Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

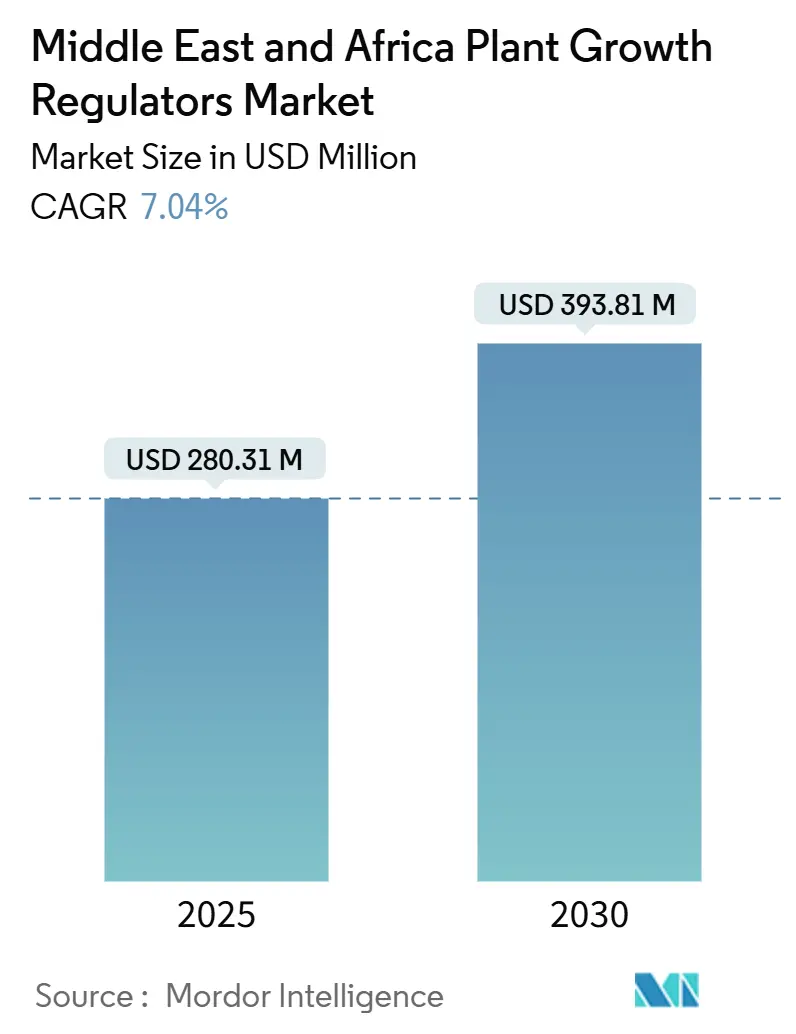

| Market Size (2025) | USD 280.31 Million |

| Market Size (2030) | USD 393.81 Million |

| Growth Rate (2025 - 2030) | 7.04% CAGR |

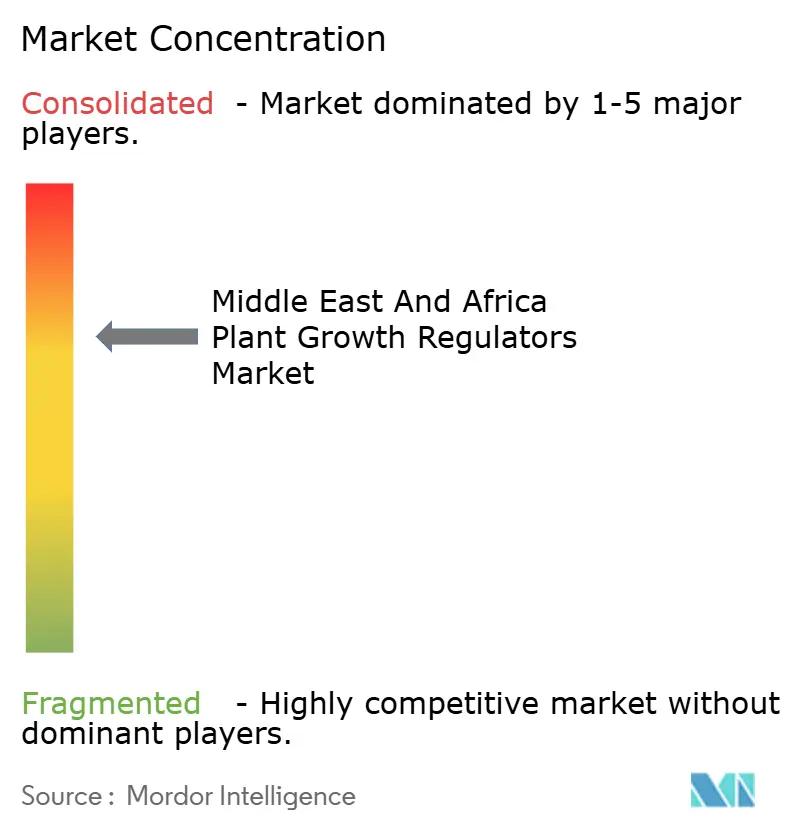

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Plant Growth Regulators Market Analysis by Mordor Intelligence

The Middle East and Africa plant growth regulators market size was valued at USD 280.31 million in 2025 and is projected to reach USD 393.81 million by 2030, growing at a CAGR of 7.04%. The market growth is driven by increasing demand for residue-free exports, expansion of protected cultivation areas, and government-supported desert agriculture initiatives. In Middle East and African countries, these regulators are applied to enhance the production of fruits such as apples, pears, and peaches. According to the Food and Agriculture Organization (FAO), Egypt's fruit production increased from 16.0 million metric tons in 2022 to 16.2 million metric tons in 2023. The growth of contract farming has led to standardized input protocols that include hormonal treatments, while local formulation facilities have reduced supply chain lengths and decreased currency-related price fluctuations. The market sees increased competition between global agrochemical companies and regional specialists, driving innovation in products with faster environmental degradation, controlled-release mechanisms, and application support. Export quality requirements and water conservation needs create opportunities for high-quality cytokinin, gibberellin, and auxin products that increase yield efficiency. These factors support the continued growth of the plant growth regulators market, despite economic pressures on agricultural input costs.

Key Report Takeaways

- By product type, cytokinin led with 36.2% of the Middle East and Africa plant growth regulators market share in 2024, while gibberellin is advancing at a 10.1% CAGR through 2030.

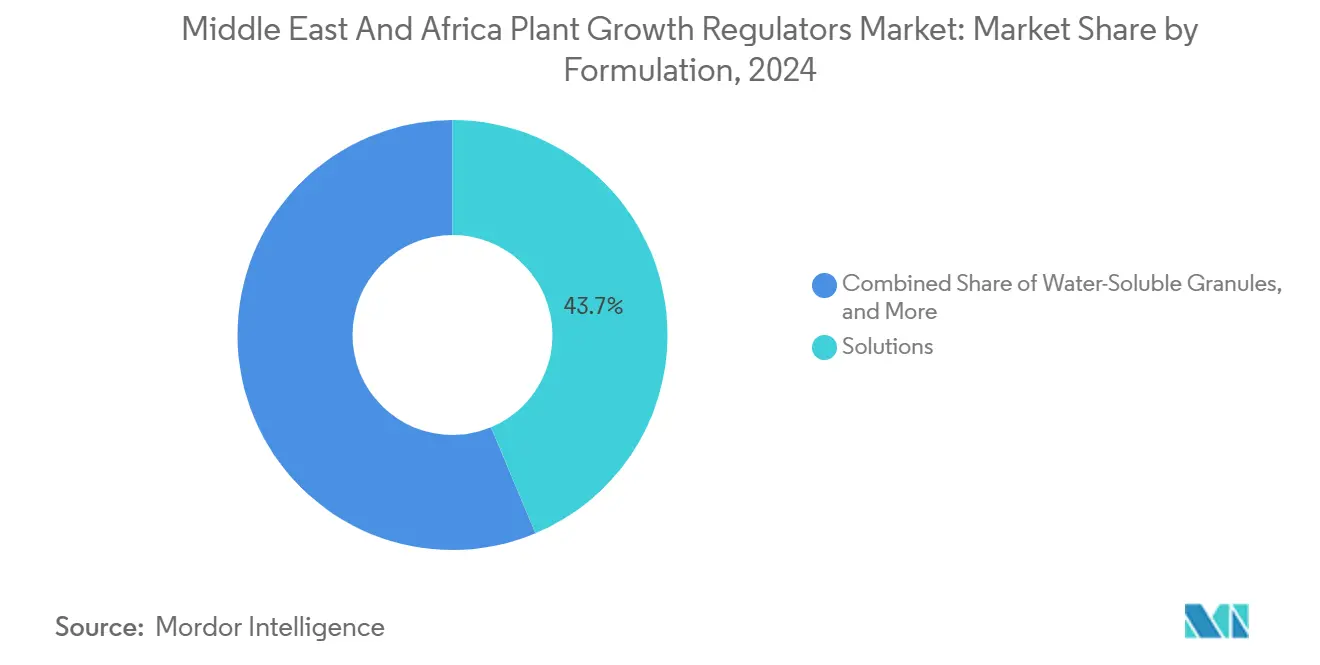

- By formulation, solutions held 43.7% of the Middle East and Africa plant growth regulators market size in 2024, whereas water-soluble granules recorded the strongest 11.2% CAGR to 2030.

- By application, fruits and vegetables commanded 40.2% of the market share in 2024 and are projected to grow at an 11.0% CAGR through 2030.

- By geography, Africa contributed 57.1% revenue share in 2024, while the Middle East exhibits the fastest 9.7% CAGR through 2030.

- BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, and UPL Limited collectively accounted for the majority share in 2024, underscoring a moderately concentrated playing field.

Middle East And Africa Plant Growth Regulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for residue-free exports | +1.2% | Africa core, Middle East emerging | Medium term (2-4 years) |

| Rapid expansion of protected cultivation acreage | +1.8% | Middle East dominant, North Africa growing | Long term (≥ 4 years) |

| Rising adoption in high-value plantations | +1.0% | Global, concentrated in export zones | Medium term (2-4 years) |

| Growth of contract farming across the region | +1.5% | Sub-Saharan Africa, Egypt expansion | Long term (≥ 4 years) |

| Post-harvest loss reduction initiatives | +0.9% | Nigeria, Kenya, Tanzania focus | Short term (≤ 2 years) |

| Pivot to desert agriculture mega-projects | +1.1% | United Arab Emirates, Saudi Arabia, and Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Residue‐Free Exports

European and North American import regulations are implementing stricter maximum residue limits, prompting regulators across Africa to expedite approvals for low-toxicity cytokinin and gibberellin products. Kenya's 2024 regulatory guidelines reduce approval timelines to 16 months for formulations that degrade within 14 days, enabling exporters to obtain premium prices for citrus and vegetables. South African citrus producers benefit from streamlined South African Health Products Regulatory Authority processes that reduce market-entry costs for multinational suppliers[1]Source: South Africa Health Products Regulatory Authority, “SAHPRA Regulatory Framework,” sahpra.org.za. Nigeria's National Agency for Food and Drug Administration and Control implements similar measures, supporting manufacturers that demonstrate rapid environmental degradation of their products.

Rapid Expansion of Protected Cultivation Acreage

In the Gulf, new agricultural investments are increasingly leaning towards controlled-environment agriculture, where synthetic hormones are adeptly used to fine-tune growth cycles under artificial lighting. In a notable 2024 initiative, the Environment Agency Abu Dhabi, in collaboration with the International Center for Biosaline Agriculture, has integrated gibberellin scheduling into hydroponic tomato production[2]Source: Environment Agency Abu Dhabi, “EAD and ICBA Sign Agreement,” ead.gov.ae. This innovation not only slashes water usage by 40% but also boosts yields. Research conducted at King Abdullah University of Science and Technology (KAUST) has demonstrated a 35% increase in yield within CO₂-enriched greenhouses, achieved through the application of targeted gibberellin sprays[3]Source: King Abdullah University of Science and Technology, “Controlled Environment Agriculture,” kaust.edu.sa. The advantages of a controlled environment enable precise timing and dosage control for applications, thereby amplifying the effectiveness of synthetic plant growth regulators while minimizing waste and reducing environmental exposure.

Rising Adoption in High-Value Plantations

Orchards and perennial crop estates are adopting auxin and cytokinin treatments to extend harvest periods and improve product uniformity. Date-palm growers in Egypt have reported 15-20% yield increases. The South African citrus industry has implemented synthetic gibberellin applications to manage harvest timing and maintain consistent fruit sizes, which helps meet European retailers' strict quality requirements. The financial returns from plantation agriculture justify the investment in plant growth regulators, as premium fruit can generate over USD 10,000 per hectare annually, compared to USD 3,000 for conventional field crops. In Ethiopia, coffee cooperatives using cytokinin treatments have achieved 12-15% price premiums through reduced defect rates, with minimal additional expenses.

Growth of Contract Farming Across the Region

In Nigeria, agricultural processors and exporters provide synthetic hormone packages to smallholder farmers through contract farming arrangements, which cover 2 million hectares. This system ensures quality standards and timely delivery while eliminating upfront costs for farmers. Kenya's horticultural export sector implements contract farming that requires synthetic cytokinin and auxin usage in production protocols, enabling smallholder farmers to meet European supermarket standards for product appearance, shelf life, and chemical residue levels. In Tanzania, the cashew processing industry implements contract farming programs that incorporate synthetic gibberellin applications during nut development. This approach increases kernel yield, reduces processing waste, and provides financial incentives for farmers to adopt these agricultural practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low product awareness among smallholders | -1.3% | Sub-Saharan Africa dominant | Medium term (2-4 years) |

| Fragmented distribution networks | -0.8% | Rural Africa, remote Middle East | Long term (≥ 4 years) |

| Stringent product-registration timelines | -0.7% | Regulatory-intensive countries | Short term (≤ 2 years) |

| Sporadic counterfeit trade at border markets | -0.5% | Cross-border trade zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Product Awareness Among Smallholders

In Sub-Saharan Africa, smallholder farmers managing 70% of agricultural land on plots smaller than 2 hectares face significant challenges in adopting synthetic plant growth regulators due to limited technical knowledge and extension support. In Kenya, the agricultural extension system reaches only one in six farmers, limiting access to crucial information about applications, timing, and dosage requirements. Most producers rely on informal knowledge networks that often provide incomplete or inaccurate guidance. The knowledge gap widens due to low literacy rates in rural areas, where farmers operating primarily in local languages struggle to understand product labels and technical materials written in English or French.

Fragmented Distribution Networks

Farmers in remote areas of the Middle East and Africa travel 50-100 kilometers to reach specialized agrochemical retailers, indicating significant access barriers for synthetic plant growth regulators. In Tanzania, the agricultural input distribution system depends on small-scale agro-dealers who often lack technical expertise, storage facilities, and working capital. This limitation is particularly important since plant growth regulators require controlled storage conditions and have a limited shelf life. Rural retailers face inventory management challenges due to seasonal demand fluctuations, with 6-8 months of low sales followed by high demand during planting and flowering seasons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cytokinin Leads Despite Gibberellin Surge

Cytokinins held a dominant 36.2% of the Middle East and Africa plant growth regulators market share in 2024. This dominance reflects their effectiveness in breaking seed dormancy, promoting lateral shoot development, and extending post-harvest life in export-oriented fruits and vegetables. The segment's prominence is particularly evident in date palm cultivation across the Middle East and citrus production in South Africa and Morocco, where cytokinin treatments improve fruit set and reduce pre-harvest drop by 15-20%.

Gibberellin products are projected to grow at a 10.1% CAGR through 2030, marking the fastest growth in the segment. This growth is primarily due to their role in stem elongation and flowering control within protected cultivation systems, which are expanding in the United Arab Emirates and Saudi Arabia's desert agriculture programs. Auxin formulations maintain their importance in root development and cutting propagation, particularly in Ethiopia's coffee regions and Kenya's tea estates. Ethylene regulators serve specific functions in fruit ripening control and flower induction, with increased usage in Egypt's mango exports and South Africa's avocado production. Brassinosteroids, an emerging segment, focus on stress tolerance and yield enhancement, gaining importance in North Africa's water-stressed regions where drought resistance is essential.

By Application: Fruits and Vegetables Drive Innovation

The fruits and vegetables segment holds 40.2% of the Middle East and Africa plant growth regulators market size in 2024, with projected growth of 11.0% through 2030. This dominance reflects the region's emphasis on export-quality crops that require precise quality control and shelf life management. The segment's strength comes from extensive synthetic plant growth regulator usage in greenhouse tomato and cucumber production in Turkey and Morocco, where controlled environments allow accurate application timing and dosage management.

Grains and cereals form a significant but moderately growing segment, with synthetic plant growth regulators primarily used for lodging prevention in wheat and tiller enhancement in rice across Egypt's Nile Delta. In commercial crops, cotton and sugarcane producers apply these regulators to enhance fiber quality and control harvest timing, particularly in Sudan's cotton regions and Egypt's sugarcane areas, where export standards drive implementation. The pulses and oilseeds segment focuses on pod development and harvest uniformity, essential for mechanized farming operations in Ethiopia's commercial agriculture zones. The turf and ornamental grass segment serves landscaping and golf course maintenance in Gulf countries, where synthetic plant growth regulators help maintain grass quality in high-temperature conditions.

By Formulation: Solutions Dominate While Water-Soluble Granules Gain Ground

Solutions formulations held 43.7% of the Middle East and Africa plant growth regulators market share in 2024. This dominance stems from their ease of application through existing spray equipment and rapid plant uptake characteristics. These features align well with the region's intensive production systems and time-sensitive application windows. The solutions segment's strong position reflects its practical advantages in foliar application and fertigation systems, which are increasingly common in protected cultivation and precision agriculture operations across the Middle East and Africa.

Water-soluble granules are experiencing the fastest growth at 11.2% CAGR through 2030. This growth is driven by their controlled-release applications and reduced application frequency, which suits extensive farming operations and areas with limited labor availability. Wettable powders maintain a stable market position due to their cost advantages and extended shelf life, making them suitable for distribution networks in remote areas with challenging storage conditions and slow product turnover. Other formulations, including emulsions, soluble powders, and gel formulations, serve specialized applications where specific release characteristics or application methods offer distinct advantages.

Geography Analysis

Africa held 57.1% of the Middle East and Africa plant growth regulators market share in 2024. Nigeria's government-supported contract farming initiatives incorporate cytokinin sprays across two million hectares of smallholder programs. The South African Health Products Regulatory Authority facilitates efficient new product registrations, creating market competition that reduces prices and increases product availability. Kenya's streamlined low-residue approval process complements European phytosanitary standards, enabling exporters to earn premium prices without significant cold-chain investments. Ethiopia's coffee and floriculture sectors implement specialized auxin protocols to enhance quality metrics and boost foreign exchange revenue.

The Middle East segment projects a 9.7% CAGR through 2030. The United Arab Emirates' greenhouse facilities, supported by the Environment Agency Abu Dhabi, demonstrate 40% water conservation through integrated gibberellin applications. Saudi Arabia's Vision 2030 initiative utilizes King Abdullah University of Science and Technology research to expand controlled-environment agriculture, achieving 35% higher tomato yields in the same land area. Turkey serves as a continental trade hub, with 12-month regulatory processes accelerating market access for its greenhouse export operations.

North Africa combines its proximity to Mediterranean export markets with desert agriculture development. Morocco's OCP fertilizer initiative integrates with specialized cytokinin programs for saline soil conditions, creating comprehensive input solutions that enhance farmer adoption. In 2024, Egypt's Toshka project implemented gibberellin applications to enhance crop establishment, supporting regional food security and reducing per-hectare input costs through scale efficiencies. The East African Community's cross-border cooperation aligns label requirements and residue standards, facilitating regional trade and promoting shared agricultural practices across member economies.

Competitive Landscape

The Middle East and Africa plant growth regulators market shows moderate concentration, with BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, and UPL Limited holding the majority market share in 2024. BASF SE maintains market leadership through its comprehensive portfolio of cytokinin, auxin, and gibberellin products, supported by digital agronomy tools for spray timing and weather risk assessment. Bayer AG integrates seed-chemistry platforms, combining hormonal treatments with stress-tolerant genetics. Syngenta Group maintains a strong protected-cultivation presence through greenhouse advisory services featuring proprietary gibberellin blends.

Multinational companies are establishing local production facilities in South Africa, Egypt, and Turkey to reduce import tariffs and manage currency fluctuations. These facilities formulate concentrates specific to regional water chemistry, reducing freight lead times by up to six weeks. Regional companies like ZAGRO Africa are expanding their distribution networks across East Africa, competing through local presence and efficient registration processes for niche active ingredients. Companies are incorporating sensors and modeling software into their products, demonstrating yield improvements of thousands of dollars per hectare through field trials.

In 2023, Abu Dhabi National Oil Company (ADNOC) acquired Fertiglobe for USD 3.62 billion, integrating hormone distribution with nitrogen-fertilizer sales networks and enabling combined nutrient-and-regulator packages. Technology companies, such as ReNile, are securing venture capital to combine IoT monitoring with hormone dosing schedules, thereby expanding competition beyond chemical products into data-driven crop management. Market leadership is increasingly determined by service quality, regulatory expertise, and anti-counterfeiting measures rather than product offerings alone.

Middle East And Africa Plant Growth Regulators Industry Leaders

BASF SE

Bayer AG

Syngenta Group

Corteva Agriscience

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: UPL Limited received notification regarding the incorporation of a new step-down subsidiary, UPL Agricultural Product Trading FZE, in Dubai, United Arab Emirates. The subsidiary will focus on agricultural trading and chemical fertilizer trading, including plant growth regulators.

- September 2023: Syngenta introduced its "NoMow" plant growth regulator (PGR) in South Africa. The product helps turf professionals reduce mowing frequency, improve turf quality, and manage turf maintenance costs efficiently.

Middle East And Africa Plant Growth Regulators Market Report Scope

Plant growth regulators (PGRs) are chemicals used to modify plant growth such as increasing branching, suppressing shoot growth, increasing return bloom, removing excess fruit, or altering fruit maturity. The Middle East & Africa Plant Growth Regulators Market is segmented by Product Type (Cytokinin, Auxin, Gibberellin, and Other Types), Application (Crop-based and Non-crop-based), and Geography (South Africa, Nigeria, Tanzania, Uganda, Cameroon, Congo, and the Rest of Africa) and (Iran Turkey, Iraq, Yemen, Egypt, and Rest of Middle East). The report offers market size and forecasts for the market in terms of value (USD) for all the above segments.

By Product Type

| Cytokinin |

| Auxin |

| Gibberellin |

| Ethylene |

| Brassinosteroids |

| Other Types (Abscisic Acid, Ethephon, etc.) |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamental Grass |

| Other Application (Forage and Fodder Crops, Floriculture, etc.) |

By Formulation

| Water-Soluble Granules |

| Solutions |

| Wettable Powders |

| Others (Emulsion, Soluble Powder, Dustable Powder, Oil Dispersion, Gel Formulation, etc.) |

By Geography

| Africa | Nigeria |

| Tanzania | |

| Uganda | |

| South Africa | |

| Kenya | |

| Ethiopia | |

| Rest of Africa | |

| Middle East | Turkey |

| United Arab Emirates | |

| Saudi Arabia | |

| Egypt | |

| Israel | |

| Rest of Middle East |

| By Product Type | Cytokinin | |

| Auxin | ||

| Gibberellin | ||

| Ethylene | ||

| Brassinosteroids | ||

| Other Types (Abscisic Acid, Ethephon, etc.) | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Crops | ||

| Turf and Ornamental Grass | ||

| Other Application (Forage and Fodder Crops, Floriculture, etc.) | ||

| By Formulation | Water-Soluble Granules | |

| Solutions | ||

| Wettable Powders | ||

| Others (Emulsion, Soluble Powder, Dustable Powder, Oil Dispersion, Gel Formulation, etc.) | ||

| By Geography | Africa | Nigeria |

| Tanzania | ||

| Uganda | ||

| South Africa | ||

| Kenya | ||

| Ethiopia | ||

| Rest of Africa | ||

| Middle East | Turkey | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| Egypt | ||

| Israel | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa plant growth regulators market by 2030?

It is forecast to reach USD 393.81 million, expanding at a 7.04% CAGR from 2025.

Which product type currently commands the largest share?

Cytokinin accounts for 36.2% of the projected 2024 revenue, driven by its versatility in breaking dormancy and extending shelf life.

Which formulation is growing fastest?

Water-soluble granules post the highest 11.2% CAGR due to controlled-release features that cut application frequency.

Why is the Middle East region outpacing Africa in growth rate?

Government-backed desert agriculture projects and large-scale greenhouse investments push Middle East CAGR to 9.7%.

How concentrated is supplier power in this field?

The top five companies hold the majority revenue share, indicating moderate consolidation and room for regional players.

Page last updated on: