Millet Market Size and Share

Millet Market Analysis by Mordor Intelligence

The Millet market size is expected to grow from USD 12.60 billion in 2025 to USD 13.22 billion in 2026 and is forecast to reach USD 16.78 billion by 2031 at 4.89% CAGR over 2026-2031. The climb reflects a decisive industry pivot toward climate-resilient crops as water scarcity, erratic monsoons, and rising temperatures undermine traditional cereals. Demand also benefits from millet’s 70% lower irrigation requirement versus rice, its proven capacity to survive on just 200-400 mm of rainfall, and its widening role in functional foods that command price premiums of 40-60% over commodity grains. Processing investments from conglomerates such as ITC Limited and policy interventions like India’s Public Distribution System inclusion have accelerated acreage expansion, while forward contracts and futures listings improve price discovery for risk-averse growers.

Key Report Takeaways

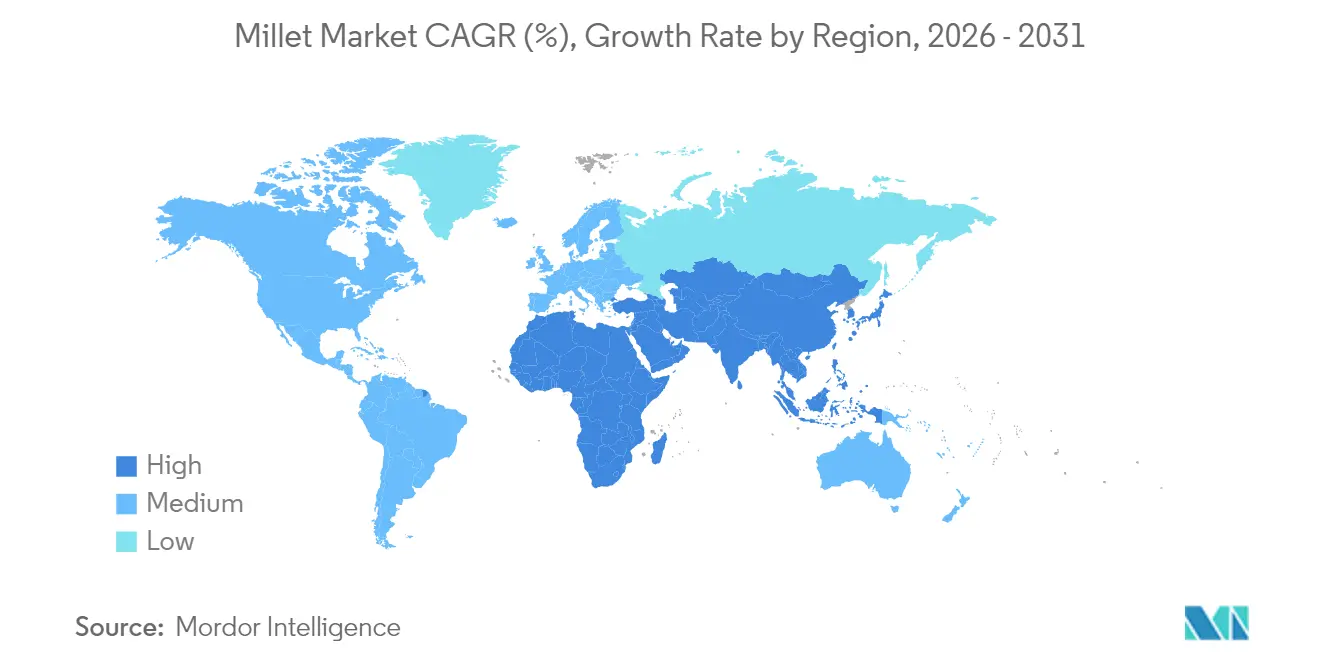

- By geography, Asia-Pacific led with a 45.72% millet market consumption value in 2025, while Africa is forecast to expand at a 5.14% CAGR through 2031, the fastest regional growth trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Millet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-resilient crop advantage | +1.2% | Global, highest in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Surge in functional food and beverage formulation | +0.8% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government millet missions and subsidies | +0.7% | India, Nigeria, Niger, and Mali | Short term (≤ 2 years) |

| Growing demand in gluten-free commodity trading | +0.6% | North America and Europe | Medium term (2-4 years) |

| Accelerated Research and Development in stress-tolerant varieties | +0.4% | Global research hubs, and spill-over to producing regions | Long term (≥ 4 years) |

| Carbon-credit potential for dryland farmers | +0.3% | Semi-arid zones worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate Resilient Crop Advantage

Millet’s capacity to produce dependable yields on marginal land turns the crop into a strategic hedge against heat and drought shocks. Varieties withstand 200-400 mm of annual rainfall, while rice demands roughly 1,200 mm. Breakthrough “resurrection millet” lines even rehydrate embolized xylem tissue after complete desiccation, a trait that safeguards yield when competing cereals lose 30-50% of output under drought.[1]Source: Agricultural Research Service, “Resurrection Millet: A Plant That Revives After Severe Drought,” ARS.USDA.GOV As climate volatility intensifies, governments incorporate millet into food-security strategies, and growers extend cultivation onto fallow, rain-fed acreage, enlarging the millet market.

Surge in Functional Food and Beverage Formulation

The functional food boom elevates millet from a subsistence staple to a premium ingredient. Nutritional analyses show 60-70% carbohydrates and up to 12.1% protein alongside high calcium and magnesium densities. Meta-analysis across 19 trials reveals millet consumption cuts fasting blood glucose by 11.8% and post-prandial glucose by 15.1%, legitimizing disease-management claims for finished products. Pearl millet flour now substitutes up to 20% of wheat in gluten-free breads without sensory penalties, sustaining the premium segment’s double-digit growth. These findings encourage processors to introduce high-margin snacks, cereals, and beverages that further enlarge the millet market.

Government Millet Missions and Subsidies

Public policy accelerates adoption by guaranteeing markets and lowering on-farm risk. India designated 2023 the International Year of Millets, embedded the grain in the Public Distribution System, and set a USD 100 million export target by 2025.[2]Source: Permanent Mission of India, “Millet at the United Nations,” PMINEWYORK.GOV.IN Similar initiatives in Nigeria, Niger, and Mali include subsidized seed, mechanization grants, and community storage units, actions that trimmed historic post-harvest losses of 20-30% to near 15%. These missions bring orchestrated procurement, market-linkage programs, and farmer-field schools that collectively support millet market expansion.

Growing Demand in Gluten-Free Commodity Trading

Gluten-free demand moved beyond celiac management into mainstream wellness, reshaping commodity flows. India exported 146,000 metric tons of millet in FY 2024, earning USD 70.89 million, a sharp pivot from a historically domestic-focused supply chain.[3]Source: APEDA, “Indian Millet Exports,” APEDA.GOV.IN Grading protocols and futures contracts introduced on regional exchanges bolster price transparency and hedge tools, drawing institutional buyers into the millet market. Western millers prefer millet’s native mineral profile and longer shelf life versus rice-based flours, fueling a trade corridor that widens the millet market size.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited mechanization and yield gap | -0.9% | Sub-Saharan Africa, and smallholder belts in South Asia | Medium term (2-4 years) |

| Volatile global commodity pricing | -0.6% | Export-dependent regions worldwide | Short term (≤ 2 years) |

| Infrastructure deficit in post-harvest handling | -0.5% | Sub-Saharan Africa, rural India | Medium term (2-4 years) |

| Competition from high-productivity cereals | -0.4% | Irrigated zones worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Mechanization and Yield Gap

Mechanized planting and harvesting reach barely 15% of millet acreage in Africa versus 80% for wheat in high-income markets. Tiny seeds clog conventional drills, and diverse landraces complicate equipment calibration. Field yields average 800-1,200 kg/ha compared with research-station ceilings near 3,000 kg/ha, locking producers into labor-intensive regimes that undercut price competitiveness. Absent affordable implements, the yield gap persists and slows millet market growth despite robust demand signals.

Infrastructure Deficit in Post-Harvest Handling

Post-harvest losses hover at 25-30% where hermetic storage, cold chains, and dehulling plants remain scarce. Farmers often sell unprocessed grain immediately to avoid spoilage, forfeiting 10-12% of potential revenue. The shortage of paved feeder roads inflates transport costs by up to 40%, eroding farm-gate returns and discouraging yield-enhancing input use. These structural gaps weigh on the millet market's competitiveness in global trade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific retained 45.72% of the millet market share in 2025, with India contributing substantial production volumes and generating notable export earnings, both of which directly fuel regional processing demand. Government minimum-support prices, integration into public ration shops, and aggressive export targets underpin the region’s entrenched leadership. China remains a vital consumption base for feed and liquor applications, yet its urbanizing dietary shift limits incremental growth, nudging Asia-Pacific toward a mature phase of the millet market.

Africa is on course for a 5.14% CAGR through 2031, the quickest climb among all continents. Niger, Nigeria, and Mali collectively harvested a significant share in 2024, equal to roughly one-third of global pearl millet output. National food-security agendas and climate adaptation policies incentivize acreage expansion, while corridor-wide processing investments improve value capture. Niger’s edible-grain exports of millet already represent a meaningful portion of the country’s total foreign earnings, and France absorbs a large share of that volume, signaling a budding Europe-Africa supply chain.

North America and Europe together form a niche but lucrative node within the millet market. Trials in the inland Pacific Northwest report proso millet varieties such as Plateau and Sunup outperforming earlier cultivars in iron, zinc, and antioxidant concentrations while delivering yields exceeding 2.5 metric tons per hectare. European buyers emphasize organic certification, sustainable sourcing, and traceable supply chains, attributes that justify price premiums sufficient to offset higher labor and compliance costs. Consequently, these high-income markets contribute disproportionate value relative to volume, thereby magnifying the overall millet market size.

Regulatory Landscape

Millet trade and food-quality regulation is moving toward greater harmonization through Codex Alimentarius. In April 2025, the Codex Committee on Cereals, Pulses and Legumes (CCCPL11) agreed to develop a global group standard for whole millet grains, supported by an Electronic Working Group chaired by India with co-chairs from Mali, Nigeria, and Senegal. The work focuses on minimum quality and safety requirements and is scheduled to deliver a report by December 2026.

Trade-policy anchors also shape cross-border flows in key consuming markets. India amended its Foreign Trade Policy in May 2025 to align export schedules with the Finance Act, 2025, bringing millet under clearer export documentation and compliance requirements. In the EU, the cereal import framework under Implementing Regulation (EU) 2023/2834 (updated July 2025) continues to govern import administration for cereals, influencing quality and entry conditions for millet shipments, while China issues annual grain import tariff quota application guidelines via its national authorities for 2025.

Value Chain Analysis

The millet value chain begins with seed systems and on-farm production concentrated in a few origins, then moves through aggregation, primary processing (cleaning, grading, dehulling), secondary processing (milling into flour and semolina, flakes, ready-to-cook mixes), and ends in branded retail and foodservice channels. Exports increasingly link surplus regions to premium gluten-free and health-food demand centers.

India anchors upstream supply, with government data placing total millet production at 180.15 lakh tonnes in 2024-2025 and USDA positioning India as the leading producer in 2025/2026 (13.23 million metric tons, about 44% of global output), followed by Niger and China. This concentration supports scale in procurement and processing, but it also makes global supply more sensitive to weather and market-linkage performance in a few geographies. Key constraints remain post-harvest handling, fragmented aggregation, and limited mechanization, which contribute to quality variability and losses before processing and export. India is building midstream capacity and formalizing market linkages through programs such as the Production Linked Incentive Scheme for Millet-Based Products (2022-2027, INR 800 crore outlay) under the Ministry of Food Processing Industries, alongside export facilitation by APEDA through its Export Promotion Forum and online initiatives. Price and income signals feed back into farm decisions as well, with India approving MSP for ragi for the 2025-26 marketing season to stabilize farmer participation in organized channels that supply processors and exporters.

Market Opportunities and Future Outlook

Standard-setting and formal procurement are opening space for exporters, processors, and ingredient buyers that depend on consistent grades and food-safety benchmarks. The Codex process that began at CCCPL11 in April 2025 to develop a group standard for whole millet grains, led by an India-chaired working group with African co-chairs, offers a practical route to reduce specification fragmentation across importing markets. That shift should support larger-volume, repeatable trade programs for whole grains and milled ingredients.

Investment and program activity across Africa and India point to actionable opportunity zones in seed systems, climate-smart extension, and value-added processing. In March 2026, FAO, The Gambia, and China launched a USD 1.5 million project to transform rice and millet food systems (seed varieties, training, and value-chain efficiency). In May 2026, Namibia launched an FAO Technical Cooperation Program project (USD 250,000, running to August 2027) to raise pearl millet productivity and develop the value chain. In India, the Production Linked Incentive Scheme for Millet-Based Products (FY 2022-23 to 2026-27; INR 800 crore) and broader 2025-26 budgetary support for millet promotion are tied to expanding manufacturing, branded products, and export readiness, alongside demand-side pull from functional foods and gluten-free formulations.

Recent Industry Developments

- May 2026: Namibia launched an FAO-backed Technical Cooperation Program project (USD 250,000) to improve pearl millet productivity and develop the value chain through August 2027. The program focuses on production and value-chain development, adding structured support for seed, agronomy, and downstream market linkages in a major millet-consuming region. This type of targeted public funding helps de-risk adoption of improved practices and supports throughput for local processors.

- March 2026: FAO, the Government of The Gambia, and the Government of China launched a USD 1.5 million initiative to transform rice and millet food systems in The Gambia. The project centers on improved varieties, climate-smart training, and value-chain efficiency, directly addressing productivity and post-harvest constraints that limit commercial scale. It also reinforces South-South cooperation as a financing and know-how channel for millet modernization in West Africa.

- December 2025: HETC Foods launched Navdhan, a range of ready-to-use sprouted millet powders positioned for convenient nutrition and ingredient use. The launch points to continued product-format innovation that moves millets into higher-margin processed categories beyond whole grain and basic flour. It also supports wider adoption by lowering preparation barriers for households and enabling new applications for food manufacturers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the commercial value of millets traded and consumed for food use, with the sizing built in USD and supported by volume signals where available. It is treated as a global market, and regional totals are aggregated into a single worldwide value.

Scope exclusions: we do not count downstream packaged foods where millet is only a minor ingredient and the selling price is mainly driven by processing, branding, or retail margins.

Segmentation Overview

- By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- North America

- United States

- Canada

- Europe

- Germany

- Italy

- United Kingdom

- Russia

- France

- Asia-Pacific

- China

- India

- Japan

- Australia

- South America

- Brazil

- Argentina

- Peru

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Africa

- Nigeria

- Niger

- Mali

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the model inputs, mainly around production trends, trade flows, and price direction for key millet varieties. Public datasets and reference sources such as FAOSTAT, UN Comtrade, USDA statistics and reports, national agriculture ministries, and trade bodies linked to grains and cereals were reviewed to understand supply patterns and cross-border movement.

We also screened annual reports, investor presentations, and credible press coverage to track procurement signals, capacity changes, and export focus in major producing regions. Where needed, a paid subscription for company financials and intelligence was used to normalize business scale, and a paid shipment-level trade database was used selectively to sanity check trade routes and unit values. These desk research sources are illustrative only, and many other public references were also used to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with grain traders, food ingredient distributors, processors, and procurement professionals, along with a few domain experts who track crop supply and pricing. Because this is a global market, we balanced responses across APAC, EMEA, and the Americas, so desk assumptions on trade mix, pricing spreads, and demand use cases could be tested and then tightened before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 52% |

| Mid tier: 55% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 16% | Managers: 44% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where global and regional production and trade data reconstruct the available supply pool, then the total is adjusted using price trend direction and the food use share implied by interviews. The value output is corroborated with selective bottom-up checks, such as sampled exporter and processor revenue signals, spot checks on average selling prices by region, and volume-to-value conversions for key millet types. Totals are adjusted when a gap is consistently seen.

Key model inputs include harvested production trends in major growing countries, export and import movements by region, price spreads between domestic and export grades, the shift toward health and gluten-free demand in urban channels, and policy-led demand signals that influence procurement (for example, food security or nutrition programs). Forecasts use scenario analysis, varying acreage and yield direction, trade openness, and price normalization within realistic bounds. The most likely path is then selected based on expert consensus. Where bottom-up inputs are missing for smaller corridors or informal trade, we apply conservative uplift factors anchored to observed trade shares, rather than assumptions that cannot be verified.

Data Validation & Update Cycle

Validation is done in layers so the final number is not driven by a single dataset. Outputs are cross-checked against independent signals such as reported production, visible trade totals, and plausible price bands, and any large variance is reviewed again before sign-off. If an anomaly is found, the related assumptions are reworked, and where required, respondents are re-contacted to confirm whether the change is structural or temporary.

Reports are refreshed annually, and interim updates are made when material events occur, such as sharp crop swings, policy changes that alter procurement, or sustained price shocks. Before delivery, an analyst performs a fresh pass on key inputs so clients receive the most current view possible.

Mordor Intelligence's Millets Market Size Versus Other Published Estimates

Published millet market values can look different even when the same crop family is discussed, because each publisher makes separate calls on what is counted, what year is treated as the current point, and how prices are translated into USD. Differences also show up when trade and production signals are used heavily by one model, while another leans more on stated demand narratives.

The benchmark table shows a noticeable spread across the quoted years and totals. In Mordor Intelligence's model, the market is tied to a 2026 current-year value and is supported by production, consumption, and trade checks rather than extending value into processed foods where millet is only a small input.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.22 B (2026) | |

| Global Data Publisher A | USD 12.87 B (2024) | Uses an earlier base year, and the public summary does not clarify how trade-based volumes are converted into value, which can shift totals when USD timing and price bands differ. |

| Industry Research Group B | USD 13.96 B (2025) | Likely applies a different inclusion set across food applications and distribution pathways, and the longer forecast horizon can embed a different price progression path that lifts the mid-year market value. |

Taken together, the spread is mainly explained by year selection, scope boundaries around what counts as the millets market, and how price and currency timing are handled. By keeping the model anchored to traceable production and trade signals and then confirming assumptions through interviews, we produce a practical total that can be repeated and updated when new crop and trade data arrive.

Key Questions Answered in the Report

How large is the millet market in 2026?

The millet market size reached USD 13.22 billion in 2026 and is projected to touch USD 16.78 billion by 2031.

Which region holds the largest share of millet sales?

Asia-Pacific leads with a 45.72% millet market share due to India's production dominance and integrated export ecosystem.

Why is Africa considered the fastest-growing territory?

Policy emphasis on food security, expanding acreage in Niger, Nigeria, and Mali, and rising export activity pushes Africa toward a 5.14% CAGR through 2031.

What are the main factors driving demand for millet-based products in the United States and Europe?

Health-conscious consumers favor gluten-free, nutrient-dense foods, while processors value millet's shelf stability and mineral profile, both of which encourage product launches.

Page last updated on: