |

| Mid West |

| South East |

| West |

| South West |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | North East |

| Mid West | |

| South East | |

| West | |

| South West |

Key Questions Answered in the Report

What is driving growth in U.S. roofing demand through 2031?

An aging roof base, recurring storm damage, stronger energy code compliance, and rising commercial activity in data centers and logistics buildings are supporting growth.

How large is the United States roofing market in 2026, and where is it headed by 2031?

The market is estimated at USD 32.5 billion in 2026 and is projected to reach USD 41 billion by 2031, with a 6.01% CAGR.

Which roofing material leads revenue in the United States?

Asphalt shingles led with 58.6% share in 2025 because they remain the standard choice in residential reroofing and have the deepest installer and distribution base.

Which roofing material is growing the fastest in the United States?

Single-ply membranes are forecast to grow the fastest at a 7.69% CAGR through 2031 as code-compliant low-slope commercial roofing shifts toward reflective membrane systems.

Why is commercial roofing growing faster than residential roofing?

Commercial roofing is benefiting from large-footprint projects such as data centers, warehouses, and healthcare facilities, and the segment is expected to expand at an 8.05% CAGR through 2031.

Which U.S. region leads roofing demand, and which one grows the fastest?

The South East led with 28.5% share in 2025, while the South West is expected to post the fastest growth at a 7.27% CAGR through 2031.

Page last updated on: