Sonobuoy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

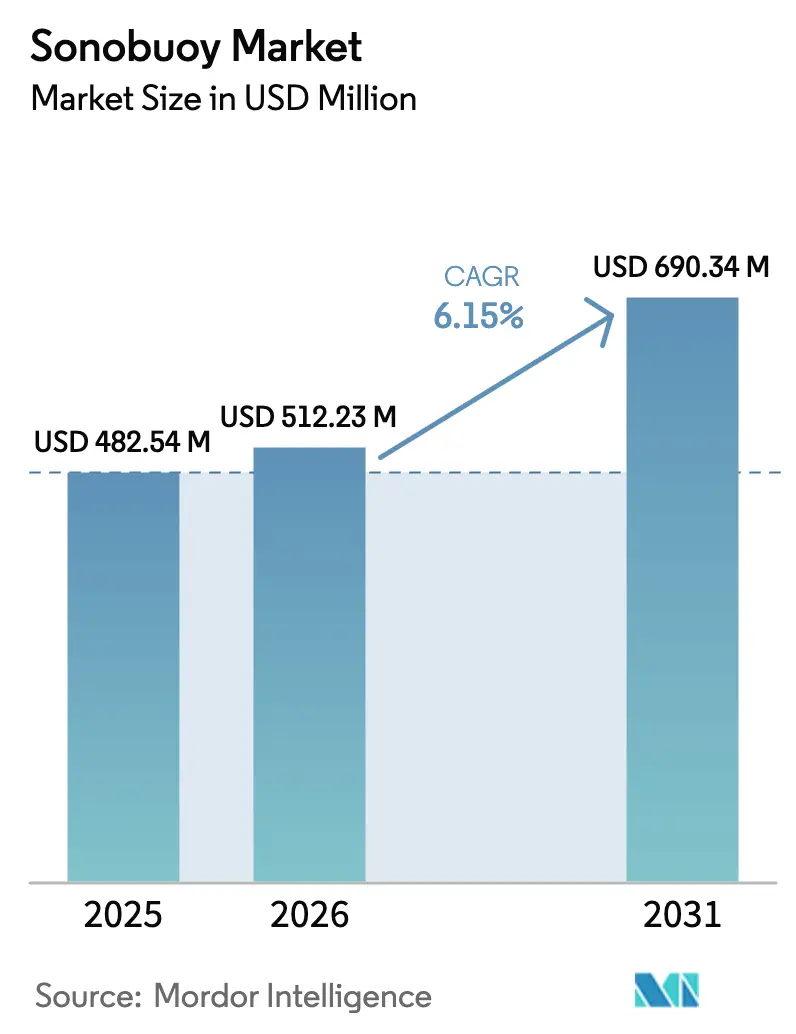

| Market Size (2026) | USD 512.23 Million |

| Market Size (2031) | USD 690.34 Million |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

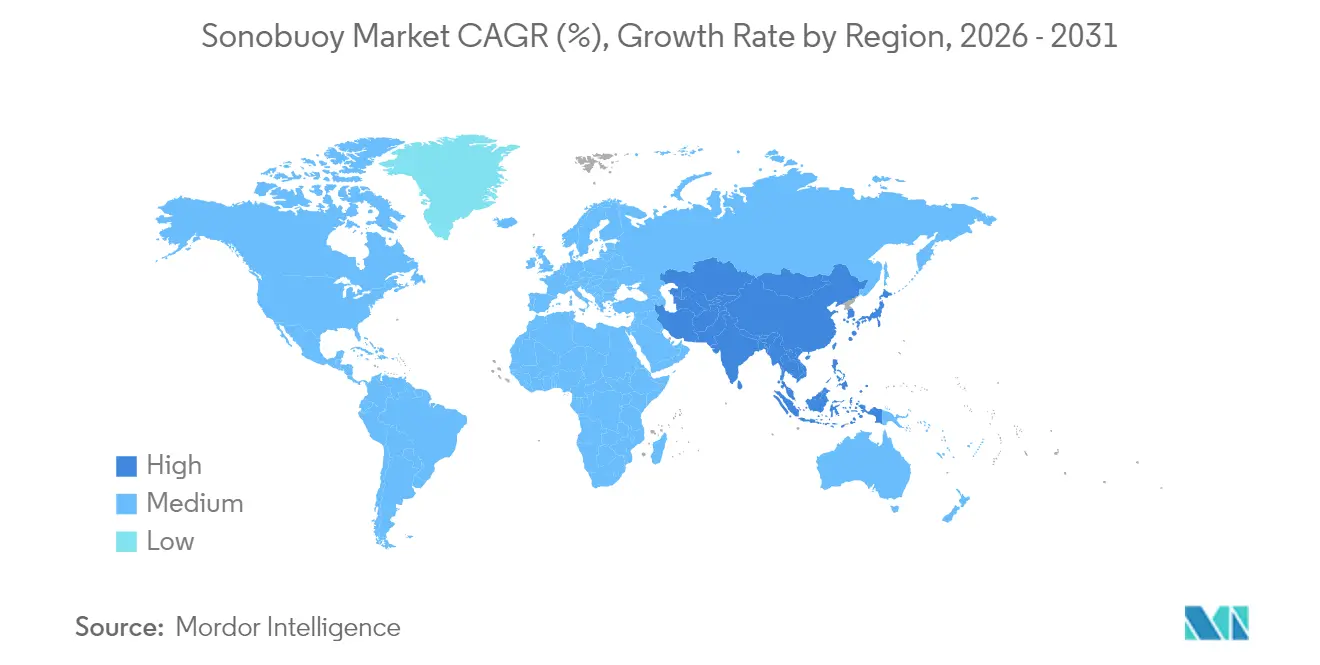

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

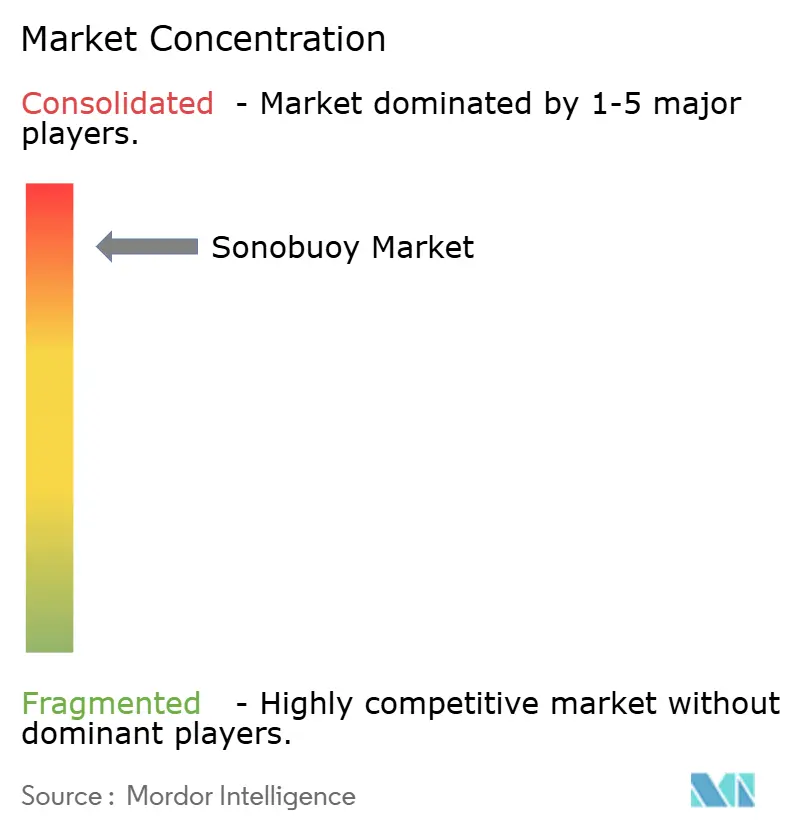

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sonobuoy Market Analysis by Mordor Intelligence

Sonobuoy market size in 2026 is estimated at USD 512.23 million, growing from 2025 value of USD 482.54 million with 2031 projections showing USD 690.34 million, growing at 6.15% CAGR over 2026-2031. Rising outlays on anti-submarine warfare, quiet diesel-electric fleets, and autonomous surveillance platforms keep demand resilient, ensuring the sonobuoy market remains a strategic priority for navies and offshore operators. North America retained procurement leadership, yet Asia-Pacific posts the quickest gains as regional submarine counts grow. Advances in digital signal processing, multistatic low-frequency architectures, and platform miniaturization are lowering the cost-per-detection, expanding coverage, and opening civil energy exploration use cases. At the same time, tighter environmental rules and export controls temper growth by adding compliance costs and supply-chain friction. Competitive intensity is high because a narrow supplier pool still dominates volume contracts, although upcoming joint-production deals and unmanned-platform integration could gradually rebalance market power.

Key Report Takeaways

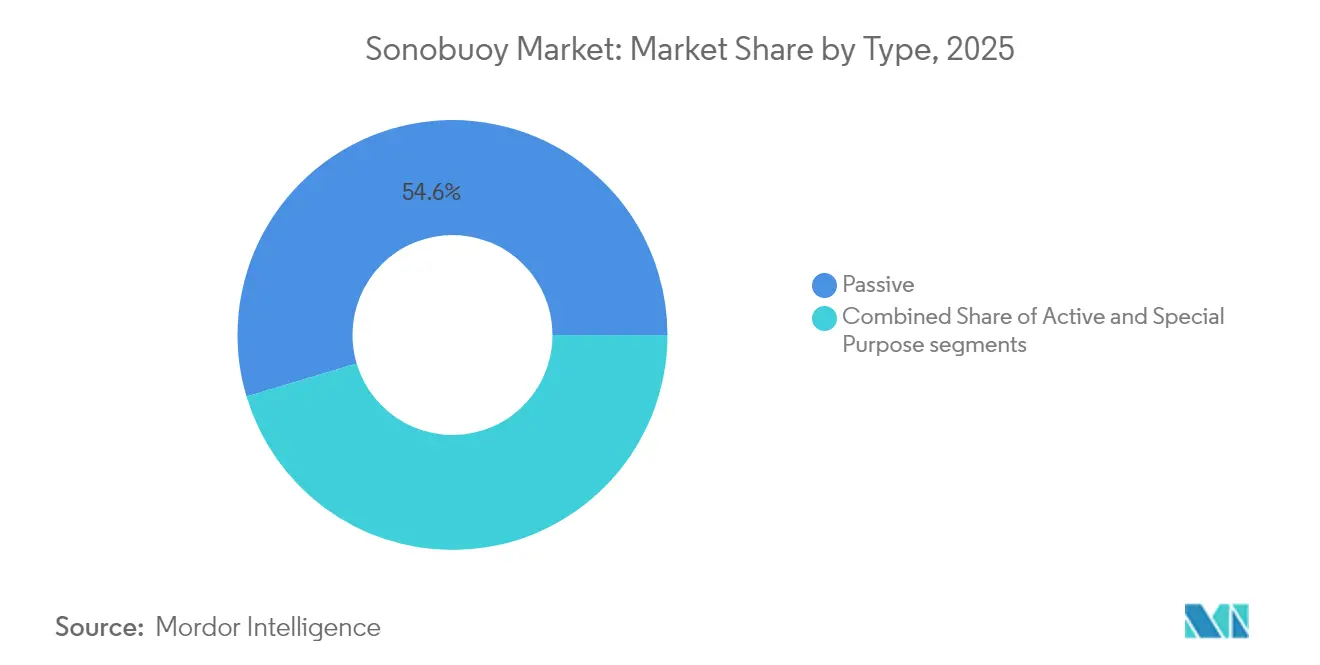

- By type, passive systems held 54.62% of the sonobuoy market share in 2025, while active variants are projected to grow at a 12.00% CAGR to 2031.

- By size class, Size A accounted for 64.55% of the sonobuoy market size in 2025; Size B units are slated to expand at 13.02% CAGR through 2031.

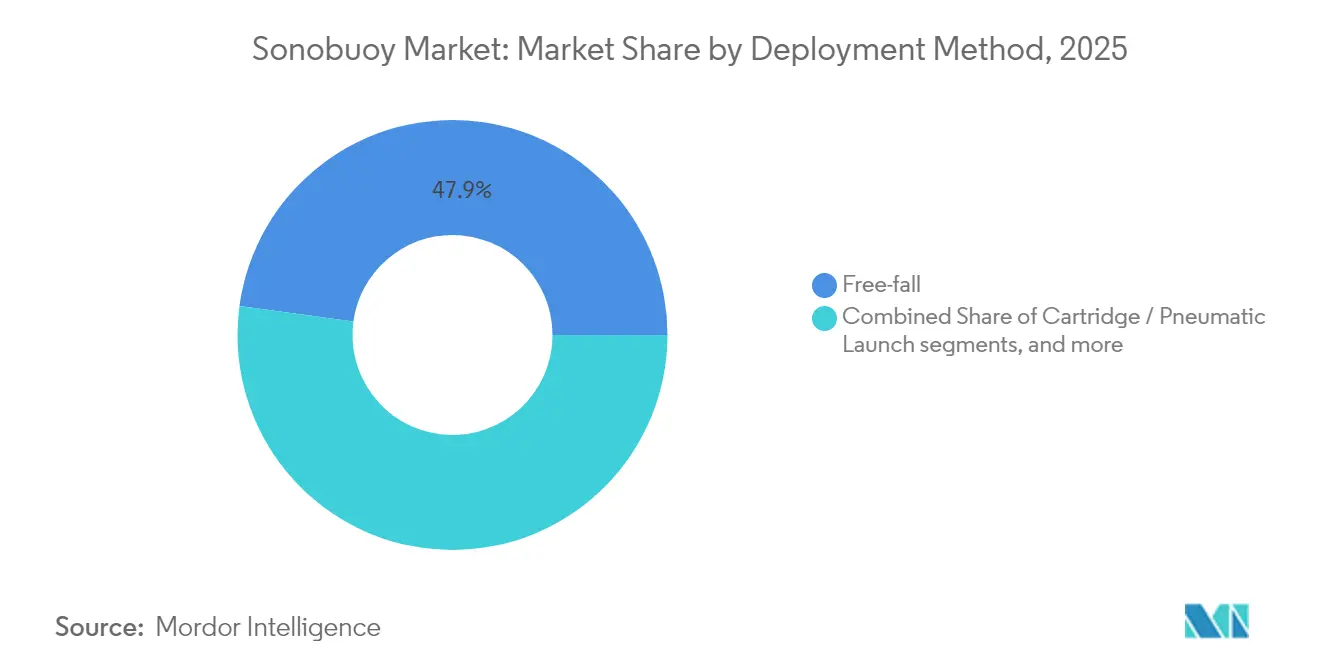

- By deployment method, free-fall solutions led with 47.85% revenue share in 2025, whereas cartridge/pneumatic formats register a 10.31% CAGR outlook.

- By application, defense captured 85.20% of the sonobuoy market size in 2025; commercial energy exploration is advancing at a 14.35% CAGR to 2031.

- By geography, North America commanded a 41.85% share in 2025; Asia-Pacific is forecast to add the fastest 11.47% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sonobuoy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Worldwide proliferation of quiet diesel-electric and AIP submarines elevating expendable ASW demand | +1.8% | Global, Indo-Pacific and North Atlantic | Medium term (2-4 years) |

| Shift from analog to digital sonobuoy architectures enabling multichannel data fusion and longer RF links | +1.2% | North America, EU, expanding Asia-Pacific | Short term (≤ 2 years) |

| Adoption of multistatic low-frequency active concepts lowering cost-per-detection and extending range | +0.9% | Global, led by NATO fleets | Medium term (2-4 years) |

| Rapid uptake of unmanned aerial and surface launch platforms boosting annual buoy deployment rates | +1.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Global standardization via NATO STANAG 4748 and MIL-STD 2525E enhancing interoperability across fleets | +0.7% | NATO and allied nations | Long term (≥ 4 years) |

| Expansion of deep-water energy exploration requiring expendable acoustics for seabed characterisation | +0.5% | Gulf of Mexico, North Sea and global offshore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Worldwide proliferation of quite diesel-electric and AIP submarines elevating expendable ASW demand

Modern diesel-electric and air-independent-propulsion boats now patrol longer in near-silence, narrowing passive detection windows and compelling navies to seed larger listening fields. Procurement plans signal this urgency: the US Navy budgets for roughly 204,000 buoys yearly to sustain inventory, while Indo-Pacific forces accelerate orders for distributed surveillance grids.[1]Stockholm International Peace Research Institute, “Trends in World Military Expenditure, 2024,” sipri.org Higher exercise tempos and real-world tracking missions translate into sustained consumption, anchoring volume growth across the sonobuoy market.

Shift from analog to digital sonobuoy architectures enabling multichannel data fusion and longer RF links

Digital signal chains compress, encrypt, and forward richer acoustic packets over extended radio links, letting operators merge feeds from dozens of nodes in near real time. Automated classification cuts operator workload and improves first-pass confidence, which is key in high-tempo patrols. These architectures also future-proof fleets against congested electromagnetic environments, making them a core upgrade catalyst within the sonobuoy market.

Adoption of multistatic low-frequency active concepts lowering cost-per-detection and extending range

Distributed source-receiver geometries exploit low-frequency propagation to cover wider ocean swaths with fewer expendables, slashing per-hour costs and bolstering standoff safety. Coherent processing dampens reverberation, increasing target-signal clarity and enabling new tactics, particularly for coalition patrols that need interoperable, plug-and-play kits. Adoption momentum feeds an innovation loop that keeps the sonobuoy market technologically dynamic.

Rapid uptake of unmanned aerial and surface launch platforms boosting annual buoy deployment rates

Unmanned aerial vehicles (UAVs) such as the MQ-9B SeaGuardian carry up to 80 small-form-factor buoys and loiter 18 hours, blanketing open-ocean gaps at lower flight-hour costs. Surface drones extend reach into contested littorals. Their arrival drives fresh procurement cycles, broadening the sonobuoy market customer base beyond traditional maritime-patrol squadrons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High supplier concentration and export-control regimes creating procurement bottlenecks | -0.8% | Global, especially non-NATO allies | Short term (≤ 2 years) |

| Stricter environmental regulations on underwater acoustic emissions constraining operational usage | -0.6% | North America, Europe, spreading Asia-Pacific | Medium term (2-4 years) |

| Competition from non-expendable alternatives such as LF towed arrays and autonomous UUV sonars | -0.4% | Global, led by technologically mature navies | Long term (≥ 4 years) |

| Volatile rare-earth and piezo-ceramic feedstock prices driving up unit production costs | -0.3% | Global, with sensitivity in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High supplier concentration and export-control regimes creating procurement bottlenecks

ERAPSCO’s long-standing dominance meant a single joint venture fed most US orders; its dissolution forces navies to identify alternate lines while navigating International Traffic in Arms Regulations. New entrants require heavy capital and long qualification cycles, so supply remains tight even as demand climbs. The Defense Production Act funding round seeks to widen capacity, yet export license hurdles still delay deliveries to partner nations, dampening near-term momentum in the sonobuoy market.

Stricter environmental regulations on underwater acoustic emissions constraining operational usage

NOAA’s updated marine-mammal acoustic thresholds impose seasonal or geographic restrictions on sonobuoy use, prompting planners to redesign exercise patterns.[2]National Oceanic and Atmospheric Administration, “Technical Guidance for Assessing Marine Mammal Acoustic Thresholds,” fisheries.noaa.gov Compliance adds cost, limits dwell time, and calls for quieter designs, trimming some growth until new eco-friendly models mature within the sonobuoy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Active Sonobuoys Gain Momentum Amid Passive Strength

Passive devices held 54.62% of the sonobuoy market in 2025, underscoring their value for covert, low-power listening over long distances. Active variants, however, will outpace the aggregate sonobuoy market with a 12.00% CAGR through 2031. They are powered by multistatic low-frequency innovations that push detection horizons while controlling battery drain. Special-purpose models for bathymetry and range monitoring fill a niche but play a crucial role in battle-group readiness.

Digital processing lifts active effectiveness, as algorithms suppress reverberation and highlight transient contacts. The resulting performance leap keeps navies investing, making this slice a pivotal revenue accelerator across the wider sonobuoy market. Parallel civil use for seismic surveys enlarges addressable demand, reflecting growing cross-sector technology spillover within the sonobuoy industry.

By Size Class: Shift Toward Compact Size B Units

Size A forms remained dominant, accounting for 64.55% of the sonobuoy market in 2025, because legacy aircraft racks favor that diameter. Yet, Size B sales rose 13.02% CAGR as unmanned and light patrol planes seek lighter loads without acoustic compromise. Miniaturization advances preserve sensitivity while halving weight, aligning with broader defense trends toward distributed sensing.

SeaGuardian’s capacity to double the carriage count when switching to Size B makes a compelling case for inventory diversification. Manufacturers betting on small-form-factor lines now unlock new platform integration fees, reinforcing growth vectors in the sonobuoy market.

By Deployment Method: Pneumatic Launchers Broaden Tactical Flexibility

Free-fall delivery captured a 47.85% share in 2025 due to simple gravity racks requiring minimal aircraft plumbing. Cartridge or pneumatic launchers, however, draw a 10.31% CAGR outlook as they allow precision patterns and quieter drops, which are advantageous against submarine forces alert to splash signatures. Spring systems cater to niche covert drops where sound discipline trumps loading rates.

Pneumatic tubes also ease retrofit onto rotary drones and corvette decks, removing structural modifications that once limited host options. This engineering agility multiplies addressable airframes and hulls, stimulating fresh procurement across the sonobuoy market.

By Application: Civil Energy Exploration Emerges as a High-Growth Adjunct

Defense still accounts for 85.20% of the sonobuoy market size in 2025. Still, commercial users in oil, gas, wind, and marine research now post the fastest 14.35% CAGR as developers probe deeper fields and stricter environmental rules demand high-resolution acoustic baselines. Training and exercise allocations remain steady since realistic live-fire scenarios hinge on expendable acoustics.

Dual-use trajectories entice suppliers to tweak models for civil regulations, diversifying revenue streams, and shielding them from cyclic defense budgets. This structural broadening undergirds the sonobuoy market's long-term resilience.

Geography Analysis

North America commanded 41.85% of the sonobuoy market in 2025 due to sizable US Navy budgets, integrated manufacturing clusters, and a long history of experimentation with anti-submarine warfare. Annual buys of roughly 204,000 units set a volume floor that sustains local lines and accelerates R&D into digital and multistatic features. Canada’s NATO patrol commitments and Mexico’s offshore energy surveys add incremental pull, reinforcing the region’s leadership role. After ERAPSCO’s breakup, supply-risk worries pushed authorities to channel Defense Production Act funds toward redundancy. This measure should stabilize the North American share, leaving room for foreign advances.

Asia-Pacific posts the fastest 11.47% CAGR through 2031 as submarine fleets expand and maritime boundary disputes intensify. India’s co-production pact with Ultra Maritime and Bharat Dynamics Limited illustrates policy support for localized build lines and allied interoperability. Japan embeds sonobuoy upgrades into its Medium-Term Defense Plan, while Australia studies sovereign manufacturing to cut shipping risk. The regional thirst for unmanned platforms also accelerates the adoption of compact buoys, widening the sonobuoy market pipeline.

Europe grows steadily due to NATO standardization, higher Baltic patrol hours, and emerging Indo-Pacific deployments by France, Germany, and Italy. Paris awarded Thales a domestic SonoFlash contract to secure supply and hedge geopolitical uncertainty. Environmental compliance shapes procurement language, pressing suppliers to innovate quieter or shorter-duration devices. Cross-border exercises, such as Dynamic Manta, fuel routine replenishment orders, ensuring Europe remains an essential demand pillar within the sonobuoy market framework.

Competitive Landscape

The sonobuoy market is highly concentrated: a handful of US and UK entities capture most defense volumes. The sunset triggers a strategic reshuffle. Ultra Maritime secured a USD 99 million AN/SSQ-53H award to affirm continuity, while Sparton outlines autonomous production plans to retain relevance. New entrants must hurdle tough qualification gates, yet government interest in diversified supply could ease timelines.

Technology differentiation becomes the main lever. Ultra and General Atomics align on small-form buoys tuned for SeaGuardian, chasing the edge in unmanned operations. Thales positions SonoFlash as a sovereign, dual-mode product for European navies and export customers. Suppliers eye civil exploration to smooth order cycles, positioning acoustic payloads as marine-survey tools that comply with eco-standards. These moves suggest the sonobuoy market will gradually migrate from a near-monopoly toward an oligopoly with distinct regional champions.

International joint ventures add a geopolitical layer. The India-US line links the Make-in-India policy with US technology safeguards, potentially inspiring similar tie-ups in Southeast Asia. Chinese and Russian efforts remain opaque but hint at indigenous development paths, indicating that strategic autonomy considerations may further fragment demand patterns across the global sonobuoy market.

Sonobuoy Industry Leaders

Thales Group

Lockheed Martin Corporation

General Dynamics Mission Systems (General Dynamics Corporation)

L3Harris Technologies, Inc.

Ultra Electronics Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: General Atomics Aeronautical Systems, Inc. and Ultra Maritime formed a partnership to enhance unmanned airborne detection and tracking of submarines by combining GA-ASI's MQ-9B SeaGuardian unmanned aerial system with Ultra Maritime's miniaturized sonobuoys and receivers. This integration enables the United States and its allies to track submarines in GPS-denied environments.

- January 2025: Thales Group signed a multi-year deal to furnish the French Navy with several hundred SonoFlash units produced domestically, bolstering national supply security.

- January 2025: India and the US formalized a co-production pact between Ultra Maritime and Bharat Dynamics Limited to manufacture sonobuoys in India under allied-interoperability requirements.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the study counts every new, expendable acoustic buoy that is air-dropped or surface-launched to detect, classify, and relay information on submarines, torpedoes, and underwater hazards across defense and commercial energy missions. The scope covers active, passive, and multistatic devices in size classes A and B, together with their integrated telemetry links and power packs.

Scope Exclusion: tethered seabed surveillance arrays or reusable unmanned sensor nodes sit outside this assessment.

Segmentation Overview

- By Type

- Active

- Passive

- Special Purpose

- By Size Class

- Size A

- Size B

- By Deployment Method

- Free-fall

- Cartridge/Pneumatic Launch

- Spring Launch Systems

- By Application

- Defense

- Anti-Submarine Warfare

- Training and Exercise

- Acoustic Range Monitoring

- Commercial

- Off-shore Energy Exploration

- Oceanographic Research

- Search and Rescue

- Defense

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview procurement officers in the United States, France, India, and Australia, retired ASW pilots, buoy design engineers, and offshore survey contractors. These conversations test desk findings, reveal confidential price corridors, and refine assumptions on digital telemetry adoption before follow-up surveys anchor regional growth rates.

Desk Research

Our desk work opens with unclassified procurement budgets from the United States Naval Air Systems Command, defense white papers from NATO and Indo-Pacific ministries, and annual spending tables compiled by SIPRI, which set the ceiling for potential unit demand. Offshore drilling statistics from the International Energy Agency and UN Comtrade customs codes flow next, which are then filtered through Volza shipment records to track cross-regional supply.

Company financials extracted through D&B Hoovers, contract notices on Dow Jones Factiva, and technical briefs published by the National Defense Industrial Association, plus peer-reviewed acoustic journals, allow us to map revenue and technology migration. This list is illustrative only; many additional sources inform data collection, validation, and clarification.

Market-Sizing & Forecasting

Demand is first built top-down by translating platform inventories and sortie rates into annual buoy consumption, which is then cross-checked with sampled manufacturer shipment logs and average selling prices to balance volume and value. Key inputs include fleet counts of maritime patrol aircraft, qualified ASW helicopters, sonar channel density per buoy, battery energy cost trends, and the tally of new deep-water wells needing seismic listening. A multivariate regression model, stress-tested through scenario analysis, generates the 2025-2030 outlook, while gaps in bottom-up estimates are bridged with conservative factor uplifts verified through re-calls.

Data Validation & Update Cycle

Our team runs variance checks against historical import volumes, noise-floor benchmarks, and tender awards; anomalies trigger fresh interviews before sign-off. Reports refresh annually, with interim updates whenever large contracts or regulatory shifts change market math.

Why Mordor's Sonobuoy Baseline Commands Operator Confidence

Published market values rarely align because firms differ on device mix, price ladders, and refresh cadence, and we acknowledge these realities upfront. The widest gaps surface when studies drop passive multistatic models, treat commercial buoys separately, or apply flat replenishment rates that ignore surge orders tied to live deployments; further variance arises from currency cut-offs and longer update cycles, whereas Mordor revises numbers every year and after major awards.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 482.54 million (2025) | Mordor Intelligence | |

| USD 455.8 million (2024) | Global Consultancy A | Excludes passive multistatic devices and assumes uniform ASP worldwide |

| USD 532.7 million (2024) | Industry Association B | Uses high ASP benchmarks and aggressive fleet-replenishment multipliers |

| USD 522.3 million (2024) | Trade Journal C | Relies on single-region inflation factor and updates only every two years |

These comparisons show that when the right scope, live contract data, and realistic price ladders converge, Mordor delivers a balanced, transparent baseline that decision-makers can trace to clear variables and replicate with limited effort.

Key Questions Answered in the Report

What is the current value of the Sonobuoy market?

The Sonobuoy market size is USD 512.23 million in 2026, with a projected CAGR of 6.15% through 2031.

Which region leads global demand for sonobuoys?

North America holds 41.85% of global revenue, supported by large US Navy procurement volumes and established production infrastructure.

Why are active sonobuoys gaining traction?

Active units benefit from multistatic low-frequency concepts and improved digital processing, enabling longer-range detection of new quiet submarines and driving an 12.00% CAGR.

How are unmanned platforms influencing the Sonobuoy market?

Uncrewed aircraft and surface vessels carry more buoys for longer periods, expanding coverage at lower cost and widening the customer base beyond traditional patrol aircraft.

What challenges could slow market growth?

High supplier concentration, export-control limits, and stricter acoustic-emission regulations introduce procurement delays and compliance costs that offset some demand momentum.

Which civil sectors are adopting sonobuoy technology?

Deep-water oil, gas, and offshore wind projects deploy buoys for seabed mapping and environmental monitoring, propelling a 14.35% CAGR in commercial applications.

Page last updated on: