Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.18 Billion |

| Market Size (2026) | USD 6.45 Billion |

| Market Size (2031) | USD 7.99 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Chocolate Market Analysis by Mordor Intelligence

South America chocolate market size in 2026 is estimated at USD 6.45 billion, growing from 2025 value of USD 6.18 billion with 2031 projections showing USD 7.99 billion, growing at 4.4% CAGR over 2026-2031. Several factors, including strong demand during Easter celebrations in Brazil, the rapid growth of e-commerce platforms, and an increasing preference for premium, single-origin chocolate products, drive the market. While mass-market chocolate products continue to dominate retail shelves, a noticeable shift is underway toward premium and plant-based options. This shift is largely influenced by urban millennials who are opting for chocolates that align with ethical sourcing and wellness trends. Stricter regulations on sugar content are pushing manufacturers to reformulate their products. This has led to a rise in higher-cacao chocolate bars, which not only avoid sugar-related warning labels but also cater to the growing demand for dark chocolate. Overall, the South America chocolate market is moderately consolidated, with key players focusing on innovation and sustainability to maintain their competitive edge.

Key Report Takeaways

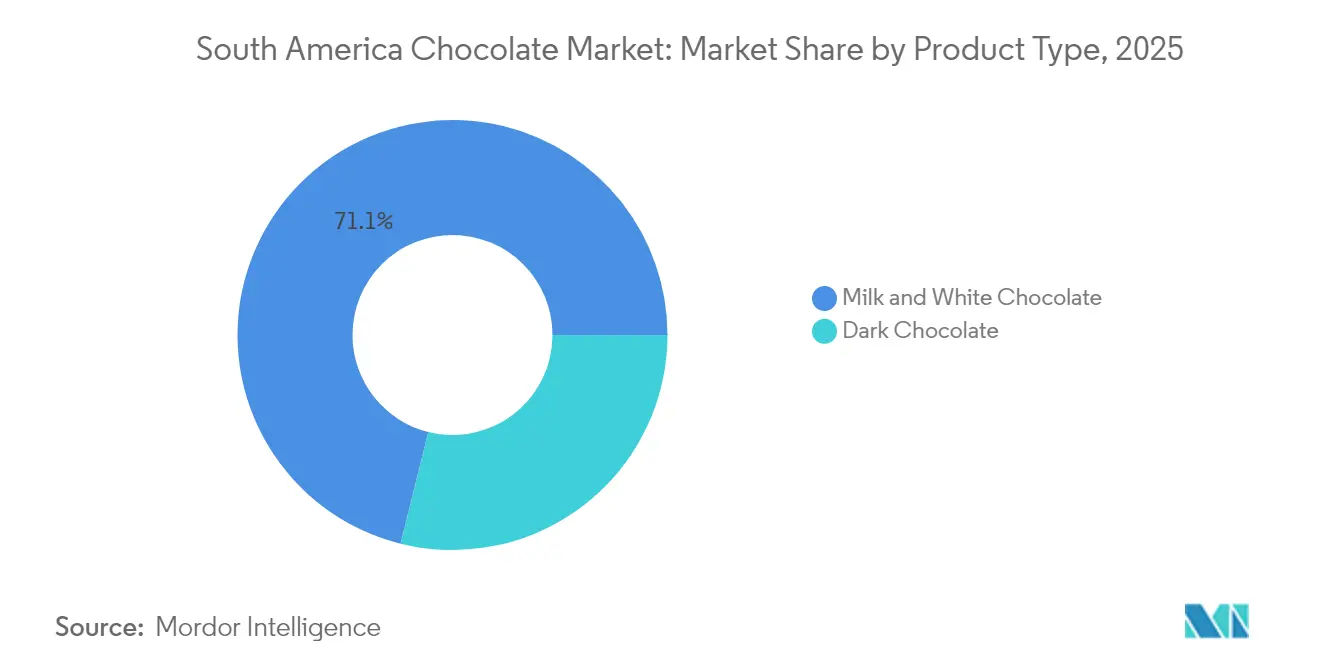

- By product type, milk and white variants led the South American chocolate market with a 71.12% share in 2025, while dark chocolate is expected to advance at a 5.45% CAGR through 2031.

- By form, tablets and bars accounted for 60.02% share of the South America chocolate market size in 2025; pralines and truffles are on track to expand at a 6.28% CAGR to 2031.

- By price range, mass products accounted for 75.10% of 2025 revenue; premium chocolate is expected to rise at a 5.96% CAGR during the outlook period.

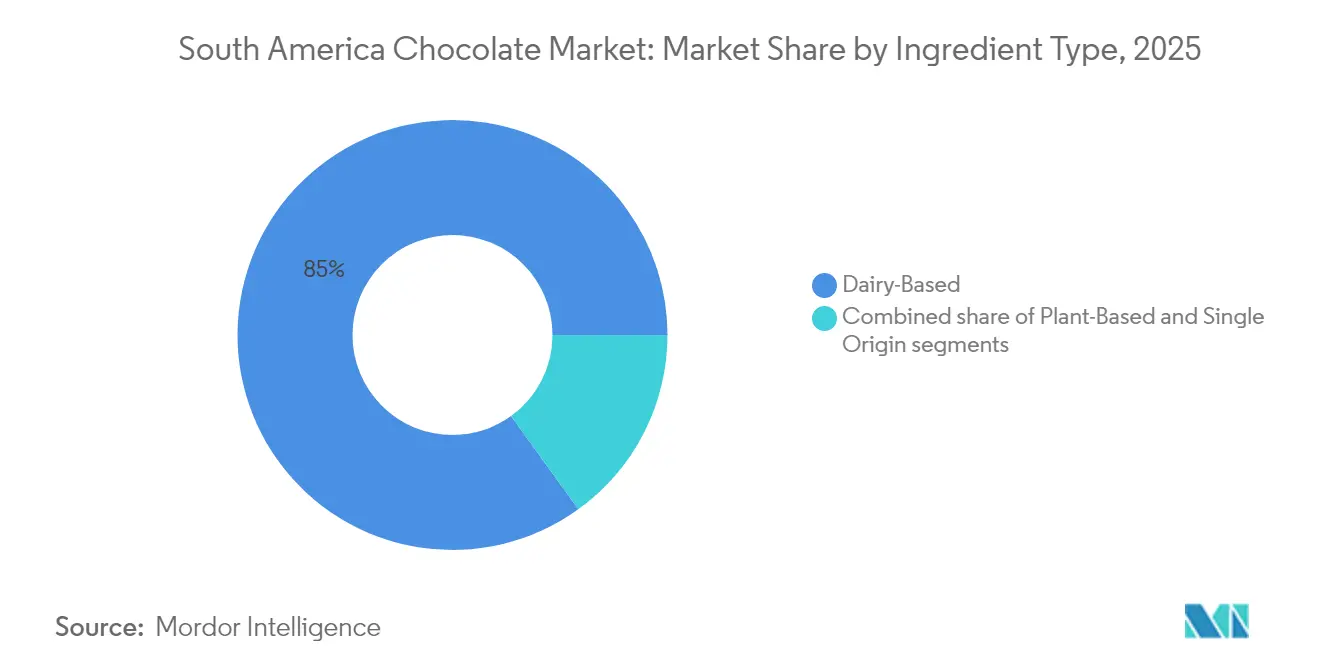

- By ingredient, dairy-based chocolate accounted for 84.95% of sales in 2025, whereas plant-based options are projected to grow at an 8.12% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 44.20% of sales in 2025; online retail is projected to grow at an 7.86% CAGR through 2031.

- By country, Brazil contributed 68.40% of the 2025 turnover, while Argentina is the fastest-growing country, with a 6.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for premium, artisanal, and single-origin chocolate | +1.2% | Brazil (São Paulo, Rio), Argentina (Buenos Aires), Chile (Santiago), Peru (Lima) | Medium term (2-4 years) |

| Demand for dark chocolate supported by increasing health awareness | +0.9% | Global, with early adoption in Brazil, Chile, Argentina urban centers | Short term (≤2 years) |

| Influence of social media and food content creators | +0.7% | Brazil, Argentina, Colombia concentrated in metropolitan areas | Short term (≤2 years) |

| Strong gifting culture and festive occasions | +0.8% | Brazil (Easter-driven), Chile, Argentina, Peru (Valentine's, Mother's Day) | Long term (≥4 years) |

| Innovation in flavors, formats, and functionality | +0.6% | Brazil, Colombia, Argentina led by local and multinational Research and Development hubs | Medium term (2-4 years) |

| Shift toward organic, clean label, and sustainable sourcing | +0.5% | Chile, Peru, Argentina spillover to Brazil premium segment | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Demand for dark chocolate supported by increasing health awareness

In South America, the demand for dark chocolate is steadily increasing as more people opt for healthier choices. Dark chocolate, as explained by the Cleveland Clinic Organization in their July 2025 article, has between 50% and 90% cacao solids and less added sugar compared to milk chocolate[1]Source: Cleveland Clinic Organization, "The Health Benefits of Dark Chocolate", health.clevelandclinic.org. It is also linked to various health benefits, including improved heart health, enhanced blood circulation, and healthier cholesterol levels. This growing awareness of its health advantages is encouraging consumers across the region to prefer products with higher cocoa content. In Brazil, companies like Cacau Show are expanding their range of dark chocolate products to cater to this trend and attract health-conscious buyers. Similarly, in Argentina, leading brands such as Águila and Havanna are introducing new dark chocolate options designed to meet the needs of wellness-focused consumers.

Growing demand for premium, artisanal, and single-origin chocolate

South America’s chocolate market is witnessing significant growth in the premium segment as consumers increasingly prefer products with authentic origins, ethical production practices, and enhanced flavor profiles. Brazil, the largest economy in Latin America with a GDP of approximately USD 4.97 trillion as reported by the International Monetary Fund, is leading this trend[2]Source: International Monetary Fund, "GDP, Current Prices", imf.org. The premium chocolate category in Brazil is expanding rapidly, encouraging multinational companies to strengthen their presence in the region. For instance, Nestlé highlighted this shift by acquiring CRM Group for BRL 4.5 billion in 2023. Artisanal brands such as Pacari are playing a crucial role in driving market growth. These brands prioritize bean-to-bar transparency and ensure fair compensation for farmers, often paying them significantly above the commodity prices.

Influence of social media and food content creators

Social media and food content creators are playing a significant role in shaping South America’s chocolate market, supported by the region's high internet usage, with 84.46% of Brazil’s population being online, as reported by the World Bank[3]Source: World Bank, "Individuals using the Internet (% of population)", worldbank.org. Platforms like Instagram, YouTube, and TikTok are helping brands reach consumers more effectively. For instance, viral unboxing videos and tasting content are boosting the visibility of brands like Cacau Show. Similarly, Dengo’s minimalist, B Corp-certified chocolate bars are gaining popularity through engaging Instagram stories that highlight their ethical and sustainable practices. Colombian micro-roaster Tibitó is utilizing YouTube tutorials to educate consumers about its products, thereby building a loyal customer base through direct-to-consumer channels.

Strong gifting culture and festive occasions

South America’s chocolate market thrives on a strong culture of gifting and a busy calendar of festivals, which consistently drive demand. In Brazil, Easter is the most significant sales period, with major brands launching a wide range of limited-edition products and starting pre-sales well in advance to meet the high demand. Similarly, in Chile, Valentine’s Day plays a key role in boosting chocolate sales, with pralines being a popular choice for gifting during this occasion. In Argentina, celebrations like Mother’s Day and Father’s Day help maintain steady annual revenue, as gifting chocolates is considered a tradition, even during times of economic challenges. In Peru, the Fiestas Patrias celebrations have been increasing the demand for premium gift hampers. These hampers combine chocolates with local specialties like pisco and coffee, which is gradually gaining popularity across other Andean markets as well.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from healthier snack alternatives | -0.6% | Brazil, Chile, Argentina urban centers with high gym penetration | Short term (≤2 years) |

| Health concerns related to sugar and calories | -0.5% | Chile, Peru, Argentina markets with active FOP labeling enforcement | Medium term (2-4 years) |

| Regulatory pressure on sugar and labeling | -0.7% | Chile, Peru, Brazil, Argentina national enforcement with municipal variation | Long term (≥4 years) |

| Cultural preferences for traditional sweets | -0.4% | Colombia, Rest of South America emerging regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from healthier snack alternatives

South America’s chocolate market is facing increasing competition from healthier snack options, which are gaining popularity among consumers seeking nutritious and filling alternatives. In Brazil, protein bars containing ingredients such as collagen and chia seeds are gaining popularity, particularly among health-conscious and fitness-focused individuals. These consumers prefer snacks that are high in protein and align with their dietary goals, which is why they choose these bars over traditional chocolate products. In Chile, there is a noticeable shift toward nuts such as almonds and cashews, as retailers promote them as heart-healthy options. This trend is further supported by front-of-pack sugar warnings on chocolate products, which discourage some consumers from purchasing them.

Health concerns related to sugar and calories

South America’s chocolate market is facing challenges as health concerns about sugar and calorie consumption grow, influencing consumer choices and government regulations. Many countries in the region have implemented front-of-pack warning labels, which alert consumers to high sugar or calorie content in products. These labels have made parents and health-conscious individuals more cautious, leading to a decline in regular chocolate purchases and a preference for products with simpler, healthier ingredients. Ongoing discussions about stricter regulations on sweeteners are creating uncertainty for manufacturers. Reformulated chocolate products could end up with multiple warning labels, further reducing their appeal. Public health campaigns across South America are also encouraging people to view chocolate as an occasional treat rather than a daily indulgence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Wellness Wave

Milk and white chocolate are the most popular types of chocolate in South America, accounting for 71.12% of the market share in 2025. Their strong appeal is rooted in cultural traditions, such as Brazil’s fondness for creamy-filled Easter eggs and Argentina’s famous alfajores. These sweeter chocolate varieties are especially favored by families and impulse buyers who enjoy their rich and indulgent taste. Their widespread availability in supermarkets and their role in seasonal gifting help maintain their dominance in the region.

Dark chocolate, on the other hand, is experiencing rapid growth as more consumers prioritize health and premium-quality products. This segment is expected to grow at a CAGR of 5.45% through 2031, gradually increasing its share in the South American market. Consumers are becoming more interested in chocolate with higher cacao content and artisanal options, particularly in urban areas. Innovations such as single-origin and ethically sourced products are also driving demand. As people look for healthier and less sugary alternatives, dark chocolate is emerging as a significant growth driver in the regional chocolate market.

By Form: Pralines and Truffles Capture Gifting Premiums

Tablets and bars are the most popular chocolate products in South America, contributing to 60.02% of chocolate sales in 2025. Their popularity is largely due to their easy availability in checkout aisles, where they catch the attention of impulse buyers with well-known brands and a variety of flavors. Global companies often secure prominent shelf space, making these products more visible and accessible to consumers. Regular discounts and affordable prices further enhance their appeal, making them a go-to choice for everyday chocolate consumption among a wide range of consumers.

Pralines and truffles are expected to grow at a faster pace, with a projected CAGR of 6.28% through 2031. These premium chocolate options are increasingly favored as boxed assortments are commonly chosen as gifts for special occasions. Seasonal events and celebrations are driving demand for curated chocolate boxes that offer a unique blend of flavors and variety. To meet this growing interest, brands are focusing on introducing high-quality fillings and visually appealing packaging, making these products more attractive as luxury gift items. This trend is likely to boost the market share of pralines and truffles in South America in the coming years.

By Price Range: Mass Dominates, Premium Accelerates

Mass chocolate continues to dominate the South American market, accounting for 75.10% of total revenue in 2025. This is largely due to its widespread availability in supermarkets and the strong presence of well-known brands, such as Mondelēz International Inc., Nestlé SA, and Mars Inc. Regular discounts and multi-pack promotions make these products affordable and appealing to households, ensuring consistent demand. With its budget-friendly pricing, mass chocolate remains a popular everyday indulgence for a majority of consumers, solidifying its leading position in the region.

On the other hand, premium chocolate is expected to grow significantly, with a projected CAGR of 5.96% through 2031. This growth is driven by urban millennials who prefer products that emphasize ethical sourcing, traceable supply chains, and high-quality ingredients like single-origin cacao. Premium chocolate stands out with its artisanal textures, richer cacao content, and unique flavor combinations, which appeal to more sophisticated tastes. Additionally, attractive packaging and its suitability for gifting further boost its popularity. As a result, the premium segment is likely to play a larger role in the South American chocolate market in the coming years.

By Ingredient Type: Plant-Based Surges from Niche Base

Dairy-based chocolate continues to lead the South America market, contributing 84.95% of total revenue in 2025. This strong performance is driven by the region’s affinity for creamy textures and traditional flavors, such as dulce de leche, which are integral to local preferences. The easy availability of these products in supermarkets and small retail outlets ensures they remain a convenient choice for consumers. The trust in well-established brands and the consistent quality of dairy-based chocolate make it a reliable and popular option across the region.

Plant-based chocolate is growing rapidly and is expected to achieve the highest growth rate among ingredient types, with a projected CAGR of 8.12% through 2031. Consumers are increasingly drawn to alternatives like oat milk and nut milk, which cater to health-conscious preferences by avoiding high sugar and dairy content. These vegan options are becoming more appealing due to improvements in taste and texture, making them more acceptable in mainstream markets. Younger consumers, in particular, are willing to pay a premium for plant-based and allergen-friendly products, driving the expansion of this segment in the South America chocolate market.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets/hypermarkets continue to dominate as the primary distribution channel for chocolate in South America, contributing 44.20% of sales in 2025. These stores attract a large number of daily shoppers and offer high visibility for chocolate products through prominent displays and seasonal promotions, particularly during events such as Easter. Consumers prefer these outlets because they provide a wide variety of chocolate options, making it easy to compare prices and packaging. Strong partnerships with major chocolate manufacturers ensure a steady supply of products, making supermarkets and hypermarkets a convenient choice for most buyers.

Online retail stores are growing rapidly in the South American chocolate market, with a projected CAGR of 7.86% through 2031. Online platforms are gaining popularity due to their convenience, offering faster delivery options and subscription services that cater to urban consumers. Brands like Dengo are leveraging social media and influencer marketing to attract customers and encourage repeat purchases. E-commerce also allows companies to showcase unique products, such as limited-edition or artisanal chocolates, which may not be widely available in physical stores. As more consumers adopt online shopping, this channel is expected to play a significant role in driving the growth of the region's chocolate market.

Geography Analysis

Brazil is the largest contributor to the South America chocolate market, generating 68.40% of the region's revenue. The country’s extensive retail network, strong franchising presence, and cultural traditions, such as Easter gifting, significantly drive its market leadership. Investments in local cacao production have enhanced domestic supply chains, enabling the development of innovative chocolate products across both mass-market and premium categories. By blending traditional favorites with modern flavor trends, Brazil continues to dominate the regional chocolate market.

Argentina is the fastest-growing chocolate market in South America, with a projected CAGR of 6.49% through 2031. Despite economic challenges, consumers are increasingly drawn to premium chocolate as an occasional indulgence, particularly through online platforms that are supported by positive customer reviews. Regulatory efforts promoting cleaner labeling are encouraging manufacturers to simplify ingredient lists, aligning with the growing demand for healthier options. Additionally, interest from regional companies highlights opportunities for cross-border collaborations, which could further accelerate market growth in Argentina.

Other countries in the region, such as Chile, Colombia, Peru, Ecuador, and Venezuela, contribute to the remaining share of the South America chocolate market and play a vital role in niche segments. Chile’s café culture has fueled demand for artisanal and high-cacao chocolates, while Colombia and Peru are gaining recognition for their bean-to-bar craft chocolate production. Ecuador and Venezuela stand out for their active participation in Fair Trade, vegan, and agroforestry-based chocolate categories. Together, these markets create a diverse and dynamic ecosystem that complements Brazil’s scale and Argentina’s rapid growth.

Competitive Landscape

The South American chocolate market is highly fragmented, comprising a mix of multinational companies, regional producers, artisanal brands, and new digital-first startups. Large global brands dominate supermarket shelves with their widespread presence, but smaller companies are carving out their space by offering unique products. These include ethically sourced chocolates, locally inspired flavors, and handcrafted options. This variety ensures a competitive market where no single company has complete control, allowing room for innovation and diversity.

Artisanal and bean-to-bar chocolate makers play a significant role in the market by targeting consumers who value transparency, high-quality cacao, and products with unique origins. These smaller brands often utilize social media platforms to directly engage with their audience, enabling them to grow without relying on traditional advertising methods. The rising popularity of plant-based chocolates and reduced-sugar options is creating new opportunities for these companies to meet the demands of health-conscious and environmentally aware consumers, further diversifying the market.

The increasing focus on traceability and food safety is also shaping the chocolate market in South America. Companies are adopting innovative practices such as blockchain technology to track their supply chains, ensuring transparency and building consumer trust. Others are emphasizing certified co-manufacturing or sustainable sourcing to meet customer expectations. By offering unique value through high-quality ingredients, compelling storytelling, or creative product designs, companies are contributing to a dynamic and competitive chocolate market in the region.

South America Chocolate Industry Leaders

-

Arcor S.A.I.C

-

Ferrero International SA

-

Mondelēz International Inc.

-

Mars Incorporated

-

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The Dutch chocolate brand Tony's entered the Brazilian market, gaining traction among consumers. The company expanded its presence by securing additional distribution agreements within the country.

- September 2024: The Italian company Ferrero announced the launch of its Ferrero Rocher chocolate bars in Brazil. This move introduced a new product format under a brand that is already highly popular among Brazilian consumers.

- October 2023: The Brazilian market witnessed the introduction of the Magnum ruby chocolate flavor. This launch marked an expansion of Magnum's product portfolio, catering to the evolving preferences of Brazilian consumers.

South America Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Product Type. Tablets and Bars, Molded Blocks, Pralines and Truffles, and Other Forms are covered as segments by Form. Mass and Premium are covered as segments by Price Range. Convenience Stores, Online Retail Stores, Supermarkets/Hypermarkets, and Other Channels are covered as segments by Distribution Channel. Brazil, Colombia, Chile, Peru, Argentina and Rest of South America are covered as segments by Country.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-Based |

| Plant-Based |

| Single Origin |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

By Country

| Brazil |

| Colombia |

| Chile |

| Peru |

| Argentina |

| Rest of South America |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-Based |

| Plant-Based | |

| Single Origin | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores | |

| Other Channels | |

| By Country | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms