Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

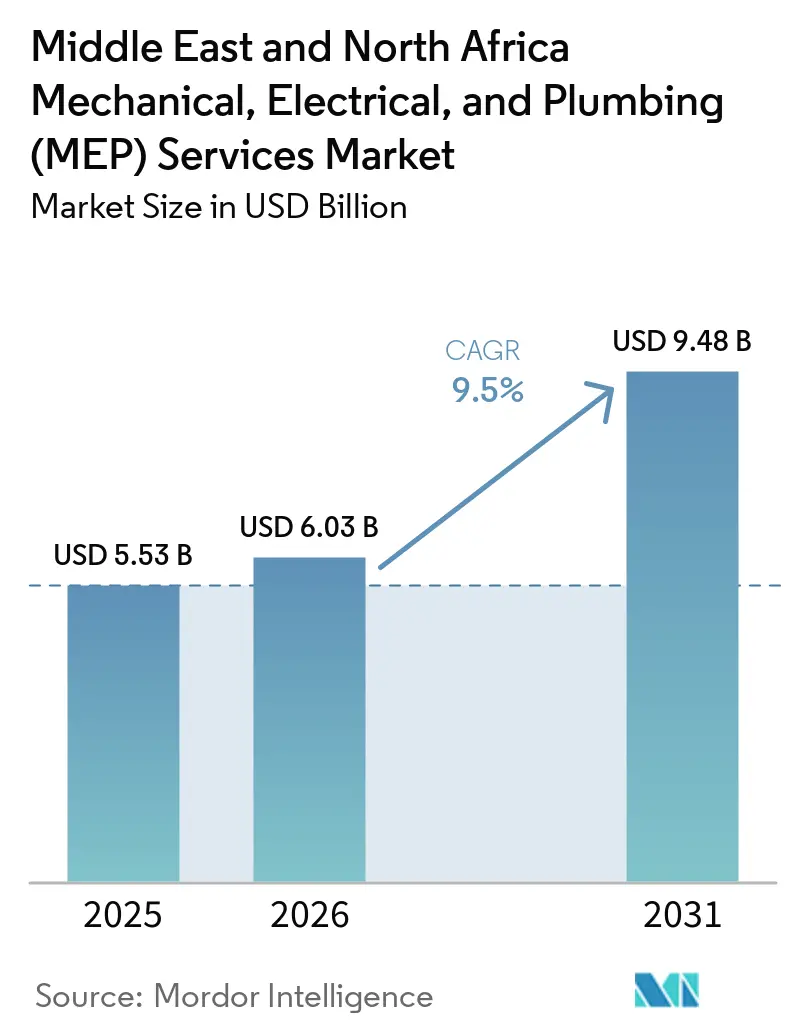

| Base Year Market Size (2025) | USD 5.53 Billion |

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 9.48 Billion |

| Growth Rate (2026 - 2031) | 9.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The Middle East And North Africa Mechanical, Electrical, And Plumbing Services Market size is projected to be USD 5.53 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.48 billion by 2031, growing at a CAGR of 9.5% from 2026 to 2031. Saudi Arabia remains the main volume driver because sovereign-backed construction keeps large mechanical, electrical, and plumbing packages moving across long-duration programs, which gives the MENA MEP services market a clear center of gravity. The UAE adds balance to the MENA MEP services market because demand comes from commercial real estate, data centers, hospitality assets, and retrofit work, rather than from a single funding channel. Energy-efficient upgrades are becoming more important in a cooling-intensive built environment, which raises the value of design-led scopes and creates longer maintenance opportunities after initial project delivery. Data-center and district-cooling work is also lifting the technical intensity of the MENA MEP services market, especially where developers want integrated accountability across multiple building systems and faster coordination between design and execution. Competition remains moderate to high, and contractors with stronger balance sheets, in-house fabrication, and digital coordination capability are better placed to manage payment delays, labor pressure, and material volatility.

Key Report Takeaways

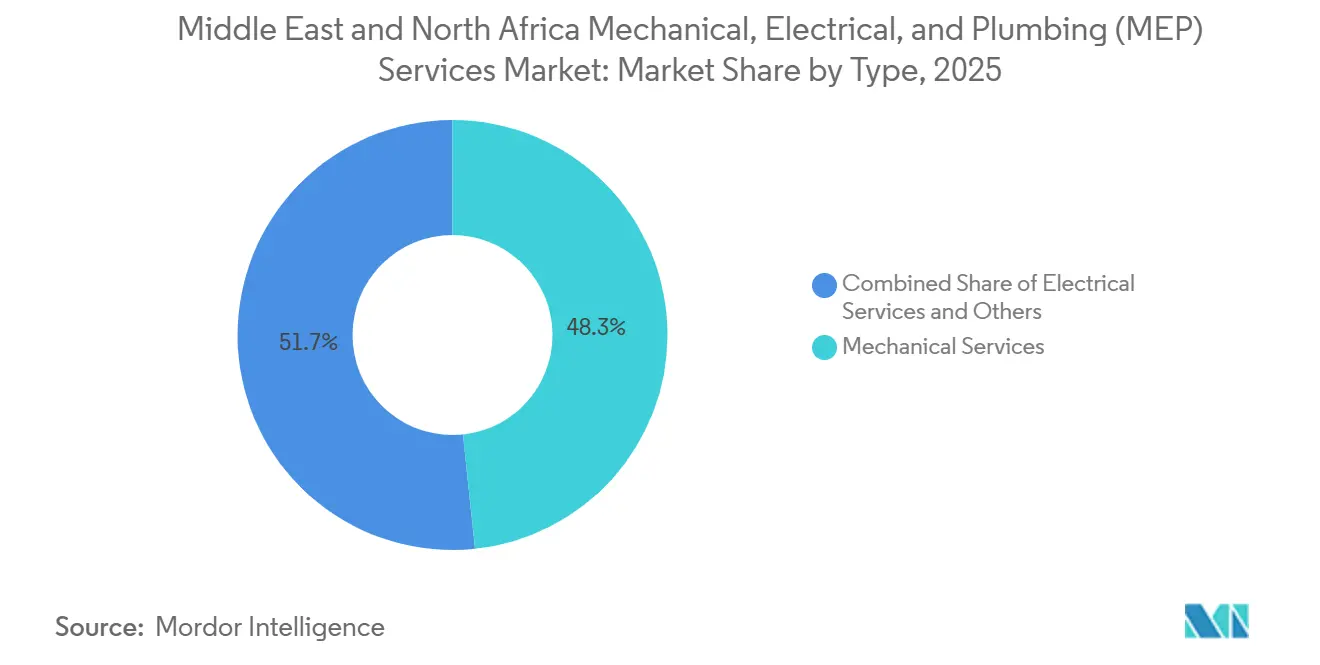

- By type, mechanical services held 48.3% share in 2025, while integrated MEP services is projected to record the fastest growth at a 12.1% CAGR through 2031.

- By service type, design and engineering held 36.3% share in 2025, while other services is forecast to expand at an 11% CAGR through 2031.

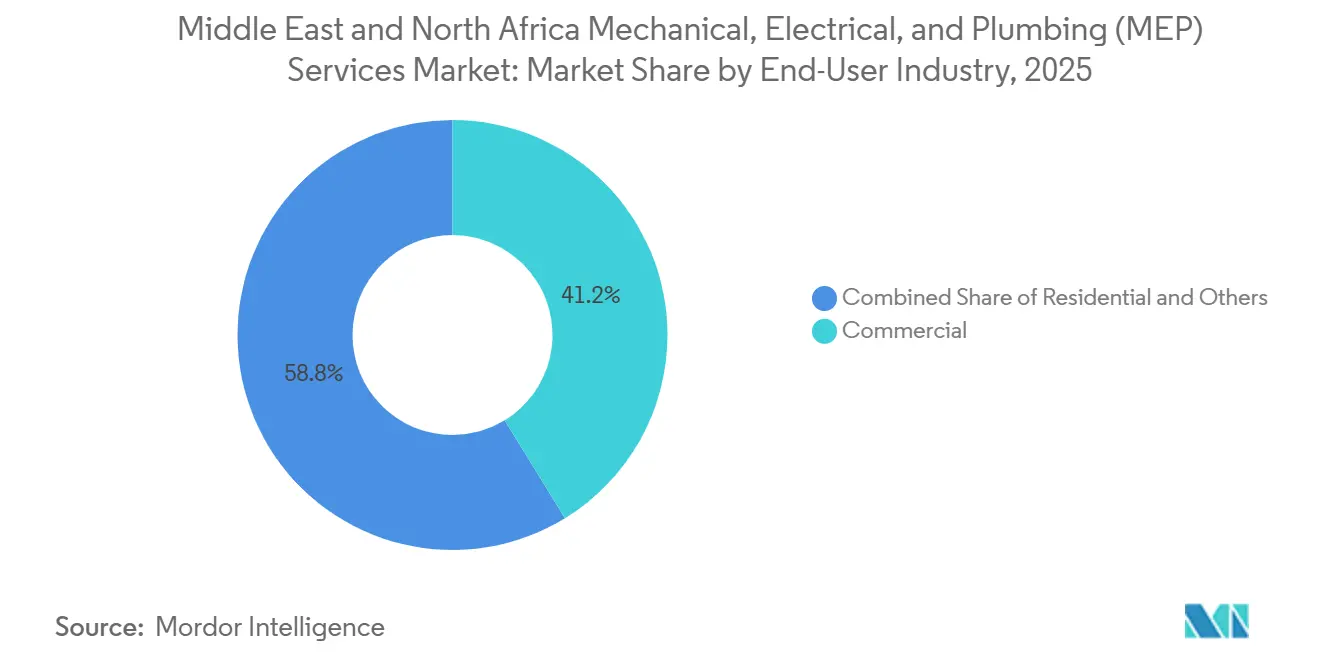

- By end-user industry, commercial held 41.2% share in 2025, while infrastructure is projected to grow at a 12.7% CAGR through 2031.

- By geography, Saudi Arabia accounted for 48.4% share in 2025, while Qatar within rest of MENA is forecast to expand at an 11.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saudi Giga-Projects and UAE Mixed-Use Expansion | +2.5% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Data-Center, District-Cooling, and Mission-Critical Demand | +2.0% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Energy-Efficiency Retrofits in Cooling-Intensive Buildings | +1.5% | Global, with concentrated gains in UAE, KSA, Egypt | Medium term (2-4 years) |

| BIM-Led Design Coordination and Modular MEP Uptake | +0.8% | UAE, KSA, regional spill-over | Medium term (2-4 years) |

| Airport, Tourism, and New-City Build-Outs in North Africa | +0.7% | Morocco, Egypt, Turkey | Medium term (2-4 years) |

| Water Reuse, Desalination Linkage, and High-Efficiency Plumbing Needs | +0.6% | Saudi Arabia, UAE, Egypt, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Saudi Giga-Projects and UAE Mixed-Use Expansion

Saudi giga-project activity remains the largest demand engine in the MENA MEP services market, even as project owners apply tighter sequencing and feasibility checks across very large programs. Expo 2030 Riyadh and the 2034 FIFA World Cup keep near-term packages tied to visible delivery milestones, which makes the active pipeline more execution-led than headline-led. In the UAE, mixed-use and destination projects keep the MENA MEP services market broad across commercial, leisure, hospitality, and residential formats, which reduces dependence on a single project class. Saudi clients are also applying in-country value requirements more actively, and that is shifting competition toward contractors with local manufacturing, training capacity, and delivery depth inside the Kingdom. Scale still matters in this part of the market, but execution credibility now matters more than announced project value.

Data-Center, District-Cooling, and Mission-Critical Demand

Data-center, district-cooling, and other mission-critical projects are changing the mix of work in the MENA MEP services market because they require deeper system integration from the first design stage. Higher rack densities are pushing designers toward more complex power redundancy, liquid-cooling strategies, and backup systems than conventional commercial buildings usually require. This shifts value toward engineers and contractors that can coordinate mechanical and electrical scopes early, rather than rely on late installation fixes after procurement decisions are already locked in. District-cooling plants and network pipework also keep the MENA MEP services market tied to master-planned urban developments where large mechanical packages move in parallel with utilities and public infrastructure. These demand streams are less exposed to short-term real estate sentiment because they are linked to digital infrastructure, utility planning, and urban service platforms.

Energy-Efficiency Retrofits in Cooling-Intensive Buildings

Energy-efficiency retrofit work is becoming a durable source of demand in the MENA MEP services market, as cooling remains one of the largest loads in Gulf buildings. In some GCC markets, cooling can account for up to 70% of peak electricity demand, which keeps retrofit payback commercially relevant for public and private asset owners[1]Global Carbon Council, “New GCC Methodology Boosts Energy Efficiency in Centralized Cooling Systems,” Global Carbon Council, globalcarboncouncil.com. Government and institutional assets in the UAE are already moving through broader retrofit programs, expanding the MENA MEP services market beyond new construction and first-fit installation work. Contractors that win retrofit scopes often stay on through maintenance cycles, which turns one capital award into a longer service relationship with recurring revenue potential. The planned CIBSE MENA Retrofit Conference in Dubai in November 2026 shows that retrofit delivery is now treated as a core engineering theme in the region, rather than a niche activity.

BIM-Led Design Coordination and Modular MEP Uptake

BIM-led design coordination and modular MEP delivery are becoming normal practice in the MENA MEP services market, especially on larger and more schedule-sensitive projects. This reduces rework, shortens site exposure, and helps contractors control labor productivity at a time when skilled staffing is still tight across several GCC markets. Modular fabrication is especially useful on ducting, pipework, and repetitive plantroom assemblies, where off-site work can improve schedule reliability and installation consistency. Clients are also using digital information requirements more consistently, which means BIM capability is increasingly a threshold issue in high-value tenders rather than a differentiator that only a few firms need to show. As a result, companies with proven prefabrication and coordination processes are winning work on quality and delivery certainty, not only on price.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor and Engineering Talent Shortages | -1.2% | GCC-wide, particularly KSA and UAE | Long term (≥ 4 years) |

| Material Lead Times and Aggressive Price Competition | -0.8% | Global supply chain effect, concentrated in UAE and KSA | Short term (≤ 2 years) to Medium term (2-4 years) |

| Payment-Certification Delays and Claims-Management Risk | -0.5% | KSA, UAE | Short term (≤ 2 years) to Medium term (2-4 years) |

| Geopolitical and Security Volatility in Select Markets | -0.4% | MENA-wide, concentrated in conflict-adjacent zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor and Engineering Talent Shortages

Skilled labor and engineering shortages remain a structural limit on the MENA MEP services market because project volume is rising faster than the supply of trained people who can manage and install complex systems. The regional pipeline needs more supervisors, project managers, commissioning specialists, and certified installers, but that workforce takes time to build and is not easily replaced once project schedules compress. When MEP subcontractors cannot staff work fronts on time, main contractors absorb schedule slippage and wider claims exposure across the full project chain. Skill inconsistency is also a quality issue because some markets still lack fully standardized installer qualification requirements across HVAC and related trades. Companies that invest in internal training centers and repeatable site processes are better protected, but the workforce gap remains material across the MENA MEP services market.

Material Lead Times and Aggressive Price Competition

Extended material lead times and aggressive price competition continue to pressure execution across the MENA MEP services market. Long procurement cycles for generators, switchgear, and other electrical packages can force contractors to commit working capital far ahead of installation, which weakens cash discipline on fixed-price jobs. That risk becomes harder to manage when imported equipment prices and metal inputs move against the contractor during the delivery window. Price-led bidding on large residential and mixed-use projects also reduces the advantage of firms that invest heavily in prefabrication, engineering depth, and digital delivery because clients do not always price those benefits correctly at tender stage. Early procurement, bulk purchasing, and shared risk mechanisms are helping on larger programs, but these practices are not yet standard across the MENA MEP services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mechanical Services Lead, Integrated MEP Accelerates

Mechanical Services held 48.3% of the MENA MEP services market share in 2025, which made it the largest type segment by a wide margin. The region's sustained cooling load keeps HVAC-related work essential across commercial buildings, residential compounds, hotels, transport assets, and public facilities, which supports large mechanical packages through both new build and retrofit cycles. Electrical Services remained the second-largest segment because data centers, smart-building systems, backup power architecture, and low-voltage networks are expanding overall system complexity in new projects. Plumbing Services stayed steady, with demand supported by desalination-linked networks, water-efficiency mandates, and wider adoption of treated-water reuse in built assets.

Integrated MEP Services is projected to grow at a 12.1% CAGR from 2026 to 2031, the fastest pace among type segments in the MENA MEP services industry. Master developers increasingly prefer single-contract accountability across mechanical, electrical, and plumbing scopes on mixed-use, hospitality, infrastructure, and giga-project programs, because coordination failures on one system can delay several others at handover. Providers with specialist teams across mission-critical systems, intelligent low-voltage work, and fast-track delivery are well positioned to benefit from this shift, particularly where project owners want fewer interfaces and tighter schedule control. Integrated delivery also aligns with stricter energy-performance expectations because cross-system modeling, testing, and commissioning are easier to manage under one lead contractor.

By Service Type: Design and Engineering Anchors Revenue, Other Services Accelerate

Design and Engineering accounted for 36.3% of the MENA MEP services market size in 2025, which reflected how much of the regional pipeline remained in front-end planning, coordination, and specification work. Large consultancies continue to compete for early-stage mandates because design control can influence equipment selection, procurement timing, sequencing logic, and lifecycle performance throughout construction. Installation, Testing, and Commissioning remained the second-largest service type and remained the most labor-intensive part of project delivery because it sits closest to site conditions, interface risks, and final handover deadlines. Mission-critical facilities are making commissioning more specialized because integrated systems testing is becoming a much bigger requirement for digital infrastructure and high-performance buildings.

Other Services is forecast to expand at an 11% CAGR from 2026 to 2031, making it the fastest-growing service type in the MENA MEP services industry. Asset owners are moving away from basic labor-only maintenance agreements and toward contracts tied to uptime, response speed, monitored performance, and clearer service-level expectations. Predictive monitoring and building analytics are becoming increasingly relevant as electricity costs rise and facility owners seek fewer unplanned failures, greater operational visibility, and more defensible maintenance spending. Maintenance and Repair also benefits from the growing stock of buildings that are entering their first major upkeep cycle in Abu Dhabi, Riyadh, Dubai, and other established commercial districts.

By End-User Industry: Commercial Dominates, Infrastructure Expands Fastest

Commercial end users represented 41.2% of the MENA MEP services market in 2025, which kept offices, hospitality assets, malls, and mixed-use developments at the center of spending. These projects usually carry high MEP values per square meter because they require complex cooling systems, dense electrical layouts, advanced low-voltage fit-outs, and tighter indoor environmental performance than standard buildings. Residential remained the second-largest end-use group, supported by large housing programs in Saudi Arabia, major villa developments in Dubai, and the New Administrative Capital in Egypt. Johnson Controls Arabia secured a USD 90 million share of the VRF package for the R5 zone in Egypt's New Administrative Capital, covering more than 11,000 YORK units across 138 buildings and 22,000 apartments[2]Johnson Controls Arabia, “Johnson Controls Arabia Secures $90 Million Share in Record-Breaking $180 Million VRF Project in Egypt's New Administrative Capital,” Johnson Controls Arabia, jcarabia.com.

Infrastructure is projected to grow at a 12.7% CAGR from 2026 to 2031, which makes it the fastest-growing end-use segment in the MENA MEP services industry. Airport expansions, water and wastewater plants, data center campuses, and urban mobility programs are expanding the opportunity set beyond pure real estate and giving contractors exposure to more utility-linked work. This segment also benefits from public planning cycles that tend to remain active even as private development sentiment softens, helping diversify future order books. Compliance demands are higher in infrastructure, so contractors with stronger documentation, testing, commissioning, and regulatory management capability can defend better margins than firms that compete only on installation cost.

Geography Analysis

Saudi Arabia held 48.4% of the MENA MEP services market size in 2025, so the regional outlook remains heavily tied to execution in the Kingdom. NEOM, Diriyah Gate, Red Sea Global, Qiddiya, New Murabba, and Jeddah Central keep Saudi Arabia at the center of the project pipeline because they combine large building services demand with long multi-package delivery schedules. Funding has become more selective, but event-linked projects tied to Expo 2030 Riyadh and the 2034 FIFA World Cup are still anchoring near-term delivery and keeping active works distinct from purely announced pipelines. This keeps the MENA MEP services market concentrated in one geography even though demand drivers span commercial buildings, hospitality, utilities, transport, and new cities. The UAE is smaller in share, but its pipeline is more diversified across private real estate, public retrofit programs, hospitality, and digital infrastructure, which gives it a more balanced demand base.

Egypt and Morocco are the main North African demand centers, and both are being shaped by long-duration public building and transport programs that generate repeat MEP scopes over several years. In Egypt, the New Administrative Capital is creating demand across housing, government buildings, and utility-linked systems, with the R5 zone already demonstrating the scale of cooling packages now being awarded in the country. Morocco is seeing airport-led demand that supports terminal HVAC, power, lighting, water, and safety packages across a wider modernization cycle that extends beyond a single airport site. Turkey adds a different pattern of demand because rebuilding work and public-private projects support steady need for hospital-grade HVAC, controls, and building management systems.

Qatar is the fastest-growing geography in the report, with an 11.4% CAGR from 2026 to 2031 within Rest of MENA. Lusail smart-city integration, sustainability retrofit mandates, and green-retrofit contracts through 2027 are creating demand for specialist, higher-value scopes rather than commodity installation work, which changes the quality of opportunity in that market. Iraq, Libya, and Jordan also present real reconstruction demand, but payment risk and security conditions limit how much of that pipeline is actionable for international contractors with stricter risk filters. The result is a geographically broader MENA MEP services market than the headline Saudi share suggests, but one where risk-adjusted opportunity still varies sharply by country and by project sponsor.

Competitive Landscape

The MENA MEP services market is moderately fragmented, with regional contractors and global engineering consultancies occupying different parts of the value chain rather than competing on identical mandates. BK Gulf, ALEMCO, Khansaheb MEP, and Al-Futtaim Engineering & Technologies are among the leading regional contractors, while AECOM, AtkinsRéalis, WSP Global, Jacobs, Cundall, and Buro Happold remain prominent on design and project-management mandates. Regional firms tend to compete on prefabrication, delivery speed, execution depth, and local labor management, while global consultancies compete on engineering coordination, digital tools, and influence over specification. This creates a competitive map where design authority and installation capacity are often held by different groups on the same project, which keeps partnership models common across large programs.

Strategic moves increasingly center on digital delivery, localization, and mission-critical capability because these are the areas where contractors can widen margins and strengthen repeat business. Al-Futtaim Technologies partnered with Johnson Controls in June 2025 to launch the OpenBlue smart building platform in the UAE, targeting intelligent infrastructure and energy-efficient operations across real estate, education, finance, and government clients[3]Al-Futtaim, “Al-Futtaim Technologies and Johnson Controls Partner to Launch OpenBlue Smart Building Platform in the UAE,” Al-Futtaim, alfuttaim.com. Johnson Controls Arabia also expanded its project footprint through its USD 90 million share in Egypt's R5 VRF package, which reinforced its position in large-scale cooling systems and complex residential delivery. Drake & Scull International signaled its operating recovery in February 2025 when it secured two Arabian Hills contracts exceeding AED 1 billion in aggregate for infrastructure, power, and sewage treatment scopes. Companies that can pair these moves with stronger balance sheets, internal training, and in-house fabrication are better placed to win repeat mandates on complex programs where schedule certainty matters as much as bid price.

White space remains in performance-based facility management, where predictive maintenance and energy-outcome contracts are still less developed than in more mature regions, even though asset owners are showing stronger interest in measurable lifecycle performance. ESCO-accredited operators are well placed because clients are paying closer attention to verified savings, uptime, and lifecycle accountability rather than only to first-year service cost. Estidama Pearl Rating, LEED in the UAE, and Mostadam in Saudi Arabia are shaping specification decisions and contractor selection across both new build and retrofit work. Overall, competition is active and technically demanding, but no single contractor group is close to controlling the MENA MEP services market.

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Industry Leaders

BK Gulf

ALEMCO

Al-Futtaim Engineering & Technologies

Khansaheb MEP

Adeeb Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Drake & Scull International secured two contracts exceeding AED 1 billion in aggregate for the Arabian Hills project in Dubai, covering infrastructure, power, and sewage treatment for Area 05 (Park Vista) and Area 10 (Sun Valley) across 224 million square feet, signalling the company's full operational return after its 2024 financial restructuring.

- February 2025: Johnson Controls Arabia secured a USD 90 million share of a USD 180 million VRF project in Egypt's New Administrative Capital R5 zone, supplying over 11,000 YORK VRF units with a combined cooling capacity of 140,000 tons across 138 buildings serving 22,000 apartments.

- June 2025: Al-Futtaim Technologies partnered with Johnson Controls to launch the OpenBlue smart building platform in the UAE, targeting intelligent infrastructure and energy-efficient operations for real estate, education, finance, and government clients.

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Report Scope

The MENA MEP Services Report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP Services), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair, Other), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Saudi Arabia, UAE, Egypt, Turkey, Morocco, Rest of MENA). The Market Forecasts are Provided in Terms of Value (USD).

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance & Repair |

| Other Services |

| Residential |

| Commercial |

| Infrastructure |

| Saudi Arabia |

| United Arab Emirates |

| Egypt |

| Turkey |

| Morocco |

| Rest of Middle East and North Africa |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance & Repair | |

| Other Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| Morocco | |

| Rest of Middle East and North Africa |

Key Questions Answered in the Report

What is the growth outlook for MENA MEP services through 2031?

The MENA MEP services market is projected to rise from USD 6.03 billion in 2026 to USD 9.48 billion by 2031, at a 9.5% CAGR over 2026 to 2031.

Which country contributes the most to regional demand?

Saudi Arabia led the region with 48.4% share in 2025, supported by giga-projects, tourism assets, and event-linked infrastructure tied to Expo 2030 Riyadh and the 2034 FIFA World Cup.

Which service category is growing the fastest?

By type, Integrated MEP Services is the fastest-growing segment at a 12.1% CAGR, as developers increasingly want single-point accountability across building systems.

Which end-user group creates the largest volume of work?

Commercial end users held 41.2% share in 2025, driven by office towers, hospitality assets, and mixed-use developments with high cooling and electrical complexity.

Page last updated on: