Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

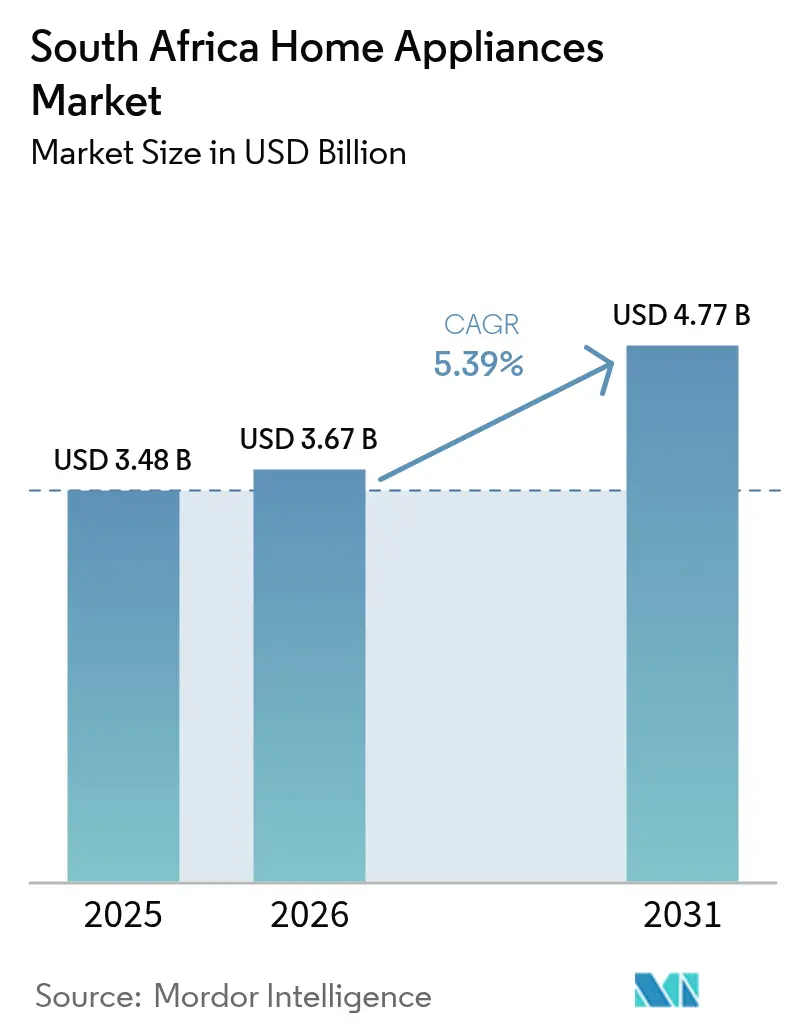

| Base Year Market Size (2025) | USD 3.48 Billion |

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 4.77 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Home Appliances Market Analysis by Mordor Intelligence

The South Africa home appliances market size is expected to grow from USD 3.48 billion in 2025 to USD 3.67 billion in 2026 and is forecast to reach USD 4.77 billion by 2031 at 5.39% CAGR over 2026-2031. This healthy trajectory persists despite inflationary pressure because households are compelled to replace load-shedding-damaged units and are simultaneously attracted to energy-efficient models that curb electricity bills [1]South African Bureau of Standards, “Minimum Energy Performance Standards,” sabs.co.za. . Essential categories such as refrigerators, freezers, and washing machines continue to anchor overall volume sales, yet a growing middle class is steadily shifting discretionary spend toward convenience-oriented small appliances that work on battery or solar backup systems. Retailers report that inverter-compatible products now move faster than legacy models as consumers future-proof against chronic power cuts, and manufacturers are responding by localizing component assembly to offset rand volatility. Multi-brand chains still dominate brick-and-mortar sales, but digital channels are scaling quickly on the back of nationwide fulfilment networks and expanded payment choices, helping brands penetrate peri-urban townships without heavy fixed-store investment. Competitive intensity is moderate: the top five vendors control 65% of revenue, enabling scale efficiencies, yet leaving room for niche entrants that differentiate on price, after-sales service, or off-grid compatibility.

Key Report Takeaways

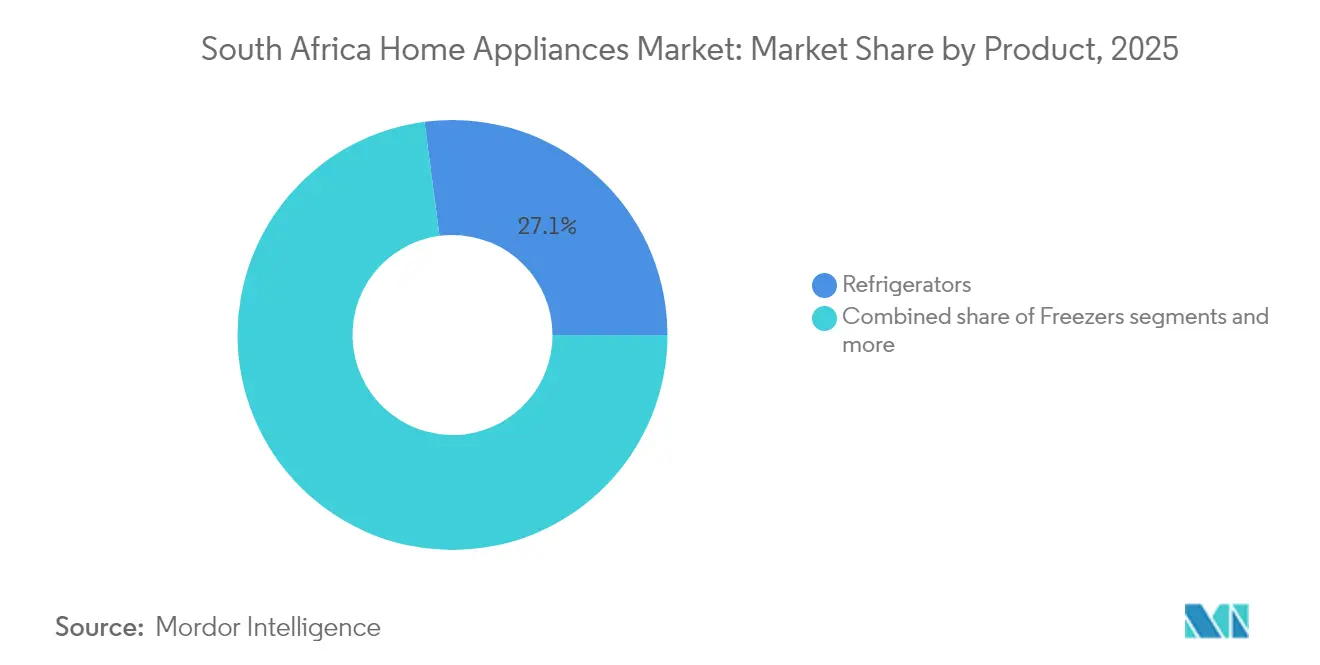

- By product type, refrigerators accounted for 27.08% of the South Africa home appliances market share in 2025, while the South Africa home appliances market size for air fryers is forecast to grow at the fastest CAGR of 5.84% between 2026 and 2031.

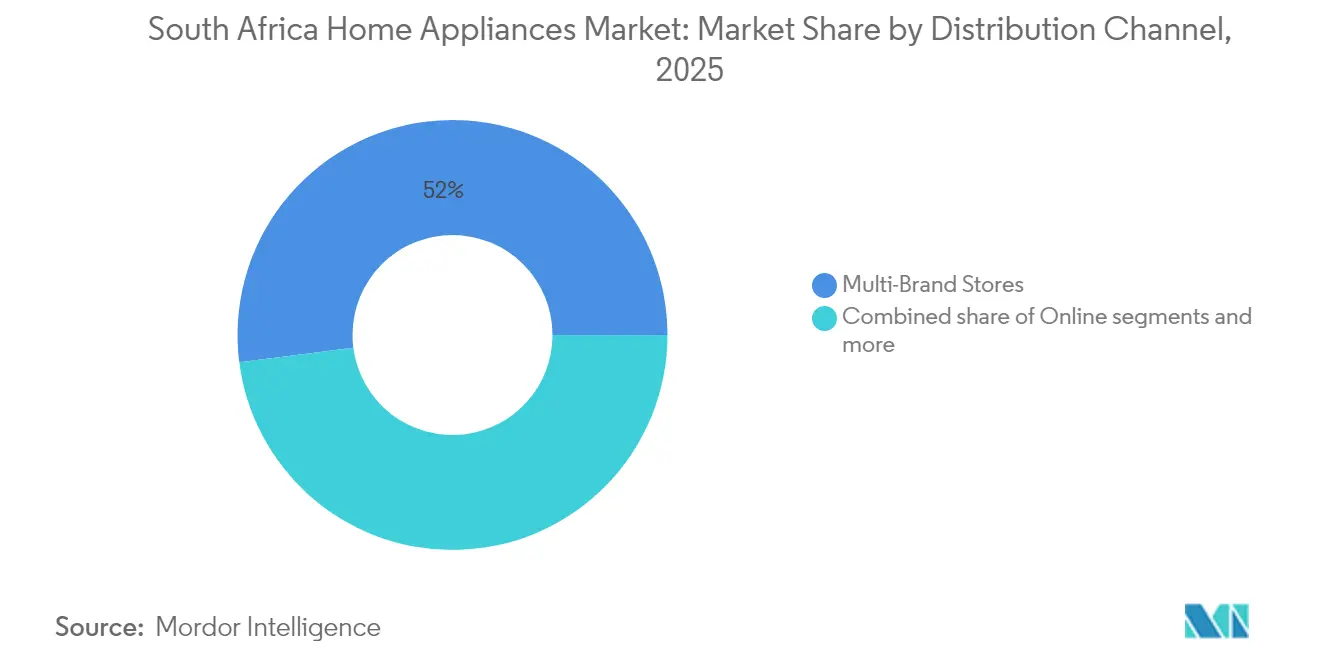

- By distribution channel, multi-brand stores captured 52.03% of the South Africa home appliances market share in 2025, whereas the South Africa home appliances market size for online channels is projected to expand fastest at a CAGR of 6.26% over 2026-2031.

- By geography, Gauteng led with 31.86% of the South Africa home appliances market share in 2025, while the South Africa home appliances market size in KwaZulu-Natal is anticipated to grow at the highest CAGR of 5.74% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class disposable income & urbanisation | +1.2% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Energy-efficiency regulations & rebate programmes | +0.8% | National, with early gains in Western Cape, Gauteng | Long term (≥ 4 years) |

| Replacement demand from ageing & load-shedding-damaged stock | +1.5% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Expansion of e-commerce & omnichannel retail | +0.7% | Urban centers, spill-over to secondary cities | Medium term (2-4 years) |

| Surge in solar-powered & battery-integrated appliances | +0.9% | Western Cape, Gauteng, Free State | Medium term (2-4 years) |

| Township micro-finance schemes enabling appliance purchases | +0.4% | Gauteng townships, KwaZulu-Natal, Eastern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Disposable Income & Urbanization

Urban migration into Johannesburg, Pretoria, Cape Town, and Durban is enlarging the addressable consumer base for durable goods. New homeowners routinely prioritize refrigeration and laundry equipment, while mid-income upgrades toward larger-capacity or smart-enabled models boost average selling prices. Retail chains have broadened consumer-finance programs, offering up to 36-month instalments that permit buyers to trade up without heavy upfront cash outlay[2]OK Furniture, “About Us,” okfurniture.co.za.. This financing, coupled with stable formal-sector employment in key provinces, underpins sustained demand even when overall GDP growth lags. The demographic bulge of younger, tech-savvy consumers further accelerates the uptake of app-controlled appliances that mesh with lifestyle aspirations. Manufacturers position energy-saving attributes as cost-containment tools, resonating with price-sensitive households facing rising power tariffs. Consequently, the driver is expected to contribute a net positive 1.2 percentage points to forecast CAGR through 2030.

Energy-Efficiency Regulations & Rebate Programs

South Africa enforces Minimum Energy Performance Standards that bar sub-optimal washers, refrigerators, and air-conditioners from entering the formal channel. Retailers must therefore stock only appliances rated Class A or better, forcing a technology refresh that lifts average unit prices. Complementary fiscal incentives—such as the 25% solar tax credit for households and 125% accelerated depreciation for businesses—encourage pairing of efficient appliances with rooftop photovoltaic systems. Compliance audits by the South African Bureau of Standards push importers toward local testing and, in turn, stimulate domestic component sourcing. Provincial initiatives in the Western Cape and Gauteng further sweeten rebates for low-consumption units, catalyzing faster turnover of the installed base. Rising Eskom tariffs amplify the cost-saving narrative, making the regulatory driver a structural tailwind that adds roughly 0.8 percentage points to long-term CAGR.

Replacement Demand from Ageing & Load-Shedding-Damaged Stock

Frequent voltage dips and sudden outages degrade compressors, electronic control boards, and sealed-system components, shortening appliance life cycles well below global norms. Insurance claims rarely cover repeated power-surge damage, pushing households to self-fund replacements every five to seven years rather than the historical ten-year window. Vendors offering inverter compressors, surge-protected power supplies, and lithium-ion battery modules gain share because they lessen downtime during rolling blackouts. Parallel growth in residential energy-storage capacity—in facilities such as Freedom Won’s recently expanded assembly plant—ensures ample demand for appliances optimized for DC-AC inverters. The resulting accelerated swap-out cycle injects an additional 1.5 percentage points into short-term market growth, cushioning revenue against macro downturns.

Expansion of E-Commerce & Omnichannel Retail

Mobile-first consumers increasingly finalize big-ticket purchases online after showroom research, a trend aided by nationwide courier networks that promise three-to-five-day delivery even to secondary towns. Leading physical retailers have launched click-and-collect programs that marry store footprints with digital catalogs, mitigating last-mile logistics costs. Payment-service upgrades, such as instant EFT and buy-now-pay-later wallets, widen affordability for first-time buyers. Online-only entrants frequently bundle installation or old-appliance haul-away to overcome customer hesitancy around complex goods. Transparent pricing and aggregated customer reviews erode legacy brand moats, compelling incumbents to sharpen loyalty schemes. The omnichannel surge is expected to lift overall market CAGR by 0.7 percentage points during the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unemployment & weak consumer spending power | -1.8% | National, concentrated in rural areas and townships | Short term (≤ 2 years) |

| Rand volatility inflating import costs | -0.9% | National, affecting all import-dependent segments | Medium term (2-4 years) |

| Chronic load-shedding delaying big-ticket purchases | -0.7% | National, urban areas most affected | Short term (≤ 2 years) |

| Grey-market cross-border imports eroding formal sales | -0.5% | Border provinces, informal retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unemployment & Weak Consumer Spending Power

National joblessness near 32% constrains discretionary budgets, particularly in rural districts and informal settlements where under-employment is pervasive. Households give precedence to urgent necessities such as refrigeration over aspirational devices like dishwashers, limiting category breadth. Inflation in food, fuel and transport absorbs wallet share, delaying non-essential upgrades even when credit is available. Township economies, though estimated at ZAR 300 billion annually, remain under-served by formal retailers due to credit-risk concerns. Micro-lending initiatives often carry double-digit interest rates, discouraging uptake among cash-constrained consumers. Consequently, the spending-power drag subtracts an estimated 1.8 percentage points from near-term growth.

Rand Volatility Inflating Import Costs

More than half of the finished units or critical subsystems originate from East Asian factories denominated in USD or CNY. Each episode of rand depreciation forces immediate wholesale price adjustments, raising retail tags and prompting buyers to postpone purchases in anticipation of currency rebounds. Hedging instruments partly shield large importers, yet smaller distributors struggle to absorb swings, squeezing margins and marketing budgets. Grey-channel traders exploit currency gaps by moving parallel-import stock through border provinces, undermining authorized dealer pricing and warranty perceptions. Local assembly efforts—exemplified by Hisense’s Atlantis plant—soften but do not eliminate component-cost exposure because compressors, motors, and chips are still sourced offshore. The net effect trims the forecast CAGR by roughly 0.9 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Essential Cooling Dominates, Small-Appliance Uptake Climbs

Refrigerators retained 27.08% of South Africa's home appliances market share in 2025, highlighting their non-discretionary role in food security, especially amid erratic power supply. Load-shedding has elevated inverter-compressor fridges, which draw 40% less power when switched to battery back-up, reinforcing their replacement appeal. The South Africa home appliances market size for refrigeration equipment is projected to expand in tandem with cold-chain urban grocery retailing, which raises consumer expectations for fresh-food storage longevity. Air fryers headline the small-appliance growth chart with a 5.84% CAGR because they cut cooking times and electricity use versus conventional ovens. Manufacturers promote dual-zone baskets and integrated recipe apps, encouraging second-time upgrades despite the category’s relative infancy. Parallel growth is visible in countertop induction stoves and programmable pressure cookers, as urban renters favor compact solutions compatible with limited power budgets.

Second-tier categories such as dishwashers, tumble dryers, and air conditioners show mixed fortunes. Dishwashers lag because plumbing retrofits are costly in older housing stock, yet premium developers in Gauteng’s northern suburbs are pre-fitting kitchens with cavity space and water lines, seeding future demand. Tumble-dryer sales rise during winter months in KwaZulu-Natal and Western Cape coastal zones where humidity prolongs drying times, but off-peak electricity-tariff programs partly mitigate operating-cost concerns. Split-unit air-conditioners gain traction in hotter northern provinces, though sales remain seasonal and heavily tied to disposable income elasticity. Ovens, particularly electric convection models, experience incremental demand from baking entrepreneurs operating home-based micro-bakeries, a trend catalyzed by pandemic-era side hustles.

By Distribution Channel: Multibrand Chains Hold Volume While Digital Gathers Pace

Multibrand retailers accounted for 52.03% of 2025 value, leveraging portfolio breadth, in-store credit desks and warehouse-level bargain events to pull foot traffic. Store assistants provide live demos and financing paperwork, anchoring loyalty among older shoppers less comfortable with online carts. The South Africa home appliances market size realized through physical multibrand outlets remains buoyant because installation services and immediate product handover reduce perceived risk for high-value goods. Nevertheless, online platforms are climbing at a 6.26% CAGR, capturing digitally fluent millennials who prioritize price comparison and doorstep delivery.

Exclusive brand stores cater to premium buyers seeking curated in-store experiences: signature kitchens, coffee bars and live chef demonstrations create halo effects that justify higher margins. Yet expansion of these monobrand boutiques is cautious because shopping-center rents escalate faster than appliance margins. Direct-to-consumer dropship arrangements from overseas factories appeal to niche importers but face customs-duty unpredictability. Informal channels—street vendors or cross-border traders—continue to offload low-spec or refurbished appliances at deep discounts, posing compliance challenges for regulators.

Geography Analysis

Gauteng contributed 31.86% of 2025 revenues, anchored by Johannesburg-Pretoria’s dense middle-income suburbs, sprawling shopping centers and proximity to logistics hubs that compress last-mile costs for bulky items. The province’s higher per-capita electricity consumption intensifies interest in inverter-ready refrigerators and lithium-battery back-up packages, making energy efficiency a decisive purchase criterion. Premium real-estate developments adopt smart-home wiring standards, paving the way for Wi-Fi-enabled ovens and washers connected through manufacturer cloud dashboards. Retailer clustering along the N1 and N3 transport corridors eases same-day delivery promises, reinforcing consumer expectations for rapid fulfilment.

KwaZulu-Natal is poised for the fastest provincial growth at a 5.74% CAGR thanks to Durban’s port-centric industrial revival and infrastructure upgrades along the N2 north-south artery. Importers benefit from direct container landings at the Port of Durban, shaving transit costs that can otherwise add 4%-6% to appliance landed prices. Secondary hubs such as Pietermaritzburg, Newcastle and Richards Bay witness retail square-meter expansion as property developers target rising urbanization. The coastal climate heightens demand for dehumidifying appliances, while a thriving hospitality segment orders commercial-grade refrigerators and dishwashers for guesthouses along the Dolphin Coast. Township micro-finance pilots in Umlazi and KwaMashu demonstrate proof of concept for extending structured credit into informal settlements, signaling untapped volume upside if replicated across other wards.

Western Cape sustains a sizable share, undergirded by Cape Town’s diversified economy, technology start-ups and strong municipal support for rooftop solar installations. Energy-conscious households actively seek appliances bearing the municipal GreenBuilding Council of South Africa endorsement, reinforcing brand messaging around low kilowatt-hour consumption. Coastal weather swings drive interest in heat-pump tumble dryers that operate efficiently in damp winter months. Tourism rebound pushes holiday-rental hosts to furnish properties with mid-to-high-end microwaves, bar fridges and smart TVs, adding seasonal demand spikes. Yet property-price inflation pressures disposable income, prompting middle-class consumers to stretch repayment horizons on new appliance finance contracts.

Competitive Landscape

The market shows moderate concentration, with the five largest vendors collectively holding a significant portion of total turnover. Their nationwide service networks reinforce this position, substantial advertising spend, and cost efficiencies from local assembly. Defy leads the market, leveraging its production facilities in KwaDukuza and Durban to supply refrigerators, chest freezers, and cooking ranges tailored to South Africa’s voltage fluctuations. Hisense expands its Atlantis site to furnish LED-lighting lines and automated foam-injection refrigerators, shortening lead times and mitigating currency exposure[4]Hisense South Africa, “About Us,” hisense.co.za. . Samsung and LG court affluent buyers through smart-home ecosystems that integrate washing-machines, TVs and smartphones within a single mobile app, reinforcing brand stickiness. Whirlpool positions on quiet-drive motors and antimicrobial gasket linings but faces channel-stuffing risks if currency shocks raise inventory-carrying costs.

Local challengers concentrate on price-value propositions in the mid-range and small-appliance space; brands such as Russell Hobbs exploit licensing models to flood shelves with kettles, toasters, and blenders sporting fashionable finishes at attainable prices. Import-only boutique labels capture design enthusiasts through direct online campaigns, though volumes remain niche. Service quality is a battlefield: vendors now advertise 48-hour repair pledges in metros and 72-hour commitments in secondary cities, differentiating against grey-import competitors lacking local parts. Supply-chain resilience strategies include dual-sourcing compressors and heating elements to shield against port congestion. Strategic partnerships with solar-panel installers and battery suppliers amplify cross-selling; for example, washing-machine bundles with 3 kWh lithium packs are marketed during load-shedding peaks.

Online marketplaces intensify price transparency, forcing manufacturers to implement unilateral minimum advertised price policies to steady margins. Brick-and-mortar retailers retaliate with experiential showrooms where customers test decibel levels, steam functions and app controls in real time. Advertising budgets tilt toward social-media influencers who demonstrate power-draw measurements under real-world outage simulations, validating manufacturer efficiency claims. Sustainability credentials gain prominence: brands publicize ISO 14001-certified factories and refrigerants with lower global-warming potential to align with evolving consumer values. Overall, technology refresh cycles, regulatory pressure and shifting retail models sustain dynamic yet disciplined competition within the South Africa home appliances market.

South Africa Home Appliances Industry Leaders

Defy (Arçelik)

Whirlpool Corp. (incl. KIC)

Hisense

Samsung Electronics

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Freedom Won completed a 48,000 m² expansion of its Edenvale battery assembly complex, elevating monthly capacity to 150 MWh and positioning the facility as the largest of its kind locally.

- August 2024: Lesaka Technologies closed its ZAR 1.59 billion acquisition of Adumo, increasing its merchant-services footprint to 119,000 outlets and streamlining appliance-retail payment acceptance.

- April 2024: Whirlpool Corporation announced global restructuring with workforce reductions affecting thousands of employees worldwide, potentially impacting South African operations and product availability through reduced promotional activities.

- February 2024: Balancell upgraded its Cape Town battery plant to 1 GWh annual capacity, supplying intelligent storage solutions to major supermarket groups.

South Africa Home Appliances Market Report Scope

A home appliance is a device that aids in various household tasks, such as cooking, cleaning, and preserving food. The South African home appliances market is segmented by product and distribution channels. By product, the market is segmented into major appliances and small appliances. Major appliances are sub-segmented into refrigerators, freezers, dishwashers, washing machines, cookers, and ovens. Small appliances are sub-segmented into vacuum cleaners, small kitchen appliances, hair clippers, irons, toasters, grills and roasters, and hair dryers, and by distribution channels, the market is segmented into multi-brand stores, exclusive stores, online, and other distribution channels. The report offers market size and forecasts for the South African home appliance market in terms of revenue (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Gauteng |

| Western Cape |

| KwaZulu-Natal |

| Eastern Cape |

| Free State |

| Limpopo |

| Mpumalanga |

| North West |

| Northern Cape |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Gauteng | |

| Western Cape | ||

| KwaZulu-Natal | ||

| Eastern Cape | ||

| Free State | ||

| Limpopo | ||

| Mpumalanga | ||

| North West | ||

| Northern Cape | ||

Key Questions Answered in the Report

What is the projected value of South Africa’s home appliances space by 2031?

The segment is expected to reach USD 4.77 billion by 2031, up from USD 3.67 billion in 2026.

Which product type currently commands the largest revenue share?

Refrigerators lead with 27.08% of 2025 value because they are indispensable for food preservation.

Why are air fryers expanding faster than other categories?

They cook quickly, use less electricity and align with healthier eating trends, driving a 5.84% CAGR through 2031.

How significant is e-commerce in appliance sales?

Online channels are growing at a 6.26% CAGR as nationwide fulfilment and flexible payments entice digital-native buyers.

Which province offers the quickest growth outlook?

KwaZulu-Natal is forecast to post a 5.74% CAGR thanks to industrial expansion and improved retail penetration.

Page last updated on: