Asia-Pacific Roofing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

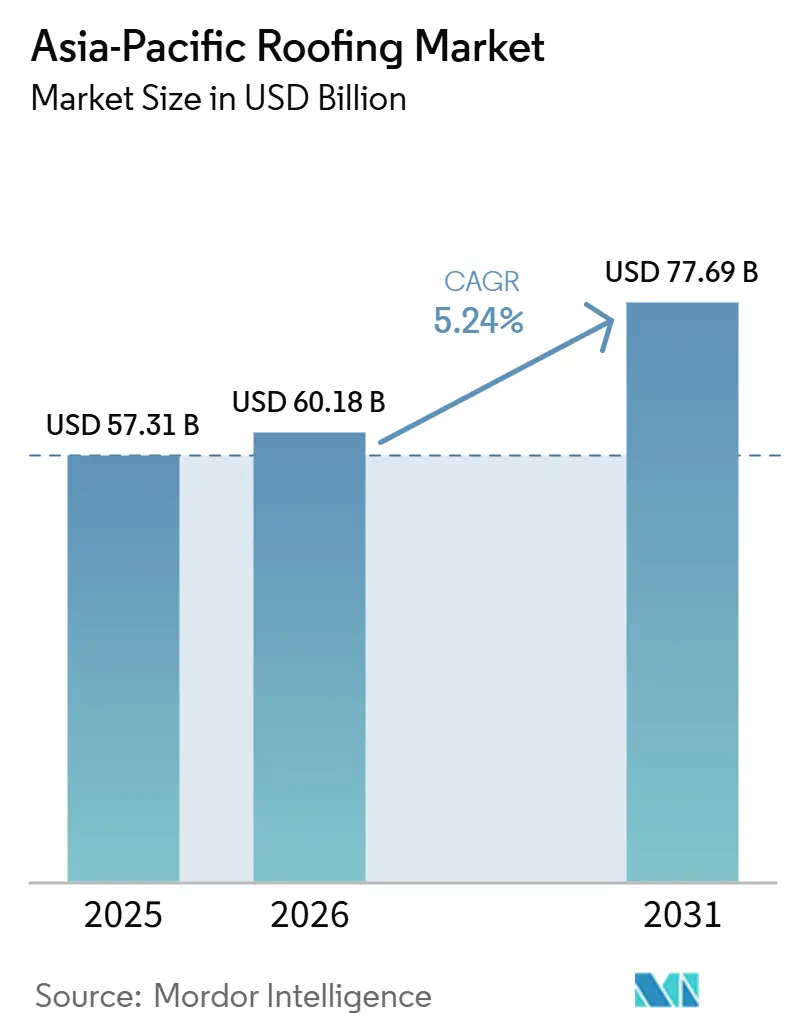

| Base Year Market Size (2025) | USD 57.31 Billion |

| Market Size (2026) | USD 60.18 Billion |

| Market Size (2031) | USD 77.69 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Roofing Market Analysis by Mordor Intelligence

The Asia-Pacific Roofing Market size is expected to increase from USD 57.31 billion in 2025 to USD 60.18 billion in 2026 and reach USD 77.69 billion by 2031, growing at a CAGR of 5.24% over 2026-2031.

Demand across the Asia-Pacific roofing market is supported by rapid urban growth in South and Southeast Asia, along with steady replacement demand in Japan, Australia, and South Korea, where aging building stock is moving into planned renewal cycles. Thermal performance rules are also raising the baseline for roof specifications across both residential and non-residential construction, pushing buyers toward coated steel, membranes, and other higher-performing systems. The region’s diverse climate, from cyclone-prone coasts to hot inland zones and high-rainfall urban corridors, supports parallel demand for multiple roof system types rather than a single dominant solution. The Asia-Pacific roofing market also remains structurally diverse because construction-led and renovation-led demand are both active simultaneously, giving suppliers room to compete across volume, compliance, and premium project tiers. Even with raw material pressure and regulatory complexity, the market outlook remains durable because climate adaptation and energy efficiency are now moving from optional upgrades to standard procurement requirements in several large countries.

Key Report Takeaways

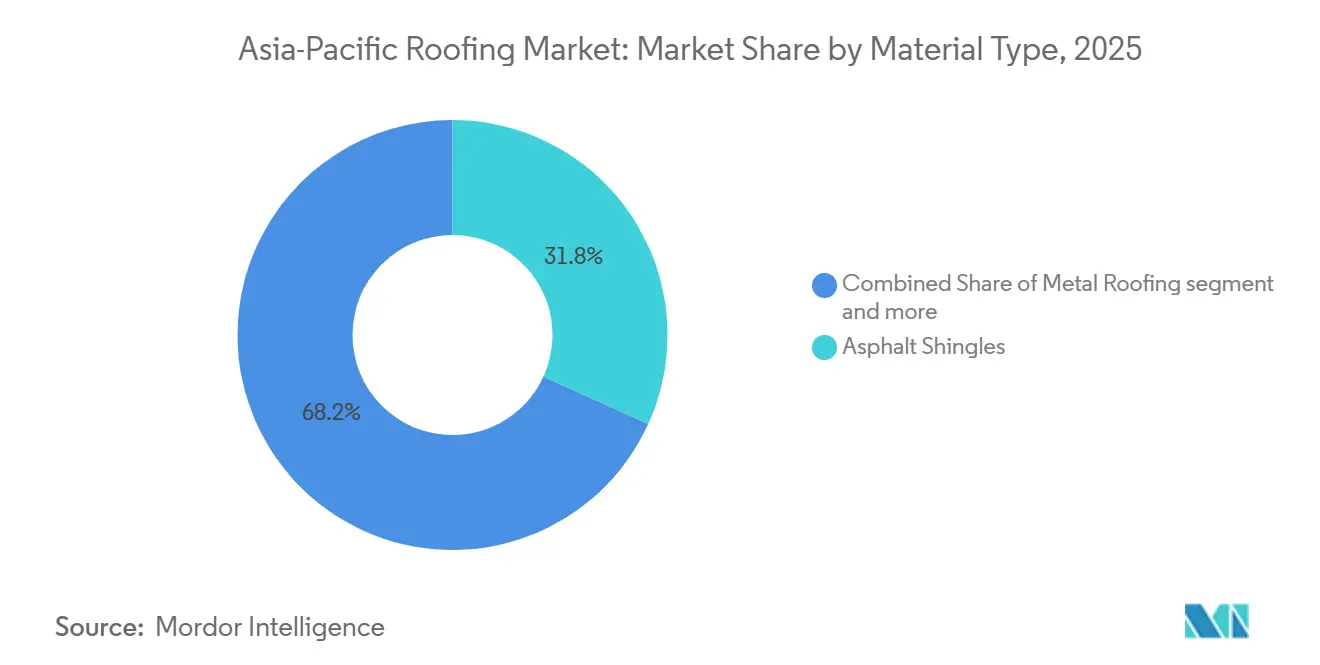

- By material type, asphalt shingles led with 31.8% of the Asia-Pacific roofing market share in 2025, while single-ply membranes are forecast to grow at a 6.8% CAGR through 2031.

- By construction type, reroofing and replacement held 58.4% of the market in 2025, while new construction is projected to expand at a 5.9% CAGR through 2031.

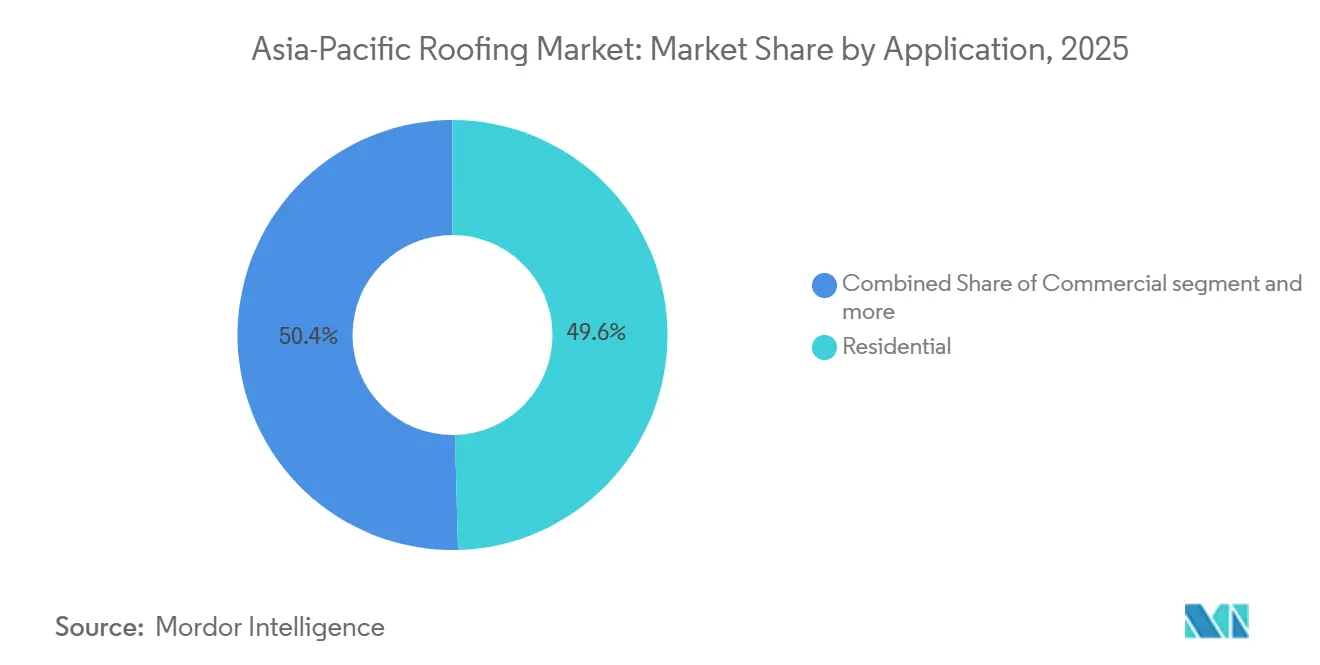

- By application, residential accounted for a 49.6% share of the Asia-Pacific roofing market size in 2025, while the industrial segment is advancing at a 6.2% CAGR through 2031.

- By geography, China held 43.7% of the Asia-Pacific roofing market share in 2025, while India recorded the highest projected CAGR at 7.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and Infrastructure-Led Roofing Demand | +1.4% | APAC-wide, concentrated in India, Southeast Asia, and China | Long term (≥ 4 years) |

| Reroofing and Renovation Demand Expansion | +1.0% | Japan, Australia, South Korea, with growing uptake in China urban renewal | Medium term (2-4 years) |

| Shift Toward Energy-Efficient and Cool-Roof Systems | +0.8% | India, Australia, China, Singapore, with spillover to Southeast Asia | Medium term (2-4 years) |

| Weather Resilience and Durable-Roof Adoption | +0.6% | Southeast Asia, Pacific corridor, and India’s cyclone-prone coastal states | Short term (≤ 2 years) |

| Subnational Cool-Roof Mandates Accelerating Premium Roof Specifications | +0.4% | India, Australia, and Singapore | Medium term (2-4 years) |

| Data-Center Buildout Creating Demand for High-Performance Roofing Systems | +0.3% | Singapore, Malaysia, India, China, and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction and Infrastructure-Led Roofing Demand

Construction activity remains a core demand engine for the Asia-Pacific roofing market, as transport corridors, logistics parks, industrial clusters, and urban housing all require large, recurring roof procurement volumes. India and Southeast Asia continue to support this pattern through expanding warehouse networks, factory shells, and public infrastructure programs that favor fast-installing metal systems and other scalable roofing formats. Industrial parks in Vietnam, Thailand, and Indonesia also strengthen this demand because pre-engineered structures typically standardize roof selection early in the project cycle, which improves supplier visibility and repeat business. Housing-led demand adds another layer of support because large residential programs concentrate purchases into repeatable product categories instead of fragmented one-off orders. This keeps the Asia-Pacific roofing market tied not only to cyclical building starts, but also to a broader procurement system in which compliance, installation speed, and lifecycle durability matter as much as first-cost economics.

Reroofing and Renovation Demand Expansion

Reroofing and renovation remain central to the Asia-Pacific roofing market because mature economies such as Japan, Australia, and South Korea are replacing large portions of building stock that entered service decades ago. These replacement cycles rarely result in like-for-like material selection because owners and contractors increasingly use reroofing projects to improve thermal performance, reduce structural load, or extend service life. That pattern supports premium metal systems, coated products, and membranes, especially when insulation and waterproofing upgrades are bundled into a single project. In Australia, supply additions by major producers reflect confidence that both new and replacement housing demand will remain active through the current cycle[1]BlueScope Steel Limited, “FY2025 Full-Year Results ASX Release,” BlueScope Steel Limited, bluescope.com. The Asia-Pacific roofing market, therefore, benefits from renovation activity, as replacement work tends to be less volatile than new construction and often carries a higher specification value per project.

Shift Toward Energy-Efficient and Cool-Roof Systems

Energy efficiency standards are becoming a stronger specification force in the Asia-Pacific roofing market as governments and building regulators place greater weight on roof reflectance, thermal comfort, and cooling load reduction. India’s policy direction and Australia’s code pathway both point toward wider adoption of high-SRI surfaces, reflective coatings, and membrane systems in buildings where heat gain has become a cost and comfort issue. Passive cooling initiatives, spearheaded by the United Nations Environment Programme (UNEP) in India's housing programs, are pushing efficient roofing features into the spotlight, transitioning them from niche green-building projects to mainstream housing designs. As these requirements spread, premium membranes and reflective-coated steel are better positioned than darker and lower-performing legacy materials in major urban zones. This is raising the average roof specification in the Asia-Pacific roofing market because compliance is increasingly connected to procurement approval, not just voluntary sustainability branding.

Weather Resilience and Durable-Roof Adoption

The Asia-Pacific roofing market is also being shaped by the region’s frequent exposure to typhoons, cyclones, heavy rain, salt spray, and high humidity. These conditions keep demand strong for roofing systems that offer better wind uplift resistance, corrosion control, and longer-lasting waterproofing performance in challenging operating environments. Coastal and island markets are especially important here because material failure costs can be high when buildings are repeatedly exposed to storm events and long wet seasons. Manufacturers are responding with more differentiated products, including advanced alloy-coated steel that targets faster corrosion than conventional galvanized formats. As a result, durable roof adoption is no longer limited to premium landmark projects, and it is becoming a broader demand driver across commercial, industrial, and even higher-value residential applications in the Asia-Pacific roofing market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -0.7% | Global, with the strongest effect in Southeast Asia and import-dependent markets | Short term (≤ 2 years) |

| Cross-Country Regulatory Fragmentation | -0.5% | APAC-wide, most complex for contractors and distributors operating across Australia, India, China, and ASEAN | Medium term (2-4 years) |

| Roofing Labor and Installer Shortages | -0.4% | Australia, Japan, South Korea, with spillover to urban India and Southeast Asia | Long term (≥ 4 years) |

| Cool-Roof Performance Degradation in Polluted and Humid Zones | -0.3% | North India, Southeast Asia coastal zones, and China industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Raw-material volatility remains a near-term constraint for the Asia-Pacific roofing market, as steel, aluminum, and bitumen costs affect both factory margins and tendering discipline. Import-dependent markets are more exposed because sudden swings in feedstock costs are harder to absorb when local backward integration is limited. The bigger issue is often project delay rather than outright cancellation, since uncertain roof package pricing can cause contractors and developers to postpone starts until bids stabilize. Bitumen-linked products face a similar problem because refinery allocation and oil price cycles can tighten supply even when end demand remains intact. This pressure does not eliminate demand from the Asia-Pacific roofing market, but it can compress quarterly volumes and make the product mix more sensitive to procurement timing.

Cross-Country Regulatory Fragmentation

Cross-country regulation is another restraint for the Asia-Pacific roofing market because product testing, fire classifications, energy codes, and installation standards differ widely across the region. Australia adheres to the National Construction Code, while India implements its own energy-efficiency standards. China utilizes GB codes, and ASEAN markets rely on a patchwork of national regulations, albeit with inconsistent enforcement. This raises certification and compliance costs for manufacturers and distributors seeking a regional footprint, especially when the same product line requires different test pathways in different countries. Mid-tier suppliers are affected more than large platforms because duplicated approvals consume capital and reduce the value of scale across borders. The Asia-Pacific roofing market, therefore, incurs structural compliance costs that slow cross-border standardization even when core product demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Asphalt Shingles Dominant; Membranes Accelerate on Specification Upgrades

Asphalt shingles held 31.8% of the Asia-Pacific roofing market share in 2025, supported by their cost competitiveness and straightforward installation across price-sensitive residential markets. Their position remains strongest where upfront affordability still outweighs thermal performance or long-life requirements in the purchase decision. At the same time, rising energy and reflectance standards create a clear medium-term limit, as conventional dark asphalt products perform worse under established cool-roof measurement frameworks. Clay and concrete tiles continue to hold meaningful demand in countries where architectural tradition, steep-slope design, and long service life remain important. Metal roofing also remains a major volume category in the Asia-Pacific roofing market, serving both industrial buildings and higher-specification renovation projects. Producer commentary supports that role, with JSW Steel reporting 14% year-on-year growth in galvalume and galvanized sales in FY 2024-25.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are forecast to grow at a 6.8% CAGR through 2031, making them the fastest-rising material group in the region. The Asia-Pacific roofing market size for this segment is being lifted by commercial and industrial buildings where low-slope systems, faster installation, and higher thermal performance are increasingly specified. TPO is gaining particular traction in data-center and logistics projects because owners value seam integrity, installation speed, and the ability to manage large roof areas with consistent detailing. EPDM still fits mature renovation settings where weather exposure and waterproofing resilience matter more than aesthetic finish. Bituminous membranes continue to serve infrastructure and waterproofing-heavy applications, while wood remains limited by fire and sustainability concerns in several developed markets. The others category captures early adoption of solar-integrated roofing, green roof assemblies, and niche high-performance systems that are still small in volume but increasingly visible in urban projects.

By Construction Type: Reroofing and Replacement Anchors Revenue; New Construction Accelerates Fastest

Reroofing and replacement accounted for 58.4% of regional demand in 2025, making them the main revenue driver for the Asia-Pacific roofing market. This reflects the installed base in Japan, Australia, and South Korea, where large parts of the built environment are entering renewal stages simultaneously. Replacement projects often become upgrade projects because owners use them to improve insulation, weather resistance, or visual appeal rather than simply restore the old system. That dynamic supports higher average revenue per project, especially when contractors shift customers toward premium coated steel, membranes, or improved waterproofing packages. Compliance rules reinforce this trend because replacement work can still trigger new thermal and performance requirements in certain jurisdictions.

New construction is projected to grow at a 5.9% CAGR through 2031, making it the fastest-growing construction segment. The Asia-Pacific roofing market for new construction benefits from industrial buildout, logistics expansion, and ongoing urban housing development in India and Southeast Asia. Pre-engineered buildings are especially important because they standardize roof packages early, increasing procurement efficiency and strengthening repeat relationships with established metal roofing suppliers. This favors manufacturers that can deliver certified products, installation support, and wide distribution reach within tight project schedules. New construction also tends to accelerate adoption of higher-performing systems because developers can integrate energy, waterproofing, and maintenance goals from the start instead of adapting around older roof structures.

By Application: Residential Dominant; Industrial Outpaces All Other Segments

Residential held a 49.6% share of the Asia-Pacific roofing market size in 2025, reflecting the sheer scale of regional housing demand and the ongoing expansion of urban and peri-urban housing stock. This segment remains broad-based, encompassing both low-cost roofing demand in emerging economies and premium replacement demand in mature housing markets. Growth is more measured in older housing markets where new starts are softer, but replacement and specification upgrades still keep activity steady. In India, branded roofing is gaining more traction beyond major cities as buyers place greater value on warranties, certified quality, and coated products that perform better in difficult weather. JSW Steel said its Colouron+ brand held 49% of the domestic color-coated market share and carried India’s first ISI certification for color-coated sheets, underscoring the growing relevance of formal branding in retail roofing channels.

Industrial is forecast to grow at a 6.2% CAGR through 2031, which places it ahead of all other application segments. The Asia-Pacific roofing market for industrial projects is growing as warehouses, pharmaceutical facilities, semiconductor fabs, and data-center shells require wide-span, low-slope, and thermally efficient roof systems. These buildings also carry heavier rooftop service loads and stricter waterproofing needs, which supports better quality materials and more complex installation standards. Commercial demand is supported by retail, hospitality, and mixed-use construction in Southeast Asia, while institutional projects benefit from public investment in healthcare and education buildings. The “others” segment includes transport terminals, stadiums, and specialized public assets where long-span membranes and engineered roof systems are selected for structural performance rather than mass-market cost efficiency.

Geography Analysis

China held 43.7% of the Asia-Pacific roofing market share in 2025, which kept it far ahead of every other national market in the region. Its growth profile is more mixed than its scale suggests because residential new-build activity remains below earlier peaks, even as industrial and commercial construction continue to create roof demand. Demand is supported by logistics facilities, advanced manufacturing sites, and ongoing urban renewal of older apartment stock in major cities. Sika’s 2025 results pointed to a double-digit decline in its China construction business, while India and Southeast Asia delivered more dynamic momentum, suggesting that regional roofing demand is becoming less dependent on a single country[2]Sika AG, “FY2025 Full-Year Results - Executing Plan to Accelerate Growth,” Sika AG, sika.com. China, therefore, remains critical to the Asia-Pacific roofing market, but the region’s next phase of growth is being distributed more widely than before.

India is the fastest-growing national market, with a projected 7.1% CAGR through 2031, providing the Asia-Pacific roofing market with a strong expansion engine outside China. The country combines housing demand, industrial construction, logistics expansion, and rising policy attention to roof performance, which supports both volume growth and product upgrading. Passive cooling programs tied to housing and urban design are helping bring energy-efficient roof specification into wider use, especially in hot-climate settings. Japan remains important because its roofing demand is sustained less by new build and more by renovation quality, waterproofing performance, and demand for durable systems in a sophisticated contractor base.

Australia and South Korea are mature markets, but they still provide steady opportunity through replacement work, code-led upgrades, and premium product adoption. BlueScope commissioned Metal Coating Line 7 at Erskine Park in late 2025, adding 240,000 tonnes per year of metal-coated steel capacity to support Australian housing and coated roofing demand. Australia’s 2026 code pathway is also lifting cool-roof requirements across climate zones, which strengthens the case for higher-reflectance roofing products. The rest of APAC, including Vietnam, Thailand, Indonesia, Malaysia, and the Philippines, remains one of the most active areas of the Asia-Pacific roofing market because industrialization, export manufacturing, logistics, and rising weather-resilience needs are all moving in the same direction.

Competitive Landscape

The Asia-Pacific roofing market is fragmented, with multinational materials groups and strong domestic manufacturers competing across different price bands, building types, and country-specific code environments. BlueScope-affiliated businesses remain prominent across Australasia, Southeast Asia, and India through premium steel roofing brands such as COLORBOND, ZINCALUME, and LYSAGHT, while domestic players in India and China retain share through cost discipline and supply-chain proximity. JSW Steel Coated Products Limited also holds a strong position in India, with 49% share in color-coated products and 72% share in galvalume, according to its FY 2024-25 annual report[3]JSW Steel Limited, “Management Discussion and Analysis - JSW Steel Annual Report FY 2024-25,” JSW Steel, jswsteel.in. That mix of global brands and local champions keeps pricing and product positioning highly segmented across the Asia-Pacific roofing market.

Competition is shifting beyond basic product performance and increasingly toward broader roofing systems that include warranty support, specification guidance, certified performance, and compatibility with modern design tools. Sika strengthened its position in premium roofing and waterproofing through acquisitions, including Singapore-based Elmich in February 2025 and Gulf Seal in November 2025, which support green roof, waterproofing, and membrane-related capability across growth markets. BlueScope’s 2025 and 2026 investments in coated steel capacity and its focus on premium volumes in Southeast Asia show a similar strategy built around value-added roofing demand rather than commodity tonnage. Tata BlueScope Steel’s rebranding to Tata Steel Colors in February 2025 also clarified ownership and kept DURASHINE and LYSAGHT in the market under a more unified brand structure. These moves show that the Asia-Pacific roofing market is rewarding companies that can combine product reach, brand trust, and application support.

Kingspan is advancing insulated roofing panels in temperature-controlled and pharmaceutical settings, while Everest Industries is expanding its position in pre-engineered building roofing systems for industrial demand in India. The competitive field is also opening in rural roofing, self-install replacement products, and solar-ready roof systems, where product design and distribution can matter more than traditional large-project bidding. Certification is becoming a stronger entry barrier in specifier-led markets such as Australia and Singapore, which makes compliance capability almost as important as manufacturing capacity. The Asia-Pacific roofing market therefore remains open to new entrants in select niches, but large-scale gains are more likely for players that can pair local execution with consistent regional specification credibility.

Asia-Pacific Roofing Industry Leaders

JSW Steel Ltd

Everest Industries Limited

The Siam Cement Public Company Limited

CSR Monier Roofing

Tata Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BlueScope Steel reported underlying Earnings Before Interest and Taxes (EBIT) of AUD 97 million (USD 68.6 million) for Coated Products Asia in H1 FY2026, a 39% improvement over H2 FY2025, driven by higher premium roofing volumes across Southeast Asia, particularly Malaysia and Vietnam, reflecting durable infrastructure demand in the region.

- April 2026: BlueScope Steel continued expanding its Asia-focused coated steel and premium metal roofing business in 2026 through investments linked to COLORBOND and LYSAGHT operations across India and Southeast Asia. The strategy is aimed at capturing rising demand for roofing in industrial, logistics, and warehouse construction projects across the Asia-Pacific roofing market.

- January 2026: Mount Roofing & Structures expanded its Tumkur manufacturing facility in India in January 2026 with an investment of approximately USD 30 million, adding new PUF panel and pre-engineered building (PEB) production lines. The expansion increased sandwich panel production capacity to 700,000 square meters per month and added solar-compatible roofing profiles, strengthening industrial and infrastructure roofing supply in the Asia-Pacific region.

Asia-Pacific Roofing Market Report Scope

The Asia-Pacific Roofing Market is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and more), Construction Type (New Construction and Reroofing and Replacement), Application (Residential, Commercial, and more), and Geography (China, Japan, India, Australia, South Korea, and Rest of APAC). The Market Forecasts are Provided in Terms of Value (USD).

| Asphalt Shingles |

| Clay & Concrete Tiles |

| Metal Roofing |

| Bituminous / Modified Bitumen Membranes |

| Single-Ply Membranes (TPO, EPDM, and PVC) |

| Wood |

| Others |

| New Construction |

| Reroofing and Replacement |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Others |

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Material Type | Asphalt Shingles |

| Clay & Concrete Tiles | |

| Metal Roofing | |

| Bituminous / Modified Bitumen Membranes | |

| Single-Ply Membranes (TPO, EPDM, and PVC) | |

| Wood | |

| Others | |

| By Construction Type | New Construction |

| Reroofing and Replacement | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| Institutional | |

| Others | |

| By Geography | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the expected value of the Asia-Pacific roofing space by 2031?

The Asia-Pacific roofing market is forecast to reach USD 77.69 billion by 2031, up from USD 60.18 billion in 2026, with 5.24% CAGR over 2026-2031.

Which material category leads demand across the region?

Asphalt shingles held the largest share in 2025 at 31.8%, mainly because they remain cost-competitive and easy to install in residential construction across several emerging markets.

Which roofing material is growing the fastest in Asia-Pacific?

Single-ply membranes are projected to grow the fastest at 6.8% CAGR through 2031, supported by higher use in commercial, industrial, logistics, and data-center projects.

Why is reroofing so important in this region?

Reroofing and replacement accounted for 58.4% of demand in 2025 because mature markets such as Japan, Australia, and South Korea have large volumes of ageing building stock that now need renewal and performance upgrades.

Page last updated on: