Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

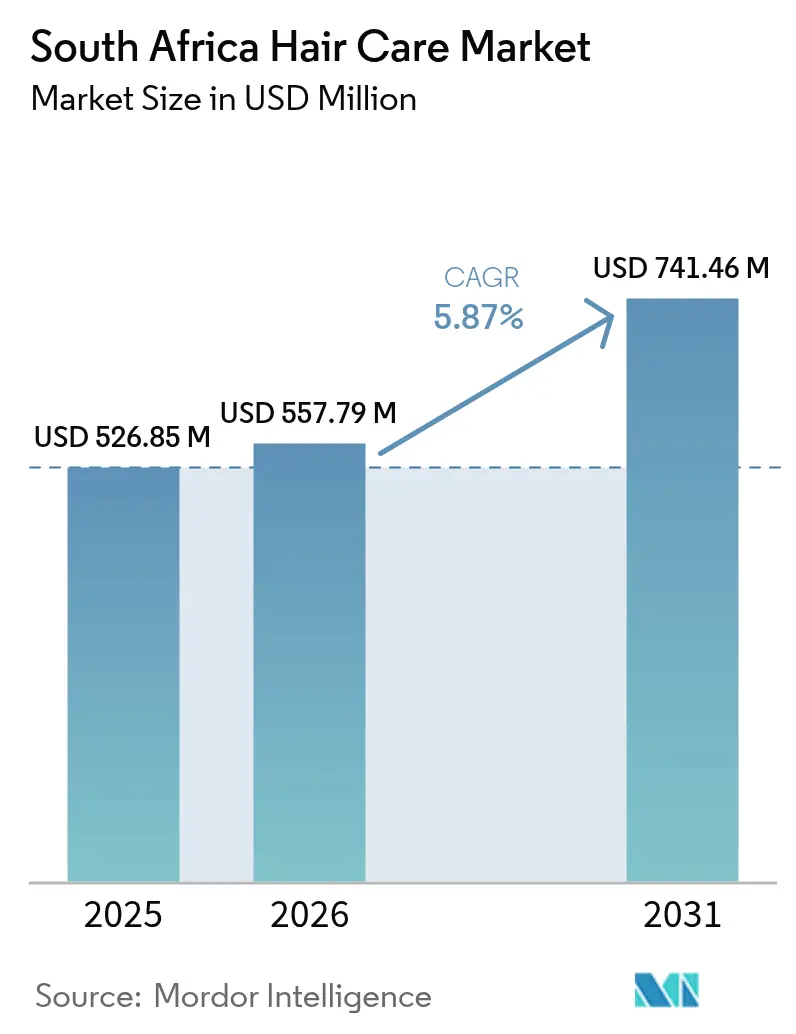

| Base Year Market Size (2025) | USD 526.85 Million |

| Market Size (2026) | USD 557.79 Million |

| Market Size (2031) | USD 741.46 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Hair Care Market Analysis by Mordor Intelligence

The South Africa hair care market size is expected to grow from USD 526.85 million in 2025 to USD 557.79 million in 2026 and is forecast to reach USD 741.46 million by 2031 at 5.87% CAGR over 2026-2031. This growth is driven by increasing urban incomes, greater awareness of beauty, and innovative products designed for different ethnic hair types. In 2024, conditioners lead the market, while hair colorants and dyes are the fastest-growing segment through 2030. The conventional/synthetic segment dominates in 2024, but natural/organic products are gaining popularity. In terms of price range, mass-market products lead in 2024, though premium products are growing as consumers show a willingness to spend more on high-quality options. Among distribution channels, supermarkets/hypermarkets dominate in 2024, but specialty and beauty stores are growing the fastest, reflecting a trend toward expert-guided purchases. The market shows moderate consolidation, with major players like Unilever PLC, L'Oréal SA, and Procter & Gamble competing alongside local brands such as Nilotiqa and AfroBotanics. Competition is fueled by the diverse needs of consumers with different ethnic hair types, driving innovation in biotech formulations and scalp-focused products.

Key Report Takeaways

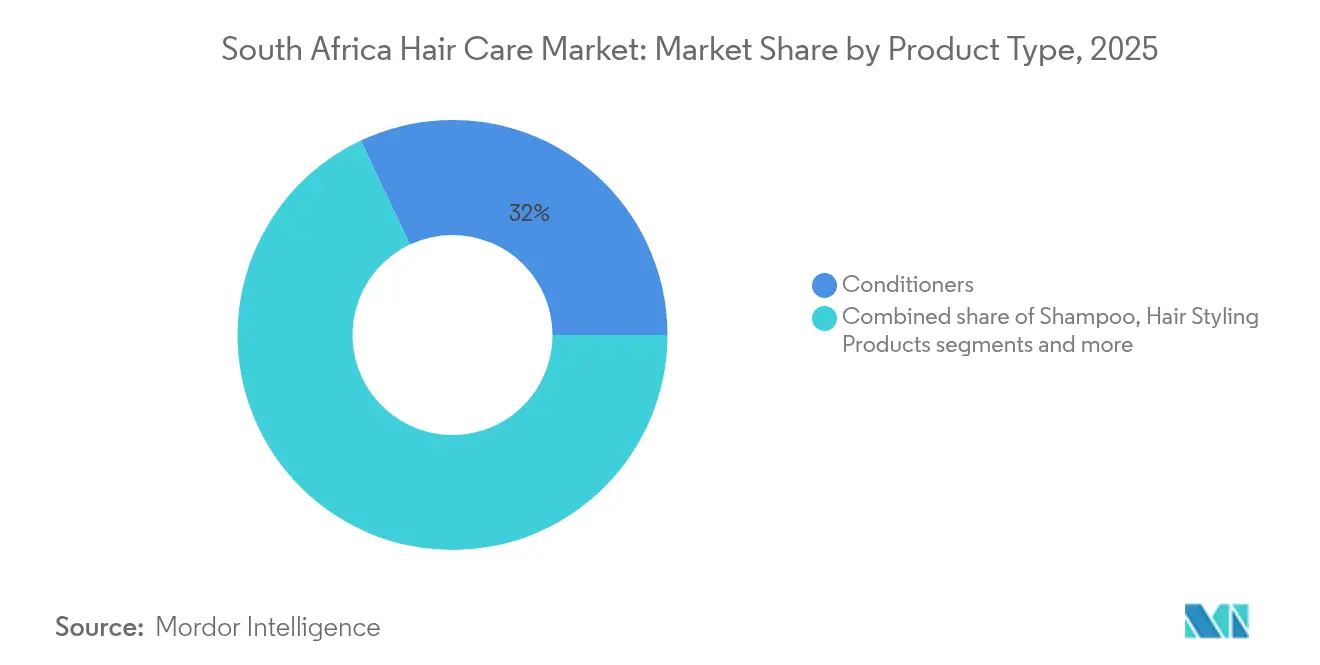

- By product type, conditioners led with a 32.02% share of the South Africa hair care market in 2025; hair colorants and dyes are advancing at a 6.66% CAGR to 2031.

- By nature, conventional/synthetic items captured 84.90% of the South Africa hair care market size in 2025, while natural/organic offerings are projected to expand at a 6.52% CAGR through 2031.

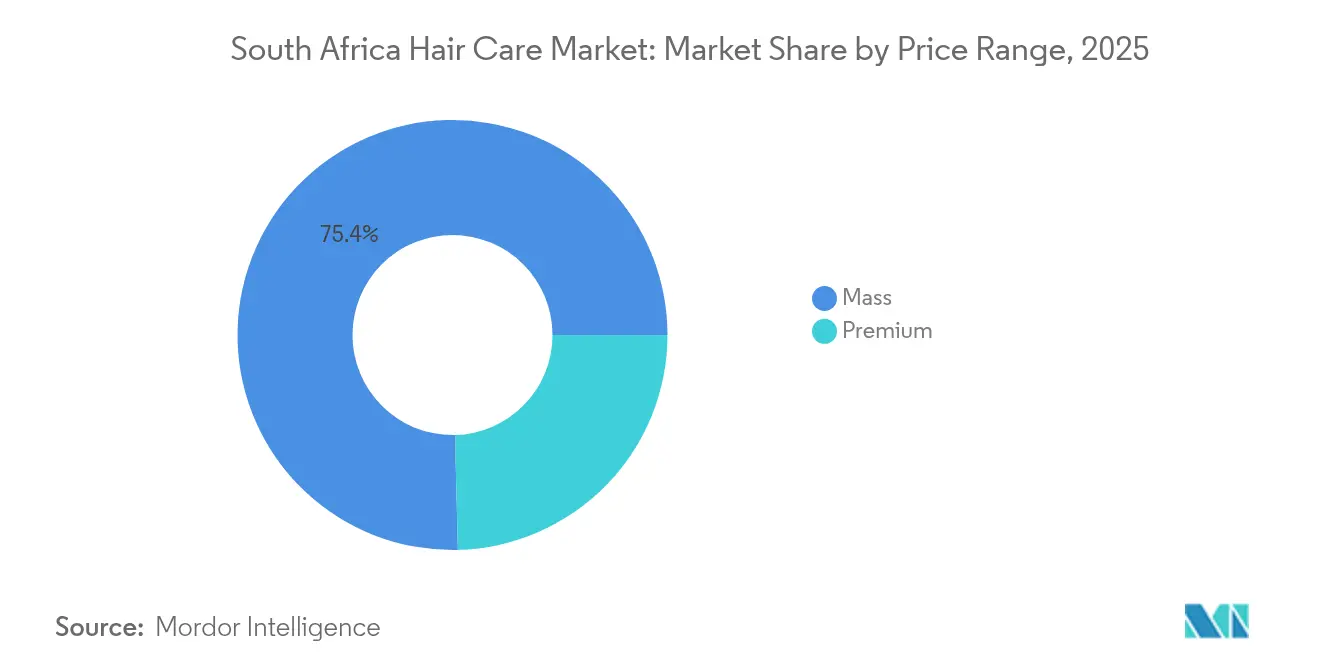

- By price range, mass market goods held 75.40% of the South Africa hair care market share in 2025; premium products are growing at a 7.08% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets accounted for 45.12% of the South Africa hair care market in 2025, whereas specialty and beauty shops lead future growth at an 7.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for ethnic and textured hair solutions | +0.9% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Demand for multi-functional and damage control products | +0.7% | National, with premium focus in metropolitan areas | Medium term (2-4 years) |

| Technological innovations in product formulations | +0.6% | National, driven by international brand investments | Medium term (2-4 years) |

| Growing male grooming consciousness | +0.5% | Urban centers, expanding to suburban markets | Long term (≥ 4 years) |

| Influence of social media and beauty influencers | +0.4% | National, strongest among youth demographics | Short term (≤ 2 years) |

| Increasing focus on scalp health | +0.4% | National, with premium positioning | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High demand for ethnic and textured hair solutions

South Africa’s hair care market has a high demand for products designed for ethnic and textured hair, with 59.4% of the population having kinky hair, the highest globally, according to a February 2025 PubMed Central survey[1]Source: PubMed Central, "Types and Characteristics of Hair Across the Globe: Results of a Multinational Study on 19,461 Individuals", pmc.ncbi.nlm.nih.gov. This drives the popularity of moisture-rich creams, curl-defining conditioners, and breakage-control oils made for coily and fragile hair types. Local brands like Nilotiqa use natural ingredients such as marula and baobab oils to meet specific hair needs in the region. Meanwhile, global brands present in South Africa enhance their appeal by collaborating with cultural influencers, like TRESemmé’s partnerships that highlight textured hairstyles at major events. Consumers now prioritize ingredient transparency, protein-bond technology, and aftercare for protective styles, which help brands build lasting loyalty.

Demand for multi-functional and damage-control products

In South Africa, consumers are increasingly looking for hair care products that offer multiple benefits in one application. These products, which combine conditioning, color protection, ultra-violet (UV) defense, and heat protection, are becoming popular among people who want salon-like results without complicated routines. With traction alopecia affecting 31.6% of South African women, as per PubMed Central, as of January 2025, there is a growing need for gentle, restorative products that prevent breakage and improve hair health[2]Source: PubMed Central, "Prevalence and Associated Factors of Traction Alopecia in Women in North Sudan: A Community-Based, Cross-Sectional Study", pmc.ncbi.nlm.nih.gov. For example, Unilever's Dove scalp + hair therapy combines microbiome-friendly ingredients with traditional nourishment, showcasing the value of such products. This trend is also driven by post-pandemic lifestyle changes, where people focus on efficiency and self-care at home, making multipurpose products a key focus for brands.

Growing male grooming consciousness

Changing social norms are encouraging men to spend more on hair care in the South African region, especially on scalp treatments and styling products for textured hair. With 33.13% of South African men experiencing male-pattern baldness in 2025, according to World Population Review, there is a growing demand for specialized solutions and preventive care[3]Source: World Population Review, "Percentage of Bald Males by Country 2025", worldpopulationreview.com. Several key developments in the market support these factors, such as, April 2025 launch of Keune’s so pure range, which included vegan, eco-friendly shampoos, conditioners, and treatments for various hair types, including textured hair. The range also featured refillable packaging, catering to environmentally conscious consumers and highlighting the industry's focus on the expanding male grooming segment.

Influence of social media and beauty influencers

In South Africa, short-form video platforms like TikTok and Instagram Reels, along with events and exhibitions, are quickly increasing awareness and use of hair care products, especially those for textured hair and multi-step routines. Viral videos showing how products work often lead to sudden sales spikes, pushing brands to adjust supply chains to avoid running out of stock. For example, the 2024 partnership between TRESemmé and MaXhosa Africa at Johannesburg Fashion Week showcased the blend of global brands with local fashion, celebrating heritage and inclusivity. Retailers are also improving shelf arrangements based on social-media-driven demand, while influencer guidelines from the Advertising Standards Authority of South Africa (ASA) ensure claims are accurate, making content more trustworthy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.8% | National, with higher incidence in informal trade channels | Short term (≤ 2 years) |

| Adoption of traditional at-home hair care solutions | -0.6% | Rural and peri-urban areas, cultural preservation communities | Long term (≥ 4 years) |

| Regulatory challenges for imported products | -0.5% | National, affecting international brands | Medium term (2-4 years) |

| Health and safety concerns related to chemical-based hair products | -0.4% | National, with higher awareness in educated demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

Fake hair oils and colorants are being sold through informal trade channels in South Africa, harming brand reputation and risking public health. The South African Health Products Regulatory Authority (SAHPRA), along with customs and police, regularly seizes illegal products during border checks. For example, in November 2024, police discovered a secret operation in Pinetown, KwaZulu-Natal, where fake hair products were being made in a pastor’s home. Undocumented foreign nationals were arrested, and invoices showed that these fake products were sent to wholesalers, retail stores in KwaZulu-Natal, and the Eastern Cape. To address this, genuine brands are using QR codes and tamper-proof seals to help consumers verify products. However, enforcement is costly, so companies are also running campaigns to educate consumers on how to buy safe products.

Regulatory challenges for imported products

Foreign hair care brands entering South Africa must deal with strict regulations, including registering with the South African Health Products Regulatory Authority (SAHPRA), submitting detailed ingredient information, and following labeling standards similar to European Union cosmetic rules. The Cosmetics, Toiletry, and Fragrance Association (CTFA) provides training on Good Manufacturing Practices (SANS 22716) to assist with compliance[4]Source: Cosmetics, Toiletry, and Fragrance Association (CTFA), "Cosmetics Good Manufacturing Practices Guidelines On Good Manufacturing Practices", ctfa.co.za. However, the lengthy approval process often delays product launches and increases costs, giving an edge to local manufacturers or companies with joint ventures. The Advertising Standards Authority of South Africa (ASA) requires brands to provide evidence for product performance claims, adding to the complexity. These challenges make it essential for new entrants to plan carefully and allocate resources for regulatory compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conditioners Maintain Leadership While Colorants Accelerate

Conditioners made up 32.02% of the South African hair care market in 2025, highlighting their role in solving common hair problems like dryness, breakage, and frizz across different hair types. The high prevalence of textured and chemically treated hair in the region has driven demand for products that provide hydration, strengthen hair, and manage frizz effectively. Premium and ethnic-focused brands are utilizing natural oils, protein-based formulas, and heat-protection technologies to stand out in the market. Meanwhile, mass-market brands are focusing on affordability and multipurpose solutions to cater to a wider consumer base. This balance between premium and budget-friendly options ensures that conditioners remain a key product category in the market.

The hair colorants and dyes segment is projected to grow at the fastest rate in the South African hair care market, with a CAGR of 6.66% through 2031. This growth is fueled by rising interest in at-home hair coloring and products that combine styling with nourishment. Brands are increasingly incorporating scalp-friendly ingredients, Ultra-violet (UV) protection, and damage-repair features into their colorant lines to meet evolving consumer preferences. The trend reflects a shift toward more personalized and texture-specific products, catering to the unique needs of South African consumers. This focus on innovation and cultural relevance positions South Africa as a significant market for both mainstream and ethnic-focused hair care solutions.

By Nature: Conventional Formulations Dominate but Organic Gains Momentum

Conventional/synthetic hair care products led the South African market in 2025, holding 84.90% of the total market share. Their popularity is largely due to their affordability and effectiveness in addressing common hair concerns like frizz caused by humidity and the management of various hair textures. These products are particularly appealing to cost-conscious consumers who prioritize reliable performance. The availability of multi-functional products, such as those offering both conditioning and heat protection, has further strengthened the position of conventional hair care products, especially in urban and suburban retail markets.

On the other hand, natural/organic hair care products are gaining traction as a fast-growing segment, with an expected CAGR of 6.52% through 2031. Increasing awareness about wellness and sustainability, particularly among urban consumers, is driving demand for products made with plant-based oils, botanical extracts, and minimal synthetic ingredients. These products not only align with ethical and environmental values but also address specific hair concerns like scalp sensitivity, breakage, and color retention. As a result, brands offering natural and organic options are able to position themselves as premium choices. This trend is making natural and organic products a key area for innovation in the South African market.

By Price Range: Premium Acceleration Shapes Bifurcated Spend Patterns

Mass-market hair care products led the South African market in 2025, accounting for 75.40% of the total market share. These products are popular due to their affordability, availability in various sizes like family packs and single-use sachets, and their presence in supermarkets and convenience stores. They cater to budget-conscious consumers who prioritize cost-effective solutions for everyday hair care. Multi-functional products, such as 2-in-1 shampoo and conditioner or anti-frizz formulas, have further strengthened their appeal. These offerings are widely used in urban and suburban households, ensuring consistent demand and brand loyalty across diverse consumer groups.

On the other hand, premium hair care products are expected to grow significantly, with a projected CAGR of 7.08% through 2031. This growth is driven by consumers increasingly willing to spend on high-quality products that offer advanced benefits, such as scalp care, damage repair, and solutions for textured or color-treated hair. Premium brands focus on using innovative ingredients and technologies to deliver superior results, justifying their higher price points. The trend highlights a shift toward more experience-driven purchases, where ingredient transparency, scientific advancements, and salon-like results play a key role in influencing buying decisions in the premium segment.

By Distribution Channel: Specialist Retail Outperforms Mass Outlets

Supermarkets/hypermarkets were the leading distribution channels in the South African hair care market in 2025, accounting for 45.12% of the total market share. These stores attract a large number of shoppers due to their convenience, wide range of products, and frequent promotional offers. They provide easy access to essential hair care items like shampoos and conditioners, especially for cost-conscious consumers. Family-size packaging and bundle deals further enhance their appeal, making them a preferred choice for households. The high foot traffic in these stores ensures consistent sales, making them a critical channel for mass-market hair care products.

On the other hand, specialty and beauty stores are expected to grow at the fastest rate, with a projected CAGR of 7.72% through 2031. These stores focus on meeting specific consumer needs by offering premium, natural, and ethnic-hair-focused products. They stand out by providing personalized shopping experiences, expert advice, and curated product selections. Consumers are increasingly drawn to these stores for high-quality and ingredient-conscious formulations. The growth of this channel highlights a shift toward more tailored and experience-driven purchasing, making specialty stores a key platform for innovative and high-margin hair care products in South Africa.

Geography Analysis

Metropolitan provinces lead the South African hair care market due to their large populations, higher income levels, and well-developed retail networks. Gauteng, home to cities like Johannesburg and Pretoria, plays a significant role, with its malls offering access to premium hair care products and professional salon services. The Western Cape, particularly Cape Town, shows a growing preference for organic and eco-friendly hair care products, driven by its environmentally conscious lifestyle and tourism influence. KwaZulu-Natal combines traditional hair care practices with modern routines, creating opportunities for products that respect cultural traditions while incorporating scientific advancements.

In rural areas, mass-market hair care products dominate, primarily sold through general dealers and small local shops. These regions prioritize affordable options, flexible packaging sizes, and products with long shelf lives. Due to infrastructure challenges, companies often avoid temperature-sensitive ingredients in these areas, ensuring product stability. However, small and medium enterprises in rural regions face higher compliance costs, which can limit the variety of products they offer. As urbanization continues to grow, rural areas are expected to see improved distribution networks and increased access to a wider range of hair care products.

South Africa also serves as a key hub for hair care products in the Sub-Saharan region, with its ports facilitating trade to neighboring countries like Botswana, Namibia, and Lesotho. This cross-border trade allows manufacturers, particularly those based in Gauteng, to benefit from economies of scale and expand their market reach. South Africa’s role as a regional innovation center for hair care products strengthens its position in the market, driving growth and fostering new product development tailored to diverse consumer needs across the region.

Regulatory Landscape

Hair care products in South Africa are governed primarily under the Foodstuffs, Cosmetics and Disinfectants Act, 1972 (Act No. 54 of 1972), which sets requirements for product safety, composition, and market conduct for both locally manufactured and imported cosmetics. In parallel, the Regulations relating to the labelling, advertising and composition of cosmetics (Government Gazette 41351) define labeling and claims rules, while the Advertising Standards Authority of South Africa (ASA) framework affects how performance claims are substantiated in marketing.

On the technical side, the National Regulator for Compulsory Specifications (NRCS), an entity of the dtic, administers compulsory specifications used to protect consumer health and support fair trade. Companies often align internal QA and documentation to meet NRCS verification requirements. The South African Bureau of Standards (SABS) maintains voluntary South African National Standards used as industry benchmarks, including SANS 10393 (hair care products, general requirements) and broader labeling guidance such as SANS 289. An August 2024 Government Gazette 51050 notice on standards matters also indicated continued standard-setting activity that can tighten ingredient and labeling expectations over time.

Value Chain Analysis

The value chain begins with ingredients (surfactants, conditioning agents, actives, fragrances, and botanical oils), followed by packaging (plastics and labeling) and formulation know-how. Manufacturing is then carried out either in-house or through local contract manufacturers, while regulatory compliance work (documentation, testing, labeling, and traceability) runs alongside production, anchored by the Foodstuffs, Cosmetics and Disinfectants Act and technical requirements overseen by the NRCS under compulsory specifications. Voluntary SANS benchmarks, including SANS 10393, also influence quality management and label readiness.

Production and filling are concentrated around major industrial provinces such as Gauteng, a key hub for national distribution, before movement into downstream retail and professional channels including supermarkets/hypermarkets, specialty and beauty stores, salons, and online. A notable value-chain shift occurred in March 2026, when Prime Product Manufacturing acquired L'Oreal South Africa's production facility in Midrand, described as doubling capacity for toiletries, fragrances, and beauty products and expanding local contract manufacturing options. Distribution is supported by large retailers and local distributors (including Sunpac and Great Africa Group), while ongoing bottlenecks reflect imported input dependencies, logistics constraints, and energy reliability, which raises the importance of local sourcing, supplier qualification, and inventory buffers.

Competitive Landscape

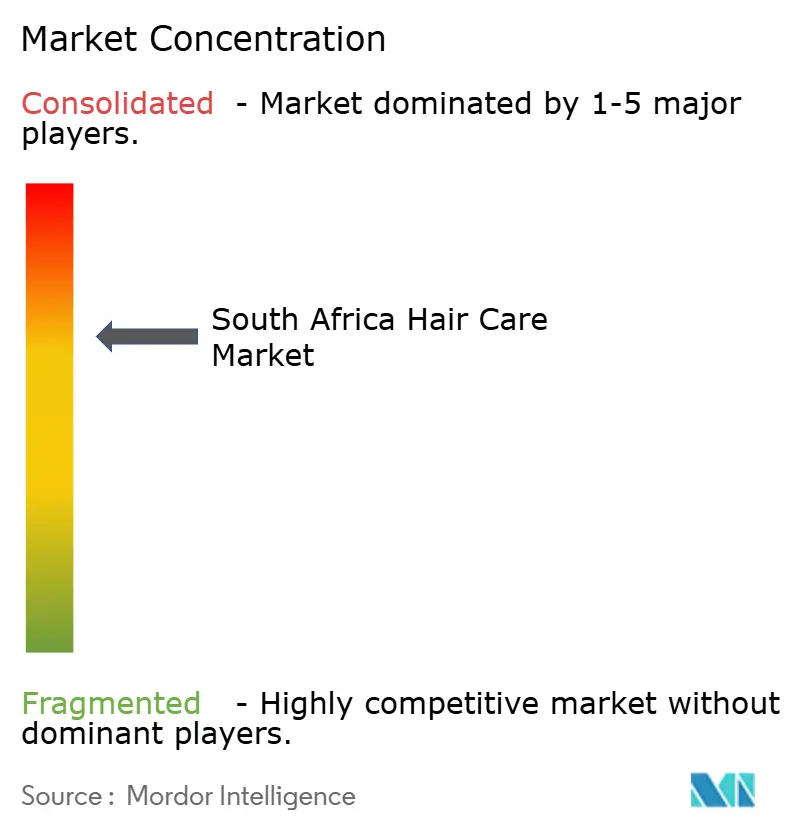

The South African hair care market is moderately concentrated, with the top 5 players holding close to 70% of the market share. Global companies like Unilever, L’Oréal, and Procter & Gamble leverage their extensive research and development capabilities and large advertising budgets to maintain a strong presence. At the same time, local brands such as Nilotiqa and AfroBotanics capitalize on their cultural relevance and understanding of local consumer needs. Unilever has strengthened its position by acquiring K18, which specializes in biotech peptides that repair hair damage.

Retailers are also playing a significant role in shaping the competitive landscape. For instance, Clicks is expanding its private-label offerings, which puts pressure on multinational brands to remain competitive. Collaborations between established brands like TRESemmé and South African fashion house MaXhosa highlight innovative marketing strategies, such as integrating hair care into fashion events. New players are entering the market by using influencer marketing and direct-to-consumer models, which allow them to bypass traditional retail channels and reduce costs. These strategies are helping smaller brands gain traction in a competitive market.

Regulatory standards, such as compliance with SANS 22716 Good Manufacturing Practices (GMP), are also influencing the market. While these regulations ensure product quality and build consumer trust, they can create challenges for smaller companies due to the associated costs. However, these standards contribute to a stable and trustworthy market environment. Overall, the South African hair care market is evolving with a mix of global innovation, local expertise, and changing consumer preferences, creating opportunities for both established players and emerging brands.

South Africa Hair Care Industry Leaders

-

Unilever Plc

-

L'Oréal S.A.

-

Amka Products (Pty) Ltd

-

Marico Limited

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on upgrading the product mix toward texture-specific, science-backed, and scalp-care positioning, with several brand moves already playing out in-market. Unilever has been pushing newer scalp and hair formats and youth-oriented brand renovation, including the January 2026 South Africa launch of Sunsilk Wondermist, which reinforces whitespace in lightweight leave-in formats and regimen layering for textured hair routines. L'Oreal Professionnel's May 2024 launch of Absolut Repair Molecular in South Africa also points to demand for higher-performing repair propositions that can support premium pricing in salons and specialty beauty retail.

A second opportunity lies in supply-side localization and faster go-to-market through South African manufacturing and contract services. Prime Product Manufacturing's March 2026 acquisition of L'Oreal South Africa's Midrand production facility, with stated doubled capacity across beauty categories, increases local capability for filling, packing, and private-label or contract manufacturing. This can shorten lead times and reduce import exposure for both multinationals and local brands. Localization also intersects with tighter compliance requirements tied to NRCS compulsory specifications and SANS-based benchmarks, giving an advantage to players that build QA, claims substantiation, and labeling readiness into product development for mass retail and cross-border distribution from South Africa into neighboring markets.

Recent Industry Developments

- January 2026: Unilever launched Sunsilk Wondermist in South Africa as part of a Gen Z-oriented brand transformation and social-first marketing push. The introduction of a science-backed hair mist supports regimen-based usage and expands Sunsilk's presence in lightweight leave-in formats that can be scaled through mass retail.

- December 2025: Unilever South Africa highlighted that local content in its locally manufactured products reached 80%, supported by a R100-million empowerment and localisation fund. Higher local sourcing of inputs such as chemicals, plastics, and fragrances strengthens supply continuity and can improve responsiveness for fast-turn hair care launches.

- May 2024: L'Oreal Professionnel launched the Absolut Repair Molecular haircare line in South Africa, positioned around repairing hair damage. The rollout adds competitive pressure in the premium repair segment across salons and specialist beauty retail, where advanced claims and professional endorsement can lift brand differentiation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of hair care products sold in South Africa for everyday cleansing, conditioning, styling, coloring, and treatment use across consumer channels, measured in USD for the years in scope.

Scope exclusions: Professional salon services revenue and barbering service revenue are excluded, even when they are linked to product use.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants and Dyes

- Hair Styling Products

- Perms and Relaxants

- Other Product Types

-

By Nature

- Natural / Organic

- Conventional/Synthetic

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty and Beauty Stores

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with understanding the size and structure of the South Africa beauty and personal care basket, and then narrowing it to hair care through public, repeatable data points. We referenced materials such as Statistics South Africa retail trade releases, South African Reserve Bank macro series, UN Comtrade trade flows for relevant hair preparations, and publications from customs and standards bodies that clarify product classifications.

To keep assumptions realistic, we also reviewed public company annual reports and investor decks for category cues, retailer and pharmacy group websites for shelf pricing patterns, and reputable press for policy or demand shifts. Where needed, we used paid access for company financials and news to cross-check local entity disclosures and corporate structure, and patent databases helped spot product activity that can change mix over time. These examples are illustrative, and many other public sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to stress-test pricing, channel mix, and category splits that are hard to resolve from public sources alone, particularly when South Africa promotions and pack-size trade-downs change frequently. We spoke with participants across manufacturing, brand teams, distributors, and retail managers, and we also checked views from professionals closer to end users to confirm what is actually moving on shelves.

Coverage was balanced across South Africa, and we re-opened interviews when desk signals and early model outputs did not match what practitioners reported in the market.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | |

| Mid tier: 54% | Functional/Unit leaders: 27% | |

| Smaller Players: 14% | Managers: 59% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where national consumer and retail signals are used to reconstruct the addressable hair care spend for South Africa, and then that total is split by product categories and channels using checks from interviews and observed market structure. Once the first cut is ready, it is corroborated with selective bottom-up approximations such as sampled shelf price bands times implied volumes, along with supplier and distributor sense checks that help correct overstatement in high-promotion categories.

Inputs used in the model include category price ladders (mass versus premium), channel share shifts (modern trade, specialty, and online), import reliance for certain subcategories, pack-size and usage frequency patterns, and macro indicators that affect discretionary spend. Forecasting is handled with scenario analysis supported by variable-level expectations from industry respondents, so changes in pricing, channel expansion, and mix upgrades are reflected without overfitting the trend line. If a bottom-up checkpoint has missing coverage for a niche category, we fill the gap using conservative penetration and price assumptions and then re-test it with at least one additional interview.

Data Validation & Update Cycle

Validation is done in a few passes so obvious issues are caught early and subtler ones are caught before final sign-off. Model outputs are compared against independent signals like trade direction, visible price movements, and channel expansion narratives, and then variances are investigated rather than averaged away.

Before publishing, another analyst reviews assumptions, formulas, and year-to-year movements to ensure they make business sense, and follow-up calls are triggered when a key input shifts or a respondent flags a mismatch. Reports are refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's South Africa Hair Care Market Market Sizing Compared With Other Published Estimates

Published values for South Africa hair care do not always match, even when the topic label looks the same, because the underlying definition and the measurement point can be different. In our checks, the biggest drivers were what is counted as product revenue versus services, whether values reflect retail selling price or another price point, and how base-year currency conversion is handled.

Salon hair services and in-salon treatments sit outside Mordor Intelligence's scope, which is one reason the 2025 product-only value can look smaller than estimates that blend products with service-led spending or attach higher channel markups. Differences also come from how companies treat promotions and pack-size trade-downs, and from refresh timing since short-term inflation and exchange rates can move USD totals quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 526.85 M (2025) | |

| Industry Publisher A | USD 950.08 M (2024) | Uses a different base year and does not clearly state whether values are retail selling price or another pricing basis, which can inflate totals when promotions and taxes are treated differently. |

| Industry Publisher B | USD 746.09 M (2024) | Headline sizing appears internally inconsistent across years on the source page, and the definition around what is included in hair care versus adjacent personal care items is not made explicit, which can shift the addressable value. |

The spread in the table mainly comes down to scope and measurement clarity, not just forecast optimism. When product categories, channel pricing basis, and year-specific currency timing are kept consistent, the estimate becomes easier to reproduce and simpler to audit with interviews and visible market signals.

Key Questions Answered in the Report

What is the current value of the South Africa hair care market?

The market is valued at USD 557.79 million in 2026, with clear growth momentum toward USD 741.46 million by 2031.

Which product type is most popular among South African consumers?

Conditioners command the largest share at 32.02% thanks to their role in moisture retention and manageability.

How fast is the premium segment growing?

Premium hair care products are expanding at a 7.08% CAGR, reflecting rising demand for advanced formulations.

Which retail channels will see the highest future growth?

Specialty and beauty stores are projected to grow at an 7.72% CAGR, driven by expert advice and curated assortments.

Page last updated on: