Sorghum Market Size and Share

Sorghum Market Analysis by Mordor Intelligence

The sorghum market is projected to grow from USD 14.70 billion in 2025 to USD 15.30 billion in 2026 and is forecast to reach USD 19.00 billion by 2031 at a 4.43% CAGR over 2026-2031. Strong consumption in Africa, rising feed substitution in Asia-Pacific, and expanding biofuel mandates in North and South America are accelerating volume growth. Gluten-free positioning is lifting consumer uptake in North America and Europe, while drought resilience is pushing acreage shifts in water-stressed zones of Australia, India, and the Middle East. Policy uncertainty around Sudanese exports continues to unsettle spot prices, yet sustained investments in traceability, carbon-credit programs, and hybrid breeding pipelines are widening commercial opportunities. Competitive intensity remains moderate because the top five grain traders retain scale advantages in origination, storage, and logistics.

Key Report Takeaways

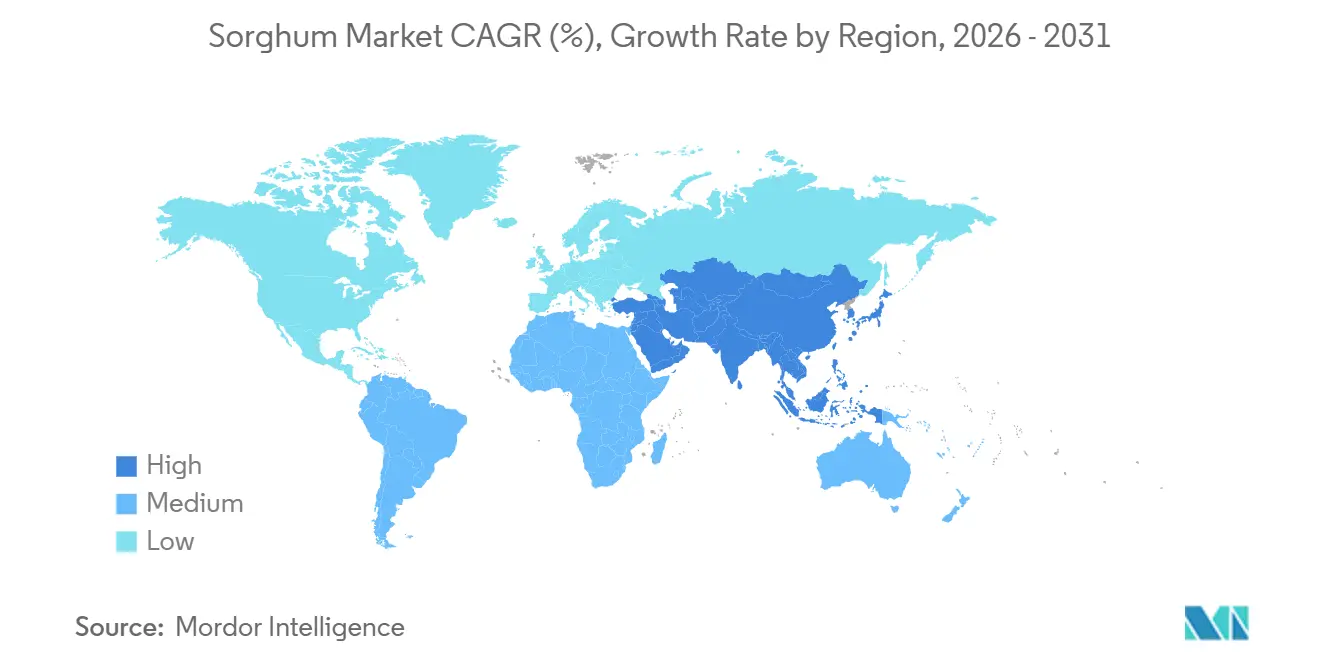

- By geography, Africa led with 34.8% consumption share of the sorghum market size in 2025, while Asia-Pacific is projected to expand at a 5.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sorghum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for gluten-free grains in human diets | +0.8% | Global, with peak adoption in North America and Europe | Medium term (2-4 years) |

| Expanding use of sorghum in animal feed rations | +1.2% | Global, strongest in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Climate resilience and drought-tolerant characteristics | +1.0% | Africa, Middle East, and South America | Long term (≥ 4 years) |

| Growing biofuel and industrial ethanol blending mandates | +0.7% | North America and South America | Medium term (2-4 years) |

| Emerging role in functional and fermented beverages | +0.3% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Carbon-credit incentives for low-input cereal rotations | +0.2% | Global, early gains in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Gluten-Free Grains in Human Diets

Diagnoses of celiac disease and non-celiac gluten sensitivity are redirecting consumer spend toward gluten-free staples. Between 2023 and 2025, the United States Department of Agriculture recorded a 22% rise in sorghum milling volumes destined for human consumption [1]Source: United States Department of Agriculture Economic Research Service, “Sorghum Milling for Human Consumption Data,” USDA.gov . European manufacturers in Italy and Spain scaled imports from Argentina and the United States to secure clean-label inputs for pasta and bakery ranges. Urban millennials and Generation Z consumers value allergen avoidance and are adopting sorghum-based snacks that also carry protein and antioxidant claims. Food processors are investing in extrusion and fermentation lines to address mouthfeel issues that previously restricted adoption, giving the sorghum market fresh traction in premium convenience foods. African smallholders benefit as domestic millers capture higher margins by selling refined sorghum flour to both local supermarkets and export channels.

Expanding Use of Sorghum in Animal Feed Rations

Feed formulators are using sorghum to offset elevated corn prices that spiked after United States weather shocks in 2024. China imported 8.7 million metric tons in 2024, a 66% increase from 2023 according to the ITC Trade Map data, reflecting state-owned mills’ effort to diversify cereal inputs. Middle Eastern buyers mirrored the shift because non-GMO grain aligns with regulatory preferences. Research published in 2024 confirmed that sorghum delivers metabolizable energy on par with corn in broiler diets, dismantling a scientific barrier to wider substitution [2]Source: American Society of Animal Science, “Nutritional Equivalence of Sorghum in Broiler Diets,” Academic.oup.com. Gulf Coast export terminals shorten sailing distances to Asia, trimming freight bills relative to Midwest corn. In humid markets, formulators appreciate sorghum’s lower mycotoxin risk, which reduces feed-quality downgrades. Together, these efficiencies are expanding the sorghum market in compound animal feeds.

Climate Resilience and Drought-Tolerant Characteristics

Sorghum uses up to 40% less irrigation than corn and withstands hotter conditions, features that resonate in areas facing groundwater depletion. The Food and Agriculture Organization documented a 12% acreage jump across sub-Saharan Africa between 2023 and 2025. Governments in the Middle East are trialing sorghum within food-security campaigns to reduce reliance on imported cereals that demand higher water footprints. Indian research institutes released heat-tolerant hybrids for rainfed belts in Maharashtra and Karnataka, aiming to smooth yield variability caused by uneven monsoon rainfall. Long-term, climate adaptation imperatives are projected to channel sizeable investments into sorghum breeding, acreage expansion, and value-chain infrastructure, deepening the sorghum market footprint.

Growing Biofuel and Industrial Ethanol Blending Mandates

Carbon-offset buyers are rewarding sorghum growers who adopt no-till practices and reduced nitrogen use. European regulators now allow sorghum-based rotations to qualify for eco-scheme payments, attracting growers seeking diversified revenue. Digital measurement platforms track soil-organic-carbon gains, supporting transparent credit issuance. These incentives support the adoption of rotation shifts in higher-yielding regions and contribute to the long-term growth of the sorghum market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility versus substitute feed grains | -0.6% | Global, most acute in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Lower average yields than corn and wheat | -0.5% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Trade-policy uncertainty on Sudanese export volumes | -0.3% | Africa and Middle East | Short term (≤ 2 years) |

| Limited genomic breeding investments outside top producers | -0.4% | Global, most pronounced in Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility Versus Substitute Feed Grains

Sorghum prices are influenced by corn and wheat futures, leading to rapid fluctuations that pose challenges for budgeting. Feed mills in Asia-Pacific and Middle East markets switch back to corn whenever sorghum premiums spike, eroding demand consistency. Local currency depreciation adds another layer of risk because sorghum invoices are denominated in United States dollars. Smaller buyers lack robust hedging tools, leaving them vulnerable to squeezes. Supply-chain fragmentation heightens search costs, and the absence of standardized forward contracts prevents growers from locking in margins ahead of planting. Until volatility eases, this restraint will temper the overall sorghum market growth rate.

Lower Average Yields Than Corn and Wheat

Global sorghum yields hovered near 1.6 metric tons per hectare in 2025 compared with 5.9 metric tons for corn and 3.5 metric tons for wheat [3]Source: United States Department of Agriculture Foreign Agricultural Service, “Global Crop Production Database 2025,” apps.fas.usda.gov . Seed companies focus research budgets on corn, which generates higher royalty streams. Public breeding programs in Africa and India face funding gaps that lengthen variety-release cycles. The lack of widespread hybrid vigor restricts yield potential, while precision agriculture adoption among smallholders remains limited. Farmers in temperate zones hesitate to switch acreage away from corn unless yield parity improves. This structural gap constrains the sorghum market’s ability to seize share from competing cereals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Africa dominated the sorghum market in 2025 with 34.8% of global consumption. In 2024/2025, according to the United States Department of Agriculture (USDA), Nigeria harvested 6.42 million metric tons, while Sudan contributed 3.3 million metric tons despite sanctions-related logistics hurdles. Ethiopia expanded its acreage as improved varieties reached drought-prone lowlands. Government procurement programs and tariff policies aimed at curbing wheat imports continue to reinforce sorghum’s role in household diets. Post-harvest inefficiencies persist, yet investments in storage and milling are improving throughput.

Asia-Pacific is the fastest-growing region, advancing at a 5.7% CAGR to 2031. China remains the single largest importer and relies on United States, Argentine, and Australian origins to diversify feedgrain inputs. India produced 4.6 million metric tons in 2025 as per the USDA data, supported by minimum support prices and crop-insurance subsidies that encourage cultivation in rainfed belts. Thailand and Myanmar entered premium export niches, targeting Japanese and South Korean buyers that demand non-GMO certification. Australian output rebounded to 2.5 million metric tons in 2025 as per the USDA data after favorable rainfall, reinforcing westbound trade lanes. Collectively, rising feed demand, policy support for climate-resilient crops, and niche food applications are propelling the Asia-Pacific sorghum market.

North America, Europe, South America, and the Middle East collectively account for the remaining share of global sorghum consumption. In North America, the United States is the leading supplier, with exports projected to reach 5.4 million metric tons in 2024, according to ITC Trade Map data. Ethanol blending mandates and strong feed demand drive this. In Europe, growth remains modest as sorghum acreage competes with wheat and barley. Rising demand for gluten-free foods and organic livestock feed increases import needs in countries such as France, Italy, and Spain. South America sees expansion as Argentina and Brazil incorporate sorghum into crop rotations to reduce reliance on soybean-corn monocultures and capitalize on export premiums. In the Middle East, sorghum’s non-GMO status supports its use in poultry and dairy production, particularly in Saudi Arabia and the United Arab Emirates, contributing to a positive outlook for the global sorghum market.

Competitive Landscape

The sorghum market is moderately concentrated. Cargill Incorporated, Archer Daniels Midland Company, Louis Dreyfus Company, COFCO Corporation, and Bunge Limited controlled a major share of trade flows in 2025. Integrated supply chains, from inland grain elevators in the United States Great Plains to Gulf Coast export terminals, allow these incumbents to capture origination and logistics margins. They also operate destination-crushing assets that supply ethanol producers and feed mills, enhancing throughput efficiency and negotiating leverage.

Competitive dynamics are shifting as West African cooperatives in Nigeria and Burkina Faso bypass traditional traders by executing direct sales to Middle Eastern and Asian buyers. Blockchain-enabled platforms reduce transaction friction, allowing smallholder collectives to achieve 5% to 7% higher Free on Board prices. COFCO Corporation introduced blockchain traceability to assure Chinese feed mills of source integrity, improving compliance with antibiotic-free livestock protocols.

Technology adoption remains uneven. Precision-agriculture tools such as variable-rate seeding and drone-based crop monitoring are standard among large-scale United States and Australian growers but scarce among African smallholders. Artificial intelligence algorithms now optimize vessel routing and inventory allocation for the top traders, reducing demurrage costs. Compliance with International Organization for Standardization quality standards and European Union mycotoxin thresholds is emerging as a critical differentiator for exporters. Although scale advantages favor vertically integrated players, niche gaps persist for agile cooperatives that can deliver certified organic, carbon-neutral, or identity-preserved sorghum, enabling a vibrant and evolving competitive field within the global sorghum market.

Recent Industry Developments

- July 2025: Sudan officially joined the FAO One Country One Priority Product (OCOP) global initiative, selecting sorghum as its priority agricultural product under the program. This initiative seeks to enhance the sorghum value chain through value addition, diversification, and sustainable production, benefiting local farmers and increasing market opportunities. The decision underscores the increasing international recognition of sorghum's importance in food security and resilient agrifood systems.

- July 2025: The International Fund for Agricultural Development (IFAD) initiated a pilot program to mechanize sorghum production in Zimbabwe. The program seeks to enhance smallholder productivity and incomes by introducing mechanized technologies for planting, harvesting, and processing. Its objectives include addressing labor bottlenecks, minimizing post-harvest losses, and strengthening market linkages for sorghum producers. This initiative highlights increasing development efforts to promote sorghum as a key crop for food security and rural income growth in Southern Africa.

- May 2025: DEKALB has announced the introduction of two new grain sorghum hybrids, DKS43-76 and DKS49-76, for the 2025 growing season. These hybrids offer enhanced wind and lodging resistance, improved stalk and root strength, and stacked tolerance to pests such as sugarcane aphid and sorghum downy mildew. Field trials conducted in 2024 demonstrated strong yield potential and resilience, with the hybrids maintaining performance even under severe wind conditions, providing significant benefits to growers in the Midwest and southern United States.

Global Sorghum Market Report Scope

The Sorghum Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Seasonality Analysis, and Logistics and Infrastructure. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Ukraine | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Romania | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | India | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Thailand | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Myanmar | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Sudan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Ethiopia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Burkina Faso | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Uruguay | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Ukraine | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Romania | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| China | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Thailand | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Myanmar | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Sudan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Ethiopia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Burkina Faso | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Uruguay | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the current and forecast value of the sorghum market?

The sorghum market size stands at USD 15.3 billion in 2026 and is projected to reach USD 19.0 billion by 2031.

Which region leads global consumption of sorghum?

Africa leads with 34.8% of global consumption in 2025, anchored by staple-food demand in Nigeria, Sudan, and Ethiopia.

Which region is growing the fastest for sorghum demand?

Asia-Pacific is forecast to grow at a 5.7% CAGR through 2031, driven by Chinese feed imports and Indian production gains.

How does sorghum compare with corn for animal feed?

Research confirms that sorghum delivers comparable metabolizable energy to corn in broiler diets, supporting its substitution when corn prices rise.

Why is sorghum attractive for biofuel production?

Sorghum ethanol carries lower greenhouse-gas intensity scores than corn ethanol, qualifying for favorable credits under North and South American low-carbon fuel policies.

Page last updated on: