GCC Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

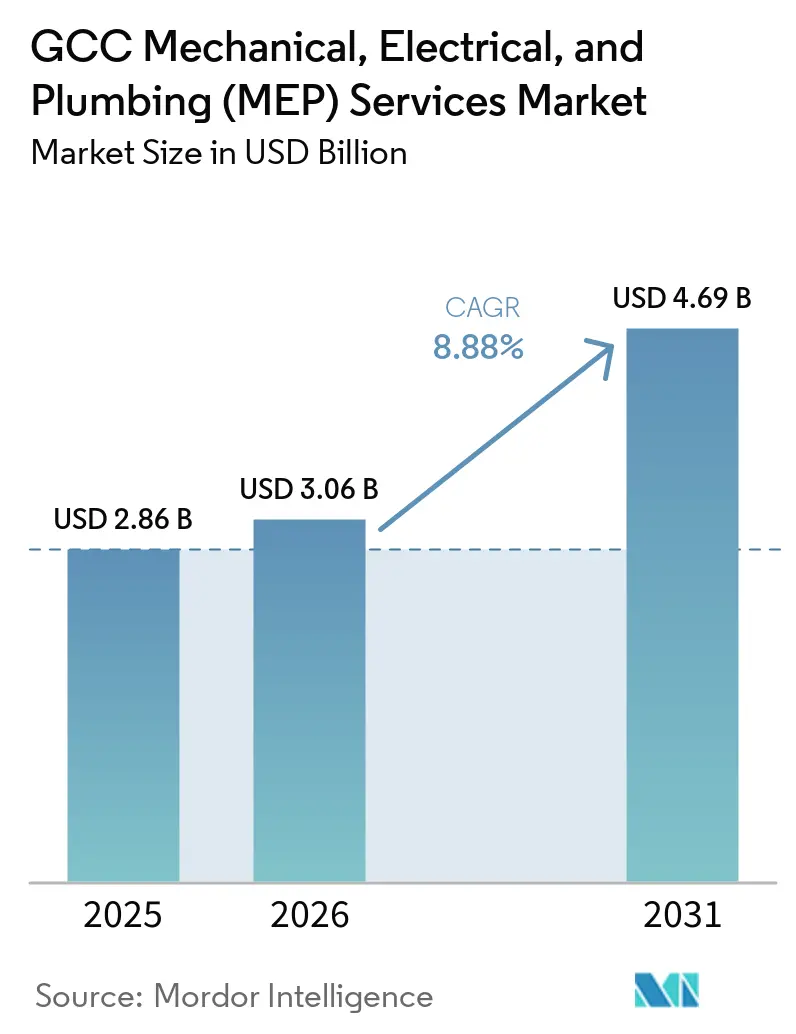

| Base Year Market Size (2025) | USD 2.86 Billion |

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The GCC Mechanical, Electrical, and Plumbing Services Market size is projected to expand from USD 2.86 billion in 2025 and USD 3.06 billion in 2026 to USD 4.69 billion by 2031, registering a CAGR of 8.88% between 2026 and 2031. This outlook is supported by a GCC project pipeline of contracts above USD 2 trillion, with Saudi Arabia holding nearly half and the UAE accounting for 27.5%, which keeps the GCC MEP services market tied to a broad base of construction activity across the region. Construction, transport, and power together represent more than 71% of that pipeline, so demand is not dependent on a single project class and the GCC MEP services market has a more durable order base than a pure building cycle would suggest. Owners are also moving toward integrated delivery, modular fabrication, AI-assisted engineering, and digital twin management to achieve tighter schedule control, fewer coordination gaps, and clearer accountability on large programs. Mission-critical facilities such as hyperscale data centers are raising the technical bar for contractors in the GCC MEP services market, as AI workloads require far heavier cooling and power design than legacy enterprise sites. Supply chain disruption, skilled labor shortages, and payment-cycle pressure still weigh on execution, but modular fabrication, in-country value rules, and the GCC 2025 contract revision are improving stability for better-capitalized firms.

Key Report Takeaways

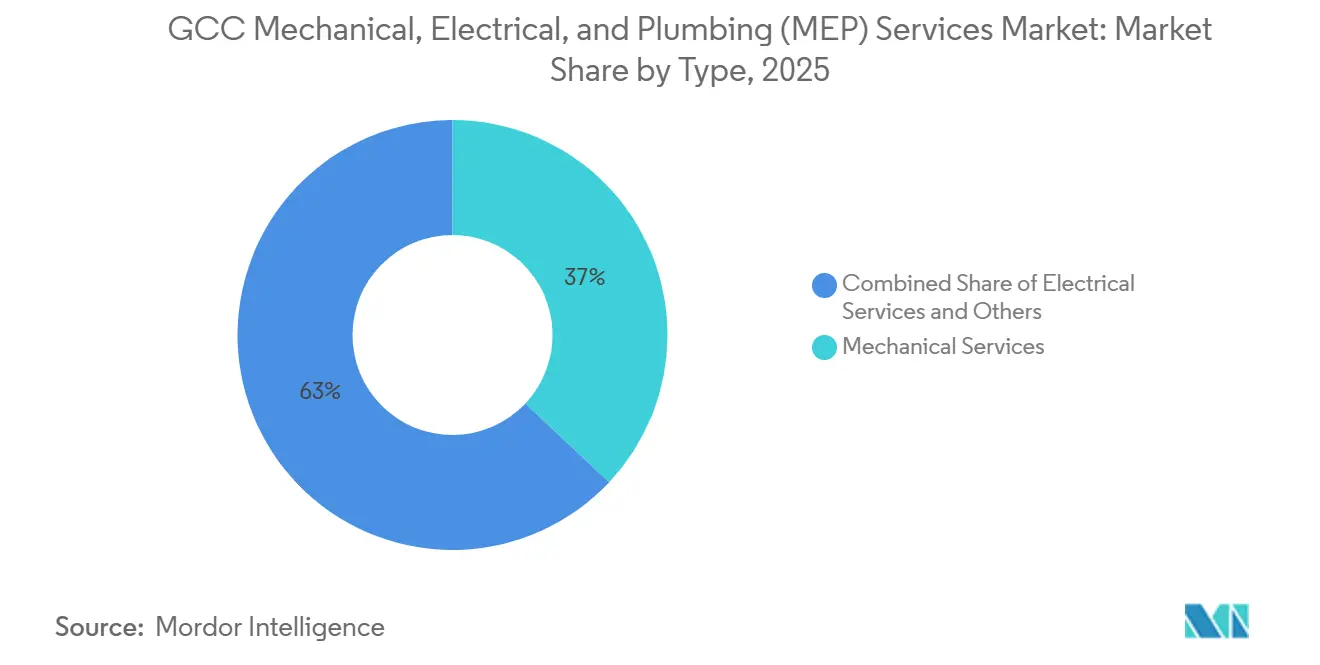

- By type, mechanical services led with 37% of GCC MEP services market share in 2025, while integrated MEP is forecast to expand at 11.37% CAGR through 2031.

- By service type, maintenance, repair, and retrofit held 34% of the GCC MEP services market size in 2025, while managed or performance-based services are projected to grow at 10.30% CAGR through 2031.

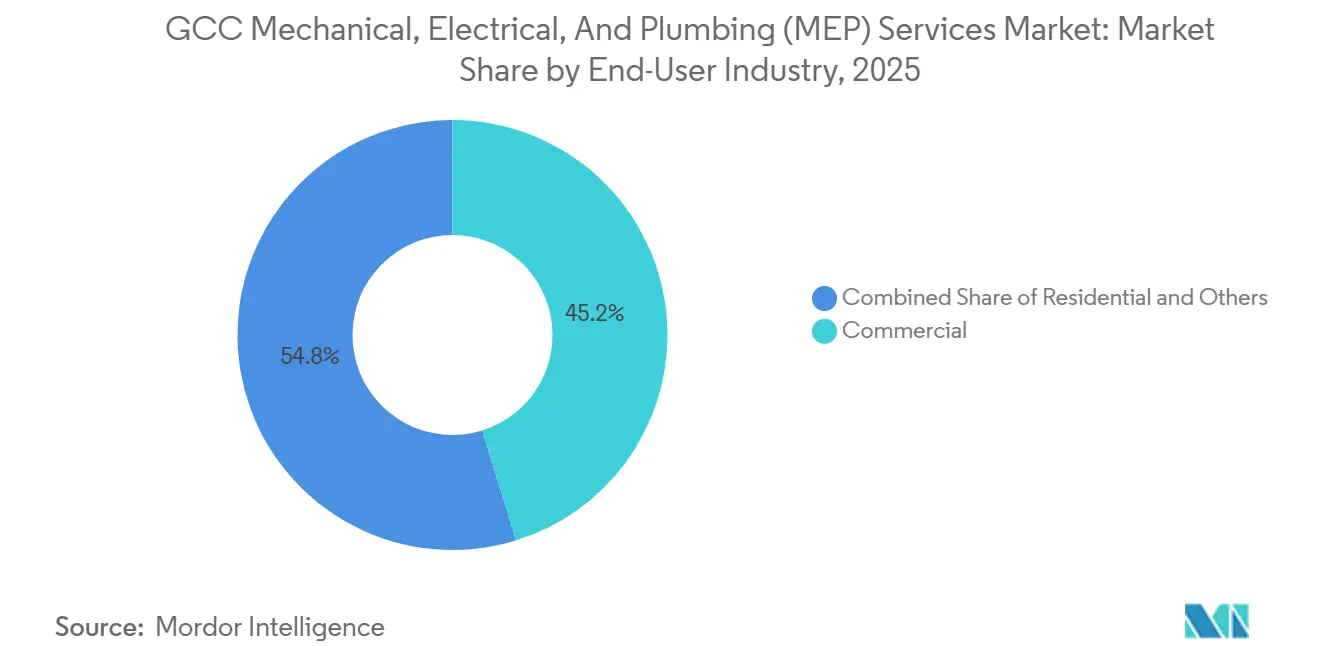

- By end-user industry, commercial applications accounted for 45.2% share of the GCC MEP services market size in 2025, while infrastructure is advancing at 11.90% CAGR through 2031.

- By geography, Saudi Arabia represented 24.50% share of the GCC MEP services market size in 2025, while Qatar records the highest projected CAGR at 10.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Giga-Projects and Mixed-Use Development Pipelines | +2.2% | Saudi Arabia and UAE, with spillover to Qatar | Medium term (2-4 years) |

| District Cooling and Green-Building Mandates | +1.5% | UAE, Qatar, and Saudi Arabia | Long term (≥ 4 years) |

| Data-Center and Specialist Cooling Demand | +1.4% | UAE, mainly Abu Dhabi and Dubai, and Saudi Arabia | Medium term (2-4 years) |

| Hospitality, Airport, and Tourism Infrastructure Expansion | +1.3% | Saudi Arabia, UAE, Qatar, and Bahrain | Medium term (2-4 years) |

| Offsite Modular MEP Adoption for Schedule Compression | +0.7% | Concentrated in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Centralized Cooling Carbon-Credit Monetization | +0.6% | UAE, mainly Dubai, and Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Giga-Projects and Mixed-Use Development Pipelines

Saudi Arabia remains the central volume engine for the GCC MEP services market because Expo 2030 Riyadh, FIFA 2034, NEOM, Diriyah Gate, and New Murabba are keeping large project packages in motion through the next delivery cycle. The important shift is that more spending is moving from early civil work into fit-out and MEP completion phases, where revenue per square meter is higher and package coordination becomes more demanding. Saudi Arabia’s Q1 2026 project awards reach USD 11 billion, confirming that award momentum remains strong even as project pacing is recalibrated across selected megaprograms. NEOM’s active on-site workforce exceeded 50,000 in 2026, which shows that execution remains live at scale and keeps downstream mechanical, electrical, and plumbing packages relevant for years rather than quarters. Across the wider region, the USD 2 trillion pipeline gives the GCC MEP services market continuous exposure to mixed-use, cultural, transport, and utility projects instead of a narrow reliance on one development model.

District Cooling and Green-Building Mandates

District cooling remains one of the most valuable recurring service streams in the GCC MEP services market because plant design, network integration, and long-term operation contracts extend revenue well beyond initial installation. Empower signed the design contract for its fifth Business Bay plant in February 2026 and had already advanced a 47,000-RT plant in Dubai Science Park in August 2025, which shows that new capacity additions continue to feed large mechanical packages in Dubai[1]Dubai Media Office, “إمباور توقع عقد تصميم محطة تبريد جديدة في مجمع دبي للعلوم,” Al Bayan, albayan.ae. Empower’s agreement with Mitsubishi Heavy Industries for 56,250 RT of centrifugal water-cooled chillers, with deliveries starting in 2025, also shows how long-term technology tie-ups are shaping procurement and installed base expansion in the regional cooling chain. Dubai Executive Council Resolution No. 87 of 2025 formalizes fees, fines, and compliance conditions for district cooling providers, thereby raising entry barriers and favoring licensed integrators with greater regulatory depth. Sustainability codes are also widening specification scope because Saudi Arabia’s Mostadam processed 7 million square meters under SBC 1001 in Q1 2025 and Qatar’s QCS 2024 added updated environmental requirements that increase the compliance burden on building services packages

Data-Center and Specialist Cooling Demand

Data centers are reshaping the upper end of the GCC MEP services market because AI racks running at 40-100 kW require cooling and electrical systems fundamentally different from those in legacy enterprise environments. In practice, this means liquid cooling, direct-to-chip architecture, immersion systems, and much larger power distribution loads, which turn the MEP layer into the defining element of the facility rather than a support package. KPMG’s 2026 benchmarking shows that a 30 MW data center in the Middle East carries construction costs of USD 7 million per MW for the general contractor scope, including USD 2 million in mechanical and USD 2.5 million in electrical content per MW, which explains why mission-critical work is becoming a high-margin specialization. AirTrunk and Humain were seeking MEP bids for a 250 MW hyperscale project in Riyadh in May 2026, which signals that single-project awards can now reach a scale usually associated with major infrastructure rather than conventional buildings. As sovereign AI plans and hyperscaler spending accelerate, the GCC MEP services market is likely to reward firms that have certified liquid-cooling capability, prefabricated module capacity, and mission-critical commissioning depth.

Hospitality, Airport, and Tourism Infrastructure Expansion

Hospitality and aviation programs are creating some of the most specification-heavy packages in the GCC MEP services market by combining comfort, safety, reliability, and brand-level commissioning requirements within a single scope. The GCC hotel development pipeline totals 161,574 rooms across more than 650 projects, with Saudi Arabia alone accounting for 92,000 rooms, keeping fit-out and system integration demand high across tourism-led developments. Airport infrastructure adds another layer of demand because Dubai World Central’s planned expansion to 260 million annual passenger carries a Dh128 billion (USD 34.9 billion) budget that includes extensive terminal, utility, and systems work. Emirates breaks ground on a USD 5.1 billion engineering complex at Dubai South in May 2026, spanning 1.1 million square meters and targeting LEED Platinum certification, indicating that aviation maintenance facilities are becoming a distinct high-value demand pool rather than an extension of general commercial buildings. These projects carry more complex HVAC zoning, structural power distribution, fire suppression, and controls integration, so contractors with hospitality and aviation experience are better placed to defend margin in the GCC MEP services market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Equipment Lead Times and Price Volatility | -0.8% | GCC-wide, with the strongest effect in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Skilled Labor and Execution Bottlenecks | -0.6% | Saudi Arabia, UAE, and Qatar | Medium term (2-4 years) |

| Payment-Cycle and Contractor Cash-Flow Pressure | -0.5% | GCC-wide, especially among SME subcontractors in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Limited Retrofit Suitability for District-Cooling Conversion | -0.3% | UAE, Saudi Arabia, Qatar; older commercial and residential clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Equipment Lead Times and Price Volatility

Import dependence still limits execution speed in the GCC MEP services market because chillers, transformers, generators, LV switchgear, and UPS systems already carry long procurement cycles before transport risk is added. The 2026 Strait of Hormuz disruption pushed landed costs for Chinese building materials up by 10-25%, with PVC pipes rising 36% and petrochemical feedstocks increasing 15%, while rerouting through the Cape of Good Hope lengthened transit times by 30%. Mid-tier contractors are more exposed because they often work on fixed-price terms without the same supplier leverage or hedging capacity as larger regional firms. Many firms have responded by ordering 30-50% of critical equipment upfront, but that approach locks up cash and raises balance-sheet pressure before site progress can convert into billing. The result is that procurement risk is starting to shift more work toward better-capitalized contractors, which supports consolidation inside the GCC MEP services market.

Skilled Labor and Execution Bottlenecks

Import dependence still limits execution speed in the GCC MEP services market because chillers, transformers, generators, LV switchgear, and UPS systems already carry long procurement cycles before transport risk is added. The 2026 Strait of Hormuz disruption pushed landed costs for Chinese building materials up by 10-25%, with PVC pipes rising 36% and petrochemical feedstocks increasing 15%, while rerouting through the Cape of Good Hope lengthened transit times by 30%. Mid-tier contractors are more exposed because they often work on fixed-price terms without the same supplier leverage or hedging capacity as larger regional firms. Many firms have responded by ordering 30-50% of critical equipment upfront, but that approach locks up cash and raises balance-sheet pressure before site progress can convert into billing. The result is that procurement risk is starting to shift more work toward better-capitalized contractors, which supports consolidation inside the GCC MEP services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Systems Anchor Revenue as Integrated MEP Expands

Mechanical services held 37% of the GCC MEP services market size in 2025, which made this the largest type segment and reflected the region’s heavy dependence on cooling infrastructure. Empower’s connected and contracted district cooling footprint in Dubai, supported by 88 operating stations and capacity close to 2.0 million refrigeration tons by end-2025, shows how deeply mechanical scope is embedded in the urban asset base. Electrical services formed the second-largest type because utility expansion remains active, with DEWA commissioning 8 main 132 kV transmission stations and 2 new 400 kV stations in 2025 under an AED 8.5 billion (USD 2.3 billion) expansion program running through 2028. Plumbing remained smaller in contract value, but it is becoming more complex as condensate reuse, treated sewage effluent use in cooling towers, and greywater recycling become more common within regional sustainability frameworks.

Integrated MEP is the fastest-growing type at 11.37% CAGR through 2031, which shows how strongly owners now prefer single-point responsibility on complex schemes. The main reason is execution risk, since multi-phase developments across hospitality, culture, transport, and mixed-use real estate have shown that fragmented packages can create coordination gaps, rework, and delay. Al-Futtaim Engineering’s nine-month delivery at the Dubai Exhibition Centre, with more than 2,000 skilled workers, 200 engineers, 90 km of LV cabling, 11 km of busbar systems, and 100,000 square meters of HVAC ductwork, illustrates the scale advantage behind integrated delivery in the GCC MEP services industry. AI use in engineering and procurement is also shortening tender cycles and design revisions, which strengthens the commercial case for integrated awards over separated subcontracting in the GCC MEP services market[2]Al-Futtaim, “Al-Futtaim Engineering Achieves Record MEP Delivery at Dubai Exhibition Centre,” Al-Futtaim, alfuttaim.com .

By Service Type: Maintenance Anchors Revenue as Performance Contracts Gain Traction

Maintenance, repair, and retrofit held 34% of revenue in 2025, making it the largest service-type segment in the GCC MEP services market. This reflects the maturity of the UAE asset base and the steady reuse of major venues in Qatar, where post-FIFA facilities are being repositioned for broader urban use. Owners are increasingly moving toward performance-based contracts that tie payment to lower energy use, less downtime, and better occupant safety outcomes rather than simple activity billing. Design and engineering is also gaining weight because BIM and 5D cost modeling require MEP teams to join earlier and influence design choices before procurement and installation are locked in.

Managed or performance-based services are the fastest-growing service segment, with a 10.30% CAGR through 2031. Predictive maintenance tools can reduce equipment downtime by up to 25%, which gives owners a measurable reason to shift from reactive maintenance to technology-led contracts. BETAM expanded its smart building technology and retrofit capabilities in 2025 and 2026, which shows how providers are repositioning away from pure installation work toward digital service delivery. The result is a more recurring revenue model where analytics, sensor data, and energy outcomes matter as much as labor deployment. That transition is changing the relationship between asset owners and contractors across the GCC MEP services market and is gradually turning service depth into a stronger competitive lever than scale alone.

By End-User Industry: Commercial Leads Revenue as Infrastructure Accelerates

Commercial applications held 45.2% of revenue in 2025, so this remained the largest end-user segment in the GCC MEP services market. Office, retail, hospitality, and mixed-use programs across Dubai, Riyadh, and Doha continue to support that base, especially where fit-out quality and operating efficiency matter more than shell construction. The GCC hotel pipeline of 161,574 rooms increases this pressure because hospitality projects require tighter HVAC zoning, high-end plumbing, and stronger BAS and ELV integration than standard office buildings. Residential MEP is also expanding in volume as ROSHN’s 300,000-plus planned units and the Al Waha Residences conversion at Expo City Dubai move more projects into active execution.

Infrastructure is the fastest-growing end-user at 11.90% CAGR through 2031, which makes it the clearest growth engine for higher-spec packages. Airport expansions, power grid upgrades, data center campuses, and water treatment facilities all carry broader electrical and mechanical scope than conventional building categories. The Emirates engineering complex, the Dubai World Central expansion, and the GCC Interconnection Authority’s USD 500 million UAE-Oman link show how live infrastructure projects are widening the demand base for the GCC MEP services market. Drake & Scull’s 116% revenue increase in 2025, supported by UAE infrastructure work and Passavant water contracts, shows how contractors with the right technical base can scale faster when exposed to utility and infrastructure packages. This also suggests that the GCC MEP services industry is gaining more resilience as demand shifts beyond office towers and mixed-use buildings into longer-duration public and industrial assets.

Geography Analysis

Saudi Arabia held 24.50% of GCC MEP services market share in 2025, which made it the largest national market and the main growth anchor for the region. Saudi Arabia’s Q1 2026 project awards reach USD 11 billion, the highest quarterly total in MENA, which confirms that project activity remains deep even as pacing has changed across selected programs. NEOM’s active site workforce exceeds 50,000 in 2026, which indicates that downstream packages for fit-out, systems integration, and commissioning will stay large as projects move through later delivery stages. ROSHN’s 300,000-plus planned homes and the Expo 2030 and FIFA 2034 build cycle add another layer of demand, especially in residential, hospitality, mobility, and public-venue assets. Mostadam’s processing of 7 million square meters under SBC 1001 in Q1 2025 also means sustainability-related MEP upgrades are now entering standard project design at scale.

The UAE remains the most commercially mature part of the GCC MEP services market because Dubai and Abu Dhabi support different but complementary demand centers. Dubai’s grid expansion program is valued at AED 8.5 billion (USD 2.3 billion) through 2028, covering 52 new 132 kV stations and 223 km of underground cables, which sustains a large electrical workload even outside the normal building cycle. Empower’s station network, connected portfolio, and new plant design work in Business Bay and Dubai Science Park provide the UAE with a recurring mechanical services base that other GCC countries do not match. Abu Dhabi’s AED 3.6 billion (USD 1 billion) Al Dhafra power plant financing to support AI data center electricity demand shows how power investment is now being tied directly to hyperscale digital infrastructure. Qatar is forecast to grow fastest at 10.74% CAGR through 2031 as stadium reuse, smart-city systems, and performance-based facility management continue to widen the regional role of the GCC MEP services market.

Kuwait, Oman, and Bahrain are smaller in absolute size, but they still add important targeted demand to the GCC MEP services market. Kuwait’s airport terminal development and linked power infrastructure continue to support aviation and electrical packages with high technical requirements. Oman’s USD 500 million interconnection project, the 530 km 400 kV corridor, Musandam Airport, and the Sustainable City Yiti program are widening project mix beyond oil and gas and into utility, transport, and low-carbon urban assets. Bahrain’s April 2026 district cooling EPC award for a 12,000-RT network expansion in Manama shows that even the smallest GCC markets are using energy-transition goals to expand specialized building services scope.

Competitive Landscape

The GCC MEP services market is moderately fragmented, with regional players such as BK Gulf, ALEMCO, Al-Futtaim Engineering, Khansaheb, and JLW Middle East competing beside a wide field of country-specialist firms. Scale still matters, but differentiation now comes more from prefabrication depth, AI-assisted engineering, BIM coordination, and digital twin capability than from labor cost alone. BIM is already standard across tier-1 contractors, while 5D cost modeling and automated procurement are emerging as the next layer of execution advantage in the GCC MEP services market. This leaves standard packages under pricing pressure, while complex work in district cooling, data centers, and integrated fit-out continues to carry better margins.

BK Gulf’s investment in the UAE’s first purpose-built MEP modular facility is one clear example of how off-site production has moved from optional to strategic. ALEMCO also accelerated automated workflows and prefabrication for hyperscale data center delivery in 2026, which shows that modular capability is now central to competing for specialist work. Royal Advance Electromechanical launched a dedicated modular factory line in January 2026 and targeted AED 50 million (USD 13.6 million) in first-year revenue, reinforcing the same market direction. Al-Futtaim Engineering’s compressed delivery at the Dubai Exhibition Centre provides another example of how labor coordination, integration, and execution discipline can win large packages even when site timelines are tight. Johnson Controls added pressure from the supplier side when it released a second AI factory cooling reference design guide in May 2026, which influences the technical baseline that GCC contractors increasingly need to meet[3]Johnson Controls, “Johnson Controls Releases Second Data Center Reference Design Guide to Advance Industrial-Scale AI Factory Cooling,” Johnson Controls, johnsoncontrols.com.

The clearest white-space opportunities are performance-based services, specialist liquid cooling, and cross-border integrated delivery for Saudi giga-projects. Adjacent players such as CCC and CSCEC Middle East are appearing in selected industrial and cultural packages, but their role is stronger in EPC-led or civil-led projects than in pure building MEP delivery. Country licensing, certification, and regulatory familiarity still matter because developers want fewer handoff risks and more reliable compliance across different GCC jurisdictions. That keeps the GCC MEP services market open to both scaled incumbents and focused niche contractors, especially where district energy, mission-critical cooling, and digital operations capability are decisive.

GCC Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

BK Gulf

ALEMCO

Al-Futtaim Engineering

Voltas

Khansaheb MEP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Emirates broke ground on a USD 5.1 billion engineering complex at Dubai South, covering 1.1 million square meters and targeting LEED Platinum certification. The facility will simultaneously service 28 wide-body aircraft and incorporates MEP scope across the world's largest free-span hangar, extensive workshop space, and 50,000 sq m of administrative infrastructure. China Railway Construction Corporation is the main contractor, with Artelia as consultant .

- May 2026: Bids were received for a 250 MW hyperscale AI data center in Riyadh, a collaboration between AirTrunk and Humain (Saudi PIF's AI infrastructure company), constituting one of the largest individual MEP scopes for a single data center project in GCC history.

- April 2026: Tabreed Bahrain awarded an EPC contract to Arabian International Company for a 12,000-refrigeration-ton district cooling network expansion in Manama's northern seafront area, supporting Bahrain's net-zero carbon commitments with operations expected in summer 2027.

- March 2026: CSCEC Middle East's joint venture with El Seif Engineering Contracting and Midmac Contracting secured the MEP scope for the Royal Diriyah Opera House in Riyadh, a flagship cultural infrastructure project within the Diriyah Gate Development Authority program.

GCC Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The GCC MEP Services Market is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance Repair & Retrofit, Managed/Performance-based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance, Repair, and Retrofit |

| Managed / Performance-based Services |

| Residential |

| Commercial |

| Infrastructure |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance, Repair, and Retrofit | |

| Managed / Performance-based Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the projected value of the GCC MEP services market by 2031?

The GCC MEP services market is forecast to reach USD 4.69 billion by 2031, up from USD 3.06 billion in 2026, with an 8.88% CAGR over 2026-2031.

Which service type currently leads revenue in GCC MEP services?

Maintenance, repair, and retrofit leads service revenue with a 34% share in 2025, supported by a large installed asset base and growing demand for performance-based contracts.

Which type segment is growing fastest across GCC MEP services?

Integrated MEP is the fastest-growing type segment, advancing at 11.37% CAGR through 2031 as developers prefer single-point accountability on complex projects.

Which end-user segment is expanding fastest in the region?

Infrastructure is the fastest-growing end-user segment with an 11.90% CAGR through 2031, driven by airports, power grids, water assets, and hyperscale data centers.

Page last updated on: