Textile Home Decor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

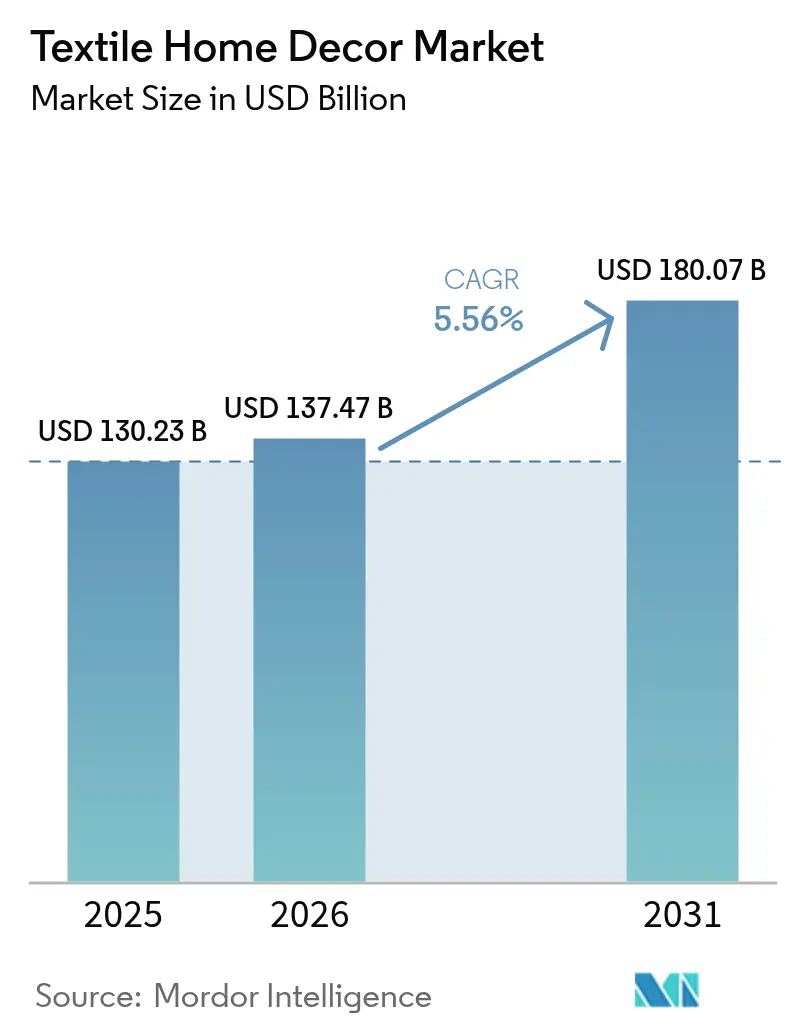

| Market Size (2026) | USD 137.47 Billion |

| Market Size (2031) | USD 180.07 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Home Decor Market Analysis by Mordor Intelligence

The textile home decor market size is expected to increase from USD 130.23 billion in 2025 to USD 137.47 billion in 2026 and reach USD 180.07 billion by 2031, growing at a CAGR of 5.56% over 2026-2031. The growth outlook reflects a steady shift from pandemic-era volatility toward disciplined expansion shaped by the European Union’s Digital Product Passport and Extended Producer Responsibility frameworks, omnichannel distribution improvements, and premiumization in both residential remodeling and commercial projects. Competitive intensity remains high due to fragmentation, which pressures margins in commodity categories while opening space for specialists in performance and circular-ready textiles. Vertical integration and energy self-sufficiency are rising priorities as manufacturers adopt captive renewables to buffer input-cost swings and to meet retailer sustainability requirements. Product development is tilting toward PFAS-free finishes and traceable materials that anticipate tightening chemical and due diligence rules in Europe and the United States, positioning early movers to win contracts that require robust compliance credentials.

Key Report Takeaways

- By product type, bed linen led with 33.78% revenue share in 2025. Rugs and carpets are projected to expand at a 5.74% CAGR through 2031.

- By material, natural fibers captured a 42.08% share in 2025. Blended materials are forecast to grow at a 5.69% CAGR to 2031.

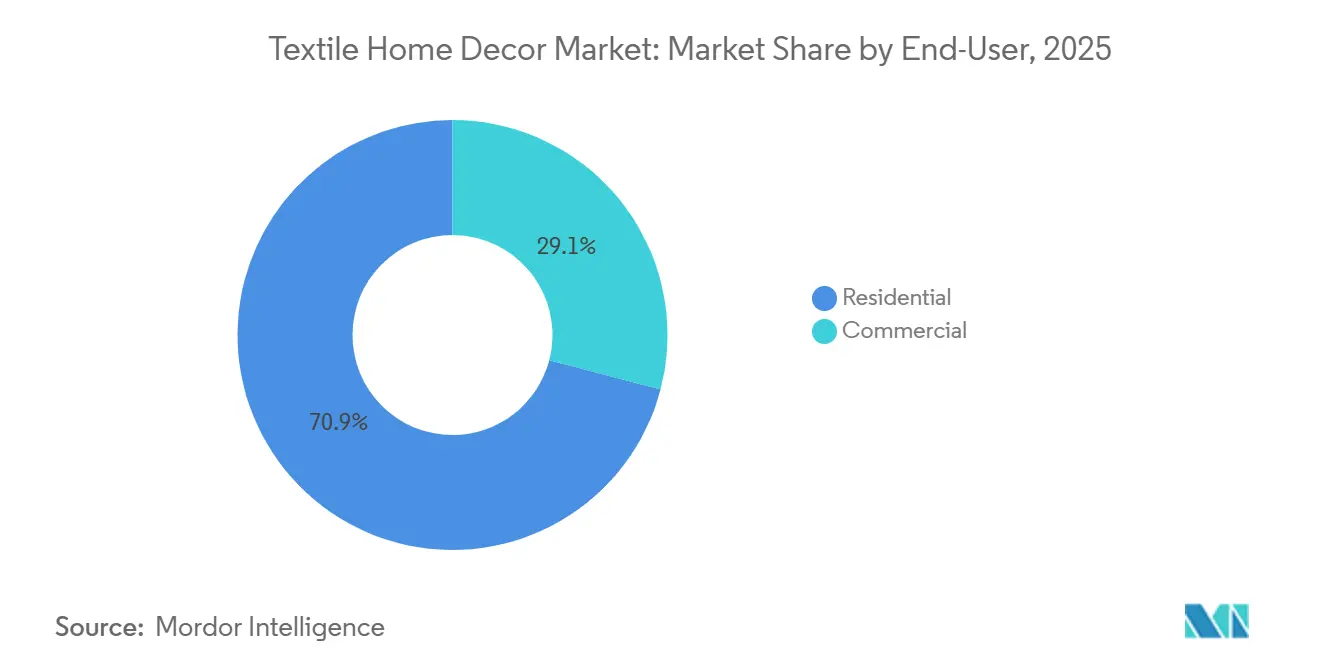

- By end-user, the residential segment accounted for 70.92% of revenue in 2025. The commercial segment is projected to grow at a 5.89% CAGR through 2031.

- By distribution channel, B2C retail held a 75.12% share in 2025. B2B direct is expected to post a 5.55% CAGR through 2031.

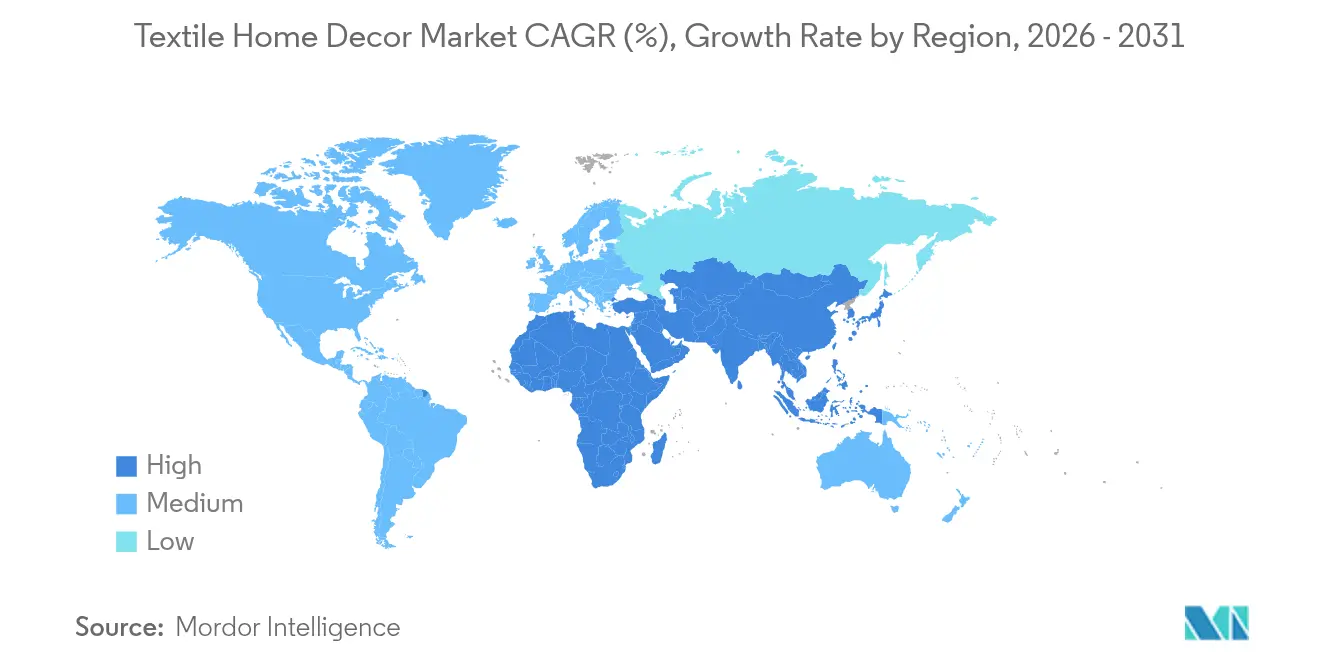

- By geography, North America contributed 31.88% of 2025 revenue. Asia-Pacific is the fastest-growing region, projected at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Textile Home Decor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2024 Home Renovation and Construction Cycle | +1.2% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| E-commerce Scale and Omni-channel Merchandising | +0.9% | Global, with faster digital adoption in the Asia-Pacific | Short term (≤ 2 years) |

| Hospitality And Short-stay Expansion | +0.8% | North America, the Middle East, GCC, and Asia-Pacific | Medium term (2-4 years) |

| Premiumization And Wellness Textiles | +0.7% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| European Union Textile EPR And Digital Product Passport | +0.6% | European Union-27, United Kingdom, with spill-over to export-oriented Asia-Pacific suppliers | Long term (≥ 4 years) |

| PFAS Phase-outs And Chemical Regulations | +0.4% | France, European Union, select United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-2024 Home Renovation and Construction Cycle Sustaining Textile Upgrades

United States housing completions and ongoing construction entering 2025 sustained a pipeline that supports steady demand for bed, bath, window, and floor textiles as projects reach the furnishing stage[1]U.S. Census Bureau, “New Residential Construction and Completions 2024,” U.S. Census Bureau, census.gov. Moderating borrowing costs by late 2025 eased financing for remodels and décor refreshes, which helped lift discretionary purchases of higher-spec linens and fresh patterns for living spaces. On the supply side, large home textiles groups continued to expand retail reach and engagement across major consumer markets, which improved sell-through and increased visibility for upgraded lines. These dynamics favor products that deliver durability, comfort, and easy maintenance across multiple rooms, often with traceable materials that comply with retailer procurement policies. As construction backlogs convert to closings and as remodel projects move from planning to execution, the textile home decor market benefits from staggered replacement cycles that smooth quarterly demand.

E-commerce Scale and Omni-channel Merchandising for Home Textiles

Direct-to-consumer programs and brand-owned channels are unlocking faster go-to-market for new collections in bedding and bath while reducing reliance on wholesale lead times. Fulfillment networks and logistics partners prioritized high-turnover home goods during maritime disruptions, which helped preserve delivery speed for key SKUs through late 2025. Retailers and manufacturers that synchronize in-store assortments with online inventories see fewer stock-outs, which protects conversion at price points where substitutability is high. Visualization tools and clearer product content for fibers, performance finishes, and certifications are reducing returns on high-touch categories like curtains and rugs by improving pre-purchase confidence. As B2B buyers also adopt digital ordering for contract linens, mills with automated cut-sew-pack capabilities are compressing lead times and improving responsiveness on replenishment.

Premiumization And Wellness Textiles (Antimicrobial, Cooling, Hypoallergenic)

Consumer and hospitality buyers are shifting toward textiles that promise specific wellness outcomes, such as allergen control, moisture management, and cooling comfort, which support premium price points. Suppliers invested in R&D during FY 2024-25 to strengthen proprietary finishes and to scale higher-margin product families that respond to these preferences. Advances in antimicrobial and odor-control treatments certified by recognized schemes are extending from hospitality and healthcare into residential channels as buyers seek hotel-like comfort at home. The channel mix favors online for these performance-led items because detailed product content can explain functionality that is not obvious on first touch, as cost-performance gaps narrow for PFAS-free repellents and alternative chemistries, adoption barriers in premium bedding and bath continue to decline[2]OEKO-TEX Association, “STANDARD 100 and 2024 Limit Updates,” OEKO-TEX, oeko-tex.com.

European Union Textile EPR And Digital Product Passport Catalyzing Traceable, Durable Products

The European Union’s Ecodesign for Sustainable Products Regulation created the legal basis for Digital Product Passports, with textiles prioritized in the first implementation waves from 2027 onward. Extended Producer Responsibility regimes in Member States are introducing eco-modulated fees, which reward products that are more recyclable, longer lasting, and free of restricted chemistries. Export-oriented suppliers are deploying traceability platforms and item-level identifiers to meet data-sharing requirements, which also streamline audits for large retail contracts. Manufacturers that standardize mono-material designs and scale recycled-content programs benefit from lower prospective compliance costs and stronger positioning with sustainability-focused retailers. Over time, DPP data can support advanced aftersales models such as repair, refurbishment, and take-back, which opens new revenue streams aligned with circularity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -0.8% | Global, sharper in Asia–United States/European Union lanes and key cotton belts | Short term (≤ 2 years) |

| Competition From Hard-surface Flooring | -0.5% | North America, Western Europe | Medium term (2-4 years) |

| Compliance Costs from Sustainability and Due Diligence Rules | -0.4% | European Union-27, United Kingdom, early adopters in North America | Long term (≥ 4 years) |

| Microfiber-shedding Scrutiny | -0.3% | European Union, selected North American buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility (Cotton, Polyester Feedstocks, Freight)

Energy, fiber, and freight swings compressed margins in 2025, with large integrated players reporting higher input costs that offset productivity gains. Ocean-route disruptions extended transit times and raised shipping rates on some Asia-Pacific - United States lanes, which complicated inventory planning and increased working-capital needs. To mitigate, leading groups accelerated renewable energy adoption, which lowered unit energy costs and reduced exposure to fossil-fuel volatility in manufacturing hubs. Investments in automation and process optimization helped recapture some margin, but smaller mills without scale advantages remained more exposed to cost shocks. Buyers with blanket purchase orders leaned on suppliers for stable pricing, prompting mills to hedge where possible and to shift mix toward higher-value SKUs with stronger pricing power.

Competition From Hard-surface Flooring Reducing Carpet Demand

In residential remodeling and new builds across mature markets, resilient and hard-surface options continued to win share in high-traffic rooms due to water resistance and simpler maintenance. Leading carpet manufacturers responded by investing in premium constructions, solution-dyed fibers, and distinctive aesthetics to differentiate on comfort, acoustic benefits, and style. Efficiency gains in adjacent categories improved capital allocation flexibility, which supported faster refresh cycles in carpet design to protect relevance in retail and specification channels. Commercial demand for modular carpet tiles provided a partial counterweight due to performance needs in offices and hospitality zones where targeted replacement and acoustics matter. The net effect is a segmented demand picture where comfort-led niches remain resilient even as hard surfaces grow in specific residential applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rugs & Carpets Accelerate Amid Broadloom Decline

Bed linen commanded 33.78% of global revenue in 2025, while rugs and carpets are projected to expand at a 5.74% CAGR through 2031, making them the fastest-growing product category within the textile home decor market. The leadership of bed linen reflects ubiquitous residential use and steady institutional replenishment, with upgraded specifications and curated aesthetics lifting average selling prices in premium channels. Suppliers scaling utility bedding and adjacent categories, including pillows and quilts, are capturing multi-category synergies across logistics and brand-building in North America. On the floor covering side, modernization in tufting, solution-dyed fibers, and design tooling allows carpet producers to defend comfort-led niches even as hard surfaces gain in kitchens and basements.

The rugs and carpet rebound are supported by corporate and hospitality specifications for modular tiles, where noise attenuation and ease of targeted replacement matter. Productivity actions at scale players yielded meaningful savings in 2025, which were redeployed into innovation and selective range expansions. Meanwhile, direct-to-consumer bedding initiatives show how brand equity built in one category can accelerate traction in complementary lines, improving lifetime value across the textile home decor market. Execution strength in automation and cut-sew-pack processes tightens service levels and supports just-in-time replenishment for B2B accounts, improving availability for recurring projects.

By Material: Blended Fibers Outpace Naturals on Recycled-content Demand

Natural fibers held 42.08% of revenue in 2025, while blended materials are set to grow at 5.69% CAGR, outpacing both natural and pure synthetic categories as brands meet recycled-content and durability requirements. Recycled polyester accounted for an estimated 12% of global polyester output in 2024-2025, which supports polycotton blends that balance softness, strength, and sustainability claims. Market acceptance is shaped by policy as well, since European due diligence and product passport rules favor traceable inputs and materials that enable circular outcomes at the end of life[3]European Commission, “Textiles and the Environment Policy,” European Commission, europa.eu. The material mix in home furnishings is therefore evolving toward blends that reduce risk under chemical and circularity rules while maintaining tactile appeal.

PFAS phase-outs in France and potential European Union-wide restrictions are spurring reformulation in repellent finishes, which is influencing fiber choice for outdoor textiles and stain-resistant linens. Testing and certification schemes updated in 2024 further tightened limits on fluorine content, nudging adoption of alternative chemistries that work across cotton and synthetic bases. As compliance requirements intensify, vertically integrated suppliers that can validate chain-of-custody and manage material diversity will carry an advantage in retailer sourcing programs within the textile home decor market[4]Welspun Living, “Automation, Lead Times, and B2B Service,” Welspun Living, welspunliving.com. Investment in scalable recycling partnerships remains a watch area as brands pilot routes to turn end-of-life polyester curtains and upholstery into fiber with virgin-equivalent quality.

By End User: Commercial Segment Gains on Hospitality and Healthcare Needs

The residential segment accounted for 70.92% of revenue in 2025, while the commercial segment is projected to grow at 5.89% through 2031 as hospitality, healthcare, and office projects upgrade soft furnishings to meet performance and hygiene standards. Hotels and managed accommodations continue to standardize higher durability and easy-care linen specifications that support quicker turnover without sacrificing guest experience. Healthcare and senior-living facilities prioritize antimicrobial and fluid-barrier properties for bed linen and privacy curtains, which favor suppliers with proven compliance credentials. Corporate offices adopting hybrid work formats are also investing in modular carpet tiles and acoustic wall textiles to improve privacy and reduce noise in collaborative zones.

Residential demand remains broad-based across bed, bath, window, and floor categories, but the mix is tilting toward better-quality staples and themed accents that refresh rooms without full remodels. Lifestyle messaging around hotel-quality sleep is feeding interest in premium pillows, protectors, and cooling sheets in higher-income cohorts. For institutional buyers, service reliability and replenishment speed are as decisive as price, which supports direct-sourcing models with tighter production-to-delivery cycles in the textile home decor market. As occupancy indicators stabilize across travel and healthcare, replacement cycles in commercial settings normalize at intervals that lift recurring linen procurement.

By Distribution Channel: B2B Direct Gains as Manufacturers Bypass Intermediaries

B2C retail captured 75.12% of 2025 revenue, while B2B direct from manufacturers is expected to grow at 5.55% as hotels, multifamily developers, and institutions contract directly with mills to compress lead times and secure consistent quality. Direct-to-consumer bedding relaunches demonstrated the scalability of brand-owned channels across the United States, which improved velocity for core ranges. Logistics partners continuing to prioritize fast-moving home goods through late-2025 disruptions helped stabilize delivery windows for replenishment orders. Large integrated suppliers also upgraded automation in cut, sew, and pack, which shortened cycle times and strengthened B2B service levels.

Within B2C, specialty and home-improvement stores remain important for flooring decisions, while online platforms lead for bedding and bath, where selection and product content drive choice. Retailers that align in-store vignettes with online assortments are improving cross-channel conversion and reducing return rates in categories with high tactile expectations. For B2B accounts, direct contracts reduce total landed costs versus wholesale channels and support standardization across property portfolios in the textile home decor market. As brands build data visibility from mill to buyer, safety stock and just-in-time replenishment models become easier to execute without service degradation.

Geography Analysis

North America contributed 31.88% of global revenue in 2025, with demand anchored by multi-room residential purchases and recurring commercial replacement cycles. United States housing completions and active projects entering 2025 created a pipeline that underpins demand for textiles as homes near handover and as remodels move to finish phases. Large suppliers signaled improving conditions into 2026 on the back of increased housing turnover and a steadier construction environment. Some producers shifted more output to domestic and nearshore facilities to manage tariff and logistics risk while protecting service levels in key product lines. Channel dynamics favor a mix of specialty retail and online for bedding and bathing, while trade-focused showrooms support specification decisions in floor coverings.

Europe’s growth outlook is bolstered by regulatory clarity around product passports, recyclability, and due diligence, which is accelerating supplier consolidation toward compliant offerings. Buyers in Northern Europe and the Benelux are placing a higher weight on third-party certifications and traceable inputs, which supports premium positioning for compliant ranges. Leading Indian suppliers expanded commercial presence in the United Kingdom and mainland Europe during 2025-2026 to accelerate customer engagement and to align with evolving trade conditions. As DPP milestones approach, retailers are prioritizing durable, mono-material, and easily sortable textiles to manage compliance costs and support circular programs.

Asia-Pacific is the fastest-growing region at a projected 6.05% CAGR to 2031 and held a substantial global share in 2025 due to manufacturing depth and steady growth in middle-income consumption. India’s sector momentum through FY 2024-25 and FY 2025-26 is supported by investment programs and cluster-based manufacturing that boost scale in spinning, weaving, and finishing. Domestic retail footprints expanded across thousands of multi-brand outlets, strengthening distribution for bed and bath ranges in fast-urbanizing markets. In the Middle East and Africa, hospitality and mixed-use development continue to anchor commercial demand for linens and floor coverings, with green-building criteria shaping product selection in leading projects.

Competitive Landscape

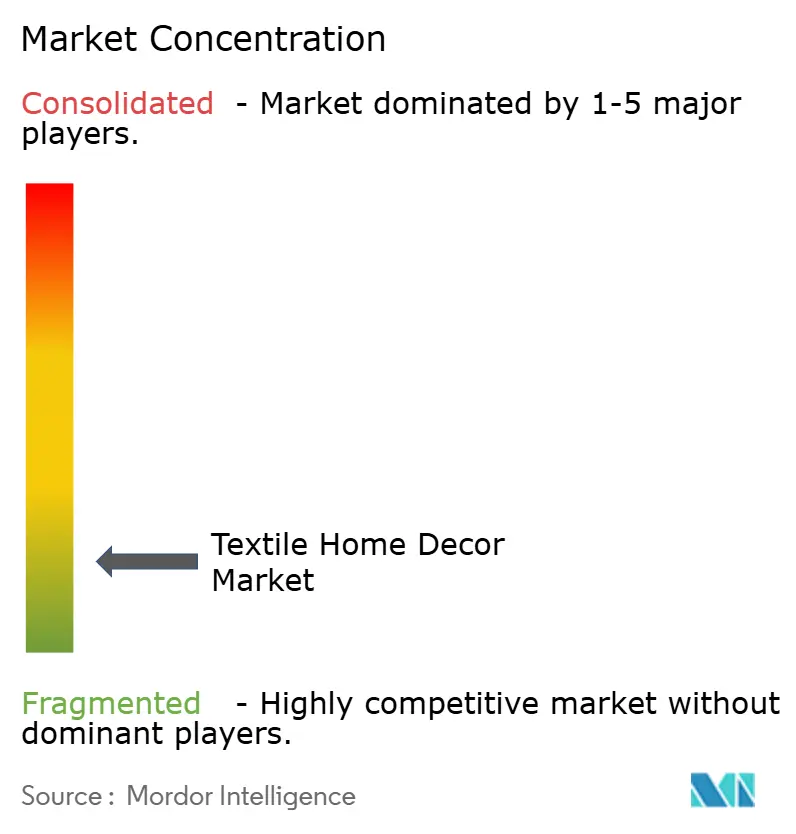

The textile home decor market remains fragmented at the global level, with the top five players holding a combined share near the high teens in 2025, which leaves significant headroom for specialists to scale in targeted niches. Pricing pressure persists in commodity segments, prompting suppliers to prioritize value-added finishes, sustainable inputs, and service differentiation. Strategic focus areas include vertical integration for input risk management, leaner production cycles, and captive renewables to reduce energy cost volatility and carbon exposure. As retailers intensify compliance checks, suppliers that can verify chain-of-custody and chemical safety are winning larger contract volumes. This environment supports ongoing mixed upgrades and selective capacity additions in categories with defensible margins.

Large groups reported productivity gains and continued to budget capital toward cost reduction and innovation programs for 2026, including automation, materials development, and adjacent category growth. Investments in modular-tile reuse and donation networks also advanced in 2025, which dovetails with retailer interest in circular solutions for commercial interiors. Solar capacity additions and energy-efficiency upgrades documented in FY 2024-25 sustainability reports improved unit economics and hedged against fuel-cost spikes. Expansion of European commercial teams and showrooms strengthened access to key retail and contract accounts, which supports faster new-product adoption. Taken together, these moves align with the regulatory and buyer landscape that rewards traceability, durability, and reduced environmental footprint.

Targeted M&A and capacity additions illustrate how leaders are widening category coverage and deepening capability moats. Pillow and utility bedding capacity in the United States rose through 2026 at select suppliers, improving service for nationwide brands and retailers. Circular initiatives, including large-scale carpet-tile reuse partnerships, signal rising emphasis on lifecycle value propositions in commercial channels. Automation in cut-sew-pack and advanced planning systems shortened lead times and supported just-in-time replenishment for B2B contracts in hospitality and multifamily properties within the textile home decor market. Across these moves, the common thread is disciplined capital allocation toward cost, innovation, and compliance capabilities that translate into durable competitive advantages.

Textile Home Decor Industry Leaders

Mohawk Industries, Inc.

Shaw Industries Group, Inc.

Tarkett S.A.

Oriental Weavers

Welspun Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Welspun inaugurated a Terry Towel plant in Gujarat, establishing it as the world's largest towel manufacturing facility.

- July 2025: Indo Count Global relaunched the American brand Wamsutta with a direct-to-consumer strategy, distributing across all 50 United States online, achieving an annualized run rate of approximately USD 85 million within six months, marking the company's sixth licensed brand alongside Fieldcrest, Waverly, GAIAM, and Tommy Hilfiger.

- July 2025: Trident Group, via its European Subsidiary Trident Europe Limited, launched the "Trident Threads" brand in the United Kingdom with an experiential showroom in Cheshire, England, offering design-driven, sustainable, premium bed and bath linens targeting the United Kingdom.

- January 2025: Trident Group revealed plans to expand into the European premium bedding segment, leveraging duty-free access and existing yarn capacity.

Global Textile Home Decor Market Report Scope

A subset of the textile industry used for home furnishings is known as "home textile decor." It consists of clothing and textiles for the interiors of the home. The textile home decor market has been segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into bed linen and bedspreads, floor coverings, kitchen and dining linens, bath and toilet linens, upholstery, and other product types. By distribution channel, the market is segmented into supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels. Also, the study provides an analysis of the textile home decor market in emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Bedding |

| Bath Linen |

| Curtains & Drapes |

| Rugs & Carpets |

| Cushions & Throws |

| Table Linen |

| Wall Textiles & Others |

| Natural Fibres |

| Synthetic Fibres |

| Blended |

| Others |

| Residential | |

| Commercial | Hospitality & Leisure |

| Corporate Offices | |

| Retail | |

| Healthcare & Educational Institutions | |

| Other Commercial Facilities |

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores |

| Specialty Flooring Stores (includes exclusive brand outlets) | |

| Furniture & Furnishing Stores | |

| Online | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Bedding | |

| Bath Linen | ||

| Curtains & Drapes | ||

| Rugs & Carpets | ||

| Cushions & Throws | ||

| Table Linen | ||

| Wall Textiles & Others | ||

| By Material | Natural Fibres | |

| Synthetic Fibres | ||

| Blended | ||

| Others | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Corporate Offices | ||

| Retail | ||

| Healthcare & Educational Institutions | ||

| Other Commercial Facilities | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores | |

| Specialty Flooring Stores (includes exclusive brand outlets) | ||

| Furniture & Furnishing Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the size and growth outlook for the textile home decor market for 2031?

The textile home decor market size is expected to increase from USD 130.23 billion in 2025 to USD 137.47 billion in 2026 and reach USD 180.07 billion by 2031 at a 5.56% CAGR.

Which product categories are leading, and which are growing fastest?

Bed linen led with 33.78% revenue share in 2025, while rugs and carpets are projected to grow at the fastest rate with a 5.74% CAGR through 2031.

How are regulations in Europe influencing supplier strategies?

European Union Digital Product Passport and Extended Producer Responsibility rules are pushing suppliers to implement traceability, adopt recyclable designs, and reformulate chemicals, which favor early movers with robust compliance infrastructure.

Which regions are most important for near-term growth?

Asia-Pacific is the fastest-growing region at a projected 6.05% CAGR to 2031, while North America accounted for 31.88% of revenue in 2025 and remains a key demand base.

What distribution models are gaining traction for home textiles?

B2C/retail remained the largest channel in 2025, while B2B direct is expanding as hotels, multifamily developers, and institutions source directly from mills to compress lead times and improve service.

Page last updated on: