Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.20 Billion |

| Market Size (2026) | USD 6.30 Billion |

| Market Size (2031) | USD 7.76 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Nigeria Oil And Gas Upstream Market size is projected to expand from USD 6.20 billion in 2025 and USD 6.30 billion in 2026 to USD 7.76 billion by 2031, registering a CAGR of 4.26% between 2026 to 2031.

Indigenous independents are absorbing onshore and shallow-water acreage divested by international majors, while the federal government directs capital toward gas infrastructure that can monetize 209 trillion cubic feet of proven reserves. Regulatory clarity under the Petroleum Industry Act (PIA) is unlocking project finance that had stalled for more than a decade, and security improvements are lifting effective crude output. Offshore deep-water developments continue to dominate value creation, but unconventional pilots are scaling faster as operators apply hydraulic-fracturing and subsea-tieback technologies. Together, these shifts reshape the investment logic across the Nigerian upstream oil and gas market as capital bifurcates toward deep-water gas and indigenous-led on-shore crude redevelopment.

Key Report Takeaways

- By location of deployment, offshore operations led with 68.1% of Nigeria's upstream oil and gas market share in 2025; unconventional wells are forecast to expand at an 8.7% CAGR through 2031.

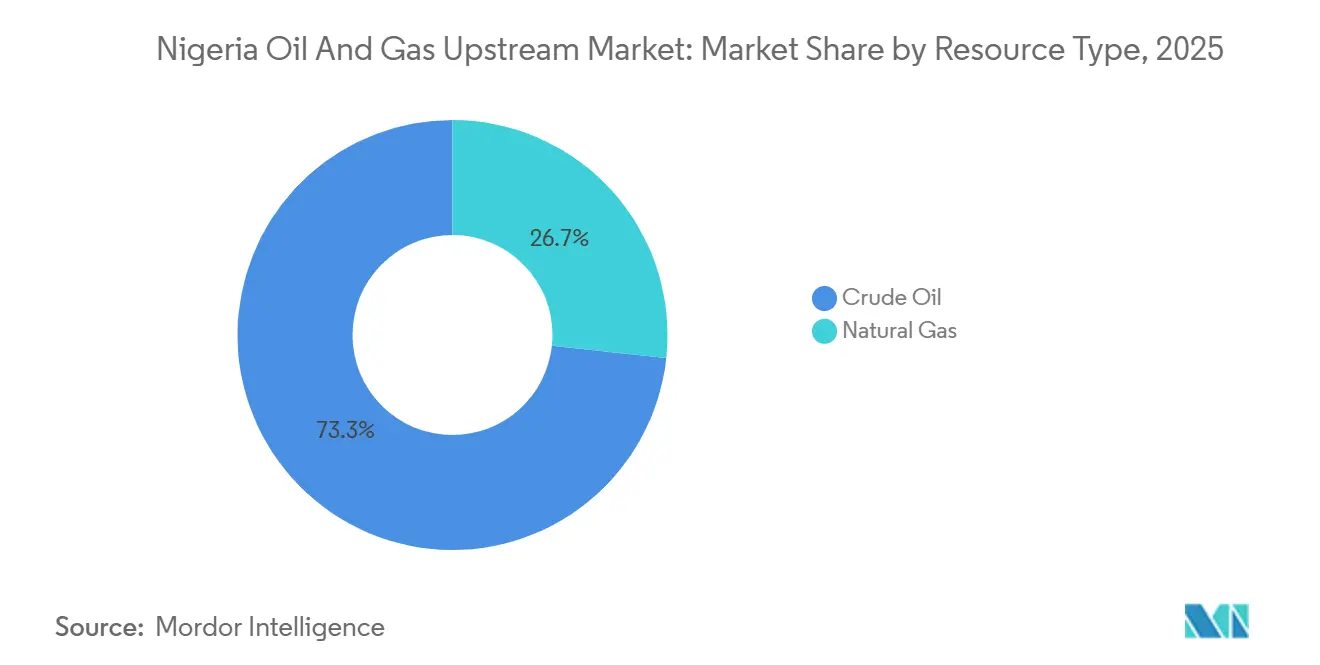

- By resource type, crude oil captured 73.3% of revenue in 2025, while natural gas is projected to post a 6.0% CAGR to 2031 as Train 7 and the AKK pipeline come onstream.

- By well type, conventional drilling held 96.4% of value in 2025; unconventional wells are expected to grow at an 8.7% CAGR through 2031.

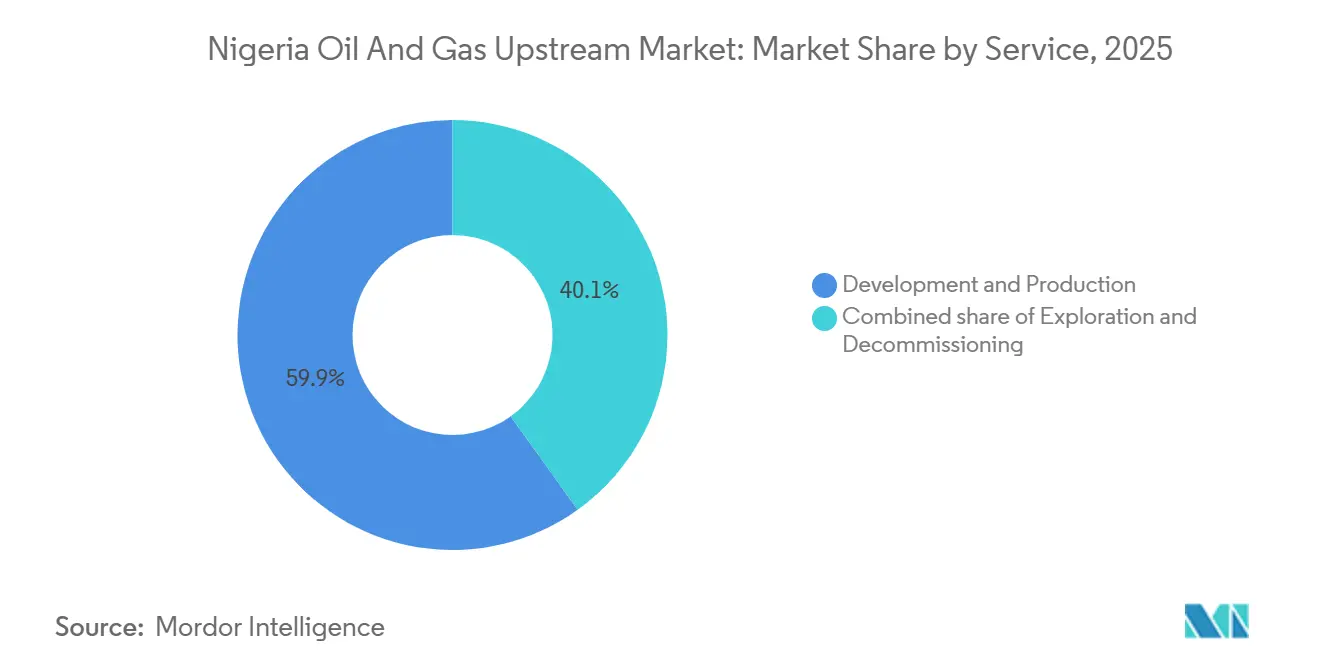

- By service, development and production accounted for 59.9% of 2025 spending, whereas decommissioning is expected to grow at 7.9% a year as 87 offshore platforms near end-of-life.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petroleum Industry Act (PIA) improves fiscal clarity | +1.2% | National, with concentration in Niger Delta and offshore deepwater zones | Medium term (2-4 years) |

| Crack-down on oil theft raises effective output | +0.9% | Niger Delta states (Rivers, Bayelsa, Delta), onshore and shallow-water fields | Short term (≤ 2 years) |

| "Decade-of-Gas" monetisation push (NLNG Train-7, AKK) | +1.4% | National, with infrastructure hubs in Bonny Island (Rivers) and northern distribution corridors | Long term (≥ 4 years) |

| CCUS pilots unlock future-proof barrels | +0.3% | Offshore deepwater fields, pilot projects in Bonga and Egina complexes | Long term (≥ 4 years) |

| Indigenous independents revive marginal fields | +0.7% | Onshore Niger Delta, shallow-water acreage divested by IOCs | Medium term (2-4 years) |

| Digital oilfield analytics cut well downtime | +0.5% | National, with early adoption in offshore platforms and NNPC-operated fields | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Petroleum Industry Act Improves Fiscal Clarity

The PIA replaced a patchwork of decrees and capped government take at 60% for deep-water projects and 75% for on-shore fields, compared with earlier effective rates above 85%.[1]Nigerian Upstream Petroleum Regulatory Commission, “PIA Fiscal Framework 2024,” NUPRC.GOV.NG NNPC’s commercialization under the Companies and Allied Matters Act eliminated opaque joint-venture cash calls, improving confidence among lenders. Transparent bidding has already produced 57 new exploration licenses, 40% more than in the preceding five-year span. Gas-pricing reforms now permit cost-reflective domestic tariffs, mitigating a long-standing disincentive to invest in gathering systems. Stabilization guarantees for projects beyond USD 500 million further lower political-risk premiums, though enforcement has not yet faced a serious judicial test.

Crack-down on Oil Theft Raises Effective Output

A multi-agency security surge dismantled 395 illegal refineries and reduced theft-linked losses from 400,000 b/d in early 2024 to under 50,000 b/d by December 2024. The Trans Niger Pipeline restart added 120,000 b/d of export capacity, helping Nigeria meet its OPEC+ quota for the first time since 2020. Real-time sensors on 18 main lines now alert operators to pressure drops within seconds, narrowing illicit tapping windows. Deep Blue maritime assets have cut piracy incidents 68% year-on-year, trimming insurance add-ons by USD 0.80 per barrel. Community infrastructure trusts funded by 3% of operating revenue have softened sabotage risk, despite occasional payment-related flare-ups.[2]Jaewon Kang, “Nigeria Indigenous Operators,” Wall Street Journal, WSJ.COM

“Decade-of-Gas” Monetization Push

The USD 10 billion Train 7 expansion will lift liquefaction capacity to 30 Mtpa by late 2026, vaulting Nigeria ahead of Algeria among African LNG exporters. The USD 2.8 billion, 614-km AKK pipeline is designed to ship 2.2 Bcf/d into northern industrial clusters beginning 4Q 2026. Domestic-supply obligations introduced under the PIA require 30% of produced gas to feed local power and fertilizer plants, anchoring off-take for gathering schemes. Chevron and TotalEnergies have earmarked USD 1.2 billion for Escravos and Amenam infrastructure that targets 1.5 Bcf/d of incremental capture by 2027. Execution risks linger because power-sector arrears above NGN 3 trillion undermine payment discipline.

Indigenous Independents Revive Marginal Fields

Local players have spent USD 4.5 billion acquiring 30-plus legacy blocks since 2021, bringing 41 marginal fields to first oil and adding 180,000 b/d of new supply. Seplat’s USD 1.28 billion deal for ExxonMobil’s shallow-water assets lifted its production by 95,000 boe/d at breakeven 25% below IOC thresholds. PIA royalty holidays and accelerated depreciation lower the effective tax take to 40% for newcomers, improving netbacks. Modular refineries, such as Waltersmith’s 5,000 b/d plant, create downstream hedges and bypass pipeline constraints. Financing remains a bottleneck because local banks restrict upstream exposure, forcing operators into mezzanine debt costing more than 18%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pipeline vandalism & security risks persist | -0.8% | Niger Delta onshore and shallow-water zones, particularly Rivers, Bayelsa, and Delta states | Short term (≤ 2 years) |

| IOC divestment delays / regulatory bottlenecks | -0.5% | National, with concentration in onshore and shallow-water asset transfers | Medium term (2-4 years) |

| ESG-driven capital flight raises funding cost | -0.6% | Onshore crude oil projects; less impact on offshore gas and deepwater developments | Long term (≥ 4 years) |

| Climate-driven extreme weather downtime offshore | -0.3% | Offshore deepwater fields, particularly in the Bight of Benin and Gulf of Guinea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pipeline Vandalism and Security Risks Persist

Vandalism incidents climbed 12% in 1Q 2025 versus 4Q 2024, underscoring residual insecurity despite the headline 90% theft reduction. Four fresh breaches on the Trans Niger line since December 2024 forced cumulative shutdowns of nearly a month and deferred USD 18 million in production values. Militant attacks on export manifolds, like the January 2025 Forcados incident that halted 420,000 barrels, expose latent grievance channels. Offshore piracy has eased but persists; hijackers boarded a Bonga supply vessel in late 2024, stealing USD 2.3 million in gear. Insurance premiums into Nigerian ports remain 35% above regional averages, inflating logistics costs and trimming trader liquidity.

ESG-Driven Capital Flight Raises Funding Cost

Shell and ExxonMobil exited multiple onshore licenses in 2024, citing decarbonization targets and high flaring intensity of 7.2 m³/bbl. European pension funds controlling EUR 4 trillion have black-listed regions where routine flaring exceeds 5 m³/bbl, prompting USD 1.8 billion of portfolio withdrawals. Banks now charge 200–300 bp carbon premiums on loans to on-shore oil projects, pushing borrowers toward mezzanine debt priced above 18%. Development-finance agencies have offered USD 600 million in blended finance for projects meeting ISO 14001 standards, but annual compliance audits costing USD 0.5 million deter smaller producers. Deep-water gas ventures, with 40% lower Scope 1+2 emissions, continue to attract mainstream capital, amplifying the bifurcation between clean-tech aligned assets and legacy on-shore crude.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Deep-Water Anchors Offshore Dominance

Offshore operations captured 68.1% of the 2025 value, reflecting the central role of Bonga, Egina, Erha, and emergent Zabazaba-Etan hubs that jointly deliver 850,000 b/d with minimal theft exposure. The Nigerian upstream oil and gas market size for deep-water segments is forecast to strengthen at a 4.7% CAGR to 2031 as operators expand brownfield clusters via subsea tiebacks. TotalEnergies has allocated USD 1.5 billion to the Ikike discovery, and Shell is investing USD 2.3 billion in Bonga Southwest Aparo, moves that illustrate how brownfield deep-water options yield faster paybacks than greenfield exploration. On-shore acreage—31.9% of 2025 value—still supports investment thanks to low USD 8 million well costs and PIA tax relief, despite 12% higher vandal-risk in early 2025.

Capital allocation trends confirm offshore primacy: 72% of the USD 12 billion in upstream pledges disclosed between January 2024 and February 2025 targeted deep-water zones. Chevron’s Nsiko start-up at 50,000 b/d showcases multilateral wells that drive per-barrel costs 30% below conventional models. On-shore independents counter these scale disadvantages by integrating modular refineries, raising project returns 15–20% and buffering logistics interruptions. The Nigerian upstream oil and gas market continues to reward operators that optimize the offshore-on-shore mix against security, cost, and carbon vectors.

By Resource Type: Gas Acceleration Narrows Crude’s Lead

Crude oil delivered 73.3% of 2025 revenue, but natural gas is set to outperform at a 6.0% CAGR through 2031 thanks to Train 7 capacity and the AKK trunk line. The Nigerian upstream oil and gas market size for gas projects will therefore expand faster than crude, a reversal of historical norms. Domestic gas obligations mandating a 30% local allocation create a stable off-take base, although weak enforcement and sub-economic flaring fees blunt full impact. Rising Asian spot LNG premiums, USD 12/MMBtu in early 2025, magnify Train 7’s export upside.

While NNPC aims for crude output of 2.6 million b/d by late 2026, divestments by Shell and ExxonMobil signal capital re-direction toward lower-carbon gas. TotalEnergies’ Ikike and Eni’s Etan deep-water gas projects attracted USD 3.2 billion in combined funding in 2024-25, dwarfing on-shore crude inflows. Associated-gas utilization still lags at 60%, leaving USD 1.8 billion a year in unrealized revenue, but upcoming gathering schemes can lift capture rates and further tilt the Nigeria upstream oil and gas market toward gas monetization.

By Well Type: Unconventional Pilots Challenge Conventional Hegemony

Conventional wells dominated 96.4% of the 2025 value, yet unconventional pilots are forecast to grow 8.7% a year as the PIA streamlines hydraulic-fracturing permits. Chevron’s multilateral designs in Nsiko cut development cost per barrel by 30% and validate the economic logic of tight-sand deep-water exploitation. TotalEnergies’ Ikike aims to unlock 500 million boe from tight reservoirs, marking the first large-scale fracture-stimulated deep-water system in the Nigerian upstream oil and gas market.

Conventional acreage benefits from legacy infrastructure and low USD 12-18 per-barrel lifting costs, but productivity is sliding; average well rates declined to 1,400 b/d in 2024. Operators are piloting polymer flooding and CO₂ injection that could raise recovery factors to 40%. With only three unconventional pilots online today, the 2026-28 cohort of FIDs will be pivotal for scaling. Should commercial success materialize, the Nigerian upstream oil and gas market could witness a structural pivot similar to the U.S. shale inflection of the 2010s.

By Service: Decommissioning Surge Outpaces Exploration

Development and production made up 59.9% of 2025 spend as brownfield tie-backs in Bonga, Egina, and Erha overshadowed frontier wildcats. Decommissioning outlays are projected to climb 7.9% annually through 2031 because 87 offshore platforms and 340 onshore heads enter retirement. Operators must pre-fund 120% of estimated abandonment cost over the last 10 years of field life, straining balance-sheets of asset buyers such as Seplat, which booked USD 320 million of provisions, 25% of its purchase price, in 2024.

Shell’s scheduled 2027 removal of the Bonga Main facility, budgeted at USD 800 million, will test local heavy-lift capacity. Exploration, only 18.2% of 2025 services, remains subdued as seismic campaigns fell 22% year-on-year and operators favor near-field tie-backs. Digital-oilfield tools adopted by NNPC slashed downtime at Forcados by 50%, hinting that predictive analytics can defer costly well workovers and shape a leaner Nigeria upstream oil and gas market services mix.

Geography Analysis

Nigeria hosts 37 billion barrels of proven crude and 209 Tcf of gas, 95% of which lie in the nine-state Niger-Delta.[3]Nigerian Upstream Petroleum Regulatory Commission, “Reserves Data 2024,” NUPRC.GOV.NG Deep-water acreage in the Gulf of Guinea supplies 850,000 b/d and anchors 68.1% of the Nigeria upstream oil and gas market value, growing 4.7% annually thanks to Egina, Ikike, Bonga, and Etan fields. Rivers State is the gas monetization nexus; Train 7 lifts LNG capacity to 30 Mtpa by late 2026, while AKK channels 2.2 Bcf/d northward.

Bayelsa and Delta onshore licenses changing hands to Seplat, Aiteo, and Oando underpin 5.2% CAGR growth despite a 12% vandalism uptick in early 2025. Meanwhile, Deep Blue patrols cut piracy 68%, lowering offshore operating risk, though a November 2024 hijack at Bonga underscores residual threats. Akwa Ibom maintains relative calm due to timely community-trust disbursements, aiding Qua Iboe and Amenam reliability. Northern frontier basins in the Chad and Benue troughs received fresh licenses but remain pre-commercial as of early 2026.

Competitive Landscape

The Nigerian upstream oil and gas market is semi consolidated. Indigenous firms now control more than 30 onshore and shallow-water licenses, lifting combined production to 330,000 boe/d and eroding IOC share. Deep-water gas remains IOC turf, favored for lower carbon intensity and technical barriers. Local independents thrive on lower cost structures, 25% below IOC averages, and political access that speeds permits.

Technology is differentiating players. NNPC’s AI-driven maintenance halves downtime at Forcados, whereas Chevron’s multilateral architecture cuts Nsiko costs by 30%. TotalEnergies and Eni file patents on subsea compression that extend deep-water plateaus by more than a decade, capabilities smaller firms cannot easily replicate. Modular-refinery pioneers such as Waltersmith and Aradel integrate downstream margin capture, disrupting the export-only paradigm.

Nigeria Oil And Gas Upstream Industry Leaders

Chevron Corporation

ExxonMobil Corporation

Royal Dutch Shell PLC

Nigerian National Petroleum Corporation

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nigeria's state oil company, NNPC, is set to commence exports of a new light, sweet crude grade named Cawthorne in March 2026. The first shipments, expected in the third week of March, could increase crude and condensate supply to approximately 1.7 million barrels per day (bpd). This development is anticipated to support recovery efforts and enhance Nigeria's positioning within OPEC+.

- February 2026: President Bola Tinubu mandated that all oil and gas revenues be deposited directly into the federal government’s Federation Account. This directive ends previous revenue retention practices by NNPC and regulatory agencies. The reform is intended to enhance fiscal transparency, strengthen public finances, and boost investor confidence in the revenue management of Nigeria’s upstream sector.

- February 2026: Nigeria’s upstream regulator has encouraged NNPC Ltd to take part in the ongoing 2025 oil licensing round alongside private and international operators. This initiative aims to foster stronger exploration and production partnerships, expand upstream activities, and support the development of petroleum assets across the country.

- December 2025: Nigeria’s upstream regulatory authority initiated the 2025 oil licensing round, offering 50 blocks across onshore, shallow-water, frontier, and deepwater areas. The round aims to attract investments of around USD 10 billion, fostering new exploration and production activities. This initiative seeks to add long-term production capacity and revitalize under-invested upstream operations in the Niger Delta and other regions.

Nigeria Oil And Gas Upstream Market Report Scope

The oil and gas upstream market encompasses the exploration and production (E&P) segment of the petroleum industry. It includes activities aimed at identifying hydrocarbon reserves and extracting them from both onshore and offshore fields.

The scope of the Nigerian oil and gas upstream market report includes:

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decommissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decommissioning |

Key Questions Answered in the Report

How large is the Nigeria upstream oil and gas market in 2026?

It stands at USD 6.30 billion in 2026 and is on track for USD 7.76 billion by 2031.

Which segment grows fastest to 2031?

Unconventional wells lead with an expected 8.7% CAGR.

What propels gas growth after 2026?

The NLNG Train 7 expansion and the AKK pipeline together boost liquefaction capacity and domestic off-take.

Why are IOCs divesting on-shore assets?

Shareholder ESG pressures and high flaring intensities raise carbon risk, steering capital toward deep-water gas instead.

What security measures curbed oil theft?

A joint military–regulatory sweep dismantled illegal refineries, fitted real-time pipeline sensors and deployed Deep Blue maritime patrols, cutting theft losses by 90%.

How big is decommissioning's opportunity?

Decommissioning spend is forecast to climb 7.9% a year as 87 offshore platforms reach design life before 2031.

Page last updated on: