Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

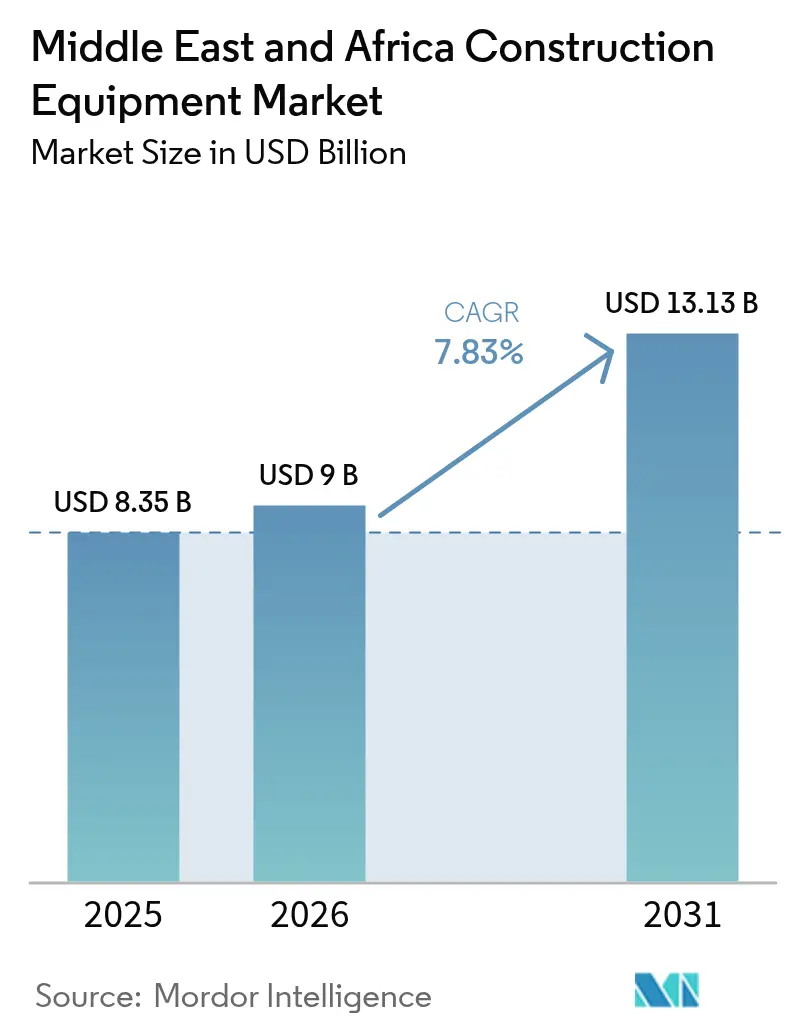

| Base Year Market Size (2025) | USD 8.35 Billion |

| Market Size (2026) | USD 9 Billion |

| Market Size (2031) | USD 13.13 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Construction Equipment Market Analysis by Mordor Intelligence

The Middle East and Africa Construction Equipment Market size was valued at USD 8.35 billion in 2025 and is estimated to grow from USD 9 billion in 2026 to reach USD 13.13 billion by 2031, at a CAGR of 7.83% during the forecast period (2026-2031). Sovereign capital inflows into giga-projects across the Gulf Cooperation Council, rising rental penetration, and battery-mineral mining in sub-Saharan Africa are keeping fleet orders resilient despite oil-price swings. Excavators continue to dominate procurement because underground utility corridors, metro tunnels, and bulk-earthmoving all rely on the same base machine fitted with quick-change hydraulic tools. Diesel platforms still lead, yet electric and hybrid models are growing as zero-emission mandates spread from NEOM and Masdar City to secondary airports and housing projects. Compact loaders below 100 horsepower now outsell heavier classes in townships where roads average 4 meters wide, while contractors increasingly shift to pay-per-use contracts that shield balance sheets from residual-value risk.

Key Report Takeaways

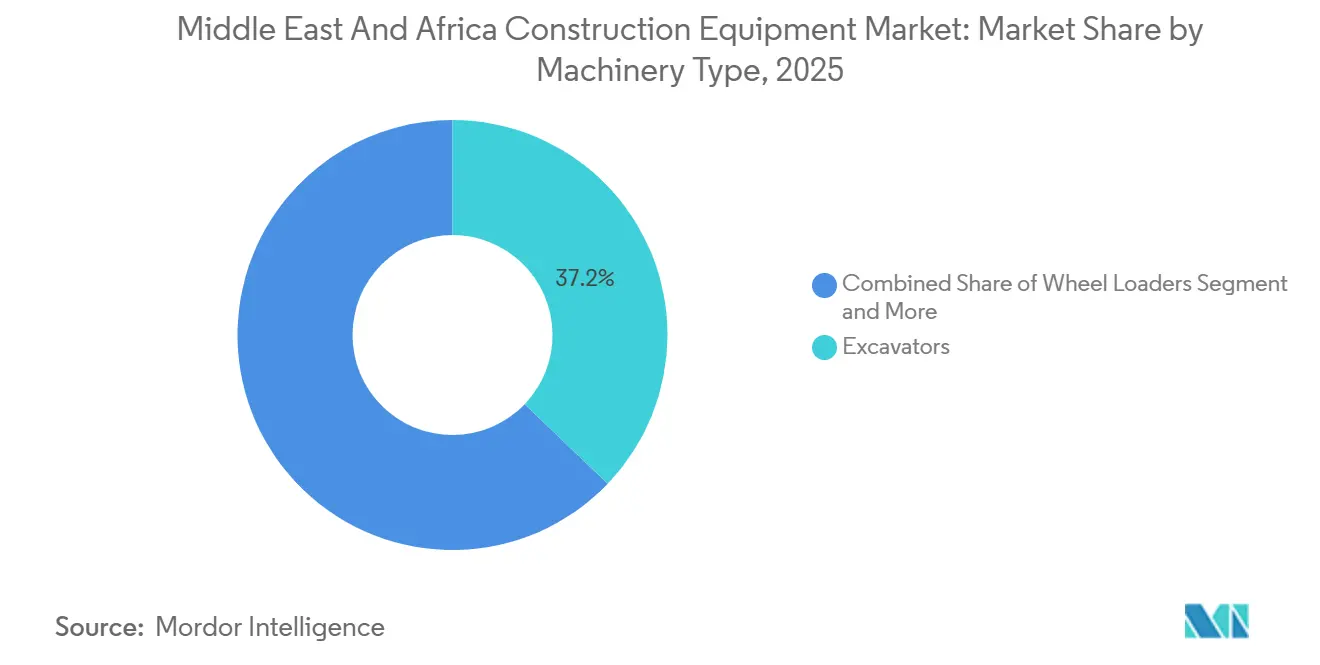

- By machinery type, excavators led with a 37.17% revenue share in 2025 and are projected to post the fastest 8.17% CAGR through 2031, reflecting persistent demand from giga-projects and corridor earthworks.

- By drive type, diesel platforms held 77.28% of 2025 sales, while electric and hybrid variants are advancing at a 7.91% CAGR on the back of zero-emission job-site mandates in NEOM and Masdar City.

- By power output, equipment rated at or below 100 horsepower accounted for 44.28% of 2025 demand and is also the fastest-growing segment, registering an 8.13% CAGR, as African township housing favors compact loaders.

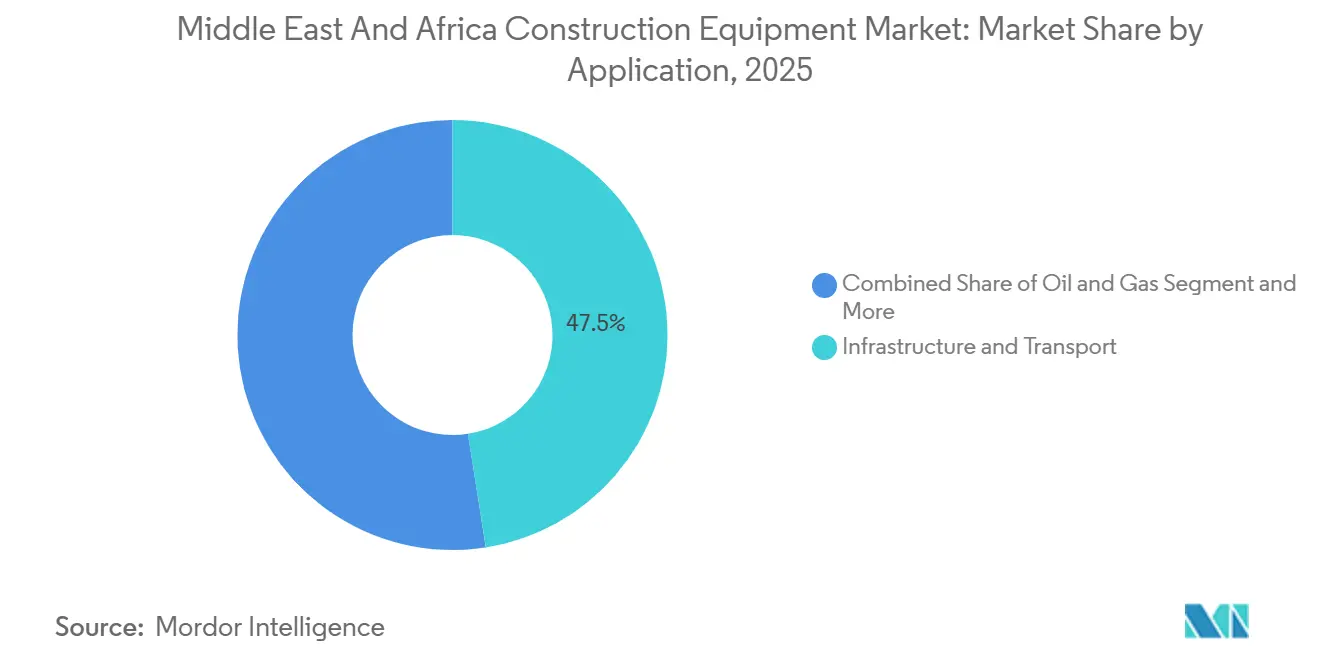

- By application, infrastructure and transport commanded 47.53% of 2025 turnover, whereas oil and gas construction is forecast to grow at an 8.06% CAGR through 2031, buoyed by refinery and petrochemical megaprojects in Kuwait and Oman.

- By end-user, contractors represented 48.74% of 2025 spending, while equipment rental companies are projected to record the highest 8.9% CAGR as asset-light models gain traction across the Gulf.

- By geography, Saudi Arabia accounted for 27.63% of regional revenue in 2025. Yet Qatar is set to be the fastest-growing country, with an 8.15% CAGR, driven by Lusail City and Doha Metro extensions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC Mega-Projects Pipeline | +2.1% | Saudi Arabia, UAE, Qatar, Oman, Bahrain | Medium term (2-4 years) |

| Region-Wide Shift From Ownership to Rental | +1.8% | Saudi Arabia, UAE, Qatar, South Africa | Short term (≤ 2 years) |

| Rapid Urban Housing Programs Across Africa | +1.5% | Egypt, Nigeria, Kenya, South Africa, Ethiopia | Long term (≥ 4 years) |

| Battery-Mineral Mining Equipment Needs | +1.4% | DRC, Zimbabwe, Namibia, Zambia | Long term (≥ 4 years) |

| Local-Content Rules Spur OEM–JV Assembly | +1.2% | Saudi Arabia, UAE, Oman | Medium term (2-4 years) |

| Telematics-as-a-Service Adoption | +0.9% | GCC deserts, North African mining belts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GCC Mega-Projects Pipeline Accelerates Equipment Demand

Saudi Arabia, the UAE, Qatar, and Oman have pre-approved multi-year transport and tourism corridors that collectively need more excavators, wheel loaders, and cranes between 2025 and 2030 [1]“National Giga-Project Portfolio,”, Saudi Ministry of Investment, invest.sa. Locked-in treasury allocations shield these projects from seasonal fluctuations in crude prices, thereby enhancing the predictability of dealers' order books. At desert sites where ambient temperatures exceed a critical threshold, OEMs are mandated to provide fortified cooling systems. Furthermore, tender documents now stipulate ISO 9001 procedures for rental fleets. Port expansions in Duqm and Hamad are set to drive significant demand for articulated dump trucks, extending demand beyond conventional oil-and-gas cycles. Together, these contracts bolster long-term visibility for the construction equipment market in the Middle East and Africa.

Region-Wide Shift From Ownership To Rental Models

Rental penetration increased significantly as contractors sought to avoid idle equipment during fluctuations in oil prices. The largest lessor in Saudi Arabia expanded its fleet by adding electric and hybrid units, aligning with the push towards zero-emission zones. Meanwhile, a prominent marine contractor in the UAE transitioned a significant portion of its procurement to rentals, achieving a notable reduction in total cost of ownership. In South Africa, engineering firms are now leasing compact loaders to navigate currency fluctuations. Looking ahead, Qatari rental revenue is projected to grow steadily. In response to these market dynamics, OEMs are rolling out pay-per-use programs, emphasizing uptime guarantees, and positioning service quality as the key differentiator in the construction equipment landscape of the Middle East and Africa.

Rapid Urban Housing Programmes Across Africa

Egypt, Kenya, Nigeria, South Africa, and Ethiopia have set ambitious housing targets, each aiming for multi-million-unit goals. These targets place a premium on compact excavators and backhoe loaders, specifically those under 100 horsepower. Given the challenges of narrow township roads, inconsistent grid power, and sensitivity to fuel costs, there's a pronounced preference for fuel-efficient machines. In Ethiopia, funding delays have led to fewer scheduled starts. However, the overarching targets still indicate a robust demand for equipment well into the next decade. Moreover, compact equipment not only aligns with government employment objectives—creating more jobs per dollar spent—but also bolsters unit sales in the construction equipment market across the Middle East and Africa.

Local-Content Rules Driving Oem‐Local Jv Assembly Lines

Saudi Arabia's IKTVA and the UAE's ICV schemes mandate that suppliers achieve local value contributions at specific percentages. To qualify for public tenders, global OEMs are now assembling graders, cabs, and hydraulic cylinders in Dammam and Jebel Ali. A Chinese company inaugurated a plant in Riyadh that uses a significant percentage of Saudi steel. This strategic move allowed them to undercut imports, securing a substantial contract for Red Sea logistics. While these regulations promote skill transfer, they pose challenges for small component vendors seeking ISO 14001 certification[2]“ISO 9001 in Construction Equipment Rentals,”, ISO Secretariat, iso.org. This struggle leads to supply-chain bottlenecks, potentially delaying deliveries in the construction equipment markets of the Middle East and Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-Price Cyclicality | -1.9% | GCC core, oil-dependent economies | Short term (≤ 2 years) |

| Political and Security Hotspots Curb Project Execution | -1.4% | Sub-Saharan Africa, conflict zones | Medium term (2-4 years) |

| Port Congestion Delays Critical Spare-Parts Flow | -0.8% | Major ports: Durban, Chittagong, Red Sea routes | Short term (≤ 2 years) |

| Shortage Of Technicians | -0.6% | Global, acute in GCC and urban Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Cyclicality Defers Capex Decisions

In recent months, Saudi non-oil spending took a hit, falling sharply as Brent prices fell. Following suit, Kuwait delayed tenders worth a substantial amount, while Nigeria slashed its infrastructure budget by a notable percentage. Angola, too, made headlines by cutting its upstream plans, pushing back the acquisition of crawler cranes for its logistics hubs. Despite the UAE and Qatar's heavier reliance on sovereign funds, even Abu Dhabi chose to halt its mixed-use tower projects. In response, OEMs introduced lease-to-own packages and adjustable rental fees tied to project cash flows, providing a buffer against short-term revenue declines in the construction equipment market across the Middle East and Africa.

Political and Security Hotspots Curb Project Execution

In Sudan, armed conflict has halted major dam and highway projects, leaving numerous machines stranded in Port Sudan, awaiting parts. Meanwhile, unrest in Tigray, Ethiopia, has delayed turbine installations at the Grand Ethiopian Renaissance Dam. In the Democratic Republic of Congo, insurgencies have led miners to relocate several dump trucks to Uganda. Additionally, security costs for convoys in Cabo Delgado's LNG operations have surged, and projects along Kenya's Lamu corridor are significantly behind schedule. As a result of these conflicts, insurance premiums for fleets operating near these tensions have risen sharply. This surge in costs has pushed smaller contractors out of the market, leading to a consolidation of orders with multinational rental firms across the construction equipment sector in the Middle East and Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Maintain Versatility Advantage

Excavators accounted for 37.17% of 2025 revenue and are projected to grow at 8.17% to 2031. This share represents the largest slice of the Middle East and Africa construction equipment market and reflects the machine’s suitability for earthworks, demolition, and piling, without requiring fleet swaps. Wheel loaders face growth limitations due to the rising adoption of conveyors in quarries. While crawler cranes cater to the high-rise market, they occupy a niche. Compact handlers and skid-steers are expanding in African housing estates, particularly in areas with narrow roads. Motor graders and bulldozers account for a significant portion of the market, while pavers, rollers, dump trucks, and trenchers share the remaining market pie. In a notable trend, electrified mini-excavators are gaining traction in urban areas, highlighting a budding wave of electrification in the construction equipment market across the Middle East and Africa.

Original Equipment Manufacturers (OEMs) are now integrating quick-hitch couplers, enabling excavators to transition seamlessly from bucket to breaker. This innovation translates to significant savings for contractors, allowing them to operate with fewer machines per site. Additionally, drone-assisted grading is revolutionizing the process, reducing follow-up passes and cutting fuel consumption. As e-commerce hubs sprout near airports in Riyadh and Johannesburg, the demand for telescopic handlers in warehousing is on the rise. Collectively, these shifts reinforce excavators’ leadership in both revenue and the evolving Middle East and Africa construction equipment market share.

By Drive Type: Diesel Holds, Hybrids Gain

Diesel power retained 77.28% of 2025 turnover, a dominant share of the Middle East and Africa construction equipment market, due to its long range and fast refueling. Electric and hybrid variants grow at 7.91%, aided by zero-emission job-site mandates. Hydraulic drives, favored for demolition and sorting tasks, command a significant market share. While electric excavators grapple with limited shift durations near chargers due to battery runtime constraints, hybrid loaders alleviate fuel costs without the worry of range limitations. Hydrogen prototypes are still undergoing trials, with pilot refueling stations currently exclusive to South Africa’s Durban corridor.

Rental fleets are shifting their pricing strategy for electric machines, now charging by the kilowatt-hour consumed instead of traditional engine hours, thereby aligning costs more closely with energy consumption. In a move towards greener initiatives, GCC tenders now offer scoring credits for hybrid or electric drives under ISO 14001 compliance clauses, subtly steering contractors towards cleaner fleets. With the expansion of charging networks along Gulf highways, diesel's dominance is projected to decline. However, it is anticipated to maintain a significant share in the construction equipment market across the Middle East and Africa.

By Power Output: Compact Classes Prevail

Machines at or below 100 horsepower held 44.28% share in 2025 and will post an 8.13% CAGR to 2031, the fastest clip within the Middle East and Africa construction equipment market share. Mid-range-horsepower units are predominantly used in metro and rail projects, where agility is prioritized over sheer power. In the mining and quarrying sectors, higher-horsepower units are used, while the largest units are used mainly in open-pit mines. Buyers are increasingly leaning towards compact equipment for township housing projects, where a single backhoe loader can efficiently trench, load, and grade a site, due to its simpler hydraulics and higher uptime.

Advancements in cordless tool batteries have now enabled skid-steers to operate for a full shift, with the added benefit of a quick midday recharge. Municipalities favor these skid-steers because they comply with nighttime noise regulations and daytime emission standards. On the other hand, ultra-class loaders saw only replacement sales after a significant drop in lithium-carbonate prices, which postponed the opening of new pits. Nevertheless, these mines continue to demand life-cycle rebuild services, bolstering parts revenue in the upper segment of the Middle East and Africa's construction equipment market.

By Application: Infrastructure Leadership Meets Oil & Gas Growth

Infrastructure and transport accounted for 47.53% of 2025 turnover, the most significant slice of the Middle East and Africa construction equipment market. Oil and gas are the fastest-growing, with an 8.06% CAGR, as refinery and petrochemical hubs expand in Kuwait, Oman, and Nigeria. Mining held the largest share, followed by commercial buildings, residential, and industrial jobs. GCC budgets allocated a significant portion to transport, utilities, and public facilities, ensuring a steady demand for equipment, even amidst pauses in private projects.

While tight regional credit increased borrowing costs, it dampened the initiation of office towers. However, road and rail corridors, backed by sovereign wealth funds, felt little impact. Battery-mineral mines, sensitive to pricing, only embark on expansion cycles when lithium carbonate prices remain favorable. This sensitivity renders my orders more erratic than infrastructure packages in the construction equipment markets of the Middle East and Africa.

By End-User: Contractors Maintain Market Leadership

Contractors accounted for 48.74% of the target market for 2025 outlays and are expected to grow at an 8.11% CAGR, mirroring the pivot to rental, which lowers balance-sheet stress. Rental companies, by bundling services and telematics into uptime guarantees, accounted for a significant share of the purchases. Government agencies, securing long-life public assets, followed with a notable share. Mining houses, with a focus on ultra-class excavators and haulers, captured a smaller portion. Pay-per-use plans, priced per operating hour, now stand in stark competition to the high price tags for excavators, driving contractors towards more flexible financing options.

In Nigeria and Angola, secondary public procurement decelerated as oil receipts dwindled, prompting agencies to extend service life beyond standard engine hours. Meanwhile, giga-project contractors in NEOM are leaning toward variable-rate rentals tied to project milestones, a trend gaining traction across construction equipment markets in the Middle East and Africa.

Geography Analysis

Saudi Arabia accounted for 27.63% of revenue in 2025, anchored by Public Investment Fund outlays on NEOM, the Red Sea Project, and Qiddiya. Local-content regulations have compelled XCMG and SANY to undertake assembly operations in Riyadh and Jeddah, thereby significantly reducing import prices. The United Arab Emirates held 19%, sustained by the USD 150 billion “We the UAE 2031” program that extends Etihad Rail and upgrades Abu Dhabi and Dubai airports. Qatar grows fastest at an 8.15% CAGR, driven by the Lusail City build-out, Doha Metro extensions, and Hamad Port Phase II.

Oman, capitalizing on Vision 2040's transport corridors and the Duqm petrochemical hub, secured a notable share of the market, with the hub requiring significant equipment. Kuwait and Bahrain are channeling their efforts into water networks and housing estates. South Africa commands a substantial portion of the market, balancing its investments between mining and freeway upgrades. The remaining share is distributed among Egypt, Nigeria, Kenya, Ethiopia, and several other nations. While political unrest in Sudan, eastern DRC, and northern Mozambique led to a deferment of capital expenditure, rapid housing initiatives in Egypt and Nigeria have bolstered steady sales of compact equipment.

Saudi Arabia's ambitious giga-projects benefit from multi-year budget locks, providing a buffer against market fluctuations. However, municipal road projects remain sensitive to crude price swings, as highlighted by a dip in capital expenditure when Brent crude prices dropped. In the UAE, in-country value regulations are accelerating knowledge transfer, but they're also causing supply chain fragmentation, with smaller suppliers scrambling for ISO-9001 accreditation. In South Africa, mining demand is influenced by commodity price trends, leading some major players to shelve fleet expansion plans. Even so, desert telematics adoption continues to progress, maintaining aftermarket revenue across the Middle East and Africa construction equipment market.

Competitive Landscape

The market exhibits moderate concentration. Caterpillar, Komatsu, and Volvo collectively command a significant share, while Chinese contenders XCMG, SANY, and Zoomlion, leveraging cost-centric joint ventures, hold a notable portion. Rental entities like Al-Bahar and Kanoo Machinery are now acquiring service depots and parts hubs to achieve higher uptime. There's a burgeoning opportunity in electric and hybrid compact gear for township developments, yet no brand has ventured into establishing a sub-Saharan charging network.

Technology is the driving force. Cat Connect has significantly reduced downtime across machines in the Gulf, while Komatsu’s Smart Construction has achieved notable reductions in excavation cycles on Qatari projects. Bobcat and JCB have disrupted traditional players by introducing modular attachments that enable a single skid-steer to perform the tasks of multiple specialized units, resulting in substantial reductions in fleet costs. Compliance challenges are intensifying: Quotas such as IKTVA and ICV mandate local assembly for OEMs, yet many regional vendors lack ISO 14001 certification, causing delays in approvals. Meanwhile, autonomous-haulage retrofits from Hexagon and Trimble are heralding a new era of competition in the Middle East and Africa's construction equipment market, promising significantly reduced labor costs in remote mining operations[3] “Autonomous Haulage Retrofit Performance,”, Hexagon Mining, hexagonmining.com.

Middle East And Africa Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Volvo AB (Volvo CE)

CNH Industrial (Case CE)

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: At a launch ceremony in Muscat, Oasis Trading, the authorized CAT dealer in Oman, introduced the new CAT 345 Hydraulic Excavator. The event highlighted the excavator's advanced features, including enhanced fuel efficiency, increased productivity, and cutting-edge technology designed to optimize performance in demanding construction environments. Industry professionals and stakeholders attended the ceremony, emphasizing the significance of this addition to Oman's construction equipment market.

- January 2025: Weir Group formed a joint venture with Olayan to localize service and assembly for high-pressure grinding rolls aimed at Saudi Arabia’s USD 75 billion mining sector.

Middle East And Africa Construction Equipment Market Report Scope

The Middle East and Africa construction equipment market report is segmented by machinery type (excavators, wheel loaders, and more), drive type (diesel/ice and more), power output (less than or equal to 100 hp and more), application (infrastructure & transport, oil & gas, and more), end-user (contractors, and more), and geography. The market forecasts are provided in terms of value (USD) and volume (units).

By Machinery Type

| Excavators |

| Wheel Loaders |

| Crawler Cranes |

| Telescopic Handlers |

| Backhoe Loaders |

| Skid-Steer & Compact Track Loaders |

| Motor Graders |

| Bulldozers & Dozers |

| Asphalt Pavers & Road Rollers |

| Articulated Dump Trucks |

| Trenchers & Misc. |

By Drive Type

| Diesel / ICE |

| Electric & Hybrid |

| Hydraulic |

By Power Output

| Less than or equal to 100 HP |

| 101–200 HP |

| 201–400 HP |

| More than 400 HP |

By Application

| Infrastructure & Transport |

| Oil & Gas |

| Mining & Quarrying |

| Commercial Buildings |

| Residential |

| Industrial / Manufacturing |

By End-User

| Contractors |

| Equipment Rental Companies |

| Government & Municipalities |

| Mining Firms |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| South Africa |

| Rest of Middle East and Africa |

| By Machinery Type | Excavators |

| Wheel Loaders | |

| Crawler Cranes | |

| Telescopic Handlers | |

| Backhoe Loaders | |

| Skid-Steer & Compact Track Loaders | |

| Motor Graders | |

| Bulldozers & Dozers | |

| Asphalt Pavers & Road Rollers | |

| Articulated Dump Trucks | |

| Trenchers & Misc. | |

| By Drive Type | Diesel / ICE |

| Electric & Hybrid | |

| Hydraulic | |

| By Power Output | Less than or equal to 100 HP |

| 101–200 HP | |

| 201–400 HP | |

| More than 400 HP | |

| By Application | Infrastructure & Transport |

| Oil & Gas | |

| Mining & Quarrying | |

| Commercial Buildings | |

| Residential | |

| Industrial / Manufacturing | |

| By End-User | Contractors |

| Equipment Rental Companies | |

| Government & Municipalities | |

| Mining Firms | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How fast is equipment demand growing in the Middle East and Africa construction equipment market?

The market is set to rise from USD 9.00 billion in 2026 to USD 13.13 billion by 2031, reflecting a 7.8% CAGR.

Which equipment type sells the most units?

Excavators lead with a 37.17% revenue share in 2025, supported by their multi-functional hydraulic attachments.

Which country shows the fastest growth in equipment spending?

Qatar posts the quickest expansion, tracking an 8.15% CAGR through 2031 on the back of Lusail City and metro extensions.

How large is the compact equipment opportunity?

Machines at or below 100 horsepower already hold 44.28% of 2025 sales and are forecast to grow at 8.13% CAGR, driven by African housing programs.

Page last updated on: