North America Mechanical, Electrical, Plumbing (MEP) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

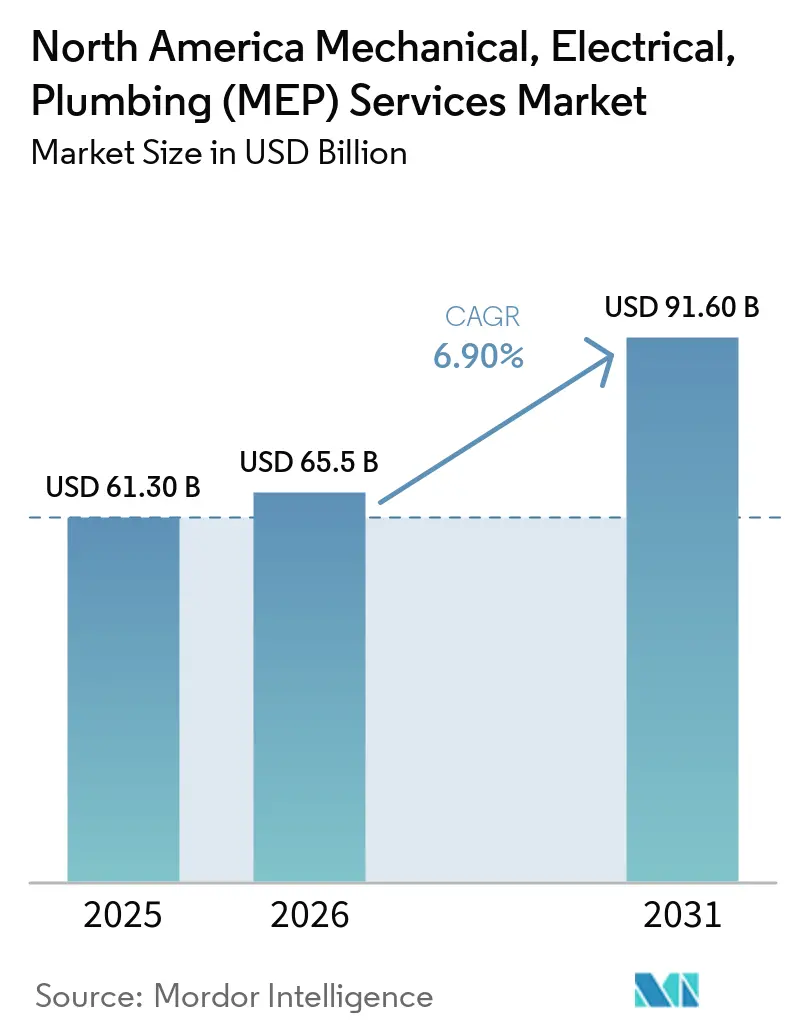

| Base Year Market Size (2025) | USD 61.30 Billion |

| Market Size (2026) | USD 65.5 Billion |

| Market Size (2031) | USD 91.60 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mechanical, Electrical, Plumbing (MEP) Services Market Analysis by Mordor Intelligence

The North America Mechanical, Electrical, Plumbing Services Market size is expected to increase from USD 61.30 billion in 2025 to USD 65.5 billion in 2026 and reach USD 91.60 billion by 2031, growing at a CAGR of 6.90% over 2026-2031. Growth in the North America MEP services market is being supported by federal infrastructure appropriations, stricter electrification and energy codes, and a data center construction cycle that is unusually intensive in electrical and cooling scope. The United States Department of Transportation had obligated USD 490.2 billion under the IIJA by April 2026, and the latest BUILD grant round has expenditure timelines through 2035, keeping water, transit, and public facility projects active for mechanical and plumbing contractors over a long period. The EPA also funded more than 1,200 drinking water State Revolving Fund projects and allocated USD 15 billion for lead service line replacement, keeping plumbing-heavy replacement work visible across municipal systems.

At the same time, the 2026 National Electrical Code, Oregon’s 2025 energy code, New York’s 2025 code update, and California’s 2025 Energy Code are widening the design, documentation, commissioning, and retrofit scope on new and existing buildings. The North America MEP services market is therefore moving toward earlier engineering engagement, tighter multi-trade coordination, and more integrated lifecycle contracts, even as labor shortages and material volatility keep delivery capacity under pressure.

Key Report Takeaways

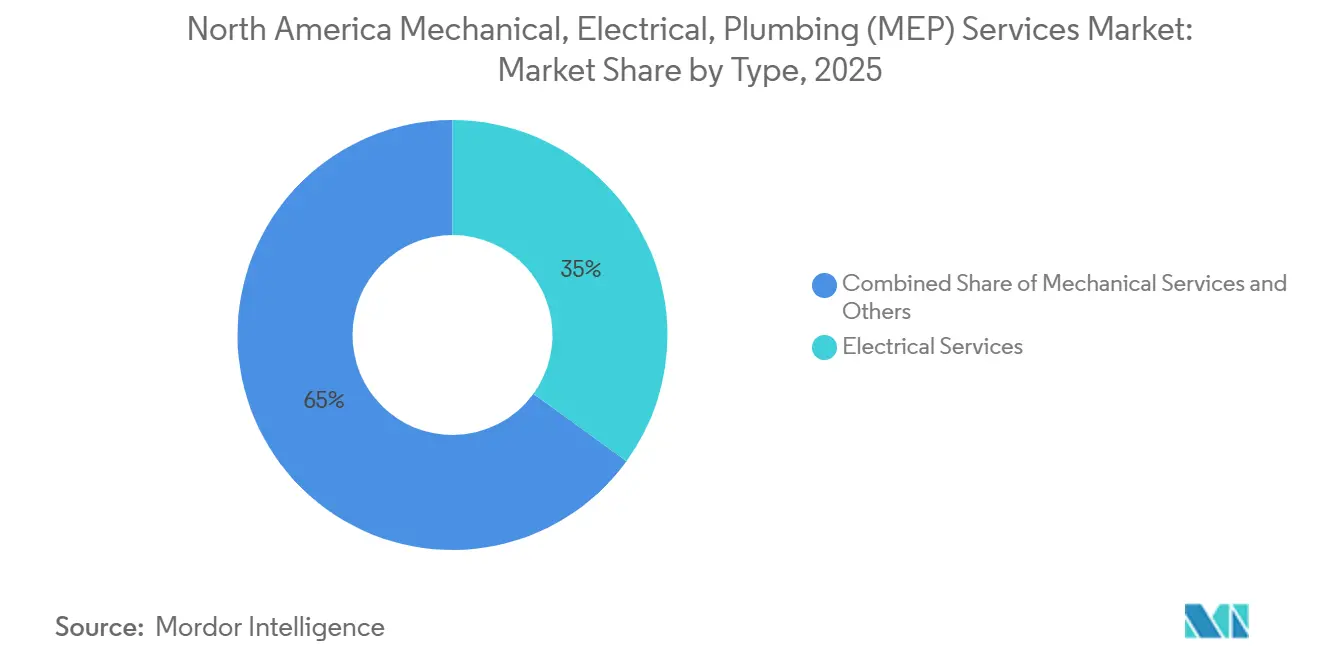

- By type, Electrical Services held 35% of the North America MEP services market in 2025, while Integrated MEP Services is forecast to record the fastest 8.86% CAGR through 2031.

- By service type, Design and Engineering accounted for 31% of the North America MEP services market share in 2025, while Managed and performance-based services is projected to expand at an 8.03% CAGR through 2031.

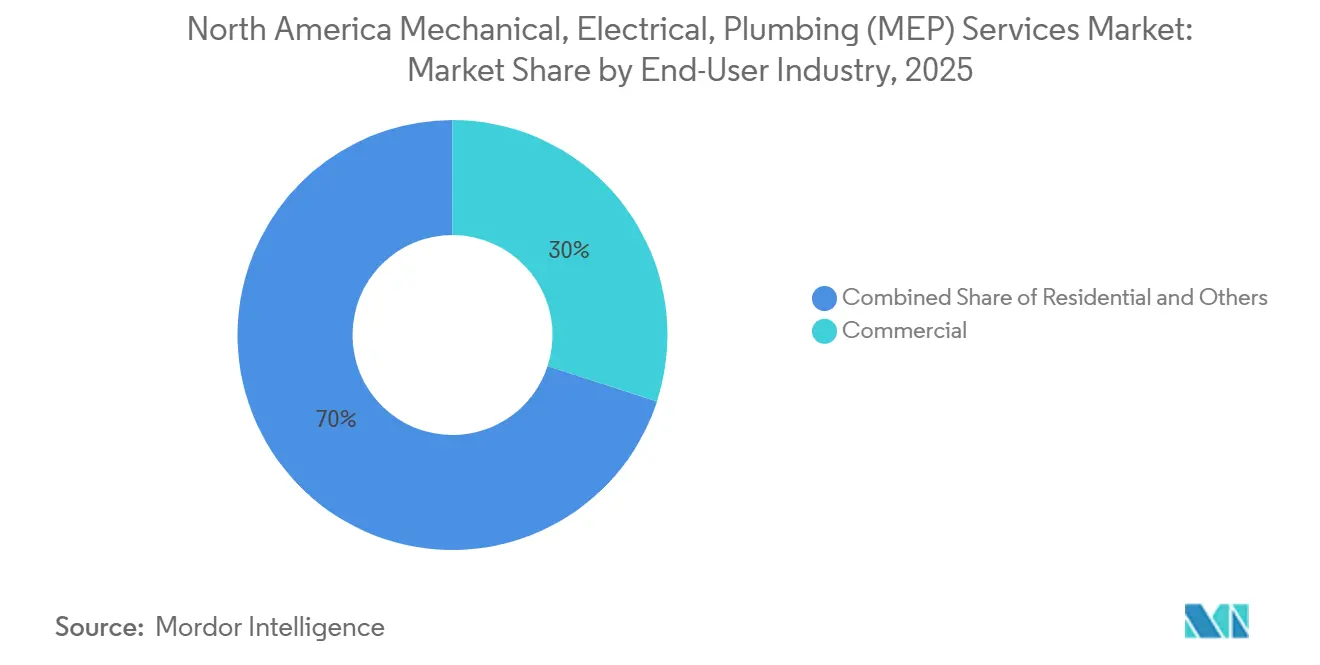

- By end-user industry, Commercial held 30% of the North America MEP services market in 2025, while Infrastructure is projected to grow fastest at a 9.27% CAGR through 2031.

- By geography, the United States held 77.5% of the North America MEP services market size in 2025, while Mexico is projected to expand fastest at an 8.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Mechanical, Electrical, Plumbing (MEP) Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and State Infrastructure Funding | +1.8% | United States and Canada, with spillover into Mexico industrial corridors | Medium term (2-4 years) |

| Data Center and EV Charging Build-Out | +1.6% | United States primary, Canada secondary | Short term (≤ 2 years) |

| Stricter Building Performance and Energy Codes | +1.0% | United States and Canada, with stronger adoption in California, New York, and Oregon | Medium term (2-4 years) |

| NEC and Utility-Driven Electrical Service Upgrades | +0.8% | United States national, strongest in electrification-intensive states | Short term (≤ 2 years) |

| Mission-Critical Cooling Redesign Complexity | +0.6% | United States hyperscale corridors, Canada emerging hubs | Short term (≤ 2 years) |

| Grid-Interactive Retrofit Demand in Secondary Cities | +0.4% | United States Midwest and Southeast, Mexico industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal and State Infrastructure Funding

Federal appropriations are giving the North America MEP services market a long runway because they support project categories that carry large mechanical, electrical, and plumbing packages. The IIJA includes major highway and transportation authorization, and DOT data showed USD 490.2 billion obligated and USD 218.6 billion outlaid across programs by April 2026, which confirms that spending has moved beyond announcement into active execution[1]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Funding Status,” U.S. Department of Transportation, transportation.gov. For MEP contractors, spending matters most in transit facilities, stormwater systems, treatment plants, pump stations, and public buildings, where electrical distribution, controls, piping, ventilation, and fire protection are built into the core scope rather than added later. The EPA’s funding pattern reinforces that view because it had already supported more than 1,200 drinking water revolving fund projects and designated USD 15 billion for lead service line replacement, which is overwhelmingly plumbing-intensive work. The 80% federal cost share on many urban projects also reduces local funding friction, which shortens procurement cycles and moves MEP-heavy public jobs forward faster than in prior infrastructure cycles. This driver supports backlog visibility in the North America MEP services market because public projects usually extend across multi-year design, procurement, installation, and commissioning phases, which spreads revenue opportunities across more than one contracting season.

Data Center and EV Charging Build-out

The North America MEP services market is also being lifted by a data center and EV charging wave that is far more power-intensive than standard commercial construction. Electrical rooms, medium-voltage distribution, substations, switchgear, direct liquid cooling loops, backup systems, and control platforms now define the critical path on hyperscale projects, which shifts a larger share of project value into MEP scope. Amazon announced a USD 15 billion investment in Northern Indiana data center campuses in November 2025, and CyrusOne, with Calpine, announced a USD 1.2 billion hyperscale data center project in Texas with 190 MW of initial capacity in July 2025, both of which illustrate the scale of current power and cooling requirements. These projects not only increase volume, but they also raise technical complexity because dense racks and resilient uptime targets demand closer integration between electrical design, cooling, controls, and commissioning. EV charging adds another layer because commercial and institutional sites increasingly need service upgrades, emergency disconnect arrangements, and coordination with building load management strategies under the 2026 NEC. The result is that the North America MEP services market is seeing stronger demand not just for installers, but also for firms that can engineer, sequence, and commission tightly integrated systems on compressed schedules.

Stricter Building Performance and Energy Codes

Code tightening is turning deferred replacement and discretionary upgrades into mandatory project scope across the North America MEP services market. Oregon adopted the 2025 Oregon Energy Efficiency Specialty Code effective January 2025, and New York incorporated ASHRAE 90.1-2022 elements into its 2025 Energy Code, which raises baseline requirements for lighting, ventilation, and major mechanical equipment. California’s 2025 Energy Code, effective January 1, 2026, introduces mandatory heat pump replacement for end-of-life rooftop HVAC units in several building types, which turns routine equipment turnover into broader electrical and mechanical redesign work. Pacific Northwest National Laboratory estimated that moving from ASHRAE 90.1-2019 to 90.1-2022 adds USD 0.57 to USD 1.69 per square foot in first costs, and that cost increase flows heavily through engineering effort, controls selection, and installation labor. ASHRAE’s newer ventilation and performance pathways also push owners toward system-level modeling and integrated trade coordination instead of checklist compliance, which favors firms with deeper preconstruction and commissioning capabilities. This is widening both the fee scope and delivery responsibility in the North America MEP services market because every code revision now touches more than one trade. package at the same time.

NEC and Utility-Driven Electrical Service Upgrades

The 2026 National Electrical Code is increasing electrical design and retrofit work across the North America MEP services market. NFPA reported that the 2026 edition processed 3,933 public inputs and introduced five new medium-voltage articles, which reflects how commercial and institutional projects are moving into more complex power configurations. The code also expands requirements around arc-flash labeling, alternate-energy source disconnect identification, and power control systems, which adds engineering documentation, coordination studies, field verification, and compliance testing to a wider set of projects. For contractors, that means electrical upgrades are no longer limited to new capacity additions, because existing facilities with solar, storage, EV charging, or major retrofit work now trigger broader review and correction cycles. Utility-driven service upgrades in electrification-heavy states add another layer, since owners often need larger feeders, switchboards, and smarter load management to support heat pumps, chargers, and digitally managed building systems. This driver supports recurring work for the North America MEP services market because compliance obligations continue after initial installation through inspection, maintenance, and later expansion phases.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages in Specialty Trades | -1.5% | United States national, with acute pressure in Texas, Georgia, North Carolina, and Florida, and in Canada’s large provinces | Short term (≤ 2 years) |

| Switchgear, Transformer, and Copper Price Volatility | -1.2% | United States primary, with spillover into Canada and Mexico through imported equipment chains | Medium term (2-4 years) |

| Utility Interconnection Delays for Electrification-Heavy Projects | -0.8% | ERCOT, PJM, CAISO, and other power-constrained U.S. regions | Medium term (2-4 years) |

| Cybersecurity Compliance Burden for Connected Building Systems | -0.5% | United States federal facilities, healthcare, and critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages in Specialty Trades

Labor availability remains the clearest short-term constraint on the North America MEP services market because demand is rising faster than the skilled workforce pipeline. The 2025 AGC and NCCER workforce survey found that 92% of firms had difficulty filling hourly craft positions, and more than 75% specifically cited electricians, pipefitters, and plumbers as hard to recruit. Associated Builders and Contractors said the construction industry must attract 349,000 net new workers in 2026, which shows that current hiring flows are not enough to meet project demand. Data center construction worsens the strain because it pulls the most experienced electricians, commissioning specialists, and controls staff toward high-pay projects, leaving conventional commercial and institutional work with tighter labor pools. That imbalance raises bid premiums, extends schedules, and pushes owners toward larger contractors with prefabrication and workforce training systems. It also creates room for integrated delivery in the North America MEP services market because owners increasingly value firms that can solve labor coordination internally rather than depend on separate trade handoffs.

Switchgear, Transformer, and Copper Price Volatility

Equipment and commodity volatility is limiting margin stability in the North America MEP services market, especially on electrical-heavy packages. Copper futures reached a record high of USD 6.61 per pound in May 2026, up 45% year on year, which directly affects cable, feeder, and other conductor-heavy scopes. Transformer inflation adds a second layer because large power transformer pricing had roughly doubled over a five-year period and lead times had stretched far beyond earlier norms, forcing contractors to commit procurement much earlier in the project cycle. Medium-voltage switchgear constraints have followed a similar pattern, with longer lead times and higher prices reshaping bid strategy and procurement sequencing. Contractors are responding with escalation clauses, early-release packages, and forward buys, but those tactics do not eliminate risk when public projects still operate within fixed budgets. This restraint matters because the North America MEP services market is now more exposed to power infrastructure content than in earlier cycles, so material inflation affects a larger share of total project value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electrical Services Anchors Revenue, Integrated Delivery Accelerates

Electrical Services held 35% of the North America MEP services market size in 2025, which made it the largest type segment by revenue. That leadership reflects the fact that data centers, commercial retrofits, and electrification programs all place power distribution, controls, protection systems, and service upgrades near the center of project budgets. EMCOR’s U.S. Electrical Construction segment generated USD 845.6 million in Q1 2026 revenue, up 12.8% year on year, and management linked that performance to high-tech manufacturing and data center activity, which supports the segment’s near-term demand base. The 2026 NEC further supports the segment because new medium-voltage provisions, expanded labeling requirements, and power control system recognition raise billable design and field compliance work on commercial and institutional projects[2]Dean Austin, “Key Changes in the 2026 NEC,” NFPA, nfpa.org. Electrical Services also captures a large share of value when existing buildings shift toward heat pumps, chargers, storage, and more digital controls, since all of those changes affect service sizing and distribution architecture. In the North America MEP services market, that makes electrical scope both volume-led and complexity-led, which is a stronger position than relying on replacement demand alone.

Mechanical Services remains the second-largest type because HVAC, fire protection, process piping, and mission-critical cooling sit at the center of hospitals, advanced manufacturing plants, and data centers. Cooling design is becoming more complex as rack densities rise and owners move from standard air systems toward liquid-assisted or liquid-based cooling strategies, which raises the need for tighter coordination between piping, controls, power, and commissioning. Plumbing Services is smaller by revenue share, but it benefits from clear replacement cycles tied to water infrastructure work and lead service line programs, which gives it a steadier municipal demand base than many discretionary building categories. Integrated MEP Services is projected to grow at an 8.86% CAGR through 2031, the fastest pace among type segments in the North America MEP services market. Owners are leaning toward this model because one accountable delivery party reduces coordination gaps, shortens commissioning time, and lowers claims risk on complex facilities. That shift suggests the North America MEP services industry is rewarding firms that can combine trade depth with program management rather than firms that only provide isolated packages.

By Service Type: Design & Engineering Leads, Performance Contracts Redefine Delivery Value

Design and Engineering accounted for 31% of the North America MEP services market size in 2025, which made it the largest service-type segment. That position reflects how much more front-end coordination is required when projects must satisfy energy codes, electrical code changes, BIM coordination, and owner sustainability targets within the same design window. ASHRAE 90.1-2022 and related state code updates increase the modeling and documentation burden, while Pacific Northwest National Laboratory’s cost analysis shows that tighter standards carry measurable first-cost additions that pass through engineering and system selection decisions. The largest projects now require earlier decisions on electrical topology, ventilation strategy, cooling configuration, and controls integration, which enlarges preconstruction scopes even before site work begins. In the North America MEP services market, that means design value is expanding because owners need fewer conflicts in the field and more certainty around code acceptance, energy performance, and commissioning readiness.

Installation, Testing, and Commissioning remains the second-largest service type because mission-critical buildings and regulated facilities are placing more emphasis on witnessed testing and functional validation before handover. Commissioning now operates as a distinct delivery phase on many data center programs, where capacity, redundancy, and uptime targets leave little tolerance for sequencing errors or documentation gaps. Managed and performance-based services is projected to grow at an 8.03% CAGR through 2031, which marks a structural move toward lifecycle accountability in the North America MEP services market. Building owners increasingly want outcome-based contracts that link maintenance, controls optimization, uptime, and energy performance into one service relationship rather than separate work orders. Maintenance, Repair, and Retrofit remains important because aging commercial stock, heat pump replacement mandates, and ventilation standard changes continue to trigger system updates on occupied buildings. This is also where the North America MEP services industry is beginning to overlap more closely with property operations, since post-installation value now depends as much on continuous performance as on the initial build.

By End-User Industry: Infrastructure Leads Growth, Commercial Sustains Volume

Commercial held 30% of the North America MEP services market size in 2025, which made it the largest end-user segment by revenue. The segment remains broad, but the largest recent demand pockets have come from data center campuses, healthcare expansions, and office retrofits that require deeper electrification, controls work, and HVAC modernization. Amazon’s Indiana data center investment and CyrusOne’s Texas hyperscale campus show why commercial work remains so important, because each site requires major electrical distribution, cooling, backup systems, and commissioning scope before it can become operational. Commercial retrofits are also becoming more MEP-intensive because code-driven heat pump adoption, energy upgrades, and smart load controls often require electrical and mechanical redesign at the same time. This makes the commercial portion of the North America MEP services market more resilient than a typical office-led cycle, because it is increasingly tied to digital infrastructure and regulatory retrofit needs rather than to one building category. The North America MEP services market share captured by commercial users therefore rests on both new mission-critical builds and the expanding technical scope of existing asset upgrades.

Infrastructure is projected to grow at a 9.27% CAGR through 2031, the fastest pace among end-user segments in the North America MEP services market. Public spending on transportation, water, sewer, and utility systems carries significant embedded MEP content across pumping, ventilation, controls, drainage, treatment, emergency power, and intelligent systems. The FHWA’s FY 2026 budget estimates included USD 72.6 billion for highway programs and USD 5.5 billion for bridge replacement, while the EPA’s revolving fund and lead line programs continue to support water-related work with long execution windows. Residential activity is smaller in the current mix, but it still benefits from all-electric code pathways, replacement cycles for legacy systems, and ongoing need for plumbing and HVAC upgrades in aging housing stock. Residential demand is more rate-sensitive than commercial or infrastructure work, yet electrification policy keeps a baseline level of MEP retrofit activity in place even when housing starts soften. Across these end users, the North America MEP services market is shifting toward projects where system performance, compliance, and long-term operations matter as much as initial installation.

Geography Analysis

The United States held 77.5% of the North America MEP services market share in 2025, which keeps it far ahead of the rest of the region in both scale and project diversity. The country benefits from the deepest public infrastructure pipeline, the largest hyperscale data center build-out, and the widest spread of state-level code changes that expand MEP scope across new construction and retrofits. DOT obligations under the IIJA and EPA water funding continue to anchor municipal and transportation work, while Amazon’s Indiana expansion and CyrusOne’s Texas development show how private digital infrastructure is adding another large layer of demand. The 2026 NEC and state energy codes also make the U.S. part of the North America MEP services market more revenue-rich per project because compliance now touches electrical service upgrades, energy modeling, ventilation design, and controls integration at the same time. Labor remains the main constraint, since the United States is also where shortages in electricians, pipefitters, and plumbers are most visible in national surveys.

Canada remains an important part of the regional demand profile because building decarbonization and public building modernization continue to support heat pump, electrical, and water system upgrades. The Canadian opportunity is less about the sheer scale seen in the United States and more about steady demand across residential, institutional, and municipal assets that require higher-efficiency systems and lower-emission building services. This gives regional contractors room in the North America MEP services market where retrofit-heavy work favors design coordination and service relationships over pure volume competition. The main constraint is labor availability, because the broader North American skilled trades shortage also affects Canadian project delivery and limits how quickly contractors can expand crews on specialized jobs.

Mexico is projected to grow at an 8.37% CAGR through 2031, which makes it the fastest-growing geography in the North America MEP services market. Growth is being supported by nearshoring-led industrial development, expanding manufacturing requirements tied to U.S. supply chains, and a larger need for industrial-grade power, ventilation, compressed systems, water handling, and process support. The Mexican construction chamber highlighted that nearshoring and Plan México are supporting investment momentum, particularly in facilities tied to export manufacturing and industrial expansion[3]Cámara Mexicana de la Industria de la Construcción, “Industria de la Construcción Aprovechará Nearshoring y Plan México Para Impulsar Inversiones,” Cámara Mexicana de la Industria de la Construcción, cmic.org. Mexico’s role as the top U.S. trading partner in 2024 reinforces that direction because cross-border production requires modern plants with higher electrical and mechanical specifications. That sets a favorable runway for contractors that can deliver industrial MEP scope at the standards expected in automotive, semiconductor, aerospace, and advanced manufacturing supply chains. As a result, the fastest-growing part of the North America MEP services market is not being driven by speculative real estate, but by production-linked investment with direct system complexity.

Competitive Landscape

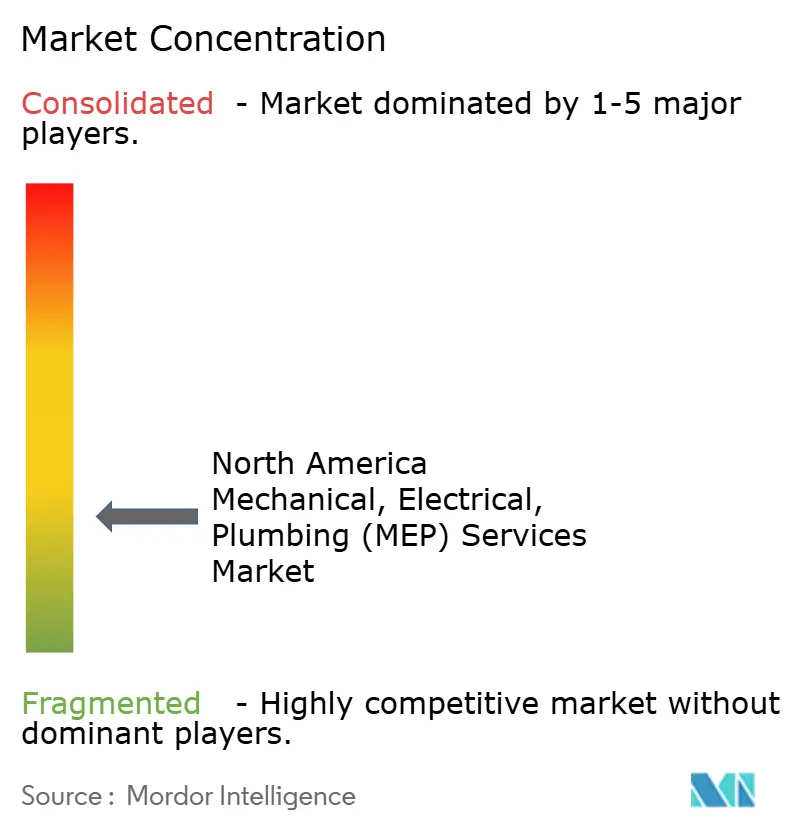

The North America MEP services market is moderately fragmented, with a mix of large public contractors, scaled private firms, and numerous regional specialists competing across mechanical, electrical, and plumbing services. No single company dominates the market, as competition is driven by factors such as technical expertise, local labor availability, prefabrication capabilities, and commissioning strength rather than only geographic scale. Major players such as EMCOR Group continue to strengthen their market positions through backlog expansion, acquisitions, and growing exposure to high-demand sectors including data centers, semiconductor facilities, and network infrastructure. Increasing demand for integrated project delivery and multi-trade coordination is also encouraging larger firms to expand their engineering and prefabrication capabilities to reduce project delays and improve execution efficiency.

Despite ongoing consolidation, regional and specialized contractors continue to maintain strong relevance in local public infrastructure, industrial projects, commercial retrofits, and secondary data center markets where local relationships and labor access remain critical advantages. The market is also evolving as facilities management and lifecycle-service companies expand into MEP contracting through acquisitions and performance-based service offerings. At the same time, many construction owners still procure electrical, mechanical, and plumbing scopes separately for less complex projects, which sustains fragmentation across the industry. As a result, the market continues to present consolidation opportunities while still allowing regional specialists and niche contractors to retain competitive positions.

North America Mechanical, Electrical, Plumbing (MEP) Services Industry Leaders

EMCOR Group

Comfort Systems USA

Southland Industries

M.C. Dean

Rosendin Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: EMCOR Group raised its FY 2026 revenue guidance to USD 17.75 billion to USD 18.50 billion after Q1 revenues of USD 3.92 billion (+11.4% YoY) and a backlog of USD 9.45 billion (+12.1% YoY), with growth attributed to continued demand in data centers, high-tech manufacturing, and network and communications infrastructure.

- February 2026: Rosendin Holdings reorganized into a collaborative co-leadership model with CEO Keith Douglas and Presidents Paolo Degrassi and Justin Tinoco, explicitly aligning senior leaders with data center, AI infrastructure, semiconductor facilities, and the Modular Power Solutions growth initiative.

- January 2026: NFPA published the 2026 National Electrical Code, incorporating 3,933 public inputs, five new medium-voltage articles (265-270), expanded EVSE emergency disconnect mandates, and expanded arc-flash labeling requirements. The code creates engineering and compliance retrofit scope for MEP electrical contractors across all commercial and institutional project types.

- November 2025: CBRE acquired Pearce Services for approximately USD 1.2 billion cash plus up to USD 115 million earn-out, integrating Pearce's 4,000-person critical power, cooling, EV charging, and renewable energy maintenance capabilities. The acquisition signals vertical integration of MEP service delivery as a competitive imperative for large asset-management platforms.

North America Mechanical, Electrical, Plumbing (MEP) Services Market Report Scope

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| Integrated MEP Services |

| Design & Engineering |

| Installation, Testing, and Commissioning |

| Maintenance, Repair, and Retrofit |

| Managed / Performance-based Services |

| Residential |

| Commercial |

| Infrastructure |

| United States |

| Canada |

| Mexico |

| By Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services | |

| Integrated MEP Services | |

| By Service Type | Design & Engineering |

| Installation, Testing, and Commissioning | |

| Maintenance, Repair, and Retrofit | |

| Managed / Performance-based Services | |

| By End-User Industry | Residential |

| Commercial | |

| Infrastructure | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2031 outlook for North America MEP services?

The North America MEP services market is projected to reach USD 91.6 billion by 2031 from USD 65.5 billion in 2026, growing at a 6.9% CAGR over 2026 to 2031.

Which service category currently leads revenue across North America MEP projects?

Design and Engineering led service-type revenue with a 31% share in 2025, reflecting higher preconstruction effort tied to code compliance, energy modeling, and system coordination.

Which type of work is expanding fastest across MEP contractors in North America?

Integrated MEP Services is the fastest-growing type segment, with an 8.86% CAGR through 2031, because owners want single-point accountability on complex facilities.

Why are electrical contractors seeing stronger demand than other trades?

Electrical Services held the largest 35% share in 2025 due to data centers, electrification upgrades, EV charging infrastructure, and broader compliance work under the 2026 NEC.

Page last updated on: