South America Commercial Real Estate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

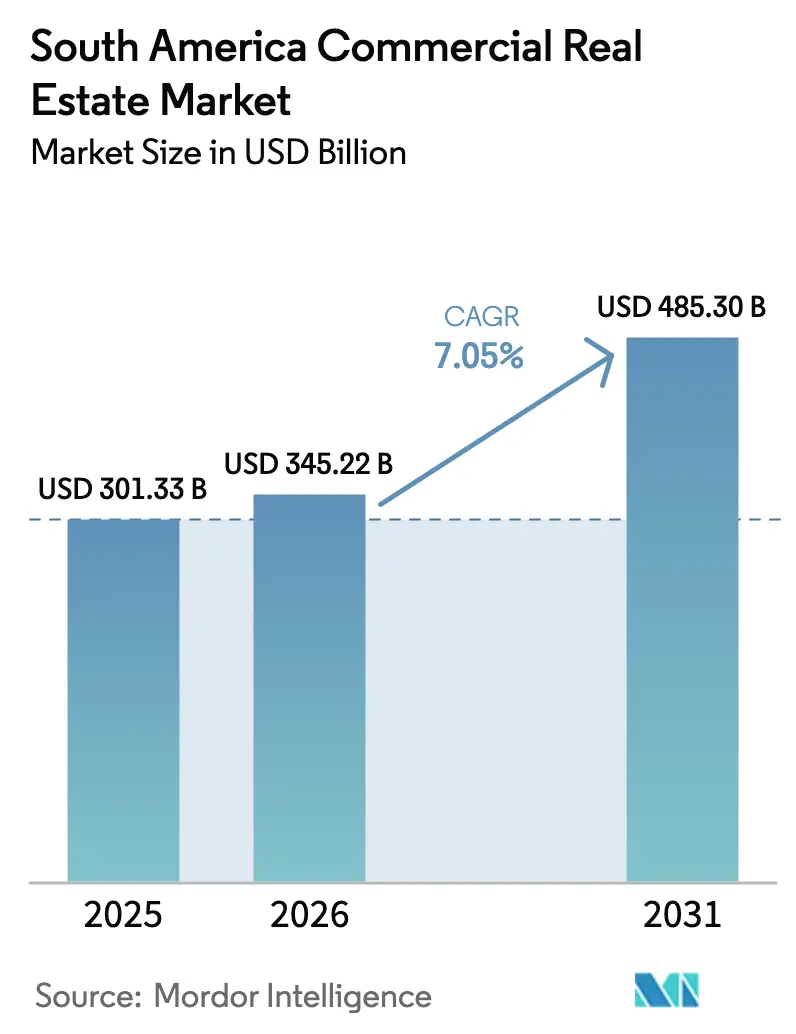

| Base Year Market Size (2025) | USD 301.33 Billion |

| Market Size (2026) | USD 345.22 Billion |

| Market Size (2031) | USD 485.30 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

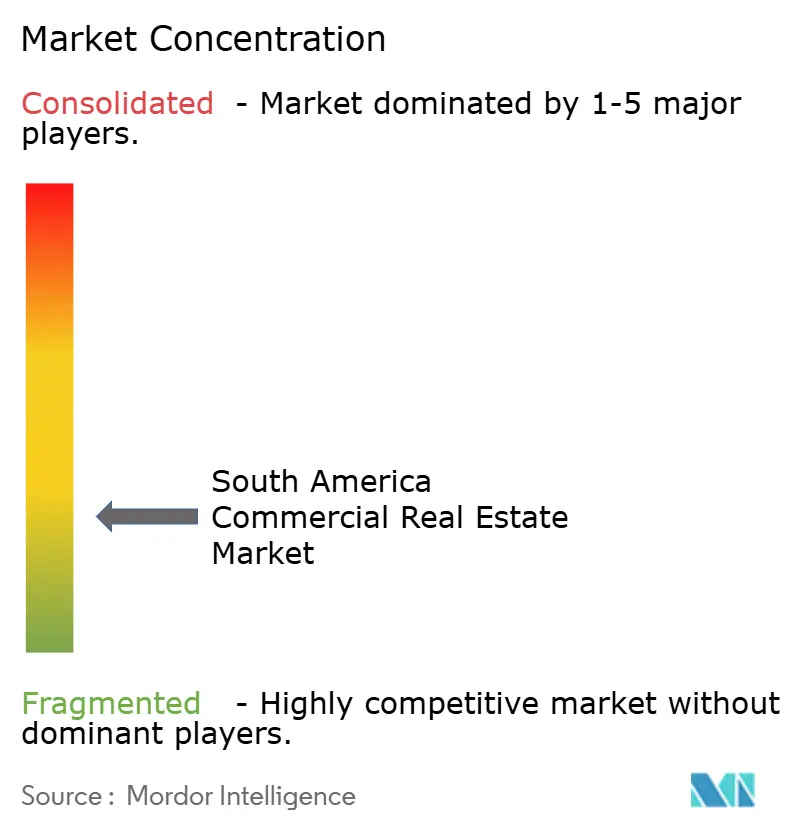

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Commercial Real Estate Market Analysis by Mordor Intelligence

The South America commercial real estate market size was valued at USD 301.33 billion in 2025 and estimated to grow from USD 345.22 billion in 2026 to reach USD 485.3 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031)[1]Ana Luiza Tieghi, “Building demolitions pave way for new projects in São Paulo,” Valor International, valorinternational.globo.com. Supply-chain re-routing from Asia, sovereign data-residency rules, and national hydrogen strategies are reshaping investment flows toward ports, inland logistics corridors, and hyperscale data-center campuses. Institutional buyers continue to gravitate to income-producing logistics assets, while a resurgence in office leasing, supported by metro extensions and zoning reforms, has narrowed prime-CBD vacancy to the mid-teens. Rising catastrophe-insurance costs and double-digit local-currency interest rates remain the chief headwinds, but regulatory streamlining in Chile and Peru is starting to compress permitting calendars and unlock shovel-ready inventory.

Key Report Takeaways

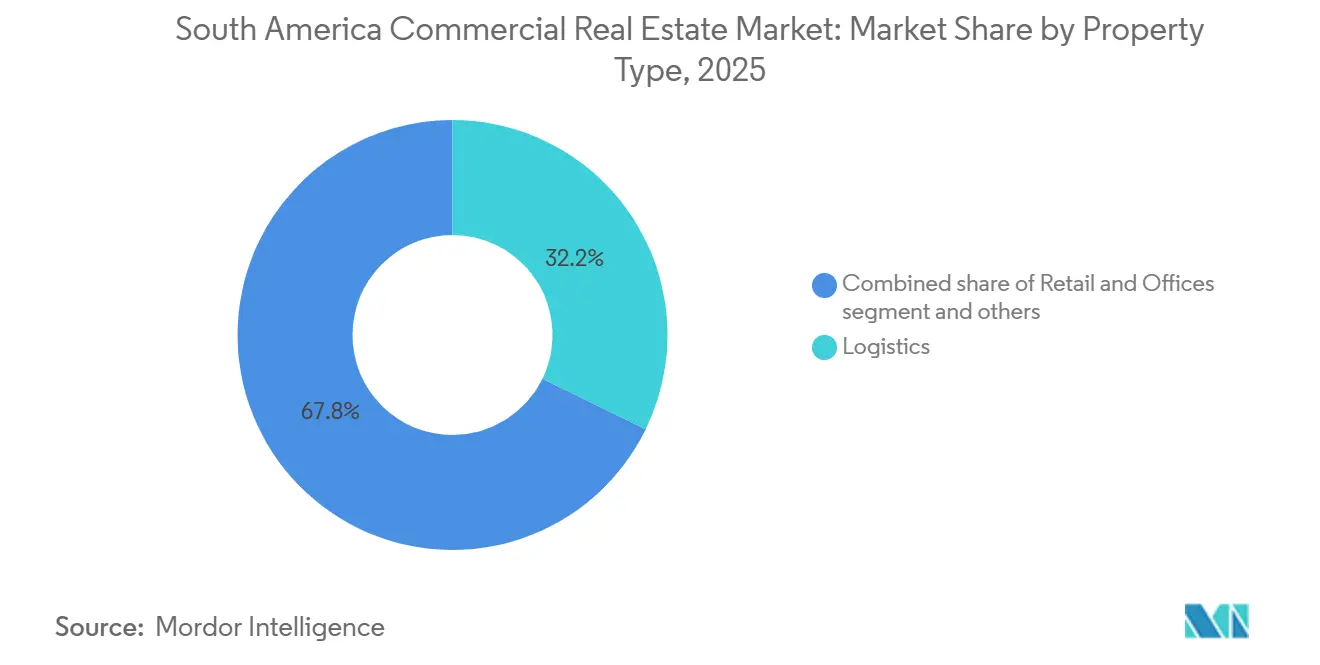

- By property type, logistics and industrial parks led with 32.22% of the South America commercial real estate market share in 2025. By property type, offices are forecast to expand at a 9.50% CAGR through 2031, the fastest among all segments.

- By business model, rental and leasing captured a 61% share of the South America commercial real estate market size in 2025 and is projected to post an 8.00% CAGR to 2031.

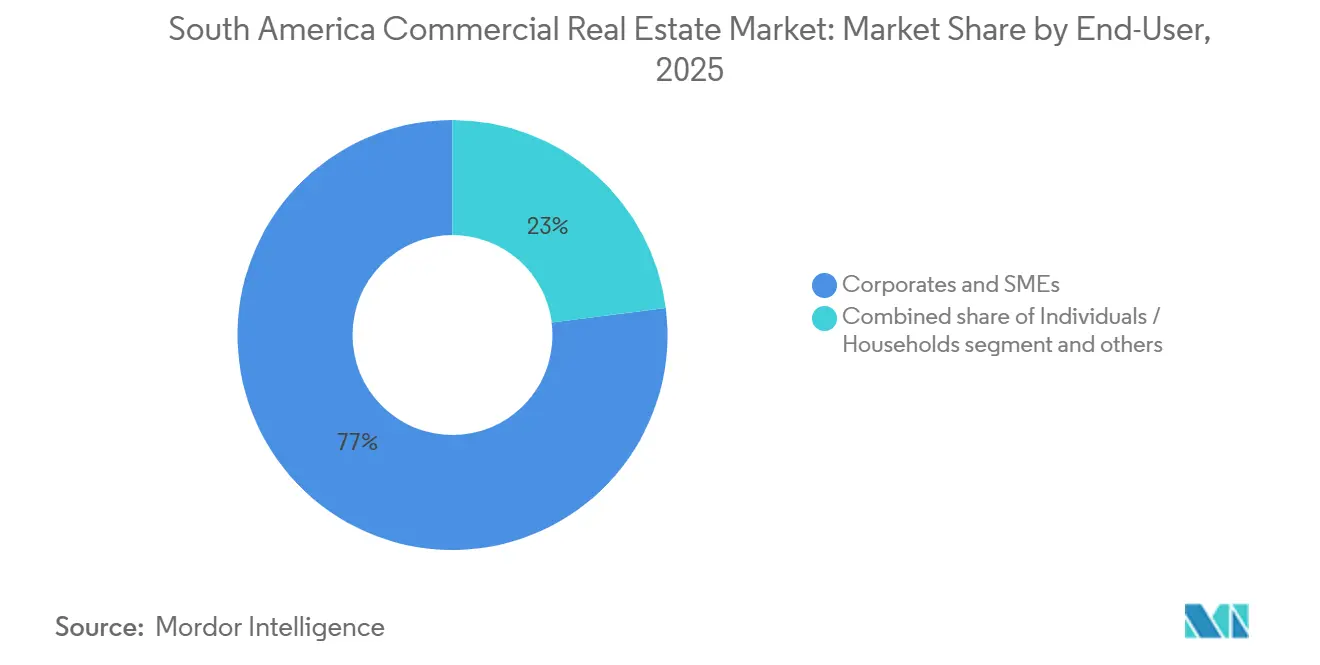

- By end-user, corporates and SMEs accounted for 77% of the 2025 transaction value, while the individuals and households segment is expected to grow at a 7.88% CAGR over 2026-2031.

- By geography, Brazil dominated with a 44% revenue share in 2025, whereas Peru is poised to record the quickest national expansion at 8.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating e-commerce lifts warehouse and cold-chain demand | +1.5% | Brazil, Chile, Argentina, Colombia | Short term (≤ 2 yrs) |

| Port, metro, and highway upgrades unlock developable corridors | +1.3% | Brazil, Chile, Peru, Colombia | Long term (≥ 4 yrs) |

| China-plus-one manufacturing shift fuels new logistics clusters | +1.2% | Brazil, Chile, Colombia | Medium term (2-4 yrs) |

| Hyperscale and edge data-center rollout births a niche asset class | +0.9% | Brazil, Chile | Medium term (2-4 yrs) |

| Tourism rebound revives hospitality-anchored mixed-use schemes | +0.8% | Brazil, Chile, Argentina, Peru | Short term (≤ 2 yrs) |

| Green-hydrogen export hubs seed heavy-industrial parks | +0.7% | Chile, Brazil | Long term (≥ 4 yrs) |

| Source: Mordor Intelligence | |||

China-plus-one Manufacturing Shift Fuels New Logistics Clusters

Global automakers and electronics firms are redistributing capacity from coastal China to Brazil’s Northeast and Chile’s Central Region, driving conversion of farmland into Grade A cross-dock parks. Anchor tenants such as BYD (Bahia) and Great Wall Motors (São Paulo) have signed long-term leases, prompting speculative developers to pre-grade secondary sites that sit within two hours of deep-water ports[2]Reuters staff, “BYD to build EV complex in Bahia,” reuters.com. Vacancy in these corridors has fallen below 6%, and average take-up periods have shortened to six months, half the 2023 cycle time.

Accelerating E-commerce Lifts Warehouse and Cold-chain Demand

Online retail penetration exceeded 15% of overall South American sales in 2025, yet less than one-quarter of existing sheds offer clear heights above 12 m or automated sortation. Platforms such as Mercado Libre committed over USD 135 million to a new Santiago fulfillment hub able to process 75,000 parcels per hour. Parallel cold-chain investments from Emergent Cold LatAm are integrating export seafood and domestic grocery flows under single roofs, tightening the South America commercial real estate market for temperature-controlled space.

Tourism Rebound Revives Hospitality-anchored Mixed-use Schemes

Inbound arrivals climbed back to 95% of 2019 levels by mid-2025, but travelers are favoring curated experiences over mass tourism. Luxury boutiques in Santa Catarina and themed resorts in Rio Grande do Sul are posting ADRs 30-40% above 2024 comparables. Retail landlords now retrofit underperforming GLA into food, culture, and entertainment venues, raising blended tenant sales per square foot by double digits. Mixed-use formats that pair hotels, residential towers, and destination retail are broadening the South America commercial real estate industry investor base.

Port, Metro, and Highway Upgrades Unlock Developable Corridors

São Paulo Metro will deliver 15 new stations by 2028, raising allowable FARs along the Urban Structuring Axis to 4× and triggering land-use conversions from single-family to high-rise mixed-use. In Peru, the USD 10 billion Lima Metro Lines 3 and 4 slash port-to-warehouse drayage by 40%, catalyzing industrial land assemblies around Callao. Chile’s USD 19 billion renegotiation of highway concessions embeds digital tolling that improves freight velocity, further concentrating demand for roadside logistics parks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and FX swings crimp underwriting | −1.8% | Brazil, Argentina, Chile, Colombia | Short term (≤ 2 yrs) |

| Cost inflation and expensive credit squeeze project IRRs | −1.4% | Brazil, Chile, Peru, Argentina | Short term (≤ 2 yrs) |

| Fragmented permitting and land-title regimes delay starts | −0.9% | Brazil, Chile, Argentina, Colombia | Medium term (2-4 yrs) |

| Climate-related floods and droughts lift insurance premiums | −0.6% | Brazil, Chile, Argentina, Peru | Long term (≥ 4 yrs) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility and FX Swings Crimp Underwriting

Brazil’s Selic reached 12.25% in early 2026 and may touch 15% by mid-year, widening debt-service coverage gaps for leveraged deals[3]Reuters staff, “Brazil’s Selic rate may hit 15%,” reuters.com. The real lost 12% against the USD from 2024-2025, eroding unhedged equity returns. Foreign investors increasingly structure joint ventures with local operators that can access subsidized BNDES lines or peso-denominated debt to stabilize capital stacks.

Fragmented Permitting and Land-title Regimes Delay Starts

Chile’s Law 21.718 caps approval windows at 60 days for large projects, yet 437 filings worth USD 54.1 billion remained in environmental limbo as of late 2025. In Brazil, more than 5,500 municipalities apply bespoke zoning codes, stretching mixed-use approvals to 18 months and adding up to 12% in carry costs. Digitization initiatives such as Chile’s SUPER platform promise 30-70% cycle-time reductions once fully operational.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices Recover While Logistics Holds the Crown

Logistics and industrial parks retained a commanding 32.22% share of the South America commercial real estate market size in 2025. Prime last-mile facilities inside 30 km urban rings repeatedly traded at sub-7% stabilized yields, underscoring the scarcity premium. Office inventory, though smaller, is slated to post a 9.50% CAGR over 2026-2031 as vacancy in São Paulo’s CBD fell from 20.8% in 2024 to 15.9% in 2025. Trophy towers near new metro stops achieved double-digit rent growth, signaling a flight to quality.

Developers are adding wellness features, biophilic terraces, and low-carbon materials to future office pipelines, differentiating them from retrofit-challenged stock. Meanwhile, cold-chain sub-segments inside the broader logistics slate command a 25-30% rental premium and often transact via long-term sale-and-leasebacks with grocery and pharma tenants, widening the investable universe within the South America commercial real estate market.

By Business Model: Leases Outpace Outright Sales

Rental structures dominated 61% of the 2025 transaction value, mirroring global capital’s preference for recurring cash flows underpinned by CPI-linked escalators. Triple-net logistics leases of 10-15 years, where tenants shoulder taxes and maintenance, are becoming the fixed-income proxy of choice for pension funds. Sales transactions remain vital for merchant builders to recycle capital; LOG Commercial Properties’ USD 183 million bulk disposal of 12 sheds in 2026 illustrates the exit avenue into core-plus investors.

Hybrid models have also emerged, forward-funding agreements that de-risk construction for developers and secure a pipeline for income funds before practical completion, further institutionalizing the South America commercial real estate market.

By End-user: Corporates Still Rule, but Households Gain Traction

Corporates and SMEs absorbed 77% of gross leasing in 2025, fueled by reshoring manufacturers and omnichannel retailers. However, the households category is slated for a 7.88% CAGR as mixed-use districts integrate branded residences, surf clubs, and concierge-run rental stock. JHSF’s high-end residential rental platform, clocking near-full occupancy across 140,000 m², showcases rising consumer appetite for managed living experiences inside premium micro-markets.

Developers that can curate live-work-play ecosystems hedge against single-tenant risk while tapping differentiated income streams, membership fees, F&B revenue, and short-term lodging, beyond conventional lease contracts within the South America commercial real estate industry.

Geography Analysis

Brazil accounted for 44% of South America's commercial real estate market value in 2025, underpinned by a 215 million-resident consumer base and the continent’s densest institutional capital pool. Prologis alone commands 19.5 million ft² of Brazilian GLA and launched USD 159 million of new starts in 2025. Metro extensions and zoning incentives in São Paulo are compressing office vacancy and catalyzing high-rise mixed-use corridors along Lines 2, 5, and 6.

Chile and Peru are punching above their weight on growth metrics. Santiago’s colocation data-center pipeline now exceeds 90 MW, creating a fresh demand node for suburban power-rich campuses. Peru is poised for an 8.20% CAGR through 2031, thanks to Lima Metro’s USD 10 billion Lines 3-4 and retail consolidation plays such as Mallplaza’s USD 454 million Falabella Perú takeover.

Argentina and Colombia offer selective upside. Buenos Aires vacancy stabilized at 18.5% in 2025 after IRSA’s incremental mall acquisitions. Bogotá’s first-line metro and 4G highway PPPs are unlocking ex-urban land banks, but permitting drag and FX instability temper near-term pipelines. Uruguay, Paraguay, and the Andean interior together represent under 10% of value yet supply niche hospitality and agrologistics opportunities sought by regional developers diversifying beyond Brazil.

Competitive Landscape

Global logistics REITs such as Prologis and GLP recycle mature Brazilian assets into local core funds, freeing capital for higher-yield greenfield plays. Retail heavyweights Aliansce-BR Malls (69 malls) and Mallplaza are consolidating to maximize tenant-mix synergies and procurement economies.

Capital-light structures are proliferating, GLP’s USD 300 million sale into a BTG Pactual-Brookfield JV retained asset-management fees while derisking exposure. Developers with digital leasing front-ends and smart-building IoT stacks achieve faster absorption and lower opex, widening performance gaps versus legacy stock. Cold-chain specialists and data-center operators, while small today, are emerging power brokers by locking in investment-grade covenants on 15-year paper.

E-commerce platforms are vertically integrating: Mercado Libre’s own distribution network shaved fulfilment costs by 22 bps year-on-year, compelling third-party landlords to match automation standards or risk obsolescence. Institutional appetite now hinges less on landbanks and more on execution capabilities, tenant relationships, and access to sub-10% USD leverage sources.

South America Commercial Real Estate Industry Leaders

Brookfield Asset Management

BR Malls Participações

Multiplan Empreendimentos

Prologis

LOG Commercial Properties

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LOG Commercial Properties divested 12 Brazilian sheds totaling 340,200 m² for USD 183 million, redirecting proceeds to landbank acquisitions in secondary corridors.

- January 2026: Parque Arauco purchased the 40,000 m² Parque Chicureo mixed-use center in Santiago for USD 106 million, expanding its capital-region cluster.

- December 2025: Mallplaza closed a USD 454 million tender for 99.77% of Falabella Perú, adding 619,000 m² GLA across 15 malls.

- March 2025: Iguatemi led a USD 450 million consortium to acquire majority stakes in São Paulo luxury malls Pátio Higienópolis and Pátio Paulista.

South America Commercial Real Estate Market Report Scope

| Offices |

| Retail |

| Logistics |

| Others |

| Sales |

| Rental/Leasing |

| Individuals / Households |

| Corporates & SMEs |

| Others |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others | |

| By Business Model | Sales |

| Rental/Leasing | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America commercial real estate market?

It was valued at USD 301.33 billion in 2025 and is projected to reach USD 485.3 billion by 2031.

Which segment leads by market share in South American commercial real estate?

Logistics and industrial parks held 32.22% of value in 2025, the highest among all property types.

Which country is expected to grow fastest in South America’s commercial property arena?

Peru is forecast to post an 8.20% CAGR between 2026 and 2031, outpacing regional peers.

Why are rental structures favored over outright sales?

Institutional capital prefers long-duration, CPI-linked cash flows from leases, which accounted for 61% of 2025 transaction value.

How are data centers shaping commercial real estate investment?

Over USD 500 million earmarked for Brazilian hyperscale campuses is spawning a new niche with 10-15-year triple-net leases, attracting pension-fund money.

Page last updated on: