South Africa Plant Growth Regulators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

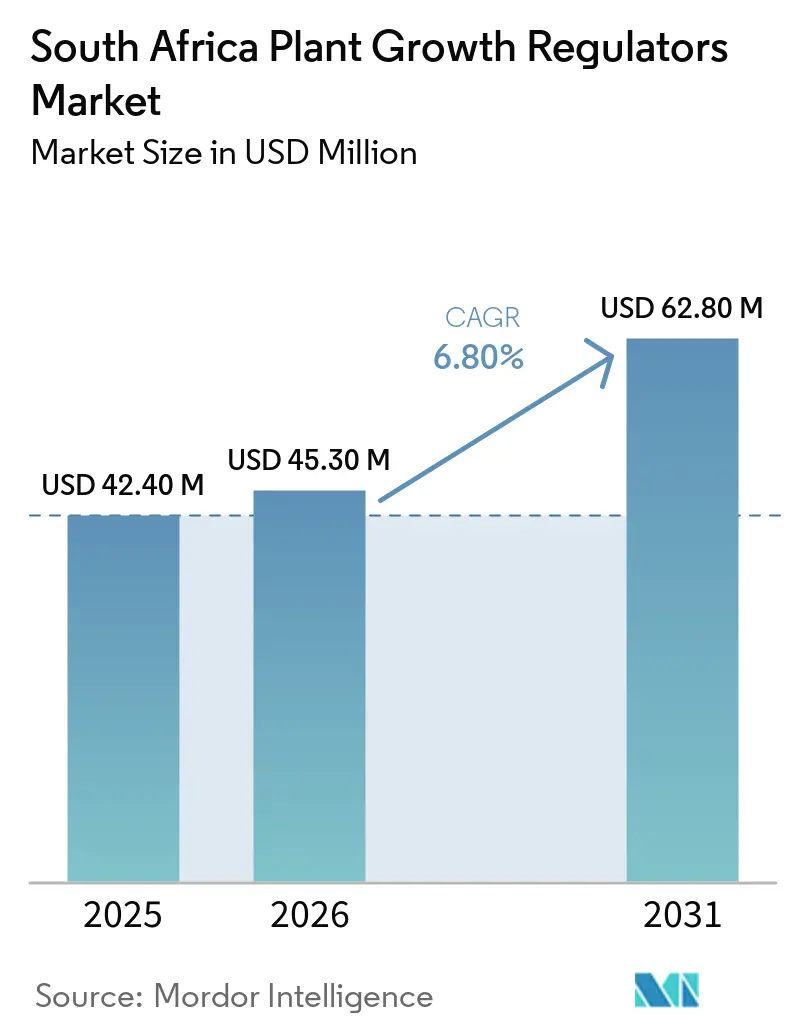

| Base Year Market Size (2025) | USD 42.40 Million |

| Market Size (2026) | USD 45.30 Million |

| Market Size (2031) | USD 62.80 Million |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Plant Growth Regulators Market Analysis by Mordor Intelligence

The South Africa plant growth regulators market size was valued at USD 42.40 million in 2025 and is projected to grow from USD 45.30 million in 2026 to USD 62.80 million by 2031, at a CAGR of 6.8% during the forecast period from 2026 to 2031. The market is supported by a well-established commercial horticulture sector, where export orchards and vineyards rely on tightly managed crop programs to protect fruit quality, harvest timing, and packout performance. The market is also gaining support from industrial sugarcane programs, where ethephon use is becoming more integrated into commercial practice as growers focus on sucrose recovery and harvest value. Product adoption continues to be shaped by Act 36 of 1947, which creates meaningful registration barriers and favors companies capable of maintaining technical dossiers, renewals, and label compliance at scale. Overseas residue requirements and domestic climate stress are making grower decisions more selective, increasing the value of proven chemistries, local advisory support, and application timing accuracy in the market.

Key Report Takeaways

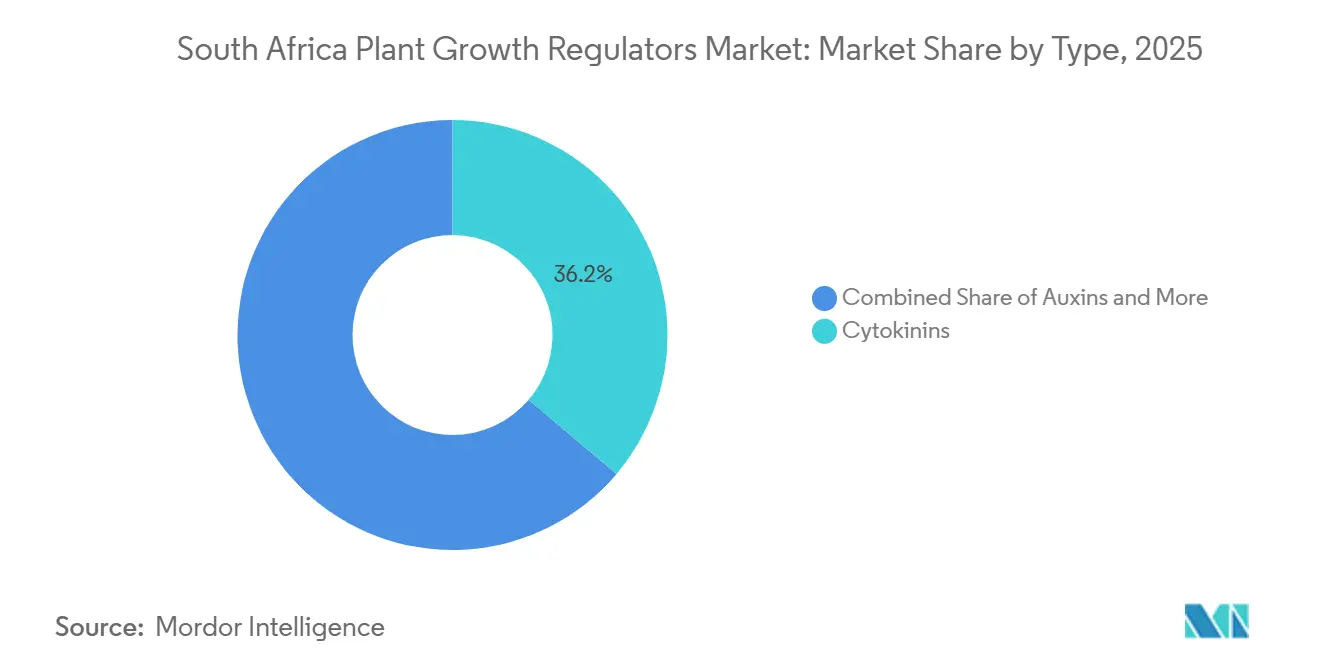

- By type, the South Africa plant growth regulators market share for the cytokinins segment held the largest 36.2% in 2025, while the gibberellins segment is projected to grow at the fastest CAGR of 10.1% from 2026 to 2031.

- By application, crop-based application accounted for the 40.2% of the South Africa plant growth regulators market share in 2025, while non-crop-based application is projected to grow at the fastest CAGR of 11.0% from 2026 to 2031.

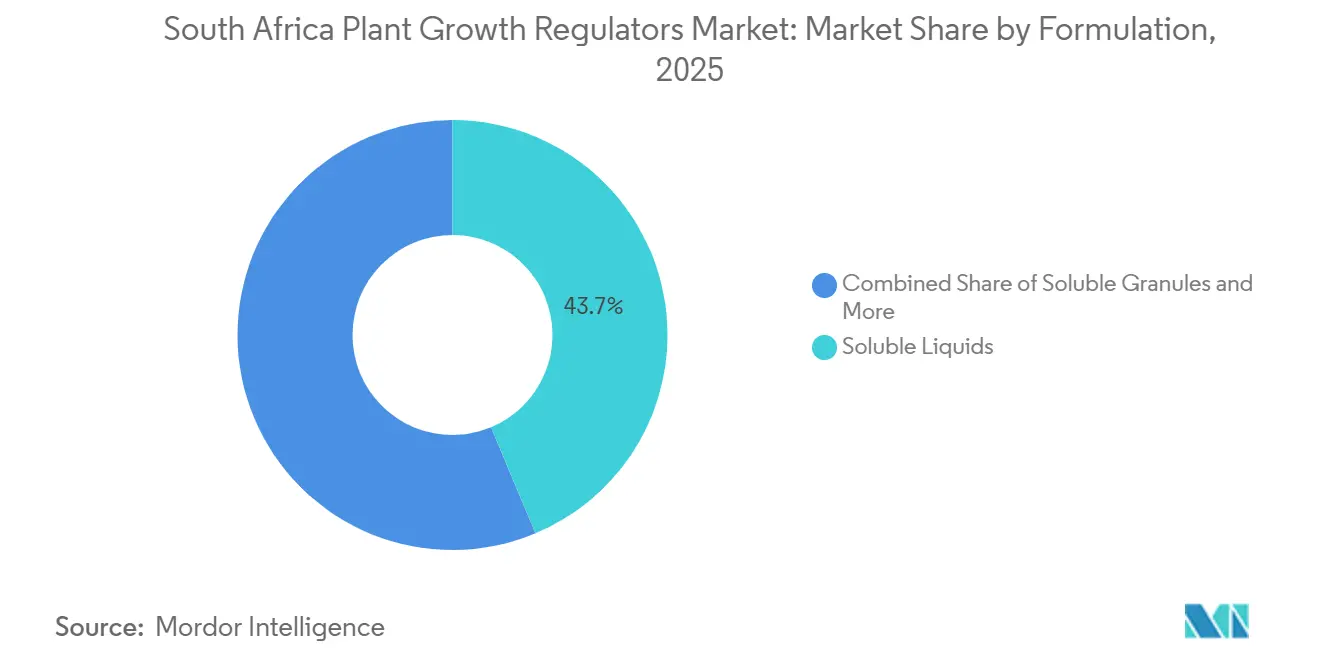

- By formulation, soluble liquids held the largest share of 43.7% in 2025, while soluble granules are forecast to grow at the fastest CAGR of 11.2% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Plant Growth Regulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-driven quality management for citrus and deciduous fruit | +1.9% | Western Cape, Eastern Cape, Limpopo, and Northern Cape | Short term (≤ 2 years) |

| Yield and packout optimization in high-value horticulture | +1.2% | National, with higher intensity in Western Cape and Limpopo | Short term (≤ 2 years) |

| Stress mitigation under water scarcity and climate volatility | +0.9% | Western Cape, Northern Cape, Eastern Cape, KwaZulu-Natal, and Free State | Medium term (2-4 years) |

| Growing use in precision and protected cultivation programs | +0.7% | National, with earlier adoption in high-value horticulture corridors | Medium term (2-4 years) |

| Low-chill winters increasing dormancy-breaker demand | +0.6% | Western Cape | Medium term (2-4 years) |

| Sugarcane ripener programs improving sucrose economics | +0.5% | KwaZulu-Natal and Mpumalanga | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-driven quality management for citrus and deciduous fruit

South Africa’s citrus sector is targeting 260 million cartons of annual exports by 2032, which keeps export quality management central to the South Africa plant growth regulators market. Registered plant growth regulators remain integrated into orchard management programs that help growers align fruit development and shipment quality with demanding export standards. Non-compliance with Citrus Black Spot and False Codling Moth protocols can cost the citrus industry ZAR 3.7 billion (USD 204 million) per season, creating a firm spending floor for crop programs linked to export acceptance. Agri Technovation’s MyGROWTH service measures citrus fruit development every 2 to 4 weeks against cultivar norms, highlighting how application timing is shifting away from fixed calendars toward field-based data [1]Source: Agri Technovation, “Vruggrootte Op Sitrus,” agritechnovation.co.za. HORTGRO revised 2026 pome fruit crop estimates following hail and wind losses in Langkloof and Ceres, reinforcing why recovery support and fruit quality management remain important in the market.

Yield and packout optimization in high-value horticulture

Packout performance remains one of the clearest measures through which growers evaluate returns from plant growth regulator use in the market. Gibberellin and cytokinin combinations are widely used to support berry enlargement and fruit sizing, while auxin-based products help manage fruit drop in crops such as avocados, where alternate bearing can affect commercial output. Laeveld Agrochem reported yield gains of 400 kilograms per hectare in wheat trials for its RELEASE LPH seaweed product, signaling that performance-led adoption is extending beyond orchard systems. This trend is important because grain, oilseed, and legume producers are also facing stronger grading and quality pressures, even though their per-hectare spending continues to trail that of export fruit crops. As a result, the market is expanding from a narrow fruit-quality toolset into a broader crop value management category.

Stress mitigation under water scarcity and climate volatility

Weather variability is shifting part of the South Africa plant growth regulators market away from pure yield enhancement and toward crop protection under stress conditions. The United States Department of Agriculture's Foreign Agricultural Service (USDA FAS) reported that South Africa's corn production for 2024/25 decreased to 13.0 million metric tons, down from 16.4 million metric tons in 2023/24. This reduction is attributed to El Niño-induced drought conditions, which significantly impacted yields in key producing regions. The decline underscores the vulnerability of commercial crop output and agricultural productivity to moisture stress and adverse weather conditions.

Low-chill winters increasing dormancy-breaker demand

Warm and dry winter conditions in the Western Cape moved the 2026 deciduous fruit season 7 to 10 days earlier than historical norms, shortening dormancy-breaking windows for apple and pear growers. This shift is increasing the importance of rest-breaking and bud-management programs in orchards, where even small timing errors can affect flowering and packout consistency. The market is benefiting from this pattern because growers require more precise intervention when natural chill accumulation becomes less reliable. The South African Fruit Journal noted that cytokinin and gibberellin combinations remain a major area of current development in deciduous fruit systems, particularly where low-chill conditions require compensation. If these winter patterns continue, demand is likely to remain firm across Western Cape orchard systems that depend on predictable bud break and early-season uniformity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Act 36 registration and renewal burden | -0.80% | National | Short term (≤ 2 years) |

| Margin pressure from input and application costs | -0.70% | National, with stronger pressure in irrigated regions | Short term (≤ 2 years) |

| Export-market MRL shifts disrupting active ingredient choices | -0.60% | Western Cape, Eastern Cape, and KwaZulu-Natal export corridors | Medium term (2-4 years) |

| Logistics, power, and weather shocks reducing timing precision | -0.40% | National, with sharper exposure in remote farm regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Act 36 registration and renewal burden

The market remains constrained by the registration burden under Act 36 of 1947. The Department of Agriculture, Land Reform and Rural Development reported 5,730 outstanding applications in November 2025, including 2,390 agricultural remedy applications, of which 2,205 were already under technical evaluation [2]Source: South African Sugarcane Research Institute, “Information Sheet IS 12.3 Ethephon,” sasri.org.za. Published processing timelines ranged from 2 weeks to 24 months, creating uncertainty for product launches, label amendments, and renewal planning. Manual submission ended on April 1, 2026, and the transition to online filing is projected to improve processing efficiency over time, though it also creates a near-term adjustment burden for smaller registrants. This matters more with plant growth regulators because dormancy-breaking, fruit thinning, and fruit-sizing windows remain narrow, meaning delays in registration or amendment can directly reduce grower choice during critical crop stages.

Margin pressure from input and application costs

Higher farm input costs are constraining how much growers can allocate to discretionary crop programs in the market. Agbiz reported that South Africa imports approximately 80% of its fertilizer requirements and that the rand weakened against the United States dollar through August 2025, transmitting global price pressure into local farm budgets. Agbiz also reported a 17.6% increase in urea prices during the first quarter of 2025, intensifying cost control across fertilizer, spray, and crop protection decisions. Under tighter farm budgets, growers typically prioritize mandatory compliance-related products first before reviewing yield-support inputs more cautiously. This keeps the commercial case for plant growth regulators closely tied to measurable field returns, reduced spray passes, and stronger compatibility with existing application schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gibberellins Lead on Export-Grade Fruit Sizing

Cytokinins accounted for the largest share, representing 36.2% of the South Africa plant growth regulators market share in 2025, while gibberellins are projected to be the fastest-growing product type with a CAGR of 10.1% during 2026-2031. Cytokinins remain widely used across berry enlargement in table grapes, root development in nursery and propagation systems, post-harvest quality programs, and antitranspirant applications under water stress in key production regions. Their leading position reflects established use across perennial crop systems, where growers tend to remain with proven chemistries once field performance is validated. Gibberellins are gaining stronger traction in citrus and table grape fruit-sizing programs where applications directly influence packout rates and export premiums. Agri Technovation’s EHE model uses FRUIT-TO-SIZE as a reference foliar product in citrus fruit growth management, with gibberellin combinations monitored against cultivar-specific size curves every 2 to 4 weeks.

Auxins continue to play an important role in pome fruit thinning programs and in root-promoting formulations for nursery crops, where concentration management remains critical during sensitive growth stages. Ethylene-releasing compounds, led by ethephon, continue supporting both the sugarcane ripener segment and the citrus rind-color management market for Valencia oranges entering the European Union and the United Kingdom export channels. Other product types, including abscisic-acid analogs, brassinolides, and seaweed-derived biostimulant actives, are gaining traction as growers respond to retailer expectations for lower synthetic input use. The South African Fruit Journal also identified strigolactones as a future active group for dormancy and branching management in local orchards, although the category remains outside the current domestic registration system. This indicates that the type mix in the South Africa plant growth regulators market is likely to broaden over time, even though current demand continues to center on established registered products.

By Application: Crop-Based Applications Define the Core Demand Engine

Crop-based applications are projected to account for the largest 78.0% of the South Africa plant growth regulators market in 2025, reflecting the strong connection between demand and the country’s export horticulture sector, industrial sugarcane regions, and expanding grain and oilseed cultivation. Within this category, fruits and vegetables represent the highest spending on plant growth regulators per hectare. This is primarily due to the use of gibberellin and cytokinin programs in crops such as citrus, table grapes, pome fruit, stone fruit, avocados, and vegetables. These inputs are considered essential for meeting export grading standards, making them a standard commercial practice rather than optional enhancements. Sugarcane also constitutes a significant portion of crop-based demand, particularly in KwaZulu-Natal and Mpumalanga. In these regions, ethephon ripener and trinexapac-ethyl lodging-control programs are integrated into mill supply systems, ensuring steady demand across different seasons.

Non-crop-based applications are projected to achieve the fastest growth within the application segment, with a CAGR of 9.2% during the period 2026-2031. This growth is driven by increased spending on professional sports facility maintenance, premium residential and commercial landscaping, and the certified export market for cut flowers and potted plants. In managed turf, growth retardants are increasingly used to reduce mowing frequency and irrigation needs, addressing labor and water constraints faced by stadium operators and municipal contractors. Additionally, ornamentals and nursery crops benefit from the application of registered rooting hormones and cytokinin products, which enhance plant uniformity and extend shelf life for retail and wholesale distribution channels.

By Formulation: Soluble Liquids Hold the Largest Share While Soluble Granules Are the Fastest-Growing Formulation

Soluble liquids accounted for the largest 43.7% of the South Africa plant growth regulators market size in 2025, reflecting a strong preference for formats that integrate seamlessly into existing spray and fertigation systems. These products are compatible with air-blast sprayers, center-pivot systems, and drip-fertigation setups, which are widely used in South Africa’s commercial orchards and sugarcane farms. Their popularity is further supported by the prevailing cost environment, where high labor and diesel expenses make additional spray rounds less feasible for most growers. Consequently, many farmers opt to apply plant growth regulators alongside adjuvants, foliar nutrients, and biostimulants in a single application. The South African Sugarcane Research Institute’s ethephon protocol, recommending 1.5 liters per hectare applied 8 to 12 weeks before harvest, underscores the integration of soluble liquid formats into commercial sugarcane programs in KwaZulu-Natal.

Soluble granules are projected to grow at the fastest CAGR of 11.2% from 2026 to 2031. Their adoption is increasing in precision and protected cultivation systems due to their dust-free handling, extended shelf life, and controlled solubilization, which are critical for applications requiring dosing accuracy. Suspension concentrates maintain a stable share in established commercial programs, particularly where active ingredients with low water solubility and consistent suspension properties are necessary. Wettable powders remain relevant in older registered products and in areas where liquid storage infrastructure is less reliable, such as smallholder and emerging commercial farming regions. Other formulations, including emulsifiable concentrates and oil-in-water systems, cater to niche applications where oil-based carriers enhance penetration through the waxy leaf surfaces of crops like citrus and avocado. This division between mature liquid systems and emerging precision-oriented granule formats highlights how the market is balancing traditional field practices with evolving application preferences.

Geography Analysis

The South Africa plant growth regulators market is geographically anchored in the Western Cape and Eastern Cape, where export fruit systems support some of the most intensive crop management programs in the country. The Western Cape is particularly important because pome and stone fruit orchards in Elgin, Ceres, Grabouw, and Villiersdorp operate within narrow seasonal windows and meet high export-quality requirements. HORTGRO reported that the 2026 pome season opened 7 to 10 days earlier than historical norms, tightening the timing for dormancy-breaking and early-season orchard decisions. The Western Cape and Eastern Cape also host much of the country’s citrus export base, where product use remains closely linked with orchard quality routines and export compliance requirements. Laeveld Agrochem’s regional advisory model also demonstrates how local language capabilities, crop-specific support, and field-level trust continue to shape purchasing behavior across these high-value production regions.

KwaZulu-Natal remains the defining geography for industrial plant growth regulator demand within the market. The United States Department of Agriculture Foreign Agricultural Service reported that KwaZulu-Natal accounts for 95% of national sugarcane production, with the balance concentrated in irrigated Mpumalanga[3]Source: United States Department of Agriculture Foreign Agricultural Service, “Sugar Annual,” apps.fas.usda.gov.. In these regions, ethephon adoption has been supported by the South African Sugarcane Research Institute and by the commercial focus on improving sucrose value rather than only maximizing field tonnage. Limpopo is also becoming increasingly important in the South Africa plant growth regulators market because avocado, mango, macadamia, and expanding citrus systems rely heavily on fruit retention, vegetative balance, and packout management. This makes the regional demand structure broader than a simple fruit-versus-cane split, because subtropical orchards add another technically intensive layer of product demand.

Smaller but commercially meaningful demand centers include the Northern Cape for irrigated table grapes and citrus, Mpumalanga for irrigated sugarcane and subtropical fruit, and metro corridors in Gauteng and the Western Cape for turf and ornamental applications. The market also benefits from the country’s role as a Southern Hemisphere supplier into counter-seasonal export channels, supporting a broader production calendar rather than a short single-crop season. Citrus, pome fruit, and grape production programs create recurring demand windows across multiple provinces, rather than concentrating product use within a single harvest period. Geography, therefore, matters less as an administrative boundary and more as a reflection of where export value, water risk, and technical farming intensity intersect.

Competitive Landscape

The South Africa plant growth regulator market remains moderately fragmented, with multinational agrochemical subsidiaries offering broader portfolios and stronger regulatory capacity, while local specialists compete through crop-specific technical support. Philagro South Africa (Pty) Ltd (Sumitomo Chemical Company, Limited), Villa Crop Protection (Pty) Ltd (Land O'Lakes, Inc.), BASF SE, Syngenta Group Co., Ltd., and UPL Limited are major companies that benefit from multi-category portfolios and access to international regulatory dossiers, which are becoming more important as the 2024 Agricultural Remedies Regulations increase compliance complexity. AECI Limited Agri Health demonstrated the value of local market depth through a 45.9% profit increase in FY2024 and earnings-per-share growth above 20% in FY2025 as Plant Health volumes improved. AECI also expanded into digital agronomic bundling through its equity acquisition of the Khula App and the integration of supPlant precision irrigation technology into its Agri Health offering. ADAMA Ltd. also repositioned South Africa within its Europe, Africa, and Middle East structure during January 2025, supporting regional revenue growth in early 2026.

Local players such as Laeveld Agrochem, Kelp Products (Pty) Ltd, Farm-Ag International (Pty) Ltd, and Rolfes Agri (Pty) Ltd remain competitive because they provide niche formulations and stronger field advisory support than larger portfolio-driven suppliers often prioritize. Laeveld Agrochem’s partnership with Rootella in May 2025 and its GROEI advisory magazine in Afrikaans demonstrate how local-language capability, trust, and crop-level service continue to build durable grower relationships in Western Cape wine and table grape regions. Kelp Products (Pty) Ltd is also positioning seaweed-derived biostimulants as lower-compliance alternatives within sustainability-linked crop programs. A clear market opportunity remains in bundled advisory models that combine registered plant growth regulators with live data tools tracking fruit growth curves, cane Brix levels, and orchard stress indicators, where no participant yet holds a fully scaled commercial position.

Compliance conditions under Act 36 of 1947 continue shaping competitive advantage more strongly than distribution reach alone. The South African Government reported a backlog of 5,730 applications in November 2025, increasing the value of in-house scientific and regulatory teams capable of managing filing, renewal, and label compliance more efficiently. The transition to mandatory online filing from April 2026 is projected to improve processing over time, though it will also add another operational layer for smaller registrants in the near term. As a result, market leadership is becoming increasingly tied to technical capability, crop advisory quality, and regulatory execution. Companies combining compliant product portfolios with trusted farm-level support are likely to maintain the strongest competitive position in the South African plant growth regulator market.

South Africa Plant Growth Regulators Industry Leaders

Philagro South Africa (Pty) Ltd

Villa Crop Protection (Pty) Ltd (Land O'Lakes, Inc.)

BASF SE

Syngenta Group Co., Ltd.

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: UPL Limited introduced HYCOXA, a seaweed-based biostimulant designed to enhance nutrient uptake, promote plant growth, and increase crop tolerance to abiotic stress. This product strengthens the company's sustainable crop management portfolio and complements plant growth regulator applications, contributing to improved crop performance and productivity.

- May 2025: Syngenta Group and Rizobacter S.A. have announced a collaboration to introduce biological seed-treatment solutions in South Africa. This partnership integrates Syngenta’s Seedcare technologies with Rizobacter’s expertise in biological solutions to enhance crop establishment, improve nutrient-use efficiency, and promote sustainable agricultural productivity.

South Africa Plant Growth Regulators Market Report Scope

Plant Growth Regulators are natural or synthetic compounds that affect plant growth and development by controlling physiological processes such as cell division, flowering, fruit setting, ripening, and stress response. They are extensively utilized in agriculture and horticulture to enhance crop yield, quality, and overall plant performance. The South Africa plant growth regulators market is segmented by type (cytokinins, auxins, gibberellins, ethylene, and other types), by application (crop-based and non-crop-based), and by formulation (soluble liquids, soluble granules, suspension concentrates, wettable powders, and other formulations). The market forecasts are provided in terms of value (USD).

| Cytokinins |

| Auxins |

| Gibberellins |

| Ethylene |

| Other Types |

| Crop-based | Grains and cereals |

| Pulses and oilseeds | |

| Fruits and vegetables | |

| Cash crops | |

| Other crops | |

| Non-crop-based | Turf and ornamental grass |

| Ornamentals and nursery crops |

| Soluble Liquids |

| Soluble Granules |

| Suspension Concentrates |

| Wettable Powders |

| Other Formulations |

| By Type | Cytokinins | |

| Auxins | ||

| Gibberellins | ||

| Ethylene | ||

| Other Types | ||

| By Application | Crop-based | Grains and cereals |

| Pulses and oilseeds | ||

| Fruits and vegetables | ||

| Cash crops | ||

| Other crops | ||

| Non-crop-based | Turf and ornamental grass | |

| Ornamentals and nursery crops | ||

| By Formulation | Soluble Liquids | |

| Soluble Granules | ||

| Suspension Concentrates | ||

| Wettable Powders | ||

| Other Formulations | ||

Key Questions Answered in the Report

What is the current size of the South Africa plant growth regulators market?

The South Africa Plant Growth Regulators market is valued at USD 45.3 million in 2026 and is forecast to reach USD 62.8 million by 2031 at a 6.8% CAGR over 2026-2031.

Which product type is expanding the fastest in South Africa?

Gibberellins are the fastest type, with a projected 10.1% CAGR over 2026-2031, driven by stronger use in fruit sizing programs across citrus, table grapes, and avocados.

Which application area generates the strongest demand?

Crop-based application are the largest application segment, with 40.2% share in 2025.

Which product type holds the largest share in South Africa plant growth regulators?

Cytokinins hold the largest share in the type segment, accounting for 36.2% in 2025, supported by broad use across berry enlargement, root development, post-harvest programs, and water-stress management.

Page last updated on: