Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

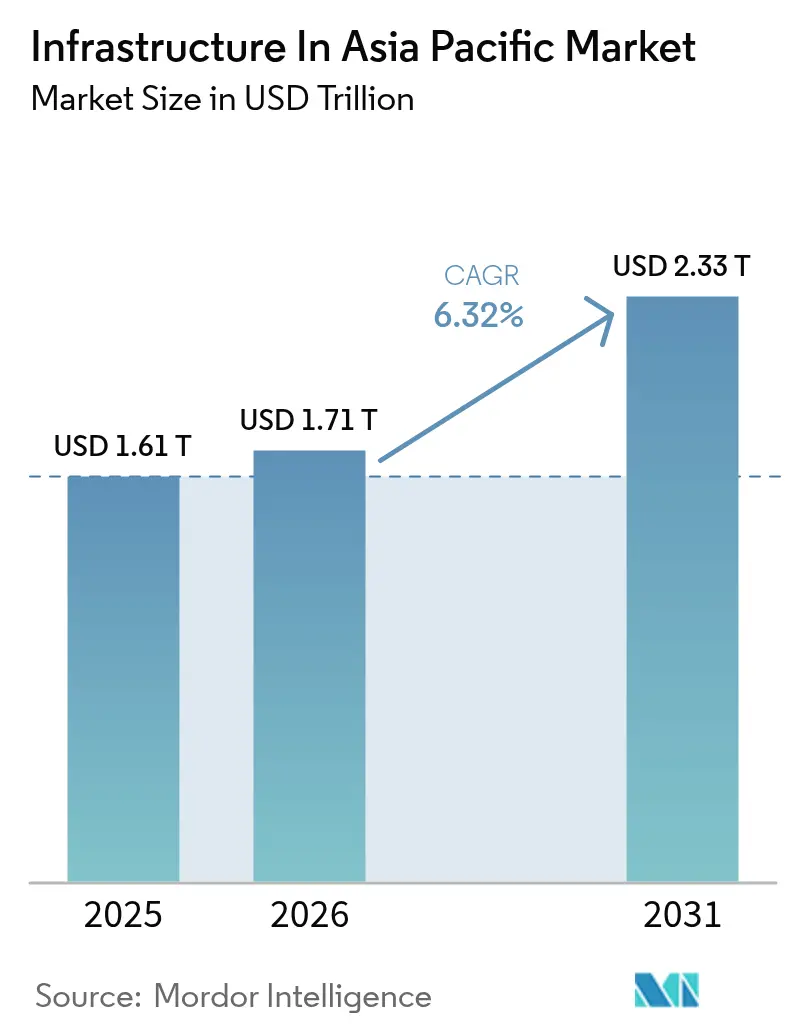

| Base Year Market Size (2025) | USD 1.61 Trillion |

| Market Size (2026) | USD 1.71 Trillion |

| Market Size (2031) | USD 2.33 Trillion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infrastructure In Asia Pacific Market Analysis by Mordor Intelligence

APAC infrastructure market size in 2026 is estimated at USD 1.71 trillion, growing from 2025 value of USD 1.61 trillion with 2031 projections showing USD 2.33 trillion, growing at 6.3% CAGR over 2026-2031. Momentum comes from governments pivoting toward economic resilience, large-scale transport corridors that link regional supply chains, and a surge in data-center builds geared toward artificial-intelligence workloads. China’s USD 167 billion hydropower project in Tibet, India’s USD 134 billion federal allocation for 2025-26, and Japan’s public backing for semiconductor hubs illustrate unprecedented state outlays that continue to anchor the APAC infrastructure market. Private investors are stepping in to bridge financing gaps through public-private partnerships that blend sovereign guarantees with performance-linked returns, while the push for climate-resilient assets is shifting a slice of capital toward green utilities and cross-border renewable grids. Supply-chain diversification away from single-country dependency further accelerates inland ports, freight rail upgrades, and port automation across emerging ASEAN economies. Finally, digital infrastructure, 5G corridors, fiber backbones, and edge data centers have become integral rather than optional, opening new revenue streams across the construction and operation phases.

Key Report Takeaways

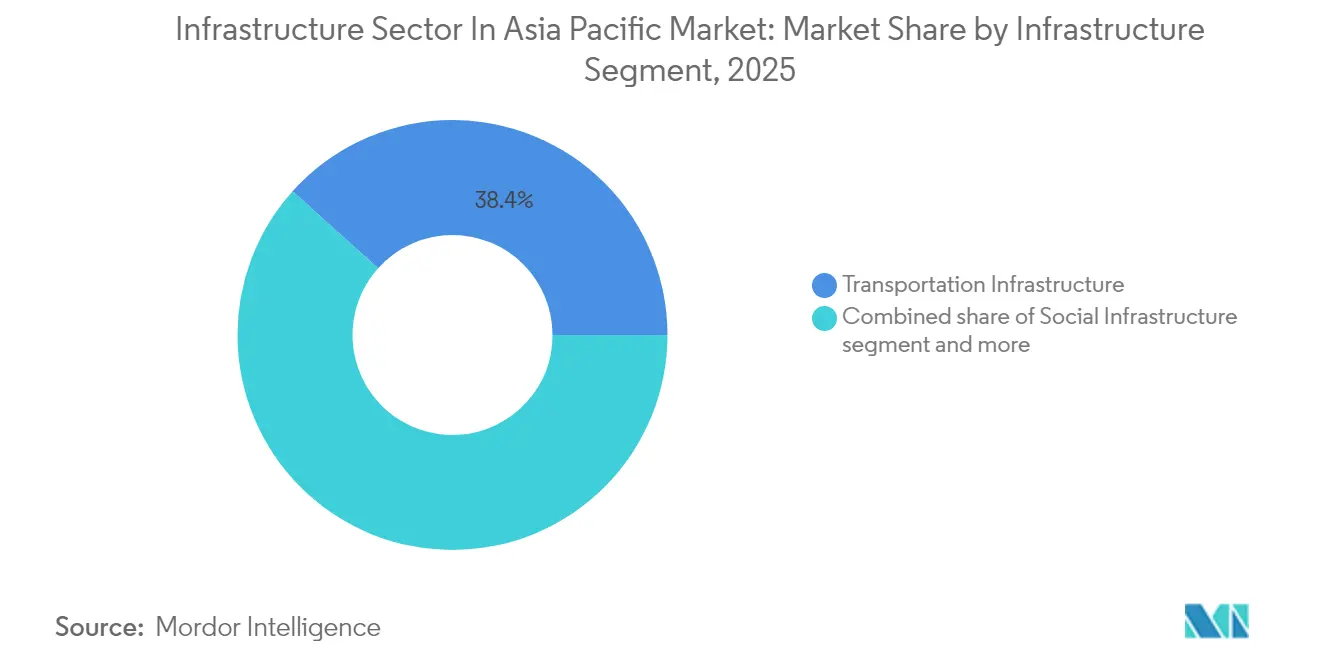

- By infrastructure segment, transportation led with 38.35% of APAC infrastructure market share in 2025 and is expanding at an 8.15% CAGR through 2031.

- By construction type, new builds accounted for 71.86% share of the APAC infrastructure market size in 2025, whereas renovation is advancing at an 7.78% CAGR during the outlook period.

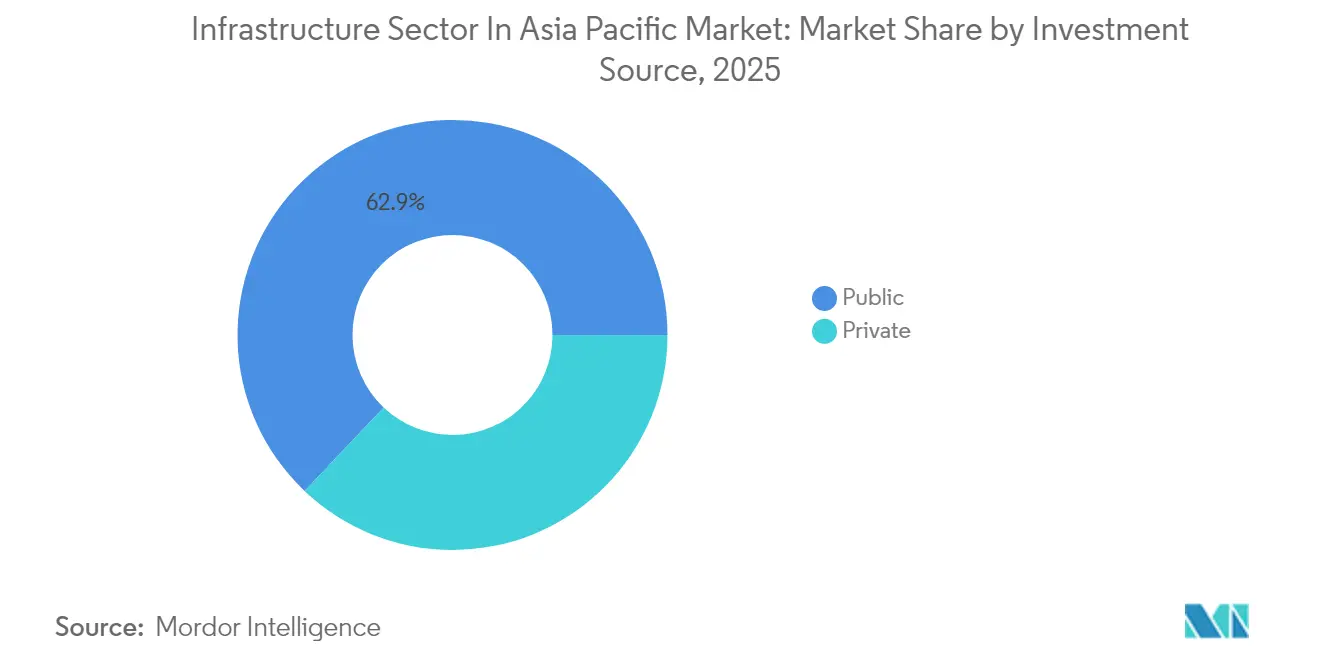

- By investment source, public capital commanded 62.92% of 2025 spending, while private financing is forecast to register the fastest 8.55% CAGR to 2031.

- By geography, China dominated with a 50.12% share of the APAC infrastructure market size in 2025; India records the highest 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Infrastructure In Asia Pacific Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government infrastructure spending | 2.1% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Accelerating urbanization & middle-class demand | 1.8% | India, ASEAN core countries | Long term (≥ 4 years) |

| 5G, data-center & fiber roll-outs | 1.4% | Global, with concentration in Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Green & sovereign-wealth capital pivot to APAC | 0.9% | ASEAN, Australia, with spillover to India | Medium term (2-4 years) |

| Supply-chain diversification into ASEAN | 0.7% | ASEAN core, spillover to India | Medium term (2-4 years) |

| Climate-resilience upgrade mandates | 0.5% | Global, early gains in Australia, Singapore, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Infrastructure Spending

Public budgets across the region continue to hit record levels. China has earmarked over USD 551 billion for “hidden” urban utilities and smart-city upgrades while concurrently adding 3,800 kilometers of high-speed rail by year-end. Japan is underwriting semiconductor “chip cities” with USD 27 billion in direct support that catalyzes USD 120 billion in downstream economic benefits. South Korea’s parliament approved USD 471 billion for a Gyeonggi semiconductor cluster and complementary road and rail links. These policies both stimulate near-term growth and strengthen technological sovereignty. Together, they raise baseline demand for construction services, machinery, and advanced project management tools across the APAC infrastructure market[1]Li Guanghua, “China to Spend 4 Trillion Yuan on Urban Hidden Infrastructure,” State Council Information Office, scio.gov.cn.

Accelerating Urbanization & Middle-Class Demand

Rapid urban migration is swelling consumption and stretching city limits. Southeast Asia’s GDP reached USD 3.6 trillion in 2022, and household spending is projected to cross USD 4 trillion by 2031, intensifying demand for mass transit and smart-utility grids. Programs such as Indonesia’s “Movement Toward 100 Smart Cities” layer digital sensors, open-data platforms, and climate-resilient drainage into every new township. Vietnam’s USD 67 billion north-to-south high-speed railway will cut travel times to six hours for 80% of urban residents, illustrating how quality-of-life upgrades translate into large transportation outlays. Urban green retrofits like Singapore’s Bishan-Ang Mo Kio Park show that nature-based drainage can raise biodiversity by 30% and still save 15% over concrete alternatives. These examples clarify why recurring city budgets and private mortgages will keep funneling capital into the APAC infrastructure market long after mega-projects finish.

5G, Data-Center & Fiber Roll-outs

Telecom infrastructure is evolving from consumer bandwidth plays to industrial productivity enablers. Thailand’s 5G factories report 15-20% efficiency gains, and Indonesian 5G warehouses see 25% faster pick-and-pack cycles. Regional data-center capacity hit 12,206 MW in 2024, with another 14,338 MW under development, fed by AI compute clusters and multi-cloud adoption. Amazon Web Services alone committed USD 15.4 billion (2.26 trillion JPY) to Japan by 2027, while CapitaLand is building a USD 700 million facility in Osaka. Second-tier cities now outbid capitals for server farms due to cost and power-grid headroom. Across the APAC infrastructure market, fiber densification underpins these deployments, anchoring private-equity interest in duct banks and tower portfolios.

Green & Sovereign-Wealth Capital Pivot to APAC

Sustainability mandates are converting boardroom pledges into shovel-ready projects. Australia approved a USD 19 billion solar farm that will export electricity to Singapore along a 4,300-kilometer undersea cable, redefining the scale of cross-border renewables. Japan’s Green Transformation Plan channels nearly EUR 1 trillion into decarbonization by 2035, funded by EUR 131.5 billion in transition bonds. Singapore’s Keppel forged a USD 1.5 billion alliance with the Asian Infrastructure Investment Bank for resilient assets across emerging markets. Meanwhile, ASEAN’s Power Grid Financing Facility backs multi-country transmission lines that could serve 670 million citizens. These flows widen the investor base for the APAC infrastructure market and add depth to secondary-market refinancing[2]John Martin, “ASEAN Power Grid Financing Facility Launch,” Asian Development Bank Institute Working Paper, adb.org.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-acquisition & permitting delays | -1.2% | India, Indonesia, Philippines | Medium term (2-4 years) |

| Public-debt & budget constraints | -0.8% | Global, acute in smaller ASEAN economies | Short term (≤ 2 years) |

| Skilled-labor shortfalls in megaprojects | -0.6% | Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Heightened geopolitical risk premiums | -0.4% | China-dependent supply chains, cross-border projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land-Acquisition & Permitting Delays

Regulatory bottlenecks extend timelines and inflate costs. Japan’s Hokuriku Shinkansen extension now exceeds USD 36 billion, more than double the original outlay, after protracted community negotiations. Southeast Asia’s USD 100 billion super-grid faces multiple sovereignty approvals before any cable is laid. Even renewables hit hurdles: Australian solar and wind farms must clear heritage surveys, flora scans, and marine assessments despite federal fast-track lists. Local land-rights consultations add two to three years to project schedules in Indonesia and the Philippines. These frictions shave growth from the APAC infrastructure market unless digital permitting portals and standardized right-of-way frameworks scale rapidly.

Skilled-Labor Shortfalls in Megaprojects

Demographics and safety laws squeeze construction headcounts. Japan’s workforce shrank 20% in a decade; 36% of remaining workers are 55 or older, jeopardizing Expo 2025 deadlines. New overtime caps compound what the industry calls the “2024 problem,” as night-shift premiums no longer attract retirees back to sites. South Korea’s semiconductor cluster must train thousands of electricians and fit-out technicians within two years to keep fab equipment schedules. Contractors now deploy robotic rebar tiers, drone surveys, and modular building systems to reduce man-hours. If labor productivity lags, it could subtract meaningful points from the APAC infrastructure market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure Segment: Transportation Extends Lead Through Smart Mobility

Transportation captured 38.35% of 2025 spending and posts the fastest 8.15% CAGR, giving it a commanding position within the APAC infrastructure market. China’s network already spans 80% of the planned 50,000-kilometer high-speed grid and will add 3,800 kilometers this year. Vietnam’s USD 67 billion line targets a six-hour Hanoi-Ho Chi Minh trip time, while Thailand’s Eastern Economic Corridor channels USD 18.3 billion into airport-to-port rail loops. Smart-ticketing, predictive maintenance, and 5G-enabled driverless metros elevate operating margins and rider experience. Utilities follow as governments chase secure water and energy. China funded 1,488 water-conservancy projects in 2023, lifting spending by 41.7% for that vertical. Social infrastructure sees steady gains as aging demographics require hospitals and elder-care campuses; India’s new AIIMS campus spans 1.5 million ft² and serves as a prototype for tech-enabled healthcare. Extraction assets receive targeted boosts from low-carbon retrofits, such as Indonesia’s USD 7 billion CCUS at Tangguh that will bury 15 million tons of CO₂. Transportation’s dominance thus mirrors both connectivity imperatives and the smart-mobility premium embedded in the APAC infrastructure market.

Segment growth also benefits from financing innovations. Asset-recycling funds in Australia package mature toll roads into listed vehicles, freeing capital for inland freight routes. Digital-twin platforms help optimize rail and port layouts before ground breaks, cutting change orders by 30%. Collectively, these advances reinforce transportation’s outsized role in the APAC infrastructure market while opening niches for specialized contractors and software suppliers.

By Construction Type: Renovation Surges on Aging Stock

New builds retained 71.86% share in 2025 as governments green-light mega dams, chip fabs, and greenfield ports that align with industrial-policy goals. However, renovation grows at 7.78% CAGR because asset lifecycles in mature economies have crossed the 30-year threshold, triggering mandatory retrofits. Japan’s Green Transformation Plan dedicates nearly EUR 1 trillion to overhaul legacy bridges, tunnels, and district heating grids for carbon neutrality. China’s USD 551 billion “hidden infrastructure” campaign modernizes sewers, cable ducts, and smart-grid nodes beneath existing streets. Renovation projects attract specialized capital that values steady cash flows from concession renewals. Digital sensors and AI diagnostics now extend asset life by predicting fatigue cracks well before failure. Singapore’s Bishan-Ang Mo Kio Park proves nature-based riverbanks can replace concrete linings, saving 15% and lifting biodiversity by 30%. These examples signal why the renovation wave is reshaping procurement criteria, contractor skills, and risk models across the APAC infrastructure market.

By Investment Source: Private Capital Gains Momentum

Public treasuries still supplied 62.92% of 2025 outlays, anchored by China’s USD 554 billion local-government bond issuances and India’s USD 134 billion federal package. Yet private capital records a 8.55% CAGR as pension funds, sovereign wealth vehicles, and buy-out firms diversify into contracted-revenue assets. DigitalBridge’s USD 470 million purchase of JTOWER and CK Hutchison’s USD 22.8 billion port divestiture to a BlackRock-TiL consortium illustrate scale and appetite. Risk-sharing PPP structures now bundle availability payments with carbon-abatement bonuses to satisfy both fiduciary and ESG mandates. CapitaLand’s USD 700 million Osaka data center reaches financial close under a build-to-core schedule that enables recycling within five years. Indonesia’s Trans-Java Toll Road financing pulled USD 2.75 billion from Dutch and Gulf institutions on the back of traffic guarantees. These examples reinforce how private funding complements sovereign budgets to keep the APAC infrastructure market growth curve intact.

Geography Analysis

China held 50.12% of 2025 expenditure and retains structural advantages through scaled state-owned enterprises that secure domestic and foreign contracts. Fixed-asset investment hit 51.4 trillion yuan (USD 7.9 trillion) in 2024, with 5.6% growth in core infrastructure lines and 39.1% in water-management spending. The USD 167 billion Tibet hydropower project alone eclipses many national budgets and anchors supply chains from cement to advanced turbines. Belt and Road rail links such as the China-Laos route cut freight costs by 30% and consolidate regional influence.

India stands out as the fastest riser with an 7.74% CAGR, underpinned by unprecedented highways, power-grid corridors, and port-led industrial parks. The federal USD 134 billion 2025-26 allocation elevates infrastructure to 3.4% of GDP, while state governments add complementary metro and irrigation schemes. Technology-enabled contractors such as Sterlite Power now prefab transmission towers off-site, reducing right-of-way hours by 38%.

Japan and South Korea concentrate on high-tech, climate-safe assets. Japan’s USD 27 billion semiconductor incentives mesh with AWS’s USD 15.4 billion cloud cluster, bringing advanced logistics and district cooling to secondary prefectures. South Korea’s USD 471 billion semiconductor mega-site seeds housing, subways, and hydrogen fueling, integrating land-use with industrial policy. Across ASEAN, USD 206 billion in 2023 FDI funds inland ports, airport expansions, and resilience projects that address flood and power-grid vulnerabilities. The tiered growth landscape thus widens opportunity sets within the APAC infrastructure market.

Regulatory Landscape

Regulatory frameworks across Asia-Pacific infrastructure are tightening around digital permitting, standardized construction methods, and performance-based codes, with public-works procurement using compliance gates to manage delivery risk. In Singapore, the Building Control (Amendment) Regulations 2026 introduce new compliance provisions effective 1 April 2026, alongside the Building and Construction Authority (BCA) move toward standardization via Buildability Type Approval for Kit-of-Parts projects (effective 30 April 2026). Singapore is also phasing in mandatory digital submissions through CORENET X, with requirements already mandatory for new projects of at least 30,000 m2 GFA since 1 October 2025 and expanding to all new projects regardless of size from 1 October 2026.

Other markets are making accredited supply chains a tender prerequisite, reinforcing greater industrialization in construction. Hong Kong’s Development Bureau (DevB) Technical Circular (Works) No. 4/2026 mandates the use of a new List of Approved Modular Integrated Construction (MiC) Suppliers for public works tenders invited on or after 1 April 2026, shaping contractor sourcing and prequalification strategies. In parallel, Australia applies the National Construction Code (NCC) 2025 maintained by the Australian Building Codes Board (ABCB), while Malaysia’s standards governance is anchored by CIDB and the Department of Standards Malaysia through construction industry standards (CIS) committees, creating a compliance environment that increasingly favors repeatable designs, auditable documentation, and lifecycle reporting discipline.

Value Chain Analysis

The APAC infrastructure value chain spans project origination and financing (public budgets, PPPs, private credit), planning and approvals, design and engineering (including BIM and digital twins), procurement of long-lead materials and equipment (cement, steel, aggregates, MEP systems, grid components), construction and commissioning, and then operations and asset management under concession or availability-payment models. Delivery ecosystems are increasingly organized around integrated consortia that bundle EPC capability with capital and concession operations, which fits the region’s mix of transport corridors, renewable grids, and data-center builds.

Supply-side constraints cluster around labor availability and long-lead electrical and transmission equipment, with industry efforts shifting toward resilience and regionalization rather than lowest-cost sourcing alone. Long-lead procurement has become a gating factor for grid expansion, with transmission sector timelines stretching to 4 to 6 years for voltage source converters and 6 to 8 years for HVDC subsea cables, encouraging earlier procurement lock-in and tighter OEM engagement. Capacity and logistics upgrades also feed upstream and midstream flows: China’s Pinglu Canal project in Guangxi (USD 13.7 billion), scheduled to open in September 2026, is positioned to shorten shipping distances to Singapore by about 740 km, which can alter material movement economics for southern China-ASEAN trade lanes. Initiatives such as the Green Grids Initiative, which includes Lucetia Group, Arup, and HSBC, further point to how coordination and standardization are being used to address bottlenecks for transmission-intensive programs and cross-border infrastructure delivery.

Competitive Landscape

Consolidation remains moderate. The top five Chinese state-owned enterprises, China State Construction, China Railway Group, PowerChina, China Communications Construction, and China Energy Engineering, collectively manage roughly 48% of regional backlogs, yet face more contestable bids overseas. Landmark wins include a USD 2.1 billion mixed-use contract in Saudi Arabia and the USD 3.8 billion Changi Terminal 5 package, both secured against global competitors. Indian conglomerate L&T shipped the world’s heaviest EO reactor at 2,306 tons, showcasing heavy-lift expertise that complements on-site construction.

Strategic alliances help bridge technology gaps: Infravision pairs drones with Sterlite Power to string conductors across valleys, while Keppel teams with AIIB to originate sustainable-project pipelines worth USD 1.5 billion. BIM, AI scheduling, and low-carbon concrete adoption are now pre-qualifiers on mega-RFPs. Data-center specialists such as CapitaLand and Korea Investment enter the field through hyperscale builds, nudging traditional builders to acquire MEP and commissioning talent. Political risk and export-credit backing continue to shape bidder pools, meaning the APAC infrastructure market remains contestable yet favors players with deep balance sheets and technology stacks.

Infrastructure In Asia Pacific Industry Leaders

China State Construction Engineering (CSCEC)

China Communications Construction Company (CCCC)

Power Construction Corporation of China (PowerChina)

Samsung C&T

Obayashi Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In APAC, opportunity is increasingly tied to bankable PPP pipelines, transport connectivity upgrades, and digitally governed delivery models that reduce schedule and claims risk in megaprojects. A noticeable whitespace is in projects that combine public-right-of-way control with private delivery and operations capability: in July 2026, Vietnam commenced construction of the 14.06 km Can Gio to Vung Tau sea bridge as a PPP with total investment of about VND 93.016 trillion, showing appetite for large-scale coastal connectivity structures and the associated demand for specialist marine works, foundations, and long-span design capability. In India, execution activity around strategic connectivity remains active, with the Zojila Tunnel (13.153 km) achieving final breakthrough in June 2026, supporting a wider program of all-weather road and tunnel assets where owners and contractors need geotechnical expertise, safety systems, and resilient O&M.

A second opportunity set relates to governance and data maturity requirements that are becoming procurement differentiators in major markets and among institutional investors funding essential assets such as renewables, digital infrastructure, and transport corridors. The shift toward AI-enabled spatial data and visual common data environments (CDE) in construction management creates openings for contractors and project managers that can deliver auditable lifecycle information, especially where sustainability reporting requirements are being integrated into project governance (including ISSB-aligned approaches and implementation pathways referenced by bodies such as the Australian Accounting Standards Board). These conditions are supporting demand for services and tools around digital permitting readiness, standardized component strategies (modular and kit-of-parts), commissioning documentation, and asset data handover, particularly in high-volume renovation and expansion programs where repeatability and compliance traceability affect bid eligibility and financing terms.

Recent Industry Developments

- May 2026: China State Construction Engineering Corporation (CSCEC) reported that a consortium led by the company secured the bid for the Laizhou to Qingdao Expressway (Qingdao section) franchise project in Shandong Province, with an estimated total investment of CNY 15.91 billion. The award reinforces the continued use of franchise and concession structures for large transport assets in China, supporting multi-year workloads that blend construction with long-duration operations responsibilities.

- July 2025: China started construction of the USD 167 billion Yarlung Tsangpo hydropower dam in Tibet, targeting annual generation of about 300 billion kWh and large-scale job creation. The project signals sustained state-led megaproject execution in utilities infrastructure and pulls through regional demand for heavy civil works, turbines, and high-voltage grid connections.

- May 2024: Australia advanced adoption of the National Construction Code (NCC) 2025 framework maintained by the Australian Building Codes Board (ABCB), setting the current baseline for technical design and construction provisions. Code updates shape specification choices and compliance workflows for contractors and designers, particularly for safety, energy performance, and documentation practices used in major public and private infrastructure programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia-Pacific infrastructure sector market is defined as the total value of infrastructure construction activity across key asset classes in the region, captured in current US dollars for the stated base year and forecast period.

Scope exclusions: We exclude routine building maintenance and small-scale repairs that do not qualify as infrastructure construction or major renovation activity.

Segmentation Overview

- By Infrastructure Segment

- Transportation Infrastructure

- Utilities Infrastructure

- Social Infrastructure

- Extraction Infrastructure

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Geography

- China

- India

- Japan

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as infrastructure and to build a consistent fact base for each major country market in Asia-Pacific. We relied on public sources such as national statistics offices and ministries of transport, energy, and public works, along with multilateral development bank publications, central bank macro series, and infrastructure pipeline documents.

To pressure-test the demand pool, we also reviewed company annual reports, investor presentations, association websites, and reputable press coverage of project awards and funding announcements. In addition, paid subscriptions were used selectively for company financials and project news tracking, and for patent and import-export visibility where it helped validate equipment-linked infrastructure spending signals. The sources mentioned here are illustrative and not exhaustive, and many other public documents and datasets were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with a mix of project owners, EPC and construction participants, materials and equipment suppliers, and financing or advisory stakeholders across Asia-Pacific. Our discussions focused on what is getting funded, how project pipelines are moving, and how pricing and timing assumptions should be adjusted when secondary indicators look out of sync.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 36% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up combination, where country-level infrastructure activity is first reconstructed from public investment plans, budget outlays, and macro indicators, which are then allocated across infrastructure categories based on observed project mix. To keep totals realistic, we corroborated the model with selective bottom-up approximations such as sampled project value rollups, supplier-side revenue exposure checks, and simple volume times ASP checks for a few large input categories.

Key inputs that were tracked (illustrative) included public infrastructure capex plans, PPP award activity, approvals and tender momentum, commodity and construction input cost movements, capacity additions in utilities and transport corridors, and renovation versus new build shares. Where a bottom-up approximation had gaps, the missing portion was handled through conservative allocation rules tied to the closest observable proxy, and then re-checked with interview feedback.

For forecasting, scenario analysis was used and anchored to country investment cycles, expected funding availability, and the timing of major pipeline projects, and then refined using expert views on schedule slippages and price escalation expectations. The final forecast path was accepted only after it stayed consistent with the direction of public budgets, major project pipelines, and construction cost inflation signals.

Data Validation & Update Cycle

Outputs were validated through multiple checks so large jumps were not accepted without a clear driver. We compared model results against independent signals such as announced project pipelines, budget execution trends, and construction input cost movement, and then reviewed any unusual variances at country and sub-sector level.

Before sign-off, the work was reviewed in steps by another analyst, and follow-up calls were triggered when key assumptions changed or when desk indicators conflicted with interview feedback. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery scan is completed so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Infrastructure Sector Market Size Measured Against Other Published Estimates

Published market sizes for Asia-Pacific infrastructure often do not match because each publisher draws the scope line in a different place and uses different ways to convert project activity into USD values. Differences also show up when the base year is not the same, or when local-currency series are converted using different exchange-rate timing.

Tender pipelines, public budget execution, and construction input cost series are the evidence checks that keep Mordor Intelligence's 2025 estimate aligned to funded infrastructure build activity across transportation, utilities, social assets, and extraction related infrastructure, rather than a narrower construction-only subset. When those signals are applied consistently, the main drivers of gaps become clearer, especially around whether telecom and digital infrastructure is included, how renovation work is treated, and whether forecasts assume aggressive pipeline conversion without re-validating timelines.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.61 T (2025) | |

| Trade Publisher A | USD 1.42 T (2025) | Applies a narrower included set of infrastructure activities, which can undercount social and utility upgrade programs, and it often uses more standardized price escalation and FX timing that may not reflect country-level cost cycles. |

| Industry Platform B | USD 1.33 T (2024) | Uses a different base year and leans more on reported project and company coverage, which can miss parts of publicly funded works and timing shifts, and it may carry multi-year programs using booked values rather than executed spend. |

Across the three figures, the spread is explained mostly by scope edges, base-year choice, and how project timing and price inflation are carried into USD values. By tying the model to observable funding and build activity indicators, we keep the estimate repeatable and easier to trace back to country drivers and assumptions.

Key Questions Answered in the Report

How large is the APAC infrastructure market in 2026?

It currently stands at USD 1.71 trillion, on track to grow to USD 2.33 trillion by 2031 at a 6.32% CAGR.

Which segment grows fastest within the region?

Transportation infrastructure shows the strongest 8.15% CAGR, driven by new high-speed rail and smart-mobility investments.

What role does private capital play?

Private financing is expanding at a 8.55% CAGR as pension funds and sovereign wealth vehicles fund data centers, toll roads, and renewable grids.

Which country adds the most infrastructure value?

China contributes 50.12% of 2025 spending, underpinned by mega-dams, rail expansion, and smart-city underground utilities.

Page last updated on: