South America Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

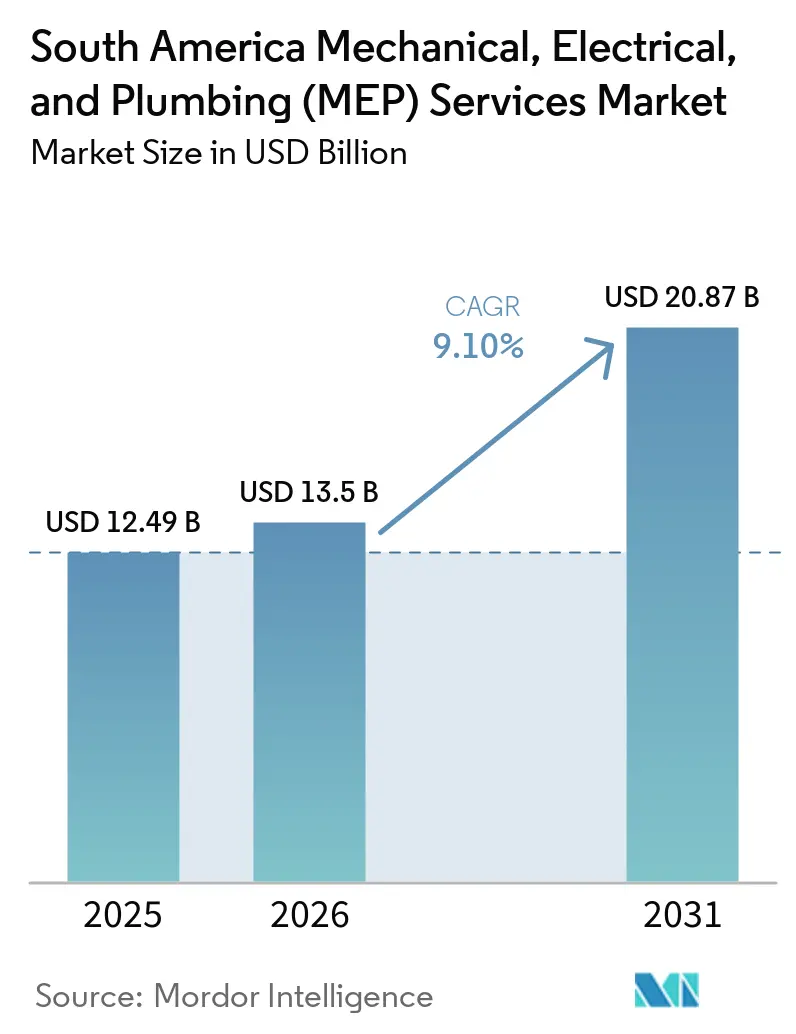

| Base Year Market Size (2025) | USD 12.49 Billion |

| Market Size (2026) | USD 13.5 Billion |

| Market Size (2031) | USD 20.87 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The South America Mechanical, Electrical, And Plumbing Services Market size is expected to grow from USD 12.49 billion in 2025 to USD 13.5 billion in 2026 and is forecast to reach USD 20.87 billion by 2031 at 9.10% CAGR over 2026-2031. The South America mechanical, electrical, and plumbing (MEP) services market is being supported by a broad infrastructure build cycle that spans hospitals, metro systems, sanitation assets, logistics facilities, and digital campuses across the region. Brazil remains the largest demand center because the PAC-3 program has committed more than USD 333 billion to public and private infrastructure, which is sustaining a deep pipeline of electrical, mechanical, and plumbing work across transport, health, and water projects.

Chile is adding a specialized layer of demand as hyperscaler investment rises and the national data center plan targets a major expansion of sector capacity, which is lifting requirements for cooling, power distribution, and backup systems. The South America mechanical, electrical, and plumbing (MEP) services market is also benefiting from commercial retrofit activity and tighter efficiency standards, which are extending contracts beyond installation into monitoring, recommissioning, and lifecycle maintenance. Interest rates, imported equipment costs, and uneven labor formalization still create execution pressure, but the water infrastructure backlog, data center density growth, and broader outsourcing of hard services continue to support the growth path of the South America mechanical, electrical, and plumbing (MEP) services market through 2031.

Key Report Takeaways

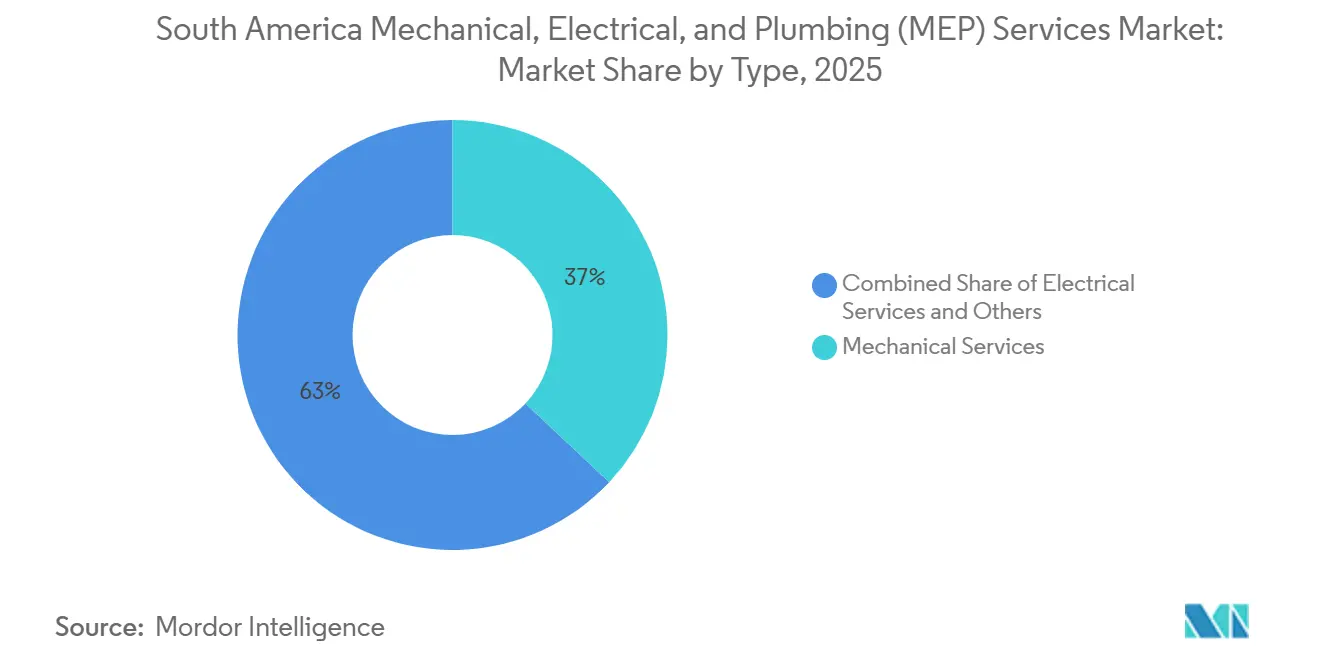

- By type, mechanical services held 37% share in 2025, while Integrated MEP Services is projected to grow at 11.7% CAGR through 2031.

- By service type, maintenance, repair, and retrofit accounted for 34% share in 2025, while managed/performance-based services is projected to grow at 10.6% CAGR through 2031.

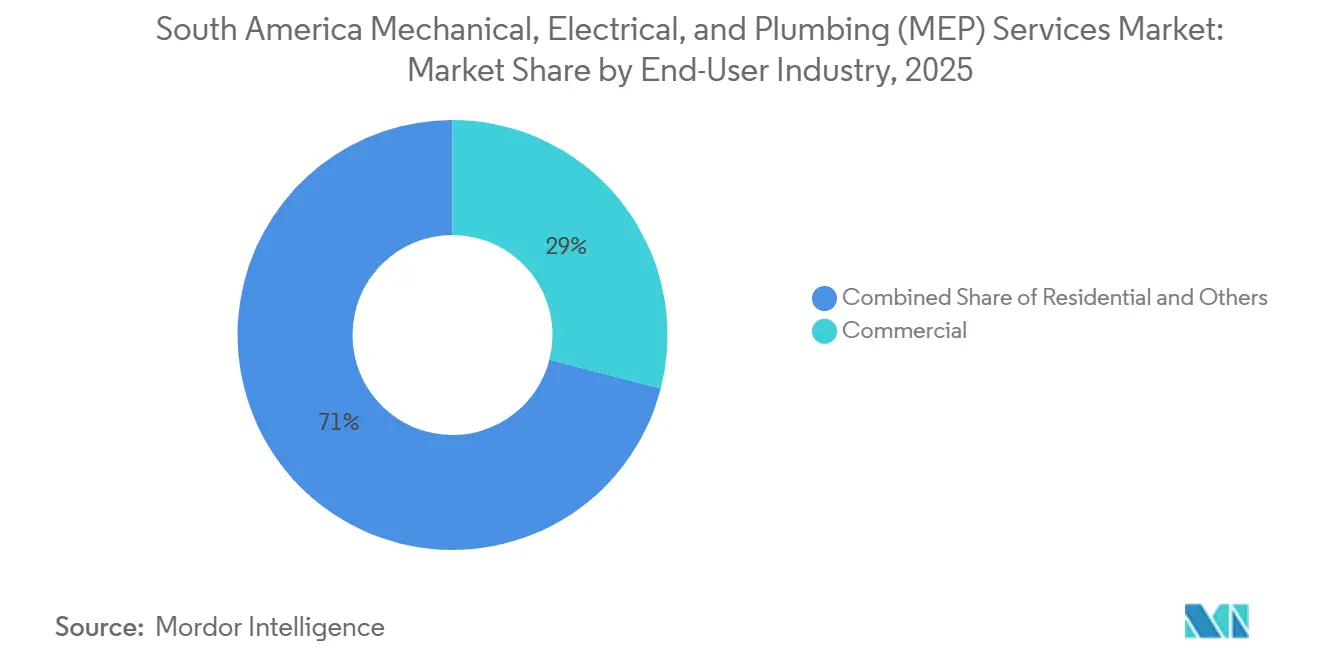

- By end-user industry, commercial real estate held 29% share in 2025, while infrastructure is projected to grow at 12.2% CAGR through 2031 in the South America MEP services market size.

- By geography, Brazil held 31.2% share in 2025, while Argentina is projected to grow at 11.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial and Infrastructure Modernization | +2.3% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| Data Center and Logistics Facility Expansion | +2.0% | Brazil, Chile | Short term (≤ 2 years) |

| Outsourcing of Hard Services and Lifecycle Maintenance | +1.5% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Chile and Brazil Power-Linked Campus Development | +1.3% | Chile, Brazil | Short term (≤ 2 years) |

| ESG-Driven Energy and Refrigerant Audit Scopes | +1.0% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Water Resilience and Closed-Loop Cooling Retrofits | +0.8% | Chile, Peru, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial and Infrastructure Modernization

The South America mechanical, electrical, and plumbing (MEP) services market is drawing steady support from the region’s wider modernization cycle in transport, health, water, and urban assets. Brazil’s construction sector contributes close to 6% of GDP, and PAC-3 has committed USD 333 billion across transport, energy, water, and urban mobility, which is converting into multi-year MEP subcontract opportunities in hospitals, airports, metro systems, and sanitation plants[1]OECD, “Scaling-up Infrastructure Investment to Strengthen Sustainable Development in Brazil,” OECD, oecd.org.. The same pattern is visible outside Brazil, where AECOM’s joint venture was selected by Peru’s Ministry of Health in 2024 to manage two major regional hospitals in Piura and Trujillo with responsibility across the MEP lifecycle under a BIM-led model. Brazil’s position among the top five countries globally for LEED-certified buildings is also deepening the role of auditable MEP performance, because certification now depends on system outcomes rather than simple installation completion. This is extending the life of contracts in the South America mechanical, electrical, and plumbing (MEP) services market and raising the value of firms that can stay involved after handover through monitoring, recommissioning, and energy optimization. It also means that the South America mechanical, electrical, and plumbing (MEP) services market is becoming less tied to one-time construction cycles and more linked to ongoing building performance obligations.

Data Center and Logistics Facility Expansion

The South America mechanical, electrical, and plumbing (MEP) services market is gaining from the expansion of data center campuses and modern logistics facilities in Brazil and Chile. Chile’s National Data Center Plan for 2024 to 2030 aims to triple the size of the sector, and projected hyperscaler investment from 2025 onward exceeds USD 8 billion, creating a sustained pipeline for cooling, power quality, backup generation, and fire suppression packages. These facilities are no longer being designed around traditional 10 kW per rack conditions, as AI-oriented halls are moving toward 100 kW per rack densities that require liquid-cooling loops, higher-voltage busways, and N+1 redundant chillers. That change is narrowing the pool of contractors capable of delivering dense mechanical and electrical packages and completing commissioning without performance failures. The South America mechanical, electrical, and plumbing (MEP) services market is therefore seeing a wider gap between standard installation vendors and specialized contractors that can work on high-density digital campuses. The same shift is spilling into adjacent logistics facilities, where operators increasingly want resilient power systems, advanced ventilation, and automation-ready service frameworks at commissioning.

Outsourcing of Hard Services and Lifecycle Maintenance

The South America mechanical, electrical, and plumbing (MEP) services market is moving further toward outsourced hard services and bundled lifecycle maintenance in commercial real estate, healthcare, and institutional facilities. EULEN Group Perú already operates comprehensive property maintenance services that use BMS and CMMS tools to support compliance with ISO 50001 and ISO 14001 across a customer base of more than 7,000 organizations in 11 countries. That model is becoming more relevant as building owners and institutional investors want documented service outcomes, lower downtime, and verifiable energy and water performance from one accountable provider. It also gives global facility management firms and energy services platforms a stronger entry point into the South America mechanical, electrical, and plumbing (MEP) services market, because recurring contracts carry lower capital intensity and better revenue visibility than project-only work. Regional MEP integrators are responding by broadening their offer from corrective maintenance into preventive and predictive service models tied to service-level agreements. This is changing procurement criteria in the South America mechanical, electrical, and plumbing (MEP) services market from day-rate competitiveness toward response time, auditability, system uptime, and measured asset performance.

Chile and Brazil Power-Linked Campus Development

Chile and Brazil are emerging as the region’s main locations for power-linked campus development, where data center growth is now being shaped by grid readiness, transmission capacity, and resilient utility design as much as by land availability. In Chile, the National Data Center Plan for 2024-2030 and hyperscaler investment commitments exceeding USD 8 billion from 2025 onward are creating direct demand for high-capacity cooling, power distribution, backup generation, and related MEP packages. Chile’s power grid reached 60% non-conventional renewable energy penetration by late 2025, but bottlenecks around Quilicura and Lampa are increasing the need for substation design, grid-side power electronics, and redundancy-focused campus engineering. Brazil is showing a similar pattern, where upstream grid investments are supporting downstream digital and infrastructure campuses, as reflected in VINCI’s March 2025 contract to build 738 km of high-voltage transmission lines for Engie Brasil. This is widening MEP scope from internal building systems into power interface design, backup architecture, and integrated commissioning across mechanical and electrical layers. Over the short term, this driver favors firms that can manage both dense cooling requirements and high-reliability electrical delivery within one coordinated project model.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX Volatility and Inflation Pressure | -1.7% | Brazil, Argentina | Short term (≤ 2 years) |

| Labor Informality and Uneven Execution Quality | -1.0% | Regional, highest in Argentina, Peru | Long term (≥ 4 years) |

| Fragmented Building and Fire-Code Enforcement | -0.9% | Regional, concentrated in Peru and Colombia | Medium term (2-4 years) |

| Grid Interconnection Delays Near Digital Clusters | -0.7% | Chile, Brazil (São Paulo metro) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FX Volatility and Inflation Pressure

FX volatility and financing costs remain a major operational brake on the South America mechanical, electrical, and plumbing (MEP) services market. Brazil’s Selic rate reached 14.8% in May 2025 and the OECD expects only gradual easing, which keeps borrowing costs high for clients and compresses contractor returns on fixed-price projects that rely on imported equipment. PVC pipe prices were already up 16.3% in the 12 months to February 2026, and construction cost inflation could push the INCC to 9.7% in 2026, which puts further pressure on contracts signed before those inputs moved higher. The effect is especially visible in renewables, digital infrastructure, and other MEP-heavy projects that depend on dollar-linked components and hedging costs. In the South America mechanical, electrical, and plumbing (MEP) services market, this can lead to delayed starts, smaller scopes, or tighter bid discipline when procurement teams cannot pass cost changes through quickly. Argentina intensifies the pressure because depreciation sharply increases the local cost of high-CAPEX MEP systems relative to legacy solutions, which can shift buyers toward deferral rather than upgrade.

Labor Informality and Uneven Execution Quality

Labor informality continues to weaken execution consistency in the South America mechanical, electrical, and plumbing (MEP) services market. The ILO reported in May 2026 that 66.9% of salaried construction workers in Argentina were engaged informally, which shows how weak labor formalization can undermine accountability and skills verification on technically demanding sites[2] International Labour Organization, “Construcción En Argentina, Radiografía De La Informalidad Y Aportes Para La Formalización,” ILO, ilo.org.. In Peru, CAPECO warned in 2025 that pseudo-union extortion was disrupting project sequencing and causing delays at construction sites, often including time-sensitive electrical and mechanical work. Informal subcontracting chains make it harder for facility owners to trace installation quality, enforce warranty obligations, and confirm that commissioning and safety testing were completed to the required standard. The absence of a regionwide certification baseline for specialized MEP trades means quality assurance often depends on the lead integrator’s own supervision capacity rather than a regulated skills framework. For the South America mechanical, electrical, and plumbing (MEP) services market, that favors better-capitalized firms with strong documentation and site controls, especially on data center and institutional projects that require high reliability at handover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Systems Dominate as Integrated Bundles Gain Ground

Mechanical Services held 37% of the South America mechanical, electrical, and plumbing (MEP) services market share in 2025, which made it the largest service cluster by type. That position reflects the large installed base of HVAC, refrigeration, and industrial process cooling equipment across commercial buildings, healthcare facilities, and digital infrastructure. The South America mechanical, electrical, and plumbing (MEP) services market continues to lean toward mechanical scopes because tropical operating conditions in Brazil and the cooling demands of high-availability facilities keep thermal management at the center of project design and maintenance. Plumbing services also retain solid relevance because Brazil still faces a major sanitation gap, with 47% of the population not connected to the sewage system, which sustains demand for water and wastewater-related retrofits and network work. Integrated MEP Services is the fastest-growing type and is projected to expand at 11.7% CAGR through 2031 as clients reduce the cost and risk of coordinating separate mechanical, electrical, and plumbing contractors.

Within the South America mechanical, electrical, and plumbing (MEP) services industry, the rise of integrated contracts is rewarding firms that can mobilize multi-discipline site teams and keep design, installation, testing, and commissioning aligned under one scope. The shift is becoming more visible in data center work, where high-density halls require simultaneous redesign of cooling loops, electrical distribution, and water management systems rather than isolated package delivery. Building owners are also using integrated contracts to reduce interface disputes, shorten handover cycles, and secure performance guarantees from one provider instead of three. That is widening the gap between firms with lifecycle capability and those that only compete on discrete installation packages in the South America mechanical, electrical, and plumbing (MEP) services market. The result is a more favorable growth path for contractors that can combine mechanical depth, electrical reliability, plumbing integration, and formal commissioning discipline in one managed offer.

By Service Type: Retrofit-Led Cycle Driving Volume as Performance Models Reshape Margins

Maintenance, Repair, and Retrofit accounted for 34% of the South America mechanical, electrical, and plumbing (MEP) services market size in 2025, reflecting the age and breadth of the region’s installed MEP base. A large share of commercial and institutional equipment was specified before current energy efficiency and refrigerant management requirements became more demanding, which is now pushing owners toward system upgrades instead of simple reactive maintenance. The retrofit cycle is especially visible in large urban office and retail portfolios where building owners are upgrading HVAC systems, lighting, controls, and automation layers to stay aligned with newer certification and reporting expectations. Design and engineering, along with installation, testing, and commissioning, continue to absorb the region’s new-build work in data centers, hospitals, sanitation assets, and power-linked infrastructure. Managed/Performance-based Services is the fastest-growing service type and the South America mechanical, electrical, and plumbing (MEP) services market size for this segment is projected to expand at 10.6% CAGR through 2031. That model shifts operational risk toward the provider, but it also creates longer contract duration and better revenue visibility for firms that can back their guarantees with technical capability and balance sheet strength. This is attracting energy services platforms and large facility management groups into the South America mechanical, electrical, and plumbing (MEP) services market, where recurring service revenue is becoming more valuable than one-time installation margins. Smaller regional players that cannot support performance guarantees may still win transactional work, but they face a growing risk of being displaced in institutional and premium commercial accounts.

Within the South America mechanical, electrical, and plumbing (MEP) services industry, performance contracting is changing the economic logic of service delivery. Chile’s energy efficiency framework has helped formalize ESCO-style structures that treat MEP maintenance as a guaranteed-savings and measured-performance service rather than a simple fee-for-service activity

By End-User Industry: Commercial Real Estate Leads but Infrastructure Commands the Growth Premium

Commercial buildings held 29% share of the end-user base in 2025, which kept them at the center of demand in the South America mechanical, electrical, and plumbing (MEP) services market. Premium office assets, retail complexes, colocation facilities, and enterprise data center sites continue to require higher-than-average cooling, power quality, building automation, and recurring recommissioning work. LEED Platinum standards, dense server rooms, and tenant comfort expectations all raise specification intensity in the commercial segment and support recurring service needs after project completion. Residential demand remains meaningful because of Brazil’s scale and ongoing housing programs, but average MEP spend per unit is still lower than in commercial or infrastructure applications. Infrastructure is the fastest-growing end-user group and the South America mechanical, electrical, and plumbing (MEP) services market size for infrastructure is projected to expand at 12.2% CAGR through 2031.

That growth premium reflects the overlap between digital infrastructure and physical infrastructure spending across the region. VINCI’s Cobra Brasil has a long track record of transmission projects in the country, and its March 2025 design-build contract with Engie Brasil for 7 high-voltage transmission lines demonstrates how large electrical scopes are being embedded in infrastructure programs[3]VINCI, “VINCI Awarded the Contract to Build 738 Km of High-Voltage Electricity Transmission Lines in Brazil,” VINCI, vinci.com.. Water, transport, power, and digital campuses are also becoming more complex at the systems level, which pushes buyers toward contractors that can prove multi-discipline coordination and commissioning quality. In the South America mechanical, electrical, and plumbing (MEP) services market, this is steadily shifting procurement away from lowest-bid single-trade installers and toward firms that can document performance across the full asset lifecycle. The South America mechanical, electrical, and plumbing (MEP) services industry is therefore seeing infrastructure projects act as a training ground for higher-value integrated service delivery.

Geography Analysis

Brazil held 31.2% of the South America mechanical, electrical, and plumbing (MEP) services market share in 2025, which kept it as the largest country market in the region. Its leadership is supported by the scale of the urban construction pipeline and by infrastructure programs that continue to generate electrical, mechanical, and plumbing demand across transport, healthcare, sanitation, and housing assets. The country also retains a large sanitation deficit, with 10% of the population lacking safe drinking water and 47% still not connected to the sewage system, which sustains long-term demand for plumbing-intensive upgrades and water treatment projects. ACCIONA’s 2025 sanitation and water concession wins in Brazil show that large integrated infrastructure contracts are continuing to create a deep pipeline for MEP-related execution. Brazil, therefore, remains the volume anchor of the South America mechanical, electrical, and plumbing (MEP) services market across both new construction and modernization work.

Argentina is the fastest-growing geography, with the South America mechanical, electrical, and plumbing (MEP) services market size in the country projected to expand at 11.0% CAGR through 2031. The country’s near-term environment remains pressured by FX volatility and labor informality, but large energy infrastructure programs are still creating meaningful demand for mechanical and electrical subcontracting. The Vaca Muerta Oil Sur Pipeline is one of the clearest examples, as the 437 km project represents the most significant energy infrastructure build in Argentina in 50 years and carries substantial mechanical installation scope. Argentina’s growth profile suggests that large, project-led opportunities are outweighing near-term execution constraints in selected end-use areas. This makes the country an important expansion market for firms that can manage technical scope while controlling procurement and commissioning risks.

Chile, Colombia, and Peru remain important contributors to the wider South America mechanical, electrical, and plumbing (MEP) services market. Chile continues to benefit from hyperscaler investment, grid-linked data center development, and building efficiency regulation, which support demand for cooling, power, and audit-linked retrofit work. Colombia is seeing a near-term lift in project activity, supported by an 11.2% year-on-year increase in construction permits in the first 11 months of 2025, which should flow into later-stage fit-out and MEP installation demand as projects advance. Peru is also strengthening its institutional pipeline through hospital and airport projects, including AECOM’s healthcare program management assignment and ACCIONA’s airport control tower contract in the Andes. Together, these markets broaden the regional opportunity base even as Brazil remains the largest and Argentina records the fastest projected growth.

Competitive Landscape

The South America mechanical, electrical, and plumbing (MEP) services market remains moderately fragmented, with global engineering firms competing alongside regional contractors and local specialists. Companies such as AECOM, WSP Global, and Jacobs are prominent in design and program management, while firms such as ENGIE and VINCI Energies maintain strong positions in electrical and multi-technical services. Regional contractors also continue to play an important role due to their local relationships and execution capabilities.

Competition in the market is increasingly shifting toward firms that offer integrated lifecycle capabilities, including commissioning, digital asset management, and long-term maintenance services rather than only installation work. Strategic infrastructure, healthcare, telecom, and transmission projects across countries such as Brazil and Peru are strengthening the position of larger integrated players with broader engineering and EPC expertise.

At the same time, white-space opportunities remain significant in areas such as preventive maintenance, building management systems, and sustainability-focused services. Adoption of digital monitoring platforms, CMMS solutions, and green building certifications such as LEED and EDGE is creating additional demand for advanced MEP service capabilities. As a result, the market continues to support both consolidation opportunities and capability-led differentiation.

South America Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

Grupo ECA

ES4Q

Propamat

CELMEC

Grupo Nortem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ACCIONA was awarded a USD 48 million (EUR 41 million) contract to construct the control tower for Chinchero-Cuzco International Airport in the Peruvian Andes, including complex MEP systems for aviation infrastructure at elevations exceeding 3,700 meters, where equipment performance margins are constrained.

- January 2026: ACCIONA was awarded a R$2.099 billion (approximately USD 390 million) contract by the City of São Paulo for a road-link project in southern São Paulo, covering three viaducts, two tunnels, drainage works, cycle infrastructure, and a landscaped park, with large mechanical and civil MEP scope.

- March 2025: VINCI's subsidiary Cobra Brasil was awarded an approximately EUR 150 million design-build contract by Engie Brasil for 7 high-voltage electricity transmission lines (525 kV and 345 kV) totaling 738 km across Minas Gerais, Paraná, and Santa Catarina, creating over 2,200 construction jobs.

- February 2025: Techint-SACDE joint venture commenced construction of the 437 km Vaca Muerta Oil Sur Pipeline in Argentina, Argentina's most significant energy infrastructure project in 50 years, designed to export 180,000 barrels per day initially and scaling to 690,000 bpd with additional mechanical installations.

South America Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The South America MEP Services Market is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation/Testing/Commissioning, Maintenance/Repair/Retrofit, Managed/Performance-based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are in Terms of Value (USD).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance, Repair, and Retrofit |

| Managed / Performance-based Services |

| Residential |

| Commercial |

| Infrastructure |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance, Repair, and Retrofit | |

| Managed / Performance-based Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of South America mechanical, electrical, and plumbing (MEP) services market?

The South America mechanical, electrical, and plumbing (MEP) services market reached USD 12.5 billion in 2025 and is projected to rise to USD 20.9 billion by 2031 at a 9.1% CAGR.

Which country leads MEP demand in South America?

Brazil led regional demand with a 31.2% share in 2025, supported by PAC-3 infrastructure spending, sanitation backlog, and a broad urban construction pipeline.

Which service type is growing fastest across South America?

Managed/Performance-based Services is the fastest-growing service type, with a projected 10.6% CAGR through 2031 as owners move toward lifecycle and outcome-based contracts.

Why are data centers important for regional MEP demand?

Data centers require dense cooling, resilient electrical systems, backup power, and advanced fire suppression, which raises both project value and technical barriers for contractors.

Page last updated on: