Australia Plant Growth Regulators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

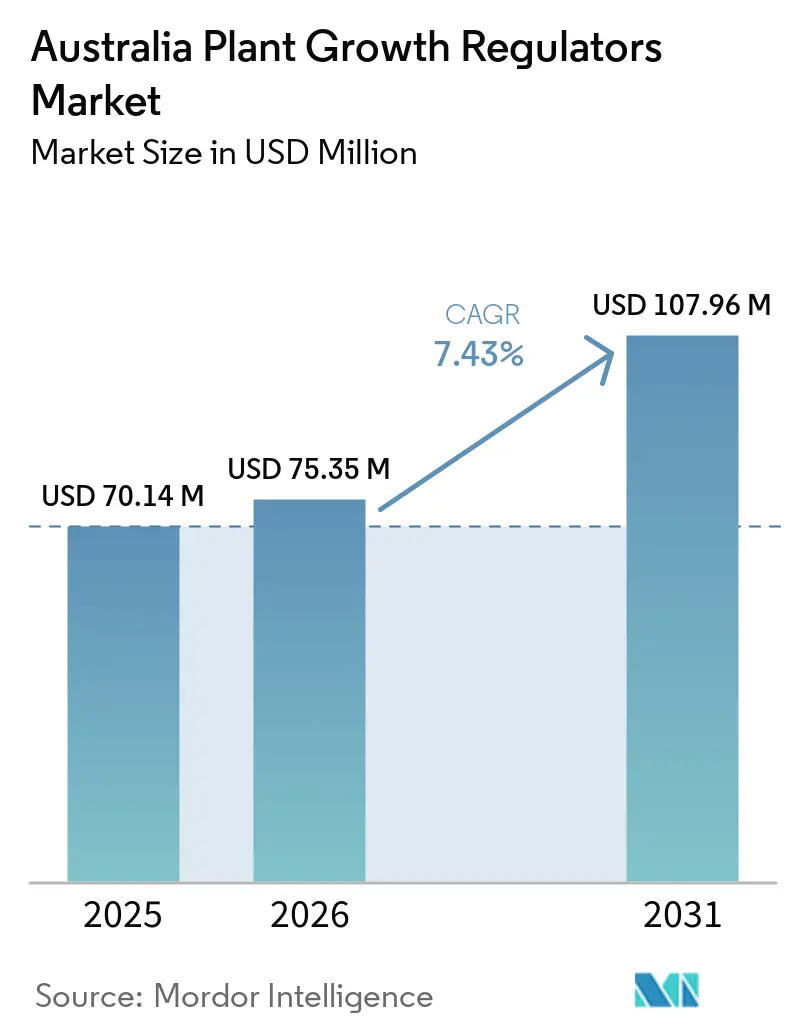

| Base Year Market Size (2025) | USD 70.14 Million |

| Market Size (2026) | USD 75.35 Million |

| Market Size (2031) | USD 107.96 Million |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

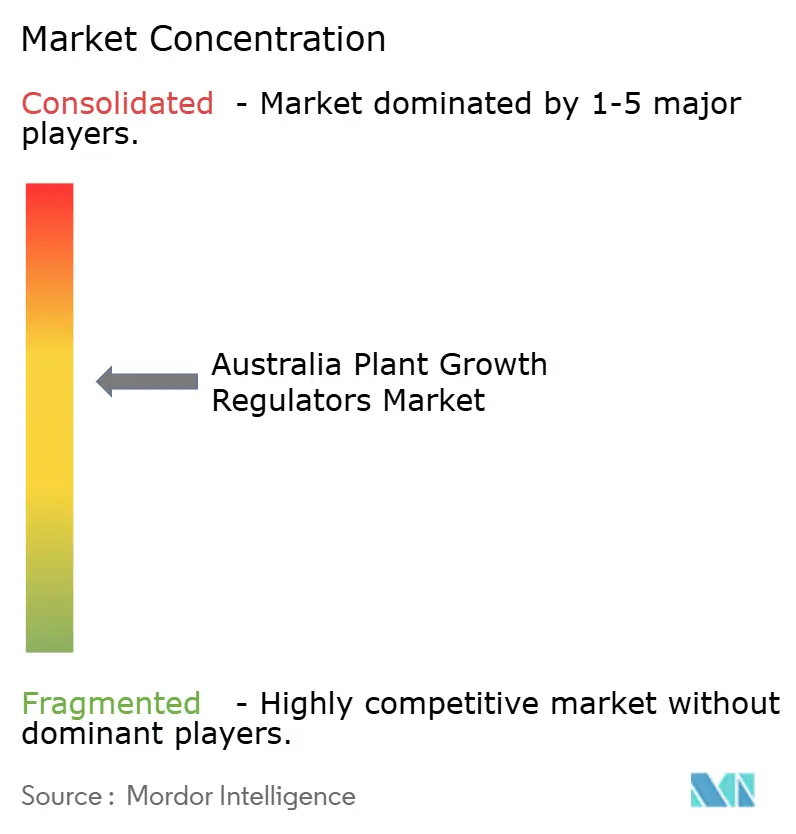

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Plant Growth Regulators Market Analysis by Mordor Intelligence

The Australia plant growth regulators market size is projected to grow from USD 70.14 million in 2025 to USD 75.35 million in 2026 and is forecast to reach USD 107.96 million by 2031 at 7.43% CAGR over 2026-2031. The market is being shaped by 3 distinct demand streams: orchard hormone management for premium fruit quality, lodging control in high-input cereals, and canopy control in irrigated cotton. Product availability is widening as the Australian Pesticides and Veterinary Medicines Authority continues to register new labels and approve product variations across turf, cereal, and horticultural uses in 2024 and 2025. Official crop data also support steady demand, with orange production forecast at 590,000 metric tons and mandarin and tangerine production forecast at 270,000 metric tons in 2025-26, while Australian fruit output reached 2.8 million metric tons in 2023-24[1]Source: Zeljko Biki, “Citrus Annual,” United States Department of Agriculture Foreign Agricultural Service, apps.fas.usda.gov. The market also benefits from stronger agronomic targeting, because growers are more likely to use regulators where yield potential and crop value are high enough to justify precise applications, while the same factor limits adoption in low-return paddocks. Competition remains moderate, and portfolio depth, label coverage, and regulatory durability matter more in the Australia plant growth regulators market than simple price competition alone.

Key Report Takeaways

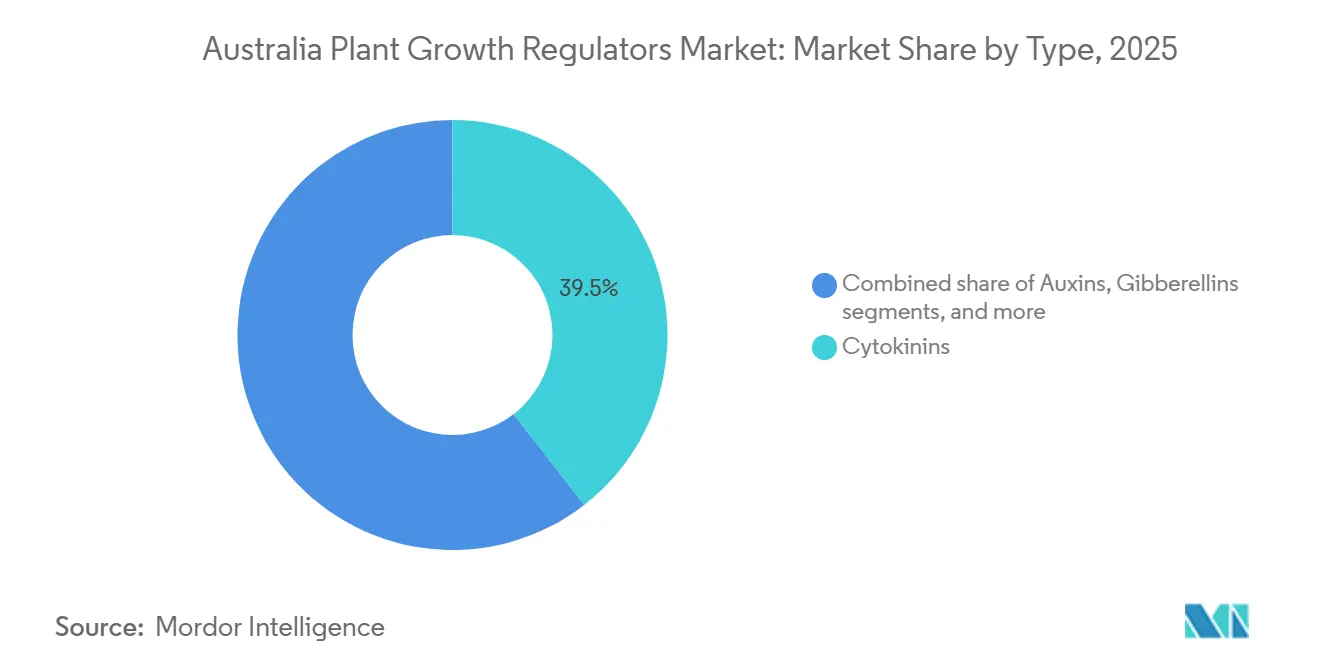

- By type, Cytokinins held 39.5% of Australia plant growth regulators market share in 2025, while Auxins will be the fastest segment and are forecast to advance at a 9.4% CAGR during 2026-2031.

- By application, Cereals and Grains accounted for 36.6% share of the Australia plant growth regulators market size in 2025, while Fruits and Vegetables are the fastest segment at a 10.3% CAGR during 2026-2031.

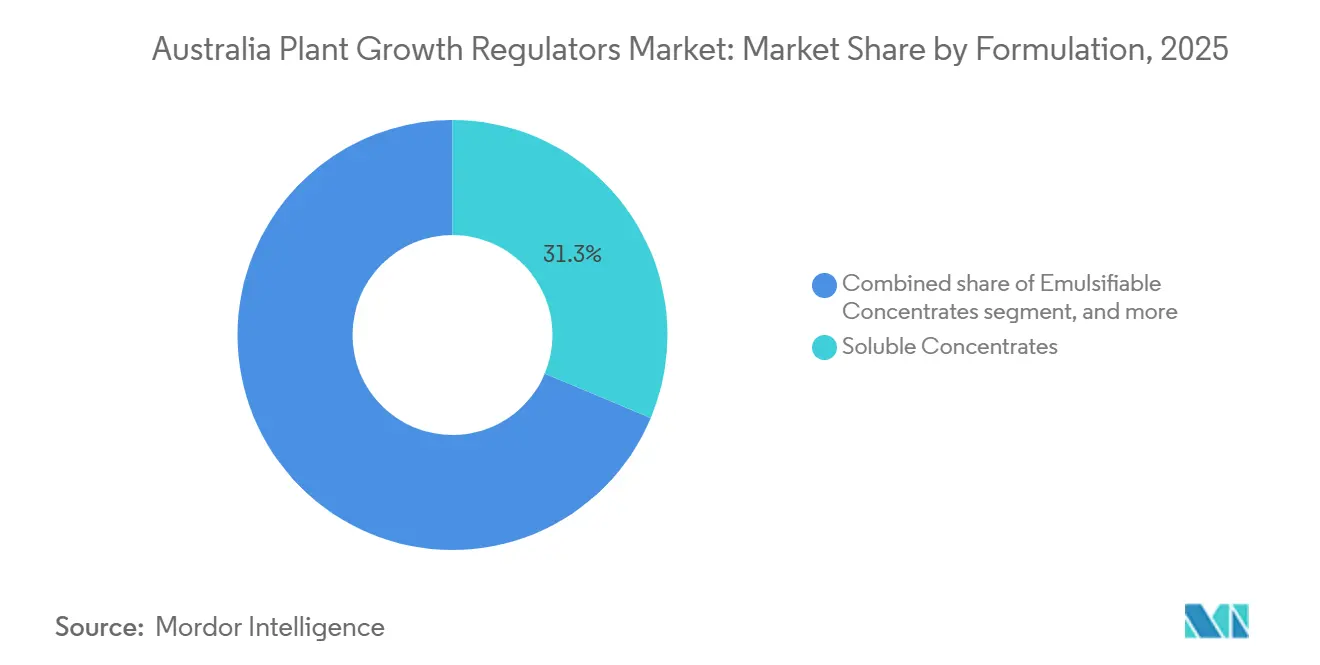

- By formulation, Soluble Concentrates led with a 31.3% share of the Australia plant growth regulators market size in 2025, while Water-Dispersible Granules are anticipated to be the fastest-growing segment at a 9.8% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Plant Growth Regulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orchard Pack-Out and Export-Grade Fruit Quality Targets | +1.80% | Strongest across Victoria, New South Wales, South Australia, and Tasmania export horticulture regions. | Medium term (2-4 years) |

| Lodging-Control Demand in High-Yield Barley and Irrigated Wheat | +1.50% | Most relevant in Western Australia, South Australia, Victoria, and southern New South Wales grain belts. | Short term (≤ 2 years) |

| Cotton Canopy Management for Boll Retention and Machine Harvest Efficiency | +1.20% | Concentrated in Queensland and New South Wales cotton-growing regions. | Medium term (2-4 years) |

| Precision Spraying and Data-Led Application Programs | +1.00% | Faster adoption across Queensland, New South Wales, and Victoria commercial farming systems. | Medium term (2-4 years) |

| Warm-Winter Chill Shortfalls Boosting Dormancy-Break Programs | +0.80% | Highest relevance in South Australia, Victoria, and New South Wales fruit-growing regions. | Long term (≥ 4 years) |

| Orchard Labor Scarcity Favoring Chemical Thinning and Harvest-Timing Tools | +0.70% | Higher impact across New South Wales, Victoria, and Queensland orchard systems. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Orchard Pack-Out and Export-Grade Fruit Quality Targets

The demand for plant growth regulators in Australian orchard systems, where fruit size, finish, timing, and uniformity directly affect commercial returns. Orange production is forecast at 590,000 metric tons in 2025-26, and mandarin and tangerine production is forecast at a record 270,000 metric tons, which keeps hormonal crop management relevant across export-facing citrus programs. Australia also exported 141,100 metric tons of table grapes in 2024-25, which reinforces the need for uniform pack-out and compliant harvest quality in premium fruit supply chains [2]Source: Zeljko Biki, “Fresh Deciduous Fruit Annual,” United States Department of Agriculture Foreign Agricultural Service, apps.fas.usda.gov. Apple and Pear Australia Limited reported commercial thinning trials in Tasmania that used metamitron, 6-benzyladenine, and ammonium thiosulfate to improve crop load management, reduce hand thinning, and support return bloom and fruit quality. That keeps the Australia plant growth regulators market closely tied to orchard revenue quality rather than planted area alone.

Lodging-Control Demand in High-Yield Barley and Irrigated Wheat

The market benefits when cereal paddocks move into stronger yield conditions and lodging risk rises. Grains Research and Development Corporation trial results showed that trinexapac-ethyl delivered the strongest responses in barley environments above 6 metric tons per hectare, and the most responsive variety posted yield gains of 0.70 to 0.80 metric tons per hectare and partial gross margin gains of USD 191.8 per hectare (AUD 295.0 per hectare). The same work showed that ethephon often reduced partial gross margins, especially outside the strongest lodging-prone settings, which makes agronomic targeting essential rather than optional. The Grains Research and Development Corporation also started its FAR2403-002SAX benchmarking program in April 2024, and it runs to July 2027, extending best-practice work for high-yield wheat and barley systems across major southern growing zones[3]Source: “Hyper Profitable Crops - Cereal Paddock Benchmarking and Innovation Groups,” Grains Research and Development Corporation, grdc.com.au. This improves commercial confidence in the Australia plant growth regulators market whenever seasonal yield potential supports a clear return.

Cotton Canopy Management for Boll Retention and Machine Harvest Efficiency

Cotton remains one of the most intensive use areas in Australia for plant growth regulators on a per-hectare basis. Peer-reviewed evidence showed that more than 90% of cotton acreage in Australia and the United States typically uses 1 or more chemical harvest aids, including thidiazuron, diuron, and ethephon, to support machine harvest and crop finish. Cotton Seed Distributors also reported that research across sites from southern New South Wales to the Darling Downs found that early, low-rate mepiquat chloride applications may lift yield under some conditions, although site response varied. Its XtendFlex research program in Gwydir and the Darling Downs is building a more systematic dataset on canopy growth, maturity, and yield response using drone-applied treatments and aerial monitoring. This keeps cotton as a durable driver of the plant growth regulators industry in Australia, as plant architecture and harvest timing both affect returns.

Precision Spraying and Data-Led Application Programs

Australia is also moving toward improved application efficiency and more precise within-field targeting. The weedSAT program, backed by the Grains Research and Development Corporation, achieved 94% positive weed-detection accuracy in research paddocks and moved toward limited release in August 2025, with full commercial Green on Brown release targeted for January 2026. Although the platform is herbicide-led, the same operational shift matters for regulators because growers gain more confidence in variable-rate spray decisions once canopy mapping and digital field management become routine. This matters most in broadacre systems, where uneven seasonal outcomes and uncertainty about the optimal rate for each zone constrained past adoption. Better decision support does not remove agronomic risk, but it lowers the cost of getting PGR placement wrong. That supports a more disciplined adoption path for the plant growth regulators market in the country.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| APVMA Registration Costs and Crop-Label Limitations | -1.50% | National, with the strongest impact across specialty crop and non-food application markets. | Long term (≥ 4 years) |

| Weather-Sensitive Response and Inconsistent Payback in Dry Seasons | -1.20% | Most significant in Western Australia, South Australia, and dryland regions of New South Wales and Victoria. | Short term (≤ 2 years) |

| Export Residue Compliance Limiting Active Choice in Fresh Produce | -0.80% | Highest relevance across New South Wales, Victoria, South Australia, Queensland, and Western Australia export produce systems. | Medium term (2-4 years) |

| Minor-Use Permit Gaps in Specialty Crops and Pasture Applications | -0.50% | National, especially across specialty fruit, viticulture, turf, and pasture applications. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

APVMA Registration Costs and Crop-Label Limitations

The market faces a structural constraint from the cost and complexity of registration. The Australian Pesticides and Veterinary Medicines Authority (APVMA) Type 1 Major Agriculture pathway covers multiple stages, from pre-application assistance and submission through technical risk assessment, recommendation, finalization, and post-finalization support, making entry and expansion a resource-intensive process[4]Source: Australian Pesticides and Veterinary Medicines Authority, “Type 1 Major Agriculture - Registration of New Product, Approval of New Active,” Australian Pesticides and Veterinary Medicines Authority, apvma.gov.au. This burden is harder to justify for small crops, narrow labels, and non-core uses where sales volumes are limited. The Australian Wine Research Institute also reported that 2 ethephon 720 SL products and 1 chlormequat product ceased registration effective July 1, 2025, which shows that label attrition can remove options as well as add them. That leaves the market dependent on a smaller set of durable registrations in some specialty uses.

Weather-Sensitive Response and Inconsistent Payback in Dry Seasons

Seasonal volatility remains a clear brake on the use of plant growth regulators in dryland cropping systems. Grains Research and Development Corporation evidence showed that ethephon applications decreased partial gross margins in more than 80% of cases across the reported barley trial set, while positive responses were concentrated in stronger yielding and more lodging-prone environments. That means application timing and product choice matter, but seasonal yield potential matters even more. When moisture outlooks are weak, growers are less willing to commit extra input spend before returns are visible. This keeps demand in certain parts of Australia sensitive to rainfall patterns and paddock-by-paddock economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Orchard Premiumization Keeps Cytokinins in the Largest Position

Cytokinins held 39.5% of market revenue in 2025, making them the largest type segment in the Australian plant growth regulators market. Their position reflects heavy use in apple, pear, stone fruit, and table grape programs where thinning, sizing, return bloom, and fruit uniformity are critical commercial outcomes. Official data showed apple production reached 294,000 metric tons in 2023-24, with a farm-gate value of USD 442.1 million (AUD 680.2 million), while table grape exports reached 141,100 metric tons in 2024-25. Apple and Pear Australia Limited reported that commercial orchard trials used 6-benzyladenine alongside metamitron and ammonium thiosulfate, which supports the central role of cytokinin-based thinning systems in premium fruit management. In practical terms, the industry gives cytokinins a revenue advantage because demand rises with fruit value and export discipline, not only with orchard area.

Auxins are the fastest-growing segment and are forecast to expand at a 9.4% CAGR during 2026-2031 in the Australian plant growth regulators market. Their growth path is supported by uses in pre-harvest drop prevention, chemical thinning, root development, and citrus and tropical fruit programs, all of which fit better with rising orchard intensity. Apple and Pear Australia Limited also noted that the industry is evaluating 1-aminocyclopropane-1-carboxylic acid for future thinning, which signals continued room for new hormonal options within orchard management programs. Gibberellins remain important because they serve fruit-sizing and related crop-management roles across several horticultural systems. Other types, including ethylene-related and growth-retardant products, continue to support cotton, cereal, turf, and specialty programs, keeping the Australian plant growth regulators industry broad rather than single-crop-dependent.

By Application: Broadacre Volume Keeps Cereals and Grains the Largest Use Case

Cereals and Grains held 36.6% of the Australia plant growth regulators market size in 2025, making this the largest application segment. The segment builds on established use of trinexapac-ethyl and ethephon in barley and wheat systems where lodging control matters most. Grains Research and Development Corporation evidence showed that the best responses came in higher-yielding, lodging-prone barley environments, which explains why adoption is concentrated in stronger agronomic settings rather than across every paddock. The same evidence showed that poorly targeted ethephon use can reduce returns, which keeps the segment tied to seasonal selectivity and agronomic discipline. That balance keeps cereals large in the industry because the area base is wide, even when per-hectare use is uneven.

Fruits and Vegetables are the fastest application segment and are forecast to grow at a 10.3% CAGR during 2026-2031. Australia produced 2.8 million metric tons of fruit in 2023-24, valued at USD 4.42 billion (AUD 6.80 billion), demonstrating the scale of high-value horticulture exposed to thinning, sizing, and harvest-timing programs. Citrus fundamentals are also strong, with orange production forecast at 590,000 metric tons and mandarin and tangerine output forecast at 270,000 metric tons in 2025-26. The non-crop segment remains smaller, but the August 2025 registration of Farmalinx Ego Plant Growth Regulator for seedhead suppression and growth control in bahia and kikuyu grasses shows that label development continues outside mainstream crop uses. This mix gives the plant growth regulators industry in Australia both broadacre stability and faster horticultural upside.

By Formulation: Soluble Concentrates Stay the Largest While Granules Gain Pace

Soluble Concentrates held 31.3% of the Australia plant growth regulators market share in 2025, making them the largest formulation segment. Their lead reflects the installed base of liquid products that fit existing orchard, cereal, cotton, and turf spray systems. The July 2025 variation for Potus Yield and Quality Enhancer, a 250 g/L trinexapac-ethyl product, extended the pack-size range from 1 liter to 1,000 liters and showed active commercial support for scalable soluble formats. The June 2025 variation for Gala Growth Regulator also confirmed continuing maintenance of registered gibberellic acid liquid products in Australia. This keeps liquid formulations central to the market because they align with current farm handling and spray practices.

Water-Dispersible Granules are the fastest formulation segment and are forecast to expand at a 9.8% CAGR during 2026-2031. Their appeal is linked to safer handling, better storage practicality, and a closer fit with precision spray workflows where dose control matters more. This direction is consistent with the broader movement toward data-led application programs already visible in Australian broadacre systems. Emulsifiable and suspension concentrates still serve specialized roles in cotton and orchard programs where penetration, coverage, or active stability remain important. Other formulations remain relevant for niche horticultural uses, but the overall mix shows how the industry is balancing installed-product habits with newer, precision-oriented preferences.

Geography Analysis

New South Wales is the largest state market in the Australia plant growth regulators market because it combines cotton, irrigated cereals, pome fruit, citrus, and table grapes within a broad commercial crop base. Victoria also holds a major position because its pome, stone, and grape systems use gibberellin and cytokinin programs as routine crop management tools in premium horticulture. Official figures showed Australian fruit production reached 2.8 million metric tons in 2023-24, with a local value of USD 4.4 billion (AUD 6.8 billion), underscoring the importance of the eastern horticulture states to national demand. Apple output alone reached 294,000 metric tons in 2023-24, and that volume remains highly relevant for orchard thinning and sizing chemistry in New South Wales and Victoria. These states are the core of plant growth regulators usage in Australia because they combine high-value fruit intensity with diversified field crop exposure.

Queensland is the fastest-growing major state market, bringing together irrigated cotton, tropical fruit, and diversified horticulture. Official horticulture data showed bananas reached 369,000 metric tons and macadamias reached 58,000 metric tons in 2023-24, confirming the scale of crop systems where hormonal management already matters or can expand further. Queensland also benefits from cotton research activity, with the XtendFlex mepiquat chloride project running across Gwydir and Darling Downs and building more current response data for commercial decisions. Tasmania remains smaller in area, but it has strong value density because commercial apple thinning programs are being tested there under the coordination of Apple and Pear Australia Limited. The Northern Territory remains small, but it offers a gradual expansion path, with cotton and tropical rotations widening the future addressable base.

Western Australia and South Australia remain important to the industry, even though their demand mix differs from that of the east coast. Western Australia matters mainly through cereals, where uptake depends on whether paddocks reach the yield and lodging conditions that justify regulator use, while South Australia combines cereals with citrus and viticulture. Export compliance adds another layer across these states because the top 5 destinations accounted for 72% of Australia’s orange exports in 2024-25, underscoring the importance of residue management across all export-facing regions. The Australian Capital Territory contributes very little because its commercial crop footprint is limited. Overall, state performance in the plant growth regulators market in Australia is strongest where crop value, export discipline, and agronomic fit converge in the same growing regions.

Competitive Landscape

The Australia plant growth regulators market is led by a group of multinational registrants with deeper portfolios and stronger regulatory standing. Sumitomo Chemical Company, Limited, BASF SE, Syngenta Group Co., Ltd., Corteva Agriscience, and Imtrade Australia Pty Ltd remain the key players in the competition. Their advantage comes from broader crop coverage across cereals, horticulture, cotton, and specialty uses, where a deeper label base reduces dependence on any 1 crop cycle. Domestic formulators and generic importers still matter because broadacre users remain price-sensitive, and some specialty segments can be served through narrower, local portfolios. This keeps the industry competitive, but not fragmented enough to remove the strategic advantage held by large registrants.

Recent moves show that market competition is being shaped by portfolio expansion and label maintenance rather than by price alone. Corteva Agriscience integrated Stoller Australia into its business effective January 1, 2025, bringing Bio-Forge, Stimulate, and Sett into a broader platform of biological and traditional crop protection solutions. Nutrien Ag Solutions Limited also added Genfarm Ethephon 900 SL Growth Regulator in November 2024, with approved uses across anti-lodging barley, crop thinning, ripening, and cotton boll opening and defoliation. Crop Culture Pty Ltd expanded the commercial flexibility of Potus Yield and Quality Enhancer in July 2025 by extending pack sizes up to 1,000 liters for trinexapac-ethyl users. Farmalinx Pty Ltd also gained a fresh turf-oriented label for Farmalinx Ego Plant Growth Regulator in August 2025, showing that selective label growth continues in niche applications.

Barriers to entry remain significant in the market because regulatory approval is technical, slow, and expensive. The Australian Pesticides and Veterinary Medicines Authority Type 1 pathway itself shows the level of process depth required before a product gains or expands access. At the same time, registration cancellation can weaken smaller portfolios, as seen in the 2025 loss of selected ethephon and chlormequat labels reported by the Australian Wine Research Institute. That favors companies with wider data packages, more stable Australian registrations, and better crop diversification. For this reason, the Australia plant growth regulators market is likely to remain led by established players, even as smaller suppliers continue to compete in narrower, price-sensitive pockets.

Australia Plant Growth Regulators Industry Leaders

Sumitomo Chemical Company, Limited

BASF SE

Syngenta Group Co., Ltd.

Corteva Agriscience

Imtrade Australia Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Elders Limited completed its acquisition of Delta Agribusiness for approximately USD 289.0 million (AUD 445.0 million), adding 62 retail stores and the Four Seasons Agribusiness proprietary label holding 106 registered Australian pesticide and veterinary products, the ACCC required divestiture of 6 Western Australian branches as a condition of approval, and the combined retail network now exceeds 300 locations nationally, materially concentrating distribution scale for plant growth regulators suppliers.

- March 2025: Case IH launched SenseApply precision spray technology in Australia for crop protection chemicals and fertilizers, including plant growth regulator variable-rate application as a live application function. This is the first major original-equipment manufacturer-level integration of plant growth regulators variable-rate dosing in Australian broadacre machinery and signals a shift toward data-driven PGR program management.

- January 2025: Corteva Agriscience completed the integration of Stoller Australia into a new Plant Performance segment, combining Stoller’s plant physiology and biological crop nutrition portfolio with Corteva’s crop protection platform. The integration created a combined biological and conventional plant growth regulator offering for Australian growers.

Australia Plant Growth Regulators Market Report Scope

Plant growth regulators in Australia are crop management products that modify plant physiological processes such as thinning, sizing, canopy control, lodging reduction, dormancy management, ripening, and defoliation. The Australia Plant Growth Regulators Market is Segmented by Type (Cytokinins, Auxins, Gibberellins, and Other Types), by Application (Crop-based and Non-crop-based), and by Formulation (Soluble Concentrates, Emulsifiable Concentrates, Suspension Concentrates, Water-Dispersible Granules, Other Formulations). The Market Forecasts are Provided in Terms of Value (USD).

| Cytokinins |

| Auxins |

| Gibberellins |

| Other Types |

| Crop-based | Grains and Cereals |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Turf and Ornamentals | |

| Other Crops | |

| Non-crop-based | Turf and Ornamental Grass |

| Other Applications |

| Soluble Concentrates |

| Emulsifiable Concentrates |

| Suspension Concentrates |

| Water-Dispersible Granules |

| Other Formulations |

| By Type | Cytokinins | |

| Auxins | ||

| Gibberellins | ||

| Other Types | ||

| By Application | Crop-based | Grains and Cereals |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| Other Crops | ||

| Non-crop-based | Turf and Ornamental Grass | |

| Other Applications | ||

| By Formulation | Soluble Concentrates | |

| Emulsifiable Concentrates | ||

| Suspension Concentrates | ||

| Water-Dispersible Granules | ||

| Other Formulations | ||

Key Questions Answered in the Report

What is the market size of the Australia plant growth regulators market in 2026, and what is its projected size by 2031?

The Australia plant growth regulators market stands at USD 75.35 million in 2026 and is projected to reach USD 107.96 million by 2031, growing at a 7.43% CAGR during 2026-2031.

Which type segment is the largest in Australia?

Cytokinins are the largest type segment, with 39.5% revenue share in 2025, supported by strong use in apple, pear, stone fruit, and table grape programs.

Which application area is growing the fastest?

Fruits and Vegetables are the fastest application segment, with a forecast CAGR of 10.3% during 2026-2031 as orchard intensity and export-quality requirements keep rising.

Why do cereals still account for the largest use share?

Cereals and Grains held 36.6% of revenue in 2025 because barley and wheat systems still provide a wide treated area, especially where lodging risk is high and yields justify regulator use.

What is limiting wider adoption across Australia?

Adoption is held back by registration cost, label limits, residue compliance, and weather-sensitive returns, especially in dryland systems where lower-yield conditions can weaken payback

Which states are most important for demand?

New South Wales is the largest state market, while Queensland is the fastest-growing major state market because it combines cotton, tropical fruit, and diversified horticulture with expanding use cases.

Page last updated on: