Soil Conditioners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

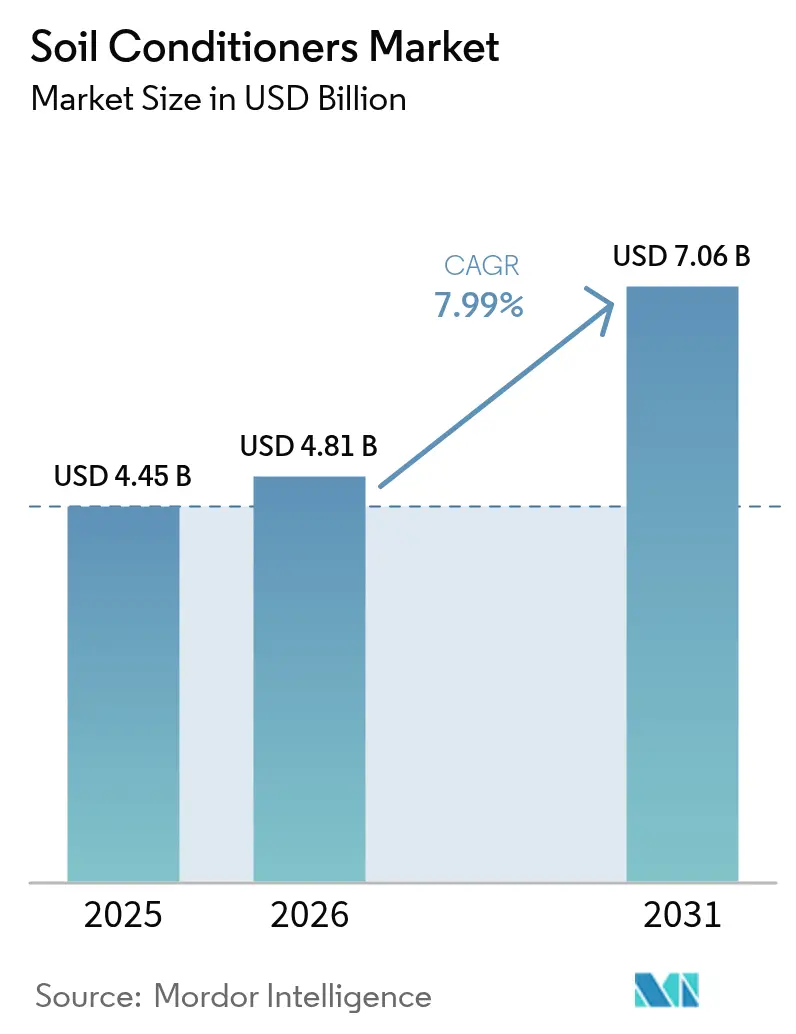

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 7.06 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

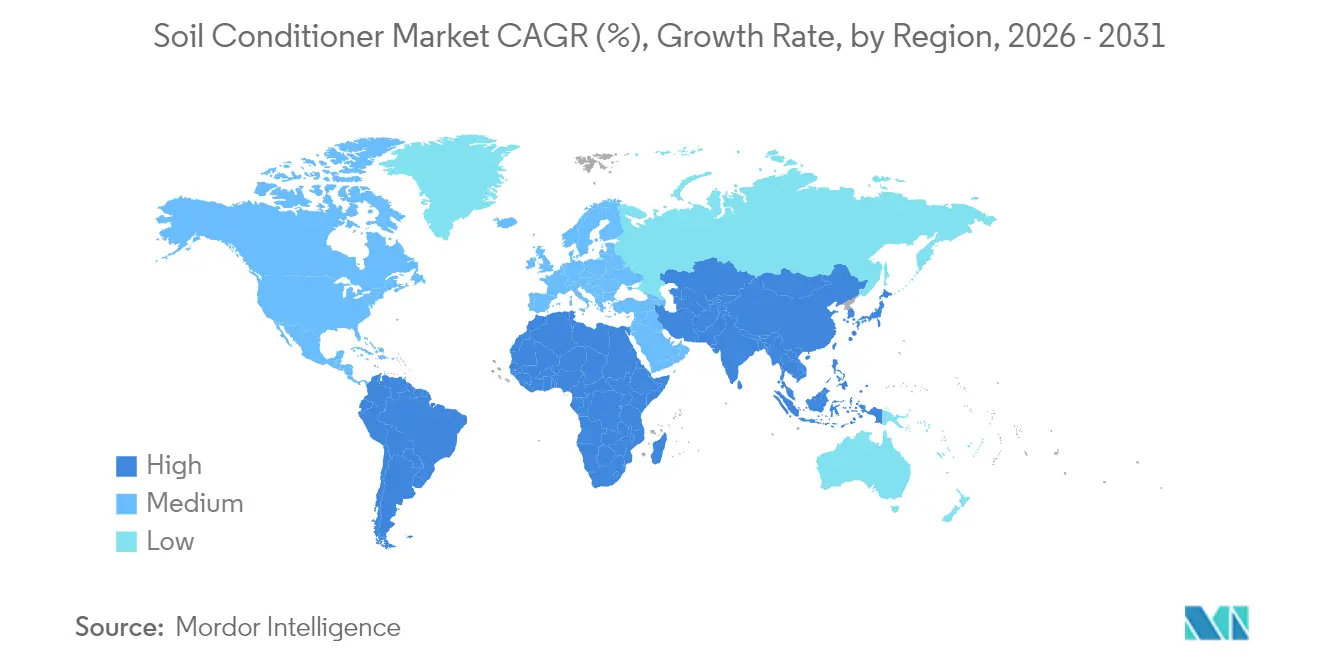

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

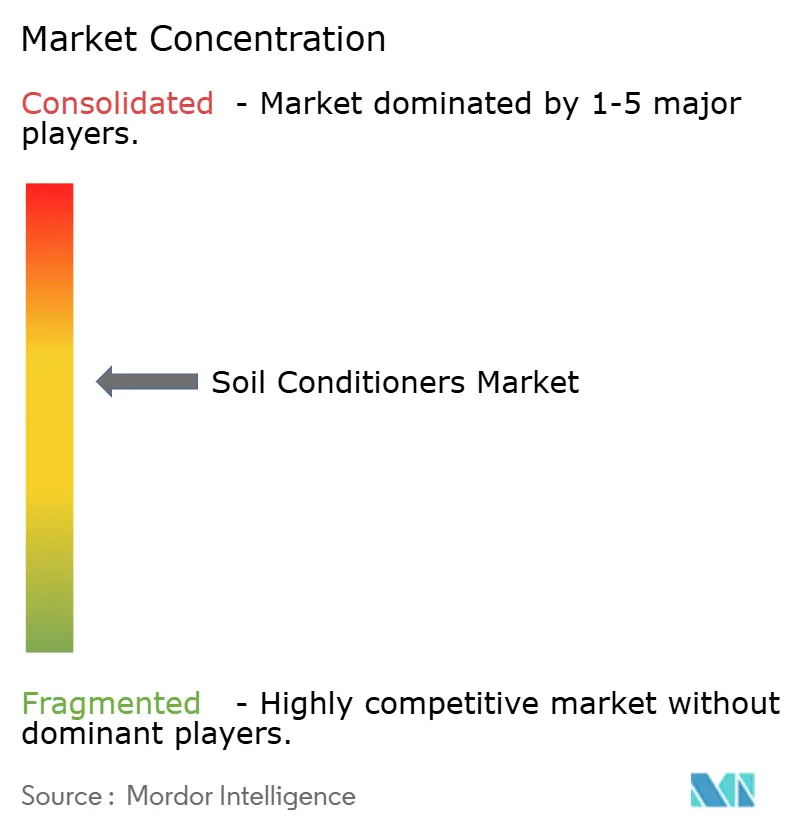

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soil Conditioners Market Analysis by Mordor Intelligence

The soil conditioners market size is expected to grow from USD 4.45 billion in 2025 to USD 4.81 billion in 2026 and is forecast to reach USD 7.06 billion by 2031 at 7.99% CAGR over 2026-2031. Organic formulations already command the majority share, and liquid products are advancing quickly as protected and vertical farming expand. Digital soil-mapping tools are sharpening application precision, while leading suppliers are bundling biological products with data-driven advisory services to differentiate in a medium-concentrated playing field. Asia-Pacific remains the largest regional contributor, but Europe, the Middle East, and Africa are registering the fastest gains on the back of stringent soil-health regulations.

Key Report Takeaways

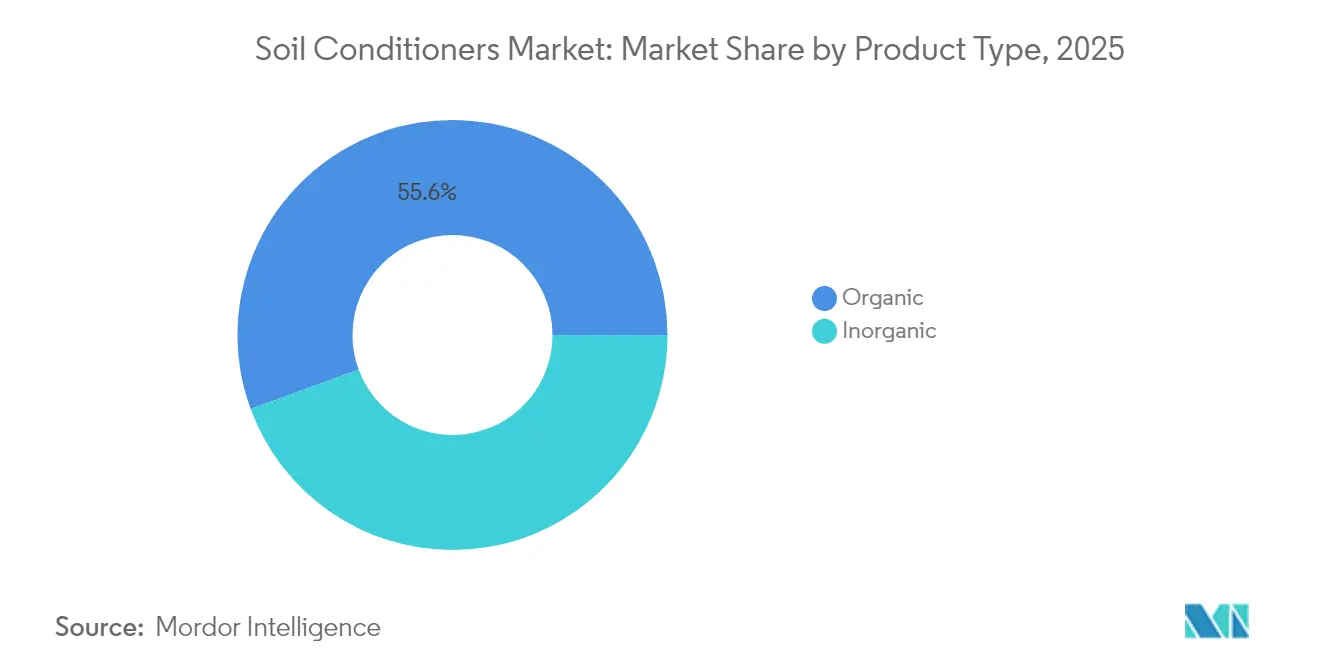

- By product type, organic inputs held a 55.60% market share of the soil conditioners market in 2025, while enzyme-enhanced variants are predicted to grow at an 8.54% CAGR through 2031.

- By crop type, cereals and grains captured 33.60% of the soil conditioners market size in 2025. Fruits and vegetables are projected to expand at a 9.21% CAGR from 2026 to 2031.

- By formulation, dry products led with a 43.20% revenue share of the soil conditioners market size in 2025, whereas liquid solutions are advancing at a 9.65% CAGR from 2026 to 2031.

- By geography, the Asia-Pacific region accounted for 37.90% market share of the soil conditioners market in 2025. South America is the fastest-growing region, with an 8.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soil Conditioners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of organic and regenerative farming | +1.2% | North America, Europe, global spread | Medium term (2-4 years) |

| Increasing soil-health degradation and erosion | +1.8% | Asia-Pacific, Africa, global | Long term (≥ 4 years) |

| Rapid growth in protected and vertical farming acreage | +0.8% | Europe, North America, urban hubs | Medium term (2-4 years) |

| Carbon-credit monetization for soil-health inputs | +1.0% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Enzyme-activated bio-conditioners boosting nutrient-use efficiency | +1.1% | Developed agricultural markets | Short term (≤ 2 years) |

| Government "4 per 1000" and similar soil-carbon initiatives are linking subsidies to conditioner adoption | +0.7% | Europe, with expanding coverage to Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Organic and Regenerative Farming

A global pivot toward regenerative practices is elevating the soil conditioners market. Retail sales of organic fruits and vegetables reached USD 60 billion in 2022, underscoring consumer willingness to pay for sustainably grown produce[1]Source: Michel Cavigelli, “The Economics of Regenerative Agriculture,” USDA Agricultural Research Service, ars.usda.gov. Agrology’s 2024 trials revealed that Merced rye cover crops boosted microbial activity and soil water retention in drought-prone orchards. As farmers seek inputs compatible with both soil health and certification standards, demand for organic conditioners accelerates.

Increasing Soil Health Degradation and Erosion

Roughly 40% of farmland is now classified as degraded, placing food security at risk, with the most severe effects in Asia-Pacific and Africa. Biochar applications have demonstrated water-retention gains of up to 154% and plant-growth increases of nearly 70% in rehabilitation trials. The soil conditioners market is therefore viewed as a strategic lever to restore productivity and mitigate the economic drag linked to land degradation.

Rapid Growth in Protected and Vertical Farming Acreage

Controlled-environment agriculture is a high-density, high-value production system that requires precise substrate management. Liquid humate solutions such as LIQHUMUS Liquid 18 have demonstrated superior nutrient uptake and root development in hydroponic tomato trials, positioning liquid conditioners as the preferred format in vertical farms. Because performance outcomes are more predictable indoors, product attributes such as enzyme activation and rapid solubility command price premiums, reinforcing the growth prospects for specialty formulations.

Carbon-Credit Monetization for Soil-Health Inputs

Carbon markets are turning soil improvement into a revenue stream. Verified biochar projects fetch between USD 171.2 (EUR 150) and USD 627.8 (EUR 550)/metric ton CO₂ on European exchanges[2]Source: Alessandro Pinzuti, “Biochar: Analysis and Economic Potential with a Focus on European Producers,” Politecnico di Torino, webthesis.biblio.polito.it. Field data from the Mid-Southern United States show that carbon-credit revenue bridges yield dips during the switch to regenerative systems. This incentive loop accelerates the adoption of conditioners that both sequester carbon and elevate soil fertility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of advanced soil conditioners | −1.1% | Developing regions worldwide | Medium term (2-4 years) |

| Fragmented on-farm advisory and awareness gaps | −0.9% | South Asia, Africa | Short term (≤ 2 years) |

| Regulatory uncertainty on emerging bio-stimulant classifications | -0.6% | Global, with particular impact in Europe and North America | Medium term (2-4 years) |

| Supply-chain risk for speciality raw materials | -0.8% | Global, with supply chains concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing of Advanced Soil Conditioners

Enzyme-activated and microbial conditioners can command higher prices, reflecting their high R&D intensity. While early adopters justify the cost through higher yields and carbon credits, smallholders in developing markets remain price-sensitive. Producers are also experimenting with tiered product lines to accommodate diverse purchasing power, tempering the negative impact on the soil conditioners market.

Fragmented On-Farm Advisory and Awareness Gaps

Optimal use of conditioners is site-specific, yet extension services in South Asia and Africa are often under-resourced. A Kenyan field study found that information deficits and dominance of inorganic fertilizer channels constrain farmers' preference for organic inputs. Partnering with ag-retail intermediaries and deploying mobile agronomy support can close these gaps, restoring growth momentum in currently under-penetrated regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic dominance, enzyme-enhanced acceleration

Organic inputs held 55.60% of the soil conditioners market share in 2025, while enzyme-enhanced variants are predicted to grow at an 8.54% CAGR through 2031, aided by burgeoning demand for residue-free produce and regulatory support for biological inputs. Organic amendments also align with carbon credit frameworks, reinforcing their uptake. Enzyme-enhanced organic variants are emerging within this space, offering faster nutrient cycling and micro-aggregate formation.

The inorganic segment, although smaller, continues to address pH imbalances and structural issues in heavy soils, with liquid gypsum gaining favour in the United Kingdom’s new Agriculture Bill compliance programs. The soil conditioners market is witnessing increased R&D in polymer-based micro-granules that combine soil structural benefits with enhanced moisture retention.

By Crop Type: Cereals retain scale, fruits and vegetables escalate

Cereals accounted for 33.60% of the soil conditioners market size in 2025, as growers seek yield stability across vast acreage. Organic amendments can raise soil organic matter by 69% and microbial biomass by 11% in cereal systems. This re-energises soils prone to monoculture fatigue and nutrient mining. Meanwhile, the high-value fruits and vegetables segment is forecast to grow at a rate of 9.21% annually to 2031, driven by quality premiums associated with taste, shelf life, and appearance.

Trials in tomato cultivation show that cow-manure conditioners yield up to 103 metric tons/ha under optimum regimes . Innovations, such as coal tailings–based pellets, increased tomato yield by 11.1%, demonstrating potential for circular-economy amendments. As controlled-environment systems scale, fruits and vegetables will further drive the growth of the soil conditioners market.

By Formulation: Dry formats lead, liquids gather momentum

Dry products accounted for 43.20% of the soil conditioners market size in 2025, supported by logistical ease and compatibility with broadcasting equipment. Granular biochar, pelletised compost, and powdery humates deliver measured nutrient release, suiting broad-acre operations. Recent enzyme-fortified granules improve microbial colonization and nutrient mineralization, widening the appeal of dry formats.

Liquid conditioners, however, are projected to rise at a 9.65% CAGR to 2031, driven by the demand for rapid assimilation from fertigation and hydroponic systems. Potassium humate liquids, exemplified by LIQHUMUS Liquid 18, have shown enhanced root elongation and stress resilience in leafy greens. Ultra-low pH acidifiers, such as Absolute Acid 1-0-0, balance alkaline irrigation water in arid zones, extending the reach of the soil conditioners market to saline-affected geographies.

Geography Analysis

Asia-Pacific accounted for 37.90% of the market share of the soil conditioners market in 2025, and South America is the fastest-growing region at 8.15% CAGR. An extensive agricultural base and acute challenges related to soil erosion drive the soil conditioners market. Government programs in China and India subsidise organic inputs, and protected cultivation is expanding in Japan and Australia. Biomass-ash conditioners increased soil pH by up to 13.6% and crop yield by 25.3% in Guizhou field tests, demonstrating notable performance gains.

Europe, the Middle East, and Africa record the fastest market growth as policy shifts embed soil health into agricultural legislation. The European Union’s organic-farming targets mandate biologically driven fertility management. Biochar adoption is surging in Germany and the Nordics, while African recycling initiatives propose that organic and bio-fertiliser streams could supply 20-40% of crop nutrient demand.

North America maintains a technologically advanced position within the soil conditioners market. Carbon-credit revenues now offset early yield dips associated with conservation agriculture, underpinning investments in soil amendments. Precision-ag platforms integrate soil-conditioner recommendations with equipment-mounted variable-rate applicators, reinforcing regional leadership.

Competitive Landscape

The soil conditioners market exhibits a medium level of concentration, with incumbent agrochemical firms and niche biological specialists competing for market share. BASF, UPL, Syngenta, and ICL steer R&D toward enzyme-activated and microbial conditioners, leveraging robust distribution networks. Monty’s Plant Food Company differentiates through proprietary humic-activation technology that enhances consistency across diverse soil types.

Merger and acquisition momentum is reshaping competitive dynamics. Huma acquired Gro-Power to expand its biological portfolio. Lesaffre purchased Altar to accelerate fermentation innovation, and ICL acquired Nitro 1000 for South American expansion, signaling a drive to embed technology and gain regional access. Companies are also forming data partnerships. Syngenta’s Interra Scan delivers soil maps that inform conditioner dosage, creating bundled service propositions appealing to progressive growers.

White-space opportunities include conditioners tailored for vertical farms and regenerative systems. Suppliers integrating digital agronomy, carbon-footprint calculators, and subscription models are likely to gain durable competitive advantage. The pursuit of multifunctional products such as UPL’s NIMAXXA, combining bionematicide and biostimulant traits further intensifies product-development races.

Soil Conditioners Industry Leaders

UPL Limited

BASF SE

Syngenta Group

Coromandel International Ltd.

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: UPL launched NIMAXXA, an innovative biostimulant bionematicide, in the Brazilian and United States markets, addressing the dual challenges of nematode control and root development enhancement.

- March 2024: AGCO reported a 60% increase in R&D investment since 2020, with a focus on precision agriculture technologies that minimize soil compaction and enhance soil health. The company's joint venture with Trimble, expected to close in 2024, aims to provide comprehensive technology offerings for the precision application of agricultural inputs.

- March 2024: The European Biogas Association published research projecting that digestate production in Europe will increase from 31 million tonnes in 2022 to 75 million metric tons by 2030, creating a significant new source of organic soil amendments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the soil conditioners market as the global demand for organic and inorganic amendments, including compost, manure, biochar, polymers, gypsum, and lime, that are applied to cultivated soils to improve structure, moisture-holding capacity, nutrient availability, and microbial activity before or during crop production.

Scope Exclusion: The analysis excludes conventional N-P-K fertilizers and standalone soil testing services.

Segmentation Overview

- By Product Type

- Organic

- Compost

- Green and Farmyard Manure

- Peat

- Other Organic Types

- Inorganic

- Polymers

- Gypsum

- Organic

- By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Oilseeds and Pulses

- Other Crops

- By Formulation

- Dry

- Liquid

- Granular

- Pellets and Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts conducted structured interviews and short surveys with agronomists, cooperative input dealers, commercial growers, and sustainability officers spanning Asia-Pacific, the Americas, Europe, and Africa. These exchanges validated usage rates, clarified emerging bio-based blends, and revealed discounting practices that are rarely captured in public documents, which helped us adjust volume and average selling price (ASP) assumptions.

Desk Research

We began with public data sets from the Food and Agriculture Organization, USDA ERS, Eurostat, and China's National Bureau of Statistics, which give acreage under key crops and soil-health indicators by region. Trade flows and average import duties were drawn from UN Comtrade and WTO tariff files, while price trends for major organic inputs were compiled from World Bank commodity dashboards. Company filings, investor presentations, and leading trade journals such as AgriPulse provided recent capacity additions and channel margins. Subscription databases that Mordor analysts routinely access, D&B Hoovers for company revenues and Dow Jones Factiva for deal pipelines, helped size the supply side. This list is illustrative; many other open and paid sources informed our desk research.

These diverse references let us benchmark adoption rates of conditioners across crop systems, flag regional regulatory incentives, and gauge historic pricing swings that influence value growth.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins the model. Top-down work starts with cultivated hectares, soil-degradation prevalence, and recommended application rates, which are then valued with region-specific ASPs. Supplier roll-ups for leading product types acted as a bottom-up check and guided tweaks where gaps appeared. Key variables include organic-farming acreage, polymer price indices, rainfall deficits, crop rotation intensity, fertilizer subsidy policies, and average application frequency. Multivariate regression, reviewed by interviewed experts, projects each driver through 2030 and feeds an ARIMA overlay that captures cyclical weather shocks. When supplier data were missing for niche geographies, we imputed volumes using adoption ratios from comparable neighboring markets.

Data Validation & Update Cycle

Before sign-off, outputs pass a three-layer review: variance scans versus historic series, cross-checks with fresh primary inputs, and a senior analyst audit. The soil conditioners dashboard refreshes every twelve months, and we issue interim revisions if policy shifts, droughts, or material mergers change the demand baseline.

Why Mordor's Soil Conditioners Baseline Earns Decision-Maker Trust

Published values often diverge because firms pick different product baskets, currency bases, and update cadences.

Key Gap Drivers: Some publishers roll in soil testing kits or exclude high-value polymer blends; others convert currencies at spot rather than annual averages or project growth on linear fertilizer trends, which inflates totals compared with Mordor's crop-specific usage logic.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.45 B (2025) | Mordor Intelligence | |

| USD 6.68 B (2025) | Global Consultancy A | Bundles soil testing reagents and lawn care additives, uses spot FX rates |

| USD 7.90 B (2025) | Industry Association B | Applies uniform 5 t/ha dosage, lacks primary ASP checks |

These comparisons show that Mordor's disciplined scope selection, blended dosage-price build, and annual refresh give stakeholders a balanced, transparent baseline they can replicate and defend.

Key Questions Answered in the Report

What is the current and forecast value of the Soil Conditioners market?

The market stands at USD 4.81 billion in 2026 and is projected to reach USD 7.06 billion by 2031 at a 7.99% CAGR.

Which product type holds the largest share?

Organic inputs represent 55.60% of market revenue owing to demand for sustainable farming practices.

Why are liquid soil conditioners growing faster than dry formats?

Liquids integrate quickly into substrates, suit fertigation and hydroponic systems, and deliver immediate nutrient availability, driving a 9.65% CAGR.

How do carbon credits influence soil-conditioner adoption?

Biochar and other amendments earn USD 171.2 (EUR 150) and USD 627.8 (EUR 550)/ metric ton CO₂ on carbon markets, offsetting costs and accelerating uptake.

Which region is expanding most rapidly?

South America lead growth, bolstered by strict soil-health regulations and rising organic-farming targets.

What technological trend is reshaping competition?

The integration of digital soil mapping with biological conditioners is enabling precision application and measurable ROI for growers.

Page last updated on: